Strategy and Program Assessment -...

102

Strategy and Program Assessment Document Stage: Final December 2005 Nepal: Public Finance Management Assessment This draft is for consultation purposes only and does not necessarily reflect the views of ADB’s Management, Board of Directors, or the Government of [country]. Comments may be submitted to [e-mail address] by [deadline].

Transcript of Strategy and Program Assessment -...

Strategy and Program Assessment

Document Stage: Final December 2005

Nepal: Public Finance Management Assessment

This draft is for consultation purposes only and does not necessarily reflect the views of ADB’s Management, Board of Directors, or the Government of [country]. Comments may be submitted to [e-mail address] by [deadline].

PREFACE As part of the preparation of the Asian Development Bank’s (ADB’s) Country Strategy

and Programming (CSP) and subsequent updates, the ADB commissions various background studies with the objective of identifying constraints to sustainable sector development and recommend measures to address these shortcomings. The findings of these studies provide critical inputs with a view to strengthening the analysis and recommendations of the CSP.

The Public Finance Management Assessment (PFMA) for Nepal was included as one of

a set of studies that would contribute to the Nepal CSP(U). The objective of the PFMA was to identify key constraints and propose recommendations across a spectrum of selected topics of public sector management. The structure of the PFMA is as follows. Chapter 1 presents a background of the socio-economic context in Nepal. Chapter 2 reviews underlying constraints in public finances with a specific focus on fiscal management. Chapter 3 reviews salient features of public resource management including the overall budget framework, revenue mobilization, the medium term expenditure framework. Chapter 4 assesses constraints across treasury and debt management. Chapter 5 reviews key issues in fiscal decentralization. Chapter 6 presents recommendations and conclusions.

The recommendations will serve to strengthening Nepal’s public resource management

policy and institutional framework with the goal of realigning public resources to policy priorities in order to better fulfill the government’s economic and social development objectives. More concretely, the PFMA will provide general guidelines for future ADB assistance in the public sector management activities.

This report was prepared by ADB staff consultant, Mr. Para Suriyaarachchi under the

overall direction of Bruno Carrasco, Principal Financial Economist and Kyung Nam Shin, Public Sector Resource Management Specialist, with assistance from Myra Teresa Mendoza, all from South Asia Department, Governance Finance and Trade Division (SAGF). The field work for the report was undertaken during November - December 2004, and the draft report was completed in the second quarter of 2005. The report has benefited from comments from the Government of Nepal and ADB staff. The views expressed in this report do not necessarily reflect those of ADB or its Board of Directors.

I would also like to acknowledge and express our appreciation for the support given by

many ADB staff members who provided substantial guidance, comments, and advice.

Kunio Senga Director General South Asia Department Asian Development Bank Manila, Philippines December 2005

ii

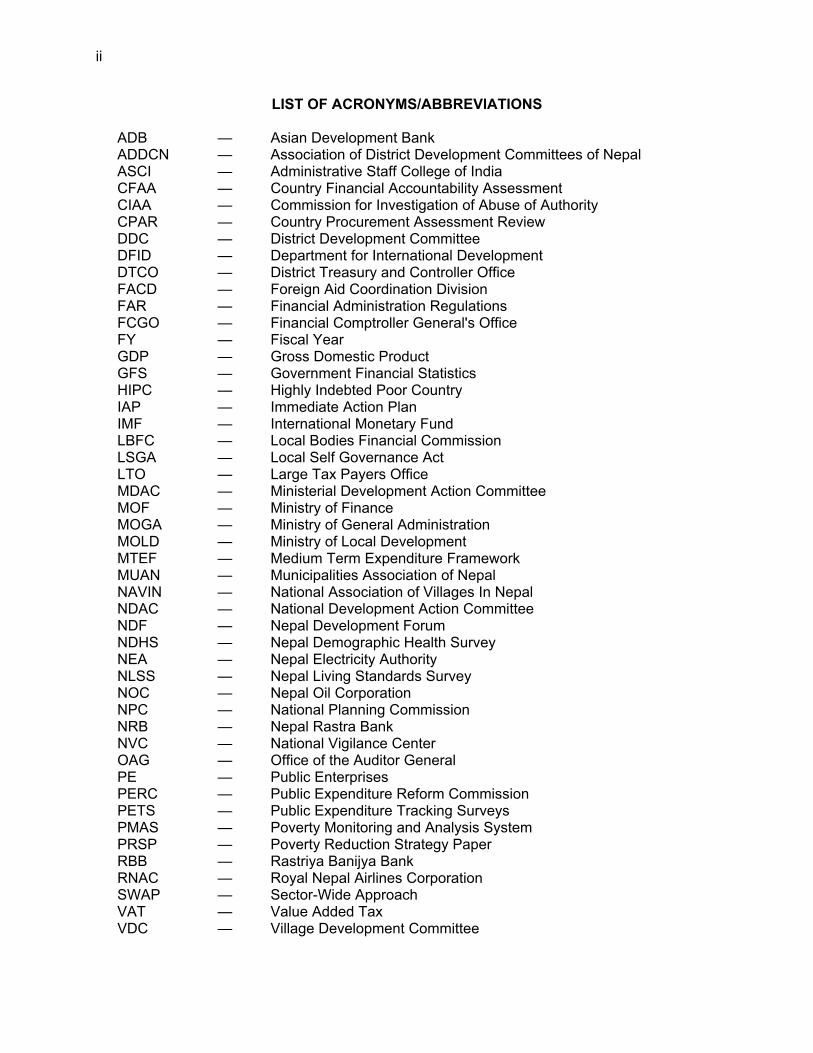

LIST OF ACRONYMS/ABBREVIATIONS

ADB — Asian Development Bank ADDCN — Association of District Development Committees of Nepal ASCI — Administrative Staff College of India CFAA — Country Financial Accountability Assessment CIAA — Commission for Investigation of Abuse of Authority CPAR — Country Procurement Assessment Review DDC — District Development Committee DFID — Department for International Development DTCO — District Treasury and Controller Office FACD — Foreign Aid Coordination Division FAR — Financial Administration Regulations FCGO — Financial Comptroller General's Office FY — Fiscal Year GDP — Gross Domestic Product GFS — Government Financial Statistics HIPC — Highly Indebted Poor Country IAP — Immediate Action Plan IMF — International Monetary Fund LBFC — Local Bodies Financial Commission LSGA — Local Self Governance Act LTO — Large Tax Payers Office MDAC — Ministerial Development Action Committee MOF — Ministry of Finance MOGA — Ministry of General Administration MOLD — Ministry of Local Development MTEF — Medium Term Expenditure Framework MUAN — Municipalities Association of Nepal NAVIN — National Association of Villages In Nepal NDAC — National Development Action Committee NDF — Nepal Development Forum NDHS — Nepal Demographic Health Survey NEA — Nepal Electricity Authority NLSS — Nepal Living Standards Survey NOC — Nepal Oil Corporation NPC — National Planning Commission NRB — Nepal Rastra Bank NVC — National Vigilance Center OAG — Office of the Auditor General PE — Public Enterprises PERC — Public Expenditure Reform Commission PETS — Public Expenditure Tracking Surveys PMAS — Poverty Monitoring and Analysis System PRSP — Poverty Reduction Strategy Paper RBB — Rastriya Banijya Bank RNAC — Royal Nepal Airlines Corporation SWAP — Sector-Wide Approach VAT — Value Added Tax VDC — Village Development Committee

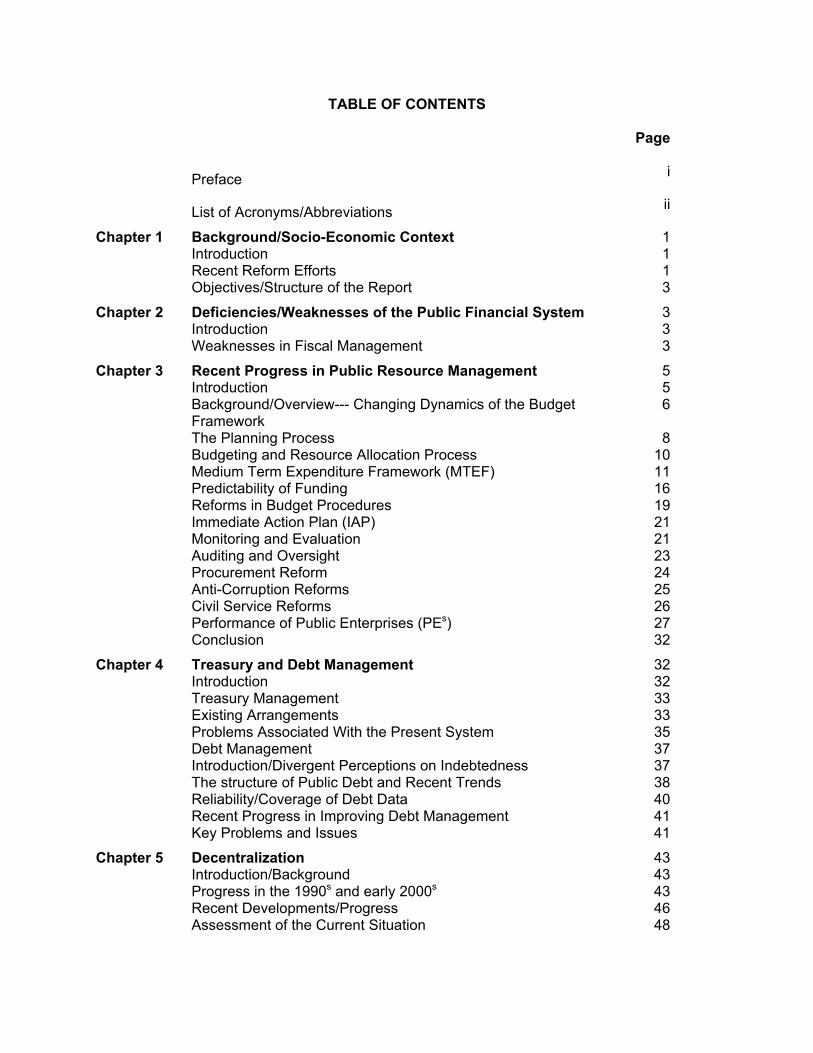

TABLE OF CONTENTS

Page

Preface i

List of Acronyms/Abbreviations ii

Chapter 1 Background/Socio-Economic Context 1 Introduction 1 Recent Reform Efforts 1 Objectives/Structure of the Report 3

Chapter 2 Deficiencies/Weaknesses of the Public Financial System 3 Introduction 3 Weaknesses in Fiscal Management 3

Chapter 3 Recent Progress in Public Resource Management 5 Introduction 5 Background/Overview--- Changing Dynamics of the Budget

Framework 6

The Planning Process 8 Budgeting and Resource Allocation Process 10 Medium Term Expenditure Framework (MTEF) 11 Predictability of Funding 16 Reforms in Budget Procedures 19 Immediate Action Plan (IAP) 21 Monitoring and Evaluation 21 Auditing and Oversight 23 Procurement Reform 24 Anti-Corruption Reforms 25 Civil Service Reforms 26 Performance of Public Enterprises (PEs) 27 Conclusion 32

Chapter 4 Treasury and Debt Management 32 Introduction 32 Treasury Management 33 Existing Arrangements 33 Problems Associated With the Present System 35 Debt Management 37 Introduction/Divergent Perceptions on Indebtedness 37 The structure of Public Debt and Recent Trends 38 Reliability/Coverage of Debt Data 40 Recent Progress in Improving Debt Management 41 Key Problems and Issues 41

Chapter 5 Decentralization 43 Introduction/Background 43 Progress in the 1990s and early 2000s 43 Recent Developments/Progress 46 Assessment of the Current Situation 48

iv

Conclusion 53

Chapter 6 Recommendations and Conclusions 53 Introduction 53 Overall Budget Framework 54 Revenue Mobilization 55 Regular/Current Expenditure 56 The Medium Term Expenditure Framework (MTEF) 57 Internalization/Ownership 58 Integration of the Regular and Development Budgets 59 Improving Cost Estimates 60 Improving the Prioritization Process 60 Monitoring and Evaluation 61 Poverty Monitoring 63 Expenditure Reporting and Oversight 64 Treasury Management 65 Public Enterprise Reform 66 Decentralization 67

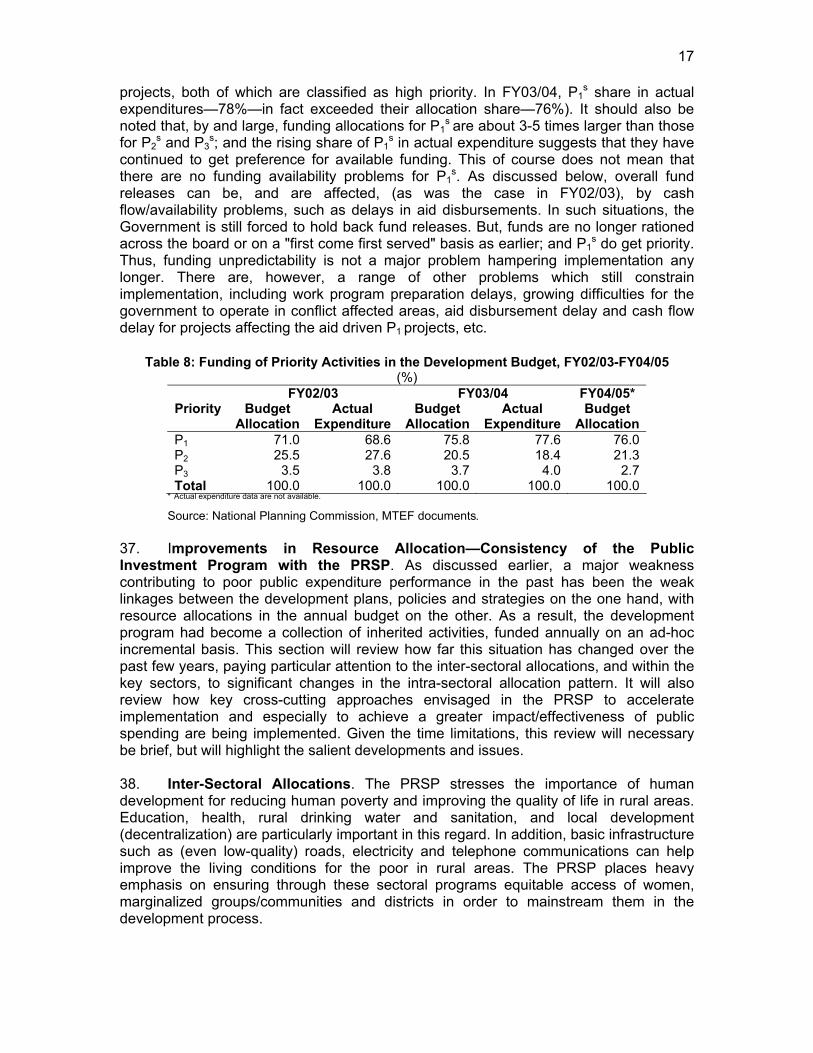

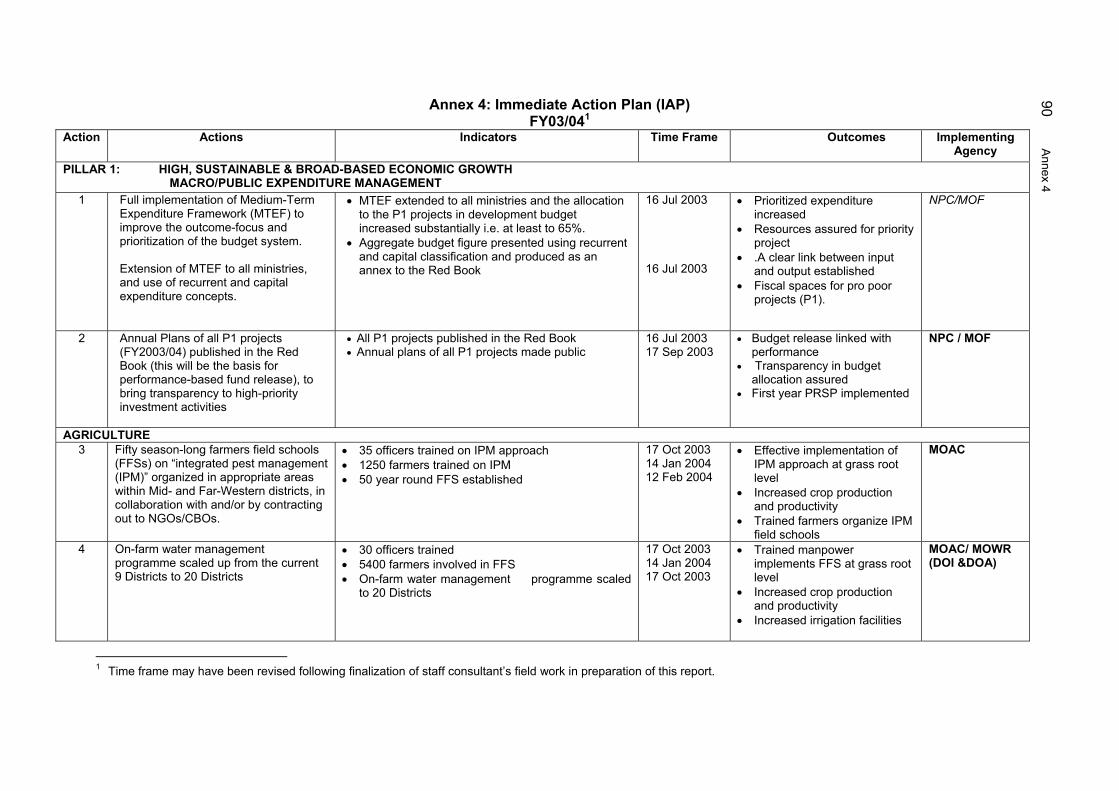

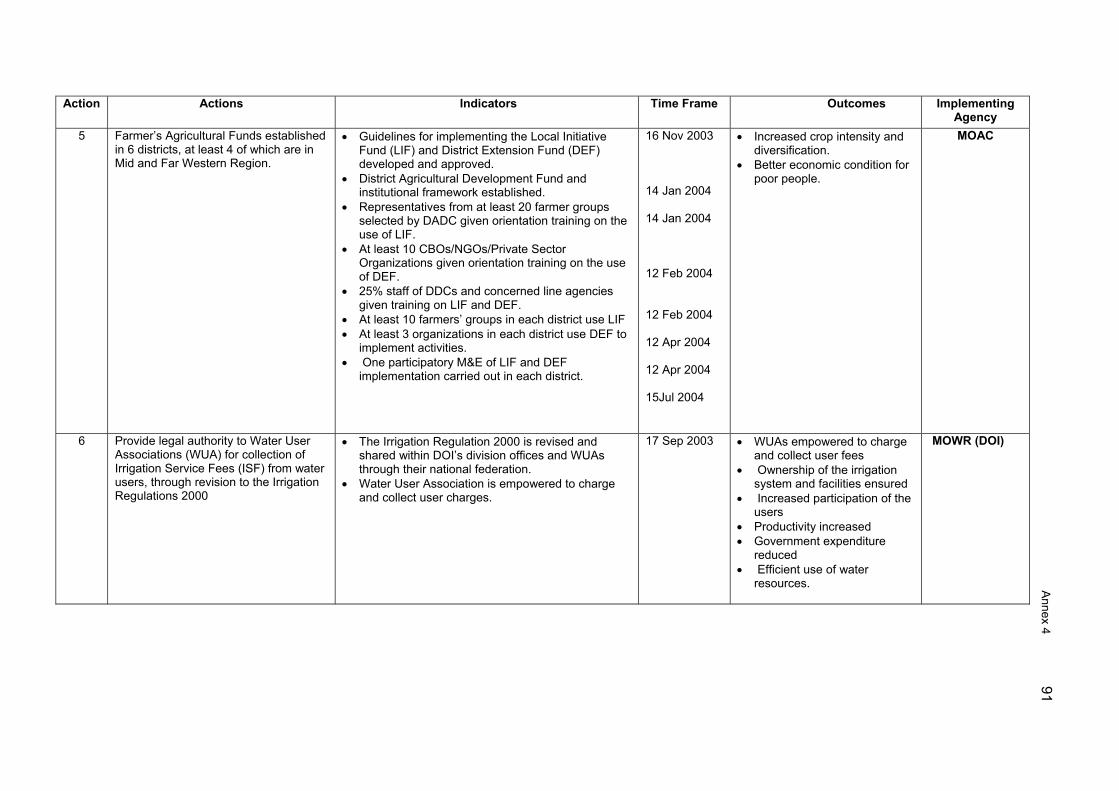

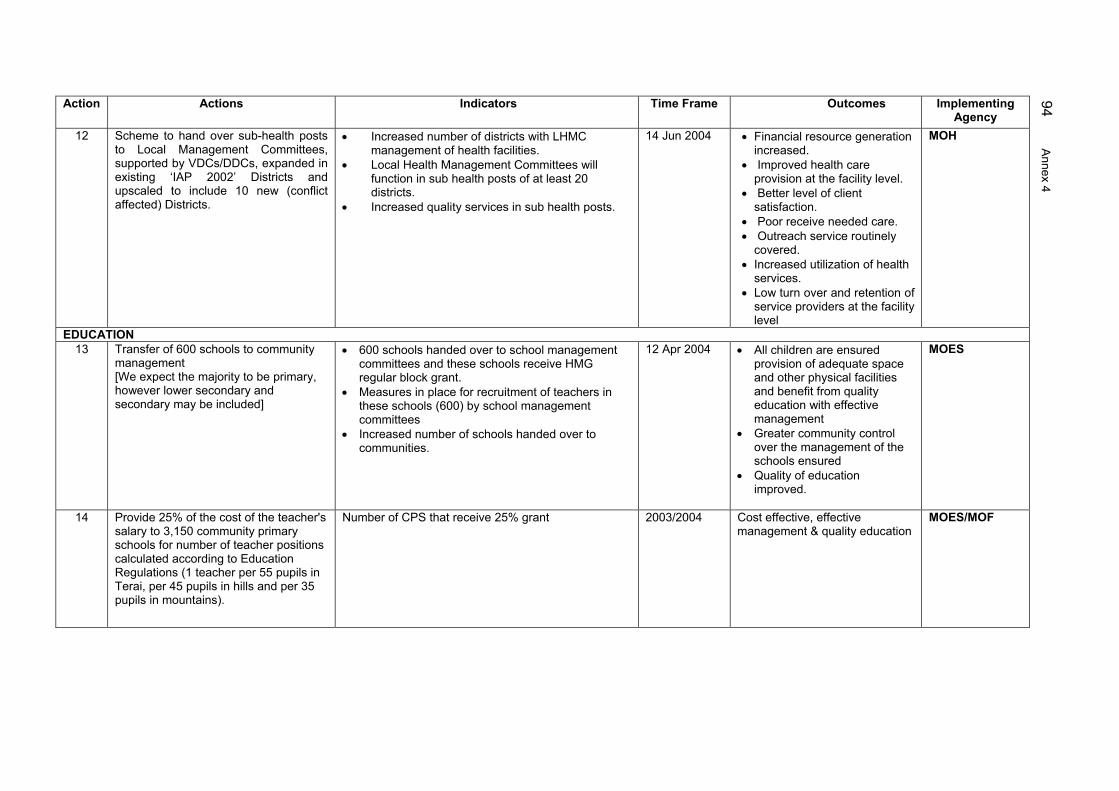

Annexes: Annex 1—Key Actions for the Future Annex 2—Intra Sector Allocations Annex 3—Immediate Action Plans of the Government (FY02/03) Annex 4—Immediate Action Plans of the Government (FY03/04)

71727583

90

CHAPTER 1: BACKGROUND/SOCIO-ECONOMIC CONTEXT

I. INTRODUCTION 1. With a per capita income of $271 per annum, Nepal is the poorest country in the South Asia Region, and one of the poorest countries in the world. Poverty incidence in the country remains high, with about 40% of the population below the poverty line at the beginning of the present decade1. Nepal has implemented several five-year development plans, supported by considerable external assistance, over the past four decades; and significant progress has been achieved from a relatively low base in many areas. Nevertheless, there has been considerable dissatisfaction both among the Nepali public and development partners that progress of overall development/poverty reduction efforts has not been fast enough, particularly against a background of growing Maoist insurgency in many districts of the country. Some2 see the "failure of development" as a prime cause of the rapid spread of the insurgency. The poor development results in turn are seen to be a consequence of continued political instability over the past decade, inadequate government commitment to pursuing appropriate economic policies and reforms, and the failure of public policies and programs to deliver the benefits of public spending to the rural poor. 2. The Nepal Development Forum meetings, held in mid 2000 and early 2002, focused heavily on these issues; and in preparation for the meetings, considerable analytical work was undertaken by development partners. A Public Expenditure Review was carried out by the World Bank in April 2000. Subsequently, the Government of Nepal itself constituted a Public Expenditure Reform Commission in September 2000, and the Commission's report was published in February 2001. Both these documents analyzed in detail the key issues and problems with regard to public resource management, and made several specific recommendations for addressing these shortcomings. Similarly, a joint Country Financial Accountability Assessment (CFAA) was carried out by the Government of Nepal and the World Bank in late 2001, and a Country Procurement Assessment Review (CPAR) was also prepared in 2001. Together, these documents provide a good baseline against which recent efforts to improve public financial management in Nepal can be measured. A. Recent Reform Efforts 3. The Government, to its credit, has taken up the challenge, particularly in the last 2-3 years. The Tenth Plan, (covering the FY02/03-FY06/07 period), which is also the Government's Poverty Reduction Strategy Paper (PRSP), was formulated in 2002; and to help implement it, a Medium Term Expenditure Framework (MTEF) was adopted for the first time in Nepal, as the basis of the Annual Budget, together with major changes in budget procedures, in July 2002. To carry out the strategy/policy initiatives envisaged in the PRSP, the government also formulated a comprehensive reform program and began to vigorously implement it, focusing particularly on key areas, (notably education, health, financial sector, and governance/anti-corruption

1 The 1996 Nepal Living Standards Survey estimated the income poverty rate at 42%. Subsequent estimates by the

National Planning Commission suggested a decline in poverty incidence to 38% by 2000; but, it has been generally believed that, since then, the escalation of the Maoist insurgency, the resulting economic slowdown and displacement of people in the conflict-affected areas may have pushed the poverty rate back up. However, the latest (2004) NLSS, (currently being processed), seems to indicate that, notwithstanding the effects of the conflict, poverty incidence has continued to decline, presumably due to increased inflow of remittances and sustained agricultural growth, both of which benefited rural areas.

2 See Country Assistance Plan for Nepal of UK's Department for International Development, 2003.

2

programs, among others). For this purpose, it also adopted the innovation of an Immediate Action Plan (IAP)—a list of critical reform actions in key areas/sectors—which it undertook to implement and closely monitor each year. A Local Bodies Fiscal Commission was constituted in 2000 in order to help implement the Local Self Governance Act (decentralization) of 1999; and some significant initial progress has been achieved. Initiatives to improve institutional arrangements to strengthen monitoring and evaluation of public spending through the adoption of a Poverty Monitoring and Analysis System (PMAS) were also begun. These efforts have been supported by a number of external donors through financial assistance (a Poverty Reduction Support Credit from the World Bank and a Poverty Reduction and Growth Facility Arrangement by the International Monetary Fund); and increased financial and technical assistance from other donors (notably by the Asian Development Bank in the form of increased project and program lending, and technical assistance for Tenth Plan preparation, for the establishment of an external and domestic debt monitoring system, and for evaluating contingent liabilities of the public sector and accelerating the privatization process—this work is currently in progress—; and by the UK Department for International Development (DFID) for MTEF preparation and facilitating budget reforms, among others. 4. Thus, after several years of slow progress, the last 2–3 years have witnessed a new wave of reforms in Nepal. It is particularly noteworthy that these reforms have been undertaken against a background of frequent government changes, a growing Maoist conflict, and a serious budget crisis, especially in FY02/03. While many countries would have cited these adverse domestic developments as excuses for inaction, the Nepalese government/bureaucracy has used the crisis as an opportunity for introducing critical reforms. The reform efforts in a number of areas have been impressive, (for example, in education, health, planning and budgeting, and the anti-corruption program). But, the benefits from these efforts are not still widely evident, because such efforts will take time to show results and also because, given the continuing conflict, effective implementation of development programs and activities remains a challenge in many parts of the country; and economic activity and investment levels are hampered directly and indirectly by conflict-related disruptions. Nevertheless, Nepal has been able to achieve a modest recovery in economic performance, as GDP grew from a negative –0.6% in FY01/02 by 3.1% and 3.7% p.a. respectively in the last two years, the balance of payments and gross reserves position strengthened, and inflation remained low (around 4% p.a.) by South Asian standards. However, as will be discussed below, much remains to be done to sustain and build on recent progress, in order to achieve the Government's development/poverty reduction goals. 5. There is little doubt that, with a small but growing private sector, the Government will continue to play an important role in socio-economic development and poverty reduction in Nepal. Annual government spending is currently around 18% of GDP; and much of development/capital spending is focused on social and economic infrastructure development, where the private sector's role, though expanding, is still relatively small. But, the growing Maoist conflict has preempted an increasing share of government revenue for security-related expenditures which, together with rising debt service payments, has created considerable fiscal stress, particularly since 2002. While the budget crisis has served as a catalyst for important budget reforms as noted above, the Government has also become increasingly dependent on external aid to an unusual extent, (nearly 70%), for financing development activities in the last two years. This dependence, unavoidable and necessary as it is for the foreseeable future, has created its own problems, such as short-term fiscal vulnerability to unexpected or performance-related slippages in aid availability. Thus, Nepal is currently facing both short-term problems of budget management, as well as more medium to longer-term challenges of strengthening its fiscal management.

3

B. Objectives/Structure of the Report 6. This study seeks to review recent efforts to improve public financial management in Nepal over the past few years, evaluate progress achieved so far, and make practical recommendations for improving fiscal management against a background of political and institutional constraints. Chapters 2 and 3 of the report focus on: (i) Deficiencies in Public Resource Management, and progress of recent public expenditure reforms, (including planning, budgeting, and institutional arrangements for monitoring and evaluation; implementing a Medium Term Expenditure Framework and how effectively it supports the PRSP goals); and (ii) Progress in implementing the key recommendations of the joint Country Financial Accountability Assessment and the Country Procurement Assessment Review in order to improve accountability and transparency of public spending. (iii) It also reviews the performance of Public Enterprises and briefly discusses related issues. Chapter 4 discusses (iv) the Treasury Management System, focusing on how the existing processes/procedures help or hinder cash management and development implementation, and how they can be improved; and (v) Debt Management capacity and related issues, focusing on recent initiatives in this area. (vi) Chapter 5 evaluates recent decentralization efforts, including transfers of both revenue and expenditure functions to sub-national levels and the key political and institutional constraints which currently hamper progress. (vii) Finally, Chapter 6 concludes with practical Recommendations for improving Public Financial Management in Nepal, both in the short term in the context of ongoing instability and conflict, and over the medium to longer term.

CHAPTER 2: DEFICIENCIES/WEAKNESSES OF THE PUBLIC FINANCIAL SYSTEM

I. INTRODUCTION 7. At the beginning of this decade, public financial management in Nepal suffered from a number of systemic/institutional weaknesses. The World Bank's Public Expenditure Review concluded that "There are no simple explanations for the apparent ineffectiveness of public spending in Nepal. A complex web of systemic factors, which cut across virtually all sectors and projects/programs have contributed to poor implementation and development results."3 That report, as well as the government's own Public Expenditure Reform Commission's Report identified and catalogued several major weaknesses, which are summarized below. A. Weaknesses in Fiscal Management 8. A major systemic weakness at the beginning of the present decade had been deficiencies in the planning, budgeting and expenditure management process. These stemmed from many sources: While Nepal had produced several five year plans as the basis of its development strategy, these plans were consistently over-ambitious; they were also unrealistic in terms of implementation/absorptive capacity and resource availability. The country did not, (and still does not), have effective project screening and appraisal systems to select projects and programs on the basis of their economic merits for inclusion in the development program. Thus, the development budget contained too many projects/programs (generally over 700 in the nineties), which could not be adequately funded. As a result, under-funding, fund rationing and poor implementation became hallmarks of the prevailing system, with very few projects/programs completed on time. 3 Nepal Public Expenditure Review, World Bank Report No. 20211-NEP. 11 April 2000.

4

9. Poor institutional arrangements for budgeting and resource allocation helped to aggravate these problems. For example, responsibilities for budget preparation were bifurcated between the Ministry of Finance, (which managed the regular budget) and the National Planning Commission (NPC) which formulated the development budget. There was very little linkage between the two budgets. There was also no systematic basis for prioritizing important development projects and programs for purposes of fund allocation. Although a core program was adopted from time to time, this practice was not consistently followed. As a result, resource allocation in the annual budget for projects, programs and sectors was often done on an ad-hoc incremental basis, based on past implementation performance, political clout and influence, and changing priorities of decision makers, rather than on development priorities. Thus, there was little linkage/connectivity between the (five year) development plans and the annual budget. While there were fund release and management procedures, these often magnified (rather than remedied) the distortions in resource allocation. For instance, since fund availability was almost always less than budgeted, fund rationing was often adopted; and funding was provided to those sectors which had utilized their previous allocations quickly. Thus the fund release system favored quick spenders, rather than development priorities, and sectors such as electricity and local development gained at the expense of agriculture, irrigation and forestry, despite their importance for poverty reduction. 10. Even where resources were allocated and provided, there were considerable intra-sectoral misallocations and inefficiencies in the use of resources. Some notable examples included: agriculture, where a large part of the development budget had been used to subsidize inefficient operations of the Agriculture Inputs Corporation; transport, where a significant proportion of resources had been channeled to unplanned construction of uneconomic (political) road projects; and health, where construction of rural health centers was not supported by adequate trained staff and basic drugs, medicines and equipment. Also, across sectors, funding for operations and maintenance activities had been inadequate. These inefficiencies have been reflected across sectors, sometimes in increased unit costs, but primarily through failure to deliver public services of acceptable quality and regularity. In addition, in a number of instances, the benefits of public spending had accrued largely to the relatively better-off segments of the community and could not be defended on equity grounds. For example, a significant proportion of increased spending on health largely benefited the relatively well-off urban population; and in education, a substantial part of the sectoral budget went into higher education which primarily benefited the upper income groups; while in power, the benefits accrued largely to urban communities; and the rural areas where the majority of the population live, were badly under-served. 11. A persisting concern from an implementation perspective was the lack of ownership of the development program at the various levels. Broadly, at the national level, the ongoing development program was seen as largely "donor driven". Most development projects/programs were included in the development budget at the behest of external donors, financed by them and sometimes directly implemented by them. Different donor procedures for expenditure reporting and disbursements and procurement often took precedence over national ones. Within the government's own program too, the planning and budgeting process and the selection of projects/programs were seen as a "top down" process, with little involvement of local communities and beneficiaries in their selection, design and implementation. As a result, there was considerable questioning of the relevance of development programs and activities; and lack of commitment to, and interest in, their effective implementation, at many levels.

5

12. The funding problems were exacerbated by the poor performance and management of the public sector, particularly public enterprises. The paternalistic role of the public sector was reflected in excessive government presence in many areas, where an emerging private sector could have played an important role. Public enterprises dominated several sectors and areas of the economy, but the performance of the vast majority of them both in terms of financial results and efficient delivery of goods and services was poor. Only a few public enterprises made an operating profit; and the large majority required annual government infusions of capital through operating subsidies, funding of virtually all new investment, and even servicing of their debt service liabilities. This was a continuing drain on the budget, which itself was often short of resources; and contributed significantly to the overall poor public expenditure management. 13. Governance issues have been a major factor undermining the effectiveness of public spending. These have taken many forms, notably (i) excessive political interference at key points in the project cycle; and (ii) increasing corruption. The most common examples have included excessive political interference in the appointments and (frequent) transfers of civil servants and project officials, political involvement even in simple procurement decisions, misuse/diversion of public funds for unauthorized purposes, and Cabinet decisions serving parochial interests. (iii) This led to increased politicization of the civil service and insecurity among public officials; (iv) Created an environment which was conducive to leakages and lack of accountability; (for example, on the revenue side, to collusion between tax officials and tax payers in regard to customs valuation, tax assessment etc; and on the expenditure side, to increased incidence of financial irregularities at various levels). (v) However, the mechanisms/legal safeguards for addressing these deficiencies were weak. For example, although the Auditor General reported numerous financial irregularities, effective steps had not been taken to check such abuses. Similarly, although the Commission for Investigation of Abuse of Authority (CIAA) had filed several cases against various individuals, its success rate in the nineties was very low. 14. While there have been several other factors of a lesser order of magnitude contributing to poor public expenditure management, the lack of coordination among government ministries, departments and agencies; duplication of offices and infrastructure at district levels; an inefficient and unmotivated civil service with ill-matched skills and staffing; and dilatory government procedures and practices, have been frequently noted. Some of these have been since addressed as part of the recent reforms, but some still remain. The Government's efforts to address these major deficiencies over the last 2-3 years are discussed in the next chapter.

CHAPTER 3: RECENT PROGRESS IN PUBLIC RESOURCE MANAGEMENT

I. INTRODUCTION 15. In the last 2–3 years, especially since the Nepal Development Forum meeting held in February 2002, the Government of Nepal has made strong efforts to improve its overall poverty reduction strategies and policies, and enhance the efficiency and effectiveness of its public expenditure program. The Reform Agenda, (which was proposed at that meeting), has been vigorously implemented. The key fiscal reforms, (aimed at addressing the systemic deficiencies identified in Chapter 2 above), include the following: the formulation of a comprehensive, well-articulated Poverty Reduction Strategy Paper (PRSP), which is fully owned by the Government; the adoption of a Medium Term Expenditure Framework (MTEF) to help implement the PRSP's key priorities; reforms in budget management to help rationalize fund release procedures to support the MTEF; introduction of innovative approaches in key sectors in order to

6

operationalize the new implementation strategies and mechanisms envisaged in the PRSP to help improve service delivery in rural areas; and the adoption of an innovative Immediate Action Plan to better monitor the implementation of key reforms. These measures, necessary as they are for addressing prevailing deficiencies in fiscal management, were also inspired by a fiscal crisis which emerged suddenly in 2002. A quick review of the changing dynamics of Nepal's fiscal situation will help to understand the motivation for the recent reforms which are discussed subsequently. A. Background/Overview—Changing Dynamics of the Budget Framework 16. Nepal's main fiscal parameters in the mid nineties and significant changes in the first half of this decade are summarized in Table 1. As to be expected of countries with similar levels of per capita incomes, Nepal's revenue/GDP ratio has been quite low—only around 11% in the mid nineties. Total government expenditures averaged around 18%, and the primary budget deficit (before grants) was around 7% of GDP in FY94/95. Since regular expenditures4 were contained within 9% of GDP, Nepal was able to maintain development spending around 9–10% of GDP. This level of development spending was financed almost equally from domestic and foreign resources. Gross foreign aid inflows were equivalent to about 56% of development spending over the FY94/95–FY99/00 period; but, the contribution of domestic resources (from a revenue surplus of about 2–2.5% of GDP per annum and modest domestic borrowing of around 1.8% of GDP per annum) was still substantial.

Table 1: Changing Dynamics of the Budget Framework, FY94/95-FY04/05 (Rs billion)

Item FY94/95

FY95/96-FY99/00 Average FY00/01 FY01/02 FY02/03 FY03/04 FY04/05

Revenue 24.58 34.27 48.89 50.45 56.23 62.23 70.32Total Expenditure 39.07 55.85 79.84 80.07 84.01 92.11 111.69 Regular 19.27 27.70 42.77 48.59 54.97 59.30 64.49 Development 19.80 28.15 37.07 31.48 29.03 32.81 47.20

Primary Deficit -14.49 -21.58 -30.94 -29.63 -27.78 -29.88 -41.37Financing Dev. Exp. 19.80 28.15 37.07 31.48 29.03 32.81 47.20

Revenue Surplusb 5.31 6.57 6.13 1.86 1.26 2.93 5.83

Domestic Borrowingc 3.24 5.68 12.14 16.24 11.89 7.31 9.06

Foreign Assistanced 11.25 15.90 18.80 13.39 15.89 22.57 32.31As Percentage of GDP (%) Revenue 11.21 11.04 11.90 11.95 12.36 12.57 13.16

4 One of the important recent changes relates to changes in the budget classification itself. Beginning with the

FY04/05 Budget (announced in July 2004), Nepal officially changed its presentation of budget accounts/fiscal data from a "Regular Budget/Development Budget" to a "Recurrent/Capital" classification. However, historical data has not been reclassified so far on the new format. Accordingly, the review and analysis of reforms undertaken in the past few years and their impact can be carried out only on the basis of the "Regular/Development" classification, which is the basis of this report. It is also important to note that the presentation of fiscal data by the Government in its Budget documents and related expenditure/revenue reports are on a gross basis, and are somewhat different from the International Monetary Fund's presentation of fiscal data, which are on a net or consolidated basis (i.e. nets out inter-governmental transactions and debt repayments). In order to make the report more easily understood by its principal users (which includes the Government and local stakeholders in Nepal), the government's database is used for this analysis, rather than the GFS classification.

7

Item FY94/95

FY95/96-FY99/00 Average FY00/01 FY01/02 FY02/03 FY03/04 FY04/05

Total Expenditure 17.82 17.99 19.43 18.96 18.47 18.61 20.90 Regular 8.79 8.92 10.41 11.51 12.08 11.98 12.07 Development 9.03 9.07 9.02 7.45 6.38 6.63 8.83

Primary Deficita -6.61 -6.95 -7.53 -7.02 -6.11 -6.04 -7.74Financing Dev. Exp. 9.03 9.07 9.02 7.45 6.38 6.63 8.83

Revenue Surplusb 2.42 2.12 1.49 0.44 0.28 0.59 1.09

Domestic Borrowingc 1.48 1.83 2.96 3.85 2.61 1.48 1.70

Foreign Assistanced 5.13 5.12 4.58 3.17 3.49 4.56 6.05Memo Item: Aid as % of Dev. Exp. 56.50 56.48 50.70 42.50 54.70 68.80 68.50 GDP(At Producers' prices) 219.18 310.36 410.79 422.30 454.94 494.88 534.47a Before Grants. b Revenue minus regular expenditure. c From bank and non-bank sources and "use of cash balances". d Grants and loans.

17. By the end of the nineties, however, signs of fiscal weakening had begun to emerge—sluggish revenue growth, rising regular expenditures particularly on security and debt servicing, falling aide levels (in relation to GDP) reflecting weak budget implementation and 'aid fatigue'. As aid levels declined by about 1% of GDP to around 4.5% of GDP, domestic borrowing had to be increased to maintain development spending around 9% of GDP. 3.4. The fiscal situation deteriorated further into a full-blown crisis in FY02/03, as the effects of the escalation of the insurgency, global recession and a weakening economy took their toll. Although efforts to increase tax collections helped to improve the revenue/GDP ratio, regular expenditures increased much faster by 2% of GDP (see Table 1). Thus, the revenue surplus virtually disappeared, while foreign assistance also fell further by another 1 ½% of GDP (to around 3% of GDP). To offset these declines, the government resorted to additional domestic borrowing, which rose to nearly 4% of GDP by the end of FY01/02. Nevertheless, development spending fell to 7 ½% of GDP in FY01/02, its lowest level for many years.

Table 2: Functional Classification of Regular Expenditure (%)

Item FY94/95 FY99/00 FY00/01 FY01/02 FY02/03 FY03/04 Social Services 23.1 24.1 25.4 27.5 25.0 23.7 Economic Services 4.3 4.0 3.3 3.3 3.2 4.0 Infrastructure 2.7 2.4 0.5 0.6 0.5 2.0 General Administration 7.2 6.4 6.0 7.2 6.2 4.5 Defense & Security 18.6 19.6 21.0 24.5 24.7 22.2 Debt Servicing 31.6 29.1 24.3 25.1 29.4 27.3 Miscellaneous 12.5 14.3 19.4 11.8 10.8 14.6a Total 100.0 100.0 100.0 100.0 100.0 100.0

a Includes contingencies, a part of which was later utilized for security expenditures.

Note: From FY04/05 onwards, budget details on the basis of regular/development expenditures are no longer provided. Source: Ministry of Finance.

18. Since then, there has been a turn-around of sorts in the last 2 years, mainly due to government efforts which are discussed in the rest of the report. The growth of regular

8

expenditure moderated somewhat, but it still preempted about half of the increase in revenues; and domestic borrowing has been cut back (by nearly 2.5% of the GDP) to 1.5% in FY03/04. The budget reforms (discussed below) have helped to trigger increased external assistance (including budget support), and raise the foreign aid/GDP ratio again by about 1% of GDP by FY03/04. But this came too late to help increase development spending in FY02/03; and in FY03/04, despite improved funding availability, the spread of the conflict has held back development spending to around 6 ½% of GDP. For FY04/05, the Government has announced an ambitious budget which aims at increasing development spending to around 8.8% of GDP, with the help of substantially increased external assistance (by another 1 ½% of GDP to about 6% of GDP). But, as discussed below, this target is unlikely to be realized (para. 116). 19. Some important observations can be made from the above analysis. Clearly, the dynamics of the budget have changed in recent years, with important implications for future policies: (i) The Government's revenue surplus, which was an important source of domestic financing of development activity in the past, has become almost negligible. (ii) Domestic borrowing (from banking and non-banking sources) has been reduced. According to the current policy stance agreed with the IMF, such borrowing will continue to be reduced over the next few years, as part of the PRGF framework. Thus, the domestic contribution to financing development activity has fallen to quite low levels by historical standards. It is therefore important to make strong efforts to increase the revenue ratio and to curtail the growth of regular expenditures, especially on defense and internal security; but this will require an abatement of the conflict, which may take time. (iii) Thus, to finance even a minimum level of development spending for achieving reasonable progress towards PRSP goals, Nepal will need to depend heavily on external financing. It is thus highly unlikely that the present degree of external dependence, (close to 70% of development spending was externally financed in FY03/04 and is projected to be financed in FY04/05 also), can be reduced any time soon. But, to trigger such assistance, Nepal will need to continue to pursue fiscal and other reforms agreed with external donors; and delays in meeting performance criteria themselves can create new sources of fiscal pressures. This indeed could happen this year; and if so, may lead to another cash management crisis (paras. 114–116). 20. The fiscal reforms that were initiated in 2002 (as part of the FY02/03 Budget) represent an important start in this context. It could be argued that, given the fiscal crisis in FY02/03, there was little alternative for the Government but to undertake such reforms. Nevertheless, it is to the credit of the Government that it turned the crisis into an opportunity to carry out much needed reforms against a background of continued conflict and political instability; and that it has stayed the course so far. The remainder of this chapter discusses these recent reform efforts in greater detail. It also reviews the impact of these measures so far, particularly how they have (or have not) helped to address the systemic problems in public financial management earlier.

B. The Planning Process 21. As discussed in Chapter 2, a major factor which contributed to ineffective public resource management in the past has been weaknesses in the planning and budgeting system—over-ambitious development plans, with unrealistic goals and targets, lack of clear priorities and strategic focus, disregard of implementation capacity and resource constraints, and little involvement of local governments, beneficiaries, civil society or development partners, among others. As a result there was little connection between planning, policy making and budgeting (resource allocation) processes. There was also little emphasis on the implementation aspects of the plans, and on monitoring and evaluation to ensure effective

9

delivery of results/outputs. Reforms introduced in the last 2-3 years have begun to address these problems, and significant progress has already been achieved (see below). 22. The Government's Tenth Plan, which is also its Poverty Reduction Strategy Paper (PRSP)5, was finalized in FY02/03, and represents a significant departure from past practices. To quote the Tenth Plan/PRSP—"the Tenth Plan represents a major effort to address these shortcomings. Its distinguishing features include the following: (i) Its has adopted a participatory and relatively more 'bottom up' approach; (ii) It is the product of an extended nation-wide consultation process over two years; and the feedback from the such consultations has been interactively utilized for finalizing the Plan's objectives, targets, policies and programs; (iii) It focuses strategically on the overall poverty reduction strategy and seeks to prioritize sectoral programs and activities accordingly; (iv) It emphasizes results and effective implementation and monitoring mechanisms; (v) It incorporates a credible macroeconomic framework by utilizing alternative scenarios; (vi) The latter is supplemented by a rolling Medium Term Expenditure Framework (MTEF), which will be updated every year, and provides for the first time in Nepal, an effective mechanism to link the annual budget with the Five Year Plan and to make periodic adjustments in programs as needed; and (vii) Finally, as the product of a highly participatory process, it can claim a far higher degree of national ownership and acceptance than earlier plans"6. 23. The Tenth Plan/PRSP's declared objective is to "achieve a remarkable and sustainable reduction in the poverty level from 38% at the beginning of the Plan period to 30% by the end of the Tenth Plan, and to further reduce the poverty ratio to 10% in about fifteen year's time". Since nearly 90% of Nepal's poor live in rural areas, the Plan's poverty reduction strategy is strongly rural-oriented. To reduce (rural) poverty, the Plan/PRSP has adopted a four-pillar strategy: (i) Accelerating income and employment generation through a broad-based pro-poor growth strategy focusing particularly on rural/agriculture growth; (ii) Accelerating social and human development, and provision of rural infrastructure (rural roads, electricity etc), to bring benefits of development/public spending particularly to rural communities; (iii) Targeted programs, as well as programs emphasizing social inclusion, in order to bring the poor, marginalized groups/communities, women and backward regions into the mainstream of development; and (iv) Good governance, to improve efficiency, accountability and delivery of public services and to reduce corruption and misuse of resources. To implement the four-pillar strategy, the Plan also stresses several cross-cutting strategies: (v) Redefining the role of the State and limiting public interventions, particularly in view of resource and implementation constraints; (vi) Promoting community participation and involvement in the choice, design and management of activities at the local levels (in order to improve efficiency and quality of service delivery; (vii) Accelerating the decentralization process (both to improve implementation and promote greater 5 The Tenth Plan/PRSP was prepared under the guidance of a Steering Committee, headed by the Vice-Chairman

of the National Planning Commission (NPC), consisting of Secretaries of line ministries to provide strategic leadership, while Technical Committees headed by the respective Secretaries of the line ministries coordinated the formulation of strategies and programs in each sector, ensuring strong inter-agency participation and ownership. All of the inputs and papers (such as the Interim PRSP, MTEF, sector policy and strategy papers, as well as various drafts of the Plan/PRSP itself), were discussed through public consultations held in different parts of the country, involving a wide range of stakeholders—including representatives from District Development Committees, from deprived communities and backward regions, academia from campuses and schools, NGOs, CBOs, women, political parties, private sector and external development partners. Several regional consultations, including two exclusively for women's groups, were held. No other government publication/policy document has ever been subjected to so much discussion/ dissemination as the Tenth Plan/PRSP.

6 The Tenth Plan/PRSP, pp.5–6.

10

accountability); and (viii) Enlisting the private sector to play a lead role in employment and income generation, and together with NGOs, INGOs, CBOs/SOs, to complement government efforts in service delivery and implementation of activities in key sectors and areas. To help carry out this agenda, the Tenth Plan/PRSP has envisaged a major re-orientation of public expenditure policies and programs; and the MTEF and the Immediate Action Plan (IAP) are two major instruments that have been utilized to this end. 24. The Tenth Plan/PRSP helps to address some of the major concerns with the planning and budgeting system which have been frequently highlighted by development partners in the past: (i) As noted above, it provides a coherent and focused approach, with clearly defined strategies and policies for poverty reduction; (ii) It is fully owned by the government and supported by domestic stakeholders; (iii) Accordingly, it provides a nationally owned framework within which development partners can harmonize their own assistance strategies for poverty reduction in Nepal; and (iv) It has helped to fill a long-standing vacuum in the development management process, with the Government now well-positioned to take over the lead role in deciding project/program priorities and adapting external assistance to fit its own needs. Thus, Nepal can justifiably claim that it is now in charge of its development/poverty reduction strategy, instead of "donor-driven" projects/programs dictating the nature and thrust of the Government's development/poverty reduction effort. A number of major donors have already accepted the PRSP framework and adapted their own assistance strategies to fit within that framework7; but it still remains to be seen whether the Government will manage to get itself into the "driver's seat" in the management of the development process. C. Budgeting and Resource Allocation Process 25. While the formulation of a coherent and focused Poverty Reduction Strategy was a major step forward, the adoption of the key elements of a Medium Term Expenditure Framework (MTEF) provided the missing link between the Plan/PRSP and the annual Budget and its resource allocation process; and made it possible to ensure the implementation of the Plan/PRSP's key priorities. 26. The Government initiated preparatory work for adopting the MTEF approach in November 2001 in parallel with the preparation of the Plan/PRSP; and initial proposals for five important line ministries8 were presented to the Nepal Development Forum (NDF) meeting in February 2002, as a part of the Government's reform agenda. Subsequently, even as the Plan was being finalized, it became evident that a major budget crisis would derail the implementation of the Plan/PRSP (para. 18). The initial resource projections for the FY02/03 Budget, which was to be announced in July 2002, clearly showed that a domestic recession, a stagnation of government revenues and a sharp increase in security-related expenditures, (all of which were directly related to the escalation of the Maoist insurgency), would severely limit the availability of resources for financing the development budget; and that the latter would have to be cut down far below the level of Rs50.5 billion budgeted in FY01/02 (Table 1). Accordingly, MTEF preparation was extended to cover all ministries and sectors; and the MTEF was adopted as the basis for resource allocation in the FY02/03 Budget.

7 Notably, the World Bank, Asian Development Bank and UK, among others. 8 Initially, MTEF preparation focused on five ministries: Education, Health, Agriculture, Irrigation and Physical

Planning and Housing (which also included Drinking Water).

11

D. Medium Term Expenditure Framework (MTEF) 27. It is worth noting that Nepal has opted for a pragmatic phased adoption of the MTEF approach. Unlike many countries which have experimented with operationalizing comprehensive MTEFs, (often with mixed results9), Nepal chose to implement the key elements of an MTEF, adapting it to its own immediate needs and institutional capacity. Thus, initially only the development budget was brought within the MTEF discipline, although the Budget framework took fully into consideration resource availabilities for meeting all (development as well as regular) expenditures. Second, the initial expenditure estimates by the line ministries were prepared on the basis of existing cost parameters, without spending considerable time and resources at the beginning on refining and improving cost coefficients. Third, efforts were made in the beginning to internalize the MTEF preparation process. For example, the preparation of the first MTEF was built into the normal annual budget preparation cycle, with the annual budget call being the basis for the sectoral allocations under the MTEF. Moreover, in order to link the MTEF directly with the Plan/PRSP, the same line ministry teams, (under the direction of their respective line Secretaries), which were involved in the Plan/PRSP preparation and are also normally responsible for the preparation of the annual sectoral budgets/programs, were utilized for MTEF preparation, with assistance from local consultants for providing technical guidance and support. However, as discussed below, this approach was subsequently changed during MTEF 3 preparation; and to ensure effective internalization, the preparation process needs to be better integrated into the budget cycle. 28. The MTEF process essentially involved, among others, the adoption of a realistic and credible budget framework, the prioritization of all programs and activities in the development budget, streamlining/cleaning up the public investment program, and changing budget and fund release procedures to ensure greater predictability in funding for priority activities. These changes are discussed below in some detail. As noted, they have helped to bring about significant improvements in fiscal management in a difficult environment. 29. The first MTEF covering the three-year period FY02/03-FY04/05 was introduced in July 2002 and was the basis of the Development Budget for FY02/03: (i) It introduced a hard budget constraint for the first time in several years, with the size of the development budget set at Rs38.7 billion, well below the preceding year's level of Rs. 50.5 billion; (ii) This in turn necessitated a sharp reduction in the number of projects/programs in the development budget; (iii) In addition, all activities in the development budget were prioritized and ranked into three categories, (on the basis of explicit criteria developed by NPC), in terms of their contribution to poverty reduction (with P1 as the highest and P3 the lowest priority); (iv) All P1 activities were assured funding during the fiscal year to the extent of their budget allocations, while P2 and P3 activities were to be funded only if sufficient funds were available. (iv) To encourage better implementation and also to facilitate cash management, a performance-based fund release system was also introduced. While all P1 projects automatically received their first trimester's allocations, subsequent releases were made contingent on certification by

9 Several developing countries have adopted the MTEF approach in the last decade. In many cases, the degree of

complexity and comprehensiveness was beyond the institutional capacity of the countries; and successful internalization to ensure sustainability became a critical issue.

12

For prioritizing the development budget, detailed guidelines, together with a scoring table, have been provided to line ministries and agencies. The main prioritization criteria include: contribution to national/poverty alleviation goals, contribution to sectoral goals/objectives, contribution to regional development (with districts having lower Human Development Index scores receiving higher priority than others), rationale for government involvement, degree of participation (by civil society/community groups, local governments, private sector etc,), project status (age of project, implementation performance), and certainty of funding (whether funding is assured/committed or not). Marks are assigned for each criteria on a scale of 0-3, with a total score of 21. Each agency is expected to rank each activity/budget line, using a total score of 21, with no discretion to drop any of the criteria. While there was considerable subjectivity in scoring and ranking of activities by agencies early on, the detailed scorecard system allows NPC and MOF to review the agency rankings and agree whether the prioritization is reasonable or not.

line ministries/departments that work programs have been satisfactorily completed. A second rolling 3-year MTEF was prepared a year later for the FY03/04-FY05/06 period. It made the prioritization process more stringent and transparent (by improving the prioritization criteria and introducing a uniform scoring system), and aligned the budget allocations more closely with the PRSP. It also strengthened the analytical rigor of sectoral MTEFs. The third rolling MTEF covering the FY04/05-FY06/07 period was announced in July 2004, and has tried to improve the cost estimation process in a few key sectors. However, it should be noted that, although each of the subsequent MTEFs built on, and generally refined and improved on the preceding MTEFs, overall progress has not been consistently smooth or steady. As discussed in Chapter 6 below, there have been some slippages/backtracking at times, for example, as in the case of MTEF 3 where its budget framework has not been sufficiently realistic and its preparation has not been effectively coordinated with the annual budget cycle. 30. How have these innovations helped to address the prevailing deficiencies in the budgeting system? A number of significant improvements can be pointed out: (i) The annual budget framework has been made more realistic; (ii) The number of projects/programs in the development budget has been significantly reduced; and (iii) Funding for priority activities has substantially increased; (iv) There is also greater predictability of funding for the priority activities; (v) Even more important, activities within the development budget have been more closely aligned with the Plan/PRSP; and the resource allocation pattern among sectors (inter-sector) and within sectors (intra-sector) has improved (see below). 31. Realism of the Budget Framework. Until the last 2 years, government revenue and particularly foreign aid projections in the annual budget were heavily overestimated, allowing the inclusion of hundreds of marginal projects (Table 3). Inevitably, budget outcomes fell far below these unrealistic expectations, especially for foreign aid disbursements and development spending, while domestic borrowing far exceeded the budget targets. The MTEF helped to mitigate these problems in the last two years. In FY02/03, budget targets for revenue, foreign aid and development spending were set at more modest levels. The revenue target was almost achieved. But, aid disbursements still fell significantly short of expectations, largely because anticipated budget support from donors (equivalent to over half the shortfall) did not come through in time. This in turn adversely affected development spending, since the government withheld fund releases to projects/programs, anticipating the funding shortfall. In FY03/04, the outcome has been slightly better. The revenue target has been fully achieved, while shortfalls in aid disbursements and development spending have been smaller. In regard to development expenditure outcome, two facts should be noted: (a) The conflict has made it difficult for the government as well donors to implement programs in some areas; and (b) The development

13

expenditure target included two large projects—Melamchi drinking water and Marsyangdi hydro power—which have been held back by design/implementation problems. When these two projects are excluded, the development expenditure outcome has been better (see Memo Item in Table 3). In the last two years, the Government has also been able to hold domestic borrowing below the budgeted level, and in fact significantly reduce it in FY03/04. However in the FY04/05 Budget, the projected levels of development spending and aid inflows have been set at too high levels, eroding the "hard budget constraint"; and it is very doubtful whether these targets can be achieved, (see below). 32. Another indicator of the degree of realism of the MTEF projections is their consistency/compatibility with the PRSP's budget framework. The PRSP's macroeconomic projections (which had been discussed extensively and agreed with the International Monetary Fund) assume two main scenarios: one for supporting a high growth path (averaging 6.2% per annum) and another consistent with lower growth (averaging 4.3 per annum) and political and resource constraints. The PRSP's key budget parameters for both scenarios, in current prices, (government revenue, regular and development expenditure, and domestic borrowing), are compared with the MTEF budget targets for the FY02/03 to FY04/05 period and actuals for the same variables in Table 4 below. As evident from Table 4, the MTEF's budget projections are closely in line with low case (constrained growth) scenario of the PRSP. Its revenue and domestic borrowing targets, and actual outcomes for the past two years, are better than assumed in the PRSP, while regular expenditures are almost identical with those of the PRSP low case. In the case of development expenditures, MTEF targets assume a 15% implementation shortfall for each year, partly reflecting normal delays and partly the uncertainties with the implementation of two large projects (Melamchi drinking water and Marsyangdi hydro power) noted above. When adjusted for these expected implementation shortfalls, the MTEF's development expenditure target (and actual achievement) is quite close to the PRSP's low case for the past 2 years. However, the current year's (FY04/05) adjusted target, though in line with PRSP, is optimistic for the reasons discussed in para. 116 below.

14

Table 3: Budget Targets Vs. Actuals, FY00/01- FY03/04

(In billion Rs) FY00/01 FY01/02 FY02/03 FY03/04 FY04/05

Item

Budget Actual Change%a

Budget Actual Change%a

Budget Actual Change%a

Budget Actual Change%a

Budget Change%b

Total Expenditure 91.6 79.8 -12.9 99.8 80.1 -19.8 96.1 84.0 -12.6 102.4 92.1 -10.6 111.7 21.3Regular 43.5 42.8 -1.7 49.3 48.6 -1.5 57.4 55.0 -4.2 60.5 59.3 -2.0 64.5 8.8Development 48.1 37.1 -23.0 50.5 31.5 -37.6 38.7 29.0 -25.1 41.8 32.8 -21.5 47.2 43.9

FINANCING Revenue 53.0 48.9 -7.7 60.3 50.4 -16.3 57.2 56.2 -1.7 62.2 62.2 0.0 70.3 13.0Foreign Aid 31.6 18.8 -40.0 30.5 14.4 -53.0 27.0 15.9c -41.1c 28.3 22.6 -20.1 32.3 42.9Domestic Borrowing 7.0 12.1 72.3 9.0 15.3 69.3 12.0 11.9 -0.8 11.8 7.3 -38.1 9.1 24.7Memo Item: Development Expenditure without Melamchi & Marsiyangdi

-

-

-

-

-

-

33.6

27.5

-18.2

35.4

28.4

-19.8

42.7

50.4

a Deviation of actual expenditure from the Budget for same year.

b Increase in FY04/05 Budget over FY03/04 actuals.

c Shortfall partly reflects slippage in the approval of Poverty Reduction Support Credit (PRSC).

Source: Ministry of Finance, (Budget Documents).

15

Table 4: Budget Projections—PRSP vs MTEF, FY02/03–FY04/05 (In billion Rs)

a Adjusted for implementation shortfall. An implementation shortfall of 15% is assumed in Table 4, to allow for normal

implementation delays as well as for uncertainties with the implementation of the Melamchi drinking water and Marsyangdi

hydropower projects.

Item FY02/03 FY03/04 FY04/05 Government Revenue PRSP High Case 53.0 61.4 71.8

Low Case 52.3 58.6 65.5 MTEF Target 57.2 62.2 70.3

(Actual) (56.2) (62.2) (n.a.) Domestic Borrowing PRSP High Case 14.0 12.2 9.8

Low Case 14.0 12.6 10.9 MTEF Target 12.0 11.8 9.1

(Actual) (11.9) (7.3) (n.a.) Regular Expenditure PRSP High Case 57.0 58.6 60.3

Low Case 55.6 59.1 63.5 MTEF Target 57.4 60.5 64.5

(Actual) (55.0) (59.3) (n.a.) Development Expenditure PRSP High Case 32.5 40.9 51.5

Low Case 29.0 35.0 40.5 MTEF Target 38.7 41.8 47.2

Targeted Adjusteda 32.9 35.5 40.1 (Actual) (29.0) (32.8) (n.a.)

Sources: The Tenth Plan/PRSP; MTEF and Budget documents. 33. Streamlining/Cleaning up the Portfolio. To make room for PRSP priorities (and security-related expenditures in the regular budget), a number of low-priority projects were eliminated in the FY02/03 budget/MTEF (Table 5). The Government had already begun to streamline the development program as part of the recommendations of the PERC, and some 83 budget lines were deleted in FY01/02. Since then, an additional 199 projects were eliminated during FY02/03. Although there has been a marginal increase (of 20) in the number of new projects/activities in FY03/04 and FY04/05, the total number of projects has been kept within tight limits. This has helped to double the budget allocation per project compared to earlier years.

Table 5: Key changes on the Development Budget Allocations, FY98/99-FY04/05

Item FY98/99 FY99/00 FY00/01 FY01/02 FY02/03 FY03/04 FY04/05 Dev. Budget (Rs Billion) 37.74 41.85 48.11 50.47 38.68 41.85 47.20 Number of Projects 770 681 715 633 434 443 454 Allocation per Project (Rs Million)

49.01 61.45 67.29 79.73 89.12 94.47 103.97

Source: HMGN Budget Documents. 34. Portfolio cleaning has helped to ensure that the projects/programs remaining in the development budget are largely those that are necessary for achieving the PRSP's poverty reduction objectives. For purposes of funding, these have been ranked further into P1, P2 and P3 in terms of their importance for poverty reduction. The P1 projects now account for 73% of the planned MTEF expenditures, up from 59% in FY02/03 (Table 6); and these are assured of full funding. As noted, P2 and P3 projects/programs will get funded only after releases are made to P1

s. These are also possible candidates for deletion in the future.

16

Table 6: Priority Classification in the MTEF, FY02/03-FY04/05

FY02/03 FY03/04 FY04/05 Item No. of

Projects Amount

(Rs. Billion)

% of Dev.

Budget

Allocation per

Project (Rs.

Million)

No. of Projects

Amount (Rs.

Billion)

% of Dev.

Budget

Allocation per

Project (Rs.

Million)

No. of Projects

Amount (Rs.

Billion)

% of Dev.

Budget

Allocation per

Project (Rs.

Million) Priority One

186 22.82 59 122.7 206 30.34 73 147.3 250 35.88 76 143.5

Priority Two

131 12.76 33 97.4 164 9.75 23 59.5 155 10.06 21 64.9

Priority Three

117 3.09 8 26.5 73 1.75 4 24.1 49 1.26 3 25.7

Total 434 38.68 100 89.1 443 41.84 100 94.5 454 47.20 100 104.0 Source: MTEF. E. Predictability of Funding 35. The MTEF has provided a degree of consistency and predictability in resource allocations and availability, enabling the line ministries to undertake forward planning of their activities on a medium term basis. This can be seen at two levels: (i) at the aggregate and sector levels (see below), and (ii) funding for prioritized activities. As Table 7 (Development Budget projections in successive MTEFs) below indicates, the projections for total development expenditures in the successive MTEFs have fallen within a narrow range, (though there is some question about MTEF 3 target for FY04/05). Thus, the overall sectoral resource envelopes for the line ministries have not been subject to erratic fluctuations; and for those sectors and sub-sectors which are PRSP priorities, the allocations have been reasonably predictable. Line ministries are now fully aware that, if they do not take the MTEF seriously and do not prioritize and justify their funding demands on that basis, they are unlikely to get funding as in the past. Conversely, those line ministries which can develop sector programs to deliver PRSP goals and objectives are now able to secure even substantially increased funding from the Government and external donors. Education and Health are two good examples. Both have been able to develop sector-wide approaches (SWAPs) recently and secure substantially increased medium term commitments from external donors---$159 million for Education and $104 million for Health---, which will allow them to implement and expand their programs in a predictable manner for the next few years.

Table 7: Development Budget Projections in Successive MTEFs

(In billion Rupees)

Item FY02/03 FY03/04 FY04/05 FY05/06 Revenue 56.1 60.2 70.3 79.5 Dev. Exp. MTEF 1 38.7 43.1 49.1 -

MTEF 2 - 41.8 44.5 50.5 MTEF 3 - - 47.2 52.9

Sources: Budget Documents; MTEF.s 36. At the individual program/activity level, funding predictability has improved significantly for priority activities. As Table 8 indicates, about 70-75% of activities in the development budget are now classified as P1

s; and their share in actual expenditures has closely matched their share of budget allocations in the last two years. (In FY02/03, their share of actual expenditures—69%—was slightly less than their allocation share—71%. But, this was due to the implementation shortfalls of the Melamchi and Marsiyangdi

17

projects, both of which are classified as high priority. In FY03/04, P1s share in actual

expenditures—78%—in fact exceeded their allocation share—76%). It should also be noted that, by and large, funding allocations for P1

s are about 3-5 times larger than those for P2

s and P3s; and the rising share of P1

s in actual expenditure suggests that they have continued to get preference for available funding. This of course does not mean that there are no funding availability problems for P1

s. As discussed below, overall fund releases can be, and are affected, (as was the case in FY02/03), by cash flow/availability problems, such as delays in aid disbursements. In such situations, the Government is still forced to hold back fund releases. But, funds are no longer rationed across the board or on a "first come first served" basis as earlier; and P1

s do get priority. Thus, funding unpredictability is not a major problem hampering implementation any longer. There are, however, a range of other problems which still constrain implementation, including work program preparation delays, growing difficulties for the government to operate in conflict affected areas, aid disbursement delay and cash flow delay for projects affecting the aid driven P1 projects, etc.

Table 8: Funding of Priority Activities in the Development Budget, FY02/03-FY04/05 (%)

FY02/03 FY03/04 FY04/05* Priority Budget

Allocation Actual

ExpenditureBudget

AllocationActual

ExpenditureBudget

Allocation P1 71.0 68.6 75.8 77.6 76.0 P2 25.5 27.6 20.5 18.4 21.3 P3 3.5 3.8 3.7 4.0 2.7 Total 100.0 100.0 100.0 100.0 100.0

* Actual expenditure data are not available. Source: National Planning Commission, MTEF documents.

37. Improvements in Resource Allocation—Consistency of the Public Investment Program with the PRSP. As discussed earlier, a major weakness contributing to poor public expenditure performance in the past has been the weak linkages between the development plans, policies and strategies on the one hand, with resource allocations in the annual budget on the other. As a result, the development program had become a collection of inherited activities, funded annually on an ad-hoc incremental basis. This section will review how far this situation has changed over the past few years, paying particular attention to the inter-sectoral allocations, and within the key sectors, to significant changes in the intra-sectoral allocation pattern. It will also review how key cross-cutting approaches envisaged in the PRSP to accelerate implementation and especially to achieve a greater impact/effectiveness of public spending are being implemented. Given the time limitations, this review will necessary be brief, but will highlight the salient developments and issues. 38. Inter-Sectoral Allocations. The PRSP stresses the importance of human development for reducing human poverty and improving the quality of life in rural areas. Education, health, rural drinking water and sanitation, and local development (decentralization) are particularly important in this regard. In addition, basic infrastructure such as (even low-quality) roads, electricity and telephone communications can help improve the living conditions for the poor in rural areas. The PRSP places heavy emphasis on ensuring through these sectoral programs equitable access of women, marginalized groups/communities and districts in order to mainstream them in the development process.

18

39. Government efforts to prioritize and realign programs and activities in line with PRSP goals and strategies have helped to bring about some major shifts in the inter-sectoral composition of the development budget in favor of the main focus areas of the PRSP: (i) The share of the social sectors—education, health, drinking water and local development—has risen from about 35% of actual development expenditure in FY00/01 to 42% in FY02/03; and has further increased to 47% of the development budget allocations in FY04/05 (Table 9). Within this group, the share of the education sector has risen from 7.5% to 13.3%, health from 5.3% to 9.6%, drinking water from 6.5% to 7.6% and local development from 12.5% to13.0% over the period. All four sectors are particularly important for achieving the PRSP's human development and social inclusion goals, and for operationalizing the decentralized, community-managed approaches to improve delivery and efficiency of public services in rural areas. The impressive increases in allocations/expenditures in both education and health also reflect the fact that the recent fiscal reforms have provided a major incentive for the more dynamic10 sectors to adopt sector-wide programs (SWAPS), with substantially increased support from external donors. (ii) To make room for these large increases, the allocation/expenditure shares of virtually all other sectors (except for the communications sector) have been reduced, notably power, (where the completion of the Kaligandaki A project as well as delays in the implementation of the Marsyangdi hydro power project have slowed down

Table 9: Composition of Development Expenditure, FY99/00-FY04/05

(Rs Billion)

Item FY99/00 FY00/01 FY01/02 FY02/03 FY03/04 Budget

FY04/05Budget

Social Services 12.41 12.87 11.53 12.19 17.58 22.38 Education 2.57 2.78 2.76 2.73 4.34 6.26 Health 2.13 1.97 1.88 1.62 3.03 4.51 Drinking Water 2.42 2.41 1.75 2.01 3.46 3.57 Local Development 4.14 4.63 4.16 5.27 5.40 6.14 Other Social Services 1.15 1.08 1.00 0.56 1.36 1.89 Economic Services 8.13 8.70 8.27 6.24 10.17 10.42 Agriculture 2.09 2.33 2.56 1.83 2.20 2.53 Irrigation 3.04 3.95 3.14 2.14 2.70 3.10 Forestry 0.52 0.48 0.63 0.62 0.63 0.67 Other Economic Services 2.48 1.94 1.93 1.65 4.65 4.12 Infrastructure 10.52 12.41 9.18 9.35 13.16 13.35 Roads/Transportation 4.70 5.35 4.52 3.73 5.39 5.66 Communication 0.28 0.24 0.27 1.72 0.85 1.34 Electricity (power) 5.54 6.81 4.40 3.90 6.92 6.35

Others 0.69 3.08 2.50 1.25 0.93 1.05 Total Development Expenditures 31.75 37.07 31.48 29.03 41.85 47.2 Percentage Share (%)

10 In the past, health has been one of the weaker sectors in terms of implementation capacity, fund

utilization and efficiency/effectiveness of public spending. But, recent sector initiatives in terms of forward planning and refocusing the sector program are promising.

19

Item FY99/00 FY00/01 FY01/02 FY02/03 FY03/04 Budget

FY04/05Budget

Social Services 39.08 34.73 36.62 41.98 42.01 47.42 Education 8.11 7.51 8.75 9.40 10.36 13.26 Health 6.70 5.32 5.96 5.58 7.23 9.56 Drinking Water 7.63 6.49 5.55 6.93 8.26 7.56 Local Development 13.03 12.48 13.20 18.14 12.90 13.01 Other Social Services 3.61 2.92 3.16 1.93 3.25 4.00 Economic Services 25.62 23.48 26.26 21.50 24.31 22.08 Agriculture 6.58 6.28 8.14 6.31 5.25 5.36 Irrigation 9.59 10.67 9.98 7.36 6.44 6.57 Forestry 1.63 1.29 2.00 2.15 1.50 1.42 Other Economic Services 7.81 5.23 6.14 5.68 11.12 8.73 Infrastructure 33.12 33.49 29.17 32.20 31.45 28.28 Roads/Transportation 14.79 14.45 14.35 12.83 12.89 11.99 Communication 0.89 0.66 0.86 5.93 2.03 2.84 Electricity (power) 17.44 18.38 13.96 13.44 16.54 13.45 Others 2.19 8.31 7.94 4.32 2.22 2.22 Total 100.00 100.00 100.00 100.00 100.00 100.00 Memo Item: Pro-poor Spending (% of total) 32.80 34.00 36.70 40.40 42.40 n.a.

Source: Budget documents, MTEF. public investment in generation). (iii) The share of transport, also critical for improving rural access, has been held reasonably stable. (iv) But, the expenditure/allocation shares of irrigation and agriculture have fallen, though they are critical for promoting broad-based income and employment growth in rural areas. As discussed below, these are partly the result of policy-induced changes within the sectors, as well as their inability to develop and effectively implement integrated programs to achieve sectoral and PRSP goals (see below). 40. Intra-Sectoral Allocations. A major problem has been the disconnect between the development plans on the one hand and sectoral programs and activities on the other. As discussed in the 2000 PER, there were considerable misallocations of resources within key sectors. The MTEF and its prioritization process have helped to considerably reduce these distortions, align sectoral activities more in line with the overall thrust of the Tenth Plan/PRSP, and improve the internal consistency of sectoral programs. While there is more to do at the sectoral level in further improving the prioritization and better aligning sectoral activities with sector objectives and expected outcomes, the progress that has been achieved so far is significant. The improvements in the major sectors in this regard as well as shortcomings are discussed briefly in Annex 2. F. Reforms in Budget Procedures 41. Changes in existing fund release procedures were an important element of the MTEF reforms introduced in July 2003. Previously, the Government's fund release procedures did not distinguish adequately between development priorities and other activities in releasing funds to them. Although a core program did exist, and priority was given to those in the core program at the beginning of the fiscal year, (core

20

projects/activities received initial releases up to 4 months' requirements, while only two months' requirement was released to others), subsequent releases to projects were largely dependant on spending progress. Those who had spent their initial releases were able to get additional releases irrespective of their priority rating. Thus, this system generally preferred quick spenders rather than priorities, and construction oriented sectors such as power and roads generally benefited at the expense of service-delivery oriented sectors such as health and agriculture. 42. To help fund the PRSP priorities, fund release procedures were changed by linking them directly to the MTEF's prioritization process. Thus, (i) all P1 activities were assured funding, while others were to be funded only if additional funds were available. (ii) Fund releases were tied to performance. Work programs had to be approved before the initial fund release was made at the beginning of the fiscal year, while subsequent releases required the submission of financial reports as well as reporting on physical progress achieved (on the basis of intermediate indicators/norms identified in the work programs) and their certification by appropriate authorities in the line ministries and agencies. Initially, these procedures wee limited to P1 activities, but they were subsequently extended to other activities and also to district and local levels, where the District Treasury and Controller Offices (DTCOs) were made responsible for the release of funds on the basis of monthly expenditure reports and trimesterly progress reports. The Government's Financial Administration Rules were changed in FY02/03 in order to institutionalize these changes. 43. These changes have clearly helped to improve the fund release process for priority development activities. Fund releases are now directly linked to development priorities. In practice, as evident from Table 8 above, the Finance Ministry and its agencies have strictly adhered to the priority classification in releasing funds over the past two years; (actual expenditures in the last two years have corresponded very closely to the priority classification of development activities). This is a major change from the previous practice under which any project would receive funding, (irrespective of their economic merits/justification), so long as they had a budget allocation, they could spend quickly, and could bring political clout and influence on their behalf. As a result, cash management by the Government has also become more rational (see para. 37). Moreover, the new process has strengthened the hands of the FCGO in enforcing reporting requirements. Work programs now have to be prepared by spending units as a pre-condition for the initial fund release, and they have to provide periodic reports to obtain subsequent releases. However, the efforts to link fund releases to performance—to physical/implementation progress11—has a long way to go. Although spending units now submit trimesterly reports on physical progress (which are certified by the line ministries/agencies), there is no capacity for verification of the accuracy of these reports (even on a sample basis) in the FCGO, who are responsible for fund releases. However, FCGO have conducted Public Expenditure Tracking Surveys (PETS) for some sectors and examined the fiduciary risk in those sectors. This is an area which needs to be strengthened, as discussed in para. 139 below.

11 Under the new arrangements, funds will be released immediately if physical achievement/progress is 80%

or more; releases will be subject to review and agreement on further action if progress is between 50% and 80%; and releases will be stopped if progress is below 50%.

21