Sadbhav Engineering Limited Relative : Overweight...

12

November 15, 2017 Analyst: Devam Modi [email protected] (+91 – 90999 87467) Page 1 of 13 Before reading this report, you must refer to the disclaimer on the last page. Sadbhav Engineering Limited Absolute : LONG Relative : Overweight 2QFY18 Result: Estimate (), Target (), Rating () Regular Coverage 33% ATR in 17Months HAM execution + WC streamlining + debt reduction = multiple re-rating Construction © 2017 Equirus All rights reserved Rating Information Price (Rs) 318 Target Price (Rs) 461 Target Date 31st Mar'19 Target Set On 14th Nov'17 Implied yrs of growth (DCF) 15 Fair Value (DCF) 369 Fair Value (DDM) 21 Ind Benchmark BSE Midcap Model Portfolio Position NA Stock Information Market Cap (Rs Mn) 54,534 Free Float (%) 53.24 % 52 Wk H/L (Rs) 350.9/256 Avg Daily Volume (1yr) 174,986 Avg Daily Value (Rs Mn) 51 Equity Cap (Rs Mn) 172 Face Value (Rs) 1 Bloomberg Code SADE IN Ownership Recent 3M 12M Promoters 46.8 % 0.0 % 0.0 % DII 32.0 % 6.7 % 5.7 % FII 16.6 % -1.7 % 0.0 % Public 4.7 % -5.0 % -5.7 % Price % 1M 3M 12M Absolute 13.6 % 15.9 % 15.1 % Vs Industry 12.0 % 11.2 % -7.8 % Ashoka 10.9 % 11.2 % 31.3 % PNC Infra 18.2 % 26.2 % 53.1 % Standalone Quarterly EPS forecast Rs/Share 1Q 2Q 3Q 4Q EPS (17A) 2.8 1.1 3.1 4.0 EPS (18E) 3.2 2.0 3.4 6.2 Sadbhav Engineering (SADE) outperformed on execution and profitability fronts in 2QFY18, and saw moderation in WC and debt reduction during the quarter. SADE enjoys revenue visibility of 2.7x FY17 net sales after factoring in a total order book (incl. L1 orders) of Rs 95bn. Margins have improved along with working capital contraction, in line with our view. Going ahead, smooth HAM project execution, margin expansion and WC improvements should play out. We maintain LONG with a SOTP-based Mar’19 TP of Rs 461 (Sep’18 TP of Rs 386 earlier). Recent EPC, mining wins take order book to Rs 95bn, pave way for steady growth: Post the recent EPC and mining wins, SADE has a healthy order book comprising 48%/19%/24%/9% share from BOT/EPC/mining/irrigation segments. Growth in the HAM model amid lower competitive intensity could increase this share to 50-60% by FY20E. Management expects Rs 300bn+ HAM bids in the coming 3-4 months and should be able to meet its FY18E order inflow target of Rs 70bn. Expect revenue mix shift away from EPC projects to enable margin expansion, WC improvements: We expect the share of WC-intensive EPC projects in overall execution to reduce post Jun’17. We have observed lower competitive intensity in the recently-bid HAM projects and also expect a more efficient WC cycle for these projects. We have modelled a reduction in non-cash WC levels, from ~58% in FY17 to 25% by FY19E. WC improvements, MBCP securitization to support reduction in standalone debt: Management expects reduction in receivables and receipt of mobilization advances to support WC streamlining, and reduce debt of Rs 2bn from current levels. It has also lined up the securitization of MBCP in SIPL, and this could support further reduction of Rs 2bn of debt. We have factored debt levels of ~Rs 12bn in the base case; in case of MBCP securitization, the standalone debt levels could head towards Rs 10bn. Re-rating apparent on lined up triggers, relative price movements; valuations provide comfort amidst business consolidation: Streamlining of verticals like mining and EPC, smooth HAM execution and WC improvements are inevitable re-rating triggers from current levels. After netting off our target BOT valuations of Rs 173/share, the EPC business is trading at ~1.3x/1.2x FY18E/FY19E P/B with RoEs of 14%/16% and 9.7x/7.9x FY18E/FY19E P/E at a 29%/21% 2/3-year EPS CAGR. Weak order inflows and lower execution are key downside risks to our estimates. Change in Standalone Estimates % change over previous estimates FY18E FY19E FY18E FY19E Sales 38,424 42,440 -1.8% 2.6% EBITDA 4,423 5,300 -1.1% 4.7% PAT 2,526 3,127 2.9% 9.9% EPS 14.7 18.2 3.0% 9.9% Standalone Financials Rs. Mn YE Mar FY17A FY18E FY19E FY20E Sales 33,203 38,424 42,440 46,077 EBITDA 3,556 4,423 5,300 5,676 Depreciation 1,000 1,006 1,051 1,093 Interest Expense 992 1,102 693 482 Other Income 333 336 353 370 Reported PAT 1,879 2,526 3,127 3,353 Recurring PAT 1,879 2,526 3,127 3,353 Total Equity 16,609 18,628 20,817 23,165 Gross Debt 15,183 11,364 6,558 6,249 Cash 230 491 4,579 5,674 Rs Per Share FY17A FY18E FY19E FY20E Earnings 11.0 14.7 18.2 19.6 Book Value 97 109 121 135 Dividends 0.8 1.9 4.7 0.0 FCFF 7.5 34.2 65.1 22.7 P/E (x) 29.0 21.6 17.4 16.3 P/B (x) 3.3 2.9 2.6 2.4 EV/EBITDA (x) 19.6 14.8 10.7 9.7 ROE (%) 12% 14% 16% 15% Core ROIC (%) 11% 13% 16% 18% EBITDA Margin (%) 10.7% 11.5% 12.5% 12.3% Net Margin (%) 6% 7% 7% 7%

Transcript of Sadbhav Engineering Limited Relative : Overweight...

November 15, 2017 Analyst: Devam Modi [email protected] (+91 – 90999 87467) Page 1 of 13

Before reading this report, you must refer to the disclaimer on the last page.

Sadbhav Engineering Limited Absolute : LONG

Relative : Overweight

2QFY18 Result: Estimate (), Target (), Rating () Regular Coverage 33% ATR in 17Months

HAM execution + WC streamlining + debt reduction = multiple re-rating Construction

© 2017 Equirus All rights reserved

Rating Information

Price (Rs) 318

Target Price (Rs) 461

Target Date 31st Mar'19

Target Set On 14th Nov'17

Implied yrs of growth (DCF) 15

Fair Value (DCF) 369

Fair Value (DDM) 21

Ind Benchmark BSE Midcap

Model Portfolio Position NA

Stock Information

Market Cap (Rs Mn) 54,534

Free Float (%) 53.24 %

52 Wk H/L (Rs) 350.9/256

Avg Daily Volume (1yr) 174,986

Avg Daily Value (Rs Mn) 51

Equity Cap (Rs Mn) 172

Face Value (Rs) 1

Bloomberg Code SADE IN

Ownership Recent 3M 12M

Promoters 46.8 % 0.0 % 0.0 %

DII 32.0 % 6.7 % 5.7 %

FII 16.6 % -1.7 % 0.0 %

Public 4.7 % -5.0 % -5.7 %

Price % 1M 3M 12M

Absolute 13.6 % 15.9 % 15.1 %

Vs Industry 12.0 % 11.2 % -7.8 %

Ashoka 10.9 % 11.2 % 31.3 %

PNC Infra 18.2 % 26.2 % 53.1 %

Standalone Quarterly EPS forecast

Rs/Share 1Q 2Q 3Q 4Q

EPS (17A) 2.8 1.1 3.1 4.0

EPS (18E) 3.2 2.0 3.4 6.2

Sadbhav Engineering (SADE) outperformed on execution and profitability fronts in

2QFY18, and saw moderation in WC and debt reduction during the quarter. SADE

enjoys revenue visibility of 2.7x FY17 net sales after factoring in a total order book

(incl. L1 orders) of Rs 95bn. Margins have improved along with working capital

contraction, in line with our view. Going ahead, smooth HAM project execution,

margin expansion and WC improvements should play out. We maintain LONG with a

SOTP-based Mar’19 TP of Rs 461 (Sep’18 TP of Rs 386 earlier).

Recent EPC, mining wins take order book to Rs 95bn, pave way for steady

growth: Post the recent EPC and mining wins, SADE has a healthy order book

comprising 48%/19%/24%/9% share from BOT/EPC/mining/irrigation segments.

Growth in the HAM model amid lower competitive intensity could increase this

share to 50-60% by FY20E. Management expects Rs 300bn+ HAM bids in the coming

3-4 months and should be able to meet its FY18E order inflow target of Rs 70bn.

Expect revenue mix shift away from EPC projects to enable margin expansion,

WC improvements: We expect the share of WC-intensive EPC projects in overall

execution to reduce post Jun’17. We have observed lower competitive intensity in

the recently-bid HAM projects and also expect a more efficient WC cycle for these

projects. We have modelled a reduction in non-cash WC levels, from ~58% in FY17

to 25% by FY19E.

WC improvements, MBCP securitization to support reduction in standalone

debt: Management expects reduction in receivables and receipt of mobilization

advances to support WC streamlining, and reduce debt of Rs 2bn from current

levels. It has also lined up the securitization of MBCP in SIPL, and this could

support further reduction of Rs 2bn of debt. We have factored debt levels of

~Rs 12bn in the base case; in case of MBCP securitization, the standalone debt

levels could head towards Rs 10bn.

Re-rating apparent on lined up triggers, relative price movements; valuations

provide comfort amidst business consolidation: Streamlining of verticals like

mining and EPC, smooth HAM execution and WC improvements are inevitable

re-rating triggers from current levels. After netting off our target BOT valuations of

Rs 173/share, the EPC business is trading at ~1.3x/1.2x FY18E/FY19E P/B with RoEs

of 14%/16% and 9.7x/7.9x FY18E/FY19E P/E at a 29%/21% 2/3-year EPS CAGR.

Weak order inflows and lower execution are key downside risks to our estimates.

Change in Standalone Estimates

% change over previous estimates

FY18E FY19E FY18E FY19E

Sales 38,424 42,440 -1.8% 2.6%

EBITDA 4,423 5,300 -1.1% 4.7%

PAT 2,526 3,127 2.9% 9.9%

EPS 14.7 18.2 3.0% 9.9%

Standalone Financials Rs. Mn YE Mar FY17A FY18E FY19E FY20E

Sales 33,203 38,424 42,440 46,077

EBITDA 3,556 4,423 5,300 5,676

Depreciation 1,000 1,006 1,051 1,093

Interest Expense 992 1,102 693 482

Other Income 333 336 353 370

Reported PAT 1,879 2,526 3,127 3,353

Recurring PAT 1,879 2,526 3,127 3,353

Total Equity 16,609 18,628 20,817 23,165

Gross Debt 15,183 11,364 6,558 6,249

Cash 230 491 4,579 5,674

Rs Per Share FY17A FY18E FY19E FY20E

Earnings 11.0 14.7 18.2 19.6

Book Value 97 109 121 135

Dividends 0.8 1.9 4.7 0.0

FCFF 7.5 34.2 65.1 22.7

P/E (x) 29.0 21.6 17.4 16.3

P/B (x) 3.3 2.9 2.6 2.4

EV/EBITDA (x) 19.6 14.8 10.7 9.7

ROE (%) 12% 14% 16% 15%

Core ROIC (%) 11% 13% 16% 18%

EBITDA Margin (%) 10.7% 11.5% 12.5% 12.3%

Net Margin (%) 6% 7% 7% 7%

Sadbhav Engineering Absolute – LONG Relative: Overweight 40% ATR in 13 Months

November 15, 2017 Analyst: Devam Modi [email protected] (+91 – 90999 87467) Page 2 of 13

Before reading this report, you must refer to the disclaimer on the last page.

Quarterly performance, standalone

Rs Mn 2QFY18 2QFY18E 1QFY17 2QFY17 % Change

Comments 2QFY18E 1QFY18 2QFY17

Net Sales 6,931 6,620 9,444 6,156 5% -27% 13%

Construction Expenses 5,550 5,230 7,436 4,839 6% -25% 15%

Employees Cost 317 381 309 353 -17% 2% -10%

Other Expenses 277 326 631 311 -15% -56% -11%

Total Expenditures 6,143 5,938 8,376 5,503 3% -27% 12%

EBITDA 788 682 1,068 654 15% -26% 20%

Depreciation 251 247 245 253 1% 2% -1%

EBIT 536 435 822 400 23% -35% 34%

Interest 215 319 322 221 -33% -33% -3%

Other Income 5 8 39 8 -34% -86% -30%

PBT 327 123 540 187 165% -39% 75%

Tax -8 12 -15 1 -167% -45% -695%

Recurring PAT 335 111 555 185 201% -40% 81%

Extraordinaries 0 0 0 0

Reported PAT 335 111 555 185 201% -40% 81%

EPS (Rs) 2.0 0.6 3.2 1.1 201% -40% 81%

EBITDA Margin 11.4% 10.3% 11.3% 10.6% 106 bps 6 bps 74 bps

EBIT Margin 7.7% 6.6% 8.7% 6.5% 117 bps -97 bps 123 bps

PBT Margin 4.7% 1.9% 5.7% 3.0% 285 bps -100 bps 168 bps

PAT Margin 4.8% 1.7% 5.9% 3.0% 315 bps -104 bps 182 bps

Tax Rate -2.6% 10.0% -2.8% 0.7% -1255 bps 24 bps -330 bps

Sadbhav Engineering Absolute – LONG Relative: Overweight 33% ATR in 17 months

______________________________________________________________________________________________________________________________________ November 15, 2017 Analyst: Devam Modi [email protected] (+91 – 90999 87467) Page 3 of 12

Key Quarterly Updates

Exhibit 1: Execution in Transport segment was affected in the quarter

Revenue (Rs. Mn) Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16 Mar-17 Jun-17 Sep-17

Transport

BOT Projects 5,926 5,596 5,618 5,607 4,577 6,902 8,237 8,223 6,138

Cash Contracts 4,610 4,281 4,016 1,114 333 420 1,461 2,076 739

Irrigation 1,316 1,315 1,601 4,493 4,244 6,482 6,776 6,147 5,399

Mining 315 1,003 2,035 1,684 902 739 1,255 804 300

Power Generation 1,198 921 871 723 658 1,002 785 392 476

Total Revenues 20 9 46 22 19 5 42 23 17

Source:Company, Equirus Securities

Exhibit 2: Toll collections normalized post demonetization

Name of SPV Units 4Q16 1Q17 2Q17 3Q17** 4Q17 1Q18 2Q18

Ahmedabad Ring Road Rs. Mn 246 237 227 216 240 234 227

Aurangabad Jalna* Rs. Mn 88 100 88 85 91 93 86

Dhule Palasner Rs. Mn 391 418 399 383 449 426 441

Hyderabad Yadgiri Rs. Mn 153 149 125 125 153 171 159

Bijapur Hungund Rs. Mn 302 304 286 241 293 296 297

Rohtak Panipat Rs. Mn 181 205 193 182 225 247 250

Maharashtra Border

Check Post Rs. Mn 432 415 406 370 448 451 432

Shreenathji Udaipur Rs. Mn 228 252 243 236 250 263 265

Bhilwara Rajsamand Rs. Mn - 23 94 95 105 116 110

Rohtak Hissar Rs. Mn - - 83 120 130 132 136

Total Toll Collections Rs. Mn 2,021 2,101 2,144 2,052 2,383 2,430 2,402

* 3Q17 numbers are calculated for some portion of the quarter due to impact of demonetization

** In MBCPNL, 13 checkposts were operational till 26th Jan'17 while 16 checkposts were operational

from 27th Jan'17. In 4Q16, 13 checkposts were operational

Source: Company BSE filings, Equirus Securities

Exhibit 3: Segment-wise details of order book

Order Book Segment Rs. Mn %age

Transport 52,365 68%

BOT 45,414 59%

Cash Contracts 6,952 9%

Mining 15,831 21%

Irrigation 8,956 12%

Total Order Book 77,152 100%

Source: Quarterly BSE Update, Equirus Securities Valuation

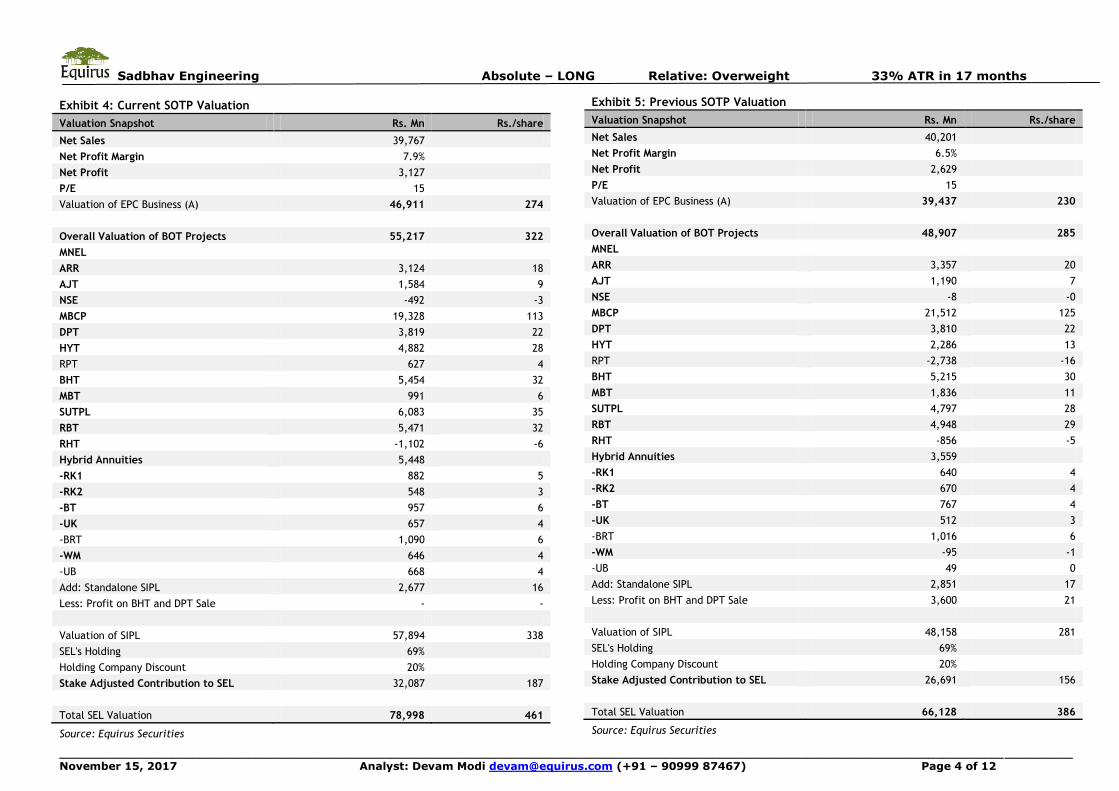

SOTP Valuation

Main changes in current and earlier SOTP valuations:

a) EPC business valuation higher by Rs 44/share: We have maintained the earlier 15x TTM Mar’18 P/E multiple.

b) Stake adjusted contribution from SIPL has been increased from 156 to 187.

Sadbhav Engineering Absolute – LONG Relative: Overweight 33% ATR in 17 months

______________________________________________________________________________________________________________________________________ November 15, 2017 Analyst: Devam Modi [email protected] (+91 – 90999 87467) Page 4 of 12

Exhibit 4: Current SOTP Valuation

Valuation Snapshot Rs. Mn Rs./share

Net Sales 39,767

Net Profit Margin 7.9%

Net Profit 3,127

P/E 15

Valuation of EPC Business (A) 46,911 274

Overall Valuation of BOT Projects 55,217 322

MNEL

ARR 3,124 18

AJT 1,584 9

NSE -492 -3

MBCP 19,328 113

DPT 3,819 22

HYT 4,882 28

RPT 627 4

BHT 5,454 32

MBT 991 6

SUTPL 6,083 35

RBT 5,471 32

RHT -1,102 -6

Hybrid Annuities 5,448

-RK1 882 5

-RK2 548 3

-BT 957 6

-UK 657 4

-BRT 1,090 6

-WM 646 4

-UB 668 4

Add: Standalone SIPL 2,677 16

Less: Profit on BHT and DPT Sale - -

Valuation of SIPL 57,894 338

SEL's Holding 69%

Holding Company Discount 20%

Stake Adjusted Contribution to SEL 32,087 187

Total SEL Valuation 78,998 461

Source: Equirus Securities

Exhibit 5: Previous SOTP Valuation

Valuation Snapshot Rs. Mn Rs./share

Net Sales 40,201

Net Profit Margin 6.5%

Net Profit 2,629

P/E 15

Valuation of EPC Business (A) 39,437 230

Overall Valuation of BOT Projects 48,907 285

MNEL

ARR 3,357 20

AJT 1,190 7

NSE -8 -0

MBCP 21,512 125

DPT 3,810 22

HYT 2,286 13

RPT -2,738 -16

BHT 5,215 30

MBT 1,836 11

SUTPL 4,797 28

RBT 4,948 29

RHT -856 -5

Hybrid Annuities 3,559

-RK1 640 4

-RK2 670 4

-BT 767 4

-UK 512 3

-BRT 1,016 6

-WM -95 -1

-UB 49 0

Add: Standalone SIPL 2,851 17

Less: Profit on BHT and DPT Sale 3,600 21

Valuation of SIPL 48,158 281

SEL's Holding 69%

Holding Company Discount 20%

Stake Adjusted Contribution to SEL 26,691 156

Total SEL Valuation 66,128 386

Source: Equirus Securities

Sadbhav Engineering Absolute – LONG Relative: Overweight 33% ATR in 17 months

______________________________________________________________________________________________________________________________________ November 15, 2017 Analyst: Devam Modi [email protected] (+91 – 90999 87467) Page 5 of 12

Earnings call takeaways

Industry Update: HAM pipeline to remain strong

The company is confident of the HAM pipeline. Several states are also expected to

come out with multiple bids.

On the Mining front bids of Rs. 10bn for 3 projects are to be given before this month.

3 Irrigation projects worth Rs 32.90bn are expected to come up in the states of MP,

Karnataka and Rajasthan. GST rate on roads and irrigation projects is 12%, while it is

18% on Mining Business. GST rate on bitumen is 12 %, Cement – 28% , other

construction commodities is 12%. GST on Labor contracts is 18%.

Input credit is available upto 7-8% depending on the type of projects. 3-5%

additional Tax impact is in line with the Pre GST era. The company doesn’t see much

impact on construction business as a result of this.

Quarterly Update: Plan to complete NHAI EPC backlog by FY18.

Growth in execution was driven by transport segment. The quarter saw margin

improvement on account of bituminous and higher share of HAM Projects. Reduction

in debt in the quarter was due to mobilization advances received from HAM Projects.

The company plans to repay another 1.5-2bn debt by Mar’18. The debt repayment

shall be done out of receivable proceeds and mobilization advances. There has also

been reduction in the finance costs along with reduction in debt. Company has

received 8 projects worth Rs 34.5bn in FY18E. Debt in the standalone business stands

at Rs . 14.23bn.

The receivables currently stand at Rs 15bn. Repayment from SIPL is expected to be

received to the tune of Rs 2bn which shall be done from securitization of MBCPNL.

The guidance for topline is Rs 38bn & the margins for the year are expected to be

about 11.5%.

The company plans to complete entire NHAI EPC backlog by FY18.

Tax rate: there will be no tax liability in FY18 as well since MAT credit is available.

The company has Rs 900mn of credit available.

Project related Updates

Work has started Rampur Kathghodam Pack -2 and Udaipur Bypass. RK-2 has received

AD on 20th Oct’17. Construction has started in 4 HAM projects.

Irrigation: Execution in these projects is lower since 3 projects have been completed

and certificate of completion has been received for same. New order intake is not

currently seen for this segment. The existing OB is expected to exhaust by FY19.

The company received Rs 1.05bn as arbitration award of which Rs 700mn is to be

received by SEL.

Award of Rs 6.25bn is expected to be received for Nagpur Seoni, Dhule Palesnar and

MNEL Projects by Dec’18.

Following was the execution run rate at the projects in Q2FY18 & Q1FY18

BT – Rs 160mn / Rs 600mn

RK 1 – Rs 190mn / Rs 500mn

UK- Rs 750mn/ Rs 420mn

Work has started in UB and execution was Rs 110mn in the quarter. Eastern

peripheral saw execution of Rs 2.75bn in the quarter.

Top 5 projects by execution in 2QFY18

Project Name Segment Rs. Mn

Eastern Peripheral Expressway I Road EPC 1,484

Eastern Peripheral Expressway II Road EPC 1,273

Yamunagar Panchkula Pckg I Road EPC 6885

Yamunagar Panchkula Pckg II Road EPC 379

Ambala Kaithal Road BOT 380

Sadbhav Engineering Absolute – LONG Relative: Overweight 33% ATR in 17 months

______________________________________________________________________________________________________________________________________ November 15, 2017 Analyst: Devam Modi [email protected] (+91 – 90999 87467) Page 6 of 12

Company Snapshot

How we differ from Consensus

- Equirus Consensus % Diff Comment

EPS FY18E 2.6 - -

FY19E 20.1 - -

Sales FY18E 51,690 - -

FY19E 60,381 - -

PAT FY18E 439 - -

FY19E 439 - -

Our Key Investment arguments: Valuations at comfortable levels after factoring base

growth scenario and assumptions for EPC and BOT business

Key Parameters Units FY17A FY18E FY19E FY20E

Standalone Sales Rs. Mn 33,203 38,424 42,440 46,077

Sales Growth %age 4% 16% 10% 9%

Standalone EBITDA Rs. Mn 3,556 4,423 5,300 5,676

EBITDAM% %age 11% 12% 12% 12%

BOT Projects

Toll Collections Rs. Mn 12,497 13,266 17,941 17,765

EBITDA Rs. Mn 9,066 8,370 12,337 12,394

EBITDA% %age 73% 63% 69% 70%

Risk to Our View

Lower than expected order inflows in FY18, Lower EPC EBITDA Margins and fall in

Traffic/Toll incomes

Key Triggers

Order book growth, Early Completion of BOT Projects, Acquisition of BOT Projects,

Winning of a large MDO order

Sensitivity to Key Variables % Change % Impact on EPS

EBITDA Margins 1 % 12 %

Interest Rate 1 % -2 %

- - -

DCF Valuations & Assumptions

Rf Beta Ke Term. Growth Debt/IC in Term. Yr

6.8 % 1.0 12.8 % 3.0 % 48.5 %

- FY18E FY19E FY20-22E FY23-27E FY28-32E

Sales Growth 13 % 17 % 10 % 5 % 3 %

NOPAT Margin 15 % 17 % 11 % 13 % 14 %

IC Turnover 0.40 0.44 0.55 0.91 1.26

RoIC 6.0 % 7.8 % 6.3 % 12.0 % 16.9 %

Years of strong growth 1 2 5 10 15

Valuation as on date (Rs) 31 202 102 280 313

Valuation as of Mar'19 37 238 121 330 369

Based on DCF, assuming 15 years of 8% CAGR growth and 12% average ROIC, we derive

current fair value of Rs. 313 and Mar’19 fair value of Rs. 369.

Company Description:

Sadbhav is in the business of EPC Contracting for Cash Contracts, Mining, Irrigation and

BOT Road Projects. It has an order book of ~Rs. 77bn and its subsidiary SIPL has a

portfolio of 16 BOT Projects. It is one of the leading road BOT companies in India that

specializes in the development, operation and maintenance of highways, roads and

related projects.

Comparable valuation Mkt Cap

Rs. Mn.

Price

Target

Target

Date

EPS P/E BPS P/B RoE Div Yield

Company Reco. CMP FY17A FY18E FY19E FY17A FY18E FY19E FY17A FY18E FY17A FY18E FY19E FY17A FY18E

Sadbhav Engg LONG 318 54,534 461 31st Mar'19 11.0 14.7 18.2 29.0 21.6 17.4 96.8 2.9 12 % 14 % 16 % 0.2 % 0.6 %

Ashoka Buildcon LONG 208 38,983 320 31st Mar'19 -0.5 13.7 21.0 -391.3 15.3 9.9 89.3 2.1 -1 % 14 % 20 % 0.4 % 1.0 %

PNC Infratech Reduce 178 45,651 129 30th Sep 18 4.6 5.5 5.7 38.6 32.3 31.2 57.0 2.9 8 % 9 % 9 % 1.4 % 0.3 %

Sadbhav Engineering Absolute – LONG Relative: Overweight 33% ATR in 17 months

______________________________________________________________________________________________________________________________________ November 15, 2017 Analyst: Devam Modi [email protected] (+91 – 90999 87467) Page 7 of 12

Standalone Quarterly Earnings Forecast and Key Drivers Rs in Mn 1Q17A 2Q17A 3Q17A 4Q17A 1Q18A 2Q18A 3Q18E 4Q18E 1Q19E 2Q19E 3Q19E 4Q19E FY17A FY18E FY19E FY20E

Revenue 8,070 6,156 8,648 10,329 9,444 6,931 10,306 11,744 10,120 7,597 11,711 13,011 33,203 38,424 42,440 46,077

Construction Expenses 6,621 4,839 6,986 8,106 7,436 5,550 8,348 9,278 7,995 6,002 9,252 10,279 26,552 30,611 33,527 36,401

Employees Cost 315 353 319 379 309 317 345 409 334 342 372 442 1,366 1,380 1,490 1,696

Other Expenses 266 311 405 748 631 277 515 587 506 380 586 651 1,729 2,010 2,122 2,304

EBITDA 868 654 939 1,096 1,068 788 1,098 1,470 1,285 874 1,501 1,640 3,556 4,423 5,300 5,676

Depreciation 254 253 250 243 245 251 254 256 259 261 264 267 1,000 1,006 1,051 1,093

EBIT 614 400 689 854 822 536 844 1,214 1,026 612 1,237 1,373 2,556 3,417 4,250 4,582

Interest 172 221 243 355 322 215 302 263 220 178 156 139 992 1,102 693 482

Other Income 48 8 60 218 39 5 63 228 41 6 66 240 333 336 353 370

PBT 489 187 506 716 540 327 605 1,179 847 440 1,148 1,474 1,897 2,651 3,909 4,471

Tax 2 1 -19 33 -15 -8 30 118 169 88 230 295 18 125 782 1,118

Recurring PAT 487 185 525 683 555 335 575 1,061 678 352 918 1,179 1,879 2,526 3,127 3,353

Extraordinary 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Reported PAT 487 185 525 683 555 335 575 1,061 678 352 918 1,179 1,879 2,526 3,127 3,353

EPS (Rs) 2.84 1.08 3.06 3.98 3.23 1.95 3.35 6.19 3.95 2.05 5.35 6.88 10.96 14.73 18.24 19.55

Key Drivers

Cash Contract Revenues 4,493 4,244 6,482 6,500 2,970 3,600 5,220 5,400 2,673 3,240 4,698 4,860 21,718 17,190 15,471 13,924

BOT EPC Revenues 1,114 333 420 2,000 2,700 2,835 3,402 4,082 4,050 4,253 5,103 6,124 3,866 13,019 19,529 29,294

Mining EPC Revenue 723 659 1,002 800 831 757 1,152 920 956 871 1,325 1,058 3,183 3,661 4,210 4,841

Irrigation EPC Revenue 1,684 903 739 1,500 1,852 993 776 1,575 2,037 1,092 854 1,733 4,826 5,196 5,716 6,288

- - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - -

Sequential Growth (%)

Revenue -6 % -24 % 40 % 19 % -9 % -27 % 49 % 14 % -14 % -25 % 54 % 11 % - - - -

(Increase) / Decrease in Work in progress

- - - - - - - - - - - - - - - -

EBITDA -4 % -25 % 44 % 17 % -3 % -26 % 39 % 34 % -13 % -32 % 72 % 9 % - - - -

EBIT 7 % -35 % 72 % 24 % -4 % -35 % 57 % 44 % -15 % -40 % 102 % 11 % - - - -

Recurring PAT 10 % -62 % 183 % 30 % -19 % -40 % 72 % 85 % -36 % -48 % 161 % 28 % - - - -

EPS 39 % -62 % 183 % 30 % -19 % -40 % 72 % 85 % -36 % -48 % 161 % 28 % - - - -

Yearly Growth (%)

Revenue -3 % -17 % 15 % 20 % 17 % 13 % 19 % 14 % 7 % 10 % 14 % 11 % 4 % 16 % 10 % 9 %

EBITDA -3 % -19 % 27 % 21 % 23 % 20 % 17 % 34 % 20 % 11 % 37 % 12 % 6 % 24 % 20 % 7 %

EBIT -11 % -32 % 32 % 49 % 34 % 34 % 23 % 42 % 25 % 14 % 47 % 13 % 8 % 34 % 24 % 8 %

Recurring PAT 23 % -53 % 94 % 55 % 14 % 81 % 10 % 56 % 22 % 5 % 60 % 11 % 24 % 34 % 24 % 7 %

EPS 23 % -33 % 84 % 95 % 14 % 81 % 10 % 56 % 22 % 5 % 60 % 11 % 42 % 34 % 24 % 7 %

Margin (%)

EBITDA 11 % 11 % 11 % 11 % 11 % 11 % 11 % 13 % 13 % 11 % 13 % 13 % 11 % 12 % 12 % 12 %

EBIT 8 % 7 % 8 % 8 % 9 % 8 % 8 % 10 % 10 % 8 % 11 % 11 % 8 % 9 % 10 % 10 %

PBT 6 % 3 % 6 % 7 % 6 % 5 % 6 % 10 % 8 % 6 % 10 % 11 % 6 % 7 % 9 % 10 %

PAT 6 % 3 % 6 % 7 % 6 % 5 % 6 % 9 % 7 % 5 % 8 % 9 % 6 % 7 % 7 % 7 %

Sadbhav Engineering Absolute – LONG Relative: Overweight 40% ATR in 13 Months

November 15, 2017 Analyst: Devam Modi [email protected] (+91 – 90999 87467) Page 8 of 13

Before reading this report, you must refer to the disclaimer on the last page.

Consolidated Financials Forecast

P&L (Rs Mn) FY17A FY18E FY19E FY20E

Balance Sheet (Rs Mn) FY17A FY18E FY19E FY20E

Cash Flow (Rs Mn) FY17A FY18E FY19E FY20E

Revenue 45,700 51,690 60,381 63,843 Equity Capital 172 172 172 172 PAT before MI -1,716 693 4,628 1,364

Op. Expenditure 33,078 35,507 39,132 41,773 Reserve 8,892 8,952 11,462 13,972 Depreciation 3,211 3,199 4,419 7,223

EBITDA 12,622 16,183 21,249 22,070 Networth 9,063 9,123 11,633 14,143 Others 10,840 0 0 0

Depreciation 3,211 3,199 4,419 7,223 Long Term Debt 95,041 112,415 120,105 120,747 Taxes Paid 188 254 1,180 1,435

EBIT 9,411 12,984 16,830 14,847 Def Tax Liability 16,429 0 0 0 Change in WC -8,866 -2,495 6,435 -655

Interest Expense 11,874 9,438 9,143 10,053 Minority Interest 3,480 3,480 3,549 3,652 Operating C/F 3,656 1,142 14,302 6,497

Other Income 842 536 553 570 Account Payables 5,605 3,053 3,372 3,661 Capex -2,578 -20,965 -9,569 4,695

PBT -1,622 693 4,628 1,364 Other Curr Liabi 8,579 7,685 8,488 9,215 Change in Invest -291 0 0 0

Tax 94 254 1,180 1,435 Total Liabilities & Equity 138,198 135,756 147,147 151,419 Others 671 22,912 -8,539 -14,372

PAT bef. MI & Assoc. -1,716 439 3,448 -71 Net Fixed Assets 102,446 92,155 113,067 126,052 Investing C/F -2,199 1,946 -18,109 -9,677

Minority Interest -1,176 0 0 0 Capital WIP 0 0 0 0 Change in Debt 8,505 17,374 7,689 642

Profit from Assoc. 0 0 0 0 Others 9,850 14,996 7,774 -2,757 Change in Equity 54 0 0 3,587

Recurring PAT -540 439 3,448 -71

Inventory 1,234 1,579 1,744 1,894 Others -10,423 -16,809 -869 -903

Extraordinaires 0 0 0 0 Account Receivables 15,912 11,580 11,627 12,624 Financing C/F -1,864 566 6,820 3,326

Reported PAT -540 439 3,448 -71 Other Current Assets 7,441 10,476 4,951 5,477 Net change in cash -407 3,654 3,013 146

FDEPS (Rs) -3.1 2.6 20.1 -0.4 Cash 1,316 4,970 7,984 8,130 RoE (%) -6 % 5 % 33 % -1 %

DPS (Rs) 0.8 1.9 4.7 5.0 Total Assets 138,198 135,756 147,147 151,419

RoIC (%) 6 % 5 % 7 % 5 %

CEPS (Rs) 8.7 21.2 45.9 41.7 Non-cash Working Capital 10,402 12,897 6,462 7,118

Core RoIC (%) 5 % 6 % 8 % 6 %

FCFPS (Rs) 81.8 54.3 13.0 20.2 Cash Conv Cycle 83.1 91.1 39.1 40.7 Div Payout (%) -27 % 86 % 27 % -1,421 %

BVPS (Rs) 52.8 53.2 67.8 82.5 WC Turnover 4.4 4.0 9.3 9.0 P/E -100.9 124.2 15.8 -769.8

EBITDAM (%) 28 % 31 % 35 % 35 % FA Turnover 0.4 0.6 0.5 0.5 P/B 6.0 6.0 4.7 3.9

PATM (%) -1 % 1 % 6 % 0 % Net D/E 10.3 11.8 9.6 8.0 P/FCFF 3.9 5.8 24.5 15.8

Tax Rate (%) -6 % 37 % 25 % 105 % Revenue/Capital Employed 0.4 0.4 0.5 0.5 EV/EBITDA 13.0 10.0 7.8 7.6

Sales Growth (%) 12 % 13 % 17 % 6 %

Capital Employed/Equity 12.5 13.7 12.5 10.6

EV/Sales 3.6 3.1 2.8 2.6

FDEPS Growth (%) -63 % -181 % 686 % -102 %

Dividend Yield (%) 0.2 % 0.6 % 1.5 % 0.0 %

TTM P/E vs. 2 yrs. forward EPS growth TTM EV/EBITDA vs. 2 yrs. forward EBITDA growth TTM P/B vs. 2 yrs. forward RoE

-40%

-20%

0%

20%

40%

60%

80%

100%

0

100

200

300

400

500

600

700

Mar

/14

Jun/

14

Sep/

14

Dec

/14

Mar

/15

Jun/

15

Sep/

15

Dec

/15

Mar

/16

Jun/

16

Sep/

16

Dec

/16

Mar

/17

Jun/

17

Sep/

17

Dec

/17

Mar

/18

Jun/

18

Sep/

18

Dec

/18

Mar

/19

EPSGrowth

21x

14x

7x

35x

28x

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

Mar/

14

Jun/14

Sep/14

Dec/14

Mar/

15

Jun/15

Sep/15

Dec/15

Mar/

16

Jun/16

Sep/16

Dec/16

Mar/

17

Jun/17

Sep/17

Dec/17

Mar/

18

Jun/18

Sep/18

Dec/18

Mar/

19

4x

8x

11x

14x

16xEBITDA Growth

0%

5%

10%

15%

20%

25%

30%

0

100

200

300

400

500

600

700

Mar/

14

Jun/14

Sep/14

Dec/

14

Mar/

15

Jun/15

Sep/15

Dec/

15

Mar/

16

Jun/16

Sep/16

Dec/

16

Mar/

17

Jun/17

Sep/17

Dec/

17

Mar/

18

Jun/18

Sep/18

Dec/

18

Mar/

19

RoE

1x

2x

3x

4x

5x

Sadbhav Engineering Absolute – LONG Relative: Overweight 33% ATR in 17 months

______________________________________________________________________________________________________________________________________ November 15, 2017 Analyst: Devam Modi [email protected] (+91 – 90999 87467) Page 9 of 12

Historical Consolidated Financials

P&L (Rs Mn) FY14A FY15A FY16A FY17A

Balance Sheet (Rs Mn) FY14A FY15A FY16A FY17A

Cash Flow (Rs Mn) FY14A FY15A FY16A FY17A

Revenue 27,325 34,468 40,658 45,700 Equity Capital 151 172 172 172 PAT before MI 261 -2,325 -2,205 -1,716

Op. Expenditure 22,870 28,624 30,655 33,078 Reserve 12,579 10,816 9,919 8,892 Depreciation 1,305 2,235 2,326 3,211

EBITDA 4,456 5,844 10,003 12,622 Networth 12,730 10,987 10,090 9,063 Others 3,127 6,047 9,040 10,840

Depreciation 1,305 2,235 2,326 3,211 Long Term Debt 55,718 66,867 86,391 95,041 Taxes Paid -561 -679 -801 188

EBIT 3,151 3,609 7,677 9,411 Def Tax Liability 800 9,293 14,187 16,429 Change in WC 3,732 -1,427 4,906 -8,866

Interest Expense 4,555 6,150 10,752 11,874 Minority Interest 2,258 1,375 4,302 3,480 Operating C/F 7,864 3,850 13,266 3,656

Other Income 306 442 667 842 Account Payables 3,880 4,573 3,907 5,605 Capex -12,042 -14,091 -16,299 -2,578

PBT 120 -882 -1,191 -405 Other Curr Liabi 3,322 5,464 8,500 8,579 Change in Invest -947 983 1,525 -291

Tax -141 343 219 94 Total Liabilities & Equity 78,707 98,560 127,377 138,198 Others -1,420 -467 1,017 671

PAT bef. MI & Assoc. 261 -1,224 -1,410 -499 Net Fixed Assets 52,313 74,661 103,086 102,446 Investing C/F -14,409 -13,575 -13,757 -2,199

Minority Interest -181 -592 -1,173 -1,176 Capital WIP 7,754 7 0 0 Change in Debt 11,454 13,646 9,435 8,505

Profit from Assoc. 2 -22 0 0 Others 3,399 6,582 7,364 9,850 Change in Equity 268 3,153 2 54

Recurring PAT 444 -654 -237 677 Inventory 1,638 2,134 1,410 1,234 Others -4,661 -6,431 -9,645 -10,423

Extraordinaires -1,217 -117 -422 0 Account Receivables 5,758 6,708 8,086 15,912 Financing C/F 7,060 10,368 -208 -1,864

Reported PAT 444 -654 -237 677 Other Current Assets 5,538 6,627 6,101 7,441 Net change in cash 516 644 -699 -407

EPS (Rs) -4.5 -10.9 -8.5 -3.1 Cash 2,309 1,841 1,329 1,316

RoE (%) -6 % -16 % -14 % -6 %

DPS (Rs) 0.7 0.7 0.7 0.8

Total Assets 78,707 98,560 127,377 138,198

RoIC (%) 5 % 3 % 6 % 6 %

CEPS (Rs) 2.0 -1.2 -1.8 8.7 Non-cash Working Capital 5,732 5,431 3,190 10,402 Core RoIC (%) 3 % 2 % 4 % 5 %

FCFPS (Rs) -17.1 -16.7 65.4 81.8 Cash Conv Cycle 76.6 57.5 28.6 83.1 Div Payout (%) 29 % -8 % -14 % -27 %

BVPS (Rs) 74.2 64.1 58.8 52.8 WC Turnover 4.8 6.3 12.7 4.4

P/E -102.0 -70.5 -29.1 -37.5

EBITDAM (%) 16 % 17 % 25 % 28 % FA Turnover 0.5 0.5 0.4 0.4 P/B 4.5 4.3 5.0 5.4

PATM (%) 2 % -5 % -3 % -1 % Net D/E 4.2 5.9 8.4 10.3 P/FCFF -18.6 -19.1 4.9 3.9

Tax Rate (%) 13 % -16 % -9 % -6 % Revenue/Capital Employed 0.5 0.5 0.5 0.4 EV/EBITDA 25.5 24.6 23.6 16.8

Sales growth (%) 27 % 26 % 18 % 12 %

Capital Employed/Equity 5.2 6.7 9.7 12.5

EV/Sales 4.2 4.2 5.8 4.6

FDEPS growth (%) 45 % 142 % -22 % -63 %

Dividend Yield (%) 0.2 % 0.2 % 0.2 % 0.2 %

Sadbhav Engineering Absolute – LONG Relative: Overweight 33% ATR in 17 months

______________________________________________________________________________________________________________________________________ November 15, 2017 Analyst: Devam Modi [email protected] (+91 – 90999 87467) Page 10 of 12

Equirus Securities

Research Analysts Sector/Industry Email

Equity Sales E-mail

Abhishek Shindadkar IT Services [email protected] 91-22-43320643 Vishad Turakhia [email protected] 91-22-43320633

Ashutosh Tiwari Auto, Metals & Mining [email protected] 91-79-61909517 SubhamSinha [email protected] 91-22-43320631

Depesh Kashyap Mid-Caps [email protected] 91-79-61909528 SwetaSheth [email protected] 91-22-43320634

Devam Modi Power & Infrastructure [email protected] 91-79-61909516 Viral Desai [email protected] 91-22-43320635

Dhaval Dama FMCG, Mid-Caps [email protected] 91-79-61909518 Dealing Room E-mail

Manoj Gori Consumer Durables [email protected] 91-79-61909523 Ashish Shah [email protected] 91-22-43320662

Maulik Patel Oil and Gas [email protected] 91-79-61909519 IleshSavla [email protected] 91-22-43320666

PrafulBohra Pharmaceuticals [email protected] 91-79-61909532 Manoj Kejriwal [email protected] 91-22-43320663

Rohan Mandora Banking & Financial Services [email protected] 91-79-61909529 Dharmesh Mehta [email protected] 91-22-43320661

Associates E-mail SandipAmrutiya [email protected] 91-22-43320660

Ankit Choudhary [email protected] 91-79-61909533 Compliance Officer E-mail

Bharat Celly [email protected] 91-79-61909524 Jay Soni [email protected] 91-79-61909561

Harshit Patel [email protected] 91-79-61909522 Corporate Communications E-mail

Meet Chande [email protected] 91-79-61909513 Mahdokht Bharda [email protected] 91-22-43320647 Parva Soni [email protected] 91-79-61909521

Pranav Mehta [email protected] 91-79-61909514

Ronak Soni [email protected] 91-79-61909525

Samkit Shah [email protected] 91-79-61909520

Shreepal Doshi [email protected] 91-79-61909541

Varun Baxi [email protected] 91-79-61909527

Vikas Jain [email protected] 91-79-61909531

Rating & Coverage Definitions: Absolute Rating • LONG : Over the investment horizon, ATR >= Ke for companies with Free Float market cap > Rs 5 billion and ATR >= 20% for rest of the companies • ADD: ATR >= 5% but less than Ke over investment horizon • REDUCE: ATR >= negative 10% but <5% over investment horizon • SHORT: ATR < negative 10% over investment horizon Relative Rating • OVERWEIGHT: Likely to outperform the benchmark by at least 5% over investment horizon • BENCHMARK: likely to perform in line with the benchmark • UNDERWEIGHT: likely to under-perform the benchmark by at least 5% over investment horizon Investment Horizon Investment Horizon is set at a minimum 3 months to maximum 18 months with target date falling on last day of a calendar quarter. Lite vs. Regular Coverage vs. Spot Coverage We aim to keep our rating and estimates updated at least once a quarter for Regular Coverage stocks. Generally, we would have access to the company and we would maintain detailed financial model for Regular coverage companies. We intend to publish updates on Lite coverage stocks only an opportunistic basis and subject to our ability to contact the management. Our rating and estimates for Lite coverage stocks may not be current. Spot coverage is meant for one-off coverage of a specific company and in such cases, earnings forecast and target price are optional. Spot coverage is meant to stimulate discussion rather than provide a research opinion.

Registered Office:

Equirus Securities Private Limited

Unit No. 1201, 12th Floor, C Wing, Marathon Futurex,

N M Joshi Marg, Lower Parel,

Mumbai-400013.

Tel. No: +91 – (0)22 – 4332 0600

Fax No: +91- (0)22 – 4332 0601

Corporate Office:

3rd floor, House No. 9,

Magnet Corporate Park, Near Zydus Hospital, B/H Intas Sola Bridge,

S.G. Highway Ahmedabad-380054

Gujarat

Tel. No: +91 (0)79 - 6190 9550

Fax No: +91 (0)79 – 6190 9560

Sadbhav Engineering Absolute – LONG Relative: Overweight 33% ATR in 17 months

______________________________________________________________________________________________________________________________________ November 15, 2017 Analyst: Devam Modi [email protected] (+91 – 90999 87467) Page 11 of 12

© 2017 Equirus Securities Private Limited. All rights reserved. For Private Circulation only. This report or any portion hereof may not

be reprinted, sold or redistributed without the written consent of Equirus Securities Private Limited

Analyst Certification

I, Devam Modi, author to this report, hereby certify that all of the views expressed in this report accurately reflect my personal views about the subject company or companies and its or their securities. I also

certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report.

Disclosures

Equirus Securities Private Limited (ESPL) having Corporate Identification Number U65993MH2007PTC176044 is registered in India with Securities and Exchange Board of India (SEBI) as a trading member on the

Capital Market (Reg. No. INB231301731), Futures & Options Segment (Reg. No.INF231301731) of the National Stock Exchange of India Ltd. (NSE) and on Cash Segment (Reg. No.INB011301737) of Bombay Stock

Exchange Limited (BSE).ESPL is also registered with SEBI as Research Analyst under SEBI (Research Analyst) Regulations, 2014 (Reg. No. INH000001154), as a Portfolio Manager under SEBI (Portfolio Managers

Regulations, 1993 (Reg. No.INP000005216) and as a Depository Participant of the Central Depository Services (India) Limited (Reg. No.IN-DP-324-2017). There are no disciplinary actions taken by any regulatory

authority against ESPL. ESPL is a subsidiary of Equirus Capital Pvt. Ltd. (ECPL) which is registered with SEBI as Category I Merchant Banker and provides investment banking services including but not limited to

merchant banking services, private equity, mergers & acquisitions and structured finance.

As ESPL and its associates are engaged in various financial services business, it might have: - (a) received compensation (except in connection with the preparation of this report) from the subject company for

investment banking or merchant banking or brokerage services in the past twelve months;(b) managed or co-managed public offering of securities for the subject company in the past twelve months; or (c) have

received a mandate from the subject company; or (d) might have other financial, business or other interests in entities including the subject company (ies) mentioned in this Report. ESPL & its associates, their

directors and employees may from time to time have positions or options in the company and buy or sell the securities of the company (ies) mentioned herein. ESPL and its associates collectively do not own (in

their proprietary position) 1% or more of the equity securities of the subject company mentioned in the report as the last day of the month preceding the publication of the research report. ESPL or its Analyst or

Associates did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ESPL nor

Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or

brokerage service transactions. ESPL has not been engaged in market making activity for the subject company.

The Research Analyst engaged in preparation of this Report:-

(a) has not received any compensation from the subject company in the past twelve months; (b) has not managed or co-managed public offering of securities for the subject company in the past twelve months; (c)

has not received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve months; (d) has not received any compensation for products or

services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months; (e) has not received any compensation or other benefits from the subject

company or third party in connection with the research report; (f) might have served as an officer, director or employee of the subject company; (g) is not engaged in market making activity for the subject

company.

This document is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ESPL and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein

may or may not be eligible for sale in all jurisdictions or to a certain category of investors. Persons in whose possession of this document are required to inform themselves of, and to observe, such applicable

restrictions. Please delete this document if you are not authorized to view the same. By reading this document you represent and warrant that you have full authority and all rights necessary to view and read this

document without subjecting ESPL and affiliates to any registration or licensing requirement within such jurisdiction.

This document has been prepared solely for information purpose and does not constitute a solicitation to any person to buy, sell or subscribe any security. ESPL or its affiliates are not soliciting any action based on

this report. The information and opinions contained herein is from publicly available data or based on information obtained in good faith from sources believed to be reliable but ESPL provides no guarantee as to

its accuracy or completeness. The information contained herein is as on date of this report, and is subject to change or modification and any such changes could impact our interpretation of relevant information

contained herein. While we would endeavour to update the information herein on reasonable basis, ESPL and its affiliates, their directors and employees are under no obligation to update or keep the information

current. Also there may be regulatory, compliance, or other reasons that may prevent ESPL and its group companies from doing so. This document is prepared for assistance only and is not intended to be and must

not alone be taken as the basis for an investment decision. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the

securities of companies referred to in this document including the merits and risks involved. This document is intended for general circulation and does not take into account the specific investment objectives,

financial situation or particular needs of any particular person. ESPL and its group companies, employees, directors and agents accept no liability, and disclaim all responsibility, for the consequences of you or

anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it. ESPL/its affiliates do and seek to do business with companies covered in its

research report. Thus, investors should be aware that the firm may have conflict of interest.

Sadbhav Engineering Absolute – LONG Relative: Overweight 33% ATR in 17 months

______________________________________________________________________________________________________________________________________ November 15, 2017 Analyst: Devam Modi [email protected] (+91 – 90999 87467) Page 12 of 12

A graph of daily closing prices of securities is available at http://www.nseindia.com/ChartApp/install/charts/mainpage.jsp and www.bseindia.com (Choose a company from the list on the browser and select the

“three years” period in the price chart).

Disclosure of Interest statement for the subject Company Yes/No If Yes, nature of such interest

Research Analyst’ or Relatives’ financial interest No

Research Analyst’ or Relatives’ actual/beneficial ownership of 1% or more No

Research Analyst’ or Relatives’ material conflict of interest No

Disclaimer for U.S. Persons

ESPL/its affiliates are not a registered broker–dealer under the U.S. Securities Exchange Act of 1934, as amended (the“1934 act”) and under applicable state laws in the United States. In addition Equirus is not a

registered investment adviser under the U.S. Investment Advisers Act of 1940, as amended (the "Advisers Act" and together with the 1934 Act, the “Acts”), and under applicable state laws in the United States.

Accordingly, in the absence of specific exemption under the Acts, any brokerage and investment services provided by Equirus, including the products and services described herein are not available to or intended

for U.S. persons. The information contained in this Report is not intended for any person who is a resident of the United States of America or a resident of any jurisdiction, the laws of which imposes prohibition on

soliciting the securities business in that jurisdiction without going through the registration requirements and/ or prohibit the use of any information contained in this report. This Report and its respective contents

do not constitute an offer or invitation to purchase or subscribe for any securities or solicitation of any investments or investment services and/or shall not be considered as an advertisement tool. "U.S. Persons"

are generally defined as a natural person, residing in the United States or any entity organized or incorporated under the laws of the United States. US Citizens living abroad may also be deemed "US Persons" under

certain rules.