Revise Lecture 25. Features of a Cheque Cheques Features of a Cheque Some important features of a...

48

Revise Lecture 25

-

Upload

blake-clark -

Category

Documents

-

view

232 -

download

4

Transcript of Revise Lecture 25. Features of a Cheque Cheques Features of a Cheque Some important features of a...

Revise Lecture 25

•Features of a Cheque

Cheques

Features of a Cheque• Some important features of a cheque are

given below;1. A cheque must be in writing and duly signed

by the drawer.2. It contains an unconditional order.3. It is issued on a specified banker only.

• Types of Cheques

Cheques

• Broadly speaking, cheques are of four types;1. Open cheque2. Crossed cheque3. Bearer cheque4. Order cheque

• Anted – dated Cheque

Cheques

• Stale Cheque

Cheques

Stale Cheque• A cheque which is issued today must be

presented at bank for payment within a stipulated period.

• After expiry of that period, no payment will be made and it is then called a stale cheque.

• Find out from your nearest bank the validity period of a cheque.

Cheques

•Mutilated Cheque

Cheques

• Post-dated Cheque

• Parties to a Negotiable Instruments

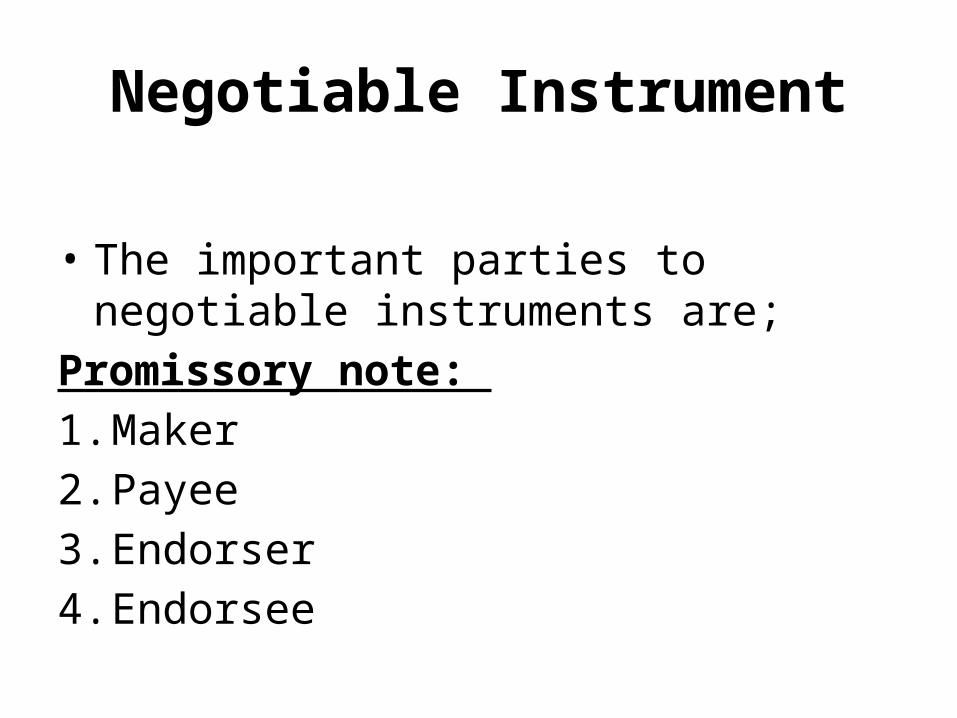

Negotiable Instrument

• The important parties to negotiable instruments are;

Promissory note: 1. Maker2. Payee3. Endorser4. Endorsee

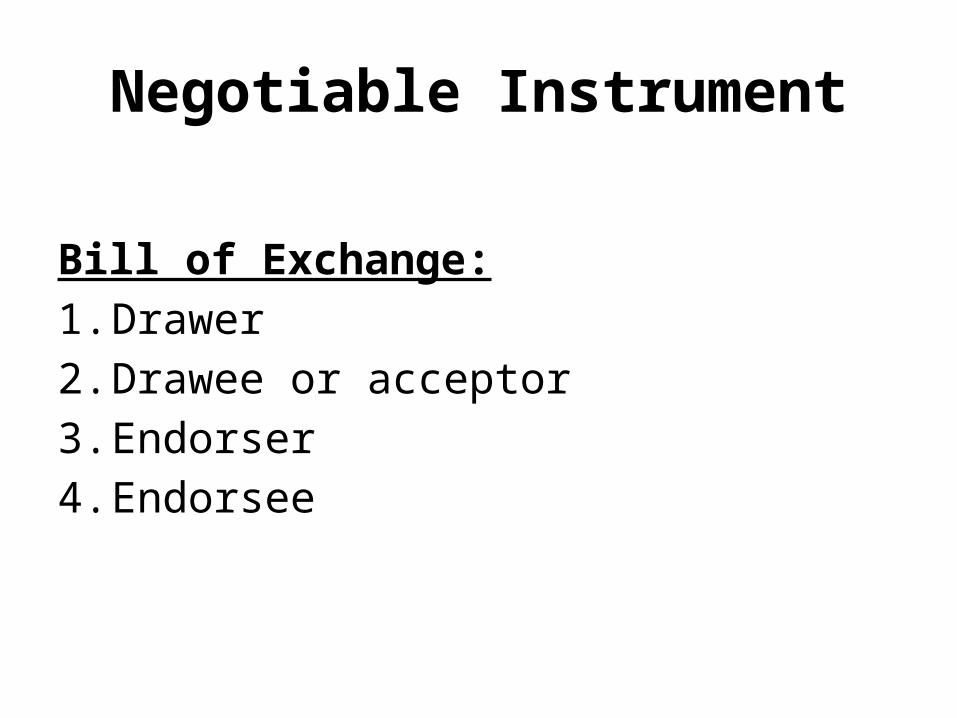

Negotiable Instrument

Bill of Exchange:1. Drawer2. Drawee or acceptor3. Endorser4. Endorsee

Negotiable Instrument

• Holder in Due Course

Negotiable Instrument

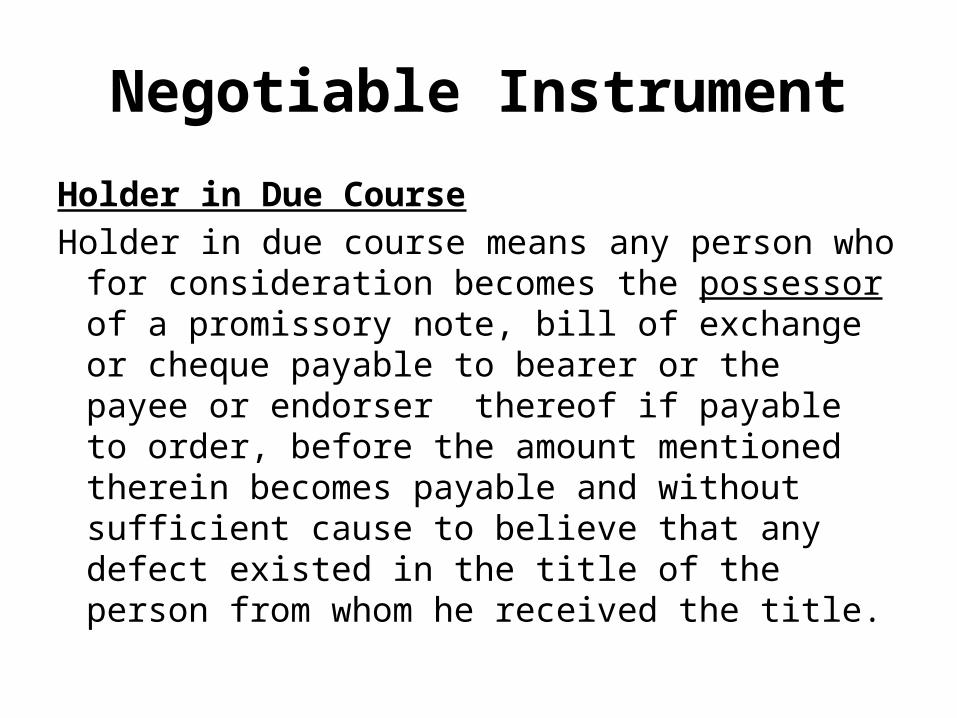

Holder in Due CourseHolder in due course means any person who for

consideration becomes the possessor of a promissory note, bill of exchange or cheque payable to bearer or the payee or endorser thereof if payable to order, before the amount mentioned therein becomes payable and without sufficient cause to believe that any defect existed in the title of the person from whom he received the title.

Negotiable Instrument

Holder in Due CourseThe definition specifies that:1. The holder has to possess the instrument in

due course and before the date of maturity.2. The consideration must be legal and adequate.3. There should be sufficient cause to believe

that he possessed the instrument in good faith and with reasonable care.

Negotiable Instrument

Holder in Due Course4. The holder should not become the holder in

due course even if he received the instrument without any suspicion or knowledge about such defects.

5. Notice of any defect in the title subsequent to the date of acquisition should not affect the rights of the holder in due course.

Lecture 26

•Banker and Customer

Banker and Customer

The Banker• The role of a banker is one filled with multiple

duties and responsibilities.• There are different types of bankers and each

one is unique in his own way. • Some of these individuals work for large

corporate conglomerates while others work for small town financial institutions.

Banker and Customer

The Banker• Each banker has his own set agenda in his role

as a banker. • A banker is an individual (or an institution) who

advises his clients with regard to financial matter.

• The duties concerning saving, loans, taxes, investment and securities are all within the job realm of a banker.

Banker and Customer

• The BankerHe will provide financial assistance to the client

in accordance with their needs.

Banker and Customer

• The Customer

Banker and Customer

The Customer• In banking, a customer is someone who makes

use of or receive the services of the bank.• The word customer historically derives

‘custom’ meaning habbit, so a customer was someone who frequented a particular shop, who made it a habbit to purchase goods there

Banker and Customer

Duties of a CustomerAll banks carry out the customer’s instructions in

a business-like manner.In return, the customer has special duties of

cooperation and other duties of care.

A customer is bound to the following;

Banker and Customer

Duties of a Customer

1. Communication of important information and changes.

2. Unambiguous information in orders and instructions

3. Care in transmission of particular orders

Banker and Customer

• Duties of a Customer4. Use of forms5. Express notification of any special instruction6. Notification of time limits and dates7. Complaints to be made immediately8. Checking of confirmation of the bank9. Liability arising from neglect of duty

Banker and Customer

• Banker’s obligation to protect customer secrecy

Banker and Customer

• The obligation of a banker to observe secrecy relating to affairs of his customers is an implied term of the contract between a banker and his customer.

• A banker would not divulge to third persons, without the consent of the customer, express or implied, either the state of the customer’s account or any of his transactions with the bank.

Banker and Customer

• Banker’s right to charge interest and commission

Banker and Customer

Banker’s right to charge interest and commission• The bank generates its profits from the

differential between the level of interest it pays for deposits and other sources of funds, and the level of interest it charges in its lending activities.

• All banks at any time and form time to time are entitled to charge the rate of interest on loan either by express agreement or right of custom or usage of trade.

Banker and Customer

Banker’s right to charge interest and commission• They also entitled to charge compound

interest and commission for services rendered to the customer.

• In the absence of an express agreement or without due notice, a bank is not allowed to debit charges at any date other than the customary dates.

•Banker’s Right to Lien

Banker’s Right to Lien• A lien is the right of a creditor in possession of

goods, securities or any other assets belonging to the debtor to retain them until the debt is repaid, provided that there is no contract express or implied, to the contrary.

Banker’s Right to Lien• Lien is, in its primary sense, a right in one man

to retain that which is in his possession belonging to another until certain demands of the person in possession are satisfied.

• In its primary sense, it is given by law and not by contract.

Banker’s Right to Lien• A banker’s lien on negotiable securities has

been judicially defined as ‘ an implied pledge’.• A banker has, in the absence of agreement to

the contrary, a lien on all bills received from a customer in the ordinary course of banking business in respect of any balance that may be due from such customer.

• Banker’s right of set-off

Banker’s right of set-off • The of right of set-off is also known as the right of

combination of accounts.• A bank has a right to set-off a debt owing to a

customer against a debt due from him.• ‘A legal set-off is where there are mutual debts

between the plaintiff and the defendant, or if either party sue or be sued as executor or administrator, one debt may be set against the other’.

Banker’s right of set-off • From a commercial standpoint, a right of set-off

is a form of security (right) for a lender.• It is an attractive security because its realization

does not involve the sale of an asset to a third party.

• A set-off must be in the form of a cross claim for a liquidated amount, and it can be pleaded only in respect of a liquidated claim.

•Deposit Account

Deposit Account• The main banking activities consist of acceptance of

deposit from the public for the purpose of lending to businessmen and others who may seek loans.

• Actually, the money deposited in any bank is mostly the saving of the people.

• Money may be needed in future for various purposes such as medical treatment, marriages and for other events.

Deposit Account• So people keep their savings with someone

where it will both be safe and earn a return.• A bank is a such place where money once

deposited remains safe and also earns profit.

• Types of deposit account

Types of deposit account• Bank deposits serve different purposes for

different people.• Some people cannot save regularly, they

deposit money in the bank only when they have extra income.

• Some, mostly businessmen, deposit all their income from sales in a bank account and pay all business expenses out of the deposits.

Types of deposit account

• Keeping in view these differences, banks offer the people the facility of opening different types of deposit accounts to suit their purpose and convenience.

Types of deposit account• Accordingly, bank deposit accounts may be

classified as;1. Savings bank account2. Current deposit account3. Fixed deposit account4. Recurring deposit account5. Salary account

• Withdrawal from deposit account

Withdrawal from deposit account

• Customer deposit his savings for use in future.

• The need for money may arise any time. So customer should know how to get back your money from the bank.

Withdrawal from deposit account

Money can be withdrawn by using;1. Withdrawal form2. Cheque3. ATM card