“Twinning” a 9% Credit Project with a Tax Exempt Bond/4% ...

State of the Art Tax Exempt Bond Structures for Large Urban ProjectsCity and County of San Francisco

Transbay 8 and Transbay 9

Adam CrayCity and County of San Francisco

[email protected](415) 701-5512

John HamiltonCSG Advisors

[email protected](415) 956-2454

Jonathan ShumRelated

[email protected](415) 677-9000

Brian DaleCiti Community Capital

[email protected](303) 308-7403

R. Wade Norris, Esq.Eichner Norris & Neumann PLLC

[email protected](202) 973-0100

SPECIAL TAX-EXEMPT DEBT FINANCING STRUCTURESFOR

LARGE URBAN “MIXED USE” PROJECTS

• Transbay 8 – Variable Rate 7-Day Demand Bonds Backed byForeign Bank Letter of Credit

• Transbay 9 – Privately Placed Nonrated Fixed Rate Bondscombined with “Total Return Swap”

• Transbay 8 and Transbay 9 are examples of major urbandevelopments on adjacent sites near San Francisco’s newTransbay Transportation Terminal in the booming South-of-Market area of San Francisco.

2

SPECIAL TAX-EXEMPT DEBT FINANCING STRUCTURESFOR

LARGE URBAN “MIXED USE” PROJECTS

• These types of large urban deals generally have 20% of theunits affordable at 50% of AMI or below and have 4% LIHTCon only the 20% of the units that are affordable.

• They are usually done by very large developers withsubstantial balance sheets and liquidity reserves.

• This permits financing structures to be used which producevery low rate borrowing but are generally not available todevelopers of 100% affordable projects at 60% of AMI.

• These financings often involve substantial equity, low LTVs(≤ 65% - 80%), and financing time frames of 5-10 yearsversus 15 or more years.

3

Transbay 8 and Transbay 9Issuer Goals, Objectives, and Role

CITY AND COUNTY OF SAN FRANCISCO – Adam Cray

• Principal goals of the City and County for Transbay 8 and Transbay 9:

• [Adam Cray to complete]

• Role of the City in the planning process:

• [Adam Cray to complete]

• City financial and other contributions:

• Transbay 8

• [Adam Cray to complete]

• Transbay 9

• [Adam Cray to complete]

4

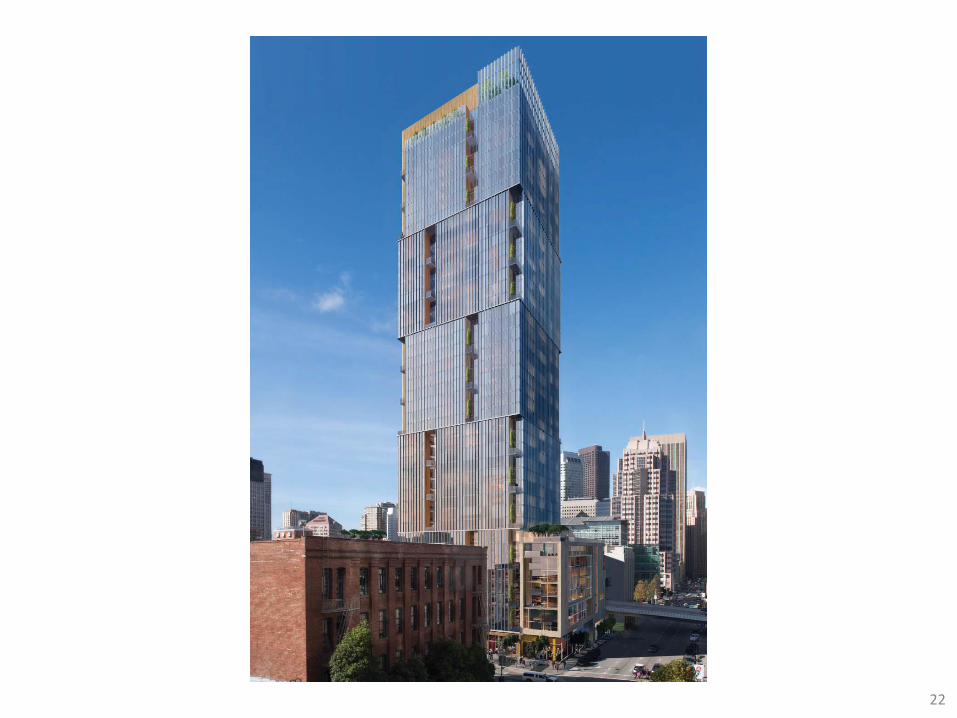

TRANSBAY 8420-488 Folsom Street

San Francisco, California 94105

5

Transbay 8

• Transbay 8 is one of the Transbay District’s tallest residential towers andonce complete, will serve as the final link to the City’s vision of a majorhigh-rise residential and neighborhood retail corridor along Folsom Street.

• Related and Tenderloin Neighborhood Development Corporation (“TNDC”)were selected to master plan and develop the project through a RFPcompetition.

• The project site is 1.14 acre city block bound by Fremont Street to thenorth, Folsom Street to the east, First Street to the south and ClementinaStreet to the west.

6

7

8

27% AFFORDABLE (150 UNITS)

9

10

11

• The Tower Financing was a combination of taxable debt, tax-exempt bondsissued by the City and County of San Francisco, mezzanine debt, preferredequity, 4% LIHTC equity, a streetscape reimbursement from OCII, andsponsor equity.

• Senior Secured Debt. The 80/20 Mixed-Income Rentals and Market RateCondos were financed with a $335 million construction loan facilitycomprised of $95 million of a taxable loan funded by Wells Fargo Bank,N.A. for the condos and $240 million of tax-exempt and taxable bonds tofinance the 80/20 Mixed-Income Rentals in the High-Rise Tower.

• The $240 million of tax-exempt bonds were sold as 7-day Variable RateDemand Bonds backed by a letter of credit provided by the Bank of China.The underwriters were Citigroup Global Markets Inc. and Goldman, Sachs& Co.

12

Transbay 8Tower Financing

(80/20 Mixed-Income Rentals & Market Rate Condos)

13

Transbay 8Tower Financing

(80/20 Mixed-Income Rentals & Market Rate Condos)

Allocation by Product

Construction Sources & Uses Amount 80/20 Rentals Condos

Sources:

Conventional Loan - Wells Fargo Bank $95,000,000 $0 $95,000,000

Bonds - Bank of China Letter of Credit $240,000,000 $240,000,000 $0

Senior Secured Debt $335,000,000 $240,000,000 $95,000,000

LIHTC Bridge Loan - Citibank $16,000,000 $16,000,000 $0

LIHTC Equity - Wells Fargo Bank $1,000,000 $1,000,000 $0

Other Sources $178,000,000 $2,000,000 $176,000,000

Total Sources $530,000,000 $259,000,000 $271,000,000

Uses:

Total Development Costs $530,000,000 $259,000,000 $271,000,000

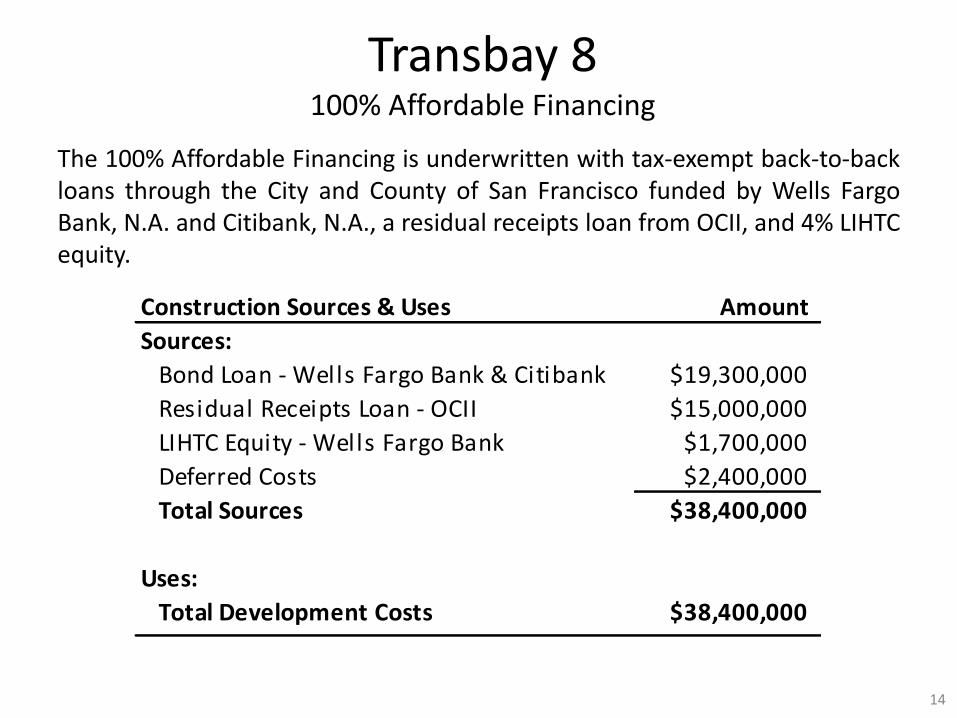

The 100% Affordable Financing is underwritten with tax-exempt back-to-backloans through the City and County of San Francisco funded by Wells FargoBank, N.A. and Citibank, N.A., a residual receipts loan from OCII, and 4% LIHTCequity.

14

Transbay 8100% Affordable Financing

Construction Sources & Uses Amount

Sources:

Bond Loan - Wells Fargo Bank & Citibank $19,300,000

Residual Receipts Loan - OCII $15,000,000

LIHTC Equity - Wells Fargo Bank $1,700,000

Deferred Costs $2,400,000

Total Sources $38,400,000

Uses:

Total Development Costs $38,400,000

Transbay 8UNIQUE ISSUES CONFRONTING

THE CITY AND COUNTY AS ISSUER

John Hamilton – CSG

• While these Bonds are non-recourse to the Issuer, its name is on the paper!

• In letter of credit backed boned issues, a prudent Issuer will not rely on the letterof credit as the sole security for the Bonds. History suggests that bondholdersneed a residual claim to real estate and/or other collateral in the event of awrongful dishonor on the letter of credit.

• Complex intercreditor issues on Transbay 8.

• Two senior lenders; sharing in developer guarantees and real estate collateralin event of a wrongful dishonor on Letter of Credit securing the Bonds.

• Bondholders given first claim to recovery against letter of creditfollowing wrongful dishonor.

• Condo lender given senior claim to developer guarantees.

• Need for coordinated action of two senior lenders.

• Other key structuring issues for the City:

• [John Hamilton to complete]15

Brian Dale – Citi Community Capital

• Challenges of relatively new foreign bank credit in very large U.S.municipal offering of tax-exempt and taxable bonds.

• Very limited number of money funds approved to buy bonds with this bank’sletter of credit.

• Buyer base is further limited as some investors only buy housing debt withGSE credit support.

• Money funds related to parties involved in the financing may have policiesprohibiting purchase of the bonds.

• Additional political risk of using a foreign bank could cause funds to sell ortender their debt.

• $68 million of the $240 million of total bonds were taxable. A “large”municipal issuance is considered small and lacks attention from taxableinvestors, who regularly purchase $1B+ of individual securities.

16

Transbay 8Underwriting

Brian Dale – Citi Community Capital

• Managing intercreditor issues.

• Wrongful dishonor is a Lender Default, eliminating bondholder’s claim on thesponsor guarantee but not the real estate collateral.

• VRDN investors expect low-complexity, high-quality, large-volume letters ofcredit. Adding a unique intercreditor structure could decrease investorappetite.

• Two underwriters and remarketing agents necessitated two separateCUSIPs for each of the taxable and tax-exempt issuances.

• Unique 2-underwriter structure for the variable rate bonds.

• Resurgence of foreign bank letter of credit backed financing – anotherpending $200+ million financing of this type in San Diego.

• Other

• [Brian Dale/Bryan Barker to complete]17

Transbay 8Underwriting

18

Transbay 9510 Folsom Street

San Francisco, California 94105

Transbay Block 9 is a high-density, mixed-income project developed byEssex Property Trust and TMG Partners located at 510 Folsom Street on a .72-acre site adjacent to and immediately to the south of the Transbay 8 site.

• The Project consists of a 43 story tower on Folsom Street attached to an8-story podium building on Folsom and First Street, and a row of twostory townhouses with three units, for a total 570 units. A total of 456market units will be located in the tower and a portion of the podium.

• A total of 114 affordable units will be located in the podium andtownhouses (the “Block 9 affordable project”).

• A shared underground car and bicycle parking garage will accommodateparking for both the Market rate project and the Affordable project.

19

Transbay 9Project Overview

20

21

22

23

TRANSBAY BLOCK 9SAN FRANCISCO, CA

Transbay 9Overall Sources and Uses

[Brian Dale and Bryan Barker to work with Borrower to provide?]

24

Total Return Swap Private Placement Bond StructureThe tax-exempt debt for the project was comprised of $132 million of privately

placed fixed-rate bonds using a “total return swap” structure. Under such a structurebonds are typically structured as fixed rate (e.g., 6.0%) unrated, non-credit enhancedtax exempt bonds sold to a bank in a private placement, in this case, Citibank, N.A.and Deutsche Bank. The Bonds are issued in large minimum denominations (e.g.,$100,000 or higher), and are subject to transfer restrictions.

• The Borrower then enters into a swap transaction with the Bank whicheffectively converts the Borrower’s fixed rate borrowing into an extremely verylow variable rate borrowing as follows: The Borrower makes floating ratepayments on the swap based upon a stated notional amount which is generallyequal to the outstanding amount of the fixed rate Bonds.

• Payments by the Borrower on the swap float, based upon the SIFMA index plus aspread of a fixed number (e.g., 100) of basis points. That amount is paid to theBank as the Swap Counterparty, often on a monthly basis.

• The Swap Counterparty in turn makes fixed rate payments at a fixed rate equal tothe fixed rate on the Bonds, generally on the same Notional Amount.

• The Good News: The net effective borrowing rate in this example is what theBorrower pays on the swap – in this example the SIFMA index (≈ 0.90) + 1.00% =1.90%, an extremely low borrowing rate.

25

Total Return Swap Private Placement Bond Structure• The Bad News: The Borrower will be required to post additional

collateral to the Bank to the extent the Notional Amount of the swapexceeds some percentage (e.g., 75%) of the market value of the Project,as determined by the Bank on a periodic basis.

• The swap generally expires on a date 5-7 years from the initial effectivedate.

• Result: This structure provides an extremely low borrowing rate, butonly for a limited term (usually 5 – 7 years, which may be rolled forward)and only for large balance sheet borrowers who can post additionalcollateral if required.

26

Multifamily Tax Exempt Debt

Helen FeinbergManaging Director

RBC Capital [email protected]

(727) 895-8892

RBC Capital Markets Disclaimer

RBC Capital Markets, LLC (“RBC CM”) is providing the information contained in this document for discussion purposes only and not in connection with RBCCM serving as Underwriter, Investment Banker, municipal advisor, financial advisor or fiduciary to a financial transaction participant or any other person orentity. RBC CM will not have any duties or liability to any person or entity in connection with the information being provided herein. The informationprovided is not intended to be and should not be construed as “advice” within the meaning of Section 15B of the Securities Exchange Act of 1934. Thefinancial transaction participants should consult with its own legal, accounting, tax, financial and other advisors, as applicable, to the extent it deemsappropriate.

This presentation was prepared exclusively for the benefit of and internal use by the recipient. This presentation is confidential and proprietary to RBCCapital Markets, LLC (“RBC CM”) and may not be disclosed, reproduced, distributed or used for any other purpose by the recipient without RBCCM’sexpress written consent.

By acceptance of these materials, and notwithstanding any other express or implied agreement, arrangement, or understanding to the contrary, RBC CM,its affiliates and the recipient agree that the recipient (and its employees, representatives, and other agents) may disclose to any and all persons, withoutlimitation of any kind from the commencement of discussions, the tax treatment, structure or strategy of the transaction and any fact that may be relevantto understanding such treatment, structure or strategy, and all materials of any kind (including opinions or other tax analyses) that are provided to therecipient relating to such tax treatment, structure, or strategy.

The information and any analyses contained in this presentation are taken from, or based upon, information obtained from the recipient or from publiclyavailable sources, the completeness and accuracy of which has not been independently verified, and cannot be assured by RBC CM. The information andany analyses in these materials reflect prevailing conditions and RBC CM’s views as of this date, all of which are subject to change.

To the extent projections and financial analyses are set forth herein, they may be based on estimated financial performance prepared by or in consultationwith the recipient and are intended only to suggest reasonable ranges of results. The printed presentation is incomplete without reference to the oralpresentation or other written materials that supplement it.

IRS Circular 230 Disclosure: RBC CM and its affiliates do not provide tax advice and nothing contained herein should be construed as tax advice. Anydiscussion of U.S. tax matters contained herein (including any attachments) (i) was not intended or written to be used, and cannot be used, by you for thepurpose of avoiding tax penalties; and (ii) was written in connection with the promotion or marketing of the matters addressed herein. Accordingly, youshould seek advice based upon your particular circumstances from an independent tax advisor.

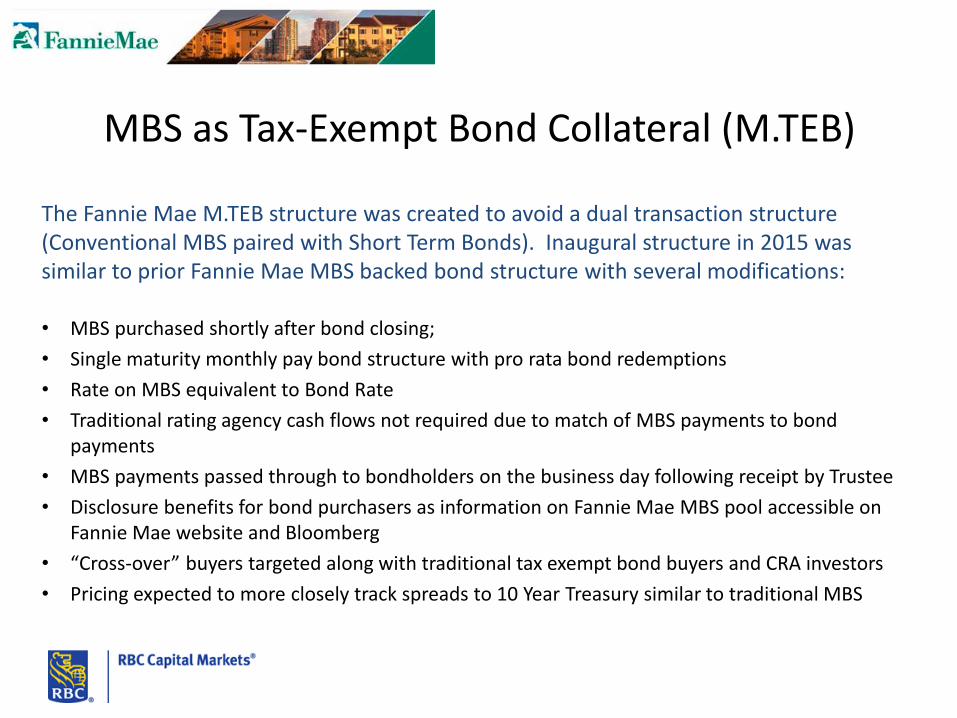

MBS as Tax-Exempt Bond Collateral (M.TEB)

The Fannie Mae M.TEB structure was created to avoid a dual transaction structure (Conventional MBS paired with Short Term Bonds). Inaugural structure in 2015 was similar to prior Fannie Mae MBS backed bond structure with several modifications:

• MBS purchased shortly after bond closing;

• Single maturity monthly pay bond structure with pro rata bond redemptions

• Rate on MBS equivalent to Bond Rate

• Traditional rating agency cash flows not required due to match of MBS payments to bond payments

• MBS payments passed through to bondholders on the business day following receipt by Trustee

• Disclosure benefits for bond purchasers as information on Fannie Mae MBS pool accessible on Fannie Mae website and Bloomberg

• “Cross-over” buyers targeted along with traditional tax exempt bond buyers and CRA investors

• Pricing expected to more closely track spreads to 10 Year Treasury similar to traditional MBS

Why Fannie Mae M.TEB?

• Interest Rates of +/- 4.00%

• Fannie Mae is aggressive on Guaranty/Servicing Fees; Providing .75% COI Rebate

• Highly cost effective structure for Acquisition/Rehab and New Construction

• Greater Certainty of Execution with Delegated Underwriting and Streamlined Processing

• Increased Investor Base for Aaa/AA+/MBS Bonds – traditional tax exempt buyers, taxable MBS buyers, CRA buyers, Financials institutions, Insurance companies

• Long Term Tax Exempt Debt; Opportunities to refund at a later date

• Flexible Structure: Premium pricing, 30-35 Yr amortization , IO & varied prepayment

• Ability to add Supplemental Loans post- closing to “earn-out” additional proceeds

30

Fannie Mae M.TEB Transactions to Date

• RBCCM has closed 7 M.TEB transactions ($115MM) since 2015 with several transactions pending

• MBS rates priced based on a spread to the 10 Year Treasury

• Bond/Pass-through Rates ranging from 2.60% to 3.45%

• Up to 90% LTV and up to 35 Year Amortization

• Issues funded developments in Illinois, Texas and Florida with additional transactions pending in California and Florida

• Delegated underwriting/streamlined processing by Fannie Mae Lender

• Structure is flexible and accommodates the following:

– Interest Only Periods of 1-2 Years

– Premium Pricing to generate additional proceeds

– Varied Prepayment Terms (e.g. 10 year par call)

31

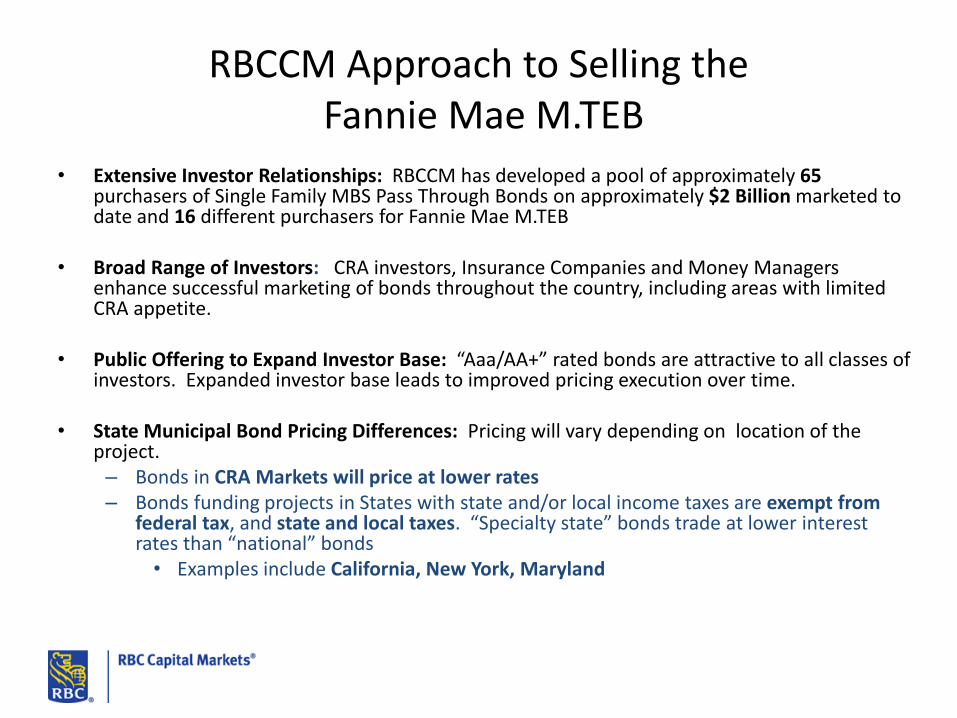

RBCCM Approach to Selling theFannie Mae M.TEB

• Extensive Investor Relationships: RBCCM has developed a pool of approximately 65 purchasers of Single Family MBS Pass Through Bonds on approximately $2 Billion marketed to date and 16 different purchasers for Fannie Mae M.TEB

• Broad Range of Investors: CRA investors, Insurance Companies and Money Managers enhance successful marketing of bonds throughout the country, including areas with limited CRA appetite.

• Public Offering to Expand Investor Base: “Aaa/AA+” rated bonds are attractive to all classes of investors. Expanded investor base leads to improved pricing execution over time.

• State Municipal Bond Pricing Differences: Pricing will vary depending on location of the project.

– Bonds in CRA Markets will price at lower rates– Bonds funding projects in States with state and/or local income taxes are exempt from

federal tax, and state and local taxes. “Specialty state” bonds trade at lower interest rates than “national” bonds

• Examples include California, New York, Maryland

Flexible Application of M.TEB Structure

• Fannie Mae – Reduced Occupancy Affordable Rehab (ROAR)

• Minimum occupancy of 50% and minimum DSC of 1.0X (interest-only)

• No Construction loan needed; rehab costs of $40,000 - 120,000 per unit and rehab period of 12-18 months

• MBS Structure modified to provide Fannie Mae direct credit enhancement during rehab phase converting to MBS at conversion

• Proceeds are fully funded at closing; amounts required for rehab are escrowed

• Increased leverage when underwritten to as-improved rents

• Interest rate savings similar to full MBS Tax Exempt Pass Through Bond execution

• Fannie Mae – New Construction

• Fannie Mae Forward Commitment – up to 36 months

• Construction loan required – Structuring as “draw down” reduces interest during construction

• Permanent bond pricing locked at issuance

• Loan proceeds secure bonds until MBS is delivered. Reinvestment in Treasuries reduces interest during construction

• Upon Conversion, MBS will be delivered to the Trustee and secure the Bonds

• All-in Rate with Bonds and Fannie Mae Guarantee & Servicing is in low 4% range

• Structure easily accommodates short term cash collateralized “50% test” bonds

Recent Developments on FHA Insured Loans andShort-Term Cash-Backed Tax-Exempt Bonds*

Paul WeissmanHunt Mortgage Group

[email protected](303) 504-6239

R. Wade Norris, Esq.Eichner Norris & Neumann PLLC

[email protected](202) 973-0100

________________________________* Copyright © by R. Wade Norris, Esq. April 10, 2017 All rights reserved. This document may not be reproduced without the prior written permission of the author.

R. Wade Norris – (202) 973-0100 Paul Weissman – (303) 504-6239

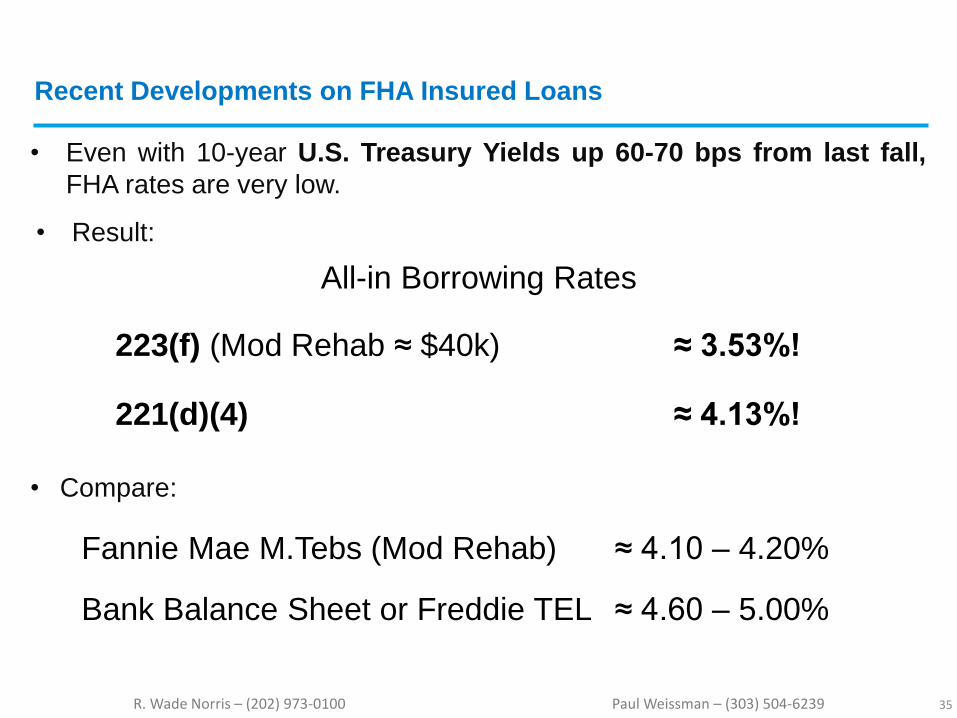

• Even with 10-year U.S. Treasury Yields up 60-70 bps from last fall,

FHA rates are very low.

• Result:

Recent Developments on FHA Insured Loans

All-in Borrowing Rates

223(f) (Mod Rehab ≈ $40k) ≈ 3.53%!

221(d)(4) ≈ 4.13%!

35

• Compare:

Fannie Mae M.Tebs (Mod Rehab) ≈ 4.10 – 4.20%

Bank Balance Sheet or Freddie TEL ≈ 4.60 – 5.00%

R. Wade Norris – (202) 973-0100 Paul Weissman – (303) 504-6239

• FHA has dramatically streamlined and improved loan

processing.

• Initial meeting with loan coordinator to screen out potential

problems.

• Four major lines of loan underwriting occur simultaneously, not

in a linear manner, under supervision of loan coordinator.

HUD now gives priority to affordable housing loans –

FHA’s affordable loan volume almost quadrupled from 2012 to 2015!

36

R. Wade Norris – (202) 973-0100 Paul Weissman – (303) 504-6239

Results: 1. Annual FHA LIHTC Production Now Tops 230 Loans

and $2.0 Billion!

Initial Endorsements FY16 (ended 09-30-16)

Section of the Act# of FHA Loans with Tax Credits

Volume of FHA Loanswith Tax Credits

New Construction / Sub Rehab Program 221(d)(4)

104 $1,133,000

223(f), 223(a)(7),and 241(a)

129 $1,043,000

Total 233 $2,176,000Source: U.S. Department of Housing and Urban Development.

37

R. Wade Norris – (202) 973-0100 Paul Weissman – (303) 504-6239

2. Greatly Accelerated Processing Times –

Forget What You Know About the Old FHA!

% of FY16 Firm Commitments within DAS Timeframes

Program TypeStandard for # of calendar

days HUD processing(net of prelim. rejects)

Percent within goal

New Construction / Sub Rehab 221(d)(4)

60 days(at each stage)

87%

Section 223(f) 45 74%Source: U.S. Department of Housing and Urban Development.

38

R. Wade Norris – (202) 973-0100 Paul Weissman – (303) 504-6239

3. Much More Predictable, Professional Underwriting Process.

Dramatically Improved “Hit Ratio”

% of applications received which are approved – based on final decisions made

Stage of Processing

% ApprovedOct 2012 – June 2013

# of DecisionsQ3-Q4 of FY16

% ApprovedQ3-Q4 of FY16

Refinancing –FIRM

75% 386 95%

NewC/Sub Rehab PREAPP

48% 115 54%

NewC/Sub Rehab FIRM

78% 100 93%

Source: U.S. Department of Housing and Urban Development.

39

R. Wade Norris – (202) 973-0100 Paul Weissman – (303) 504-6239

Remember: 50% Test: Must Use Short-Term Cash-Backed Tax-Exempt

Bonds ≥ 50% of Eligible Basis in Buildings and Land to Qualify for 4% LIHTC.

Major Advantages:

1. Qualifies the Project for 4% LIHTC.

2. Still lowers Mortgage Rate by 50 to 100 basis points.

3. Avoids huge (4-8%) negative arbitrage deposit on new

construction/sub rehab (§221(d)(4)) deals.

4. Eliminates on-going issuer/administrative fees after 1-3 years;

huge benefit where issuers charge major (25-50 basis points)

ongoing fees as long as bonds are outstanding.

Major Disadvantages:

0. None (ok, a now very small cap i deposit).

40

R. Wade Norris – (202) 973-0100 Paul Weissman – (303) 504-6239

Increased Volume of Section 221(d)(4)

New Construction/Sub Rehab Loans

• Section 221(d)(4) loans now make up a much larger percentage of

FHA loans we see – 104 or 45% of 233 FHA/LIHTC Loans on slide 5.

• Have longer expected placed-in-service dates, e.g., 1.5 – 2 years.

• Thus longer, e.g., 2 – 3 year bond maturities.

• Thus higher bond coupons, e.g., 1.20 – 1.60% (v. 0.60 – 0.80% for

§223(f)).

• Thus much greater negative arbitrage – potentially 3 – 4%

of Bonds (v. 0.50 – 1.00% for §223(f)).

41

R. Wade Norris – (202) 973-0100 Paul Weissman – (303) 504-6239

Increased Volume of Section 221(d)(4)

New Construction/Sub Rehab Loans

• Managing reinvestment becomes critically important.

• With properly structured investments, may be able to reduce negative

arbitrage by half or two-thirds or more.

BUT

• Bond Counsel firms may vary on what type of investment vehicles they

will permit and on whether they will permit long-term investments with this

structure.

• If the Borrower has a choice of Issuers and Bond Counsel, it should discuss

alternatives carefully with the bank or investment bank and/or the registered

municipal financial advisor structuring the tax-exempt debt and with the bond

purchaser’s counsel at the outset of the financing. In these cases differences

in Bond Counsel firm positions on reinvestment may critically impact the results

which can be achieved.

42

R. Wade Norris – (202) 973-0100 Paul Weissman – (303) 504-6239

Use of Cash-Backed Tax-Exempt Short-Term Bonds

with Broader Range of Taxable Loans

• Short-term cash-backed tax-exempt bonds are now being used in any scenario

where Borrower can achieve lower borrowing rates and/or lower negative

arbitrage than through a taxable loan as compared to a long-term tax-exempt

municipal debt structure.

• Also now used with:

• Fannie Mae and Freddie Mac Mod Rehab Loans;

• Rural Development Loans (financed with taxable GNMA sales);

• Seller “Take-Back” Loans;

• Other Subordinate Loans (e.g. HOME, CBDG);

• 50/50 Risk Share Mod Rehab Loans under new Federal Financing

Bank loan purchase program; and

• Other Taxable Loans.

43

Forward Refinancing forAffordable Housing Projects Approaching Year 15*

R. Wade Norris, Esq.Eichner Norris & Neumann PLLC

[email protected](202) 973-0100

________________________________* Copyright © by R. Wade Norris, Esq. April 10, 2017 All rights reserved. This document may not be reproduced without the prior written permission of the author.

Today; Year 12, 13 or 14UST ≈ 2.50%

Year 15UST ≈ 3.5% to 4.5%?

FORWARD REFINANCING FOR AFFORDABLE HOUSING PROJECTS

APPROACHING YEAR 15

R. WADE NORRIS, [email protected]

(202) 973-0100(202) 744-1888 (cell)

EICHNER NORRIS & NEUMANN PLLC

R. Wade Norris [email protected] (202) 973-0100 (o) (202) 744-1888 (c)

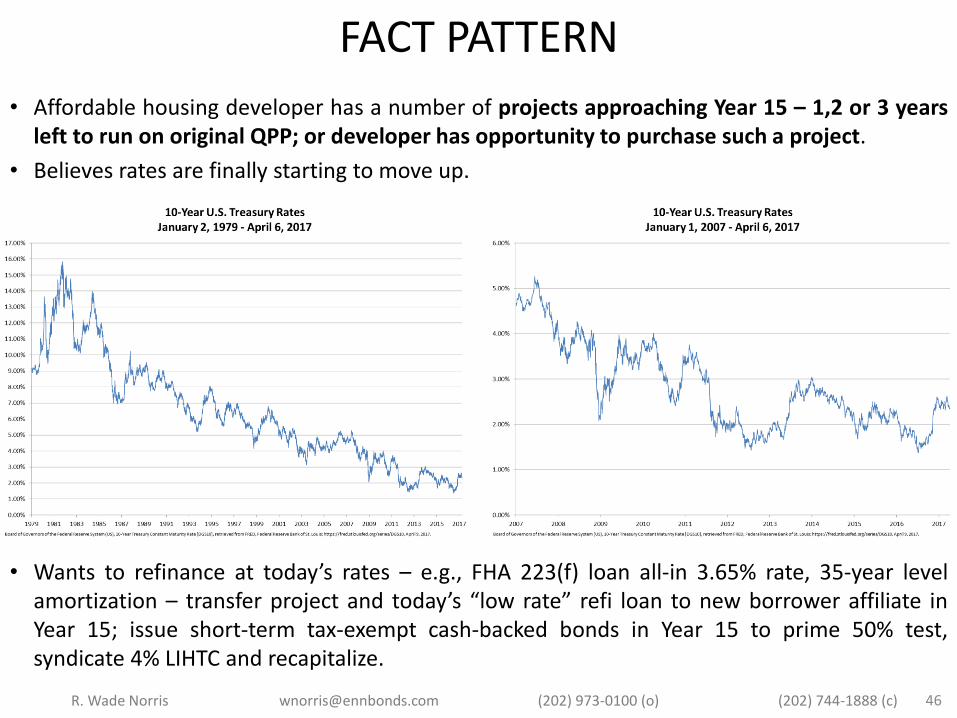

FACT PATTERN

• Affordable housing developer has a number of projects approaching Year 15 – 1,2 or 3 yearsleft to run on original QPP; or developer has opportunity to purchase such a project.

• Believes rates are finally starting to move up.

• Wants to refinance at today’s rates – e.g., FHA 223(f) loan all-in 3.65% rate, 35-year levelamortization – transfer project and today’s “low rate” refi loan to new borrower affiliate inYear 15; issue short-term tax-exempt cash-backed bonds in Year 15 to prime 50% test,syndicate 4% LIHTC and recapitalize.

46

R. Wade Norris [email protected] (202) 973-0100 (o) (202) 744-1888 (c)

DILEMMA

If too large a loan is transferred, cannot spend the amount of tax-exempt bond proceeds in Year 15

required to satisfy 50% test.

47

R. Wade Norris [email protected] (202) 973-0100 (o) (202) 744-1888 (c)

YEAR 15

48

Uses

Acquisition Cost $15.0mm

Rehabilitation & Other Costs $6.0mm

Total Development Costs (Yr. 15) $21.0mm → $11.0mm TE Bonds for 50% Test

Sources

4% LIHTC & Other Funds $8.0mm

Assumed 223(f) Refinancing Loan $13.0mm

Total Sources $21.0mm

Required Tax-Exempt Bond Proceeds Expenditure $11.0mm

Costs to be Paid from Tax-Exempt Bond Proceeds(4% LIHTC & Other Funds Flowed Through Tax-ExemptBond Indenture)

$8.0mm

Tax-Exempt Bond “Use of Proceeds Gap” $3.0mm

R. Wade Norris [email protected] (202) 973-0100 (o) (202) 744-1888 (c)

2 SOLUTIONS

1. Orrick, Herington & Sutcliffe LLP “look through” theory.

• Take appropriate steps contemplating Year 15 bonds beforetaxable refi.

• Can effectively treat part of taxable refi loan as expenditure bynew borrower of Year 15 tax-exempt bond proceeds to acquireproject in Year 15.

• Uses 18-month reallocation rules; cannot close refi more than18 months before new bonds are issued.

• Section 42 bar has yet to get comfortable with reallocationtheory on Section 42 side, but several syndicators and Section42 counsel considering.

49

R. Wade Norris [email protected] (202) 973-0100 (o) (202) 744-1888 (c)

2. Partially Prepayable Refi Loan + Supplemental Loan in Year 15.

• In above example, split 223(f) refi loan into two components: (i)$10.0mm component with standard prepayment lock out; (ii) $3.0mmcomponent prepayable at par in Year 15 (sold at discount).

• Close $3.0mm Section 241(a) supplemental FHA loan for new borrowerin Year 15. $3.0mm supplemental loan and $8.0mm of LIHTC (andperhaps other Year 15 funds) will collateralize the $11.0mm short-termcash-backed issue, freeing up $11.0mm in tax-exempt bond proceeds toacquire and rehab the project as the 50% Test requires.

• Permanent debt financing now consists of original $10.0mm standard223(f) FHA loan and new $3.0mm supplemental 241(a) loan. Tax-exempt bond “use of proceeds gap” disappears.

50

2 SOLUTIONS

R. Wade Norris [email protected] (202) 973-0100 (o) (202) 744-1888 (c)

• Disadvantages:

• Difficult to lock pricing/rate on $3.0mm section 241(a) loan in advance of Year 15.

• Must fit expenditures in Year 15 to be financed from Section 241(a) loan into permittedcategories.

• Advantages:

• Have still locked today’s low rates on 70% to 80% of the loan.

51

ADVANTAGES AND DISADVANTAGES

• Refinance can occur > 18 months before new bonds are issued.

• Tax analysis very straight forward; should not raise issues on tax-exempt debt orsyndication side.

• Substantial Interest Rate Savings

Assume 2.50% 10-Yr UST → 4.50% 10-Yr UST at Year 15 (200 basis point increase)

Annual Debt Service on $13.0mm of Debt

$13.0mm @ 5.40% ML Rate $813,138

$13.0mm @ Split ML Rate

($10.0mm @ 3.40%; $3.0mm @ 5.40%) 643,341

Annual DS Savings: $169,797 (21%)

Almost $6,000,000 debt service savings on $13,000,000 loan over 35 years!

R. Wade Norris [email protected] (202) 973-0100 (o) (202) 744-1888 (c)

RESULTS

• Available mechanism for many projects to lock in today’s rates forsubstantial part of debt needed to recapitalize project at Year 15.

• Not all projects will work; careful analysis of projected sources anduses at refi and Year 15 required.

• Same approach may be used, albeit at probably higher rates anddifferent underwriting criteria, using Fannie Mae MBS (probably ≈4.35% rate), Freddie Mac and/or bank balance sheet (probably ≈5.0%+) structures.

52

Jeree Glasser-Hedrick, Executive Director

CALIFORNIA DEBT LIMIT ALLOCATION COMMITTEE

April 2017

2017 Allocation:

◦ $3.925 Billion in new Cap (slight increase from 2016)

◦ $1.06 Billion in old (Carryforward) Cap

Prior to 2015 CDLAC’s resources were underutilized

2016 deployed $4.8 Billion in QRRP (Plus another $1.8 Billion of other programs in 2016) for a total of $6.6 Billion

54

• National 2015 PAB Usage• $90 Billion Available ($34.9 Billion in 2015 Cap)

$19.9 Billion Issued (MCC’s included)

• California 2015 PAB Usage• $11.9 Billion Available ($3.9 Billion in 2015 Cap)

$4.6 Billion Issued (MCC’s included)

55

• 2015 National Utilization Rate (minus CA): 19.5%

• 2015 California Utilization Rate: 38.9%

56

57

58

67

93

39

22

54 54 5870

99

117

114

149

72

57

135

101

83

107

138

181

0

20

40

60

80

100

120

140

160

180

200

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

QRRP Awards

Acq/Rehab Total

59

Trends

$1,57B

$1,71B

$992M

$935M

$1,82B

$1,56B

$1,15B

$1,53B

$2,86B

4,86B

$663M

$1,55B

$785M

$432M $453M $517M $483M$225M

$1,71B

1,33B

$3,12B

$4,03B

$1,96B

$1,70B

$2,42B

$2,80B

$1,91B

$1,93B

$4,65B

6,62B

$3,10B $3,11B$3,31B $3,33B

$3,54B $3,58B $3,61B$3,83B $3,88B 3,91B

$0

$1,000,000,000

$2,000,000,000

$3,000,000,000

$4,000,000,000

$5,000,000,000

$6,000,000,000

$7,000,000,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

All Allocation Dollars by Program w/cap

QRRP SFH Total Allocation Bond Cap

60

$1.75 B

$1.42 B

$1.28

$1.11

1

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2013 2014 2015 2016

Billion o

f A

llocati

on

Year

Amount of Private Activity Bond Allocation

Abandoned 2013-2016

61

$221,340

$250,419

$249,314

$285,458

$254,072

$249,198

$242,664

$279,902

$324,741

$367,351

$200,000

$220,000

$240,000

$260,000

$280,000

$300,000

$320,000

$340,000

$360,000

$380,000

$400,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Average Cost per Unit

62

4,344

5,247

2,884

3,831

6,175

5,440

2,075

3,041

3,908

6,721

7,735

8,905

3,264

1,987

5,988

3,080

5,900

6,722

10,140

14,029

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

QRRP New Construction vs. Acq/Rehab

New Constr. Units Acq. & Rehab Units

2015 2016

Bond Structure Number of Projects

Private Placements

140

Public Sales (w/Private CreditEnhancement)

1

GSE (Freddie/Fannie)

2

FHA (Public -Cash Collateralized)

4

TOTAL QRRP 147

Bond Structure Number of Projects

Private Placements

141

Public Sales (w/Private CreditEnhancement)

2

GSE (Freddie/Fannie)

32 (13 SF RAD)

FHA (Public -Cash Collateralized)

6

TOTAL QRRP 181

64

Disruptions caused uncertainty

◦ Precipitous drop in tax credit pricing

◦ Rates on tax exempt and taxable financing have increased

◦ The changes have impacted both 9% and 4% projects

Delegated authority to waiver performance deposit forfeitures for projects requesting extension until March 31st

A request for additional delegated authority will be heard by the at the March 15th Committee Meeting

◦ Performance deposits

◦ Assessment of negative points

67

OpportunitiesBond Recycling

CDLAC is investigating the potential to recycle bond

What is recycling?

How does it?

How can it be helpful?

Working with TCAC to streamline the application process

Looking forward to establishing a recycling program

Preparing for utilization

68

CDLAC Contact Information

Jeree Glasser-HedrickExecutive Director

California Debt Limit Allocation Committee915 Capitol Mall, Room 311

Sacramento, CA 95814(916) 653-3255

[email protected]/cdlac