Running on the China bridge to innovation

94

CONFIDENTIAL AND PROPRIETARY Any use of this material without specific permission of McKinsey & Company is strictly prohibited November 2019, Shanghai Running on the China bridge to innovation

Transcript of Running on the China bridge to innovation

CONFIDENTIAL AND PROPRIETARYAny use of this material without specific permission of McKinsey & Company is strictly prohibited

November 2019, Shanghai

Running on the China bridge to innovation

McKinsey & Company 2

2019 in the mirror: Nine key trends to watch

9 New era of pharma deals7 Funding the future of local biotech 8

3 Access for all?1 China takes center stage for MNCs1 2 Continued NMPA2 reform

Resurgence in external innovation investments

Biosimilars at the gate6VBP goes nationwide4 Opening the floodgate for digital healthcare

5

1 Multinational corporations.

2 National Medical Product Administration.

McKinsey & Company 3

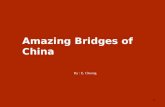

1: World exposure to China’s economy continues to rise given China’s scale and prominence as a trading nation

Source: McKinsey Global Institute analysis

1 The China-World Exposure Index measures the relative importance of these economic flows for the Chinese and global economies, compared with other large economies. The new MGI China-World Exposure Index consists of five components covering trade, capital, and technology. On trade, MGI considered exposure to a country’s supply (exports divided by rest-of-world consumption) and demand (imports divided by rest-of-world gross output). On capital, MGI considered exposure to a country’s capital (outbound FDI divided by rest-of-world inbound FDI) and investment opportunities (inbound FDI divided by rest-of-world outbound FDI). On technology, MGI considered exposure to a country’s technology exports (exports of IP and technology services and equipment divided by rest-of-world R&D spending).

2 China, Japan, Germany, France, India, United Kingdom, and the United States.

China’s global scale China-World Exposure Index1

Data802mn

internet usersTop 3 financial

system

Capital110 Global Fortune 500 companies

Firms11% of

global goods trade

Trade

45% of renewables investment

Environment2nd on R&D

spending

Technology2nd largest

pharmaceutical market

Healthcare150mnoutbound

trips

People

Weighted average exposure of 7 large economies2

=1.0

2000 2017

0.4

0.8

0.6

1.2

World exposure to China

China exposure to the world

McKinsey & Company 4

2: First major revision of the Drug Administration Law in 18 years

Source: NMPA, press release

1.Drug Administration Law

Key changes in 2019 DAL1 revision

• Require a legal representative from MNCs to hold obligation and liability of MAH

• Adopt drug tracking to ensure accountability • Re-define counterfeit drug based on active

ingredients and claims, rather than regulatory approval

• Remove “prohibition of online sale of Rx drug” from the draft proposal

Ensure drug safety

Legalize online Rx drug sales

Accelerate innovation• Implement Clinical Trial Notification• Replace pre-certification of clinical trial sites with self-

reporting and follow-up inspection

Sep 1984First adopted at the Sixth National Peoples Congress

Feb 2001First revision

Dec 2013Minor amendment

Apr 2015Minor amendment

The second major revisionAug 2019

18 Years

McKinsey & Company 5Source: CDE; EvaluatePharma; GBI; McKinsey analysis

1. Including both innovative chemical drugs and biologics. | 2. As of October 25, 2019.

2: Sustained momentum of NMPA reform has led to a tsunamiof new launches and a significant reduction in launch lag

4

4045

28

3

9

6

2019YTD22016

1

54

2018

34

2017

7

41

Local MNC

# of innovative drug approved1 Launch lag between China and global first launch2016 2019Selected brands

approved in 2019

必特

Launch lagYears

Brand(4)

Launch lagYears

Brand(28)

3.9 0.6

14.0 2.2

8.8 1.8

……

Average 8.4 4.6Average

Average launch lag in 2019 still skewed by “legacy” delays from prior years

8.8

6.9 1.6

McKinsey & Company 6

3: Access broadens with more frequent National Reimbursement Drug List (NRDL) updates and continued optimization

1,8502,127

2,588 2,709

2004 2009 20171 20192

Source: Press release; McKinsey analysis

1 “2017 version NRDL”, which includes 2017 and 2018 negotiated molecules. http://www.nhsa.gov.cn/art/2019/8/22/art_38_1677.html2 “2019 version NRDL”, which includes 2019 negotiated molecules. http://www.nhsa.gov.cn/art/2019/11/28/art_14_2052.html

Highlight of NRDL update in 2019

# of NRDL listed molecules (2004–19)

More dynamic update of NRDL

70 drugs added through negotiation, and 27 drugs renewed NRDL contract through re-negotiation

150 drugs with limited clinical value removed from the list

Uniform list for all provinces. PRDL removed to enforce NRDL implementation

HTA and HEOR leveraged in NRDL negotiation

1st NRDL 2nd NRDL 3rd NRDL 4th NRDL 5th NRDL

2000 2004 2009 2017 2019

McKinsey & Company 7

3: In November 2019, 70 new drugs added to NRDL through negotiation

2017

-61%

201918

-45%-57%

16 56811

11

15

17

2017 2019

31

74

Blood

Oncology

Others

Alimentary/MetabolismAnti-infective/anti-virus

CVImmunology

2019

-26%

First-time negotiation Renegotiation 150 drugs went through negotiation in 2019• 119 drugs are negotiated for the first time

and 31 drugs are re-negotiated since contract signed in 2017

• 97 drugs successfully got listed. Among those, 70 drugs (52 western drugs) were first-time negotiation and 27 drugs (22 western drugs) were re-negotiation

• Among the 74 western drugs, 51 drugs come from MNC pharmacos and 23 come from local biotechs and local pharmacos

Magnitude of price reduction %

Breakdown of NRDL-negotiation drugs by TA, western drugs only# of drugs

Source: Press search; GBI; McKinsey analysis

McKinsey & Company 8

4: VBP expansion will likely continue to put pressure on LOE originators

Latest policy of VBP expansion

Source: NMPA, McKinsey analysis

1. VBP products include the 25 listed from the first batch 2. Depending on the number of bid winners

2015-19E revenue growth for VBP impacted LOE originators1

B USD, %19%

17

12% 13%

2015

9%

16 18

-1%

2019E

MoleculeUnchanged with 25 molecules

Geographic coverageFull expansion to all provinces

Bidding ruleUp to 3 bid winners and higher guaranteed volume2

25 VBP bids won by 19 pharmacos

Revenue 2.6 2.9 3.3 3.9 3.8

~800M USD missing in

topline

McKinsey & Company 9

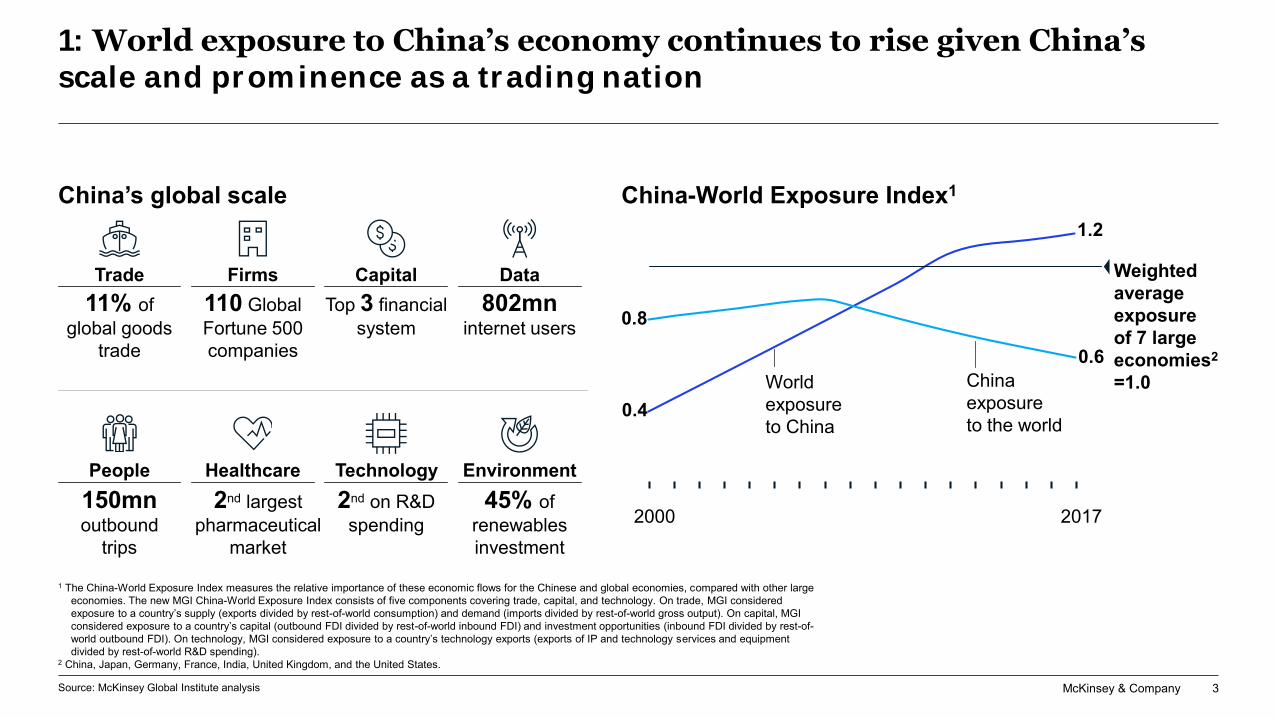

5: A series of favorable policies are opening the floodgates for digital healthcare

Source: Press search; McKinsey analysis

The 13th National People’s Congress removed “Prohibition of online Rx drug distribution”in recent revision of the Drug Administration Law

Aug 2019 Jul 2018General Office of the State

Council endorsed the legitimacy of online

consultation and published relevant regulations

1. NHSA: National Healthcare Security Administration

Online consultation

Online Rx drug fulfillment

ReimbursementMay 2019General Office of the State Council designated NHSA1

to formulate the reimbursement policy for online consultation

Long termRegional pilots on

reimbursement for online Rx drug in select cities; time

required for national rollout

McKinsey & Company 10

6: Biosimilars at the gate – a significant number of competitors jockeying for position

Crowded local biosimilar pipeline targeting high-profile biologics

1. The average only includes the 8 local biopharma companies listed on this page | 2. Henlius’ biosimilar was priced at RMB 1398 for 100ml dosage, 42% lower than MabThera 100ml.

Pricing pressure on Loss-Of-Exclusivity originators

42% lower2 than MabThera

Number of biosimilars pipeline

4 on average1 for selected molecules

Accelerated registration approval

Indication extrapolation allowedfor approved biosimilars

Phase III NDA Approval

Source: CHP; GBI; press search; McKinsey analysis

McKinsey & Company 11

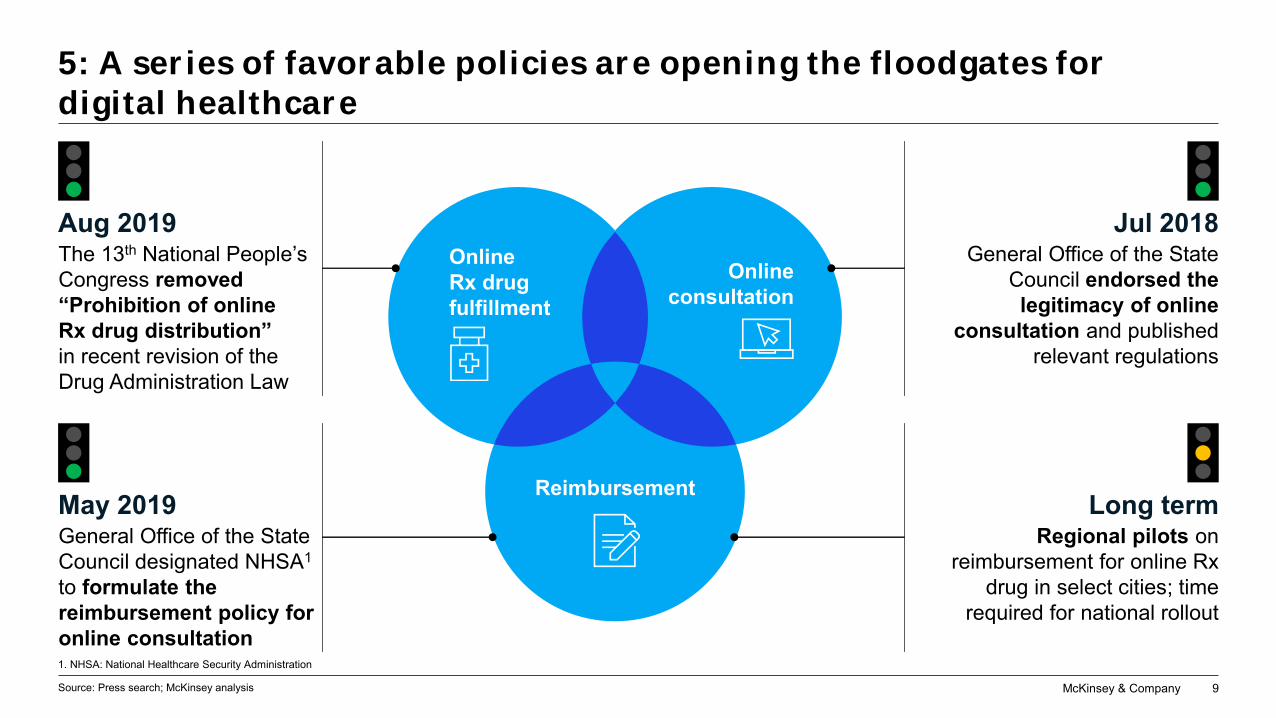

7: Capital market continues to provide diversified financing channels for biotech startups

Source: BCIQ; Wind; Press search; McKinsey analysis

1. As of Nov 2019; 2. Early stage defined as pre-A and A series VC funding; Late stage defined as pre-B, B, and later stage of VC funding; 3. Does not include established local pharma (e.g. Hansoh). STIB: Science Technology and Innovation Board

Early stage VC funding2 Late stage VC funding2 IPO

2019 Chinese biotechs fundings1

9 deals

Median size: 26M USD

17 deals

Median size: 55M USD

8 IPOs3 (7 HKEX 1 STIB3)

Average market cap: 1.5B USD

Oct

Nov

Feb 1.4B

1.0B

0.5B

Jan

Oct

May

160M

60M

28M

Apr

Oct

Jul

26M

132M

17M

…

…

…

…

…

Mar 1.1B

…

McKinsey & Company 12

8: Resurgence in external innovation investments – wave of new openings by leading MNCs

Source: Press release

1 With China International Capital Corporation.

Signed settlement contract to open Global Research Institute in Suzhou that focuses on oncology, autoimmune, and metabolic diseases.

Opened INNOVO Innovation Platform in Beijing to partner

with local academic institutions and start-ups.

Opened Innovation hubs in Shanghai and Guangzhou for collaborations

across start-ups, academic institutions, and local government.

Opened the Roche Innovation Center Shanghai focused on

antibiotics, Hepatitis B, and autoimmune diseases.

Opened JLAB in Shanghai, 1st

one outside of North America to incubate start-ups.

Opened I-Campus in Wuxi; launched a $1bn USD fund1 to invest in local start-ups; announced plan to upgrade current R&D platform and set up an AI-Innovation center in Shanghai.

November 2018 June 2019 September and November 2019

October to November 2019October 2019March 2019

McKinsey & Company 13

9: New deal / partnership models emerging with changing China pharma landscape

Source: Press search; McKinsey analysis

Example deals

Shedding of mature brands

Partnership for mature portfolio

Acceleration of local Gx/ biosimilars

Strategic partnership for China market

Local pharmacos form partnership to develop biosimilars and Gx for China, in particular with Indian companies

Description

MNC pharmcos out-license and spin off mature products to better focus on innovative portfolio

MNC pharmacos complement mature products with other products in the same TA to maximize the value of existing commercial engine through portfolio play

MNC pharmcos build strategic partnership with local partners, to rapidly expand footprint in China ~20 pipeline assets

20.5% stake

McKinsey & Company 14

The great decoupling and expectations of China

McKinsey & Company 15

A brief history of MNCs commercial performance in China

20072002 2003 20082004 20112005 2006 2010

15

2012 2013 2014 2015 2016 20172009

10

2018

20

20190

5

25

30

35

+23% p.a.

+31% p.a.

+12% p.a.

+23% p.a.

Source: Industry association; McKinsey analysis

1 Only include MNCs in the industry association database

Top 15 MNC pharma companies, China Rx sales1, $bn USD

~6bnadded in 2019

with 23%YOY average growth

Relevance era Hyper-growth era Rebalancing era Global stage era

China appears on the global map

Some invest aheadof the curve

China’s economic boom

Healthcare reform kicks off

Large and rapid field forces expansion

Access initiatives

Market turbulences

Uncertainty on innovation

Closer look at productivity

Rebalancing of investments

Accelerating innovation and growth

“Second launch” of NRDL products

McKinsey & Company 16

From “Key Market”

to “Top 2 Global

Priority”

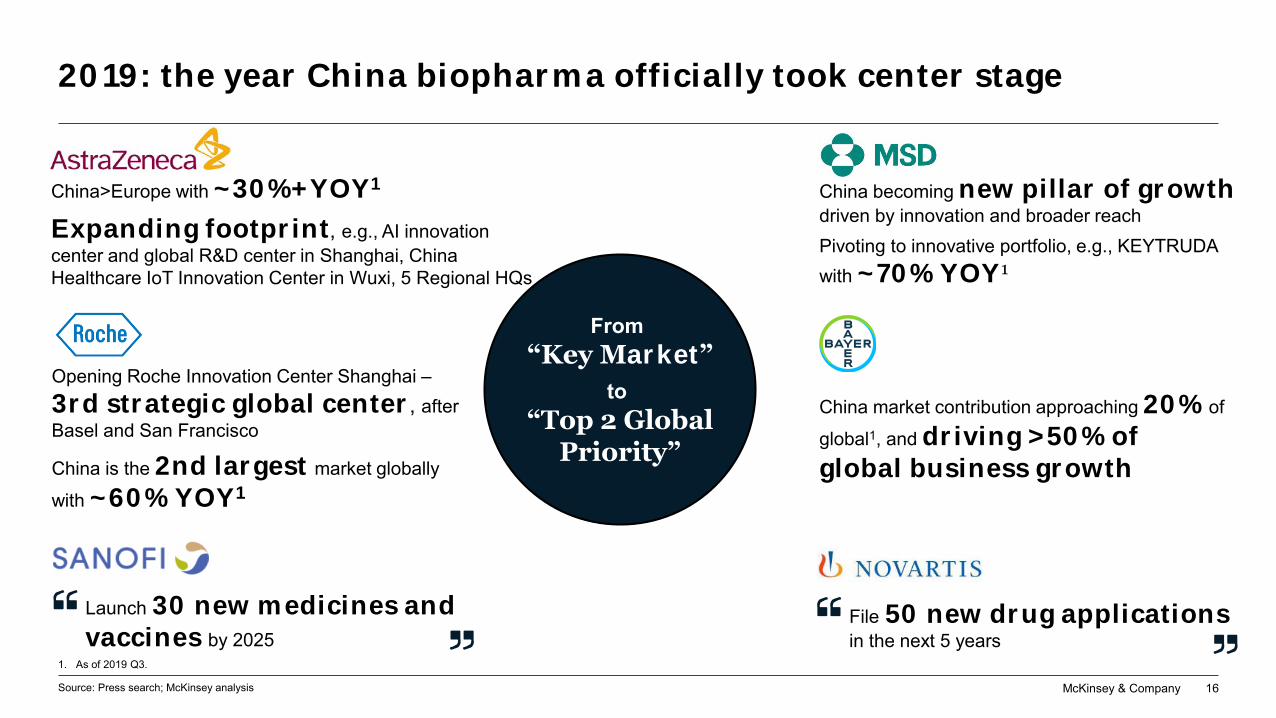

2019: the year China biopharma officially took center stage

Source: Press search; McKinsey analysis

China>Europe with ~30%+YOY1

Expanding footprint, e.g., AI innovation center and global R&D center in Shanghai, China Healthcare IoT Innovation Center in Wuxi, 5 Regional HQs

Opening Roche Innovation Center Shanghai –3rd strategic global center, after Basel and San Francisco

China is the 2nd largest market globally

with ~60% YOY1

1. As of 2019 Q3.

China becoming new pillar of growthdriven by innovation and broader reachPivoting to innovative portfolio, e.g., KEYTRUDA with ~70% YOY1

Launch 30 new medicines and vaccines by 2025

File 50 new drug applications in the next 5 years

China market contribution approaching 20% of

global1, and driving >50% of global business growth

McKinsey & Company 17

Established portfolio brands still account for 80% of revenues; however innovative portfolio brands are growing 10X faster

26.7(787)

6.5(183)

Source: Industry association; McKinsey analysis

16%

Selected MNC pharma China revenue, 2019E1, $bn USD

155%

YOY growth 2018–19E1XX%,

2010 2019

1 2019E sales are extrapolated based on 2018 sales and first 3Q 2019 vs first 3Q 2018 growth rate; covering companies included in industry association report.2 Using 2010 as a proxy and arbitrary cutoff for innovation.

MNC pharma revenue in China could reach ~33.2bn in 20191

Established portfolio – defined as products launched before 2010 - account for ~26.7bn (~80%), growing at 16%

Innovative portfolio – defined as products launched since 2010 - account for ~6.5bn (~20%), growing at 155%

Launchtime

Innovative portfolio2Established portfolio

# of brands(XX),

McKinsey & Company 18

Portfolios can be further disaggregated in four key segments with varying dynamics and outlook

2.0

4.6 (23)

22.1 (764)

0.3

3.2 (37)

1.0

26.7

Impacted by VBP

2

3

Source: Industry association; McKinsey analysis

2015

NRDL

1

6.5

-5%

288%

85%

1 2019E sales is extrapolated based on 2018 sales and first 3Q 2019 vs first 3Q 2018 growth rate; covering companies included in Industry association report.

Innovative portfolio1 New launch since 2015

Significantly improved launch performanceStrong growth driver of many MNCs

2 NRDL listingAcceleration in the NRDL listing for innovative portfoliosA chance of “second launch” for innovative products from earlier years

Established portfolio3 Volume-based purchasing impact

Implementation expanding nationwideMolecule number and category expansion in foreseeable future

EP impacted by VBP NRDLEP not yet impacted by VBP New launch

22%

Innovative portfolio non-NRDL

194%

Not yet impacted by VBP

Selected MNC pharma China revenue, 2019E1, $bn USD

Launchtime

2010 2019

YOY growth 2018–19E1XX%,

Innovative portfolioEstablished portfolio

4

4 Under threat of future volume-based purchasing expansion

(105)

(41)

# of brands(XX),

McKinsey & Company 19

1: Despite gaps with developed markets, relative launch performance in China has improved in the past few years

New launch

Source: Company reports; EvaluatePharma; Fuji Keizai; Industry association; Prospectus; Testa Marketing; WHO (2014); McKinsey analysis

Launch performance of selected drugs1 across markets

1,600

Y5Y4Y2Y1Y0 Y3 Y3Y0 Y5Y4Y1 Y2 Y0 Y3Y1 Y4Y2 Y5

XX Relative average sales

1x ~2x ~5x

Selected Examples

Recent launch performance in China has improved compared to historical launches

Recent

Japan ~2x of China

United States ~5x of China

Historical

Japan ~6x of China

United States ~30x of China

1. Newly launched drugs (since 2015) with largest sales and at least three years of sales numbers.

McKinsey & Company 20

1: Not all launches are equal: oncology launches generally have steeper launch curve than non-oncology ones

Launch year Year 1 Year 2 Year 31. Sales ranking based on 2019 H1 Industry association data, 2019 full year sales predicted from 2019 H1 sales if needed; 2 Co-developed by Lilly and Innovent

Onco average Non-onco average2018

2018

2018

2018

20182

2017

2017

2017

2018

2015

Source: Industry association; McKinsey analysis

Product profile and local market potential are important differentiation factors for launch performance

Company’s launch excellence capability further differentiates successful launches from the crowd

McKinsey & Company 20

Sales of top 5 oncology / non-oncology new launches1

~6x Average sales of oncology vs. non-oncology new launch at Year 2

New launch

McKinsey & Company 21

2: Improved market access results in shorter timelinesto reimbursement

NRDL

Time lag between launch and NRDL inclusion is shortening

Brand Time lagYears

Brand Time lagYears

Source: CDE; GBI; EvaluatePharma, Industry association, McKinsey analysis

15.0

Brand Time lagYears

2017 Batch 2018 Batch 2019 Batch

2.0 1.0 1.0

4.0 1.0 1.0

4.0 1.0 1.0

… … …

8.7 5.3Average 4.5

7.0 2.0Median 2.0

36 17# Negotiation drugs 521

18.0 19.0 16.0

1. Not including TCM

McKinsey & Company 22

2: 2019 NRDL negotiation scaled up in breadth and depth

Source: Press search; McKinsey analysis

Larger scale negotiation with new model being tested

• Since 2017, NRDL negotiation list has expanded three times

• New negotiation model, i.e., competitive negotiation, is adopted for HCV drugs. In exchange, government guaranteed no NRDL inclusionof competitor drugs for two years

Broader scope of negotiation

• Indication coverage more evenly distributed across cancer, chronic diseases, and rare diseases, versus prior rounds where half of the negotiation drugs were oncology drugs

• Drugs for HCV, PAH, and Niemann-Pick Disease, and PD-1 (Sintilimab) got on NRDL for the first time

Price cut pressure continues

• Steeper price cut year by year• Drugs in renegotiation after

contract expiration continue to face pricing pressure, with an average price cut of 26% for 2019 contract renewal

McKinsey & Company 23

3: VBP rolled out nationwide with further price reductions, suggesting the potential for greater impact in the future

Impacted by VBP

Source: GBI; press search; McKinsey analysis

Before VBP “4+7” VBP

100

36 32

–64 –68

Comparison of average price level before and after volume-based purchasing1

% price before VBPn=25 same molecules in the two rounds of VBP

VBP implementation expands nationwide

Same list of 25 molecules as initial “4+7” round

VBP implementation rolled out nationwide

Average price cut in the 2nd round of VBP reaches ~68% compared to before VBP—even greater than the 1st round average of ~64% cut1

1 Simple average of 25 molecules in the two rounds of VBP—pricing cut defined as the pricing gap between the VBP tendering price and the average tendering price from 2016 to 2018, non VBP tendering price.

McKinsey & Company 24

3: VBP scale and coverage expected to evolve soon, putting more pressure on established products

Impacted by VBP

Source: Industry association; McKinsey analysis

5-year impact

Likely scenario of VBP impact

Estimated value at stake (2019E1) USD

~55%–60% of total MNC revenue (2019E1)

3-year impactMolecules impactedMolecules impacted

Molecules contributing to top

80% of today’s revenue

Molecules contributing to top

80% of today’s revenue

Solid oral

Sterile injectable

Biosimilars for some leading brands

Molecules contributing to top

60-80% of today’s revenue

Solid oral

Molecules contributing to top

30% of today’s revenue

Sterile injectable

~40%–45% of total MNC revenue (2019E1)~14

bn~18–20

bn1 2019E sales are extrapolated based on 2018 sales and first 3Q 2019 vs first 3Q 2018 growth rate.

McKinsey & Company 25

Decoupling performance among top 10 MNCs is also apparent under those new market condition

1.3

20172016

0.6

1.5

1.4

2018

7.5

2.30.8

2.1

0.3

0.30.3

0.30.1

2019E1

3.8

1 Ranking based on 2019E absolute revenue growth compared to 2018, 2019E sales is extrapolated based on 2018 sales and first 3Q 2019 vs first 3Q 2018 growth rate; covering companies included in industry association report.

Absolute growth in China revenue1

$bn USDGrowth rate (simple average of each archetype)

2018–19E1, YOY“Emerging growth powerhouses” “Mainstay players” “Tracking performers”

Source: Industry association; McKinsey analysis

29% - 2 MNCs

70% - 3 MNCs

19% - 5 MNCs

McKinsey & Company 26

Favorable portfolio composition is necessary yet not sufficient to achieve high growth; many other factors have impact

Emerging growth powerhouses

Mainstay players

Tracking performers

Source: Industry association; McKinsey analysis

1 2019E sales are extrapolated based on 2018 sales and first 3Q 2019 vs first 3Q 2018 growth rate; covering companies included in industry association report.2 Including the established portfolio not yet impacted by VBP and innovative portfolio, launched in 2010 to 2015, not in NRDL.

Breakdown of revenue growth for MNC pharma companies in Chinabn USD, %, 2018-2019E1

Characteristics of emerging growth powerhouses—strategy still matters despite the portfolio at hand

Recent launches with steep performance curves

2nd launch success post-NRDL listing

Sustained investments in scale, coverage, and innovative commercial models

21%

1.3

80%

76% 3%

23%

53%

68%

38% 3%

30% 17%

46%13%

16%4%

78%

11%

13%9%

1.5

22%

0.8

79%

2.1

15%

100%

44%43%

0.1

0.6

126%

0.3

0.3

0.3

0.3

NRDLNew launch Impacted by VBP

Others2

McKinsey & Company 27

A rapidly shifting portfolio structure requires ever more dynamic adaptation of strategy and resources

Impacted by VBP NRDL uplift

New launch

Not yet impacted by VBP

20152010 2019

Already decoupling and slowing down Some very large legacy brands Re-invention of GTM model needed

Core business exposed in short to mid-term to expansion of VBP, in particular oral molecules

Growth expected to slow down with some exceptions

Focus of investments

Expected to grow rapidly with healthy flow of new upcoming launches (several 100s in the next 5 years) and improving access environment

Requiring “2nd launch” mind-set Potentially shift significant resource

Innovative portfolioEstablished portfolio

McKinsey & Company 28

Portfolio archetypes and strategic implications for companies moving forward

EP impacted by VBP NRDLEP not yet impacted by VBP New launch

Decoupling of portfolio performance is happening now and will have much greaterimpact soon

Accelerated transition to innovation more critical now than everCompanies with deep pipeline of innovative drugs are likelyto become the next generationgrowth powerhouses

High VBP exposure

Launch engine

Balanced portfolio

Typical portfolio archetypes…. …have profound implications on strategic options

Acceleration of innovative product approvals (including integrated development capabilities), new product launch excellence, and NRDL capabilities will be key for future success

Rethink operating model to mitigate VBP impact, deepen customer engagement and improve overall organizational effectiveness

McKinsey & Company 29

China taking center stage: We interviewed and surveyed global leaders with accountability for the China market

Structured survey10 leading companies interviewed

McKinsey & Company 30

Top of mind tailwinds and headwinds in China for the next three years

System evolution fueled by digital healthcare infrastructure and novel service model

Innovation hub driven by strengthening local capability and further improving policy environment

Growth engine with demographic shifts and improving reimbursement and affordability

Talent war due to constrained pool and increasing cost

Intensifying competition from both MNCs and local biopharma companies

Pricing pressure from NRDL negotiation for innovative products, and VBP for mature productsPricing pressureproducts, and VBP for mature products

McKinsey & Company 31

4 key predictions for the next 10 years

Strengthened local playersUpgraded industry

Innovation driven growthIncreasingly attractive market

01 02

03 04

▪ More promising market for company with innovative portfolio, driven by larger volume with reimbursement

▪ Actions needed to elevate innovation quality, to avoid hyper competition in certain therapeutic areas

▪ At least one China based company will become a top 10-15 global pharmaco

▪ Attractive in both size and growth potential, no other market has the demographics and the economy scale

▪ To be successful, industry players need to drive greater globalization while still be rooted in China

▪ Shake out as result of VBP will lead to winners and losers in short term, but result in better industry fundamentals in the long term

▪ How healthcare is provided and funded is likely to be re-defined

McKinsey & Company 32

The strategic importance of China affiliate to global keeps rising

Source: McKinsey China and the world 2019 survey

Strategic importance of China (current status)

Strategic importance of China (3-year outlook)

Degree of alignment on China opportunityWe need to up our game in China to drive growth and rethink about our portfolio strategyHighly aligned Lots of debates

1 32

ø1.5

Some degree of alignment

Now China is equally as important as our US market. We used to focus on US, EU and Japan. Now it is more like US and China

Top 3 market Outside of top 10

41 32

ø1.5

Top 5 market Top 10 market

Top 3 market Outside of top 10

41 32

ø1.5

Top 5 market Top 10 market

McKinsey & Company 33

China is becoming a major growth contributor in global market, driven by a more innovative asset centric portfolio

Source: McKinsey China and the world 2019 survey

Early stageNot a main growth pillar

Top 3 growth contributor

3baseline-1-2-3 21

ø1.7

China growth contribution to global market

Decrease by more than 5%

Increase by more than 5%

3baseline-1-2-3 21

Ø 1

Stay at current level

Size of the prize – change in the China contribution to global revenue comparing to 2018

China contribution to global will increase 1-3%. Historically China has a long time lag for launching innovative products, but things have changed now

Innovative portfolio contribution to revenue change in 3 years

Ø 1.8

Innovative portfolio contribution will grow by in the next 3 years. Chinese government has done a great job in balancing cost while providing reimbursement for innovative products

Decrease by more than 10%

Increase by more than 30%

Stay at current level

Increase by 10-30%

China today is the second biggest affiliate, only after US. China business is growing at low double digit growth, vs. US is flat – while sales in US is still 4-5x larger than China

Decrease by 1-3%

Decrease by 3-5%

Increase by 1-3%

Increase by 3-5%

1 2 3 4

McKinsey & Company 34

China’s role in global R&D expected to expand

Source: McKinsey China and the world 2019 survey

China to build functional CoEs to support global programs We’ve been a bit skeptical as our research center in China is not on par with our headquarter and US centers. Therefore, we are starting off with pilots today and will gradually roll out to scale

China to help accelerate global enrollment

China has the unique advantage to help accelerate global patient enrollment. We will put more focus on that in the future

Status quo In 3 years

China to lead global programs for a given asset

Not a strategic objective

Rolled out at scale

41 32

Not happening yet

Pilot in limited scale

We expect China to play a much more strategic role in clinical development moving forward, with China possibly leading select global programs

Not a strategic objective

Rolled out at scale

41 32

Not happening yet

Pilot in limited scale

Ø2.4 Ø3.3

Not a strategic objective

Rolled outat scale

41 32

Not happening yet

Pilot in limited scale

Ø2.8 Ø3.5

Ø2.3 Ø3.2

McKinsey & Company 35

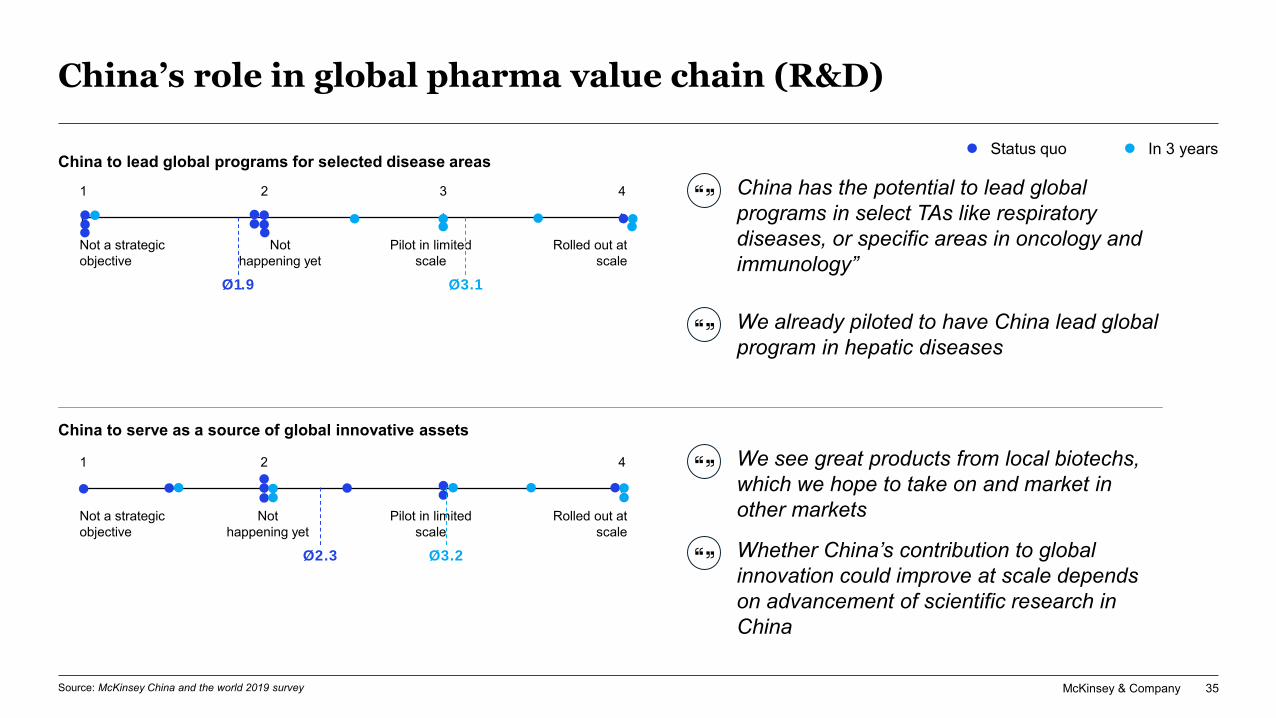

China’s role in global pharma value chain (R&D)

Source: McKinsey China and the world 2019 survey

China to lead global programs for selected disease areasChina has the potential to lead global programs in select TAs like respiratory diseases, or specific areas in oncology and immunology”

Not a strategic objective

Rolled out at scale

41 32

Not happening yet

Pilot in limited scale

China to serve as a source of global innovative assets

We see great products from local biotechs, which we hope to take on and market in other marketsNot a strategic

objectiveRolled out at

scale

41 2

Not happening yet

Pilot in limited scale

We already piloted to have China lead global program in hepatic diseases

Whether China’s contribution to global innovation could improve at scale depends on advancement of scientific research in China

Ø1.9 Ø3.1

Ø2.3 Ø3.2

Status quo In 3 years

McKinsey & Company 36

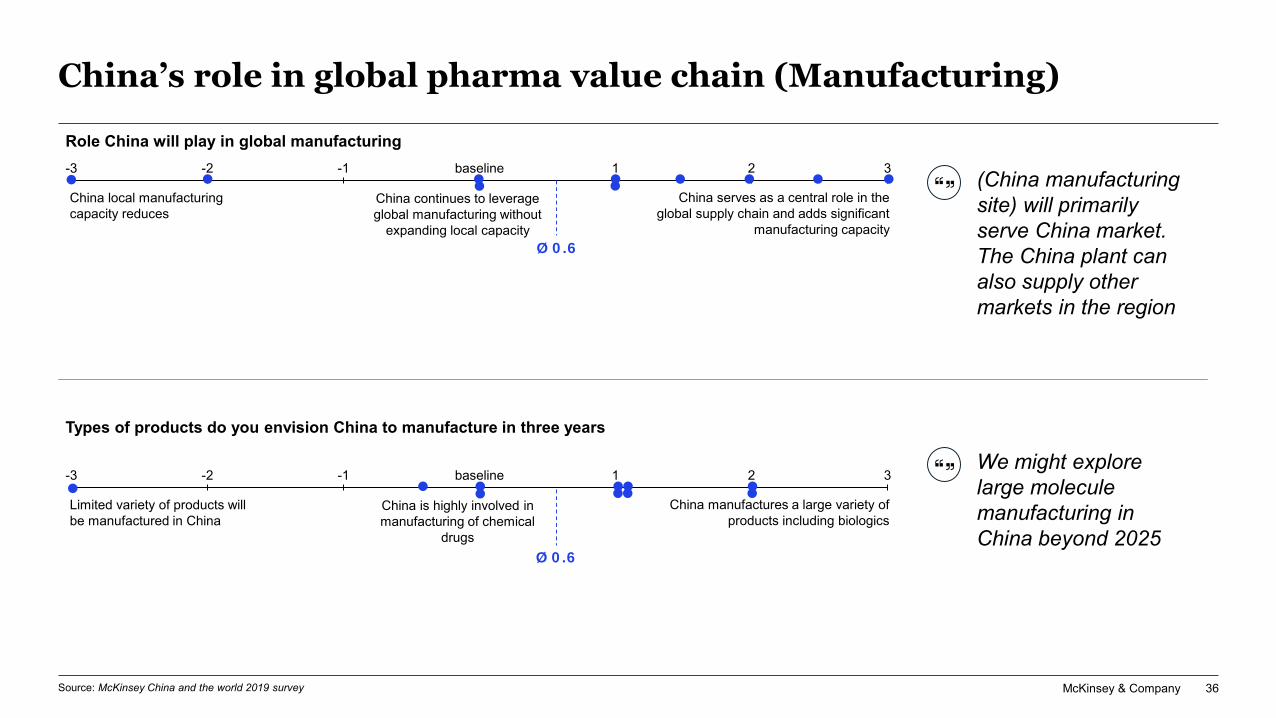

China’s role in global pharma value chain (Manufacturing)

China local manufacturing capacity reduces

China continues to leverage global manufacturing without

expanding local capacity

China serves as a central role in the global supply chain and adds significant

manufacturing capacity

-3 321baseline-1-2

Limited variety of products will be manufactured in China

China is highly involved in manufacturing of chemical

drugs

China manufactures a large variety of products including biologics

-3 321baseline-1-2

(China manufacturing site) will primarily serve China market. The China plant can also supply other markets in the region

We might explore large molecule manufacturing in China beyond 2025

Role China will play in global manufacturing

Types of products do you envision China to manufacture in three years

Ø 0.6

Ø 0.6

Source: McKinsey China and the world 2019 survey

McKinsey & Company 37

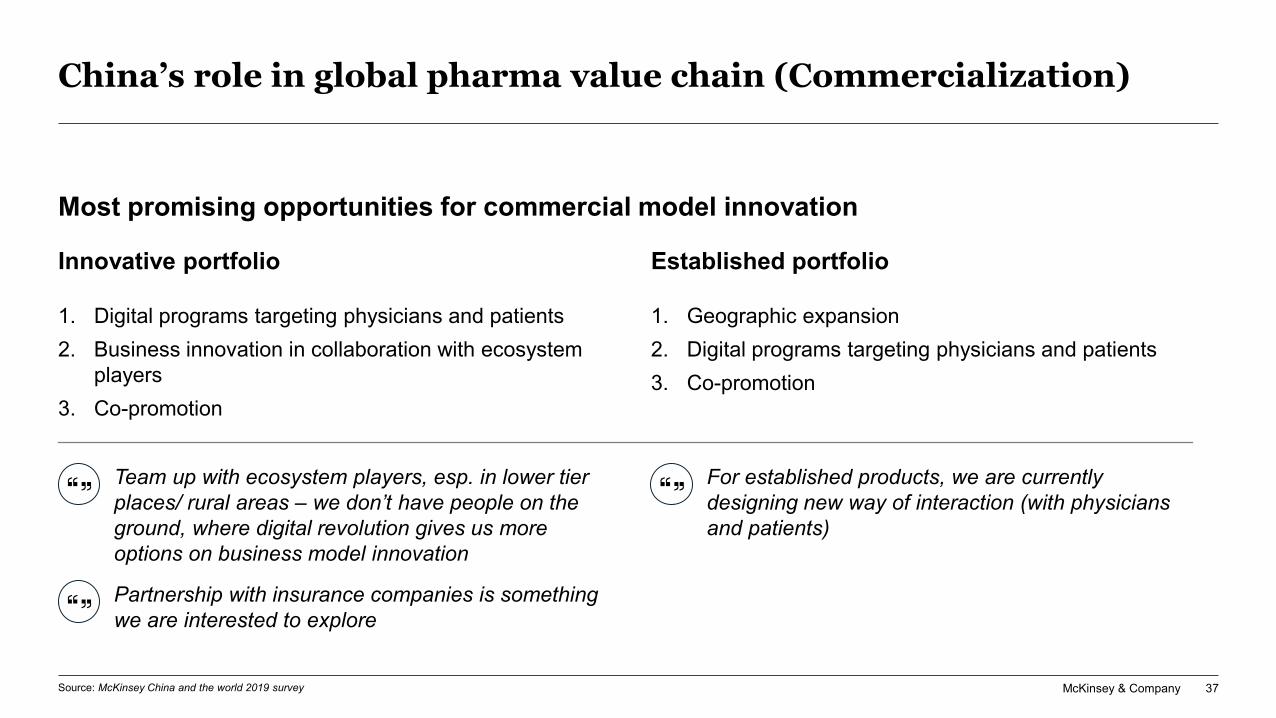

China’s role in global pharma value chain (Commercialization)

Source: McKinsey China and the world 2019 survey

Most promising opportunities for commercial model innovation

1. Digital programs targeting physicians and patients2. Business innovation in collaboration with ecosystem

players3. Co-promotion

1. Geographic expansion2. Digital programs targeting physicians and patients3. Co-promotion

Established portfolioInnovative portfolio

Team up with ecosystem players, esp. in lower tier places/ rural areas – we don’t have people on the ground, where digital revolution gives us more options on business model innovation

For established products, we are currently designing new way of interaction (with physicians and patients)

Partnership with insurance companies is something we are interested to explore

McKinsey & Company 38

China’s role in global pharma value chain (Commercialization)

Pace of commercial model innovation

The pace of commercial innovation will gradually slow down due to failed pilots

Commercial innovation boom will continue at similar pace compared

with today

There will be a significant boost in commercial innovations with disruptive

new models and applications

-3 321baseline-1-2

China innovations largely apply to China only

China becomes the regional innovation hub with best practices

shared within the region

China serves as the global center of excellence in commercial innovation

1 765432

Business model innovation is the right answer. China has spearheaded business innovation

Digital innovation in healthcare is moving fast – China will lead and be able to showcase the rest of the world how to change business model using digital approach

China innovation contributes to regional and global market

Ø 2.2

Ø 4.0

Source: McKinsey China and the world 2019 survey

McKinsey & Company 39

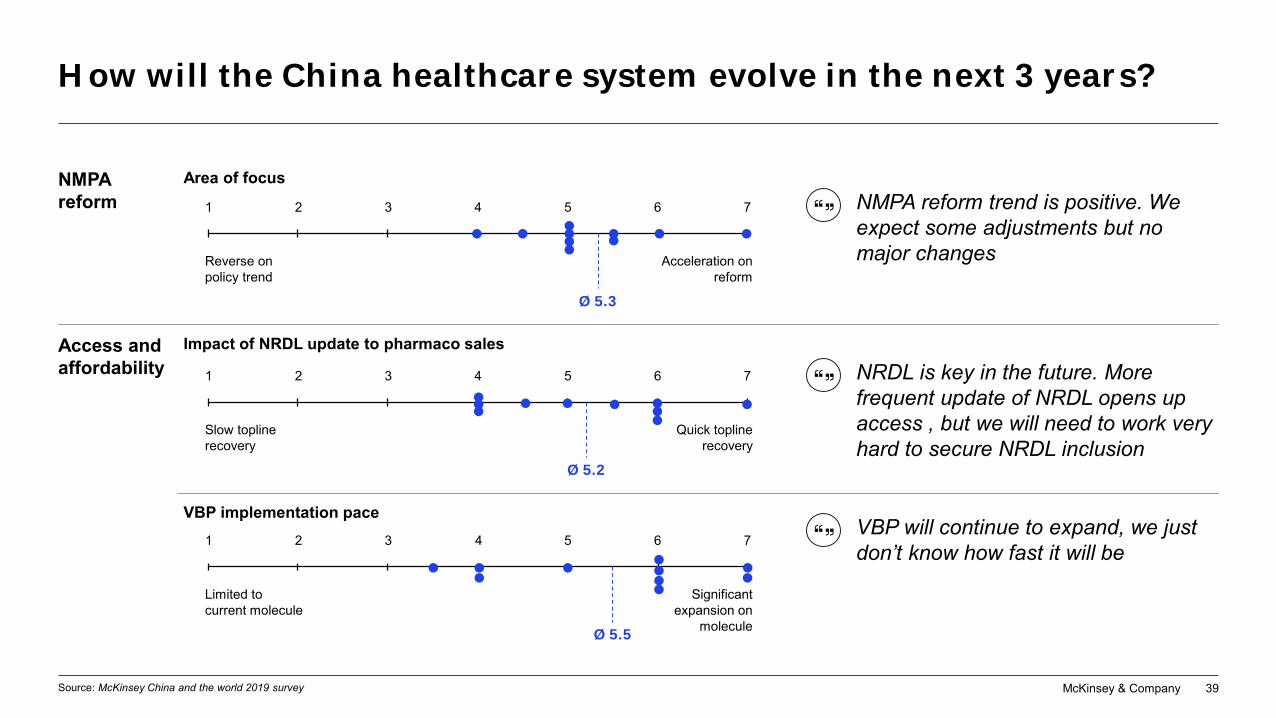

How will the China healthcare system evolve in the next 3 years?

VBP will continue to expand, we just don’t know how fast it will be

NMPA reform

NRDL is key in the future. More frequent update of NRDL opens up access , but we will need to work very hard to secure NRDL inclusion

VBP implementation pace

Limited to current molecule

Significant expansion on

molecule

71 52 63 4

Ø 5.5

Area of focus

Reverse on policy trend

Acceleration on reform

71 52 63 4

Ø 5.3

Impact of NRDL update to pharmaco sales

Slow topline recovery

Quick topline recovery

71 52 63 4

Ø 5.2

Access and affordability

NMPA reform trend is positive. We expect some adjustments but no major changes

Source: McKinsey China and the world 2019 survey

McKinsey & Company 40

How will the China healthcare system evolve in the next 3 years?

We aim to drive a high share of digital touch points, but the question is how

We have more talents today compared to 20 years ago, but local biotech companies are competing for the same pool of talents

Talent

It will take 5-10 years for AI and big data to have real impact in healthcare in China

Share of digital touch points

Small fraction of engagement

Fundamental change

71 52 63 4

Ø 5.3

Industry talent supply

Intense talent war

Sufficient supply of talent

71 52 63 4

Ø 2.9

Role of AI and big data

Limited application

Fundamental change

Ø 5

Digital, big data, AI

71 52 63 4

Source: McKinsey China and the world 2019 survey

Mckinsey & Company 41

Momentum of China biopharma

innovationthrough two lenses

Fresh perspectives on the progress of China’s biopharma innovation ecosystem

01Views of leading China biotech CEOs

02Business strategy and aspiration

Future outlook for innovation

Views of leading China biotech CEOs

McKinsey & Company 42

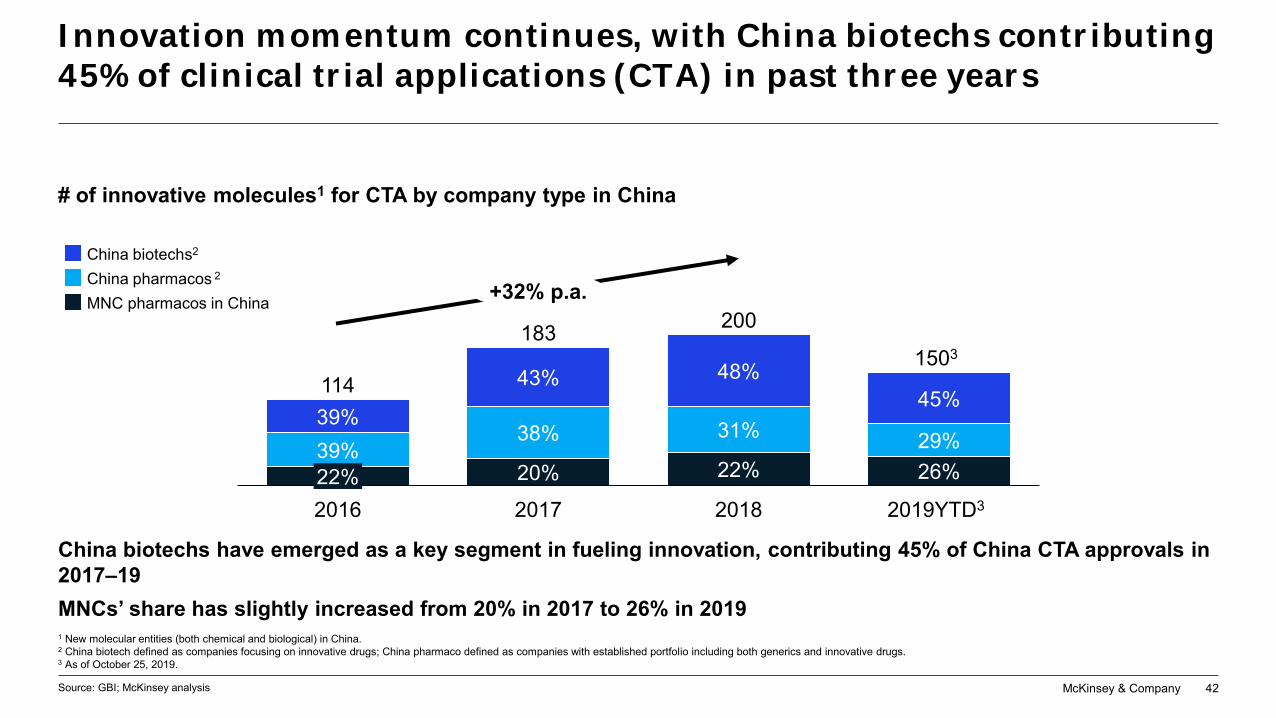

Innovation momentum continues, with China biotechs contributing 45% of clinical trial applications (CTA) in past three years

Source: GBI; McKinsey analysis

# of innovative molecules1 for CTA by company type in China

1503

39%

20%39%

201622%

43%

38%

48%

2017

31%

22%

2018 2019YTD3

114

183 200

29%26%

45%

+32% p.a.

1 New molecular entities (both chemical and biological) in China.2 China biotech defined as companies focusing on innovative drugs; China pharmaco defined as companies with established portfolio including both generics and innovative drugs. 3 As of October 25, 2019.

MNC pharmacos in China

China biotechs2

China pharmacos 2

China biotechs have emerged as a key segment in fueling innovation, contributing 45% of China CTA approvals in 2017–19MNCs’ share has slightly increased from 20% in 2017 to 26% in 2019

McKinsey & Company 43

Oncology continues to account for about half of newly initiated clinical development efforts in China; despite high unmet medical needs, several other important therapeutic areas are attracting less investment

Oncology remains the leading therapeutic area, accounting for half of molecules gaining CTA approval

2016

183

49%

10%4%

4 4

14%

19%

52%

18%

11%11%

7%

15%

9%

17

58%

6%6%

5

18

47%

150

13%9%

2019 YTD3

8%4

18%

114 200

# of innovative molecules approved for CTA1 by TA in China

Total =

1. New molecular entities (both chemical and biological)2. Includes Blood, Musculo-skeletal system, CV, Respiratory system, Dermatologicals, Immune, Genito Urinary System, Sensory Organ, Systematic Hormone3. As of Oct 25th, 2019

Source: GBI; 2019 China healthcare yearbook; McKinsey analysis

Alimentary/Metabolism

CVD

Oncology

Neurology

Anti-infective

Others2

McKinsey & Company 44

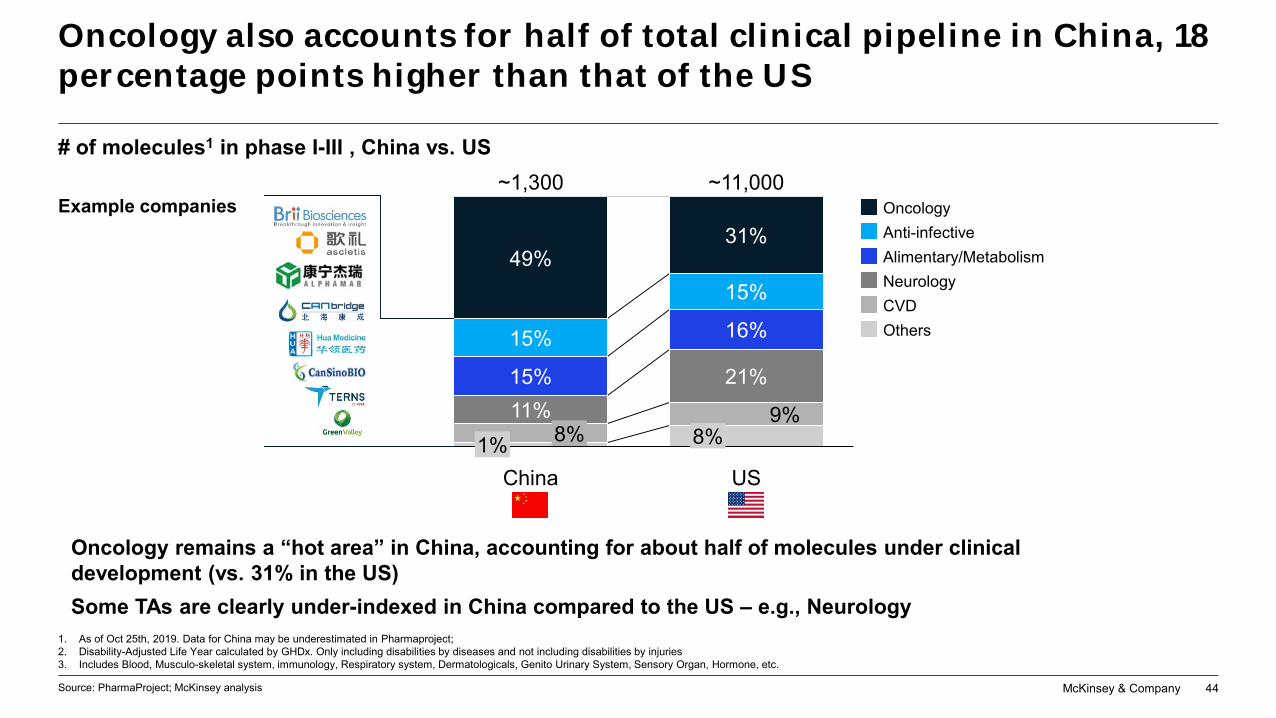

Oncology also accounts for half of total clinical pipeline in China, 18 percentage points higher than that of the US

US

15%

15%49%

China

15%

21%

31%

11%1% 8%

16%

9%8%

~1,300 ~11,000# of molecules1 in phase I-III , China vs. US

1. As of Oct 25th, 2019. Data for China may be underestimated in Pharmaproject;2. Disability-Adjusted Life Year calculated by GHDx. Only including disabilities by diseases and not including disabilities by injuries3. Includes Blood, Musculo-skeletal system, immunology, Respiratory system, Dermatologicals, Genito Urinary System, Sensory Organ, Hormone, etc.

Source: PharmaProject; McKinsey analysis

Example companies Oncology

CVD

Anti-infectiveAlimentary/MetabolismNeurology

Others

Oncology remains a “hot area” in China, accounting for about half of molecules under clinical development (vs. 31% in the US)Some TAs are clearly under-indexed in China compared to the US – e.g., Neurology

McKinsey & Company 45Source: GBI; press search; McKinsey analysis

37

64 72

108

China fromGlobal

3

2017 2018

China toGlobal

2019YTD2

40

7480

+85% p.a.

1. Include deals over development rights and commercialization rights; exclude global deals with China rights. | 2. As of October 25, 2019. Figures may not sum to 100% because of rounding.3. Including CNS, sensory organ, metabolism, CVD, musculo-skeletal system, dermatology, genito urinary system and sex hormones, respiratory system.

Cross-border deals remain active, with China biotechs starting to in-license more non-oncology assets

Breakdown of major licensing deals1

by asset origin, # of assets

8%

49%

5%

Others3

16%

3%

32%

55%

2017

33%

2018

38%

15%

13%

35%

2019YTD2

Oncology

Auto-Immune

AI

37 64 72

Breakdown for “China from global” deals by TA

Owner Acquirer

Upfrontinvestment (USD, M)

15

18

20

2

65

20

Asset

Enoblituzumab

INCMGA0012

BA3071

SPR206/SPR741

Sacituzumabgovitecan

Inebilizumab

In-licensing continues to be the main form of partnership (versus out-licensing), accounting for 90% of cross-border deals

Autoimmune deals are on the rise, poised to become the “next Oncology” in China

Selected Examples

McKinsey & Company 46

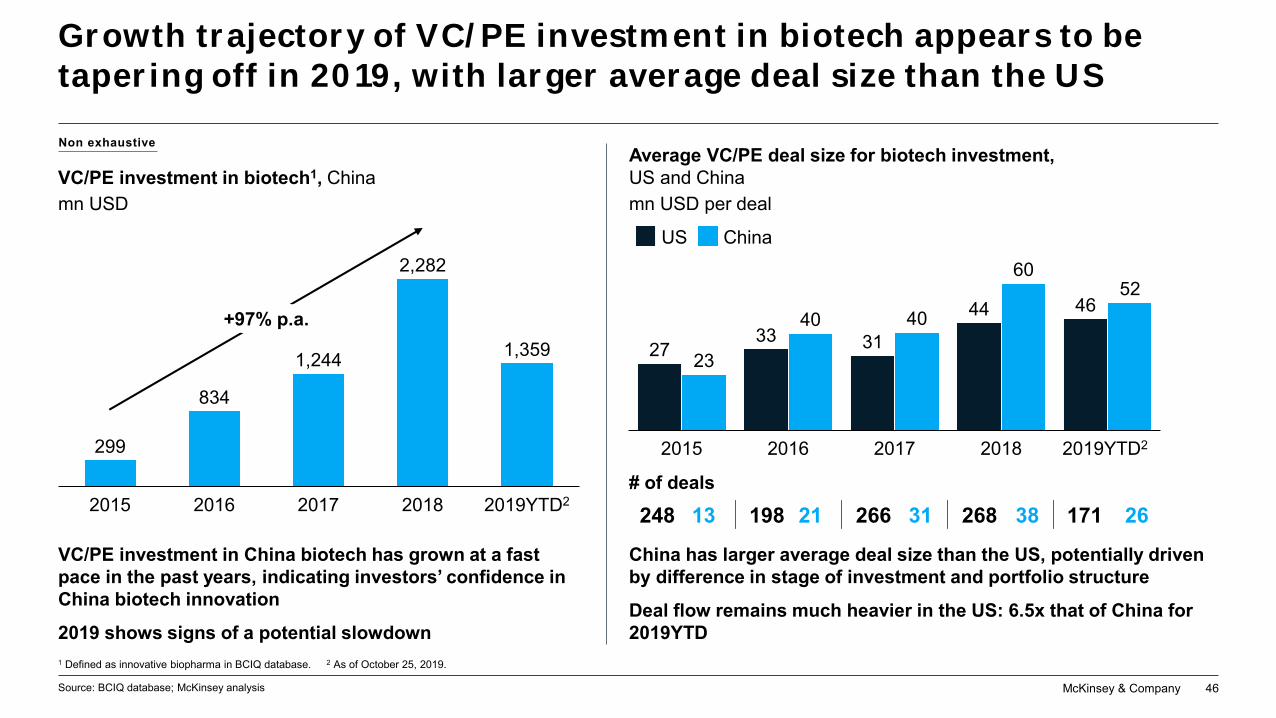

Growth trajectory of VC/PE investment in biotech appears to be tapering off in 2019, with larger average deal size than the US

mn USD per dealmn USDVC/PE investment in biotech1, China

Source: BCIQ database; McKinsey analysis

2733 31

44 46

23

40 40

6052

2016 20182015 2017 2019YTD2

1 Defined as innovative biopharma in BCIQ database. 2 As of October 25, 2019.

US China

Average VC/PE deal size for biotech investment, US and China

VC/PE investment in China biotech has grown at a fast pace in the past years, indicating investors’ confidence in China biotech innovation

2019 shows signs of a potential slowdown

China has larger average deal size than the US, potentially driven by difference in stage of investment and portfolio structure

Deal flow remains much heavier in the US: 6.5x that of China for 2019YTD

834

2019YTD220182015 2016 2017

299

1,244

2,282

1,359+97% p.a.

13 198 21 266 31 268 38 171 26# of deals

248

Non exhaustive

McKinsey & Company 47

HKEX1 and newly launched STIB2 provide much needed funding sources for China biotechs

1. Hong Kong Stock Exchange | 2. China mainland Scientific -Technology Innovation Board | 3. As of November 8, 2019. Using exchange rate: 1USD=7RMB | 4. Prospectus submitted as of November 8, 2019. 5. Haohai Biological Technology is already listed on HKEX .

Source: Press search; Wind

Notable IPOs in recent yearsHKEXNASDAQ STIB

Raised$mn

Market cap3

$bn

More IPOs queuing up—example companies filing for IPO4

5

410

2019.9

3

Henlius

511

2017.6

14

WuXi

150

2017.9

2

ZaiLab

400

2018.8

0.6

Ascletis

110

2018.9

0.9

Hua

400

2018.1

4

Innovent

400

2018.12

3

Junshi

285

2019.2

1.4

CStone

161

2019.3

1.1

Cansino

158

2019.5

0.6

Mab-pharm

180

2019.5

1.0

Viva

150

2019.8

3

Chip-screen

2018.8

12

BeiGene

981

2019.6

18

Hansoh

54

2019.10

1.0

Ascent-age

72

2019.11

0.5

Tot Biopharm

903

5 Bn USD has been raised so far by those biotech companies at IPO and the total market cap for them exceeds 60 Bn USD (as of November 2019)

McKinsey & Company 48

Manufacturing excellence is a must-have for China biotechsLeading biotechs are building up in-house GMP capabilities

Guangdong

Jiangsu

Zhejiang

Shanghai

Suzhou

$10mn initial investment

4.2k sqm

$280mn investment

50k sqm

Annual capacity: 15mn vials

$500mn investment

Annual capacity: 78kl

100k sqm

Annual capacity: 26kl

Shanghai Annual capacity: 20-30 products

Guangzhou $30mn initial investment

100k sqm

Annual capacity: 24kl

Hangzhou $785mn investment

In partnership with Hangzhou government

Source: Company website; literature research; McKinsey pharma manufacturing benchmarks (POBOS)

Leading China biotechs see in-house manufacturing (especially biologics) as a critical capability to remain competitive in the market; quality@scale with competitive cost

Manufacturing sites are concentrated in several hubs such as Suzhou, Shanghai, Hangzhou, and Guangzhou

CMO capacity is also being added (e.g., Lonzain Guangzhou)

Mckinsey & Company 49

Momentum of China biopharma

innovationthrough two lenses

Fresh perspectives on the progress of China’s biopharma innovation ecosystem

01Views of leading China biotech CEOs

02Business strategy and aspiration

Future outlook for innovation

Views of leading China biotech CEOs

McKinsey & Company 50

…sharing their perspectives on

Business strategy and aspiration

The CEOs of 15 leading China biotechs shared their latest perspectives and insights

Outlook for biopharma innovation environment in China

Top operational priorities in light of rapidly evolving environment

CEOs of 15 leading China biotechs…

Source: McKinsey 2019 China Biotech CEO survey

A

C

B

McKinsey & Company 51

A. Business strategy and aspiration at a glance

Source: McKinsey 2019 China Biotech CEO survey

One TA or multiple TAs?

10 out of 15 companies primarily

Innovative drugs or biosimilars?

9 of 15 companies solely focus on

First-in-Class/Best-In-Class or me-too/me-better?

While portfolio novelty varies, biotechs are generally moving towards

4 companies focus exclusively on one TA

focus on 1 TA, of which: innovative drugs

100% first-in-class/best-in-class for late-stage

increasing novelty inearly-stage pipelines

6 companies report 100% first-in-class/best-in-class among their early-stage

assets versus 4 companies reporting

The other 6 mainly focus on innovative drugs, but also pursue biosimilars6 focus heavily on 1 TA while exploring

other synergistic TAs

McKinsey & Company 52

A. Business strategy and aspiration at a glance (continued)

Source: McKinsey 2019 China Biotech CEO survey

In-house or external innovation sourcing?

“Polarized” for late-stage:

China or global? In-house commercial team or partnership?

11 out of 15 companies view China as the most important market, among which 3 companies only play in China

All 15 companies plan to build an in-house commercial team in China

6 of them plan to cover the China market 100% via an in-house sales team, while others are open to leveraging partnership to cover selected TAs/hospitals

In-house manufacturing or CMO?5 companies willrun manufacturing solely from in-house plants

The other 7 companies will rely on in-house plants for commercial-stage products, and CMO for clinical-stage

3 companies will fully leverage CMOs

5 companies source early-stage assets ~1/2 from in-house and ~1/2 from partnership;

Mixed model for early-stage:

fully in-house, while 4 companies developed 100% through partnership

5 companies developed late-stage assets

2 companies source 100% through partnership;

only 3 companies source 100% from in-house

McKinsey & Company 53

A. TA breadth: focused TA strategy is preferred by many

Business strategies and aspiration of leading biotech companies

54321

Single TA Multiple TAsFocus on one TA while exploring other TAs with synergies

3.0Most leading biotechs (10 out of 15) primarily focus on one TA; 2 even focus on a single TACompanies focus on one TA in order to achieve sufficient depth in disease expertise and R&D capabilities

Companies who choose multiple TAs are adopting a “platform” play and hope to diversify risks and avoid placing all the bets in a single TA

“We adopt a different strategy by bringing global FIC assets across TAs to China to diversify risks”

“We used to have multiple TAs but we decided to narrow down to 1 TA so that we can focus our resources. We will keep this strategy in mid future”

What is the TA distribution of your company’s pipeline?

Source: McKinsey 2019 China Biotech CEO survey

McKinsey & Company 54

A. Portfolio mix: Heavy focus on innovation, with few biotechs diversifying with a biosimilar pipelineHow would you describe the mix of your asset portfolio?

Business strategies and aspiration of leading biotech companies

Source: McKinsey 2019 China Biotech CEO survey

Dual focus: innovative and biosimilar

54321

1.7

Purely innovative Mainly innovative, with some biosimilar capabilities

Most leading biotechs (9 out of 15) focus purely on innovative drugs Protected by patent and larger revenue

upside as asset owner Improving government policies that

encourage innovation

However, some companies are keeping biosimilars in the portfolio because they still have market relevance including: Better affordability for patients given lower price Lower risk with proven clinical profiles Potentially, faster adoption upon launch as physicians are

familiar with the products

McKinsey & Company 55

A. First-in-class/best-in-class: China biotechs aspire to higher novelty in portfolios, albeit from different starting points

Source: McKinsey 2019 China Biotech CEO survey

Innovative portfolio mix FIC/BIC versus me-better/me-too

Business strategies and aspiration of leading biotech companies

Key observations

2 types of first-in-class/best-in-class1 models seen amonglocal biotechs License in China rights of global FIC/BIC assets Discover/develop FIC/BIC assets by internally (e.g., via in-

house research team, partnership with academics and other companies)

China biotechs are generally progressing towards more innovative portfolios, as evidenced by more companies reporting 100% FIC/BIC in early-stage versus late-stage assets

0% 100%

54321

3.7

54321

0% 100%

3.5

1 FIC/BIC asset % reported by biotech CEOs, including assets licensed from western companies that are "first to China."

“We still have miles to go to catch up with true innovation, which is based on research capabilities (e.g., knowledge about disease and its pathway). However, some combination trials undertaken by Chinese biotechs could be regarded as best in class”

Among all early- and late-stage assets/combinations, what % would you describe as global first-in-class/best-in-class?

Late-stage

Early-stage

McKinsey & Company 56

A. Ways to source innovative assets: companies are adjusting sourcing strategy for early stage after securing late stage assets

Business strategies and aspiration of leading biotech companies

Source: McKinsey 2019 China Biotech CEO survey

Where do you mainly source late stage assets, e.g. phase II/III?

54321

100% in-house

100% through partnership2.7

Where do you mainly source early stage assets, e.g. discovery, pre-clinical, phase I?

100% in-house

100% through partnership

54321

2.7

“Polarized” innovation sourcing strategies observed for late stage assets4 companies developed late stage assets 100% through partnerships, potentially for faster speed to the market; while 5 companies developed late stage assets 100% in-house

Companies are moving to a mixed model: companies relying 100% on partnerships now are adding more assets developed in-house, similarly for companies at the other end of the spectrum

“A mix of in-house and partnership is the sweet spot where biotechs can enjoy both the benefits of owning innovative assets, and the fast speed to market through partnership”

McKinsey & Company 57

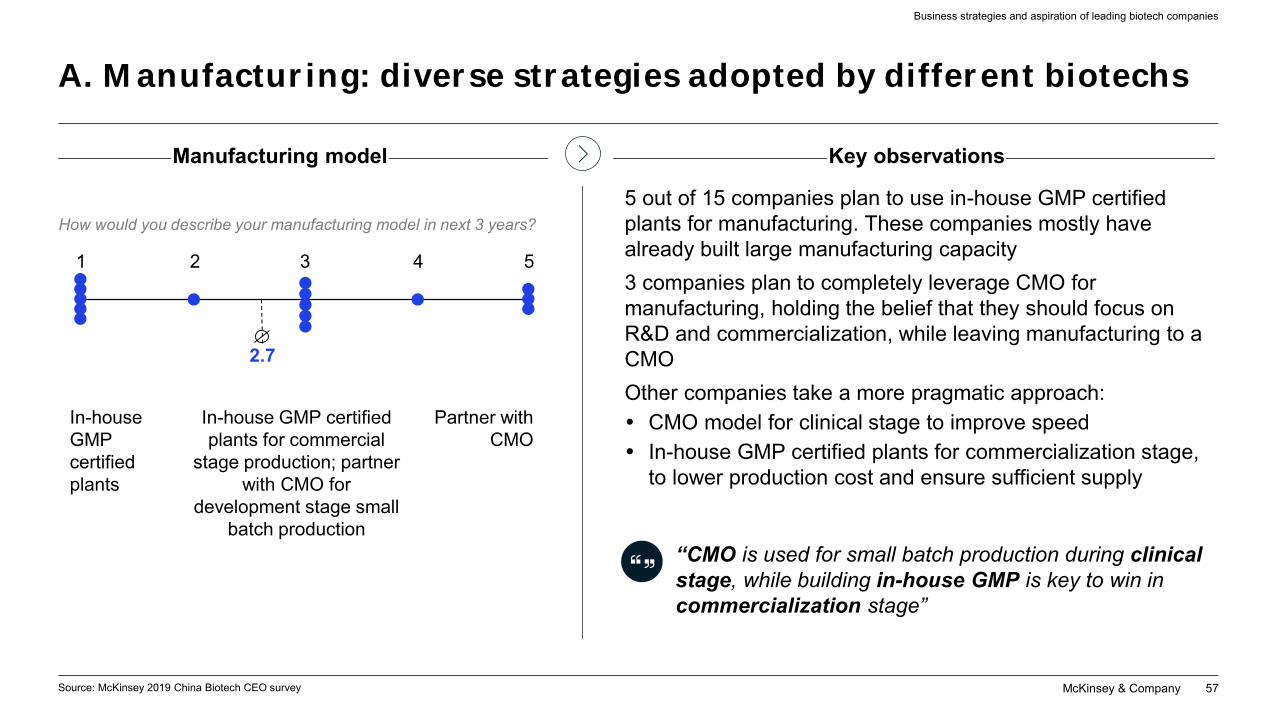

A. Manufacturing: diverse strategies adopted by different biotechs

Manufacturing model

How would you describe your manufacturing model in next 3 years?

Key observations

54321

Partner with CMO

In-house GMP certified plants

In-house GMP certified plants for commercial

stage production; partner with CMO for

development stage small batch production

5 out of 15 companies plan to use in-house GMP certified plants for manufacturing. These companies mostly have already built large manufacturing capacity3 companies plan to completely leverage CMO for manufacturing, holding the belief that they should focus on R&D and commercialization, while leaving manufacturing to a CMO Other companies take a more pragmatic approach: CMO model for clinical stage to improve speed In-house GMP certified plants for commercialization stage,

to lower production cost and ensure sufficient supply

Business strategies and aspiration of leading biotech companies

Source: McKinsey 2019 China Biotech CEO survey

“CMO is used for small batch production during clinical stage, while building in-house GMP is key to win in commercialization stage”

2.7

McKinsey & Company 58

A. Commercial: China remains a “must-win” market, with clear appetite for partnership to expand global footprint and China commercialization

Business strategies and aspiration of leading biotech companies

Source: McKinsey 2019 China Biotech CEO survey

100% through in-house sales team

100% through partnerships

54321

2.1

In-house sales team for selected TAs or

accounts; rest through partnerships

China market only

China and selected high potential

global markets

54321

China as the most important market while exploring opportunities in other markets

2.9

Biotechs aim to build up in-house sales teams in China as they scale up, with many open to partnerships to drive market penetration in a highly competitive market

Aspiration on global commercial footprint varies; majority view China as the primary focus while ex-China expansion is viewed as an opportunistic play where synergies exist

“We will focus on the China market as our starting point and home market. For ex-China key markets, we will likely leverage partnerships for coverage to maximize our product potential.”

Global commercial footprint aspiration: what is your commercial footprint aspiration in the next 3 years?

“Our company focus is on specialty care. We don’t need to cover that many hospitals, and we hope our sales team has deep TA knowledge. Hence an in-house sales team is a better choice.”

Commercial model in China: how do you envision your sales-coverage model in China in the next 3 years?

McKinsey & Company 59

B. Four common operational priorities among China biotech CEOs

Top operational priorities for biotech companies in the evolving industry environment

1. Define and implement clear portfolio strategy aligned with company's core competencies1

4. Evolve organization (e.g., structure, processes, culture) to ensure both stability and agility as business scales up4

3. Build and enhance critical capabilities, e.g., clinical development, manufacturing, and commercial3

2. Form strategic partnership(s) to support company strategy2

4 common themes identified as operational priorities for biotech CEOs(more than 50% of respondents choose these 4 factors as their top 3 most important priorities)

Other important factors include:

• Fundraise to secure sufficient funding for continued operation (4 votes)

• Develop winning “talent formula” to attract, develop, and retain high quality talent in a highly competitive environment (4 votes)

• Optimize governance model and decision-making process to maximize efficiency (3 votes)1 11 votes.

2 8 votes.3 7 votes. 3 ranked this as top 1, 3 ranked as top 2.4 7 votes. 3 ranked this as top 1, 2 ranked as top 2.

Source: McKinsey 2019 China Biotech CEO survey

McKinsey & Company 60

B. Strategic partnership example: BeiGene and Amgen recently formed a broad strategic collaboration in oncology

Top operational priorities for biotech companies in the evolving industry environment

Source: Company announcement; press release

Announced in November 2019

BeiGene to commercialize Xgeva, Kyprolis, and Blincyto in China with parties equally sharing profits and losses

Two parties to collaborate on advancing 20 medicines from Amgen’s innovative oncology pipeline in China and globally

Amgen to acquire 20.5% stake in BeiGene for approximately $2.7bn

Potential benefitsGreatly strengthening BeiGene’s portfolio and commercial momentumAccelerating Amgen's expansion of oncology presence in China

McKinsey & Company 61

C. Future outlook of China biopharma industry as seen by biotech CEOs

Optimistic and conservative views are both seen in the capital market

Uncertain funding environment

More industry leaders conduct clinical trials outside China

Expanding global footprint

Talent shortage in clinical development likely to remain as a big pain point for the industry

Talent shortage

Global first-in-class/best-in-class drugs emerge as China gradually becoming a global source of innovation

Emerging global level innovation

Despite clear challenges, people remain optimistic about the pace of improvement; especially on development infrastructure

Enhancing R&D capabilities and infrastructure

Steady release and implementation of favorable policies (in both regulatory approval and market access) will continue to encourage innovation

Improving policy environmentA B

C D

E F

Source: McKinsey 2019 China Biotech CEO survey; McKinsey analysis

Positive trends Mixed views Challenges

McKinsey & Company 62

C. CEOs anticipate continued improvement of innovation environment; some challenges (e.g., talent) will take time to alleviate

1 Funding: 1 means PE/VC shrinking and IPO opportunities becoming limited; 3 means maintain current level. 2 Talent: 1 means significant shortage; 3 means talents with specific skills in shortage; 5 means sufficient talent supply. 3 Global clinical development footprint: 1 means China-focused, 5 means global expansion.

Global clinical development footprint3

Source: McKinsey 2019 China Biotech CEO survey

How do you think the market environment will evolve in next 3 years?

Market access and reimbursement

Research capabilities

Portfolio mix (FIC versus me-too)

Development infrastructure

Regulatory environment

1 5432

3.6

3.1

Funding1 2.5

3.0

3.3

2.1

2.3

2.7

Policy environment

Funding

Capabilities and infrastructure

Portfolio profile

Most biotech CEOs are confident that policy environment will improve, especially regulatory review and approval

Mixed view on funding environment, half think that funding will become more limitedMost anticipate improving R&D capabilities and infrastructure; more are cautiously optimistic about research capabilities versus development infrastructure improvement

More FIC innovation will emerge in China; more industry leaders will conduct global trials to accelerate clinical development, tapping into larger market potential

1 Maintain current status

5 Significantly improved

Average of responsesxx

Talent

Global footprint

Expected to remain an issue as demand surges

Range of responses

Talen supply for clinical development

McKinsey & Company 63

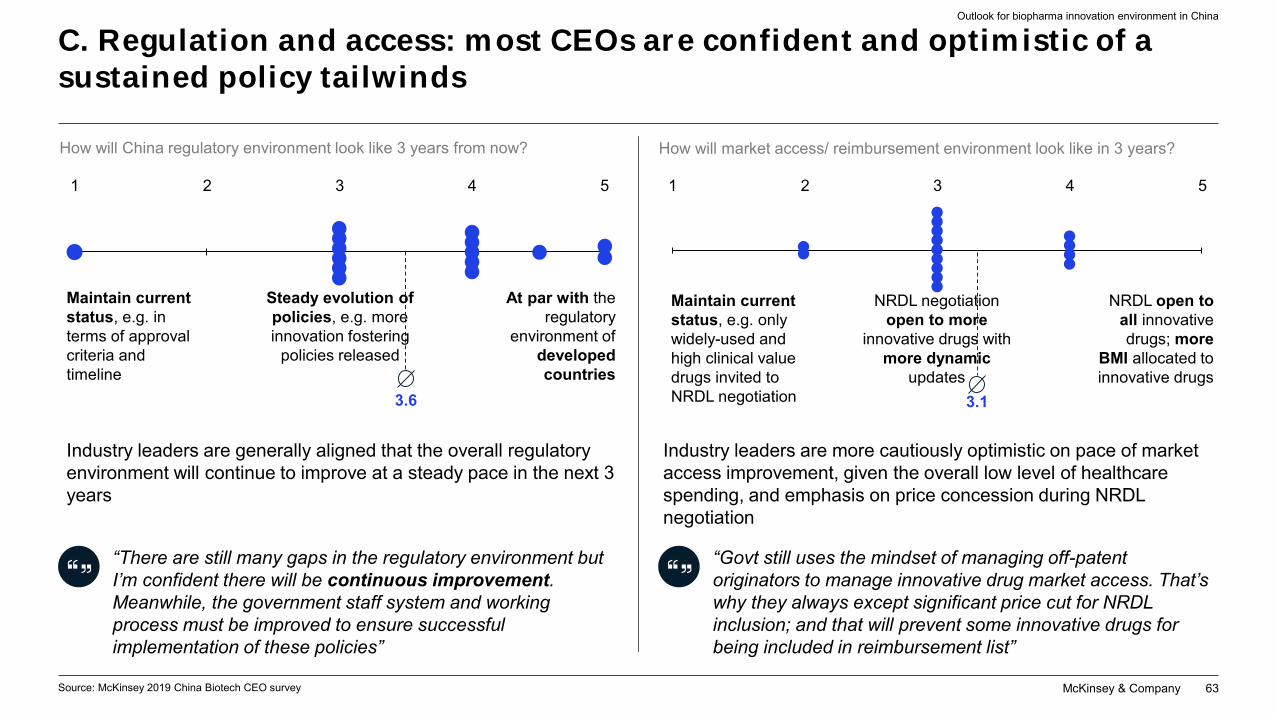

C. Regulation and access: most CEOs are confident and optimistic of a sustained policy tailwinds

Outlook for biopharma innovation environment in China

How will China regulatory environment look like 3 years from now?

Maintain current status, e.g. in terms of approval criteria and timeline

Steady evolution of policies, e.g. more innovation fostering

policies released

At par with the regulatory

environment of developed countries

1 5432

3.6

Maintain current status, e.g. only widely-used and high clinical value drugs invited to NRDL negotiation

NRDL negotiation open to more

innovative drugs with more dynamic

updates

NRDL open to all innovative drugs; more

BMI allocated to innovative drugs

1 5432

3.1

How will market access/ reimbursement environment look like in 3 years?

Industry leaders are generally aligned that the overall regulatory environment will continue to improve at a steady pace in the next 3 years

Industry leaders are more cautiously optimistic on pace of market access improvement, given the overall low level of healthcare spending, and emphasis on price concession during NRDL negotiation

“There are still many gaps in the regulatory environment but I’m confident there will be continuous improvement. Meanwhile, the government staff system and working process must be improved to ensure successful implementation of these policies”

“Govt still uses the mindset of managing off-patent originators to manage innovative drug market access. That’s why they always except significant price cut for NRDL inclusion; and that will prevent some innovative drugs for being included in reimbursement list”

Source: McKinsey 2019 China Biotech CEO survey

McKinsey & Company 64

C. Funding: Level of excitement for funding outlook has scaled back

Outlook for biopharma innovation environment in China

1 5432

Shrinking of VC/PE funding; IPO opportunities restricted to a handful of industry leaders

Maintain current level despite slight structural changes, e.g., VC/PE investment

shrinking yet more IPO opportunities

Significant increase of VC/PE funding and IPO opportunities providing

abundant funding for biotech

Rationale behind optimistic views“IPO bullish” First movers are well-received by the capital market Sufficient demand exists for high-tech companies

including biotechs, driven by the launch of STIBLeaders with good products will prevail to receive sufficient funding even the overall environment is cooling down

Rationale behind conservative viewsOverall funding environment becomes challengingThe excessively high valuation of biotech industry makes it harder for future deals to happenBar becomes higher: investors look for differentiation among early stage companies as the market getting over-crowded with homogeneous competition

2.5

Source: McKinsey 2019 China Biotech CEO survey

How will funding level for biotech industry evolve in the next 3 years?

McKinsey & Company 65

C. CEOs are cautiously optimistic about capability built-up, recognizing that it takes time for China to catch up

Outlook for biopharma innovation environment in China

How do you think the research capability of China will evolve in next 3 years?

No significant improvement from current status

Moderate improvement in # of quality publication and patent converted to

clinical development

Significant improvement, e.g.,

considerable increase in quality publication

and patent conversion

1 5432

3.0

How do you think the clinical development infrastructure of China will evolve in 3 years?

No significant improvement from current status

Moderate improvement in infrastructure, e.g.,

some increase in quantity and quality and of sites

Significant improvement, e.g.,

considerable increase in sites with global

development quality

1 5432

3.3

Research capabilities improvement takes a longer time, as this is more closely related to overall capabilities of university education, basic research, etc.

Clinical development infrastructure will be enhanced driven by demand and supply factors Learning will accelerate driven by large volume clinical trials in

the coming years (including increasing number of early stage studies, and China-led global/regional trials)

New sites are on the initial learning curve of conducting clinical trials and the capabilities are gradually building up

“Research capability improvement is more systematic. It requires the change of the whole education system, research system. And this cannot happen overnight”

Source: McKinsey 2019 China Biotech CEO survey

McKinsey & Company 66

C. Clinical development talent: biggest pain point everyone has to face today and in the near future, calling for an industry-wide solution

Clinical development talent Observations

Average: 2.1

Significant talent shortage due to the surge in demand from NMPA reform and rise of biotech startups

Talents with specific skillsets (e.g., clinical science and regulatory knowhow)may be in shortage, but overall supply should be sufficient

Sufficient supply of

clinical development talents from

increasing talent pool

1 5432

What’s your perspective on the talent supply for clinical development in next 3 years?

Biotech industry is facing talent insufficiency due to surge in demand Very few talents with relevant experience in the market as

biotech clinical trials are still at very nascent stage Significant talent shortage especially for critical positions,

e.g. clinical scientist (which requires interdisciplinary knowhow across science, commercial, and operation to design trials) and trial operation

Lack of training program and certification system On top of that, the clinical trial process and governance

backbone have headroom for improvement in biotech companies

Industry-wide aspiration and collaboration is needed to form ecosystem transformation through a joint effort with government, education platform, and certification system

Outlook for biopharma innovation environment in China

Source: McKinsey 2019 China Biotech CEO survey

McKinsey & Company 67

C. Portfolio mix: CEOs have high aspirations to be more innovative, but also highlight the importance of capturing value from current portfolio

Portfolio mix (FIC/BIC vs. me-better/ me-too) Observations

What’s your perspective on portfolio mix (first-in-class/best-in-class vs. me-too/me-better) of China biotech industry in next 3 years? Industry leaders agree on the steady evolution of first-in-

class/ best-in-class in portfolio mix, but don’t anticipate a rapid shift of portfolio structure in the short term• Me-too/me-better will remain as an important portfolio

strategy as there is still market relevance for me-too/ me-better products in foreseeable future in China

• However, some companies are selectively making efforts to add more innovative drugs to their portfolio

“There will not be leap-frog change in the portfolio mix, constrained by the talent supply andregistration process. At the same time, the capital market is less patient and gives more credits to companies close to commercialization stage, e.g. biosimilar, CRO, me-too companies”

Outlook for biopharma innovation environment in China

Average: 2.3

Maintain current status: focus on me-too/me-better in late stage/ launched products

Reach first in class/best in class in certain TA in

late stage/ launched products

Innovation level reach global leading

position: FIC in multiple TAs/

modalities in late stage/launched

products

1 5432

Source: McKinsey 2019 China Biotech CEO survey

McKinsey & Company 68

C. “Green shoots” of first-in-class drugs developed by Chinese biotechs starting to appear

Source: Literature research

Outlook for biopharma innovation environment in China

1. PIV = Parainfluenza; IFV = Influenza; 2.Fatty Acid Synthase; 3.As of November 2019 4. CDE review is finished and awaiting NMPA approval in China

Company Indication MOAProduct China Stage3

Heart Failure HER2/4 agonist NDA filing

Diabetes GKA agonistDorzagliatin Phase III in China

CNS mGluR5 inhibitorPD-LID Pre-clinical in China

Breast Cancer IRE-1α inhibitorORIN1001 Pre-clinical in China

Nonalcoholic steatohepatitis FASN2 InhibitorASC40 CTA approved

Alcoholic steatohepatitis IL-22 agonistF-652 Phase I

Alzheimer’s disease Gut microbiota remodelingGV971 Conditional approved

PIV/ IFV1 Viral entry inhibitorDAS181 Phase III/ Phase II

NASH/Obesity/ Diabetes GLP-1/GCG activatorPB-718 CTA

Non-exhaustive

Promising gesture from NMPA on conditional approval of GV971 as a way to encourage breakthrough innovation While still a long way to go for Chinese biotechs to fully demonstrate clinical impact of these drugs

MCL BTK inhibitor NDA filing in China4

(Approved in US)

McKinsey & Company 69

C. East goes west? CEOs are not short on aspiration to go global, but China remains must-win for all

Global clinical development footprint ObservationsHow quickly do you expect China biotechs to expand registrational clinical development programs globally?

Average: 2.7

Most players focus on China while industry leaders pilot trials in selected overseas countries

More industry leaders will

conduct global trials for high

priority assets in multiple countries

Most industry leaders will

launch global trials for

multiple assets and in multiple

countries

1 5432

“China is loosening regulations on early stage development; but doing early stage trials overseas still can accelerate registration in China in many cases. Besides, companies also conduct overseas trials to enter those markets and maximize the product potential”

Outlook for biopharma innovation environment in China

China will remain as geographic focus for clinical trials, while more industry leaders will conduct global trials for high priority assets in multiple countries For accelerated registration in China, given less strict

regulation especially on early stage studies To tap into ex-China market opportunities, especially

for assets with global relevance

Source: 2019 China Biotech CEO survey

McKinsey & Company 70

C. Local biotechs are expanding their global presence

Outlook for biopharma innovation environment in China

1. As of Nov 7th, 2019

Overseas clinical trials1

3 trialsIn US, Australia, and New Zealand

39 trials (11 new trials in 2019)Expand to 10 new countries in 2019, reaching 34 in total

6 trials (1 new trial in 2019)In US and Australia

3 trials (1 new trial in 2019)In US and Singapore

10 new countries in 2019: Finland, Georgia, Greece, Hungary, Ireland, Moldova, Portugal, Romania, Singapore, Turkey (all by BeiGene)

3 trials In Australia

2 trials (1 new trial in 2019)In US and Australia

Source: Clinicaltrials.gov; Press search; Company websites; McKinsey analysis

2019 new footprint

McKinsey & Company 71

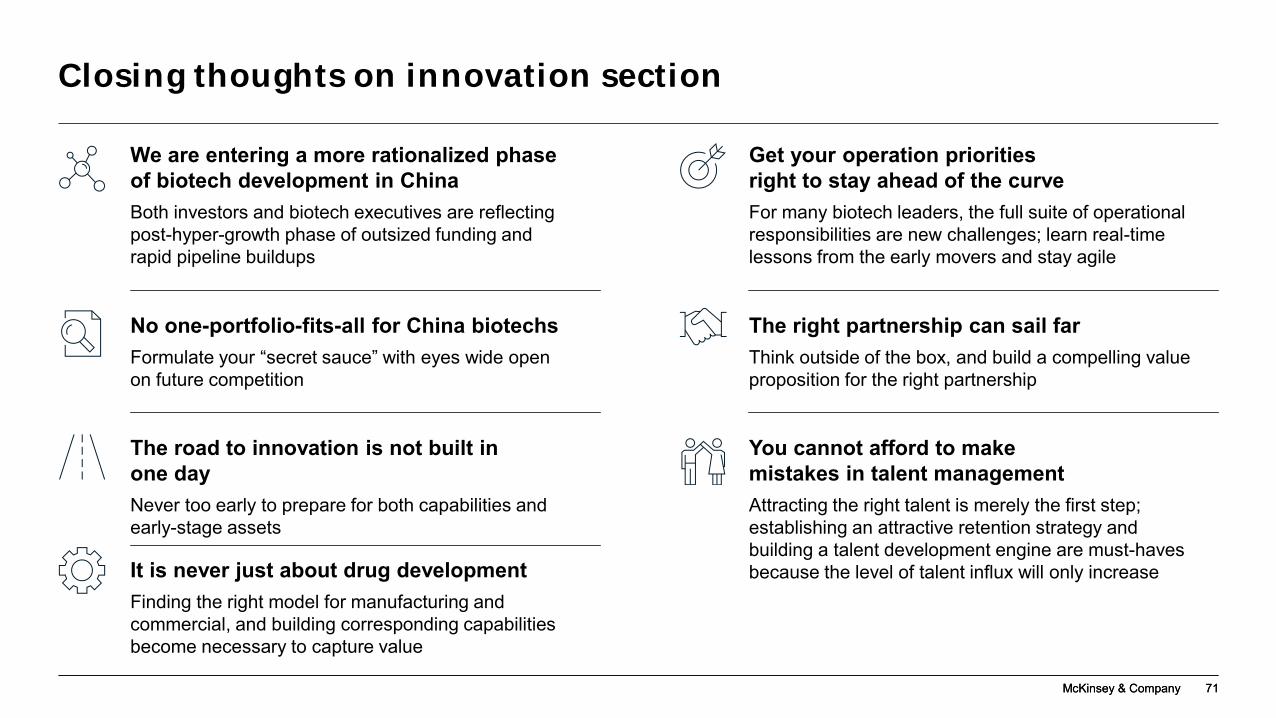

Closing thoughts on innovation section

McKinsey & Company 71

We are entering a more rationalized phase of biotech development in ChinaBoth investors and biotech executives are reflecting post-hyper-growth phase of outsized funding and rapid pipeline buildups

No one-portfolio-fits-all for China biotechsFormulate your “secret sauce” with eyes wide open on future competition

The road to innovation is not built in one day Never too early to prepare for both capabilities and early-stage assets

It is never just about drug development Finding the right model for manufacturing and commercial, and building corresponding capabilities become necessary to capture value

Get your operation priorities right to stay ahead of the curve For many biotech leaders, the full suite of operational responsibilities are new challenges; learn real-time lessons from the early movers and stay agile

You cannot afford to make mistakes in talent managementAttracting the right talent is merely the first step; establishing an attractive retention strategy and building a talent development engine are must-haves because the level of talent influx will only increase

The right partnership can sail far Think outside of the box, and build a compelling value proposition for the right partnership

Mckinsey & Company 72

China oncology market deep dive

McKinsey & Company 73

China has a huge oncology burden to manage

Chinese HCC patients are diagnosed in stage III and IV

15% in US

5% in Japan

55% vs

61% lung cancer patients are EGFR subtype

Late diagnosis

Unique patient profile in selected disease areas

11% in US

Massive disease burden

Different epidemiology

global GC, HCC, and esophageal cancer patients are from China

50% vs

of global total population

Chinese population

18%

5.5people die from cancer every minute in China

1.3from lung cancer

0.8from GC

0.7from HCC

Source: Wang R, Pan Y, Li C, et al. “Analysis of major known driver mutations and prognosis in resected adeno-squamous lung carcinomas;” De Martel et al. “The International Epidemiology of Lung Cancer: Latest Trends, Disparities, and Tumor Characteristics;” “Tumor stage and primary treatment of hepatocellular carcinoma at a large tertiary hospital in China: A real-world study; Global Cancer Observatory;” “China Cancer Registry Annual Report;” press search; McKinsey analysis

vs

McKinsey & Company 74

Improving outcomes and infrastructure due to healthcare reform, but fundamental gap still exists

but

1 Triangulation based on multiple industry reports.2 As of October 25, 2019.

Healthcare infrastructure has also developed

# of oncologists in China per million of population increased

from 14 in 2005 to 26 in 2018

60 in the US

Oncology is one of the fastest growing TAs

14% 2013–18 CAGR, one of the fastest growing TA1

11% of overall pharma market size1

40% of NME approved in 2019YTD2but

Patient outcomes have improved significantly

Lymphoma 5-year survival in China increased from

44% in 2005 to 61% in 2015

94% in the US

Source: Analyst reports; China healthcare statistics yearbook; GBI; press search; McKinsey analysis

McKinsey & Company 75

Bridging from oncology R&D to patient access

Accelerating oncology innovation, bringing many treatment options to patients with high unmet needs

Maximizing commercial

potential through transformative

ecosystem-shaping initiatives grounded

in local context

R&DPatient Access

McKinsey & Company 76

Four key trends in China oncology R&D

Source: McKinsey analysis

A. Tailoring portfolios for success: Both MNCs and local biopharma generally focus on China’s most prevalent tumor types. Some top targets are unique to China.

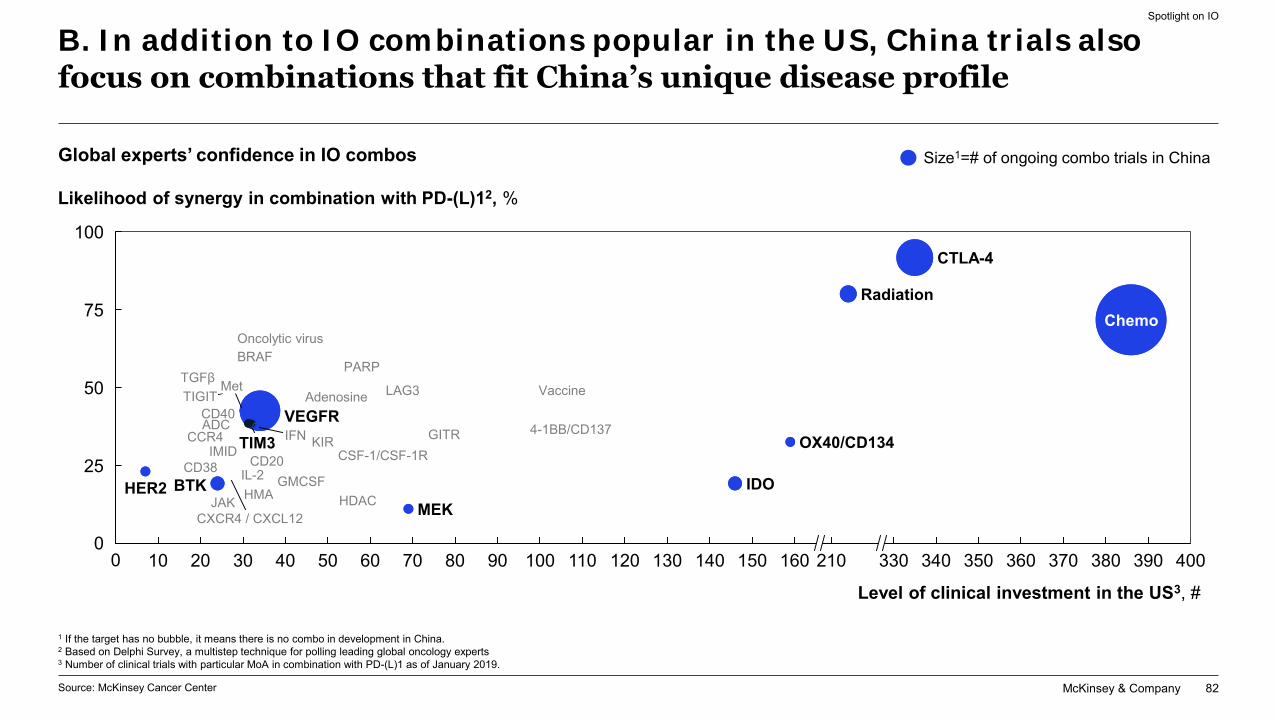

B. Spotlight on IO: IO remains the most active class, with pharmacos tailoring combo strategies to fit Chinese disease profiles.

C. Largest number of cell therapy clinical trials: China has a high level of activity in cell–therapy clinical trials and is emerging as a global leader.

D. Quality to fuel innovation: Quality of local innovation continues to improve, and it is expected to fuel future innovation in oncology.

McKinsey & Company 77

A. Both MNC and local players generally focus on tumor types with high prevalence or proven record of success (e.g., lymphoma) # of innovative assets under development1 for tumor types with high incidence rate2

Oncology pipeline

1 Assets from CTA to NDA filing. 2 Possible double-counting if in clinical trial for several indications. Source: GBI; Global Cancer Observatory; press research; McKinsey analysis

337

111515

24

817

227

27

38

MNC

0

8212

4128

417

43

852

276

712

98

LungCRC

Liver

MM

Stomach

Bladder

Esophagus

Leukemia

Breast

PancreasCervixProstateLymphoma

BrainOvary

Melanoma

Local Incidence, k

774 521 456 393 368 307 116 106 99 93 83 82 76 53 20 7

Total 347 161

McKinsey & Company 78

A. Significant rise in number of MOAs expected, making treatment choices increasingly complexApproved MOAs1 expected (estimated using historical industry attrition rates2 )

Oncology pipeline

64 3

11

6 7

18

8

13

+17% p.a.

+11% p.a.

+23% p.a.

1. Single agent MoA only; Combo MoA is not included.2. Standard attrition rates are applied to estimate new MOA classes from development to launch (Ph3 49%, Ph2, 26%, Ph1 21%). Wong et al., “Biostatistics,” Vol

20, Issue 2, April 2019, Pages 273–86) . NSCLC: non-small cell lung cancer, CRC: colorectal cancer, HCC: Hepatocellular Cancer

Incidence

NSCLC CRC HCC

2018 2023 2025 2018 2023 2025 2018 2023 2025

Source: GBI; Global Cancer Observatory; McKinsey analysis

658k 521k 393k

McKinsey & Company 79

1500 35050 200100 250 300 400 450

40

500 5500

10

20

70

30

50

90

60

80

100

Cumulative industry-wide clinical assets1, %

Targets, #

Source: Pharmaproject; McKinsey China Cancer Center; McKinsey analysis

A: China’s clinical trials are much more concentrated in top targets compared to the US

Oncology pipeline

1. As of October 25, 2019.

xx% Percent of the total targets in development

21% 30%

McKinsey & Company 80

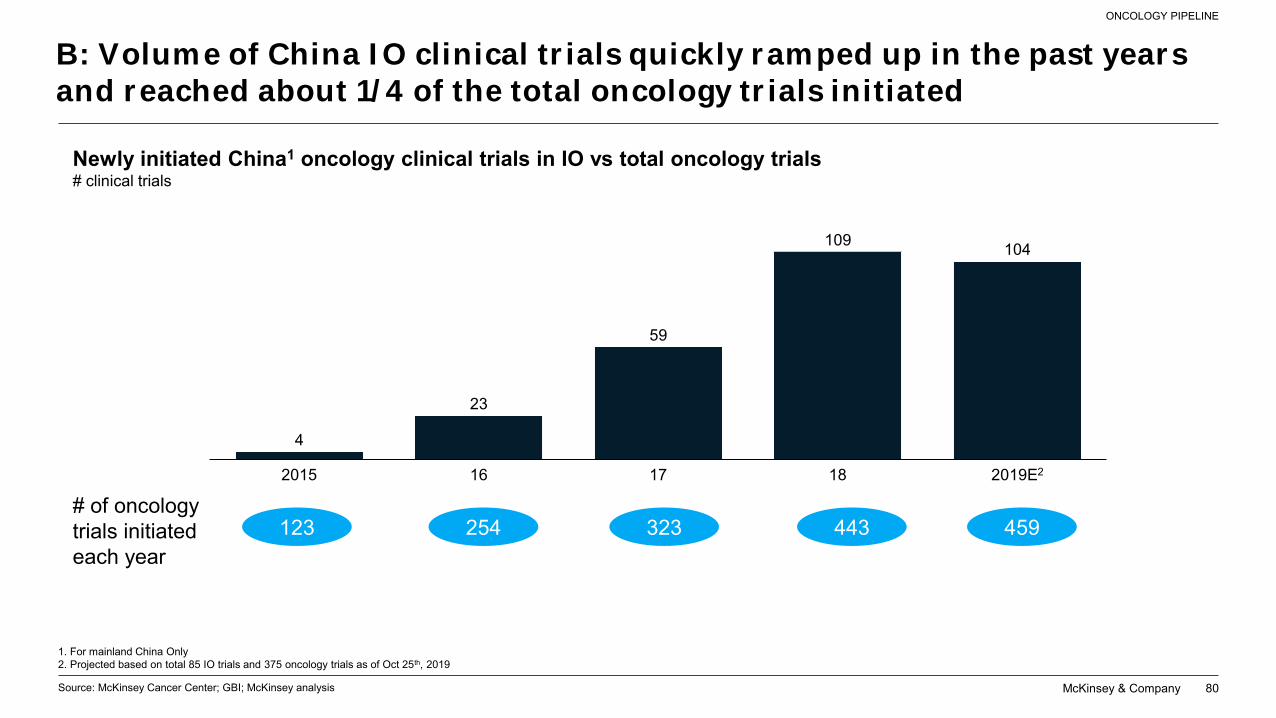

4

23

59

109 104

172015 16 18 2019E2

Newly initiated China1 oncology clinical trials in IO vs total oncology trials# clinical trials

1. For mainland China Only2. Projected based on total 85 IO trials and 375 oncology trials as of Oct 25th, 2019

Source: McKinsey Cancer Center; GBI; McKinsey analysis

B: Volume of China IO clinical trials quickly ramped up in the past years and reached about 1/4 of the total oncology trials initiated

ONCOLOGY PIPELINE

123 254 323 443 459# of oncology trials initiated each year

McKinsey & Company 81

B. China’s IO pipeline focuses on tumor types with high prevalenceActive IO single agent and combo in phase II/III1 trials

Spotlight on IO