South East England Councils: Fair Funding for the … · County Leaders Group (SECL), working with...

53

Jude Ranasinghe Director of Consultancy and Training [email protected] 01908 424 387 FINANCE WITH VISION LG Futures, Technology House, 151 Silbury Boulevard, Milton Keynes MK9 1LH | www.lgfutures.co.uk | T. 01908 424387 Local Government Futures Ltd. Incorporated in England and Wales under registration number: 05308266 | VAT registration number: 855940493 South East England Councils: Fair Funding for the South East Stage 2 Research Report November 2011

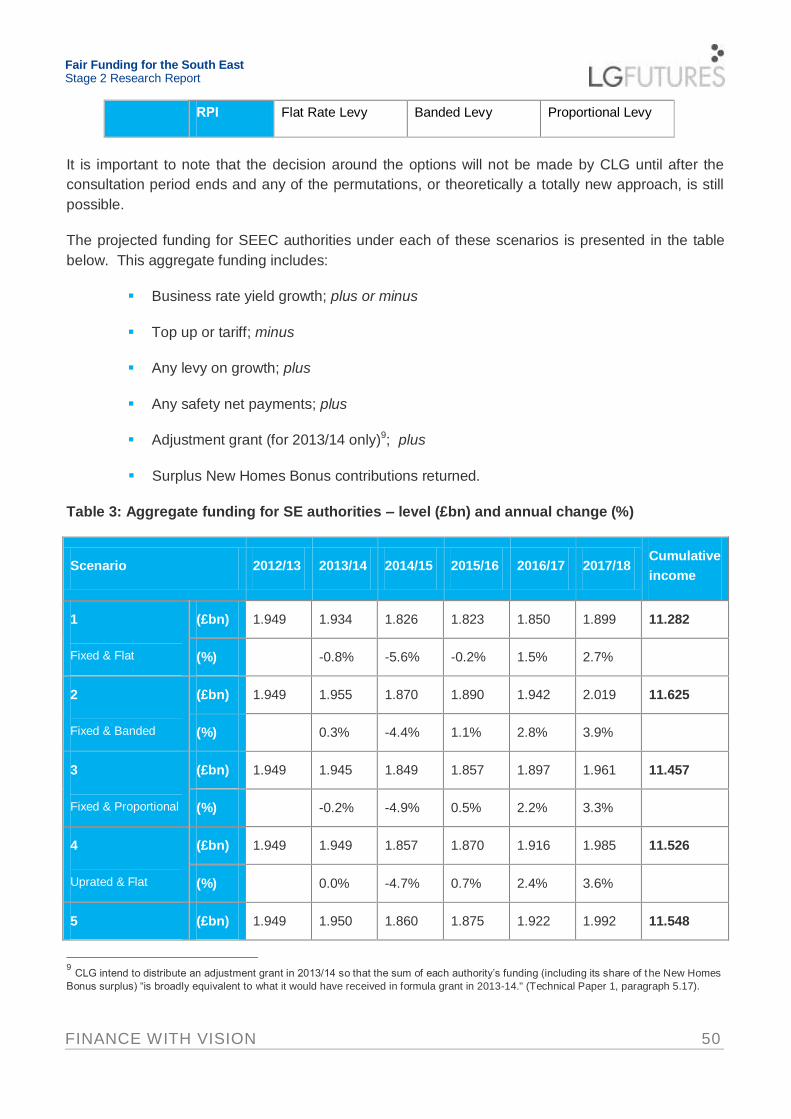

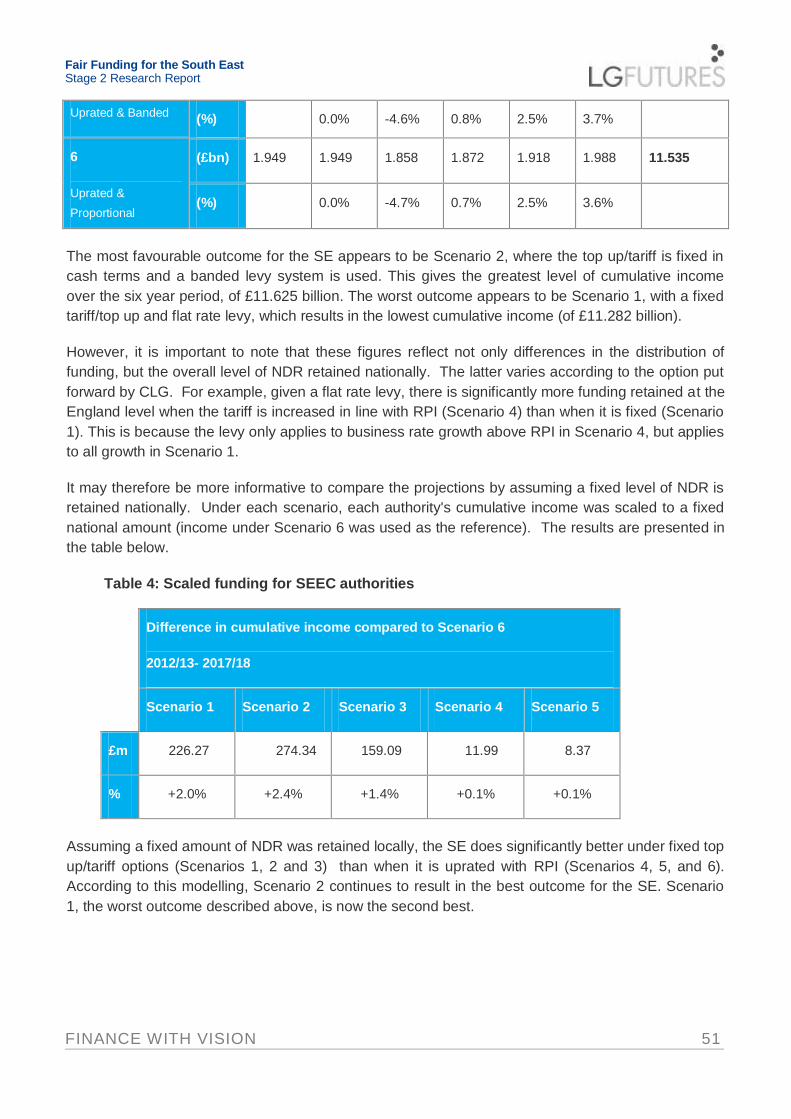

Transcript of South East England Councils: Fair Funding for the … · County Leaders Group (SECL), working with...

Jude Ranasinghe

Director of Consultancy and Training

01908 424 387

FINANCE WITH VISION

LG Futures, Technology House, 151 Silbury Boulevard, Milton Keynes MK9 1LH | www.lgfutures.co.uk | T. 01908 424387

Local Government Futures Ltd. Incorporated in England and Wales under registration number: 05308266 | VAT registration number: 855940493

South East England Councils:

Fair Funding for the South East

Stage 2 Research Report

November 2011

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 2

Contents

1. Introduction ....................................................................................... 3

2. Implications of Changes to the Current Funding Formulae ................. 6

3. Business Rates Retention ............................................................... 25

4. Incentive Measures ......................................................................... 31

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 3

1. Introduction

1.1 South East England Councils (SEEC) was established in April 2009 to promote the views and

interests of local government in the region, with a large majority of the 74 unitary, county, district

and borough councils across the South East being members of SEEC. Much of SEEC's work

involves making the case for the high level strategic and funding priorities for the South East.

1.2 LG Futures was commissioned by SEEC in March 2011 to undertake research into the specific

public sector funding issues and cost pressures for the South East, with a particular focus upon

local government. The research took place in the context of the Department for Communities

and Local Government's (DCLG's) Local Government Resource Review, which also

commenced in March 2011.

1.3 The report updates previous research carried out by LG Futures in 2007 for the South East

County Leaders Group (SECL), working with Oxford Economics. This 2007 report, “Taken for

Granted: Why Britain needs a Fair Deal for the South East”, considered public sector funding

issues affecting county councils in the South East and parts of the East of England1.

1.4 Stage 1 of LG Futures' research was presented to SEEC Executive Members on 7 June 2011.

This research focused upon the background to the current local government funding system,

funding levels for the South East and key cost pressures for the region. The main summary

findings of the Stage 1 research included:

The SE region received the lowest Formula Grant per head from 2009/10 to 2011/12

and is expected to continue to do so for the provisional 2012/13 allocation. Average

Formula Grant for 2011/12 for the SE region was £374 per head, with the average for

England being £560 per head and the average for London (the highest funded region)

being £834 per head.

The SE has experienced the second highest Council Tax increase over the last 15

years; at 129% (the highest was the East of England at 132% and the lowest was the

North West at 84%).

Of the 10 Strategic Health Authorities (SHAs) nationally, the South Central SHA is the

lowest funded at £1,401 per head, which is 13% below the England average. The South

East Coast SHA, at £1,551 per head, is funded 4% below the England average and is

the 5th lowest funded overall. Taken together, the South East Coast and South Central

SHA's have 58% of their Primary Care Trusts (PCTs) funded in the lower quartile, which

is the largest proportion nationally.

At £257 per head, the SE had the lowest level of capital funding in 2009/10. This

compared with the England average of £412 per head (excluding the Greater London

Authority). The SE has also consistently had the lowest level of capital funding per head

of population of all regions over the period 2005/06 to 2009/10.

1 http://www3.hants.gov.uk/finance_report.pdf

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 4

The SE has seen the largest increase in relative deprivation between the Indices of

Deprivation 2007 and Indices of Deprivation 2010, with an increase of 6.8%. The second

highest increase was for the East of England, at 2.6%. The SE has also had more

people move into the 20% most deprived areas in England of any region between 2007

and 2010, with an additional 88,500 people in the SE moving into the two most deprived

deciles, compared to a reduction of 151,000 people for the London region.

Over the period 2005/06 to 2009/10, spending on older people's (65+) social care has

increased by 16% in the SE, the largest of any region in England (the England average

was 10%). This can be compared with a population increase of only 8% during the same

period, with spending therefore increasing at twice the rate of the change in population.

Combining population and expenditure projections, spending on older people's social

care is projected to rise faster in the SE than any other region, representing an increase

in spend of 70%, from £1.2bn in 2009/10 to £2.0bn in 2020/21. The equivalent England

increase in spending is 54%, and the next highest regional increase is 56%.

The SE has higher unit costs for a range of social care services. In 2009/10, unit costs in

the SE were: 12% above the national average for nursing and residential care; 7%

above the national average for home care; 12% above the national average for

residential care; and 5% above the national average for foster care. This compares with

the SE region's 4.4% uplift from the Area Cost Adjustment in its needs assessment.

1.5 Given the above context, the intention of the Stage 2 research was to consider the impact of

potential changes to the funding system. The research explored three key themes:

1. Implications of making changes to the current funding formulae. This included

analysing the financial impact of:

i. Potentially making the existing funding system more transparent

ii. Changing specific components/indicators currently used within the

funding system

iii. The operation of a simpler funding formula

2. Business Rates Retention Proposals. The government published its consultation

paper outlining the principle features of a proposed business rates retention scheme, in

July 2011, and eight further technical papers to supplement the initial consultation

paper, in August 2011. Analysis was undertaken to consider:

i. The current net contribution that the SE makes to the national business

rates “pool”

ii. The potential size of the “incentive” available under the proposals

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 5

iii. The potential impact of various consultation options put forward about the

operation of the scheme

iv. The potential impact of the scheme compared to Formula Grant

3. The operation of other incentive schemes. In addition to the business rates retention

proposals, there are a range of other “incentive” schemes in operation and the key

features of these schemes and specific issues for the SE region have been considered.

The schemes considered were:

i. New Homes Bonus

ii. Community Infrastructure Levy

iii. Business Improvement Districts

iv. Tax Increment Financing

v. Business Rate Supplement

vi. Business Increase Bonus Scheme

vii. Renewable Energy Projects

viii. National Insurance Contribution Reductions

ix. Enterprise Zones

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 6

2. Implications of Changes to the Current Funding Formulae

Introduction

2.1 This section considers the existing local government funding system (the “four block” model)

and considers changes that could be made to the system, including the potential funding

implications. The changes considered relate to:

i. Potentially making the existing funding system more transparent

ii. Changing specific components/indicators currently used within the funding system

iii. The operation of a simpler funding formula

2.2 The local government funding formulae receive considerable attention and are the subject of

significant debate, both within local government and between local and central government. As

context, it is worth considering some of the key reasons that result in this focus.

2.3 The CLG's July 2011 consultation, “Local Government Resource Review: Proposals for

Business Rates Retention”, identified that, “Britain's local government finance system is one of

the most centralised in the world. The Organisation for Economic Co-operation and

Development (OECD) has calculated that local authorities in the USA, Spain, France, Germany,

Spain and Japan all have greater autonomy over budgets than do their counterparts here.”

2.4 As an illustration, in 2010/11, 74% of total local government revenue spending in England was

derived from central government grants, with only 26% being locally “controlled” (from Council

Tax and sales, fees and charges), although there are restrictions on the extent to which income

can be raised from these sources.

2.5 Clearly, other countries have different contexts; for example, responsibility for different

functions, but local government in England is only able to “control” property taxes i.e. Council

Tax, given that business rates, although currently collected locally, are paid into the national

pool and then distributed as government grant. In addition, even with CLG's business rates

retention proposals, local government will not have control over the multiplier (the rate of tax),

which will continue to be set nationally.

2.6 Given this context, the funding received through Formula Grant (£29.4bn in 2011/12) is highly

important to local government and the mechanism by which this funding is distributed is key.

Alternative means of distributing this funding have therefore been considered as part of this

section. It should be noted that local government funding is often described as a zero-sum

game, in that there is only a fixed quantum of funding available, and distributional changes for

any individual authority or group of authorities results in changes in funding for all other

authorities.

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 7

2.7 Analysis has therefore been presented to show the scale of change that could result from

alternative means of distribution. It should be noted that this does not necessarily suggest that

such means of distribution are “correct” or more appropriate than the current basis, but instead

are intended to show the extent to which specific changes to individual factors within the system

influence distribution patterns between authorities.

2.8 It should also be noted that damping (as considered further below) can ‘distort’ the change that

would otherwise have occurred from making changes to the funding formulae, as this provides

an additional overlay within the system, in terms of the level of protection applied to authorities.

Current operation of the four block model

2.9 The current local government funding system is based upon the “four block” model, which was

introduced in 2006/07. Authorities are allocated Formula Grant (£29.4bn nationally for

2011/12), which can be used for any revenue purpose, using the following approach:

Relative Needs Block

Less: Relative Resources Amount

Plus: Central Allocation

Plus: Floor Damping Block

Equals: Formula Grant

2.10 In summary, the four blocks are intended to operate as follows:

Relative Needs Block – reflects spending requirements, based on local circumstances,

assessed through Relative Needs Formulae (RNF) and taking account of

population/client numbers and a range of socio-economic and geographical factors

RNF are derived for seven major blocks: Children’s Services; Adults’ Personal Social

Services; Highway Maintenance; Environmental, Protective and Cultural Services;

Police; Fire & Rescue and Capital Financing

Relative Resource Amount – takes account of authorities' relative abilities to raise

local funding through Council Tax

Central Allocation – distributes funding based upon a per capita basis

Damping – provides “protection” through a grant floor

2.11 The system is complex, but the basic principle underpinning the formula is to allocate each

authority the same “basic amount” and then add “top-ups” for deprivation, population density

and sparsity and other factors. Further adjustments are added to reflect the different levels of

input costs (the Area Cost Adjustment) and, to ensure overall affordability, the calculations are

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 8

scaled to the government’s “control totals” for each of the service blocks. It should be noted that

one feature of the four block model is that it is not possible to break down the grant that an

individual authority receives into separate amounts for the individual services within the RNF.

(i) Potentially making the existing funding system more transparent

2.12 Within the funding system, a series of “thresholds” are determined by the lowest need and

lowest resources authorities. The SE is home to the perceived lowest need authorities for

upper, lower and mixed tier services in 2011/12 (Wokingham for upper tier, Hart for lower tier

and Kent for mixed tier).

2.13 Authorities' needs are assessed relative to those of the threshold. Each authority's relative

needs per head (RNF per capita) are compared to that of the threshold authority. As illustrated

in the simplified diagram below, all authorities will have a proportion of their needs above the

threshold and the remaining proportion below (the exception is the threshold authority itself,

which by definition has 100% of its needs below the threshold).

Figure 2.1: Illustration of relative needs compared to the threshold

2.14 Local authorities might reasonably expect that assessed needs below the threshold are funded

at the same rate as those above (as was the case before the introduction of the four block

model). A key feature of the four block model, however, is that relative needs (RNF) below the

threshold are converted into funding at a different rate than needs above the threshold.

2.15 This means that lower need authorities are penalised in comparison with higher need

authorities, as a larger share of their total needs is below the threshold and converted into

Relative Needs

Formula (RNF) per

head

Authority

1

Authority

2

Authority

3

Authority

4

Share of needs

above the threshold

Share of needs

below the threshold

Threshold authority

Threshold

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 9

funding at this lower rate. Councils in the SE are assessed as having the lowest funding needs

in England. On average, they therefore receive less funding for each assessed unit of need.

2.16 For upper tier services (children's services, adult social care, highways and county-level EPCS),

councils in the SE receive 4.7% less funding per unit of RNF compared to the national average.

London, on the other hand, receives 3.9% more. This is illustrated in Chart 2.1 below.

Chart 2.1: Funding per unit of need (upper tier RNF), regional summary

2.17 At an individual local authority level, Wokingham receives 18% less funding for each unit of

RNF than the national average. This is solely due to the different amounts for funding below the

threshold and above the threshold, rather than differences in need as measured by deprivation

and other such factors, and is illustrated in Chart 2.2 below for SE upper tier authorities.

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 10

Chart 2.2: Funding per unit of need (upper tier RNF), SE authorities

2.18 For district services, the difference is less pronounced than for upper tier services, but councils

in the SE still receive 1.0% less funding per unit of RNF compared to the national average. This

is illustrated in Chart 2.3 below.

Chart 2.3: Funding per unit of need (lower tier RNF), regional summary

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 11

2.19 In summary, this means that relative levels of overall need (as assessed by RNF) do not

translate into relative levels of funding. If funding for upper tier services was allocated as a

proportion of total need, the South East would have received £169m more in undamped grant in

2011/12, if an equal amount of funding was assigned to each unit of "need", whether it was

above or below the floor (assuming the total envelope of funding was held constant). London,

at the other extreme, would have received £182m less funding. This is illustrated in Chart 2.4.

Chart 2.4: Change in funding for upper tier services if based on need shares

2.20 This issue could, however, be addressed in the current system, if relative funding were to reflect

relative need. This could be achieved by changing the parameters of the four block model, so

that there is equal funding per unit of RNF both above and below the threshold. This could be

achieved by changing the relative size of the Needs, Central and Resource blocks.

(ii) Impact of changing specific components/indicators in the Relative Needs Formulae

2.21 The degree of complexity inherent in the RNF means that there are a vast amount of changes

that could potentially be modelled. To assess the implications for Formula Grant allocations

resulting from changes to the funding formulae, modelling was undertaken through changing

the “weightings'” assigned to four specific indicators used within the funding system. The

changes were modelled on the 2011/12 formula, using the DCLG's own model. The changes

modelled were:

a. Increase the basic allowance for each service by 25%

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 12

b. Reduce the amount allocated for deprivation by 25%

c. Reduce the amount allocated for density by 50%

d. Increase the amount allocated for sparsity by 50%

2.22 As identified previously, these scenarios were chosen to illustrate the order of magnitude of

changes between regions, rather than there being any specific statistical basis for the changes.

As highlighted above, the Formula Grant model includes a damping block to limit the financial

impact of any changes. In order that authorities are protected from detrimental grant changes,

the government sets a guaranteed minimum change in grant, compared to the previous year,

on a like-for-like basis. This is known as the grant “floor”, and is calculated separately for

different groups of authorities, depending on the services they provide.

2.20 As the total amount level of Formula Grant is fixed, the amount paid in floor damping is paid for

by scaling back the grant paid to other authorities who are above the floor. This can have a

perverse effect on the outcome of the modelling, in that authorities that may gain from a change

before damping may lose after damping has taken effect and vice versa.

2.21 As identified further below, the use of these alternative scenarios also illustrate volatility, as

changing a single component can make significant differences to distribution, but with damping

subsequently acting upon such changes, which can reduce the impact of changes in “need”

which result through operation of the formulae itself.

2.22 The use of thresholds, based on the minimum RNF per head for an authority, has already been

described above. For example, Wokingham receives the lowest RNF per head for all the unitary

authorities and the RNFs per head for every other unitary authority are therefore relative to that

of Wokingham’s. Therefore, if there are major changes to the formula and the threshold

authority’s RNF per head changes, the relative difference between the threshold authority and

other authorities also changes. This can have considerable implications for the modelling and

can result in some significant and counterintuitive outcomes.

a. Increasing the basic amount by 25%

2.23 Increasing the amount allocated through the basic allowance reduces the amounts allocated

through deprivation or other top up factors. By implication, therefore, it would be expected that

more resources would be allocated to perceived lower need authorities, to the detriment of

those with higher needs.

2.24 Each service has a basic amount, which is multiplied by the relevant client group as the first

building block in the RNF. For example, the basic formula for Older People’s Personal Social

Services (PSS) is:

Older People’s Basic Amount per person aged 65+ + Age related top up + Deprivation top up

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 13

2.25 The Area Cost Adjustment and scaling factors are applied after this calculation. The effect of

increasing all basic allowances in the funding formula by 25% were modelled. Table 2.1 shows

the effect of this change on SE authorities, in terms of losses, gains and no difference in

funding; both before and after damping. The effect upon individual regions, both before and

after damping, is shown in Chart 2.5.

Table 2.1: Impact on Formula Grant for SE authorities of increasing the basic allowance

by 25%

Chart 2.5: Impact on Formula Grant by region of increasing the basic allowance by 25%

2.26 The analysis identifies that an increase in the basic allowance by 25% disadvantages SE

authority districts, as this would allocate greater funding to larger, upper tier authorities. In the

SE, the major gainers from increasing the basic allowance are Wokingham, Buckinghamshire

and Surrey i.e. the perceived lowest needs authorities.

2.27 In regional terms, although the SE as a whole benefits from the change before damping (by

+£22.7m), it can be seen that, after damping, the SE loses (by -£30.3m). The key reason for

Impact of Change

Total Effect on South

East £m / %22.7 0.7% -30.3 -0.9%

South East councils

Counties /

Unitaries Districts

Counties /

Unitaries Districts

Losers 3 55 0 50

Gainers 16 0 9 5

Neutral 0 0 10 0

Before Damping After Damping

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

SE EE EM ILB OLB NE NW SW WM YH

Percentage Changes in Formula Grant

Pre-Damping Change (%) Post-Damping Change (%)

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 14

this is because of shifting thresholds in the damping block, whereby an increase in the damping

threshold tends to benefit higher needs authorities.

b. Reducing deprivation by 50%

2.28 There is a deprivation top up factor in each of the service blocks, with the exception of

Highways Maintenance and Capital Financing. The individual factors vary between service

blocks. For example, the factors included in the Older People’s PSS block are the proportions of

people aged over 65 who are:

In receipt of Income Support or Pension Credit

In receipt of Attendance Allowance

Living in rented accommodation

Living alone in a household

2.29 The sources of data for the deprivation top ups vary, but include Census data, which implies

that the data is “locked-in” for up to 10 years until the next Census. Table 2.2 shows the

outcome of the modelling for SE authorities. The effect upon individual regions, both before

and after damping, is shown in Chart 2.6.

Table 2.2: Impact on Formula Grant for SE authorities of reducing the deprivation

weighting by 50%

Chart 2.6: Impact on Formula Grant by region of reducing the deprivation weighting by

50%

Impact of Change

Total Effect on South

East £m / %126.7 4.1% -30.6 -1.0%

South East councils

Counties /

Unitaries Districts

Counties /

Unitaries Districts

Losers 3 30 1 37

Gainers 16 25 11 18

Neutral 0 0 7 0

Before Damping After Damping

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

SE EE EM ILB OLB NE NW SW WM YH

Percentage Changes in Formula Grant

Pre-Damping Change (%) Post-Damping Change (%)

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 15

2.30 Again, the SE gains overall before damping (by +£126.7m), but loses after damping (the loss

being -£30.6m). One of the reasons for this change is that the damping model shifts resources

away from previous gainers from damping, many of whom were in the SE, to the “new” losers

from the change to the deprivation weighting.

2.31 One surprising outcome from the modelling was that Inner London, which attracts a significant

deprivation allocation, is a gainer both before and after damping under this change (although

the change after damping is lower than that before damping). This arises as a result of the

changes in thresholds that occur and highlights the inherent instability of the formula.

c. Reducing density by 50%

2.32 Density is used in the formula in the Environmental, Protective and Cultural Services (EPCS)

block of the RNF. By definition, it favours urban authorities with a high population density. Table

2.3 shows the outcome of reducing the amount included in the formula for density by 50%. The

effect upon individual regions, both before and after damping, is shown in Chart 2.7.

Table 2.3: Impact on Formula Grant for SE authorities of reducing the density weighting

by 50%

Chart 2.7: Impact on Formula Grant by region of reducing the density weighting by 50%

Impact of Change

Total Effect on South

East £m / %10.1 0.3% 1.5 0.0%

South East councils

Counties /

Unitaries Districts

Counties /

Unitaries Districts

Losers 7 20 5 0

Gainers 12 35 3 55

Neutral 0 0 11 0

Before Damping After Damping

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

SE EE EM ILB OLB NE NW SW WM YH

Percentage Changes in Formula Grant

Pre-Damping Change (%) Post-Damping Change (%)

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 16

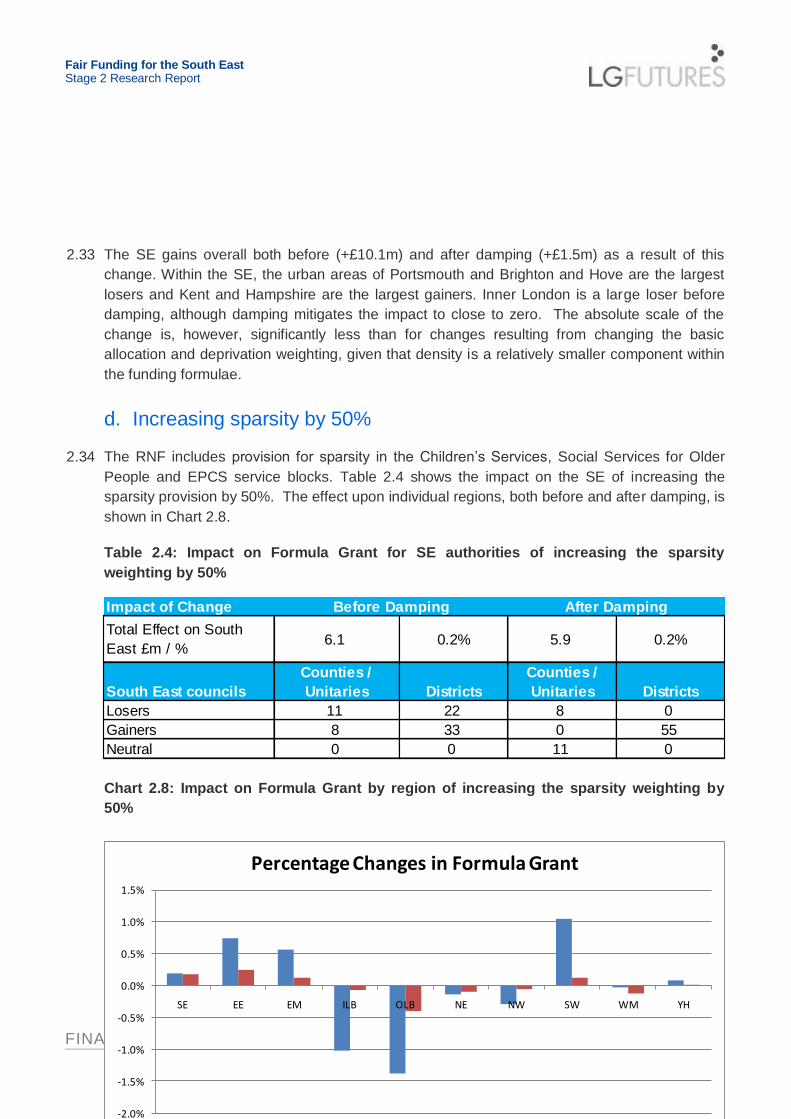

2.33 The SE gains overall both before (+£10.1m) and after damping (+£1.5m) as a result of this

change. Within the SE, the urban areas of Portsmouth and Brighton and Hove are the largest

losers and Kent and Hampshire are the largest gainers. Inner London is a large loser before

damping, although damping mitigates the impact to close to zero. The absolute scale of the

change is, however, significantly less than for changes resulting from changing the basic

allocation and deprivation weighting, given that density is a relatively smaller component within

the funding formulae.

d. Increasing sparsity by 50%

2.34 The RNF includes provision for sparsity in the Children’s Services, Social Services for Older

People and EPCS service blocks. Table 2.4 shows the impact on the SE of increasing the

sparsity provision by 50%. The effect upon individual regions, both before and after damping, is

shown in Chart 2.8.

Table 2.4: Impact on Formula Grant for SE authorities of increasing the sparsity

weighting by 50%

Chart 2.8: Impact on Formula Grant by region of increasing the sparsity weighting by

50%

Impact of Change

Total Effect on South

East £m / %6.1 0.2% 5.9 0.2%

South East councils

Counties /

Unitaries Districts

Counties /

Unitaries Districts

Losers 11 22 8 0

Gainers 8 33 0 55

Neutral 0 0 11 0

Before Damping After Damping

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

SE EE EM ILB OLB NE NW SW WM YH

Percentage Changes in Formula Grant

Pre-Damping Change (%) Post-Damping Change (%)

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 17

2.35 Increasing the provision for sparsity has a similar outcome to reducing the provision for density;

which is not unexpected, given the types of authorities most affected. As a region, the South

East gains both before (by +£6.1m) and after damping (by +£5.9m). London is a significant

loser from the change, although again this is mitigated by the damping formula. The largest

gainer is the South West, which contains counties such as Devon and Cornwall, although again,

these gains are considerably reduced by damping.

Changing RNF components – key issues

2.36 We have modelled, at a high level, the outcome of changing four individual areas within the

funding formula. Key points arising from this modelling include:

The RNF is a volatile funding formula and changes can result in unexpected outcomes.

This is predominantly because of the use of thresholds; which, coupled with fixed

national control totals, can result in counterintuitive redistribution patterns at a regional

level. For example, Inner London gains from a reduction in deprivation, despite having

some of the most deprived authorities in the country.

The damping arrangements can result in perverse outcomes. For example, the SE gains

from a reduced deprivation weighting before damping, but loses after damping, because

resources are switched to protect the "new" losers arising from the change.

Given that the SE is comprised of authorities with varying demographic and

geographical features, it is highly unlikely that there will be a change to the RNF that

would favour every authority in the region.

There are a large number of changes to the funding formula that could be modelled,

many of which involve the use of judgment and which are therefore not evidence-based.

Although there is clearly potential for ministerial judgment within the funding formulae,

the use of current indicators within the formulae have been statistically tested, and the

options selected for this modelling exercise have been chosen purely for illustrative

purposes, to identify the potential scale of the change.

(iii) Developing a simpler funding formula

2.37 As identified previously, the current funding formulae are complex in nature and contain a large

number of indicators. Modelling therefore took place to identify the effect of a “simple formula”,

with this being developed for two different elements of current funding for local government -

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 18

social services for older people (an upper tier service) and lower tier Environmental, Protective

and Cultural Services (EPCS). For each of these areas, three separate models were developed,

with each model attributing funding to local authorities based upon:

Model 1: Population only. For this model, funding was simply distributed based on population

only, using the total funding currently allocated to the service area divided by the relevant

population for each service block to give a “per capita” allocation. This was multiplied by the

service block population for each local authority to calculate its allocation.

Model 2: Population and Deprivation. For this model, the approach started with calculating a

standardised IMD score for each local authority. This standardised IMD score was then used to

calculate a weighted service block population for each local authority. The weighted population

was calculated as follows:

Local authority population + (10% of local authority population * IMD standardised score)

Therefore, for local authorities with standardised IMD scores less than 0 (i.e. lower levels of

deprivation), the weighted population would be less than the actual population to represent

lower levels of need. For local authorities with standardised IMD scores greater than 0 (i.e.

higher levels of deprivation), the weighted population would be higher than the actual

population to represent higher levels of need.

A new “per head” allocation was then calculated and this was multiplied by the IMD-weighted

service block population for each local authority to calculate its allocation.

The overall impact of this approach was to increase allocations to local authorities with higher

levels of deprivation. An assumption of 10% was used in this model to approximate the

weighting currently applied to need factors in the RNF. Changing the assumption would have

the following impact:

Using a value of more than 10% would transfer more funding to authorities with higher levels of deprivation, moving funding away from authorities with lower levels of deprivation; and

Using a value of less than 10% would transfer less funding to authorities with higher levels of deprivation, moving funding back to authorities with lower levels of deprivation.

Model 3: Population, Deprivation and Area Costs. For this model, the modelling followed a

similar approach to that outlined above. The IMD weighted population was calculated as

above and the IMD weighted population was then multiplied by the ACA value for each local

authority (ranging from 1.000 to 1.198) to give a new weighted population.

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 19

A new “per head” allocation was then calculated and this was multiplied by the ACA-and-IMD-

weighted service block population for each local authority to calculate its allocation. The

overall impact of this approach was to increase allocations to local authorities with higher

levels of ACA when compared with the model based on IMD only.

2.37 Variations in deprivation were measured using the Index of Multiple Deprivation (IMD) as a

proxy indicator. Variations in area costs were measured using the Area Cost Adjustment (ACA).

Two main data sources were used to undertake the modelling:

The 2010 Index of Multiple Deprivation (IMD) ; and

The 2011/12 local government settlement data.

2.38 The IMD is a composite indicator, drawing together a range of economic, social and housing

issues. It was used in this analysis as a proxy for need i.e. to identify authorities with higher

levels of need associated with deprivation, which should impact on the amount of funding that

they would receive through the simple models. The IMD provides a single deprivation “score”

for each small area in England and the small area scores are also uplifted to scores for upper

and lower tier authorities.

2.39 For the modelling relating to Older People’s Social Care, the overall scores (and relative

ranking) for upper tier authorities were obtained. For the modelling relating to lower tier EPCS,

the overall scores (and relative ranking) relating to lower tier authorities were obtained.

2.40 Using this data, IMD scores were standardized relative to zero to provide a measure of relative

deprivation compared to other authorities i.e. authorities with a standardized score of less than

zero were the least deprived and authorities with a standardized score of greater than zero

were the most deprived.

2.41 The standardized IMD scores for the upper tier authorities ranged from 2.36 (for the highest

level of deprivation) to -2.07 (for the lowest level of deprivation). This approach provided a

simple method for identifying relative deprivation2.

2.42 The 2011/12 Local Government Settlement Data was obtained from the DCLG. From the

settlement data spreadsheets, data was obtained on:

The quantum of funding allocated through the relative needs formulae (RNF);

The proportion of funding allocated through each RNF;

The proportion of funding allocated to each authority for each RNF;

The relevant service block population data used in each of the funding elements being

investigated (i.e. older people and lower tier population statistics); and

2 The individual IMD scores provide a relative measure of deprivation but need to be interpreted with care i.e. if an authority has a score

which is twice the value of the score for its neighbour, this should not be interpreted as it having twice the level of deprivation. This is why the approach has been used to create standardised scores.

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 20

The ACA data for each funding stream was used as the measure for variable input costs

to take account of differences in labour costs and business rates.

Modelling approach – changes in funding share

2.43 The RNF data does not explicitly identify how much funding each local authority receives for

each of the funding blocks and the current four block model, on which the Relative Needs

Formula is based, does not allow a simple calculation of the breakdown of an authority’s

Formula Grant into cash amounts for each service block.

2.44 However, we have used the overall funding quantum of £29bn for 2011/12 as a basis for

estimating the “funding share” for each local authority i.e. the proportion of the total funding that

is allocated to each authority in each of the funding blocks. This “funding share” for each

authority was then compared with the funding allocated under the simple models developed as

per the methodology outlined below. This is shown for both services considered in Chart 2.9

and 2.10 below.

Chart 2.9: Social services for older people – changes in funding share for the three

“simpler” formulae

Chart 2.10: Lower tier Environmental, Protective and Cultural Services (EPCS) – changes in

funding share for the three “simpler” formulae

0%

20%

40%

60%

80%

100%

120%

East

Midlands

East of

England

Inner

London

North East North West Outer

London

South East South West West

Midlands

Yorkshire

and the

Humber

Population Only

Population + Deprivation

Population + Deprivation + ACA

No Change

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 21

2.45 The key points to note are that:

The SE region as a whole benefits most from the simplest model i.e. population only,

with there being an average increase across the region’s authorities in funding share

compared to the current funding formulae of 10% for older people’s social services and

13% for lower tier EPCS.

The two other models (population + deprivation and population + deprivation + ACA),

also benefit the South East region as a whole compared to the current funding formulae,

although this is less pronounced than for the simplest population only model. Of these

two models, population + deprivation + ACA provides a more favourable result than

population + deprivation alone, for the SE region, given the high input costs faced by the

SE.For older people’s social services, the main regions that would lose from a simpler

formulae would be Inner and Outer London; particularly Inner London, which would see

the average funding share for its authorities reduce to 58% of the current share for a

population only model, 65% for population + deprivation and 74% for population +

deprivation + ACA.

For older people’s social services, the North West, North East and West Midlands

regions would also lose out for the simplest population only model (with average funding

shares reducing to 93%, 94% and 98% respectively), although the inclusion of the IMD

then brings these regions close to their existing funding shares.

For lower tier EPCS, the main regions that would lose from a simpler formulae would

again be Inner and Outer London; particularly Inner London, which would see its funding

share reduce to 55% of the current share for a population only model, 62% for

0%

20%

40%

60%

80%

100%

120%

140%

East

Midlands

East of

England

Inner

London

North East North West Outer

London

South East South West West

Midlands

Yorkshire

and the

Humber

Population Only

Population + Deprivation

Population + Deprivation + ACA

No Change

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 22

population + deprivation and 70% for population + deprivation + ACA. All other regions

except for London benefit from each of the three simpler models for lower tier EPCS.

SE Individual Authority Position

2.22 It is important to note, however, that this represents the regional position as a whole. Given the

diversity of SE authorities, the position for individual authorities within the SE is very different,

depending upon their particular characteristics. This is illustrated in Charts 2.11, 2.12 and 2.13

below.

Chart 2.11: Social services for older people – individual SE authorities’ position

Chart 2.12: Lower tier EPCS – individual SE authorities’ position (A-M)

0%

20%

40%

60%

80%

100%

120%

140%

160%

Bra

cknell

Fore

st

Brighto

n &

Hove

Buckin

gham

shire

East S

ussex

Ham

pshire

Isle

of W

ight C

ouncil

Kent

Medw

ay

Milt

on K

eynes

Oxfo

rdshire

Port

sm

outh

Readin

g

Slo

ugh

South

am

pto

n

Surr

ey

West B

erk

shire

West S

ussex

Win

dsor

and

Maid

enhead

Wokin

gham

Local Authority

Perc

en

tag

e C

han

ge

Population Only

Population + Deprivation

Population + Deprivation + ACA

No Change

0%

20%

40%

60%

80%

100%

120%

140%

Adur

Aru

n

Ashfo

rd

Ayle

sbury

Vale

Basin

gsto

ke a

nd D

eane

Bra

cknell

Fore

st

Brighto

n &

Hove

Cante

rbury

Cherw

ell

Chic

heste

r

Chilt

ern

Cra

wle

y

Dart

ford

Dover

East H

am

pshire

Eastb

ourn

e

Eastleig

h

Elm

bridge

Epsom

and E

well

Fare

ham

Gosport

Gra

vesham

Guild

ford

Hart

Hastings

Havant

Hors

ham

Isle

of W

ight C

ouncil

Lew

es

Maid

sto

ne

Medw

ay

Mid

Sussex

Milt

on K

eynes

Mole

Valle

y

Local Authority

Perc

en

tag

e C

han

ge

Population Only

Population + Deprivation

Population + Deprivation + ACA

No Change

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 23

Chart 2.13: Lower tier EPCS – individual SE authorities’ position (N-W)

2.23 The key points to note for SE authorities in relation to simple funding formulae are:

Lower need authorities will gain from simpler funding formulae and vice versa, with the

impact upon individual authorities often being significant.

0%

20%

40%

60%

80%

100%

120%

140%

New

Fore

st

Oxfo

rd

Port

sm

outh

Readin

g

Reig

ate

and B

anste

ad

Roth

er

Runnym

ede

Rushm

oor

Sevenoaks

Shepw

ay

Slo

ugh

South

Bucks

South

Oxfo

rdshire

South

am

pto

n

Spelthorn

e

Surr

ey H

eath

Sw

ale

Tandridge

Test V

alle

y

Thanet

Tonbridge a

nd M

alli

ng

Tunbridge W

ells

Vale

of W

hite H

ors

e

Waverley

Weald

en

West B

erk

shire

West O

xfo

rdshire

Win

cheste

r

Win

dsor

and M

aid

enhead

Wokin

g

Wokin

gham

Wort

hin

g

Wycom

be

Local Authority

Perc

en

tag

e C

han

ge

Population Only

Population + Deprivation

Population + Deprivation + ACA

No Change

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 24

For example, for upper tier authorities in relation to social services for older people,

Wokingham would see its share of funding increase to 150%, 123% and 130% of its

current funding levels for a population only, population + deprivation and population +

deprivation + ACA model respectively.

Conversely, high need authorities would lose out, with Southampton and Slough being

the biggest losers in relation to social services for older people, with a population only

model resulting in them receiving 83% and 87% of their current funding share

respectively.

For lower tier EPCS, Hart would be the largest gainer from a population only model

(receiving 130% of its current funding share), whereas Crawley would only receive 95%

of its current share.

2.24 SEEC will therefore need to consider the effect on individual member authorities, in addition to

the region as a whole, when considering any potential changes to funding formulae. As

considered in the following section of this report, however, if a business rates retention

scheme is introduced by government, under current proposals, the “needs baseline” will be

fixed for a specified period, locking in any potential perceived inequities within the funding

formulae in place at the time that the baseline is set.

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 25

3 Business Rates Retention

Introduction

3.1 On 18 July 2011, the Department for Communities and Local Government published the paper,

“Local Government Resource Review: Proposals for Business Rates Retention – Consultation”.

The consultation paper included reference to eight further technical papers on business rates

retention, which were subsequently released on 19 August 2011.

3.2 The eight technical papers are as follows:

Table 3.1 – Technical Papers

Technical Paper Content

1) Establishing the baseline

How, technically, the government establishes the baselines and the

implications of fixing them for a number of years between resets.

2) Measuring business rates

The issues associated with measuring business rates and options for

doing so.

3) Dealing with non-billing authorities

The basis for funding police and fire authorities in 2013-14 and 2014-15

and, more widely, that for apportioning rates between authorities.

4) Business rates administration

The consequences for business rates administration of the scheme

outlined in the consultation paper.

5) Tariff, top up and levy options

Options for the design of tariffs, top ups, the levy and the use of levy

income.

6) Volatility Causes and the options for dealing with it.

7) Revaluation and transition

The practicalities of assessing business rate income following a

revaluation. It will also consider the implications of the transition

scheme – and in particular, how this affects business rate

administration and the payments made between authorities.

8) Renewable energy

Definitions of renewable energy, the treatment of rates from renewable

sources for the purposes of tariffs, top ups and levies, and their

distribution between the tiers.

3.3 The government's stated aim through business rates retention is to provide a greater incentive

to local authorities to increase non-domestic rate (NDR) revenues. This incentive would be

created through proposals that would allow authorities to retain an element of any increased

revenues due to growth in NDR revenues.

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 26

3.4 The complex nature of local government finance, the need for some element of funding stability,

and, in particular, the variation between local authorities in terms of the amount of business

rates retained locally, means that the proposed scheme will require a number of features to

provide sufficient incentives to all authorities and protect those that are not able to increase

NDR revenues or may have one-off reductions in the amount of NDR collected.

3.5 The key features of the proposed system are as follows:

Local authorities will still need to operate within the existing NDR system. They will not

have control over how the level of tax is determined for ratepayers i.e. the rateable value

of properties or the national multiplier (the rate of tax).

Each local authority will be provided with an initial baseline level of funding - this is

known as its “needs baseline”. Local authorities' needs baselines will be based upon

the 2012/13 Formula Grant allocation (with adjustments for the 2013/14 control totals

and possibly other changes to the formula and underlying data). The needs baseline is

effectively the starting point for the rates retention system.

Not all growth in NDR receipts will be distributed to local authorities – sufficient

resources to fund the New Homes Bonus scheme will be retained centrally. There will

also be deductions for Police authorities, where funding will continue (at least in the

short term) to be provided through a formula-based grant (and potentially for single

purpose Fire and Rescue authorities, depending upon the option chosen from the

consultation).

An additional amount will also need to be removed from the system in 2013/14. This

represents the difference in funding for local authorities between 2013/14 and 2014/15.

It is necessary to remove this amount, as the baselines need to be based upon the

lowest funding point (i.e. in 2014/15). The government plans to distribute the amount

removed from the baseline to local authorities in 2013/14 as section 31 grant, using

authorities’ needs baselines as the basis for apportionment. This funding will be known

as the “2013/14 adjustment grant”.

A system of “tariffs” and “top ups” will be introduced, in order to allow for the fact that

authorities have significantly different capacities to generate NDR income, depending

upon their NDR taxbase. A tariff will be paid by an authority to government where their

NDR income exceeds their needs baseline. A top up will be received by authorities from

government where their NDR income is below their needs baseline. Tariff/top up

amounts could be (i) indexed to RPI or (ii) fixed as a cash amount.

There will be a “reset mechanism”, designed to keep resources broadly in line with

need. Without resets, there is the potential for authorities' levels of need (based upon

population and socio-economic factors, for example), to become significantly higher or

lower than the amount that is being received through rates retention. Each year

between resets, individual authorities will either pay the same tariff or receive the same

top up. Resets could be (i) partial (where authorities benefit from growth in business

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 27

rates obtained before the reset) or (ii) full (authorities only benefit from any growth in

their local business rates obtained in the time period between two resets).

There will be a “safety net” for payments to local authorities experiencing negative

volatility in business rate income. There could be (i) an “annual” safety net (where

income in any year declines by more than a set percentage when compared to the

previous year's income) or (ii) a “baseline” safety net (where income in any year

declines by more than a set percentage below the baseline funding level).

A “levy” system will scale back the amount of resources that are retained locally (and

this may be linked to the size of authorities' NDR base). Three options have been put

forward for how a levy could be calculated: (i) Flat rate levy, such that an authority pays

x pence of every pound of business rate growth into the levy pot, (ii) Banded levy,

where authorities would be grouped into bands based on their gearing ratios, with the

levy being higher for those authorities in bands with higher levels of gearing or (iii)

Proportional levy, with each authority being assigned an individual levy rate, set such

that a 1% increase in an authority's business rates would result in a fixed percentage

increase in its retained income.

South East authorities – net NDR contributions

3.6 Currently, business rates are collected locally, paid into a national pool and then redistributed to

authorities in the form of Formula Grant. Based on provisional 2012/13 figures, the SE currently

contributes significantly more (£895m) into the national NDR pool than it receives in Formula

Grant.

3.7 In 2012/13, authorities in the SE are projected to collect £3.269bn in business rate receipts.

Meanwhile, they will receive only £2.373bn of Formula Grant in return, including funding for

their police and fire services3. This means that, for every pound of Formula Grant received, the

South East contributed £1.38 in business rates. This is summarised in Table 3.2 below.

3.8 This ratio is the highest in England and makes it one of only three net contributing regions,

alongside London and the East of England. The South East's projected net contribution of

£895m to the national funding pool is the largest in absolute terms (London's net contribution is

£701m).

3 Formula Grant includes both redistributed NDR and Revenue Support Grant, but excludes the separate Home Office police grant.

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 28

Table 3.2: Business Rates Compared to Formula Grant (including Police & Fire), 2012/13

Region

Projected

NDR

contribution

(£m)

Damped

Formula

Grant*

(£m)

Net

contribution

(£m)

Ratio

(NDR/Grant)

South East 3,268.73 2,373.30 895.43 1.38

London 5,697.82 4,996.90 700.92 1.14

East 2,091.72 1,843.60 248.12 1.13

South West 1,715.92 1,771.70 -55.78 0.97

East Midlands 1,381.23 1,741.70 -360.47 0.79

West Midlands 1,878.51 2,603.70 -725.19 0.72

Yorkshire & Humber 1,700.69 2,484.50 -783.81 0.68

North West 2,389.56 3,629.60 -1,240.04 0.66

North East 776.25 1,470.10 -693.85 0.53

ENGLAND 20,900.43 22,915.00 -2,014.57 0.91

* Excludes the separate Home Office Police Grant

3.9 These projected NDR contributions are based upon using the following assumptions:

The 2010/11 actual NDR revenues from the 2010/11 NNDR 3 returns (published 25

August 2011)

The actual increase to the national multiplier for 2011/12 from 41.4p to 43.3p

A forecast increase to the national multiplier for 2012/13 of 5.6% (using the September

2011 RPI rate)

No growth/decline in the regional taxbases (i.e. the only change in NDR revenues is due

to increases to the multiplier)

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 29

Potential size of the business rates retention incentive

3.10 The potential level of incentives for authorities in the SE region under the proposed business

rates retention system was considered, to identify the scale of the incentive available.

3.11 CLG's proposals to exclude the effects of revaluation when considering business rates growth

will restrict a council's potential income growth to the expansion of its physical taxbase (plus

inflation). Historical data has been used to assess how this would translate to potential real-

terms income growth for the SE.

3.12 Rateable values are based upon market rental values and are assessed independently by the

Valuation Office Agency. All rateable values are reassessed every five years at revaluation, the

last taking effect in April 2010.

3.13 At revaluation, the overall increase in aggregate yield is capped nationally by the Retail Prices

Index (RPI). The multiplier is adjusted to achieve that effect. Therefore, if national rateable

value growth is greater than RPI, as was the case in the 2010 revaluation, the multiplier is

scaled down accordingly.

3.14 This causes considerable variation at the local authority level. Yields in each authority can

increase or fall significantly, depending on whether the rateable value in that area has grown

faster or slower than the national average. Authorities whose rateable value growth has been

less than the national average see a reduction in their business rate yields.

3.15 At the 2010 revaluation, for example, over 200 billing authorities experienced a fall in the rates

they collected. The SE region saw its business rates yield fall by 3.8% (£136m).

3.16 Under a retained business rates system, this would cause considerable turbulence in local

authorities' retained income. To deal with this turbulence, government is proposing to neutralise

the effects of revaluations on business rate retention. It is proposed that "tariffs and top ups

should be adjusted at revaluation to ensure that, as far as possible, business rates income is

unaffected." In other words, CLG will "ensure that retained income is the same after revaluation

as immediately before"4.

3.17 Retained business rates will therefore be limited to growth in business rate yield between

revaluation years. Between revaluation years, gross business rate yield growth is comprised of:

The increase in the multiplier, which increases with RPI each year; and

The growth in each authority's rateable value. Between revaluation years, this reflects

the establishment of new businesses in an area, minus the impact of any closures or

relocations. The net impact on the authority's tax base will depend on both the change in

4 Technical Paper 7, paragraphs 2.5 and 3.7

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 30

the number of physical properties or “hereditaments” and the average rateable value of

each5.

3.18 Whilst providing stability, government's decision to neutralise the effects of revaluations will

have major implications for the incentives provided by the business rates retention system.

Analysis was therefore carried out to assess:

The proportion of rateable value growth that, historically, has been attributable to

revaluations (both nationally and among South East authorities); and

The potential “real terms” business rate growth for South East authorities once

revaluations are excluded, based on historical taxbase data.

3.19 Business rates data from 2006/07 to 2011/12 was examined, which includes the effect of the

2010 revaluation. As shown in Table 3.3, the results show that nearly all the growth in

authorities' rateable value has been due to revaluation.

Table 3.3: Business rateable value growth in South East England 2006/07 to 2011/12

£bn

Starting rateable value in the South East 7.349

Total growth in rateable value over 5-year period 1.132

Of which: growth resulting from revaluations 1.009

Of which: growth excluding revaluation 0.123

Average annual growth rate, excluding the

effects of revaluation

0.33%

3.20 As identified above, once the effects of revaluation are excluded, as CLG are proposing,

average annual growth falls to just 0.33% per year for the SE. This was higher than the national

average (0.14% per annum), but still low in absolute terms. As CLG intends to apply a levy on

'disproportionate' growth, if a proportional levy is in operation, whereby a 1% increase in

individual authority business rates could not result in more than a 1% increase in retained

income, no authority's retained income could grow faster than its growth in rateable value.

Therefore, the SE would have seen real retained income growth of not more than 0.33% per

annum.

3.21 Had authorities in the SE received this incentive in 2011/12, then this would have generated

real-terms income growth of only £8.6m (after adjusting for inflation) i.e. 0.33% of the SE’s

2011/12 Formula Grant of £2.611bn. The 74 SE local authorities would obviously only receive

a small proportion of this each.

5 For example, a local authority may gain an advertising hoarding and a mobile telephone mast, but lose a major retail store. In this case

the number of taxable hereditaments has increased but its overall taxbase/rateable value will have reduced in size.

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 31

Business rates retention compared to the current system

3.22 As identified above, the government's business rates retention proposals set out a number of

options in terms of the potential operation of the system. To assess the potential impact of

these proposals on the SE authorities, a five-year resource projection has been undertaken.

These projections are then compared to estimates of the authorities’ income had the current

distribution methodology been retained (that is, if the funding had continued to be distributed via

the existing four block model instead).

Step 1: Resource projections

3.23 To produce the projections, it was necessary to make assumptions about which business rate

retention options would be implemented. Some of these assumptions will have a major impact

on the projected income for SE authorities. Rather than anticipate which of these options would

be applied from 2013/14 onwards, these are instead presented as a set of scenarios. The

scenarios are based on two policy variables: one relating to the size of the levy, and the other to

the tariff/top up.

3.24 The levy. CLG has put forward three options for how the levy on business rate growth will be

set: either as a fixed rate for all authorities, as a series of bands, or proportional to business rate

yield growth (3 options).

3.25 Tariff/top up. Each authority’s tariff or top up could be held constant in cash terms, or

increased in line with RPI each year (2 options).

3.26 This gives rise to six scenarios (the combination of the three levy options and two top up/tariff

options), which are summarised below. These scenarios form the basis of the resource

projections.

Table 3.4: Scenarios used in resource projections

Levy Option

Flat Rate Banded Proportional

Tariff / Top

Up Option

Fixed tariff or

top up Scenario 1 Scenario 2 Scenario 3

Uprate tariff or

top up by RPI Scenario 4 Scenario 5 Scenario 6

Step 2: Compare resource projections to existing distribution methodology

3.27 The resource projections were then compared to estimates of authorities’ funding had the

current distribution methodology been retained. Under each scenario, the projected England

total is allocated according to the existing four block model distribution.

3.28 The results are presented in the table below. For example, under Scenario 2, the projected

annual income for SE authorities would be 5.1% higher in 2017/18 than it would have been if

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 32

the same envelope of funding (i.e. the projected England total) had instead been distributed

using the existing Formula Grant model.

Table 3.5: Projected retained business rates versus Formula Grant

Difference in annual income compared to the equivalent Formula Grant

distribution (after damping)

2013/14 2014/15 2015/16 2016/17 2017/18

Scenario 1

Fixed & Flat

+0.6% +1.5% +2.4% +3.3% +4.3%

Scenario 2

Fixed & Banded

+0.8% +1.8% +2.9% +4.0% +5.1%

Scenario 3

Fixed & Proportional

+0.4% +1.0% +1.7% +2.3% +3.0%

Scenario 4

Uprated & Flat

+0.0% +0.1% +0.1% +0.2% +0.4%

Scenario 5

Uprated & Banded

+0.0% +0.0% +0.1% +0.2% +0.3%

Scenario 6

Uprated & Proportional

-0.1% +0.0% +0.0% +0.0% +0.1%

3.29 Overall, this analysis suggests that funding for the SE (as a whole) could potentially be at least

as favourable under the proposed business rate retention system compared to an equivalent

Formula Grant. Most notably, the decision to fix top ups/tariff in cash terms (the first three

scenarios) would result in significantly more funding for SE authorities than if they were indexed

to RPI (the final three scenarios).

3.30 Full details of this modelling, along with a complete description of assumptions, is presented as

a technical appendix to this report (see Appendix A).

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 33

4. Incentive Measures

Introduction

4.1 The Local Government Resource Review places emphasis on the importance of changes to the

local government finance system to reward authorities that aim for growth, by ensuring that they

receive the benefits from stimulating housing and economic development. This reflects the

intention set out in the Coalition Agreement that: “We will provide incentives for local authorities

to deliver sustainable development, including for new homes and businesses.” (Coalition

Agreement, May 2010.)

4.2 A key criticism of the current local government funding system is that local authorities do not

benefit significantly from any increases in their council taxbase, as these may be “equalised

away” by the operation of the Formula Grant system. Equally, there may be little direct fiscal

incentive to an authority to grow its business rates base, as any increases will be pooled for

redistribution to all local authorities in England.

4.3 In addition to the specific business rates retention proposals considered in section 3, a number

of measures have been introduced, or are being considered, with the intention of providing

greater financial incentives to local authorities to develop both their domestic and business

taxbases. A number of these incentives deal with similar issues; for example, the use of the

proceeds from business rates in relation to Business Improvement Districts; Tax Increment

Financing; Business Rate Supplement; Business Increase Bonus Scheme; Renewable Energy

Projects; and Enterprise Zones. These are described in this section and include:

i. The New Homes Bonus

ii. The Community Infrastructure Levy

iii. Business Improvement Districts

iv. Tax Increment Financing

v. Business Rate Supplement

vi. Business Increase Bonus Scheme

vii. Renewable Energy Projects

viii. National Insurance Contribution Reductions

ix. Enterprise Zones

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 34

i. New Homes Bonus

Key features

4.4 In the summer of 2010, the Housing Minister, Grant Shapps MP, announced the government's

proposal to introduce a New Homes Bonus (NHB). The intention of the scheme would be to

provide a financial incentive to local authorities to encourage house building, with the

government match funding the additional council tax generated when a new home is built or a

property is brought back into use, including an additional amount for affordable homes.

Consultation proposals were published in November 2010 and details of the final scheme were

announced in February 2011. The main features of the scheme are:

The NHB scheme did not require primary legislation and the scheme was introduced for

the 2011/12 financial year. Grant allocations to individual local authorities for 2011/12

were announced on 4 April 2011.

The scheme will provide local authorities with a New Homes Bonus (NHB) grant, equal

to the national average for the council tax band on each additional property and paid for

the following six years as an unringfenced grant. Currently, this means for a new Band

D property, a grant of £1,439 per annum, or £8,634 over six years. The amount paid will

be reviewed annually.

To help ensure that affordable homes are sufficiently prioritised within supply, there will

be a flat rate enhancement of £350 per annum for each additional affordable home -

equal to around 25% of the current Band D council tax.

The NHB will also apply to empty properties brought back into use, to strengthen the

incentive for local authorities to identify empty properties and to work with owners to find

innovative solutions that allow these properties to be brought back into use.

DCLG has allocated £200m to fund the scheme fully in 2011/12, using resources from

the cessation of the Housing Planning and Delivery Grant. For the following three years

of the Spending Review (2012/13 to 2014/15), £250m per annum has been allocated for

the NHB, with funding beyond these levels coming from Formula Grant.

The payment of the New Homes Bonus will be split between tiers in shire areas: 80% to

the lower tier and 20% to the upper tier, as a starting point for local negotiation. Local

authorities will have flexibility on how to spend the NHB grant, which, in many cases, will

involve advanced planning with other local service providers to ensure the timely delivery

of infrastructure for new development. Also, authorities may choose to pool some

funding at the level of the Local Enterprise Partnership, to invest in shared priorities

which support long term prosperity for the area.

Potential issues for SE authorities

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 35

4.5 Local authorities in the South East received £34.1 million (17.1%) of the England total for the

NHB of £199.3 million in 2011/12. For five districts in the South East, the NHB grant was

equivalent to more than 10% of their Formula Grant for 2011/12. The 17.1% share of the NHB

grant going to authorities in the SE can be compared with their share of 2011 projected

population (16.3%), the share of council taxbase (18.0%) and the share of Formula Grant

(10.9%).

4.6 Authorities in the SE therefore currently benefit more from the NHB than they would from a

comparable increase to aggregate Formula Grant. For the second and subsequent years of the

scheme, where any funding above £250 million is taken from Formula Grant, if the reduction in

Formula Grant was made as a pro rata percentage reduction to Formula Grant, for each £200

million of additional funding through the NHB, SE local authorities would lose £21.8 m in

Formula Grant, but gain £34.1 m in NHB grant – a net gain of £12.3 m.

4.7 However, the net effect on grant from 2012/13 onwards will depend crucially on how the

adjustment is made to the Formula Grant system to accommodate any transfer from Formula

Grant to the NHB. Rather than just top-slicing the overall amount of Formula Grant, one option

would be to make an adjustment to the EPCS control totals, and particularly to the lower tier

EPCS block, to reflect the fact that the tier split of the NHB is 20% for upper tier authorities and

80% for lower tier. Depending on how this was undertaken, and on any other related changes

to the revenue grant system, the net gain for SE authorities arising from the NHB might be

significantly reduced.

4.8 The introduction of the NHB is likely to be of net benefit to local authorities in the SE, and, for a

number of districts, represents a substantial increase in revenue funding. However, in the

longer term, the net effect for SE authorities will depend on the changes that are made to the

Formula Grant system to accommodate the transfer of funding to the NHB. For the SE region

as a whole, it could be argued that, to retain the incentive effect of the NHB, there should be a

pro rata top slice to Formula Grant, rather than making changes to grant mechanisms which

would "equalise away" some of the benefits to authorities in the SE. This is an issue that the

SE authorities will need to keep under review, as part of the potential other changes to be made

to the Formula Grant system.

ii. Community Infrastructure Levy

Key features

4.9 The Community Infrastructure Levy (CIL) will allow local authorities to raise funds from

developers undertaking new building projects in their area. The funding raised can be used to

fund a wide range of infrastructure needed as a result of development – such as new road

schemes, schools, health and social care facilities, and parks. The CIL will be charged by

district and unitary authorities. The CIL is seen by the government as fairer, faster and more

certain and transparent than the current system of planning obligations, which may cause delay

as a result of lengthy negotiations. Currently, only 6% of all planning permissions bring any

contribution to the cost of supporting infrastructure.

Fair Funding for the South East Stage 2 Research Report

FINANCE WITH VISION 36

4.10 Though the CIL came into force from April 2010, no local authority has yet implemented the

new levy. This is partly due to changes to regulations, including the Community Infrastructure

Levy Regulations (Amendment) Regulations 2011, and changes to the levy set out in the

Localism Bill. The Planning Advisory Service is working with a group of local authorities – the

front runners – to develop their charging schedules and consider effective ways of implementing

the levy in their local areas. Initially, eight local authorities were selected to be front runners –

but none from the South East. However, at the end of June 2011, another 20 local authorities

were selected to join the front runners project, including 4 authorities from the South East –

Elmbridge, Milton Keynes, Oxford and Wycombe. It seems likely that income from the first CIL

schemes will come on stream for some councils in 2012/13.

4.11 Rates for the new levy will be set in consultation with local communities and developers and are

intended to provide developers with more certainty about how much they will be expected to

contribute. Local authorities are required to spend the levy on the infrastructure needed to

support the development of the area, and the Planning Act 2008 provides a wide definition of

the infrastructure that can be funded by the levy.

4.12 The Localism Bill proposes changes to the levy to make it more flexible. It will allow the money

raised to be spent on maintaining infrastructure, as well as building new infrastructure. It will