Tax Presentation on Bullions and Jewellery

21

9 th India International Gold Convention 2012 Taxation on gold, silver and platinum- India vs. Rest of the world

Transcript of Tax Presentation on Bullions and Jewellery

9th India International Gold Convention 2012

Taxation on gold, silver and platinum- India vs. Rest of the world

India – Bullion and Jewellery Sector

� India is the world’s largest gold consumer market, due to its jewellery sector which constitutes approximately 80% of total gold demand.

� India has one of the highest savings rate in the world; estimated at around 30% of the total income, of which, approximately 10% is invested in gold.

� Rapid economic growth, urbanisation and inflation continues to stimulate gold demand in the country

� As per 2011 Census, approximately 68.84% India’s population is in rural areas, which does not have sophisticated banking network/ system

� Gold is the second most preferred mode of investment behind bank deposits� Gold is the second most preferred mode of investment behind bank deposits

� With domestic inflation vis-a-vis strong domestic demand for the jewellery, in past 10 years, India has witnessed highest average increase in the price of precious metals, as compared to other major economies of the world

� Gold Price Increase – Average @ 18.5% (www.gold.org)

� Silver Price Increase – Average @ 22.9% (www.gold.org)

This has a spiralling effect on all other economic indicators

2

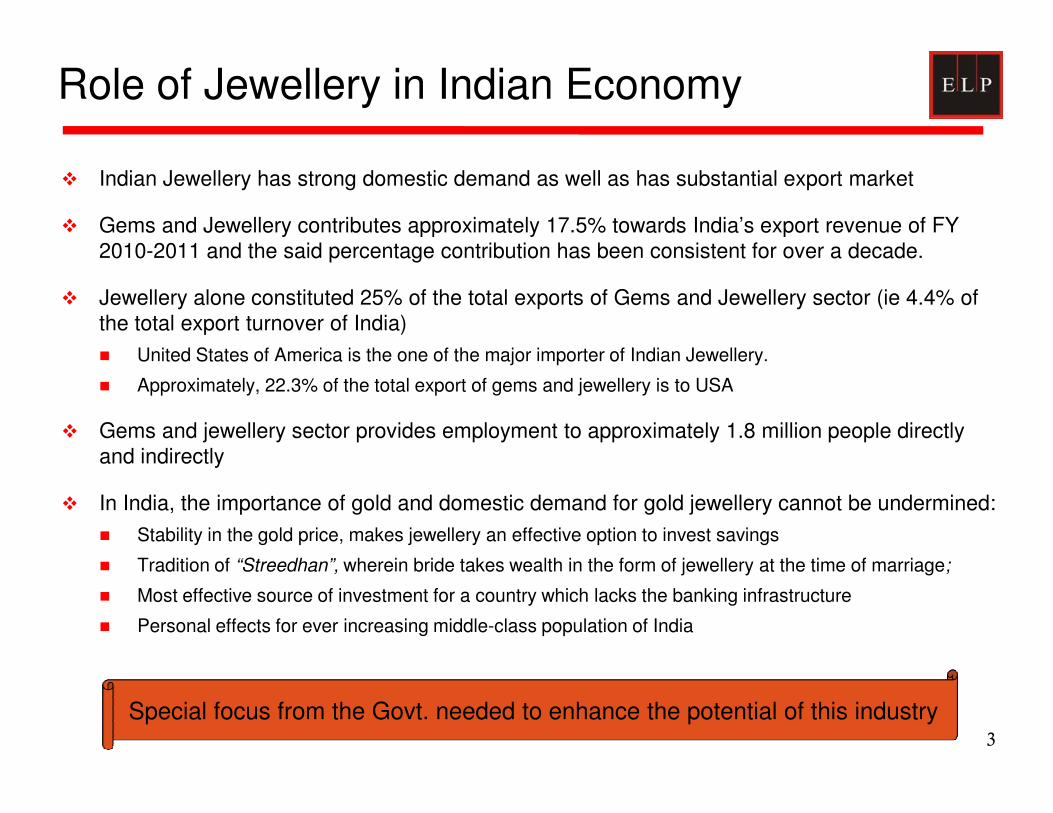

Role of Jewellery in Indian Economy

� Indian Jewellery has strong domestic demand as well as has substantial export market

� Gems and Jewellery contributes approximately 17.5% towards India’s export revenue of FY 2010-2011 and the said percentage contribution has been consistent for over a decade.

� Jewellery alone constituted 25% of the total exports of Gems and Jewellery sector (ie 4.4% of the total export turnover of India)

� United States of America is the one of the major importer of Indian Jewellery.

� Approximately, 22.3% of the total export of gems and jewellery is to USA

� Gems and jewellery sector provides employment to approximately 1.8 million people directly and indirectly

� In India, the importance of gold and domestic demand for gold jewellery cannot be undermined:

� Stability in the gold price, makes jewellery an effective option to invest savings

� Tradition of “Streedhan”, wherein bride takes wealth in the form of jewellery at the time of marriage;

� Most effective source of investment for a country which lacks the banking infrastructure

� Personal effects for ever increasing middle-class population of India

3

Special focus from the Govt. needed to enhance the potential of this industry

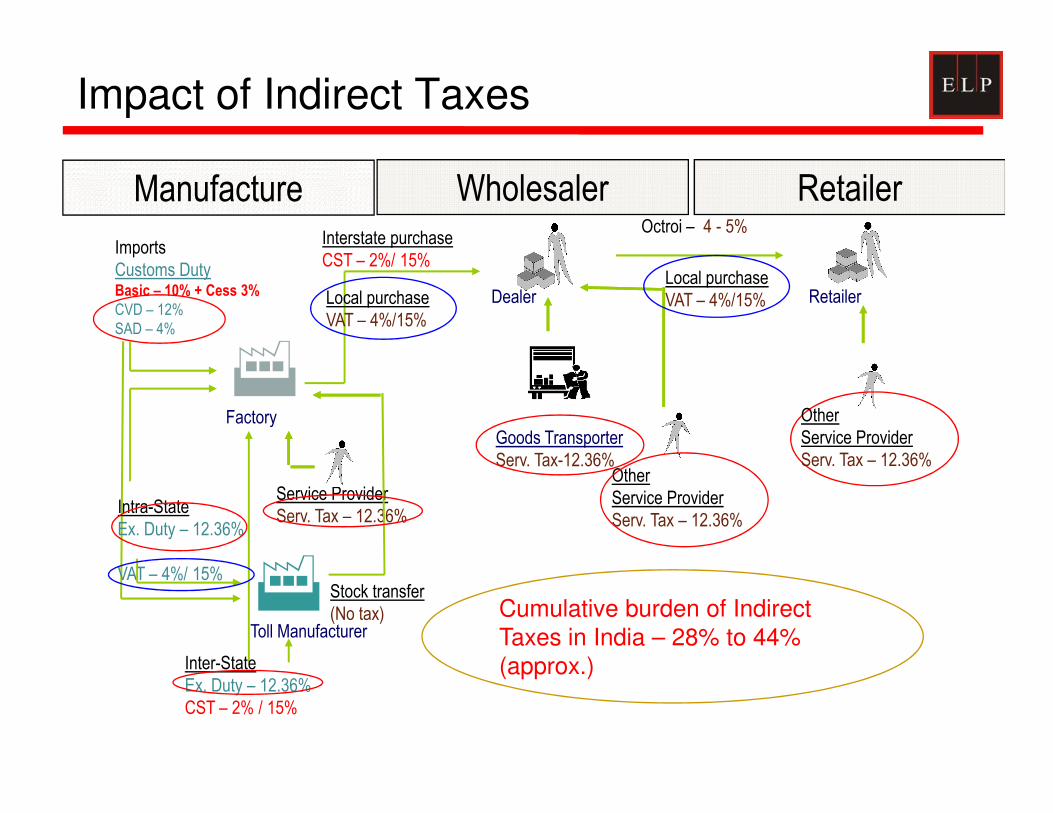

Imports

Customs DutyBasic – 10% + Cess 3%

CVD – 12%

SAD – 4%

Factory

RetailerDealer

�

Interstate purchase

CST – 2%/ 15%

Octroi – 4 - 5%

Impact of Indirect Taxes

Local purchase

VAT – 4%/15%

Local purchase

VAT – 4%/15%

Other

Wholesaler RetailerManufacture

Intra-State

Ex. Duty – 12.36%

VAT – 4%/ 15%

Service Provider

Serv. Tax – 12.36%

Factory

Toll Manufacturer

�

Goods Transporter

Serv. Tax-12.36%

Stock transfer

(No tax)

Inter-State

Ex. Duty – 12.36%

CST – 2% / 15%

Other

Service Provider

Serv. Tax – 12.36%

Other

Service Provider

Serv. Tax – 12.36%

Cumulative burden of Indirect Taxes in India – 28% to 44% (approx.)

Indian Tax Structure for Domestic Transaction

� Excise duty, tax on manufacture, is increased from 10.3% to 12.36%

� Ores (Gold/ Silver) - Excise duty is exempted

� Dore BarsBars with ≤95% Purity (other than tola bar) manufactured from ore/ concentrate/ dore bars

� Gold increased from 1.5% to 3% ad- valorem

� Silver retained at 4% ad- valorem

� Waste/ Scarp of precious metal arising in course of manufacture

� Excise duty is exempted

� Jewellery (whether or not branded)

� Excise duty exemption is available (8 May 2012 to 30 May 2012)

� Gold Jewellery 1% without Cenvat Credit – Silver Jewellery - Nil

� Strips/ sheets/ wires/ plates and foils of gold used in the manufacture of jewellery is exempted

� Strips/ sheets/ wires/ plates and foils of silver is exempted

� Option to be pay Excise duty @ 6%, (especially for units catering to export sector), and avail CENVAT credit/ refund of excise duty/ CVD paid inputs used to manufacture of jewellery

5

Indian Tax Structure for Domestic Transaction

� Bullions/ Coins/ Investment Gold

� Branded Bullion/ Coins – 6% - Avail Cenvat Credit [typically opted by export sector]

� Branded Bullion/ Coins (irrespective of purity) – 1% - No CENVAT on inputs and input services

� Unbranded Bullions/ Coins – Exempted

� Branded Gold Coins (≥99.5% Purity) and Silver coins (≥ 99.9% purity) manufactured from duty paid gold/ silver - Exempted

� Primary Gold (unfinished/ semi-finished bars) Silver (other than mentioned specifically mentioned) / Platinum (unfinished/ semi-finished bars)mentioned) / Platinum (unfinished/ semi-finished bars)

� Gold not converted from ore/ concentrate/ dore bar

� Excise duty is Nil

[Typically covers gold provided by customer]

� Goods manufactured during process of copper smelting from copper ore/ concentrate

� Gold bars (other than tola bars) and Gold Coins ≥99.5% Purity increased from 2% to 3% ad- valorem

� Silver in any form (except silver coins of < 99.9% purity) reduced from 6% to 4%

� Gold arising in course of zinc smelting

� Excise duty is exempted

6

VAT / CST is levied @ 1% on the bullions/ jewellery/ articles of precious metals

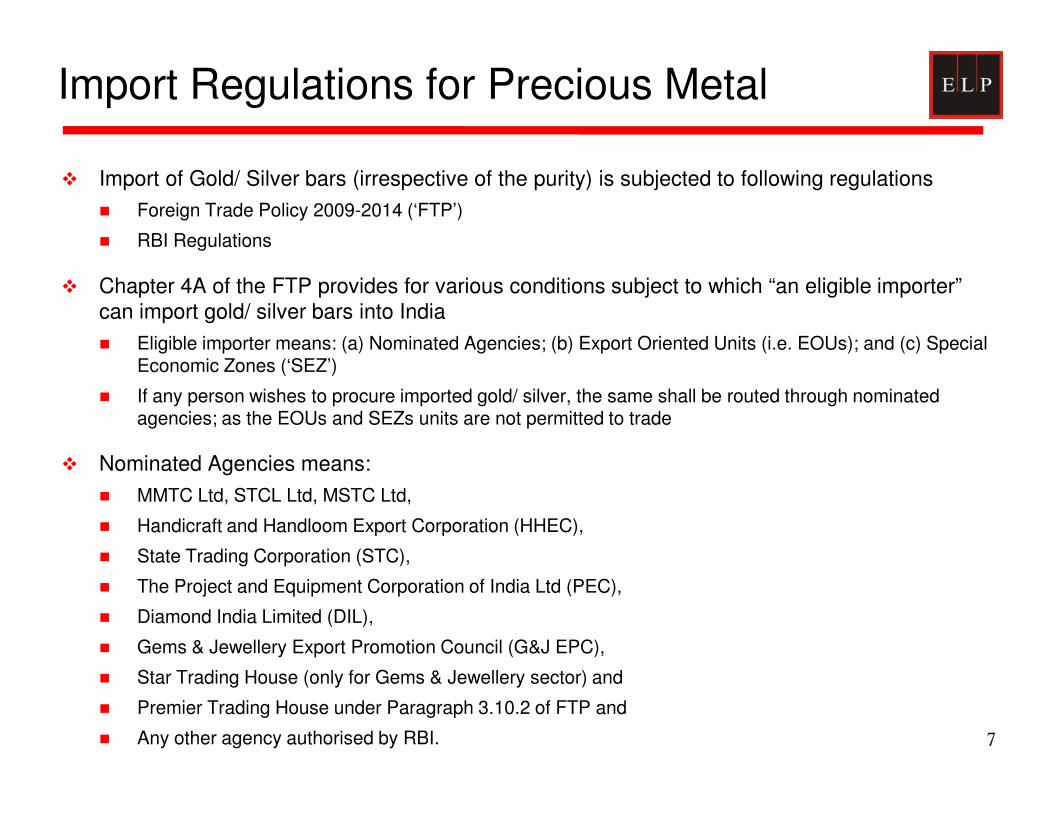

Import Regulations for Precious Metal

� Import of Gold/ Silver bars (irrespective of the purity) is subjected to following regulations

� Foreign Trade Policy 2009-2014 (‘FTP’)

� RBI Regulations

� Chapter 4A of the FTP provides for various conditions subject to which “an eligible importer” can import gold/ silver bars into India

� Eligible importer means: (a) Nominated Agencies; (b) Export Oriented Units (i.e. EOUs); and (c) Special Economic Zones (‘SEZ’)

� If any person wishes to procure imported gold/ silver, the same shall be routed through nominated agencies; as the EOUs and SEZs units are not permitted to trade

� Nominated Agencies means:

� MMTC Ltd, STCL Ltd, MSTC Ltd,

� Handicraft and Handloom Export Corporation (HHEC),

� State Trading Corporation (STC),

� The Project and Equipment Corporation of India Ltd (PEC),

� Diamond India Limited (DIL),

� Gems & Jewellery Export Promotion Council (G&J EPC),

� Star Trading House (only for Gems & Jewellery sector) and

� Premier Trading House under Paragraph 3.10.2 of FTP and

� Any other agency authorised by RBI. 7

Indian Tax Structure for Imports

� Customs duty is levied on tariff value

� Gold - $527 per 10 grams ( ~ Rs 29,500)

� Silver - $913 per 1 kilo gram ( ~ Rs 51,000)

� Gold ore/ concentrate used in manufacture of gold [Free to be imported]

� BCD: Nil – CVD : 2% (increased CVD rate from 1% to 2%)

[Imported by anyone without any restriction]

� Dore barsBars with ≤95% Purity for manufacturing bars of minimum purity - 99.5%(gold) & 99.9%(Silver) Bars with ≤95% Purity for manufacturing bars of minimum purity - 99.5%(gold) & 99.9%(Silver)

� Gold – BCD : Nil – CVD : 2% (increased CVD rate from 1% to 2%)

� Silver – BCD : Nil – CVD : 3% [no change]

[Imported by actual user. Charge being CVD, CENVAT credit can be availed]

� Bullions/ Coins- Investment GoldGold bar/ coin having gold content ≥ 99.5% or Silver in any form including coin having silver content ≥ 99.9%, but excludes jewellery

� Gold – BCD : 4% - CVD - Nil (increased BCD rate from 2% to 4%)

� Silver - BCD : 6% - CVD – Nil [no change]

[Imported by eligible persons]

[These rates are commensurate with local excise duty rate]

8

Indian Tax Structure for Imports

� Platinum (other than jewellery)

� BCD 4% + CVD as applicable – (increased from 2% to 4%)

[Imported by any persons]

� Jewellery of gold, silver or platinum

� BCD 10% + SAD 1%

� CVD is exempted as corresponding excise is exempted

[Imported by any person]

[Excise duty on jewellery manufactured by EOU and cleared to DTA in accordance with FTP is:

� For Plain Gold Jewellery - increased from 5% to 10% ad valorem

� For Studded Gold Jewellery - 5% ad valorem

� For Plain Silver Jewellery - 6% ad valorem]

� Special Additional Duties of customs (‘SAD’) is exempted for all items of gold/ sliver/ platinum other than jewellery

� Since, items other than jewellery is imported through nominated agency, such agencies would be required to charge VAT on re-sale accordingly, SAD is not changed

� Further, since jewellery could be purchased by traded directly, each purchase shall be subjected to SAD @ 1%, which is equivalent to VAT/ CST rate

9

Reporting Requirement

� India, like other major economies, has introduced reporting of the transaction of precious metal, to track unaccounted monies,

� Purchaser of bullions or jewellery of Rs 5 lacs or more during a Financial Year needs to furnish his Permanent Account Number (‘PAN’) issued under the Income tax Act, 1961 (‘IT-Act’)

� Dealers are required to collect all such information and quote the same on the Invoice issued to such Purchaser

� However, there is no added compliance requirement on part of Dealer (ie No Need to file Annual Information Statement Under Rule 114E of the IT Act)

� However, there is no provision / requirement, which restrict quantum of gold possess by an � However, there is no provision / requirement, which restrict quantum of gold possess by an individual

� Also, there is no requirement to disclose the quantum of gold owned and possessed with Income tax authorities

� Typically, bullion and jewellery sectors, are likely areas which may need to undergo rigorous reporting requirements and third party enquires from tax departments

10

International Tax Laws – Bullions & Jewellery

Countries Taxation Provision

USA Silver/ Gold/ Platinum (Customs duty)• Unwrought Bullions/ dore – Nil*• Bar with ≥ 99.5% purity – Nil*

Bar with lesser purity • Silver – 3%; Gold – 4.1%• Platinum - Nil

Jewellery - 5% to 13.5%• Gold, Silver, Platinum

Articles – 2.7% to 7.9%• Gold, Silver, Platinum

VAT (varies from State to State)• Authorised to collect 3%

over and above normal @ • Eg New York has normal

@ of 4%, accordingly VAT is 7% (4%+3%)

Commentsvis-a-vis

• US, as compared to Indian, is far more developed and have efficient organised banking channel. Accordingly, investment in Bullions/ Coins is preferred over jewellery. In US, jewellery is typically vis-a-vis

IndiaAccordingly, investment in Bullions/ Coins is preferred over jewellery. In US, jewellery is typically viewed as article of personal effect and not as investment. Hence, jewellery attract higher tax burden as compared to bullions

• Articles made of gold or alloys thereof are prohibited importation into the United States if the gold content is one half carat divergence below the indicated fineness. In the case of articles made of gold or gold alloy, including the solder and alloy of inferior fineness, a one-carat divergence below the indicated fineness is permitted.*

• Restrictions on the purchase, holding, selling, or otherwise dealing in gold were removed as of December 31, 1974, and gold may be imported subject to the usual CBP entryrequirements.Unofficial gold coin must be marked with the country of origin*

11

* We have relied on the data available on the government website with www.cbp.gov. It is advisable not to rely on the data and instead obtain specific advise on the rates while analysing taking any commercial decision

International Tax Laws – Bullions & Jewellery

Countries Taxation Provision

Euro Zone(including UK)

Bullions/ Investment Gold• Gold Bullions irrespective of purity is exempted from

Customs duty • Bullions ≥ 99.5% purity is exempted from VAT

• Import of Silver/ Platinum bullions is tax free is UK

VAT$ is applicable at standard rate of 20%• Other Gold with lesser purity• Bullions of Silver/ Platinum

Jewellery• Import of jewellery in UK is taxed

at 2.5%• VAT is applicable at standard rate

of 20%

• Bullions of Silver/ Platinum

Commentsvis-a-visIndia

• In order to prevent tax frauds, in certain circumstances, Member States may designate purchaser as the person liable to pay VAT (ie reverse charge)

• UK, as compared to Indian, is far more developed and have efficient organised banking channel. Accordingly, investment in Bullions/ Coins is preferred over jewellery. In UK, although Bullion is exempted from customs duty and VAT, jewellery is typically viewed as article of personal effect and levied VAT @ 20% standard rate.

12

* We have relied on the data available on the government website with http://customs.hmrc.gov.uk and $ Directive (EC) No 1998/80EC available on http://europa.eu/legislation_summaries/taxation/I31012_en.htm . It is advisable not to rely on the data and instead obtain specific advise on the rates while analysing taking any commercial decision

International Tax Laws – Bullions & Jewellery

Countries Taxation Provision

China Bullion• Customs duty on import of bullions

into China is exempted• However, semi-finished bars are

subjected to 10.5% of customs duty

• Consumption tax is not levied on Bullions

• VAT is levied at 17% on sale of

Jewellery• Customs duty on Jewellery is as under

• Silver - 20%• Gold/ Platinum – 27.5% / 35%

• Consumption tax on jewellery of gold, silver & platinum is levied @ 5% and the same is payable by producer of the jewellery

• VAT is levied at 17% on sale of Jewellery• VAT is levied at 17% on sale of

bullions

Comments from India perspective

India has been the leading gold imported/ consumer in the world, especially due to presence of largest jewellery market of the world.

Jewellery constitutes approximately 78% - 80% of the total gold demand, which is approximately 0.5 grams of gold on per capita basis.

With an increase in the import duty rate from 3% to 4% in India, with corresponding reduction in the duty rate in China, the demand of gold import in India is expect to reduce, ensuring China’s path to No 1 ranking in gold consumption.

13

* We have relied on the data available on the government website with http://english.tax861.gov.cn and www.wto.org . It is advisable not to rely on the data and instead obtain specific advise on the rates while analysing taking any commercial decision

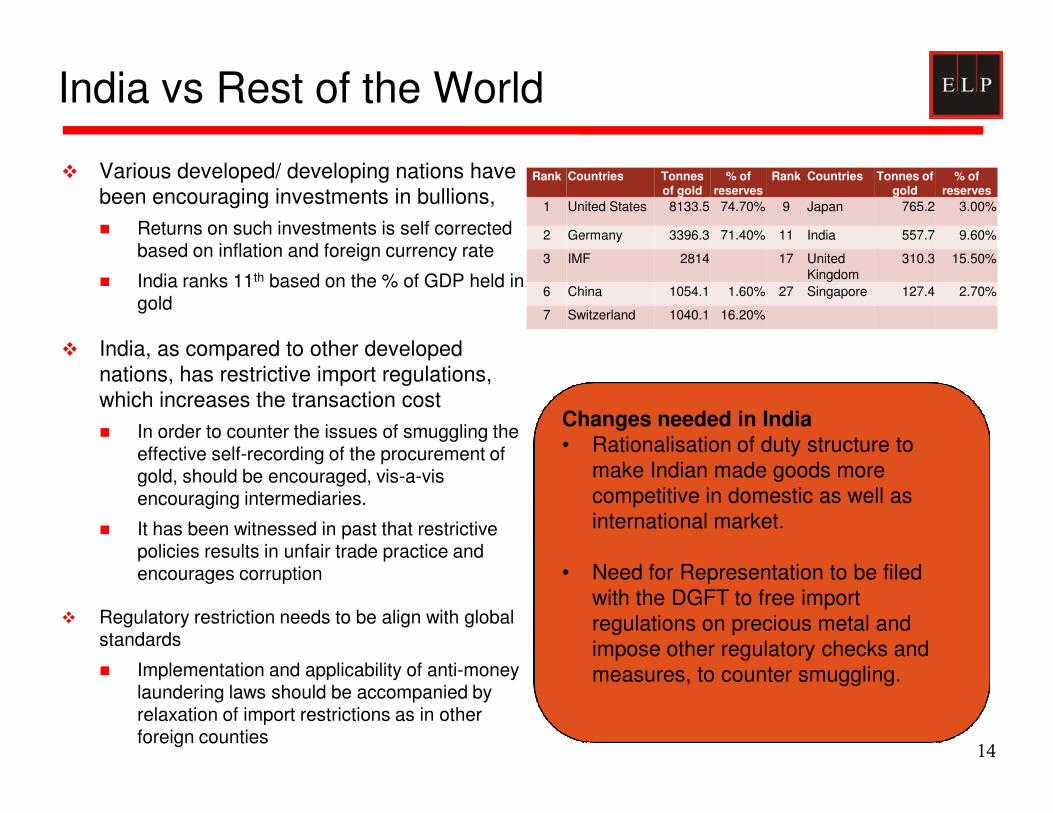

India vs Rest of the World

� Various developed/ developing nations have been encouraging investments in bullions,

� Returns on such investments is self corrected based on inflation and foreign currency rate

� India ranks 11th based on the % of GDP held in gold

� India, as compared to other developed nations, has restrictive import regulations, which increases the transaction cost

Rank Countries Tonnesof gold

% of reserves

Rank Countries Tonnes of gold

% of reserves

1 United States 8133.5 74.70% 9 Japan 765.2 3.00%

2 Germany 3396.3 71.40% 11 India 557.7 9.60%

3 IMF 2814 17 United Kingdom

310.3 15.50%

6 China 1054.1 1.60% 27 Singapore 127.4 2.70%

7 Switzerland 1040.1 16.20%

Changes needed in Indiawhich increases the transaction cost

� In order to counter the issues of smuggling the effective self-recording of the procurement of gold, should be encouraged, vis-a-visencouraging intermediaries.

� It has been witnessed in past that restrictive policies results in unfair trade practice and encourages corruption

� Regulatory restriction needs to be align with global standards

� Implementation and applicability of anti-money laundering laws should be accompanied by relaxation of import restrictions as in other foreign counties

14

Changes needed in India• Rationalisation of duty structure to

make Indian made goods more competitive in domestic as well as international market.

• Need for Representation to be filed with the DGFT to free import regulations on precious metal and impose other regulatory checks and measures, to counter smuggling.

GST Proposed Structure

� Dual and Concurrent Goods and Services Tax (‘GST’)Federal Government may legislate – Central GST;

� Central Excise duty, Service tax and CST to be abolished

� Basic Customs duties to be continued on import of goods- ACD and SACD may be replaced by creditable GST

State Government may legislate – State GST;

� To subsume VAT, Entry tax - No clarity on Octroi, other levies – the same may continue

� Introduction of uniform levy, whereby following aspects shall be same across all States� Introduction of uniform levy, whereby following aspects shall be same across all States

� Tax Base; valuation, GST Rates, Credit Rules

� Almost all goods and services are expected to be taxable under the GST regime expect few specific goods

� Inter-state transaction would be subject to Integrated GST (‘IGST’) which shall be the total of CGST and SGST

� IGST will combine CGST and SGST

� May be levied by the Centre in the origin State

� Tax equivalent to SGST passed over to destination State

� via a clearing house mechanism15

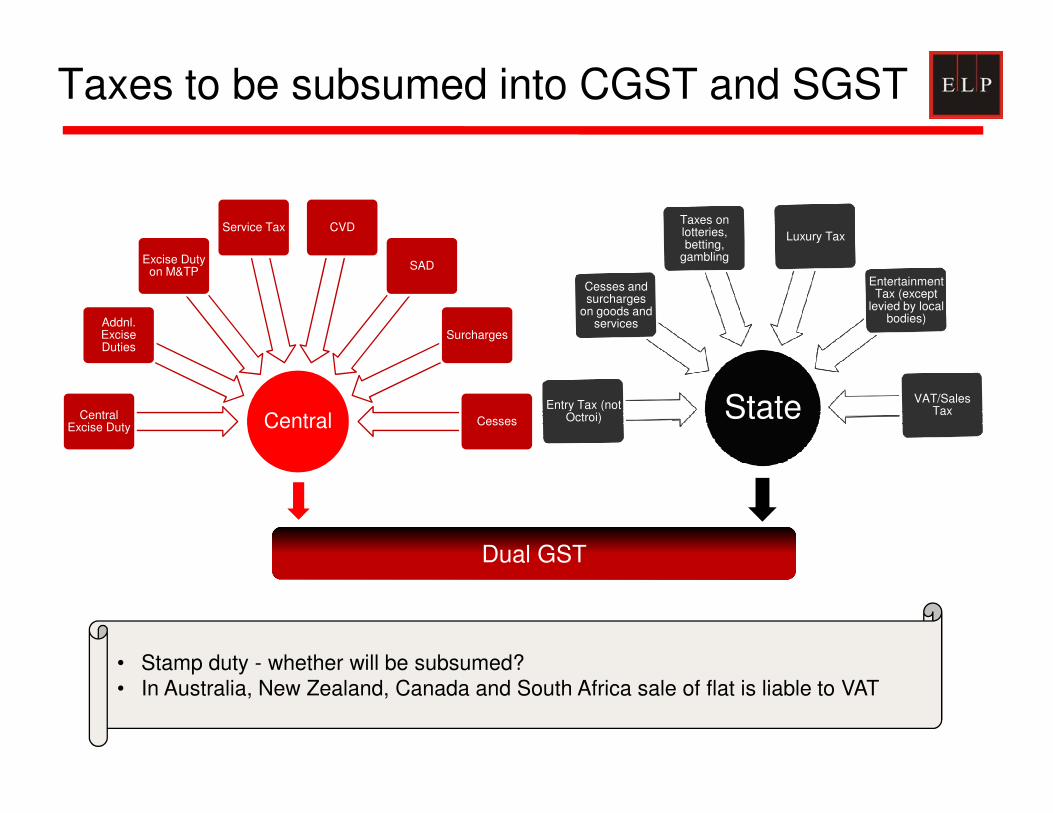

Taxes to be subsumed into CGST and SGST

Addnl. Excise Duties

Excise Duty on M&TP

Service Tax CVD

SAD

Surcharges

StateEntry Tax (not

Cesses and surcharges

on goods and services

Taxes on lotteries, betting,

gambling

Luxury Tax

Entertainment Tax (except

levied by local bodies)

VAT/Sales Tax

CentralCentral Excise Duty

CessesStateEntry Tax (not

Octroi)Tax

Dual GST

• Stamp duty - whether will be subsumed?• In Australia, New Zealand, Canada and South Africa sale of flat is liable to VAT

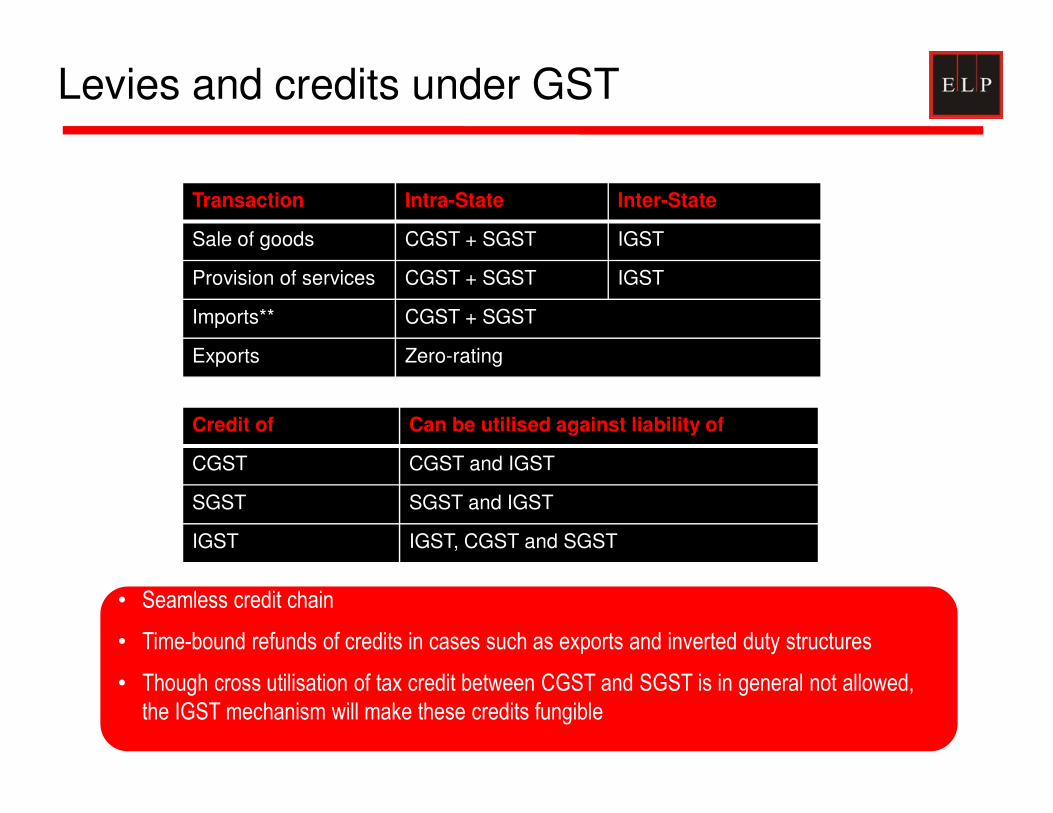

Levies and credits under GST

Transaction Intra-State Inter-State

Sale of goods CGST + SGST IGST

Provision of services CGST + SGST IGST

Imports** CGST + SGST

Exports Zero-rating

Credit of Can be utilised against liability of

CGST CGST and IGST

SGST SGST and IGST

IGST IGST, CGST and SGST

• Seamless credit chain

• Time-bound refunds of credits in cases such as exports and inverted duty structures

• Though cross utilisation of tax credit between CGST and SGST is in general not allowed,

the IGST mechanism will make these credits fungible

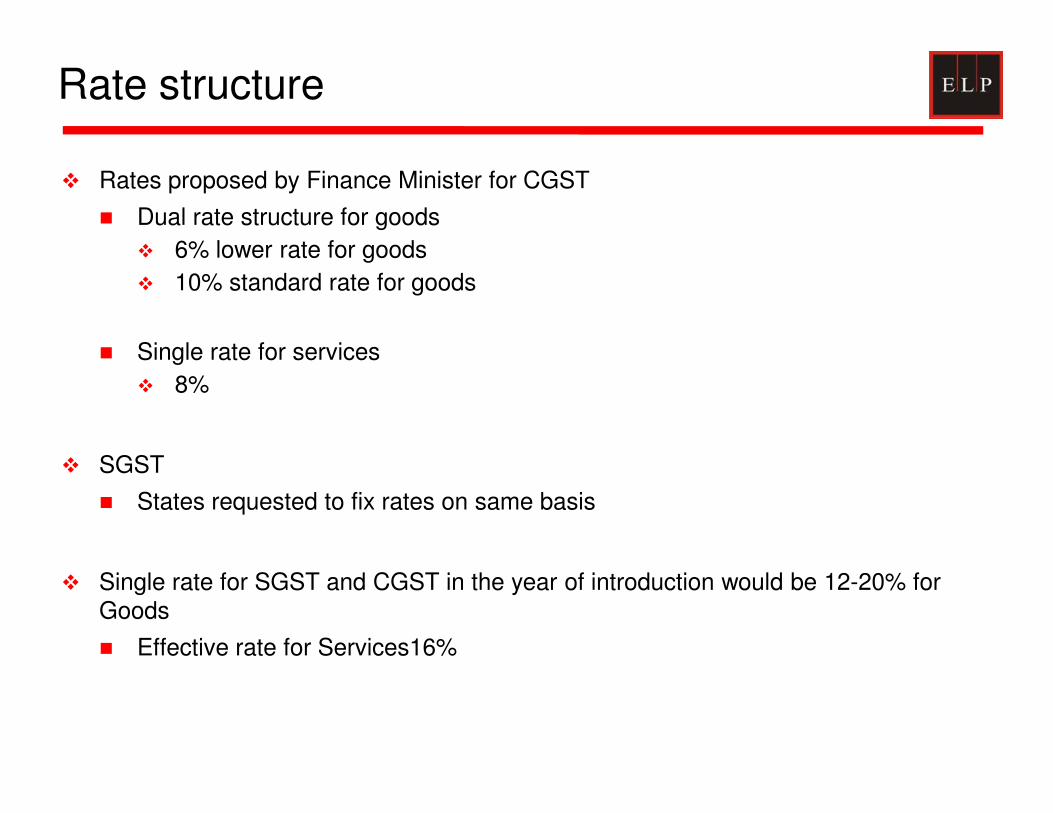

Rate structure

� Rates proposed by Finance Minister for CGST

� Dual rate structure for goods

� 6% lower rate for goods

� 10% standard rate for goods

� Single rate for services

� 8%

� SGST

� States requested to fix rates on same basis

� Single rate for SGST and CGST in the year of introduction would be 12-20% for Goods

� Effective rate for Services16%

Advent of GST

� GST regime, is absolutely essential to curtail cascading effect of domestic taxes

� Under GST regime, total tax incidence across the sectors is expected to be around 16%/ 20%, and there is no exception for bullions and jewellery

� GST does not provide for concessional rate of 1%

� In most of the developed/ rapidly developing economies, GST/ VAT on bullion and jewellery, is either exempted or at concessional rates

Further, vide proposal TN/MA/W/61/ dated 21 September 2005 (as amended from time to time) various � Further, vide proposal TN/MA/W/61/ dated 21 September 2005 (as amended from time to time) various signatories to World Trade Organisation has proposed free international trade on bullions and jewellery, in following phases

� To reduced the existing customs duty to [x%] in [y] number of years in equal instalments

� Members may opt to retain [x%] for additional period of [z] years without further reducing the rates

� Complete duty exemption on import of gems and jewellery after the end of [z] years

� The said proposal is under consideration for various other members of WTO

� There are no comments from India, however, any acceptance would result in reduction of Customs Duty on import of bullions into India

� Under GST regime high tax on bullion, would impact the sustainability of the sector in India

19

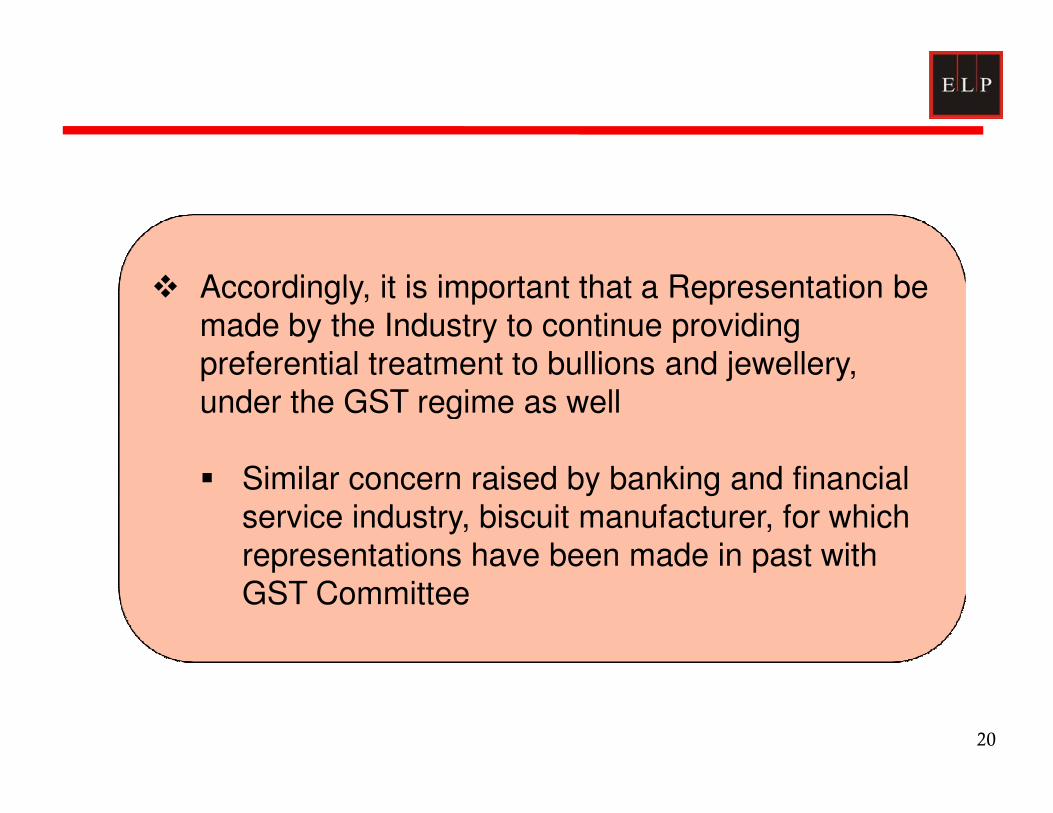

� Accordingly, it is important that a Representation be made by the Industry to continue providing preferential treatment to bullions and jewellery, under the GST regime as well

20

under the GST regime as well

� Similar concern raised by banking and financial service industry, biscuit manufacturer, for which representations have been made in past with GST Committee

Mumbai1502, A Wing, Dalamal Towers, Nariman Point, Mumbai 400 021

Phone: + 91 22 6636 7000, Fax: + 91 22 6636 7172

Delhi405-406, 4th floor, World Trade Centre, Barakhamba Lane, New Delhi 110 001

Phone: + 91 11 4152 8400, Fax: + 91 11 4152 8404

Ahmedabad801, Abhijeet III, Mithakali Six Roads, Ellisbridge, Ahmedabad 380 006

Phone: +91 79 6605 4480 / 8, Fax: +91 79 6605 4482

Pune7th Floor, Suyog Fusion, 97, Dhole Patil Road, Pune 411001.

21