Risk and Accounting IFRS 9 Financial...

25

IFRS 9 ‐ Financial Instruments Marco Venuti 2018 Risk and Accounting

Transcript of Risk and Accounting IFRS 9 Financial...

IFRS 9 ‐ Financial Instruments

Marco Venuti2018

Risk and Accounting

Reasons for issuing IFRS 9

Classification approach by IFRS 9

Classification and Measurement of financial assets

Contractual cash flow characteristics test (step 1)

Business model test (step 2)

Fair Value Through Other Comprehensive Income

Fair Value Option

IFRS 9 vs IAS 39: Impairment

Expected loss model

Agenda

Pagina 2

Reasons for issuing IFRS 9Reasons for issuing IFRS 9

3

IAS 39 requirements were difficult to understand, apply and interpret.

The IASB’s objective in issuing IFRS 9 was to develop a new Standard for the financial reporting of financial instruments that is principle‐based and less complex.

IFRS 9 is IASB’s response to the financial crisis and represents a fundamental reconsideration of the accounting for financial instruments.

Main changes in comparison to IAS 39 Classification of financial assets Impairment of financial assets

The deadline for IFRS 9 compliance and implementation is for periods commencing 2018

4

Two criteria for classification of Financial Assets

Solely Payment of Principle and Interest (SPPI test)

Principal: amount transferred by holder (fair value at initial recognition)Interest: consideration for time value of money and credit risk associated with the principal amount outstanding during a particular period of time.

Business Model (BM)

BM refers how an entity managesits financial assets in order togenerate cash flows :• Hold to collect (contractual cash

flow)• Hold to collect and sell• Other Business Model

Classification approach by IFRS 9IFRS 9 replaces the rules based model in IAS 39 with an approach which bases classification and measurement on the business model of an entity,

and on the cash flows associated with each financial asset.

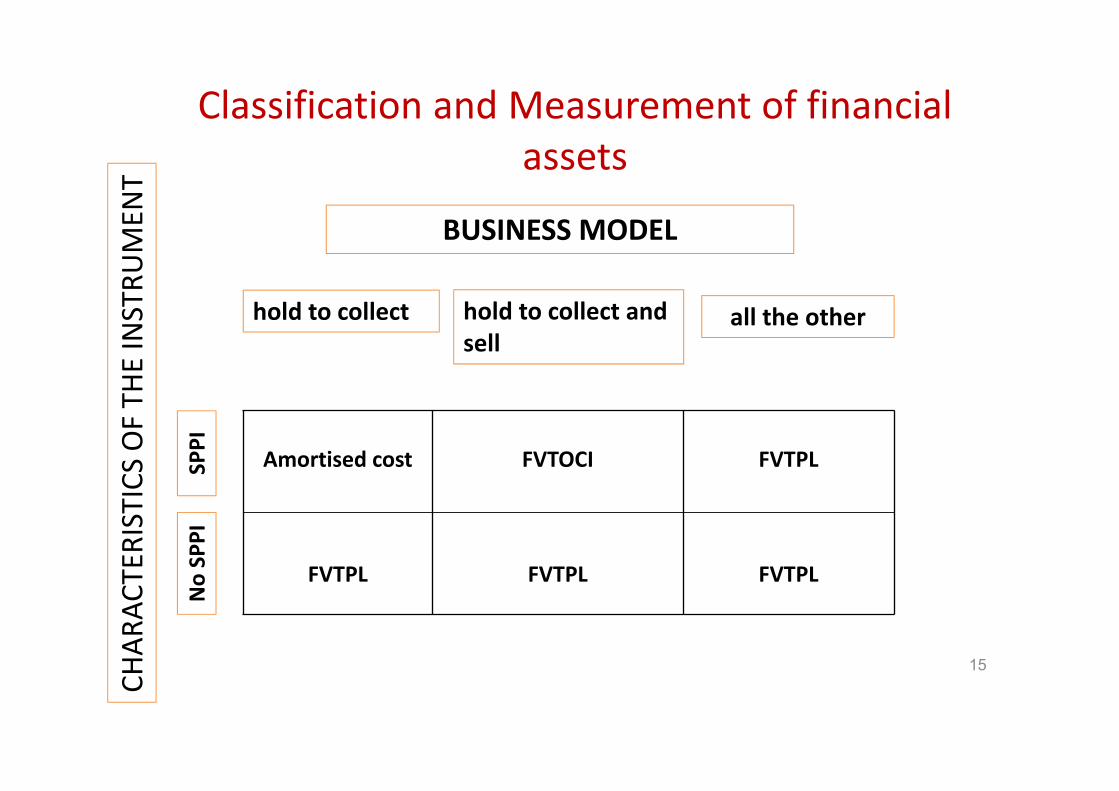

Classification and Measurement of financial assets

5

Cash flows are solely payments of principal and interest (SPPI)

Business model = hold to collect

Business model = hold to collect and

sell

Other business models

Other types of cash flows

Amortised cost FVOCI

FVTPL FVTPL

FVTPL

FVTPL

Step 1

Step 2

Contractual cash flow characteristics (step 1)

• The first condition for a financial asset to qualify for amortised cost classification is that the financial asset must meet the SPPI (solely payments of principal and interest) contractual cash flow characteristics test.

• Contractual cash flows are considered to meet SPPI if the contractual terms of the financial asset give rise to cash flows that are solely payments of principal and interest on the principal amount outstanding on specified dates i.e. the contractual cash flows are consistent with a basic lending arrangement.

Remarks:• If the contractual cash flows are linked to features such as changes in equity

or commodity prices, they would not pass the SPPI test because they introduce exposure to risks or volatility that are unrelated to a basic lending arrangement

• Contractual cash flow characteristic that introduces leverage do not have the characteristics of interest e.g. option, forward and swap contracts

6

Example : contractual cash flow characteristics

• Instrument A is a bond with a stated maturity date.• Payments of principal and interest on the principal amount outstanding are

linked to an inflation index of the currency in which the instrument is issued. • The inflation link is not leveraged and the principal is protected analysisThe contractual cash flows meet SPPI test? Yes. The interest rate on the instrument reflects ‘real’ interest as the interest amounts are consideration for the time value of money on the principal amount outstanding. It does not reflect other factors.For example, if the interest payments were indexed to another variable such as the debtor’s performance (eg the debtor’s net income) or an equity index, the contractual cash flows are not payments of principal and interest on the principal amount outstanding.

7

Page 8

‘Characteristics of the financial asset’ testExamples

Instruments that will qualify Instruments that will NOT qualify

A bond with a stated maturity date. Principal and interest are linked to an inflation index that is not leveraged.

A convertible bond that is convertible into equity instruments of the issuer.

A variable interest rate loan with a stated maturity date that permits the borrower to change the period of the market interest rate at each interest reset date on an ongoing basis.

A loan that pays an inverse floating rate, i.e. the interest rate has an inverse relationship to the market interest rates.

A bond with a stated maturity date and pays a variable market interest.

A constant maturity bond with an interest payments indexed to an equity instrumentA full recourse loan secured by

collateral.

Questions for youWhich kinds of investment meet the ‘SPPI’ contractual cash flows characteristic test?

♦ a bond repayable in five year with a fixed interest rate

♦ a loan repayable on demand with a fixed interest rate

♦ a perpetual bond (which provide the holder with the contractual right to receive payments on account of interest at fixed dates extending into the indefinite future)

♦ a bond with repayable at maturity date and with interest linked to an inflation index that is not leveraged

♦ a bond with contractual interest payments linked to a share price (e.g. the price of FCA, GM etc.)

♦ a convertible note that converts into equity instruments

♦ a derivative

Page 10

‘Business model’ testThe second condition for the qualification of a financial asset is the business model.An entity's business model refers to how an entity manages its financialassets in order to generate cash flows.The objective of the entity’s business model is to hold instruments to collect contractual cash flows rather than to sell instruments prior to contractual maturity to realise fair value changes:

– Not an instrument‐by‐instrument approach– Classification to be determined at the portfolio level – It is a matter of fact and not management intent

• an entity’s business model is determined at a level that reflects how groups of financial assets are managed together to achieve a particular business objective.

Kinds of business model (step 2)

Holding assets in order to collect contractual

cash flows

Realise cash flows by collecting contractual

payments over the life of the instrument

Typically involve lower frequency and

value of sales

Measurement: amortised cost

Both collecting contractual cash flows and selling financial

assets

Both collecting contractual cash flows and selling –sale integral to achieving

the objective of the business model

Typically involve greater frequency and value of sales

Measurement: FVOCI

Other business models

Neither held to collect nor held to collect and for sale

Collection of contractual cash

flows is incidental to the objective of the

model

Measurement: FVTPL

11

Business model’ testhold to collect

Example

• A financial institution holds financial assets to meet liquidity needs in a ‘stress case’ scenario.

• Credit quality of the financial assets is monitored• Objective in managing the financial assets: collect the contractual cash flows. • Financial assets are monitored on the basis of their fair value from a liquidity

perspective – Objective: cash amount that would be realised in a stress case scenario

would be sufficient to meet the entity’s liquidity needs. • Periodically, the entity makes sales that are insignificant in value to

demonstrate liquidity.

12

Business model test: hold to collect and sell

Example• Entity A holds investments to collect their contractual cash flows. • Entity A performs credit risk management activities – to minimise credit

losses. • In the past, sales have typically occurred when the financial assets’ credit risk

has increased, ie credit criteria specified in the entity’s documented investment policy no longer met.

• Infrequent sales have occurred as a result of unanticipated funding needs.• Reports to key management personnel focus on the credit quality of the

financial assets and the contractual return. • Entity A also monitors fair values of the financial assets, among other

information.

*

13

Questions for youWhich elements are compliant with a ‘hold to collect’ business model?

♦ Purchased loans hold to collect their contractual cash flow

♦ Infrequent sales of purchased loans

♦ Frequent sales of purchased loans

Which elements are compliant with a ‘hold to collect and sales’ business model?

♦ Purchased bonds hold to collect their contractual cash flow

♦ Sale bonds in the case that the contractual interest is belowmarket interest (past frequent sales)

♦ Trading activity

15

Classification and Measurement of financial assets

Amortised cost

FVTPL

FVTOCI

FVTPL

FVTPL

FVTPL

CHAR

ACTERISTICS OF TH

E INSTRU

MEN

T

BUSINESS MODEL

hold to collect hold to collect and sell

all the other

SPPI

No SPPI

Fair Value Through Other ComprehensiveIncome (FVOCI)

16

Investments in debt

instruments

Meet SPPI

FVOCIVariazioni di FV a OCI Recycling al momento della derecognition

Hold to collectand Sell

Equityinvestments

FVPLFVOCI Option

(Irrevocable election)

FV changes are recognised in OCI

No recycling

ElectionIrrevocable election at initial recognition.Election on an instrument‐by‐instrument

basis

Page 17

Fair Value Option (FVO) for financial assets*

Fair value option available, if…

Accounting mismatch

Managed on fair value basis

Embedded derivative(s)

Not managed to collect contractual cash flows FV

Hybrid contracts with financial host classified in entirety

* FVO unchanged for financial liabilities

Which statements are correct?Financial assets that meet both hold to collect test and SPPI test are

measured at amortised cost

All equity investments to be measured at fair value

For equity investments that are not held for trading, entities can make an irrevocable election at initial recognition to classify the

instruments as at FVOCI

IFRS 9 required that the derivative embedded within a hybrid contract is to be bifurcated from the host contract and accounted

for separately

When an equity instrument measured at is derecognised as a result of a disposal, the cumulative change in fair value is required to

remain in OCI

IFRS 9 vs IAS 39: ImpairmentIFRS 9 represents a step change when compared to IAS 39 (the ‘incurred loss’ model).

IAS 39 uses an incurred loss approach for financial assets, where loss is only recognised when a trigger event occurs. This results in ‘too little, too late’ recognition of loan losses.IFRS uses an expected loss approach in a way to recognise timely credit losses

IFRS 9 vs IAS 39: Impairment

Modello IAS 39

Incurred loss model

Performing loansNO impairment loss

Non‐performing loansLifetime impairment loss

Modello IFRS 9

Expected loss model

Performing loansExpected loss prossimi

12 mesi

Non‐performing loansLifetime impairment loss

UnderPerforming loansLifetime expected loss

VERSUS

IFRS 9 – Expected Credit Loss Model

Recognition credit expectedlosses (loss allowance)

At the reporting date, credit risk of the portfolio has increased significantly since initial recognition ?

12‐month expected credit losses (ECL)

Lifetimeexpected credit losses (ECL)

Example 1: assessing significant increases in credit risk since initial recognition

Significant increase in credit risk

22

• Bank X provides a loan to Company Y.• At the time of origination of the loan:

– It was expected that Company Y would be able to meet the covenants for the life of the instrument.

– Generation of revenue and cash flow was expected to be stable in Company Y’s industry over the term of the loan.

• At initial recognition, Bank X considers that the loan is not an originated credit‐impaired loan.

• Subsequent to initial recognition: – Company Y has underperformed on its business plan for revenue

generation and net cash flow generation due to macroeconomic changes.– Company Y has increased its leverage ratio – Company Y is now close to breaching its covenants– Trading prices for Company Y’s bonds have decreased, market spreads

have increased, not explained by changes in the market environment – Bank X expects a further deterioration in the macroeconomic environment

Example 2: assessing significant increases in credit risk since initial recognition

No significant increase in credit risk

• Bank X provides a loan to Company Y.• At the time of origination of the loan:

– It was expected that Company Y would be able to meet the covenants for the life of the instrument.

– Generation of revenue and cash flow was expected to be stable in Company Y’s industry over the term of the loan.

• At initial recognition, Bank X considers that the loan is not an originated credit‐impaired loan.

• Subsequent to initial recognition– Sales of Company are stable– There are not macroeconomic changes.– Company Y has increased its leverage ratio in non meaningful way– Company Y is not close to breaching its covenants

23© IFRS Foundation

Current 1–30 dayspast due

31–60 days past due

61–90 days past due

More than 90 days past due

Default rate

0.3% 1.6% 3.6% 6.6% 10.6%

24

*

A provision matrix is used to determine the expected credit losses for the portfolio, based on its historical observed default rates over the expected life of the trade receivables and is adjusted for forward‐looking estimates

Gross carrying amount

Default rate

Lifetime ECL allowance

CU CUA B AxB

Current 15.000.000 0,3% 45.0001–30 days past due 7.500.000 1,6% 120.00031–60 days past due 4.000.000 3,6% 144.00061–90 days past due 2.500.000 6,6% 165.000More than 90 days past due 1.000.000 10,6% 106.000

30.000.000 580.000

Example 3: Provision matrix

A question for youWhich elements are taken in consideration for impairment test?

♦ Past events

♦ Current conditions

♦ Future economic conditions (forward‐looking information)

♦ Determining whether there is a significant increase in credit risk since initial recognition

♦ Not reasonable and supportable information

![1-2018 programme.ppt [modalità compatibilità]host.uniroma3.it/facolta/economia/db/materiali/insegnamenti/576...Directive 2013/34/EU Legislative Decree 139/2015 Agenda Pagina 2. ...](https://static.fdocuments.in/doc/165x107/5ada6cfc7f8b9a53618c910e/1-2018-modalit-compatibilithostuniroma3itfacoltaeconomiadbmaterialiinsegnamenti576directive.jpg)