Insurance Accounting -...

22

Insurance Accounting Giovanni Rago 16 th of March 2018 Risk and Accounting

Transcript of Insurance Accounting -...

Insurance Accounting

Giovanni Rago 16th of March 2018

Risk and Accounting

Introduction on Insurance & Accounting

Accounting framework for Italian insurers

Local gaap versus IAS/IFRS

Individual financial statements

Consolidated financial statements

Other source of information

Annex

2

Agenda

3

• Insurance allows individuals & corporates to transfer the risks and their potentially costly financial outcome:

“Insurance is a contract whereby the insurer, against payment of a premium, undertakes to repay the insured, within the agreed limits, the damage caused to him from an event, or to pay a principal or an annuity upon the occurrence of an event relating to human life” (art. 1882 Civil Code)

Introduction on Insurance (1/3)

• The insurance sector plays an important role in the EU economy (i.e. growth, stability) by taking on risks and mobilising savings.

• Inverted production cycle: policyholders pay premiums upfront, and payments by insurers only if/when an insured event has occurred → stable cash flows to insurers (no liquidity risk) → loss sharing (mutualism): many people pay to cover the losses of few → law of large numbers: when the pool of risks increase, it is more likely that actual loss is equal the expected loss (i.e. correct pricing)

• 3 hypothesis for pricing: demographic, financial and expenses

components

4

Introduction on Insurance (2/3)

• 2 main items in the insurer’s balance sheet (annex 1): - Investments: funded by premiums and held-to-match liabilities (ALM) - Technical provisions: estimates of future obligations (expected losses) • Insurers are highly regulated (Solvency II in EU – annex 2): they

are required to hold - among other things - eligible own funds (equity) to cover capital requirements (on top of TP) to cover unexpected losses

• 2 main products: 1) non-life (P&C): the insurer indemnifies the policyholders from loss or

damage caused by specific risks → purpose: compensation/indemnity → examples: car insurance, fire, aviation/marine, travel, health, etc

2) life: the insurer pays the beneficiary a sum of money (the benefit) in exchange for a premium, upon the death of an insured person → purpose: investment/saving → examples: term insurance, with-profits contracts, unit/index linked → 3 categories: term life insurance, whole life and endowment → subject involved: insurer, beneficiary, insured person and policyholder.

ALM = Asset-Liability Management

5

Premiums (2016)*

Global = $ 4,732 bn EU = €1,189 bn

(=7% of GDP) IT = € 138 bn

(=8% of GDP)

Breakdown of premiums in EU (2016)*

Life (€696bn)

Non-Life (€363bn)

Breakdown of Investments in EU (2016)*

Total Investments = €10,112 bn (=62% of EU GDP)

Market structure in EU (2016)*

- 3 500 insurance companies (IT: 108)

- 944 000 direct employees

- Distribution channel: • Bancassurance in life • Agents and brokers in non-life

* European Insurance in Figures: 2016 data, February 2018

Introduction on Insurance (3/3)

6

• Objective: to provide information about the financial position and financial performance of an entity that is useful to a wide range of users in making economic decisions (IAS 1 & CF)

Introduction on Accounting (1/2)

• Pros & Cons of FS: (+): info on amount/timing/uncertainty of future cash flows (-): no all info, no value of an entity, no ‘exact’ figures but estimates

• Structure: FS comprises a statement of (IAS1+art. 2423 cc): - Financial position - Profit or loss (incl. OCI) - Changes in equity - Cash flows - Notes

- assets, liabilities & equity - incomes & expenses - contribution by/to owners - cash flows

Info about entity’s:

FS = Financial Statements │ CP = Conceptual Framework │ cc = Civil Code │ OCI = Other Comprehensive Income

• General features (IAS1): - Fair presentation - Going concern - Accrual basis

- Materiality & aggregation - offsetting - Frequency of reporting

- comparability - consistency

7

• The financial analysis of FS depends on the objectives of users

Introduction on Accounting (2/2)

• Shareholders • Investors

• Financial analyst

• Supervisory Authorities

• Policyholders

• Management

USE

RS

•Risk analysis •Return on investments •Value creation

• Solvency •Protection of policyholders

•Prudent management

•Stewardship or accountability of management

•Internal planning OBJ

ECTI

VES

8

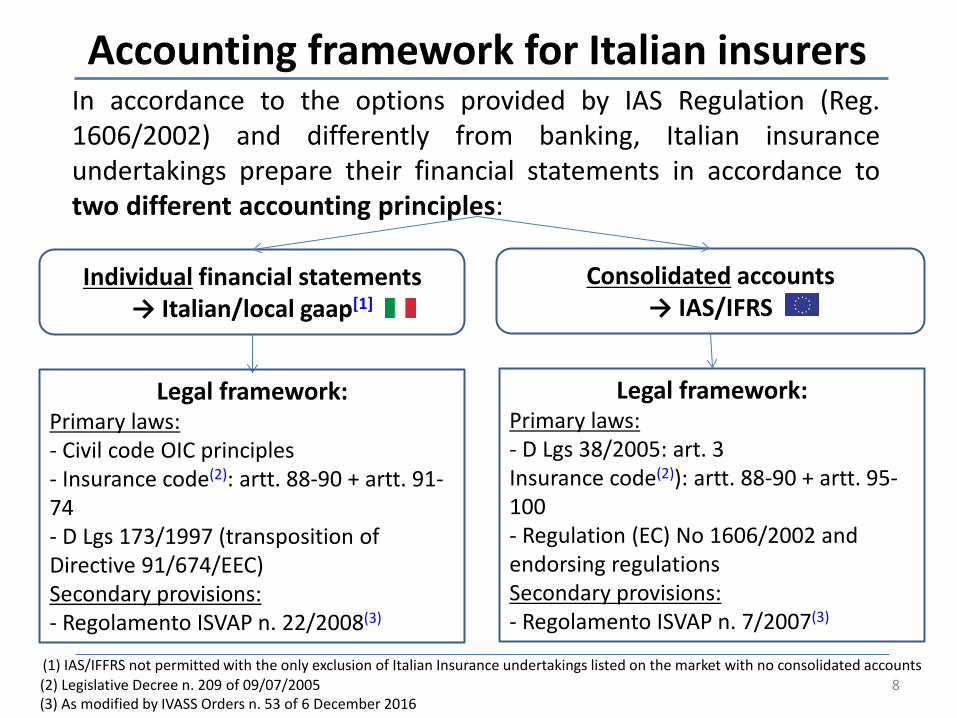

In accordance to the options provided by IAS Regulation (Reg. 1606/2002) and differently from banking, Italian insurance undertakings prepare their financial statements in accordance to two different accounting principles:

Individual financial statements → Italian/local gaap[1]

Consolidated accounts → IAS/IFRS

Legal framework: Primary laws: - Civil code OIC principles - Insurance code(2): artt. 88-90 + artt. 91-74 - D Lgs 173/1997 (transposition of Directive 91/674/EEC) Secondary provisions: - Regolamento ISVAP n. 22/2008(3)

(2) Legislative Decree n. 209 of 09/07/2005 (3) As modified by IVASS Orders n. 53 of 6 December 2016

Legal framework: Primary laws: - D Lgs 38/2005: art. 3 Insurance code(2)): artt. 88-90 + artt. 95-100 - Regulation (EC) No 1606/2002 and endorsing regulations Secondary provisions: - Regolamento ISVAP n. 7/2007(3)

(1) IAS/IFFRS not permitted with the only exclusion of Italian Insurance undertakings listed on the market with no consolidated accounts

Accounting framework for Italian insurers

9

Local gaap versus IAS/IFRS (1/2) • The two frameworks (i.e. local gaap and IAS/IFRS) are based on

different underlying principles:

Local gaap IAS/IFRS

Information to lenders Information to (actual and potential) investors

Historical cost Fair value

Prudence Mark to market

Form over substance Substance over form

Realized gains and losses Unrealized gains and losses

10

Local gaap versus IAS/IFRS (2/2) • … in relation to insurance accounting the main differences are: Local gaap

IAS/IFRS

Structure of layouts Separately for Life (L) & Non-Life (NL) No separation L/NL + segment reporting

Goodwill Amortised (over 5 years) At cost less impairment losses (no amortisation)

Premiums from Life investments contracts*

P&L: Written premiums BS: insurance liabilities (item D) at FV No premiums + Financial liabilities (IAS 39)

Properties Cost + depretiation Own use (IAS 16) or Investment (IAS40) Cost or fair value

Investments Current portfolio: lower cost & market value Fixed ptf: cost + permanent write-down

HTM : amortised cost (+ impairments to P&L) LR: amortised cost AFS: FV to OCI (+ impairments to P&L) HFT: FV to P&L

Derivatives Off-balance sheet P&L: ‘matching principle’ for hedging

On-balance sheet Hedge accounting

Technical provisions (TP) Prudent valuation IFRS 4 allows the use of local gaap with minor

amendments (LAT)

Life Technical provisions:

shadow accounting N.A.

Applied to par contracts to reduce accounting mismatch between assets, valued at FV, and TP, valued at cost with local gaap.

Additional provisions Equalisation and catastrophe provisions Equalisation and catastrophe provisions are derecognised

FV = fair value │ par contracts = participating contracts (contracts with discretionary participation features ) * With no significant insurance risk

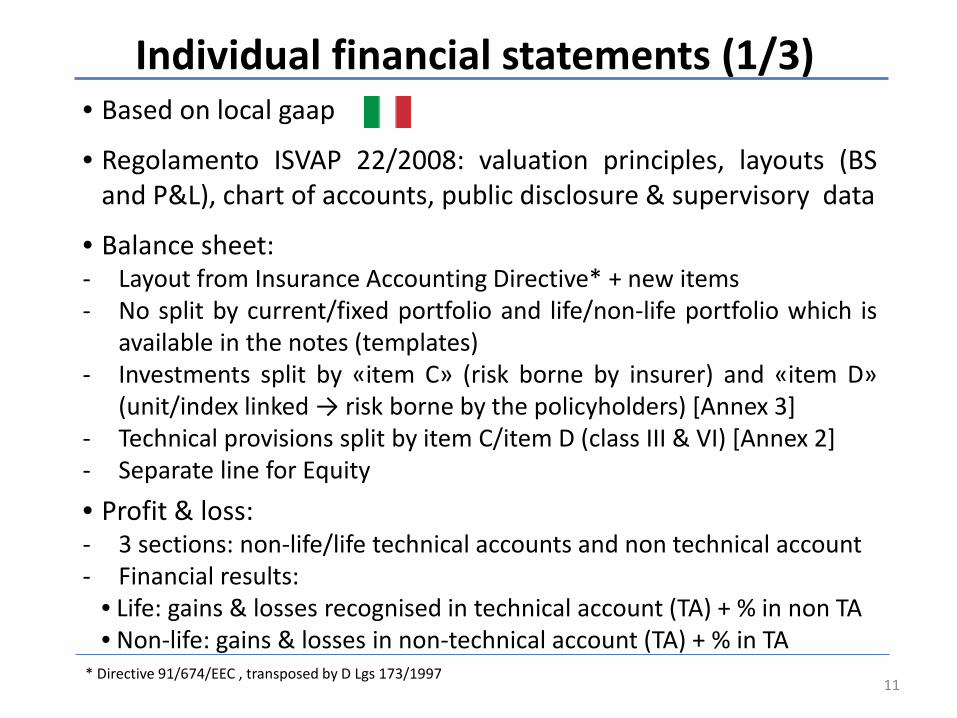

• Based on local gaap

• Regolamento ISVAP 22/2008: valuation principles, layouts (BS and P&L), chart of accounts, public disclosure & supervisory data

• Balance sheet: - Layout from Insurance Accounting Directive* + new items - No split by current/fixed portfolio and life/non-life portfolio which is

available in the notes (templates) - Investments split by «item C» (risk borne by insurer) and «item D»

(unit/index linked → risk borne by the policyholders) [Annex 3] - Technical provisions split by item C/item D (class III & VI) [Annex 2] - Separate line for Equity • Profit & loss: - 3 sections: non-life/life technical accounts and non technical account - Financial results:

• Life: gains & losses recognised in technical account (TA) + % in non TA • Non-life: gains & losses in non-technical account (TA) + % in TA

11

Individual financial statements (1/3)

* Directive 91/674/EEC , transposed by D Lgs 173/1997

Framework for the valuation of technical provisions (TP):

• legal framework: D Lgs 173/1997+ Regolamento ISVAP 22/2008*

• Principles for non-life reserving: - TP sufficient to face the obligations towards policyholders (reserve risk) - TP gross of reinsurance (recoverables from reinsurance) - Prudent valuation method based on analytical evaluation of each claim + verification applying statistic/actuarial methodology

12

Individual financial statements (2/3)

* Annex 14, 15, and 16

- 2 main provisions: 1) provisions for unearned premiums. It includes:

- provisions for unearned premiums: part of gross written premiums which is to be allocated to the following financial year(s) - provisions for unexpired risks: to cover the risk of mis-pricing (expected losses >

provisions for UP + future premiums) 2) provisions for claims outstanding: provisions for insurance claims which have been reported and not yet settled (RBNS) or which have been incurred but not yet reported (IBNR).

Framework for the valuation of technical provisions (TP) – con’t

13

Individual financial statements (3/3)

• Principles for life reserving: - Mathematical provisions is the most important provisions - TP gross of reinsurance (recoverables from reinsurance)

- Valuation per each single contract but possible to aggregate similar risks - Calculation methods: 1) Prospective actuarial method (default) to estimate all future and expected cash out flows by the insurer (payments to policyholders), net of cash in-flows (future premiums by policyholders) 2) Retrospective actuarial method (at certain condition)

- Type of demographic/financial assumptions used to estimate TP: Technical basis of 1st order: same assumptions used for pricing + additional reserve for

demographic and financial risks (∆ pricing vs experience) Technical basis of 2nd order: most up-dated assumptions

- TP for unit/index linked valued in accordance with close matching principle

• Based on IAS/IFRS

• legal framework: Regolamento ISVAP 7/2007: NO valuation principles but layouts (BS and P&L) and public disclosure

14

Consolidated financial statements (1/3)

• Balance sheet: Assets - 7 macro-items - Split of investments &

reinsurance (TP & receivables) Liabilities - 6 macro-items - Insurance liabilities (IFRS 4) and

financial liabilities (IAS 39) - Insurance and reinsurance playbles

- equity

Balance sheet Assets Liabilities

15

Consolidated financial statements (2/3) Other Comprehensive Income Income statement

16

Consolidated financial statements (3/3) • Investments (BS/assets) are mostly valued at fair value (IAS 39):

• Technical provisions (BS/liabilities) are mostly valued at cost (IFRS 4: local gaap), excluding unit/index linked: 816,721 €/mln (2015)

→ Accounting mismatch between assets and liabilities • Shadow accounting: mitigates the accounting mismatch for

insurance/investment contracts with DPF splitting the unrealised gain (losses) from investments by the policyholders’ share – increase(decrease, subject to the guarantee rate) of TP – and the insurer’s share (see example in annex 4).

The financial statements include: - the Notes to accounts which includes information on: • Part A: summary of significant accounting policies • Part B: information on the Balance Sheet and Profit and Loss • Part C: other information • Detailed quantitative templates with breakdown of BS/P&L items - the management report with information about the performance of the company , the principal risks/uncertainties faced by the undertaking and the compliance with of capital requirements - Risk report with information on: • Risk management system • The solvency position • The risk profile: underwriting risk (life and non-life) financial risk (market and credit risk) operational risk other risks: liquidity, strategic, reputational, contagion, emerging risk.

17

Other source of information (1/2)

Since January 2016, EU insurers have to comply with Solvency II regulation which requires – among other things – to disclosure the Solvency and Financial Condition (SFCR) report with info on: - Business and performance: qualifying shareholders, material line of business, significant operations, info on source of performance (underwriting, investments, other activities) - System of governance: Structure of the Board, remuneration policy, fit & proper policy, risk management system, internal control system, etc. - Risk profile: underwriting risk, market risk, credit risk, liquidity risk, operational risk, other material risks; use and effect of risk mitigation techniques; stress testing; etc. - Valuation for solvency purposes (TP and investments) - Capital management Capital management policy, eligible own funds to cover capital requirements with reconciliation with account equity, info on capital requirements (standard formula vs internal model) and use of simplifications, etc.

18

Other source of information (2/2)

19

Annex 1

Source: Insurance and Financial Stability, IAIS, November 2011

Synthetic balance sheet for European life/non-life insurance groups

20

Annex 2

21

Annex 3

(Consolidated data as of 2013 year-end – source IVASS)

22

Annex 4 Let consider an Available-for-Sale assets (whose change of fair value is recognised in Equity/OCI), included in the segregated fund related to a participating contract, with a fair value of 100 CU at t and a fair value of 80 CU a t+1. At t+1, the unrealised loss of 20 CU (80-100) is split - assuming a share of 85% of returns distributed to policyholders – between the insurer’s share (4 CU=20%*20 CU) e the policyholders’ share (16 CU=80%*20 CU):