A Conversation about Medicare Part A,B,C and D - A Concise Understanding Of Medicare In 18 Slides!

Upload

jelutharasCategory

view

388download

2description

THE FUTURE OF LONDON SINGLE CONVERSATIONBREAKFAST SERIES:

LAUNCH EVENTTuesday 15 June 2010

Barnet’s Borough Investment Plan: How was it for us?

Presented by: Pam WharfeHead of Housing & Environmental HealthLondon Borough of Barnet

LB Barnet: How was it for us?

What we are going to cover…

Barnet’s context How did we put the plan together?What has worked well/less well?A flavour of what is in our plan…

Barnet’s context

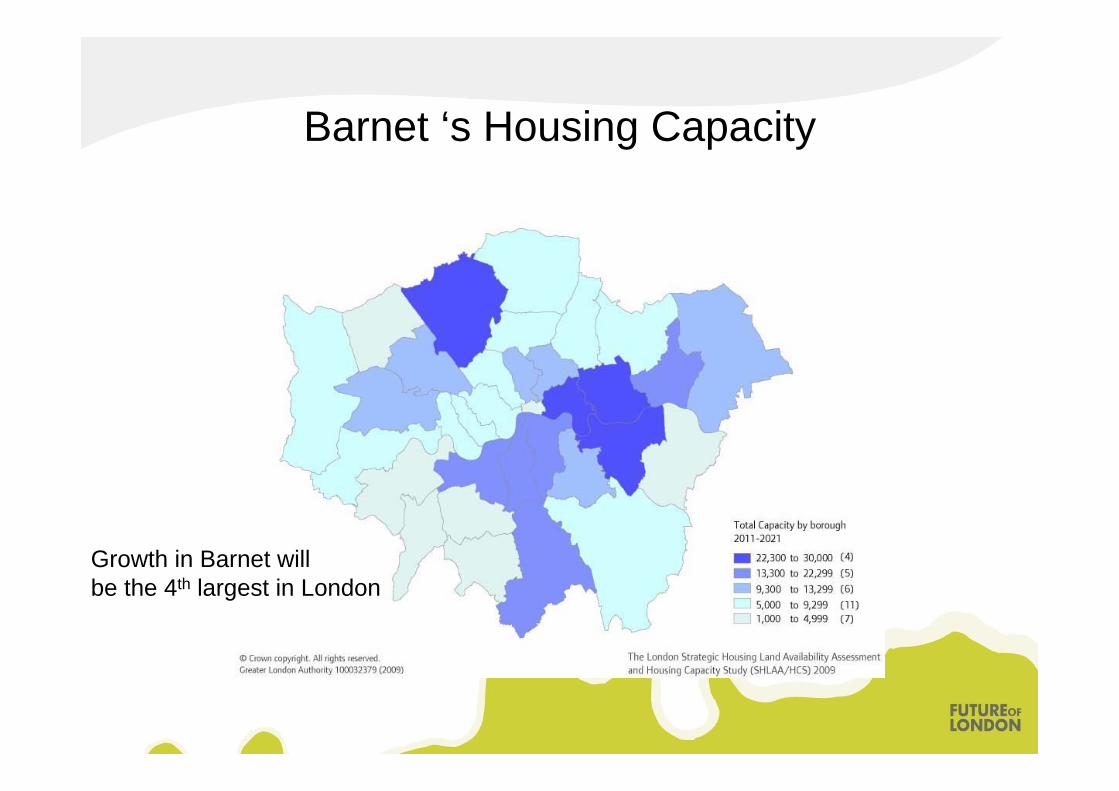

Barnet ‘s Housing Capacity

Growth in Barnet willbe the 4th largest in London

Barnet’s offer

• A place people want to live

• The scale of the opportunity

• Deliverability

• Capacity, innovation and performance“This is about building places, and homes

in places where people want to live”B.Kerslake (2009)

How did we put the plan together?

How did we put the plan together?

• Worked with the HCA from the start• That helped us understand each other’s

perspectives• We commissioned Navigant to work with

us to produce the document– They worked with all stakeholders to

understand their issues

What worked well/less well?

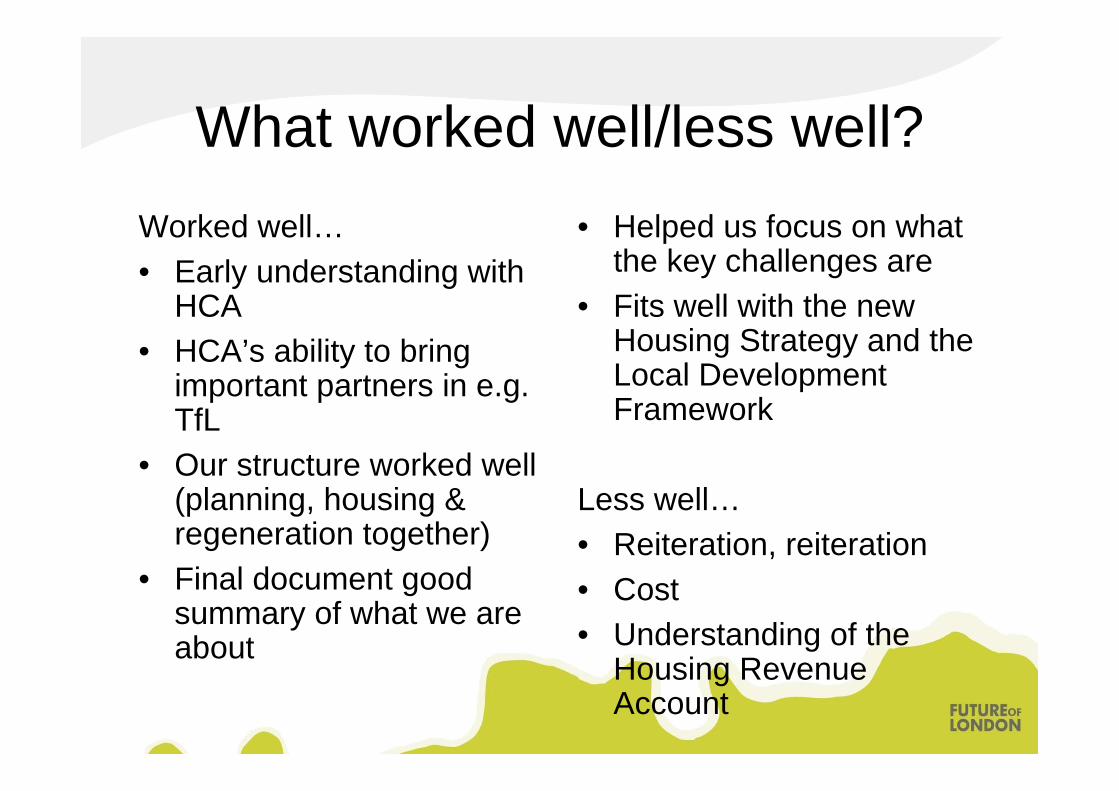

What worked well/less well?Worked well…• Early understanding with

HCA• HCA’s ability to bring

important partners in e.g. TfL

• Our structure worked well (planning, housing & regeneration together)

• Final document good summary of what we are about

• Helped us focus on what the key challenges are

• Fits well with the new Housing Strategy and the Local Development Framework

Less well…• Reiteration, reiteration• Cost• Understanding of the

Housing Revenue Account

A flavour of what’s in our plan…

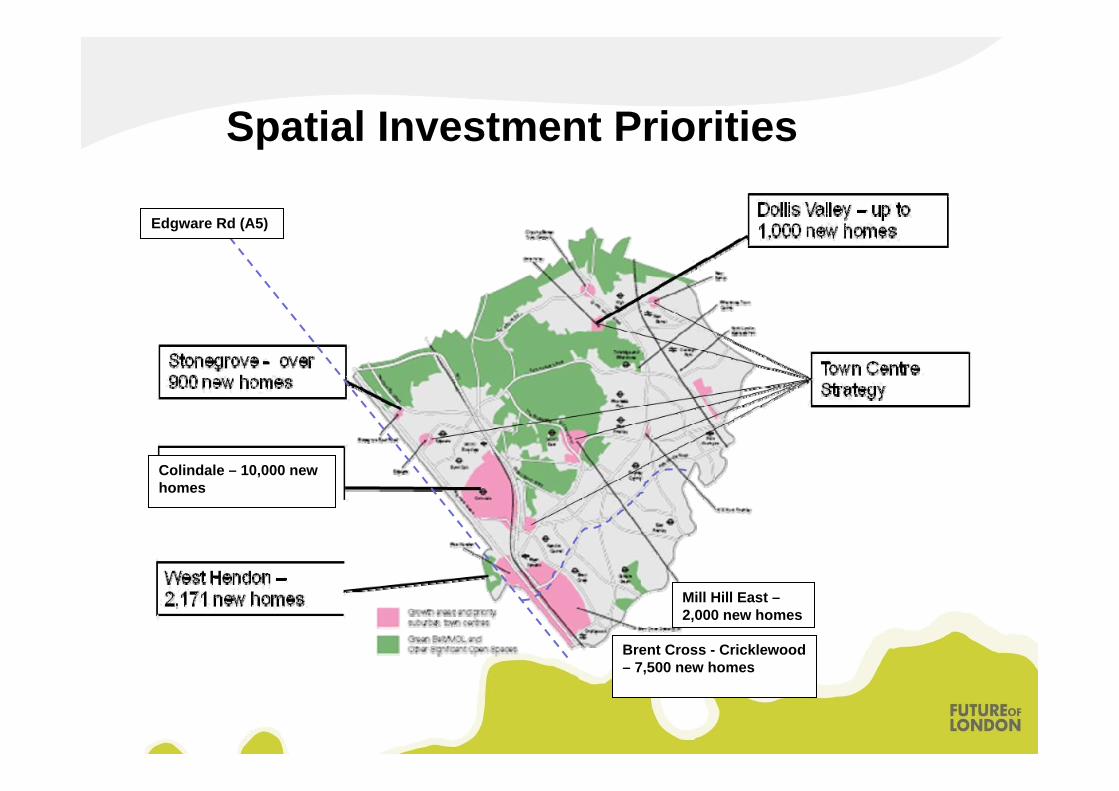

Spatial Investment Priorities

Mill Hill East –2,000 new homes

Brent Cross - Cricklewood – 7,500 new homes

Edgware Rd (A5)

Colindale – 10,000 new homes

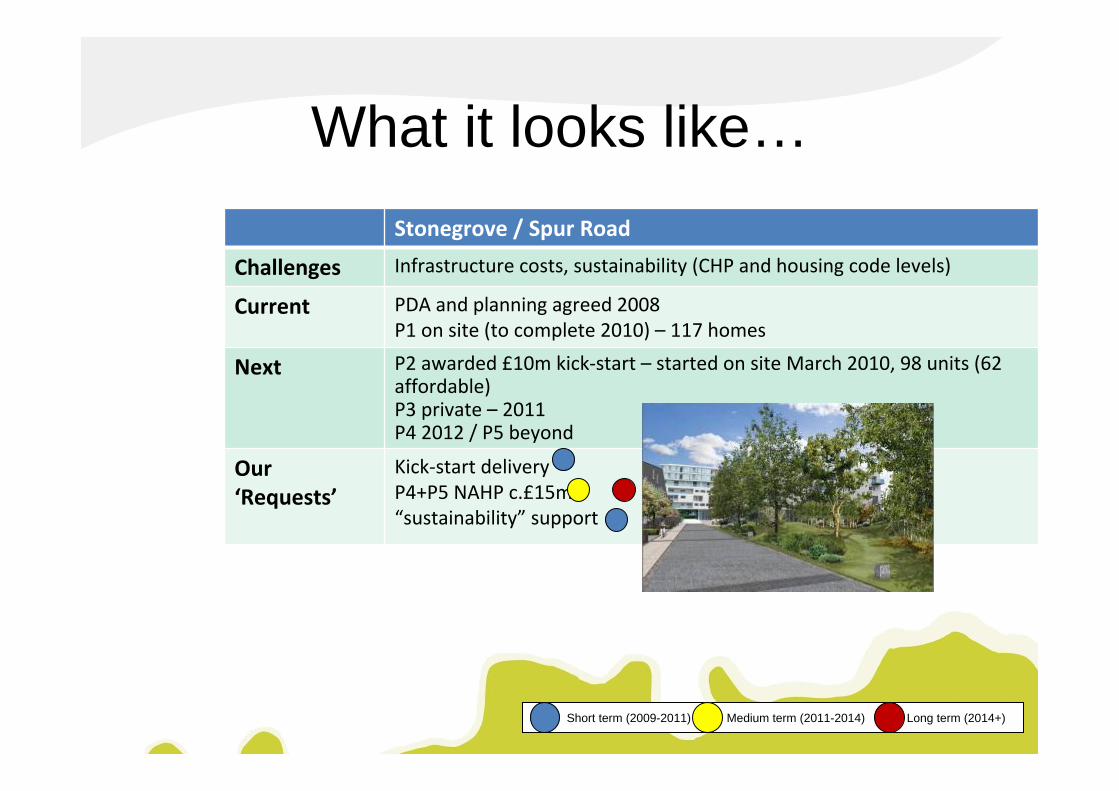

What it looks like…Stonegrove / Spur Road

Challenges Infrastructure costs, sustainability (CHP and housing code levels)

Current PDA and planning agreed 2008P1 on site (to complete 2010) – 117 homes

Next P2 awarded £10m kick‐start – started on site March 2010, 98 units (62 affordable)P3 private – 2011P4 2012 / P5 beyond

Our ‘Requests’

Kick‐start deliveryP4+P5 NAHP c.£15m“sustainability” support

Short term (2009-2011) Medium term (2011-2014) Long term (2014+)

Delivering for the Future – Thematic priorities

• Decent Homes & Beyond (retro-fitting)• Reducing temporary accommodation levels (+ on estates)• HRA Reform and ongoing funding• Sheltered Plus /extra care/supported housing• LABV – Granville Road, Town Centres• A new Private Rented Sector model

Local investment planning

Reflections on progress

Future of LondonJim Bennett, 15 June 2010

Single Conversation

Replaces previous ‘multiple conversations’

Main business process for the HCA

Focus on places – delivering local priorities

Joint approach with local authorities and partners

Comprehensive coverage of housing and regeneration

Progress

c160 Single Conversation areas

Conversations started in 157

24 LIPs agreed

Some delayed by election

Independent Interim Evaluation

Interim evaluation - purpose

Provide feedback from local authorities and partners on the process

Provide an overview of how the model is being applied in different regions and circumstances

Identify barriers and challenges in implementation

Provide early evidence of the benefits achieved to date, and further benefits that could be realised

Inform further implementation of the business model

Inform our Spending Review discussions with CLG / HMT

Good progress

Strong support from local authorities and partners

Consistent with wider direction of travel for public policy

Already influencing investment decisions on current programmes

Local Investment Plans (LIPs) effectively support local authorities’ strategies

Initial focus on housing and regeneration; expected to develop into comprehensive approach to place shaping

Benefits

Harnessing HCA & other resources for communities and places

Place focus brings coherence of partners for efficiencies

Long term public investment management can help leverage

Overall strategic approach increases performance and impact

Challenges

Inherited programmes, flexibilities, uncertainties

Balance of national and local priorities

Guidance and information – interpretation– flexibility– inconsistency

Capacity and track record - progress is faster with strategic partnerships eg MAAs

Milestones for starts exceeded, but no target date for completing all LIPs

Recommendations

More consistencyMore certainty in funding and flexibilityEncourage sub-regional partnerships / two tier approachEncourage LAs to bring in delivery partners earlierRefresh definition as holisticClarify appraisals of LIPsPeer assessment

Responding to the reflections

Define core elements for LIPs for more consistency while keeping local flexibility

Internal peer assurance of early LIPs for appraisal and sharing good practice

Aim to complete Local Investment Plans by March 2011.

Community engagement

Statutory duties

Housing Supply

Prioritisation –using an

Appraisal based approach

Outputs and outcomes

EconomicGrowth

Core Elements

Core elements

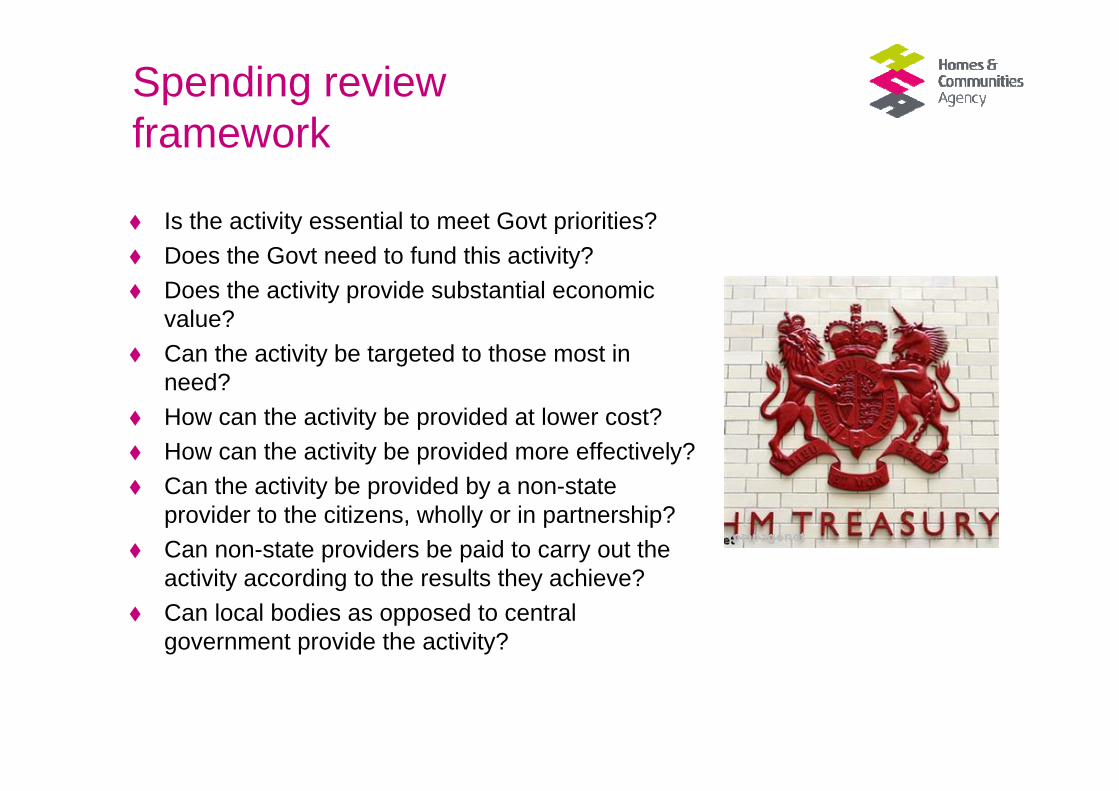

Spending review framework

Is the activity essential to meet Govt priorities?Does the Govt need to fund this activity?Does the activity provide substantial economic value?Can the activity be targeted to those most in need?How can the activity be provided at lower cost?How can the activity be provided more effectively?Can the activity be provided by a non-state provider to the citizens, wholly or in partnership?Can non-state providers be paid to carry out the activity according to the results they achieve?Can local bodies as opposed to central government provide the activity?

Next

Publish interim evaluation

Implement core elements and peer assurance process

Continue to deliver localistapproach, but have an eye for Spending Review

Delegated Delivery – what’s on offer?

Presented by: Stephen McDonaldAD RegenerationLondon Borough of Hackney

Contents

• Hackney context

• So what is the Delegated Delivery Pilot (DDP) all about

• Emerging ideas

• Colville – the challenge

• Next steps

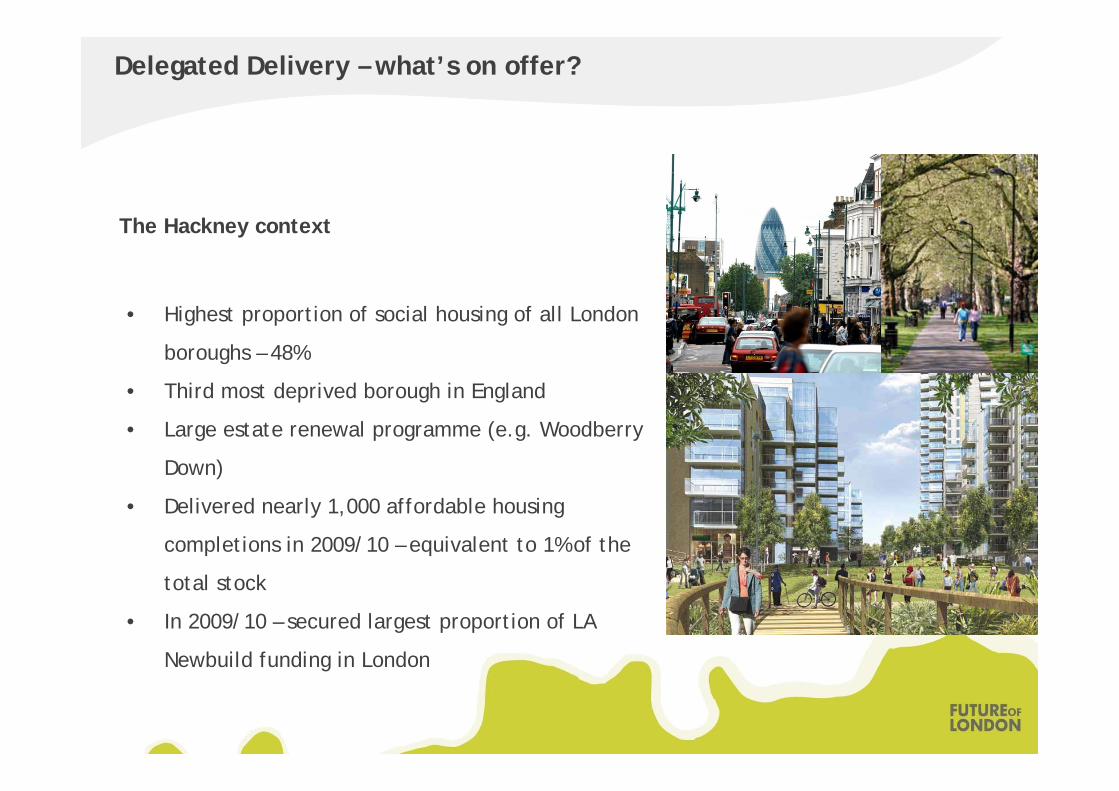

Delegated Delivery – what’s on offer?

The Hackney context

• Highest proportion of social housing of all London

boroughs – 48%

• Third most deprived borough in England

• Large estate renewal programme (e.g. Woodberry

Down)

• Delivered nearly 1,000 affordable housing

completions in 2009/10 – equivalent to 1% of the

total stock

• In 2009/10 – secured largest proportion of LA

Newbuild funding in London

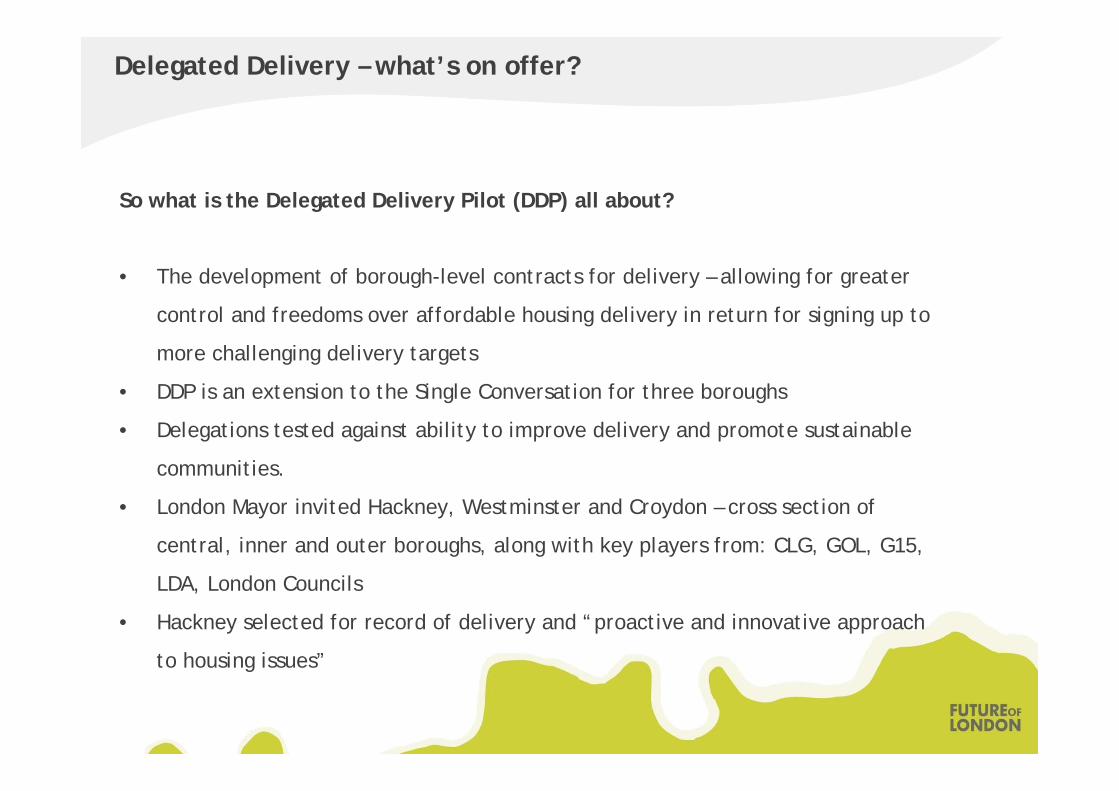

Delegated Delivery – what’s on offer?

So what is the Delegated Delivery Pilot (DDP) all about?

• The development of borough-level contracts for delivery – allowing for greater

control and freedoms over affordable housing delivery in return for signing up to

more challenging delivery targets

• DDP is an extension to the Single Conversation for three boroughs

• Delegations tested against ability to improve delivery and promote sustainable

communities.

• London Mayor invited Hackney, Westminster and Croydon – cross section of

central, inner and outer boroughs, along with key players from: CLG, GOL, G15,

LDA, London Councils

• Hackney selected for record of delivery and “proactive and innovative approach

to housing issues”

Delegated Delivery – what’s on offer?

Emerging ideas

Each borough has produced an initial paper on their designated topic, and will lead on developing proposals with partners on the Steering Group.

Boroughs to highlight how proposals will increase delivery, improve efficiency, and tailor delivery to local circumstances.

• Intermediate housing offer (Westminster) – provision of bespoke intermediate housing

products, commissioned at the local level

• Selecting and commissioning delivery partners (Croydon) – working with HCA, CLG and

G15 to develop proposals

• Estate renewal (Hackney) – investment flexibility e.g. HCA providing subsidy to

purchase leasehold interests at the outset, based on returns in later phases of a

project.

Delegated Delivery – what’s on offer

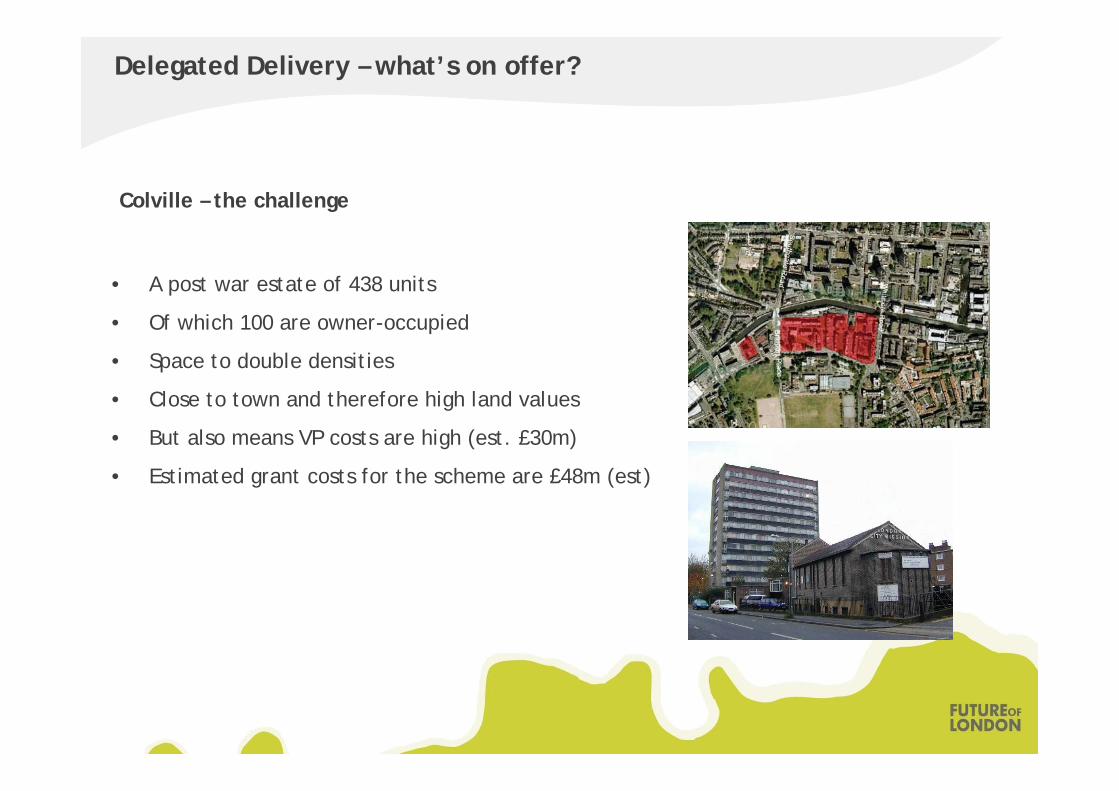

Colville – the challenge

• A post war estate of 438 units

• Of which 100 are owner-occupied

• Space to double densities

• Close to town and therefore high land values

• But also means VP costs are high (est. £30m)

• Estimated grant costs for the scheme are £48m (est)

Delegated Delivery – what’s on offer?

Next Steps

The timetable is designed to enable individual borough contracts to come into operation from April 2011. At this point the Pilot will be rolled out to other local authorities.

• Now - September 2010 - draft borough contracts developed

• 22 September 2010 – draft borough contracts reviewed by HCA London Board

• September to March 2011 – finalise borough contracts and test flexibilities

• April 2011 – potential to roll out Pilot to other local authorities

Delegated Delivery – what’s on offer?

.

Future Seminars:• 27 July• 7 September• 19 October

Suggested topics (no. of requests)

• New Delivery Models (6)

• Intermediate Tenures (6)

• Infrastructure Investment (4)

• Family Housing (3)

• BIP Best Practice (2)

• Working with Stakeholders (2)

• Some other Suggestions:

Housing quality and viability, Unlocking private sites, Supported Housing, Total Place, Role of East London in housing delivery, Institutional Investment, Sustainability and CO2