SMC Global Monthly Report on Bullions & Energy

19

SPECIAL MONTHLY REPORT ON Bullions & Energy (May 2014)

-

Upload

smc-global-securities-ltd -

Category

Economy & Finance

-

view

87 -

download

0

Transcript of SMC Global Monthly Report on Bullions & Energy

SPECIAL MONTHLY REPORT ON

Bullions & Energy(May 2014)

2

BU

LL

ION

S &

EN

ER

GY

May 2014

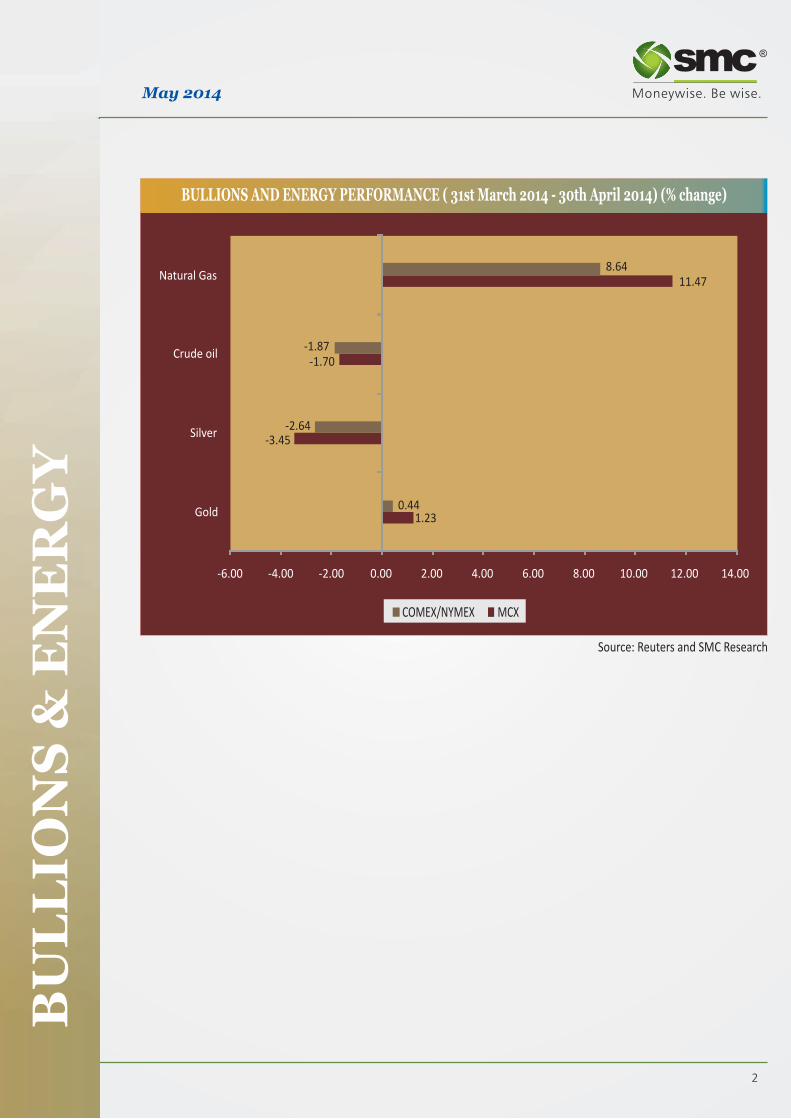

BULLIONS AND ENERGY PERFORMANCE ( - 30th April 2014) (% change) 31st March 2014

Source: Reuters and SMC Research

COMEX/NYMEX MCX

1.23

-3.45

-1.70

11.47

0.44

-2.64

-1.87

8.64

-6.00 -4.00 -2.00 0.00 2.00 4.00 6.00 8.00 10.00 12.00 14.00

Gold

Silver

Crude oil

Natural Gas

3

BULLIONS

In the month of April bullion counter moved in very

thin range on mixed fundamentals. Dollar index

took support near 79.5 levels and recovered last

month which pressurized the bullions lower. Slow

China physical demand capped the upside in gold.

Overall gold traded in range of 27770-28670 in MCX

and $1268-1332 in COMEX. Silver traded in range of

$18.91-20.38 in COMEX and 41500-43800 in MCX.

Recently rising greenback and better economic data

have kept the prices downbeat. Meanwhile

geopolitical tensions in Ukraine kept the downside

capped as it increases safe haven demand of yellow

metal. COMEX Gold has rallied 7.5 percent this year,

rebounding from the worst annual drop in more

than three decades, partly as the conflict between

Russia and Ukraine fueled demand. U.S. Secretary

of State John Kerry warned that Russia was running

out of time to comply with an accord aimed at easing

tensions in Ukraine, as Russian forces began

exercises on the two countries' border. President

Vladimir Putin warned Ukraine against continuing

an anti-separatist offensive. Holdings in the SPDR

Gold Trust, the largest gold backed exchange traded

product, held at a 12-week low of 792.14 metric

tonnes.

In the month of May 2014 bullion counter can move

sideways with upside bias. On domestic bourses the

movements of local currency rupee will be key factor

to watch out which can move in range of 59-61.50 in

the month of May. Gold can trade in range of Rs

26000-29500 in MCX and $1220-1350 in

COMEX. Silver can trade in range of 40000-

44000 in MCX and $19-21 in COMEX. The

gold/silver ratio has moved to nearly 66.7 from 61

since start of the February which showed that silver

fell at faster pace than gold recently. This ratio can

hover in range of 64-68 in the month of May.

Recovery in US economy has also led to reduced safe

haven demand in bullion counter. Investors looked

ahead to a series of key economic events in this

month for further indications on the strength of the

U.S. economy and the future course of monetary

policy. An improving economy and slowing stimulus

measures hurt gold's appeal as an investment

compared with other assets. Meanwhile, hundreds

of pro-Moscow separatists stormed government BU

LL

ION

SMay 2014

buildings in one of Ukraine's provincial capitals on

recently and fired on police holed up in a regional

headquarters, a major escalation of their revolt despite

new Western sanctions on Russia. Geopolitical tensions

usually increase gold's appeal as a safe haven asset. Gold

has gained from rising Ukraine tensions this year, but it

has recently been weighed down by strong economic

data. Turkey cut its gold holdings by 14.3 tonnes to 483

tonnes in March, while Russia lowered its bullion

reserves slightly last month. As per industry forecast,

gold imports to India for April and May are likely to be

feeble against March imports as restrictions on cash

movements during the general elections possibly

reduced the purchasing power of consumers.

Gold and emerging markets

Over the past decade, emerging markets have benefited

from strong growth and cheap funding. Investors have

increased their exposure and, given the positive long-

term view of these economies, there is a strong rationale

for investors to have EM in their portfolios. However,

given recent market volatility and concerns about the

sustainability of EM growth, it is more pressing than

ever for investors to understand how to hedge exposure

to the asset class and, even if they don't have direct

holdings, how to reduce the effects of a spillover in their

portfolios. While EM crises may have been regionally

contained in the past, the increasing weight of these

markets in global GDP and international trade could

increase the risk of contagion in any future crisis. In that

context, there is a strong argument for using gold to

enhance EM hedging strategies.

Ukraine tensions and Gold

Recently escalating military tension between Ukraine

and Russia bolstered demand for assets such as gold

which is perceived to be relatively safe haven. Any

escalation in tensions between Russia and the West over

Ukraine could push prices higher. Ukraine sought to

dislodge rebels from its eastern industrial heartland

amid violence that's also spread to the Black Sea

gateway of Odessa. Troops in the Donetsk area, near

Russia's border, took back a television tower overnight

that had been seized by pro-Russian forces.

4

BU

LL

ION

SMay 2014

Election cash restrictions to dent India's

gold imports

India's gold imports in April and May could be less

than half of arrivals in March, as restrictions on the

movement of cash during general elections dent the

buying power of consumers, jewellery industry.

Lower imports by the world's No.2 buyer of gold

after China could hurt a recovery in global prices of

the precious metal after a sharp 28 percent drop last

year.

India's 2013/14 gold, silver imports down 40

pct at $33.46 bln-govt source

Gold and silver imports into India, the world's

second-biggest buyer of the metal, dropped 40

percent to $33.46 billion in 2013/14, following a

series of restrictions imposed by the federal

government to curtail the current account deficit.

China imports less gold as demand wanes,

currency weakens

Banks in China have been importing less gold over

the past month as demand waned after the festival

season, while cheaper prices at home due to a softer

yuan also curbed overseas purchases of the precious

metal. Nickel usage (consumption) will continue to

increase this year, although at a lower rate than in

recent years, with China being the main growth

market.

China Gold market

China's economy has grown by an astonishing 140%

over the past decade. Yet this figure is eclipsed by

spending on gold jewellery, which is estimated to

have risen by 500% in real terms over the same

period. Although this outperformance implies that

other factors have been at work, their positive

impact on the jewellery market has been

underpinned by the huge strides made by the

Chinese economy. Economic growth has not only

lifted hundreds of millions of China's citizens out of

poverty but also helped create sufficient wealth to

drive a boom in expenditure on a wide range of

consumer discretionary goods and services. Average

GDP per capita in China has increased to over

RMB42,000 (around US$7,000). However, income

distribution between social groups and regions is very

unequal. This means that there are a substantial

number of Chinese citizens whose incomes are a

multiple of the average. Indeed, the 'middle class',

defined as those households with incomes greater than

RMB50,000, now consists of almost 300 million

people and is forecast to grow to 500 million by 2020.

Such people have sufficient disposable income to

purchase higher value non-essential items, such as

jewellery and luxury goods. This group of wealthier

individuals has expanded considerably both in absolute

terms and in spending power. Moreover, its presence

has also grown in those parts of China, such as the West

and North East of the country, where economic

development has historically lagged behind that of

Beijing and the prosperous Eastern seaboard.

China Jewellery market

From humble beginnings China has become the world's

number one jewellery market, nearly trebling in size

over the past decade. Over the past decade the Chinese

jewellery market has been transformed. In terms of gold

demand this has meant a near tripling in volume from

2004's 224t to 669t last year.

Even more impressive is that over the same period

expenditure on gold jewellery has risen close to six-fold.

In 2013 China eclipsed India to become the world's

largest consumer and manufacturer of jewellery.

Moreover, in 2013 the country accounted for no less

than 30% of global jewellery demand. As explained

below, this tremendous expansion has been founded on

a combination of economic, demographic and cultural

factors.

According to Thomson Reuters GFMS China's

fabrication of gold jewellery jumped to 724t in 2013, a

31% rise over the previous year's figure. Over 85% of

fabrication is destined for the domestic market. Exports

to the US and Europe increased substantially in the

2000s.

5

BU

LL

ION

SMay 2014

Silver jewellery has performed especially well in China over recent years. Data from Thomson Reuters GFMS

show that fabrication demand has almost trebled in the past decade, reaching 1,762t in 2012.32

6

BU

LL

ION

SMay 2014

Key reason for surge in China demand

�China's transformation over the past 30 years

from rural poverty to urban prosperity has

created a new middle class, with economic

growth producing hundreds of millions of new

consumers.

�A huge expansion in manufacturing capacity

and retail outlets has provided the foundation

for explosive growth in jewellery demand.

�Demand has benefited from a substantial

increase in the working age population and a

rise in the number of marriages: we estimate

that wedding demand accounts for 40% of gold

consumption.

�Development of the supply-side infrastructure,

making products available to the public, has

been essential for investment demand growth.

�Investors in China believe that US economic

policies will eventually undermine the dollar

and drive up the international price of gold.

China Gold outlook for 2014

2014 is likely to be a year of consolidation after 2013's

spectacular growth in demand, although much will

depend on the trend in local gold prices. Over the

medium term the expected increase in real income and

purchasing power will support growth in jewellery

consumption.

China Gold investment demand

Since investment in bullion was permitted in 2004

demand for bars and coins has soared from a mere 10t to

397t in 2013. This phenomenal increase is connected to

the relatively limited set of investment options for

savers in China. It is also a reflection of investors' desire

to diversify assets away from an over-reliance on

volatile equities, illiquid property and bank deposits

that pay negative real rates of interest. It is expected by

WGC that medium term prospects are very positive and

demand could reach close to 500t by 2017, although in

the meantime we expect 2014 to be a year of

consolidation.

7

BU

LL

ION

SMay 2014

SHFE Gold trading

Speculative investment in gold, especially via the Shanghai Futures Exchange, has also grown tremendously in

recent years. A different type of private investor, or rather speculator, is active in the 'paper' markets, be that the

SGE or, more notably, the Shanghai Futures Exchange (SHFE). By definition, in order to access these markets

even through intermediaries the investors need to be large and relatively sophisticated. They are also usually

taking positions based upon short-term price expectations. Unlike physical bullion where investors typically

invest for the long-term, these are actively traded gold markets not 'buy and hold' ones. As explained below, these

markets have thrived, experiencing a major jump in turnover in recent years. Gold is a very high profile, liquid

and internationally traded asset that Chinese speculators are increasingly keen to trade on domestic bourses, or

even loco-London or Comex. These markets offer a less costly and more highly leveraged means of speculating on

gold than, for example, ETFs.

China industrial demand

Industrial demand for gold has grown strongly but is tiny compared to jewellery and investment demand. Gold

use in a variety of industrial applications accounted for around 5.5% of total private sector demand and 8% of

Chinese fabrication demand in 2013. Around two-thirds of industrial demand in China is related to electronics,

with the balance largely required for a variety of decorative uses.

Overall industrial demand has grown strongly in the past decade, climbing from 16t in 2003 to around 66t in

2013. This is in line with China's rise to prominence as the world's manufacturing hub. Data on industrial

production show the same trend, with output in 2013 over 2.5 times greater than it was in 2004. China has

become the world's dominant producer of electronics goods, the world's largest manufacturer of automobiles

and a growing centre for the production of branded luxury goods.

8

BU

LL

ION

SMay 2014

China official reserves

Based on a declared stock of 1,054t China is the world's sixth largest holder of bullion but this only represents 1%

of its total official reserves. In fact, there have been three occasions in the recent past when China has reported a

sudden increase in its official monetary reserves to the IMF. In 2001 reported monetary gold holdings increased

from 395t to 500t and in 2002 to 600t . Then in April 2009 gold holdings jumped to 1,054t, a level that has been

maintained since then through to the end of 2013. The most recent increase in reported gold holdings has led to

China becoming the world's sixth largest holder of gold behind the US (8,134t), Germany (3,387t), the IMF

(2,814t), Italy (2,452t) and France (2,435t).

9

BU

LL

ION

SMay 2014

Range

Gold MCX Rs 26000-29500 per 10 gms

COMEX $1220-1350 per troy ounce

Gold Hedge NCDEX Rs 24700-26700 per 10 gms

Silver MCX Rs 40000-44000 per kg

COMEX $19-21per ounce

Silver Hedge NCDEX Rs 3600-4000 per 100 gms

Gold Silver ratio

Source: Reuters

Analysis: The gold/silver ratio has moved to nearly 66.7 from 61 since start of the February which showed that

silver fell at faster pace than gold recently. This ratio can hover in range of 64-68 in the month of May.

In the month of May 2014 bullion counter

will remain sideways with upside bias.

Ukraine tensions and movement of

greenback will give further direction to the

prices. Moreover condition of global

economy and movement of local currency

rupee coupled with Physical, ETF demand

will also influence its prices.

ENERGYENERGYCRUDE OIL & NATURAL GASCRUDE OIL & NATURAL GAS

11

EN

ER

GY

ENERGY COMPLEX

Crude Oil

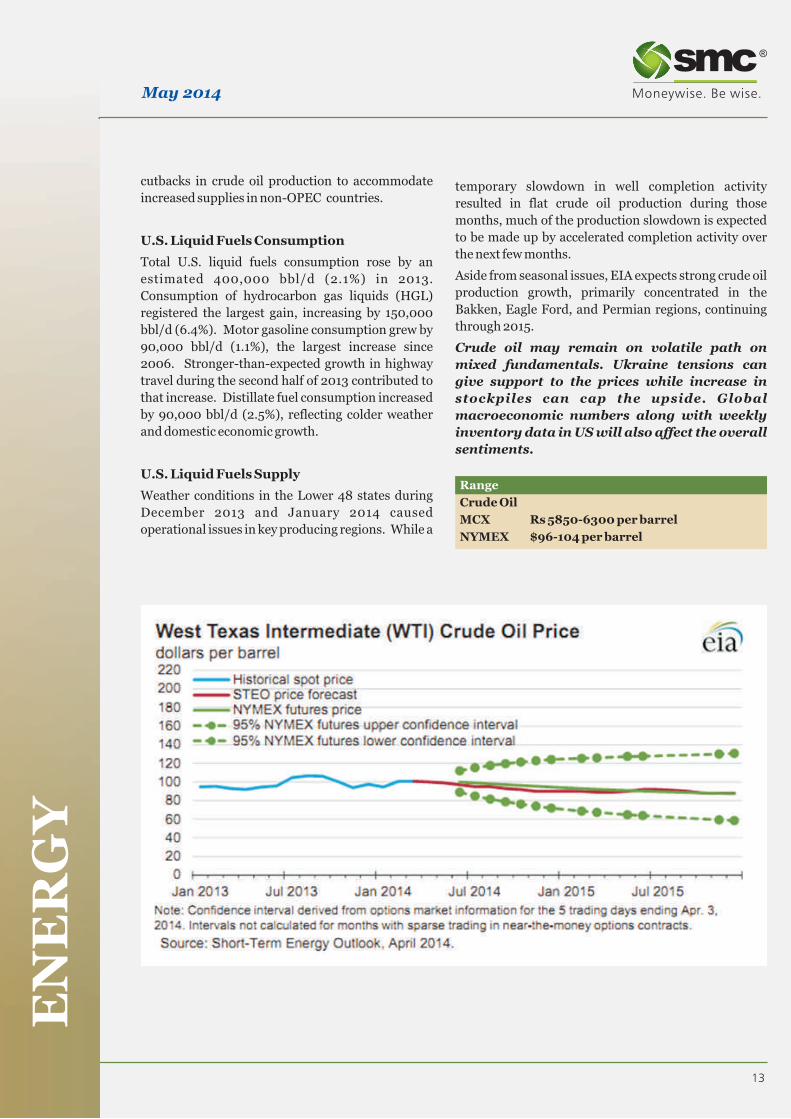

In the month of April crude oil prices traded on

volatile path amid recovery in greenback and

increasing stockpiles. On domestic bourses volatile

local currency rupee has kept the prices on sideways

path. Meanwhile Ukraine and Russia tensions gave

support to the prices. According to Energy

Information Administration “U.S. crude stockpiles

expanded by 3.52 million barrels to 397.7 million ”

Supplies have increased in the Gulf coast since

January as the southern leg of the Keystone XL

pipeline began moving oil from Oklahoma to the

Gulf of Mexico while U.S. law bars almost all

exports. Inventories along the Gulf Coast climbed by

2.44 million barrels to 209.6 million which are the

highest in EIA data going back to 1990.Prices traded

in range of nearly $98.8- 104.98 in NYMEX and

5928-6322 in MCX.

Crude oil futures can move on sideways with weak

bias in the month of May. Economic data from US

May 2014

and Europe will give direction to the crude oil prices.

Middle East tensions may result in reduced supplies

which may also give support to the crude oil prices.

Crude oil can move in range of 5850-6300 in the

month of May. Meanwhile U.S. Secretary of State

John Kerry warned Russia of making “an expensive

mistake” in Ukraine as Russia's military began drills

near the border. Russia is the world's second-largest net

oil exporter and supplied 30 percent of Europe's natural

gas last year. Libya's National Oil Corporation is set to

resume exports from Zueitina after declaring an end last

week to a force majeure imposed on the eastern port,

which was blocked by rebels for nine months. Investors

continued to monitor events in Ukraine, as hostilities

between Kiev and Moscow escalated after pro-Russian

rebels in east Ukraine took eight European military

inspectors hostage. In response, the U.S. and the

European Union said they will step up sanctions against

Moscow, underlining concerns over a disruption to

global supplies.

Brent WTI Spread

Source: Reuters

Analysis: Brent WTI spread expanded to above 8 after testing low of below 4 in beginning of this year .This

spread can hover in range of 7-10 in near term. Cushing inventories have decreased since January as the

southern leg of the Keystone XL pipeline began moving oil from the hub to Gulf Coast refineries. Supplies

dropped to 26 million in the week ended April 18, the least since October 2009, according to the Energy

Information Administration.

12

EN

ER

GY

May 2014

US oil rigs at record highs

The total number of drill rigs deployed onshore in

the US rose from 1,809 to 1,818 last month. Rigs

deployed in oil plays lifted from 1,487 to 1,498, while

rigs deployed in gas plays decreased from 318 to 316,

the lowest level since May 1993. Oil rigs have

increased to a record high since Baker Hughes

separated oil and gas rigs in 1987, as energy

producers utilise hydraulic fracturing and

horizontal drilling technologies to access shale

deposits.

IMF cuts world growth forecast in 2014

The International Monetary Fund (IMF) is

forecasting the world economy to grow by 3.6% this

year, down from its earlier estimate of 3.7%. The US

economy is expected to grow by 2.8% with China's

up 7.5% and Australia's to grow by 2.6%.

IEA lifts OPEC crude oil output forecast

The International Energy Agency (IEA) estimates

that crude oil supply from the Organisation of

Petroleum Exporting Countries (OPEC) fell

890kb/d from 30.51mb/d in February to

29.62mb/d March, reflecting weaker crude oil

output from Saudi Arabia, Iraq and Libya. The IEA

estimates that OPEC will need to supply 30.6mb/d

in 2014, above OPEC's collective 30mb/d target,

after the IEA cut its forecast for crude oil output

from Russia and Kazakhstan.

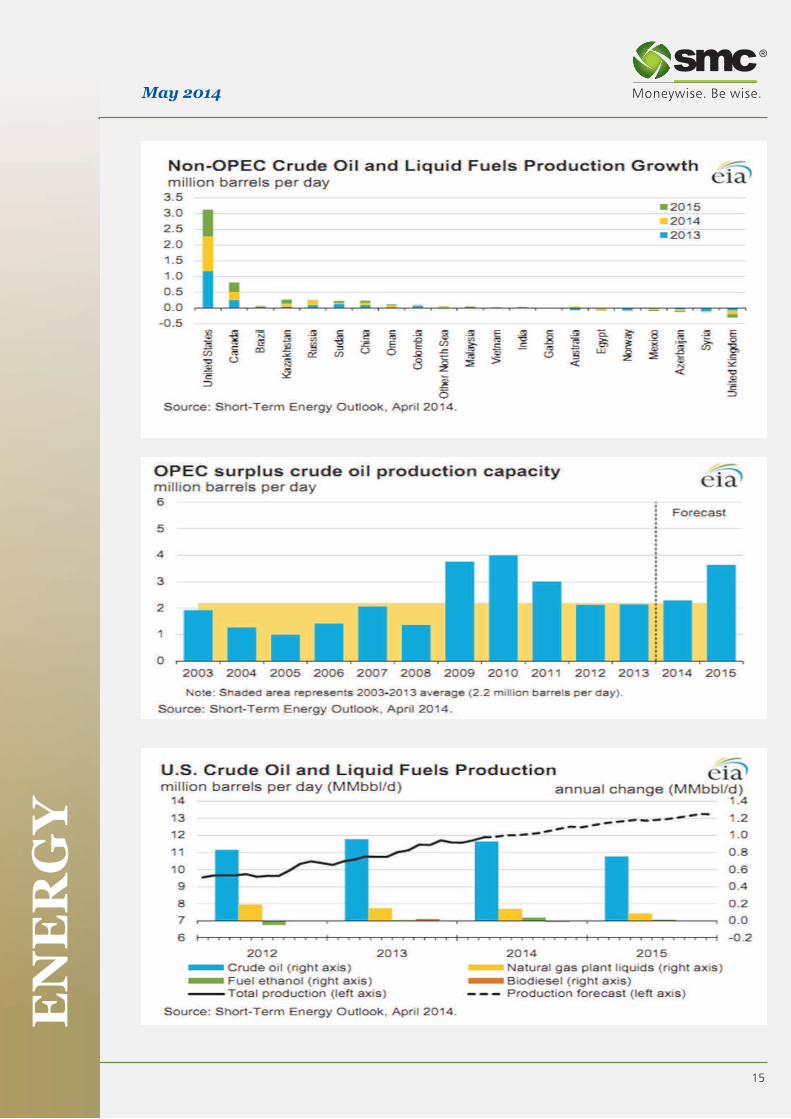

Some key points from EIA estimates

Global Crude Oil and Liquid Fuels

Consumption

EIA estimates that global consumption grew by 1.2

million bbl/d in 2013, averaging 90.4 million bbl/d

for the year. EIA expects global consumption to

grow 1.2 million bbl/d in 2014 and 1.4 million bbl/d

in 2015. Projected global oil-consumption-

weighted real GDP, which increased by an estimated

2.3% in 2013, grows by 2.9% and 3.4% in 2014 and

2015, respectively.

Non-OECD countries account for all of the expected

consumption growth in 2014 and nearly all of the

growth in 2015. China is the leading contributor to

projected global consumption growth, with

consumption increasing by 400,000 bbl/d in 2014

and 430,000 bbl/d in 2015. However, China's

economic and oil consumption growth rates have

moderated compared with rates before 2012, when

annual GDP growth exceeded 9% and oil consumption

growth averaged almost 800,000 bbl/d from 2009

through 2011.

EIA expects lower OECD consumption in 2014, led by

projected consumption declines in both Japan and

Europe. EIA expects Japan's oil consumption to fall by

an annual average of 150,000 bbl/d in 2014 and 2015, as

the country continues to increase natural gas and coal

consumption in the electricity sector and returns some

nuclear power plants to service in the second half of

2014 and in 2015. EIA projects that OECD Europe's

consumption, which fell by 100,000 bbl/d in 2013, will

decline by 60,000 bbl/d in 2014 and then remain

relatively flat in 2015. U.S. liquids consumption, which

increased by 400,000 bbl/d in 2013, is expected to

remain relatively flat in 2014 and then increase by

90,000 bbl/d in 2015.

Non‐OPEC Supply

EIA estimates that non-OPEC liquids production grew

by 1.3 million bbl/d in 2013, averaging 54.0 million

bbl/d for the year. EIA expects non-OPEC liquids

production to grow by 1.6 million bbl/d in 2014 and 1.3

million bbl/d in 2015. EIA forecasts production from

U.S. Energy Information Administration . United States

and Canada to grow by a combined annual average of 1.4

million bbl/d in 2014 and 1.2 million bbl/d in 2015. EIA

estimates that the Former Soviet Union's production

will rise by an annual average of 0.16 million bbl/d over

the forecast period, led by Russia in 2014 and

Kazakhstan in 2015.

Unplanned supply disruptions among non-OPEC

producers averaged 0.6 million bbl/d in March 2014,

about 40,000 bbl/d lower than in February as a result of

fewer outages in the North Sea and Indonesia. South

Sudan, Syria, and Yemen accounted for almost 90% of

total non-OPEC supply disruptions. EIA does not

assume a disruption to oil supply or demand as a result

of ongoing events in Ukraine.

OPEC Supply

EIA estimates that OPEC crude oil production averaged

30.0 million bbl/d in 2013, a decline of 0.9 million bbl/d

from the previous year, primarily reflecting increased

outages in Libya, Nigeria, and Iraq, along with strong

non-OPEC supply growth. EIA expects OPEC crude oil

production to fall by 0.2 million bbl/d in both 2014 and

2015, as a result of supply disruptions in OPEC and

13

EN

ER

GY

May 2014

cutbacks in crude oil production to accommodate

increased supplies in non-OPEC countries.

U.S. Liquid Fuels Consumption

Total U.S. liquid fuels consumption rose by an

estimated 400,000 bbl/d (2.1%) in 2013.

Consumption of hydrocarbon gas liquids (HGL)

registered the largest gain, increasing by 150,000

bbl/d (6.4%). Motor gasoline consumption grew by

90,000 bbl/d (1.1%), the largest increase since

2006. Stronger-than-expected growth in highway

travel during the second half of 2013 contributed to

that increase. Distillate fuel consumption increased

by 90,000 bbl/d (2.5%), reflecting colder weather

and domestic economic growth.

U.S. Liquid Fuels Supply

Weather conditions in the Lower 48 states during

December 2013 and January 2014 caused

operational issues in key producing regions. While a

Range

Crude Oil

MCX Rs 5850-6300 per barrel

NYMEX $96-104 per barrel

temporary slowdown in well completion activity

resulted in flat crude oil production during those

months, much of the production slowdown is expected

to be made up by accelerated completion activity over

the next few months.

Aside from seasonal issues, EIA expects strong crude oil

production growth, primarily concentrated in the

Bakken, Eagle Ford, and Permian regions, continuing

through 2015.

Crude oil may remain on volatile path on

mixed fundamentals. Ukraine tensions can

give support to the prices while increase in

stockpiles can cap the upside. Global

macroeconomic numbers along with weekly

inventory data in US will also affect the overall

sentiments.

14

EN

ER

GY

May 2014

15

EN

ER

GY

May 2014

16

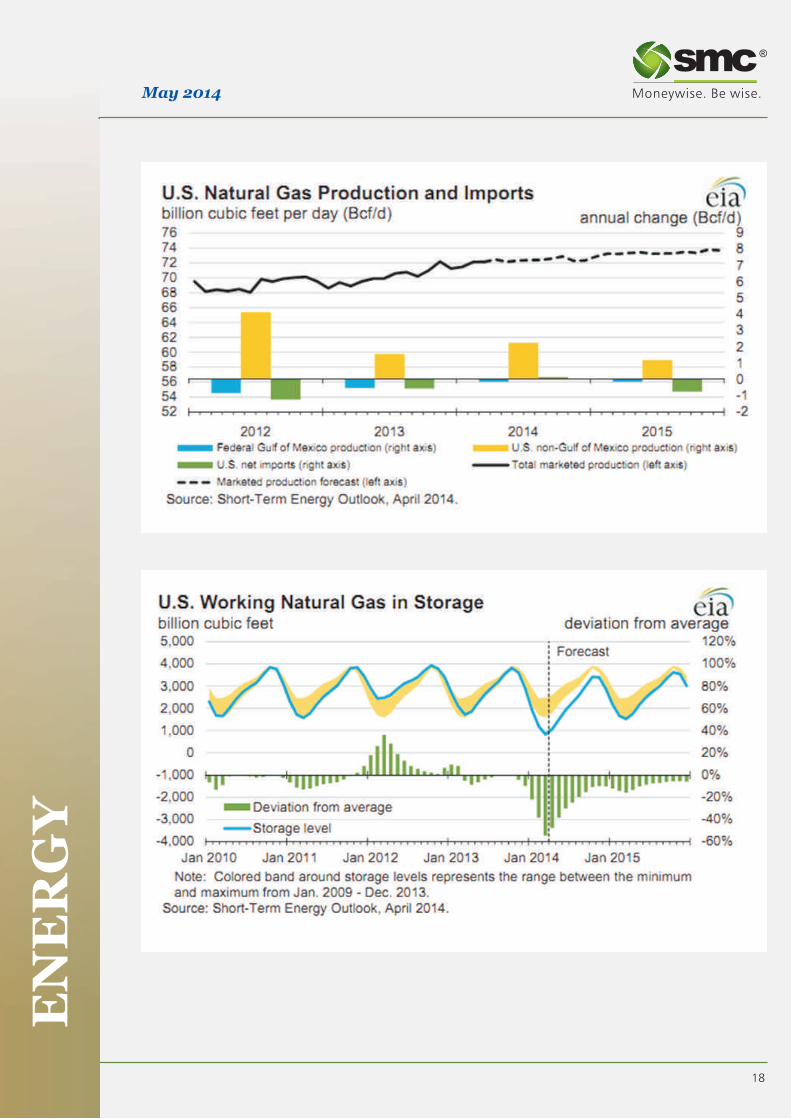

Natural Gas EIA Natural gas estimates

U.S. Natural Gas ConsumptionNatural gas prices recovered swiftly in the month of

April on cooler weather conditions and rise in EIA expects total natural gas consumption will

heating demand Overall it traded in range of $4.20-average 72.1 Bcf per day (Bcf/d) in 2014, an increase

4.83 in NYMEX and 256-294 in MCX. Prices got of 0.7 Bcf/d from 2013. Increased residential,

support as updated weather forecasting models commercial, and industrial use offsets declines

continued to call for below normal temperatures from the electric power sector, which are related to

stretching across portions of the central and eastern higher natural gas prices. In 2015, total natural gas

U.S. Portions of the Midwest and eastern regions of consumption falls by 0.4 Bcf/d as a decline in

the U.S. residential and commercial consumption more

than offsets consumption growth in the industrial Natural gas can move in range of 260-315 in and electric power sectors. EIA expects natural gas the month of May as weather concerns and consumption in the power sector to increase to 22.8 position of stockpiles will give further Bcf/d in 2015 with the retirement of some coal direction to the prices. Investors are betting plants. seasonably mild weather typical of this time of year

will curb demand for both heating and air

conditioning across much of the U.S. Updated

U.S. Natural Gas Production and Trade weather forecasting models continued to call for

slightly warmer than normal temperatures over the EIA expects natural gas marketed production will

next 15 days. Spring and fall see the weakest grow by an average rate of 3.0% in 2014 and 1.5% in

demand for natural gas in the U.S, as the absence of 2015. Rapid natural gas production growth in the

extreme temperatures curbs demand for heating Marcellus formation is contributing to falling

and air conditioning. Approximately 52% of U.S. natural gas forward prices in the Northeast, which

households use natural gas for heating, according to often fall even with or below Henry Hub prices

the Energy Department.outside of peak winter demand months.

Consequently, some drilling activity may move

away from the Marcellus back to Gulf Coast plays Latest inventory report

such as the Haynesville and Barnett, where prices

are closer to the Henry Hub spot price. Recently natural gas storage in the U.S. rose by 82

billion cubic feet last week, above forecasts for an Natural gas prices will depend upon

increase of 75 billion cubic feet. Inventories rose by weather conditions and power generation

41 billion cubic feet in the same week a year earlier, demand coupled with its consumption

while the five-year average change for the week is a pattern and inventory position in the

build of 58 billion cubic feet.month of May 2014.

Total U.S. natural gas storage stood at an 11-year

low of 981 billion cubic feet. Stocks were 790 billion

cubic feet less than last year at this time and 984

billion cubic feet below the five-year average of

1.965 trillion cubic feet for this time of year.

EN

ER

GY

May 2014

Range

Natural gas

NYMEX $4.45- $4.90 per mmBtu

MCX Rs260-315 per mmBtu

17

EN

ER

GY

May 2014

18

EN

ER

GY

May 2014

SMC Global Securities Limited is proposing, subject to receipt of requisite approvals, market conditions and other considerations, a further public issue of its equity shares and has filed a Draft Red Herring Prospectus (DRHP) with the Securities and Exchange Board of India (SEBI). The DRHP is available on the website of the SEBI at www.sebi.gov.in and the website of the Book Running Lead Managers i.e. Tata Securities Limited at www.tatacapital.com and IL&FS Capital Advisors Limited at www.ilfscapital.com. Investors should note that investment in equity shares involves a high degree of risk. For details please refer to the DRHP and particularly the section titled Risk Factors in the Draft Red Herring Prospectus.

Disclaimer:

This report is for the personal information of the authorized recipient and doesn't construe to be any investment, legal or taxation advice to you. It is only for private circulation and use .The report is based upon information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied upon as such. No action is solicited on the basis of the contents of the report. The report should not be reproduced or redistributed to any other person(s)in any form without prior written permission of the SMC.

The contents of this material are general and are neither comprehensive nor inclusive. Neither SMC nor any of its affiliates, associates, representatives, directors or employees shall be responsible for any loss or damage that may arise to any person due to any action taken on the basis of this report. It does not constitute personal recommendations or take into account the particular investment objectives, financial situations or needs of an individual client or a corporate/s or any entity/s. All investments involve risk and past performance doesn't guarantee future results. The value of, and income from investments may vary because of the changes in the macro and micro factors given at a certain period of time. The person should use his/her own judgment while taking investment decisions.

Please note that we and our affiliates, officers, directors, and employees, including persons involved in the preparation or issuance if this material;(a) from time to time, may have long or short positions in, and buy or sell the commodities thereof, mentioned here in or (b) be engaged in any other transaction involving such commodities and earn brokerage or other compensation or act as a market maker in the commodities discussed herein (c) may have any other potential conflict of interest with respect to any recommendation and related information and opinions. All disputes shall be subject to the exclusive jurisdiction of Delhi High court.

Your valuable feedback will be appreciated

For further queries

Pls. Contact

Sandeep Joon Senior Research Analyst

Phone 011-30111000 Extn - 683

E-mail [email protected]

Supportive team

Pramod Chhimwal Graphic Designer

May 2014