Strategic Operational Innovations: Critical Success Factor For … · 2008-05-28 · Strategic...

21

Strategic Operational Innovations: Critical Success Factor For Multi-Play Services An Executive Brief “Partnering with clients to create innovative growth strategies” November 2006

Transcript of Strategic Operational Innovations: Critical Success Factor For … · 2008-05-28 · Strategic...

Strategic Operational Innovations:

Critical Success Factor For Multi-Play Services

An Executive Brief

“Partnering with clients to create innovative growth strategies”

November 2006

Frost & Sullivan reports are limited publications containingvaluable market information provided to a select group of customers in response to orders. Our customersacknowledge when ordering that Frost & Sullivan reportsare for our customers’ internal use and not for generalpublication or disclosure to third parties.

No part of this report may be given, lent, resold, ordisclosed to non-customers without written permission.Furthermore, no part may be reproduced, stored in aretrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording,or otherwise, without the permission of the publisher.For information regarding permission, write:

Frost & Sullivan7550 West Interstate 10, Suite 400San Antonio, TX 78229United States

Stratecast Whitepaper 2

TABLE OF CONTENTS

Executive Summary 4

Multi-Play Services-Situation Analysis 5

Multi-Play Strategies 7

An Integrated Operations Strategy for Service Provider Transformation 11

Search and Other Interactive Services 14

OSS Requirements to Support Advanced Interactive and Search Services 15

1. Common Telecom Data Models 15

2. Common Data Backbone 16

3. Analytics 17

Other Investment Considerations 19

The Last Word 20

About Stratecast 21

LIST OF FIGURES

Figure 1. Convergence Redefines the Competitive Landscape and

Business Models 5

Figure 2. Hybrid Services Create Unprecedented Complexity 7

Figure 3. U.S. Cable Operators Basic Subscribers vs. RGUs 8

Figure 4 Success Factors in a Multiplay World: Optimizing Partnerships 9

Figure 5. Network Operators Possess Unique (And Valuable) Customer Data 10

Figure 6. How Service Providers Measure OSS Project Success 12

Figure 7. OSS/BSS Consolidation: Doing More with Less 14

Figure 8. Search and Advertising Evolution 14

Figure 9. OSS/BSS Shifting from Functional to Data Backbone 17

Figure 10. Paradigms for Object Oriented OSS/BSS Modeling 17

TABLE OFCONTENTS AND

LIST OF FIGURES

Stratecast Whitepaper 3

EXECUTIVE SUMMARY

A top priority for telecommunications service providers today is to plan the evolution ofmulti-play services—including voice, video, data and other communications and mediaservices, as well as hybrid combinations of these. Stratecast believes that, while protectingthis critical base of multimedia connectivity is important, the telecom industry’s singlegreatest opportunity in the multi-play bundled services area will be in advanced highlycustomized search, advertising and interactive services.

Although telcos face a range of non-traditional competitors also targeting the multi-playmarket, we believe that telecommunications operators are uniquely positioned to applyanalytics to customer data culled from a range of sources to create a wealth of newadvertising and personalization revenue opportunities involving multi-play services. But todo so, the telcos must make fundamental changes to their operations support system(OSS) architecture—Consolidating OSS, breaking down traditional product/operationalsilos, migrating to a data infrastructure that will enable them to share key customer andother types of data among multiple operational areas, substantially improving dataintegrity, and applying sophisticated analytics to that data. It is also very important tonote that the benefits to be derived from these infrastructure investments andorganizational evolution will not be restricted to emerging service types. For networkoperators that must find ways to optimize existing operations that still provide themajority of revenue and also become agile enough to react to new opportunities to driveorganic growth and pursue emerging opportunities for consolidation, strategic planningand investment are absolutely critical. Service providers must commit to restructuringtheir entire business to closely align business operations and the processes, procedures,and partnerships underlying those operations with customer needs and desires. Breakingdown traditional silos of operation - whether based on product, marketing, channels,partners, or other factors - is a crucial foundation for rebuilding telco business modelsaround user centric bundles of services for the emerging multi-play future.

In this white paper, we look at the drivers for multi-play services, a sample of some of thecompelling new multi-play and hybrid services that are being created, and the newcompetitive market. We also explore a variety of strategic choices for network operators.Chief among these are new opportunities in advanced highly customized search,advertising and interactive services.

We also review the status of service providers’ operations support systems today andexplore the specific upgrades they must make and types of analytic and data managementcapabilities they must gain in order to capitalize on new opportunities in the multi-playmarket.

Stratecast Whitepaper 4

MULTI-PLAY SERVICES-SITUATION ANALYSIS

The concept of “triple play” services providing voice, video and data over a single physicalcommunications line to the end user has now grown into something much broader andpotentially more powerful. Although the concept had its genesis in network convergence(or the consolidation of multiple types of communication onto a single physical medium),it now unlocks and encompasses many more types of convergence. Figure 1 illustratesthis evolution.

Figure 1. Convergence Redefines the Competitive Landscape and BusinessModels

Source: Stratecast CMS1-2 Multi-Play Landscape: Setting the Scene for n-Play Services1

One important type of convergence is device convergence, such as PDAs that enablevoice and data communications and also run a full suite of desktop applications; or theChocolate device from LG, which combines an MP3 player with a mobile phone. Anotherexample of an important converged device is a WiFi phone combined with a mobilephone, which enables a single handset to be used for mobility or in the home using abroadband connection. Such devices are a key driver of fixed-mobile convergence, whichwill – according to Deutsche Telekom – comprise one third of its telecom market by2010.2

Stratecast Whitepaper 5

1. For a copy of this and other Stratecast reports mentioned in this white paper, please contact [email protected], or 877-463-7678

2. October 2006 presentation by Dr. Rain Deutschmann, vice president of strategy, Deutsche Telekom

Another important form of convergence is application convergence. Here, applicationsoriginally developed on a single platform are extended to multiple platforms. Forexample, a browser interface designed for a broadband data connection could beextended to operate on devices originally designed for use with other platforms, such aswireless phones with data connectivity or a gaming platform that supports voicecommunications. We emphasize, however, that while these elements are crucial toleverage in the multiplay arena, they do not yet provide a seamless, converged userexperience.

Driving the demand for converged applications are increasingly converged lifestyles.Communications service customers are mixing their personal and professional domains,working interchangeably between their home and office and using applications originallydesigned for the consumer market, such as instant messaging and chat, to conductbusiness more efficiently.

Convergence is also occurring among the service providers themselves, as providers thatpreviously only offered individual elements of multi-play services (such as cable companiesthat focused on video and telecommunications operators that focused on voice and data)now enter one anothers’ businesses. Increasingly, these providers find themselves as bothpartners and competitors. Among these partnerships are several that pair a telco with adirect broadcast satellite provider, as well as a joint venture between several cablecompanies and Sprint, which today has become largely a wireless company.

We include interactive content and search companies such as Google and Yahoo amongthe companies that will be both competitors and partners to service providers.Increasingly such players, which we refer to as X-factor companies, are moving into themulti-play arena. Several offer VOIP for example—and Google also has ventured intomunicipal WiFi.

The concept of multi-play services is also evolving in another important dimension.Increasingly, providers are seeking to create hybrid services that combine elements frompreviously separate services to create new offerings—such as podcasting, which combineselements of audio broadcast and data download offerings, or click to talk, which combinesdata and voice to create a new service capability. Figure 2 demonstrates the complexityinherent in designing, deploying, marketing and managing these new service types.

Stratecast Whitepaper 6

3. For additional insight on this topic, please see Stratecast’s SPIE 05-37: Google and Content Delivery.

Figure 2. Hybrid Services Create Unprecedented Complexity

Source: Stratecast CMS1-2 Multi-Play Landscape: Setting the Scene for n-Play Services

Network technology enhancements will create rich new services, but also introduce newbusiness challenges. Several hurdles must be overcome before hybrid services can bebroadly deployed. These may include trans-carrier service delivery issues such as billingand revenue sharing, end user authorization and authentication, and digital rightsmanagement. It’s worth noting, however, that some stakeholders downplay the importanceof digital rights management. For example, Gerd Leonhard, music futurist and CEO ofstreaming music player developer Sonific believes that end users will move to asubscription-based model of content consumption, which would minimize the need fordigital rights management. Leonhard argues that users will access, rather than own,content and notes that he already sees content owner priorities shifting away fromcopyright protection and toward monetization. These changes will create additional shiftsin the content supply chain, with continuing demands for changes to telecominfrastructure.

MULTI-PLAY STRATEGIES

Each type of company offering multi-play services faces a unique set of challenges andstrategy choices. Network operators, whose focus traditionally has been on the accesslink itself, increasingly are experiencing disintermediation, as X-factor companies leveragewhat they learn about mutual customers through their online behavior to offer highlypersonalized one-on-one services to those customers and build more direct relationshipswith them. The most immediate form of X-factor company disintermediation may be

Stratecast Whitepaper 7

severe price compression, as these companies include “free” communications services as away to drive increased usage of their core search and content businesses. Examples todate include voice-enabled chat from Yahoo!, Google, and others; the addition of Skypevoice capabilities to Ebay’s ecommerce platform, and the involvement of various X-factorcompanies in deploying free municipal WiFi access—essentially giving away the servicesthat network operators depend on for revenue.

Some network operators may strive to retain control of their customersthrough a “walled garden” that offers only carrier-selected content or bymanipulating quality of service on the broadband link to favor their owncontent offerings. That is absolutely the wrong way to go. Even if networkoperators succeed in dominating the broadband access market, preventing customersfrom enjoying open access to the content they want and/or degrading the performanceand quality of the user experience in accessing that content will seriously diminish thevalue of the providers’ access services and the customer relationships they seek toprotect.

Instead, network operators should learn some lessons from the U.S. cableindustry, where basic subscriber growth has been negative to flat for a numberof years. During that same period, the cable companies have driven theaverage monthly revenue per user (ARPU) from the $40 range to the $90range, as illustrated in Figure 3, by adding content and introducing newservices, including digital video, high-speed data, and voice and keeping serviceprices steady. While delivering these new services has required considerablecapital outlays, because they are delivering multiple services over a singleinfrastructure, cable operators have been able to control operating costs.

Figure 3. U.S. Cable Operators Basic Subscribers vs. RGUs

Source: Stratecast U.S. Cable MSOs: Strategic Market Assessment & Forecast

8Stratecast Whitepaper

In this context it is important to note that this success has not been accomplished alone.From content producers to advertisers to network equipment manufacturers and nowmobile wireless providers, the cable industry has pursued partnerships to create theservices required to drive this impressive revenue growth. All network operators faceformidable new entrants in the multi-play market, particularly on the content side.Network operators (and their vendors) must forge new partnerships with players fromoutside the communications industry or they will eventually compete against them. Foroperators to ensure that they are viewed as high-value partners in the content valuechain, they absolutely must optimize the operations support systems that provide theability to access, analyze and take advantage of existing, vast stores of customer data torapidly create and introduce compelling new services for both end users and partners. Ifoperators optimize their networks to support partner business models, theycan position themselves to impact (and derive revenue from) multiple links inthe overall consumer content and communications service value chain. Figure 4illustrates the varying - and often complimentary - areas of core leadership of the variousplayers that will shape the new landscape.

Figure 4 Success Factors in a Multiplay World: Optimizing Partnerships

Source: Stratecast CMS1-2 Multi-Play Landscape: Setting the Scene for n-Play Services

It is important to include advertising as a class of increasingly interactive content that willboth place great demands on network capabilities and also provide lucrative newopportunities within the multi-play arena. This opportunity is not yet widely recognizedby service providers, who have been more focused on IPTV services—even though suchservices may not represent the best revenue opportunity. According to a forecast fromglobal media research firm Screen Digest, IPTV in 2010 will have just over 10 millionsubscribers and represent just 14% of the television market in the top five Europeanmarkets.4

Stratecast Whitepaper 9

Network

Operations

Enabling

Technologies

Services

Serv

ices

Sta

ck

Network

Operators

VNOs X-Factor Content

Owners

Currently ‘stove-

piped’ by access

technology,

operators could

cling to existing

customers by

creating walled

gardens, partner

with X-factor

companies and

content owners, or

provide VNOs with

network services.

Also ‘stove-piped’ by

access technology,

VNOs win business

with unique segments

through focused

targeting.

X-Factor companies

can bridge the gap

between content

owners and operators

or extend their own

on-line expertise into

new network

channels.

Content owners can

sell through new

channels created by

partnerships with

operators and X-

factor companies, or

they can create their

own channels by

establishing VNOs.

4. The top five European markets, according to Screen Digest, are the U.K., Spain, Italy, Germany and France.

Stratecast expects IPTV services to generate no more than $20 billion inworldwide revenues by 2010. In contrast, looking only at the U.S. market,advertising revenues by 2010 are projected to be nearly $260 billion, accordingto a forecast from Veronis Suhler Stevenson.5 Although not all of these revenues areaddressable within the multi-play and interactive services area, advertisers are increasingspending for online and wireless advertising, and shifting away from traditional media.According to research from Stanford University and Goldman Sachs, keyword searchadvertising is a $2.8 billion market in 2006. Other important Internet advertisingcategories, according to the same group, are display advertising, classifieds and directmarketing, which it expects to generate revenues of $2.2 billion, $1.2 billion and $.59billion respectively, in 2006.

As advertisers continue to experience the power of interactive marketing alternativessuch as the one-to-one highly personalized advertising delivery and presentation optionsoffered by the X-factor companies, Stratecast believes they will shift even more dollars inthat direction.6 While advertising creates direct opportunities for service providers interms of both traditional mass advertising and, increasingly, on-line advertising, serviceproviders must find ways to significantly increase those revenues going forward.

Network operators already have vast stores of customer information such as call detailrecords, service usage patterns for an ever-increasing range of services, payment data, andcustomer demographics. By augmenting this data with that of partners such as the on-linebehaviors tracked by X-factor companies, we believe network operators are uniquelypositioned to leverage data analytics to gain a competitive edge in creating newadvertising revenue opportunities.

Figure 5. Network Operators Possess Unique (And Valuable) Customer Data

Source: Stratecast CMS1-2 Multi-Play Landscape: Setting the Scene for n-Play Services

10Stratecast Whitepaper5. Veronis Suhler Stevenson 2005-2009 Communications Industry Forecast6. For a detailed discussion, see SPIE 05-40 - X Factor Tech: Search and Web Innovations

in a Multiservice Content Environment.

Network operators must recognize the value of their unparalleled customer relationshipsand the associated data. To unlock that value they must be intentional about theirbusiness model. They will need to invest in consolidating and cleaning data repositories,re-architecting their operations support systems, and developing the analytic capabilitiesthat will allow them to act upon that data. In making this or any infrastructureinvestment, service providers must take care that the investments they make are either inline with anticipated slow growth in consumer spending on access and othercommunications services or enable them to tap new revenue sources, specifically contentand advertising.

Ironically, despite the fact that no service provider has yet built a true “quad play service”it is clear that the ability to offer flexible bundles of tightly integrated, customer centricservices has for all intents and purposes already been relegated to “table stakes” status,without which operators will find it difficult or impossible to compete. Clearly in thisrapidly changing and challenging environment, creative thinking is needed at the highestexecutive levels. If top network operator executives are making more trips to WashingtonD.C. and Brussels than to New York City, London, Silicon Valley, Tel Aviv and othercreative hot spots, those operators will quickly fall behind and, in our opinion, will fail inthe long term.

In our view, service providers simply cannot achieve these goals on their own. Networkoperators must develop meaningful strategic alliances with third parties that allow themto avoid distractions and focus on their core operations while still taking advantage ofnew content opportunities and related revenue streams. Partnerships and “rightsourcing”can help operators to address those opportunities, optimize service quality, and deliver aunique customer experience—a strategy that Glenn James, president of communicationsand media for system integrator and software developer Unisys, calls “embracing thegiants.” Just as important, network operators must foster an environment of creativityand experimentation that includes both technological and cultural orientation. This goesfar beyond technology choices and service development and will require service providerinvestments in personnel and other resources required to reorient their business modelsfrom a network and service focus to content and customer focus. Service providersmust commit to making the investments necessary to restructure their entirebusiness. It is absolutely critical to closely align business operations - and theprocesses, procedures, and partnerships underlying those operations - withcustomer needs and desires.

AN INTEGRATED OPERATIONS STRATEGY FOR SERVICE PROVIDERTRANSFORMATION

The recognition of the new opportunities within the multi-play arena that can be realizedthrough a targeted investment in operations support systems comes at a time whennetwork operators already are making substantial changes in those systems.

Price erosion in their traditional markets has driven network operators to leverage theirOSSs to obtain operational efficiency. Other key concerns are multi-service bundling;

11Stratecast Whitepaper

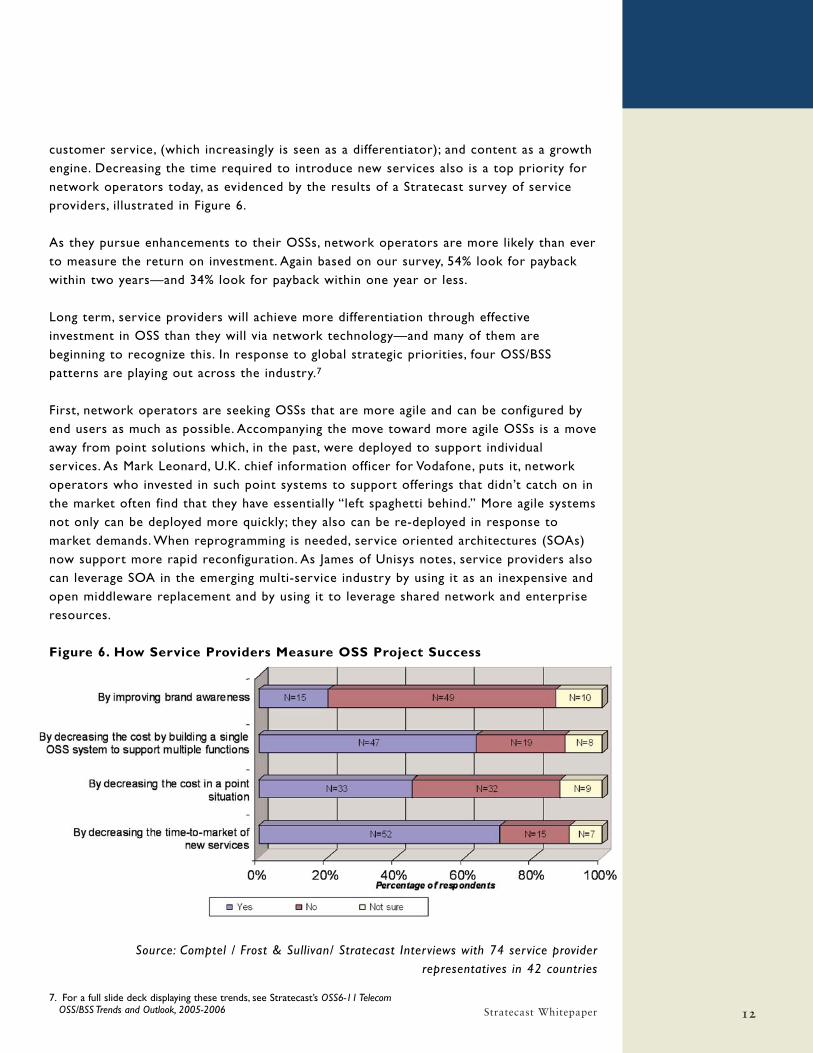

customer service, (which increasingly is seen as a differentiator); and content as a growthengine. Decreasing the time required to introduce new services also is a top priority fornetwork operators today, as evidenced by the results of a Stratecast survey of serviceproviders, illustrated in Figure 6.

As they pursue enhancements to their OSSs, network operators are more likely than everto measure the return on investment. Again based on our survey, 54% look for paybackwithin two years—and 34% look for payback within one year or less.

Long term, service providers will achieve more differentiation through effectiveinvestment in OSS than they will via network technology—and many of them arebeginning to recognize this. In response to global strategic priorities, four OSS/BSSpatterns are playing out across the industry.7

First, network operators are seeking OSSs that are more agile and can be configured byend users as much as possible. Accompanying the move toward more agile OSSs is a moveaway from point solutions which, in the past, were deployed to support individualservices. As Mark Leonard, U.K. chief information officer for Vodafone, puts it, networkoperators who invested in such point systems to support offerings that didn’t catch on inthe market often find that they have essentially “left spaghetti behind.” More agile systemsnot only can be deployed more quickly; they also can be re-deployed in response tomarket demands. When reprogramming is needed, service oriented architectures (SOAs)now support more rapid reconfiguration. As James of Unisys notes, service providers alsocan leverage SOA in the emerging multi-service industry by using it as an inexpensive andopen middleware replacement and by using it to leverage shared network and enterpriseresources.

Figure 6. How Service Providers Measure OSS Project Success

Source: Comptel / Frost & Sullivan/ Stratecast Interviews with 74 service providerrepresentatives in 42 countries

12Stratecast Whitepaper7. For a full slide deck displaying these trends, see Stratecast’s OSS6-11 Telecom

OSS/BSS Trends and Outlook, 2005-2006

Some stakeholders see these more agile OSSs eventually supporting automated servicecreation, where a user’s service selections (such as media bundle, Web purchases orbrowsing) and behavioral evaluation (such as digital entertainment consumption orlocation frequency) are used to generate next-generation services such as digital media,surveillance, and unified communications. A consumer’s use of those services would, inturn, help form the basis for the next round of new service creation.

A second priority for network operators is strategic telecom information managementand analytics (TIMA), aimed at supporting data integrity, interoperability and a singlecustomer view.8 Third, network operators are more open now than in the past to usingtechnologies developed outside the telecom industry, such as SOAs, analytics and IP itself.Using open source software such as Linux and Apache can enable telcos to free upinvestment dollars to support the transition to a more agile OSS, which may require anevolutionary upgrade that spans several years.

Finally, service providers are consolidating multiple functions onto a single platform toobtain increased efficiency, thereby reducing operational expenditures. Such consolidationalso can be essential after a merger or to support inter-service operation. Among thenetwork operators consolidating their OSSs is Telstra, which has a $300 millionconsolidation project underway. Meanwhile, a large US operator is consolidating 60different billing systems—and other operators are consolidating hundreds of currentlyseparate systems. A redundant inefficient OSS/BSS infrastructure is no longer an option(Figure 7).

OSS consolidation projects often have a hidden cost, however. Data migration costs oftenare underestimated and usually exceed the license cost of the new software – in somecases by as much as a factor of six.9 Many data migration efforts are complicated bycorrupt, missing or duplicated data, and every project is unique. Yet vendors aremotivated to underestimate the effort required to migrate data. Operators need torecognize this reality and must place a greater emphasis on effective data migrationstrategies and architectures, particularly if they are to capitalize on new opportunities tosupport advanced interactive advertising and services, which will rely on impeccable data.In the emerging telecom business model, data is as important as services have been in thepast.

13Stratecast Whitepaper

8. For a detailed discussion see Stratecast OSS 6-09, Telecom Information Management and Analysis: A New OSS/BSS Function

9. For a detailed discussion see Stratecast SPIE 06-28 OSS/BSS Data Migration: A Critical and Often Overlooked Enabler of OSS Consolidation

Figure 7. OSS/BSS Consolidation: Doing More with Less

Source: Stratecast

SEARCH AND OTHER INTERACTIVE SERVICES

In considering opportunities for telecom operators within interactive services andadvertising and what is needed to support them, it is helpful to look at how search, themost fundamental interactive service, and related advertising opportunities have evolved.Figure 8 illustrates a basic Search and Advertising evolutionary timeline, here with aGoogle focus.

Figure 8. Search and Advertising Evolution

Source: Stratecast

14Stratecast Whitepaper

Consolidated

OSS

Increasing SP competition

drives emphasis low TCO

Service Providers

Offer Multiple Services

Mergers and

Acquisitions

Technology Enables

Consolidation

Organizational

Barriers

Legacy System

Migration

Legacy Data

Migration

Although network operators have not traditionally participated in the search market, theyare moving more toward that area as their multi-play plans open up new opportunities.Meanwhile, the desire to further refine their targeting capability and the desire tobroaden the media to which they can deliver advertising messages is driving X-factorcompanies to also broaden their business model.

Telecom and content are on a collision course, as both network operators and X-factorcompanies are now looking to offer a full gamut of voice, broadband, wireless, video,content and search services. Through effective partnering, however, the two typesof companies could have the opportunity to deliver unparalleled multi-playofferings that maximize the value of each player’s strengths. Properlydelivered, highly targeted advertising can be perceived as a service by endusers.

Moreover, the same predictive analytics used to develop advertising targets also can beused to deliver other personalized interactive services. For example, caller ID displayedon a television screen — a widely touted multi-play capability — could be furtherenhanced if the system had the ability to learn the users’ preferences based on previousbehaviors. For example, if the user repeatedly sends calls from a particular family memberto voice mail, the system could learn to anticipate this response and handle the callaccordingly.

OSS REQUIREMENTS TO SUPPORT ADVANCED INTERACTIVE ANDSEARCH SERVICES

OSS requirements to support advanced interactive and search services are threefold.Network operators must develop common information models for telecommunicationsdata. They must consolidate data into common backbones. And they must leverage thisdata for competitive differentiation using technologies like analytics.

1. Common Telecom Data Models

How separate OSS functions or systems interoperate is evolving. In a traditional approachwith no shared data bus, each individual system must have a link to every other systemwith which it needs to communicate. As OSS communications proliferate, the linksrequired can be particularly burdensome—and if there is a change to any individualsystem, it impacts every system to which it is connected.

The next evolutionary step is towards a model in which OSSs communicate through anEAI, ESB, or other information bus as provided by companies like JBoss, IBM, BEA, Tibco,and others. Widespread within telecom today, such an approach can significantly reducecommunication costs.

To gain the full value of an EAI or similar messaging infrastructure, however, requires thatOSSs share data in a common format. Otherwise, every time that an OSS interfacechanges, all interfacing systems must also be changed. By, instead, mapping telecom

15Stratecast Whitepaper

information to a common information model, these cascading changes can be reduced. Inother words, to fully realize the benefit of a messaging infrastructure for OSSintegration requires a common object/data model that is shared by allinterfacing OSS systems. Using such an approach, if an individual system changes, onlya single link—to a shared model—is impacted.

2. Common Data Backbone

Underlying many OSS functional consolidation efforts is more often than not a significantdata consolidation effort as well. To illustrate, consider the example of a networkoperator’s CRM and billing, service assurance and SLA management, and serviceprovisioning and activation systems. These systems rely heavily on inventory functionalitythat, in the past, was duplicated in each one.

But increasingly, such systems are being designed so that they can share common masterdata sets. Here, individual systems, such as CRM and service assurance, draw from acommon master, reducing errors, duplicates, and cost. This shift is shown in Figure 9.10

This model clearly is gaining traction. For example, the majority of service providerstoday have consolidated revenue assurance and fraud departments - both of which relyheavily on looking though patterns of usage data to find aberrant behaviors - onto asingle platform using a common intermediation model.

The movement from an inefficient multiple linked database model – through sharedinformation models as described in the previous section - to the single source model isillustrated in Figure 10. As an industry, the most advanced service providers are todayworking to create integrated data models, yet the process of creating these modelsremains inefficient, lacking automated approaches to maintaining metadata that might beused for validation. Many less advanced service providers, however, still have stovepipeddata and have not yet created governance bodies for coordinating and centralizing them.

The common data sources described above solve OSS integration problems andreduce OSS management costs but more importantly going forward, form aplank of multiple, clean data sources on which to build important newfunctionality. Probably the most important technology to leverage these sources isanalytics, described below.

16Stratecast Whitepaper

10. Note that Figure 9 shows that OSS / BSS functions are more componentized in this new model, and can be modularly composed into new systems. Although it is not the focus on this white paper, service oriented architecture (SOA) functionality can create much more agile systems, and is today the de facto approach in the telecommunications industry for building more agile software. Unisys, again, offers a very sophisticated SOA architecture to its service provider clients. Also see OSSCS7-03 Service Oriented Architecture Overview and Best Practices for Telecommunications from Stratecast.

Figure 9. OSS/BSS Shifting from Functional to Data Backbone

Source: Stratecast

Figure 10. Paradigms for Object Oriented OSS/BSS Modeling

Source: Stratecast

3. Analytics

Assuming that network operators are able to establish unified data sources withimpeccably accurate data, the next requirement to support interactive and search serviceswill be analytics. To illustrate the options, consider the example of a system that predictsa customer’s likelihood of churning and based upon that knowledge, presents anappropriate promotion for that customer to a customer service representative. Although

17Stratecast Whitepaper

the analytic details will not be visible to the CSR, the results of that analysis will directthe CSR’s interaction with the customer. Over time, the ability to gather and analyze userdata will enable sophisticated upselling, as well. For example, the service provider mightoffer a premium subscription to a collection of on-demand programming based on userinterests as expressed by their viewing habits and Internet search patterns.

The simplest form of analytics is yes/no questions. In our example, a network operatormight find that all customers in a particular geographic area are churning, and mightdevise a promotion to them—or conversely, might write those customers off and notprompt the CSR to offer any special promotion. The test “does this customer reside inthe target geographic area” is answered with a simple yes/no question and would be usedto make this decision.

A slightly more sophisticated type of analysis involves adding a test against a numberassociated with a particular customer. Customers under a certain age may be most likelyto churn, for example.

Systems also may use a combination of two or more types of analysis to predict acustomer’s behavior. In our example, perhaps the best way to pinpoint a customer’slikelihood of churning is to consider both his geographic location and his age. Thesimplest kind of combination is through a linear equation, which creates a formula topredict a customer’s behavior. Such a formula might read as follows: If 2.3 x Age + 4.4 xIncome > 40: Yes, otherwise: No.

Predictive analytics is a further refinement of linear combinations that obtains elements ofthe formula by analyzing historical data. Adaptive analytics goes even further by updatinghistorical data and re-deriving numbers periodically to take changing situations intoaccount.

Other analytic options include high-dimensional analysis, which use three or more variablesto predict a customer’s behavior, as well as nonlinear analytics, where the equations usedto make decisions are more sophisticated than the linear form shown above.

Predicting churn is just one example of how telecom and X-factor companies can usepattern recognition provided by a wide portfolio of analytic tools to build compellingrevenue generating functions in telecom, media and entertainment. Analytics can also beused for a wide variety of traditional and new applications, including revenue assuranceanalysis, customer profitability analysis, targeted marketing (through direct mail, online,and other means), one-to-one advertising (as above), collaborative filtering(recommending products and services to “customers like you”), and many more. Retailand other industries that have crossed the threshold from technology- to a customerservice-based focus have all leveraged these approaches for improved customer care andcompetitive differentiation. From this point of view, this same shift is inevitable withintelecommunications.

18Stratecast Whitepaper

Although the analytics functionality described above uses the same commondata models that some service providers are building to reduce integrationcosts, this fact is not widely recognized nor exploited within the industry.Data warehousing and business intelligence / decision support functionsremain – by and large – separate from OSS integration efforts.

More generally, network operators that understand that telecom is movingfrom a technology to a service industry and treat OSS/BSS as a strategicpriority with a focus on the importance of data architectures will be bestpositioned to compete in the new content-focused competitive environment.

OTHER INVESTMENT CONSIDERATIONS

As telcos transition to a more agile OSS including more sophisticated data modeling andanalytics, it will be crucial to balance agility and cost. In other words, network operatorsmust take care not to over-invest. Using open source software such as Linux and Apachecan help minimize investment—and rather than starting from scratch in this area, networkoperators may be able to draw on the experience of companies such as Unisys thatalready have considerable expertise in this area. Long wary of open source software,telecoms only recently can draw on the experience of other operators to be confidentthat the movement to open source can be done while controlling risk.

Telcos also may want to consider outsourcing some portion of their development tolower-cost software developers such as those in India. Network operators should takethe long view before outsourcing such projects, however. As Leonard of Vodafone notes,outsourcing initially may appear economical. But network operators may find that suchwork cannot easily be extended and ultimately may be more costly if such extension laterbecomes a requirement. Some stakeholders use the term “rightsourcing” to describe theprocess of outsourcing only projects that are of appropriate scope.

It is worth noting that the software underlying the end user interface also will play a keyrole in the new service creation architecture that will be the next evolutionary step fortoday’s OSSs. The most powerful new services will be supported when the interfaces inconverged devices (such as set-top boxes and dual-mode handsets) are based on openstandards such as HTML and XML. As Viet Nguyen Cao, business development director forMicrosoft TV notes, this creates significant agility for operators to innovate new services.Some network operators may even choose to open up such standards-based interfaces sothat end users can configure their own self-managed and personal media experience.

19Stratecast Whitepaper

20Stratecast Whitepaper

877.GoFrost

http://www.frost.com

Silicon Valley2400 Geng Road, Suite 201

Palo Alto, CA 94303

Tel 650.475.4500

Fax 650.475.1570

San Antonio7550 West Interstate 10, Suite 400,

San Antonio, Texas 78229-5616

Tel 210.348.1000

Fax 210.348.1003

London4, Grosvenor Gardens,

London SWIW ODH,UK

Tel 44(0)20 7730 3438

Fax 44(0)20 7730 3343

CONTACT US

ABOUT STRATECASTStratecast directly assists clients in achieving their objectives by providing critical, objective andaccurate strategic insight, in a variety of forms, via an access-and-industry-expertise-basedstrategic intelligence solution. Stratecast provides communications industry insight superior toa management consultancy, yet priced like a market research firm. Stratecast’s product lineincludes: Monthly Analysis Services [Convergence Strategies & Network Architectures (CSNA),OSS Competitive Strategies (OSSCS), Network Professional Services Strategies (NPSS),Consumer Market Strategies (CMS), and Business Market Strategies (BMS)]. Weekly AnalysisService [Stratecast Insight for Executives (SIE)], Standalone Research, and Business StrategyConsulting.

ABOUT FROST & SULLIVANFrost & Sullivan, a global growth consulting company founded in 1961, partners with clients tocreate value through innovative growth strategies. The foundation of this partnership approachis our Growth Partnership Services platform, whereby we provide industry research, marketingstrategies, consulting and training to our clients to help grow their business. A key benefit thatFrost & Sullivan brings to its clients is a global perspective on a broad range of industries,markets, technologies, econometrics, and demographics. With a client list that includes Global1000 companies, emerging companies, as well as the investment community, Frost & Sullivan hasevolved into one of the premier growth consulting companies in the world.

Bangalore

Bangkok

Beijing

Buenos Aires

Cape Town

Chennai

Delhi

Dubai

Frankfurt

Kuala Lumpur

London

Mexico City

Mumbai

New York

Oxford

Palo Alto

Paris

San Antonio

Sao Paulo

Seoul

Shanghai

Singapore

Sydney

Tokyo

Toronto