RETAIL REAL ESTATE IN VIETNAM - Vietnam Business · Legal updates on Retail Real Estate CONTENT ....

94

OUTLOOK FOR 2015 RETAIL REAL ESTATE MARKET UPDATE

Transcript of RETAIL REAL ESTATE IN VIETNAM - Vietnam Business · Legal updates on Retail Real Estate CONTENT ....

OUTLOOK FOR 2015

RETAIL REAL ESTATE MARKET UPDATE

2

VIETNAM RETAIL MARKET

Vietnam Market Overview

Market Trends

Other Indochina Markets Updates

Retailer Analytics

Legal updates on Retail Real Estate

CONTENT

VIETNAM MARKET OVERVIEW

4

VIETNAM RETAIL MARKET

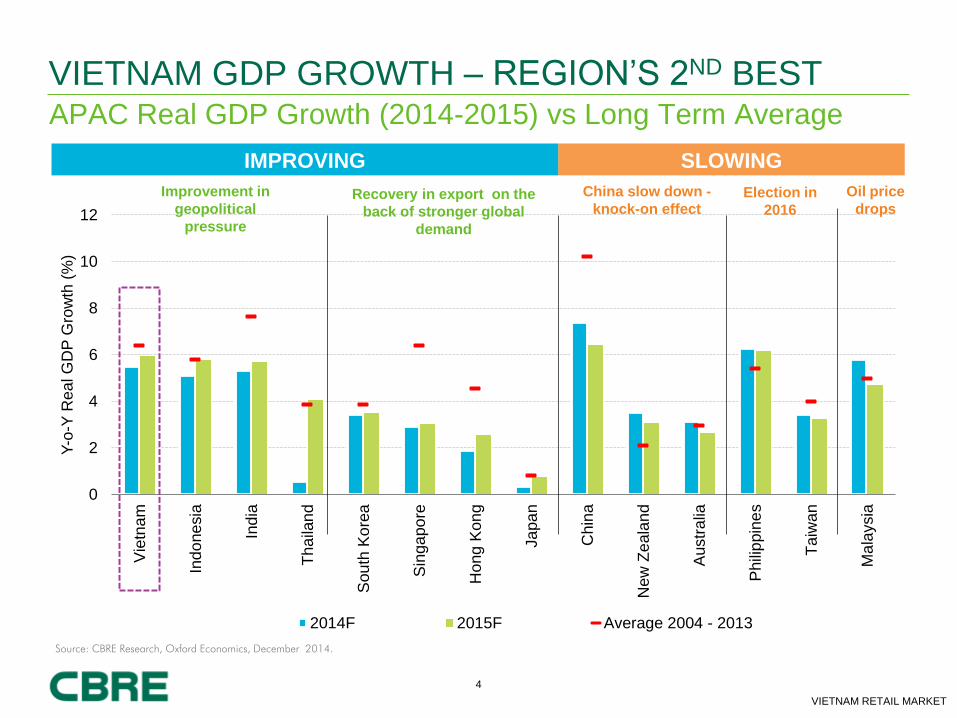

APAC Real GDP Growth (2014-2015) vs Long Term Average

VIETNAM GDP GROWTH ndash REGIONrsquoS 2ND BEST

0

2

4

6

8

10

12

Vie

tna

m

Ind

one

sia

Ind

ia

Thaila

nd

Sou

th K

ore

a

Sin

ga

po

re

Hong

Kon

g

Ja

pa

n

Chin

a

New

Ze

ala

nd

Austr

alia

Phili

ppin

es

Taiw

an

Ma

laysia

Y-o

-Y R

ea

l G

DP

Gro

wth

(

)

2014F 2015F Average 2004 - 2013

Improvement in

geopolitical

pressure

China slow down -

knock-on effect

Source CBRE Research Oxford Economics December 2014

The chart does not tell this Group markets in

Export driven

Improvement in geopolitical tension

China slowdown ndash knock-on effect on commodity-export markets like Australia and New Zealand

Japan growth is minimal

Recovery in export on the

back of stronger global

demand

Oil price

drops

SLOWING IMPROVING

Election in

2016

5

VIETNAM RETAIL MARKET

OIL PRICES GETTING INCREDIBLY CHEAP

Oil had been getting stronger since 2009 2010 but then declined significantly since mid-2014

Crude oil price

Good consequences

Stronger consumptions due to lower industrial

input and logistics costs (-3 approx)

Lower construction cost

Lower building operating cost (service charge)

Bad consequences

Weakening VNDUSD

Falling oil world prices would slash Vietnamrsquos

state budget by around US$3 billion

But just a minimal impacts against VND

(Sufficient USD reserves surplus trade balance

robust FDI low inflation)

6

VIETNAM RETAIL MARKET

0

5

10

15

20

25

2007 2008 2009 2010 2011 2012 2013 2014

Inte

rest ra

te (

)

Average CPI (y-o-y) Rediscounting rate Refinancing rate Lending rate Deposit rate

FUNDING GETTING CHEAPER

Source Vietnamese General Statistical Office

Interest Rates and Inflation

Lending rate for the first 12 months

bull Techcombank 949

bull Vietcombank 799

bull ACB 89

7

VIETNAM RETAIL MARKET

Turnover continues to increase whilst growth continues to slow

RETAILS amp SERVICES TURNOVER

0

8

16

24

32

40

0

500

1000

1500

2000

2500

3000

35002

00

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4P

Gro

wth

Ra

te (

)

Tu

rno

ve

r (T

rilli

on

do

ng

)

Retails and Services Turnover Retails and Services Turnover Growth

8

VIETNAM RETAIL MARKET

Strong supply from Hanoi market

RETAIL MARKET UPDATE

Source CBRE Vietnam Q2 2014

Retail supply by city (NLA lsquo000 sqm)

0

200

400

600

800

1000

1200

HCMC Hanoi HCMC Hanoi HCMC Hanoi HCMC Hanoi HCMC Hanoi HCMC Hanoi

2011 2012 2013 2014 2015F 2016F

Re

tail

su

pp

ly b

y c

ity (

NL

A lsquo0

00

sq

m)

9

VIETNAM RETAIL MARKET

0

200

400

600

800

1000

1200

Beiji

ng

She

nzhe

n

Ban

gkok

New

De

lhi

Kua

la L

um

pur

Gua

ngzh

ou

Hano

i

Sha

ngh

ai

Ma

nila

Mu

mb

ai

Sin

ga

po

re

Me

lbou

rne

Ho

Chi M

inh C

ity

Tokyo

Sydn

ey

Ade

laid

e

Brisb

an

e

Hong

Kon

g

Ja

kart

a

Auckla

nd

Pert

h

Taip

ei

De

ve

lop

me

nt

Pip

elin

e (

lsquo00

0 s

qm

)

2015F

APAC Development Pipeline

RETAIL MARKET UPDATE

Source CBRE Research Q4 2014

10

VIETNAM RETAIL MARKET

Softer rents but vacancy still up

Source CBRE Vietnam Q4 2014

AVERAGE ASKING RENT

(US$smmonth)

VACANCY RATE

()

2014

Q4

Q3

Q2

Q1

2013

Q4

Q3

Q2

Q1

2012

Q4

Q3

Q2

Q1

2011

Q4

Q3

Q2

Q1

NON-CBD CBD

050100150 0 50 100 150

-3

3

9

15

21

-40000

0

40000

80000

120000

160000

2010 2011 2012 2013 2014

Va

ca

ncy R

ate

(

)

Net A

bso

rptio

n (

sm

)

Net Absorption (sm) Vacancy

HANOI MARKET PERFORMANCE 2014

11

VIETNAM RETAIL MARKET

Consistent performance for the last eight quarters

HOCHIMINH CITY PERFORMANCE 2014

Source CBRE Vietnam Q4 2014

AVERAGE ASKING RENT

(US$smmonth)

VACANCY RATE

()

2014

Q4

Q3

Q2

Q1

2013

Q4

Q3

Q2

Q1

2012

Q4

Q3

Q2

Q1

2011

Q4

Q3

Q2

Q1

NON-CBD CBD

050100150 0 50 100 150

0

4

8

12

16

20

-20000

0

20000

40000

60000

2011 2012 2013 2014

Va

ca

ncy R

ate

(

)

Net A

bso

rptio

n (

sm

)

Net absorption Vacancy rate

12

VIETNAM RETAIL MARKET

HANOI

NEW SUPPLY IN 2014

LOTTE MART

(Mipec Tower)

Dong Da District

GFA 27000 sm

Opened Q12014

Shopping Centre amp Department Store

LOTTE

DEPARTMENT STORE

Ba Dinh District

GFA 21480 sm

Opened Q32014

Trang Tien Plaza reopening

Add more FampB

More affordable brands

ALMAZ by Vingroup

Convention ndash FampB ndash Retail amp Entertainment Center

Long Bien District

GFA 25 ha

Opened Q42014

13

VIETNAM RETAIL MARKET

HoChinhMinh City

NEW SUPPLY IN 2014

AEON MALL

TAN PHU CELADON

Tan Phu District

GFA 42100 sm

Anchor Aeon Mart Aeon

department store CGV Dream

Games

Opened Q12014

Shopping Centre amp Department Store

AEON MALL

BINH DUONG CANARY

Binh Duong

GFA 62100 sm

Anchor Aeon Mart Aeon

department store CGV Play

Time

Opened Q42014

LOTTE MART CONG HOA

Tan Binh District

GFA 10000 sm

Anchor Lotte mart Lotte Cinema

Wall Street English California

Fitness

Opened Q42014

14

VIETNAM RETAIL MARKET

Hanoi

UPCOMING RETAIL DEVELOPMENT

AEON MALL HANOI

bull Long Bien district

bull GFA 108000 sm

bull 4 floors

bull Under construction

bull Expected to open

Q4 2015

Expect to open in 2015

HOA BINH GREEN CITY

bull Hai Ba Trung District

bull GFA 25000 sm

bull 4 floors

bull Opened on Jan 31st

bull Offering free rentals in

perpetuity

HO GUOM PLAZA

bull Ha Dong District

bull GFA 23400 sm

bull 5 floors

bull Completed Open

for lease

bull Anchor tenants

Tran Anh CGV

bull Expected to open

(fully) Q2 2015

VINCOM NGUYEN CHI

THANH

bull Dong Da District

bull GFA 44500 sm

bull Under construction

bull Expected to open Nov

2015

15

VIETNAM RETAIL MARKET

Ho Chi Minh City

UPCOMING RETAIL DEVELOPMENT

Expect to open in 2015

VINCOM THU DUC

Thu Duc District

GFA 27860 sm

Expected to open Feb 8

2015

SC VIVOCITY

District 7

GFA 62000 sm

Expected to open April 2015

PEARL PLAZA

Binh Thanh District

GFA 20000 sm

Expected to open July 2015

THAO DIEN PEARL

District 2

GFA 20000 sm

Expected to open July 2015

16

VIETNAM RETAIL MARKET

METRO LINE NO 1 AND RETAIL PROJECTS

Taken in front of Rex Hotel on Jan 7 2015

Vinhomes Central Park

Thao Dien Pearl

The Vista An Phu

Vincom MegaMall Masteri Thao Dien

Cantavil Premier

The Estella Heights

NEW EASTERN BUS STATION

LONG BINH DEPOT

The One

Union Square Tax Plaza

Saigon Center

17

VIETNAM RETAIL MARKET

Retailing hospots across APAC ndash strong activities in Hanoi

RETAIL MARKET UPDATE

HANOI

27 ENTRIES

18

VIETNAM RETAIL MARKET

Hanoi amp HCMC Markets

NEW RETAIL ENTRIES IN 2014

Ho Chi Minh City

Hanoi

MORE TO COMEhellip

MARKET TRENDS

20

VIETNAM RETAIL MARKET

Vingrouprsquos movements in retail sector

LOCAL PLAYERS EXPAND

VINCOM MEGAMALL THAO

DIEN

GFA 100000 sm

Expected completion 2015

VINCOM

NGUYEN CHI

THANH

GFA 44500 sm

25 Shopping Centers in 2015 - HCMC HANOI BAC NINH

VIET TRI DA NANG CAN THO BIEN HOA AN GIANG

HAI PHONG hellip

To open 100

supermarkets and

1000 convenience

stores in the next

3 years

VINCOM

DA NANG

GFA 31000 sm

VINCOM

CAN THO 2

GFA 14500 sm

MampA activity by Vingroup

13 supermarkets and convenience

stores with ~ 40000 sm retail area

VINCOM MEGAMALL

TRUONG CHINH -

HCMC

GFA 100000 sqm

To invest US$166 million

hellip

21

VIETNAM RETAIL MARKET

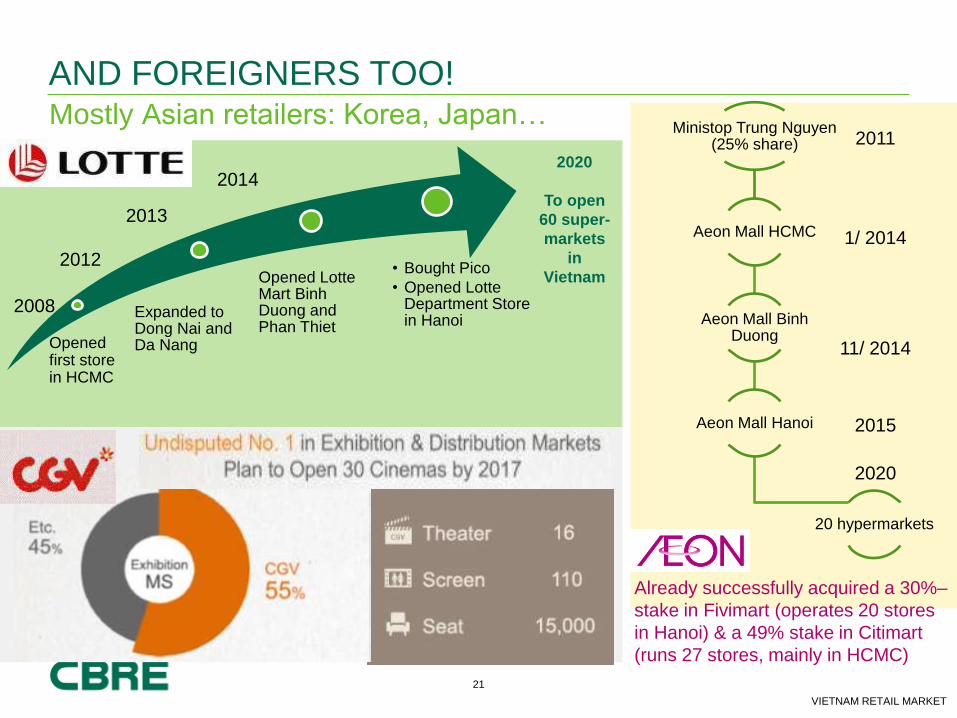

Mostly Asian retailers Korea Japanhellip

AND FOREIGNERS TOO

Expanded to Dong Nai and Da Nang

Opened Lotte Mart Binh Duong and Phan Thiet

bull Bought Pico

bull Opened Lotte Department Store in Hanoi

2008

2012

2013

2014 2020

To open

60 super-

markets

in

Vietnam

Ministop Trung Nguyen (25 share)

Aeon Mall HCMC

Aeon Mall Binh Duong

Aeon Mall Hanoi

20 hypermarkets

2011

1 2014

11 2014

2015

2020

Already successfully acquired a 30ndash

stake in Fivimart (operates 20 stores

in Hanoi) amp a 49 stake in Citimart

(runs 27 stores mainly in HCMC)

Opened first store in HCMC

22

VIETNAM RETAIL MARKET

hellipand Thailand

AND FOREIGNERS TOO

BJCrsquos Bs Mart bought 94 Family marts in Vietnam

aim to expand to 300 stores by 2018

BJC acquires Metro Vietnam for

US$879 million incl 19 distribution

centers and related real estate

Central Grouprsquos Robins Department

Store in Hanoi and HCMC

Central Group buys 49 stake in Nguyen Kim

49 51

Target gt 50 stores in 2019

23

VIETNAM RETAIL MARKET

DEPARTMENT STORE

2005

2013 - 2014

Robins Department Store

Diamond Plaza

Parkson Department

Store

2015 - 2016

Vingroup

Department

store

1999

Lotte Department Store

Takashimaya

Source Google Images

24

VIETNAM RETAIL MARKET

AFFORDABLE RETAIL

SAIGON SQUARE 3

District 3 HCMC

GFA 3100 sm

Opened 1 Jan 2015

HUNG VUONG SQUARE

District 5 HCMC

GFA 9500 sm

Opened 31 Dec 2014

More Bazaar emerged Supermarket

AEON CITIMART

Go Vap District HCMC

Opened Jan 2015

Rent-free Shopping Center

V+ Shopping Center ndash Hoa Binh

Green City

Minh Khai Street Hai Ba Trung District Hanoi

GFA 25000 sqm

Open 31st Jan 2015

Lower number of SKUrsquos

Rental free for all store selling ldquoMade-in-Vietnamrdquo

products

25

VIETNAM RETAIL MARKET

76

24 Shopping center

High Street

FampB is increasingly dominant with 47

Tenants enquiries by preferences 2014

High Street stores are still highly

preferred by retailers

Tenants enquiries by categories 2014

of enquiries

Source CBRE Vietnam Q4 2014

FampB

Fashion

Accessories

Education

Cosmetics

Furniture

Others

Source CBRE Vietnam Q4 2014

Source CBRE Vietnam Q4 2014

High-end restaurants moving out

More casual FampB moving in

FOOD amp BEVERAGE Steady demand ndash New Entries - Expansion

26

VIETNAM RETAIL MARKET

FOOD amp BEVERAGE DESTINATIONS

Crescent Lake

ndash D7 HCMC

West Lake Hanoi

Almaz ndash Long Bien

Dist Hanoi

Source Google Images

27

VIETNAM RETAIL MARKET

ESTABLISHED amp EMERGING RETAIL NODES IN HANOI

West Lake

Korean Town ndash Trung Hoa Nhan Chinh Old Quarter

Source Google Images

28

VIETNAM RETAIL MARKET

UNCONVENTIONAL RETAIL IN HCMC

CBD Location

Cheaper rent

New concept young cool

Word of Mouth

Roof-top beer Club

Upstairs Cafeacute Fashion store ndash In small allyrsquos

Cinema in 4-star Hotel

Source Google Images

29

VIETNAM RETAIL MARKET

Therersquos enough of the pie for everyone

ONLINE SHOPPING

Foreigner Players keep investing Rocket

Internet (Lazadavn Zaloravn Lamidovn)

701Search (ChoTotvn)

More Big Local Players to join market

VinEcom (Vingroup) Sendo (FPT) VCCorp

24h

Contribution from services providers

online payment shipping

Support from Government Vietnam E-

commerce and Information Technology

Agency ndash Ministry of Industry and Trade

Individual sellers mostly through

Facebook Instagram

30

VIETNAM RETAIL MARKET

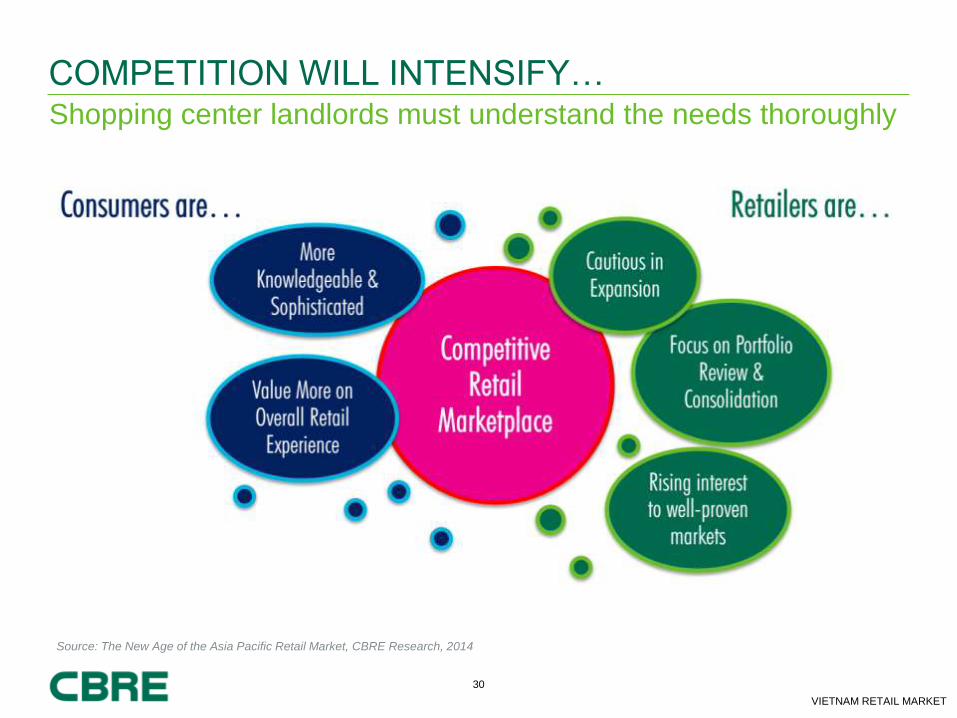

Shopping center landlords must understand the needs thoroughly

COMPETITION WILL INTENSIFYhellip

Source The New Age of the Asia Pacific Retail Market CBRE Research 2014

31

VIETNAM RETAIL MARKET

CBRE recommends shopping cente landlords four strategies

STRATEGIES FOR SUCCESS

Source The New Age of the Asia Pacific Retail Market CBRE Research 2014

32

VIETNAM RETAIL MARKET

CBRE recommends retailers adapt their online strategy

WHAT SHOULD LANDLORDS DO TO CATCH THE TREND

Big data is here to help Use existing data provided by

customers to formulate a

more tailored strategies to

enhance overall shopping

experience

Create simple and useful apps 35 of survey

respondents admitted

to have never been

using mobile

applications

designed specifically for shopping

centers For most app users simplicity

and ease of use is critical

Build your brand Holding special events at shopping centers may

not generating additional sales however they

are the key to crafting a mallrsquos brand and image

BRAND

OTHER INDOCHINA MARKETS UPDATES

34

VIETNAM RETAIL MARKET

LAOS MARKET UPDATE - VIENTIANE

Home Ideal Talat Sao

Mall 1

Talat Sao

Mall 2 ASEAN

Mall

D Mart

Vientiane

New World

San Jiang

market

450

Vanthong

Plaza

Lane Xang

Arcade

Vanthong

Plaza

Vientiane

Centre

View Mall

That Luang

Plaza

TTTM

Nakhone Sup

Vientiane

Complex

(BIM)

World

Trade

Centre

Future projects Current projects

35

VIETNAM RETAIL MARKET

LAOS MARKET UPDATE ndash FUTURE SUPPLY

VIENTIANE CENTER Vientiane Laos

Complex of Office Shopping center amp Service

Apartments

Developer North Nong Chan

Development amp Commercial

Center Company Co Ltd Retail GFA 53333 sqm

Completion 2015

WORLD TRADE CENTER Vientiane Laos

Complex of Office Shopping center Residential amp

Hotel

Developer Lao International Development Co Ltd

Retail GFA 200000 sqm

Completion 2016

36

VIETNAM RETAIL MARKET

THAT LUANG PLAZA Vientiane Laos

Shopping center

Developer Chitchareune That Luang

Plaza Sole Co Ltd

Retail GFA 26880 sqm

Completion Q22016

VIENTIANE NEW WORLD Vientiane Laos

Complex of Business Center

Shopping center amp Residential

Developer CAMCE

Retail GFA 80000 sqm

Completion Q22016

LAOS MARKET UPDATE ndash FUTURE SUPPLY

37

VIETNAM RETAIL MARKET

CAMBODIA MARKET UPDATES ndash EXISTING SUPPLY

38

VIETNAM RETAIL MARKET

TK AVENUE

Developer TK Avenue Co

GFA 11000 sq m

Opening Date 2011

PARAGON

Developer Paragon

GFA 10000 sq m

Opening Date 1995

AEON PHNOM PENH

Developer Aeon

GFA 104000 sq m

Opening Date 2014

SORYA SHOPPING CENTER

Developer Canadia

GFA 40000 sq m

Opening Date 2003

CAMBODIA MARKET UPDATES ndash EXISTING SUPPLY

39

VIETNAM RETAIL MARKET

CAMBODIA MARKET UPDATES ndash EXISTING SUPPLY

VATTANAC TOWER

Developer Vattanac

GFA 7000 sq m

Opening Date 2014

NAGAWORLD

Developer NagaCorp

GFA 1055 sq m

Opening Date 1995

SOVANNA

Developer Canadia

GFA 25000 sq m

Opening Date 2008

YOUNG

Developer Young Co

GFA 28000 sq m

Opening date 2013

40

VIETNAM RETAIL MARKET

CAMBODIA MARKET UPDATE ndash FUTURE SUPPLY

LANDMARK

Developer HK Land

GFA 13000 sq m

Opening Date 2017

PARKSON PCC

Developer Hassan

GFA 70000 sq m

Opening Date 2016

41

VIETNAM RETAIL MARKET

CAMBODIA MARKET UPDATE ndash FUTURE SUPPLY

PARKSON LION CITY

Developer Lion Group

GFA 80000 sq m

Opening Date 2017

OLYMPIA CITY

Developer Canadia

GFA TBC sq m

Opening Date 2018

BPH TOWNCENTER

Developer Peng Huoth

GFA 143000 sq m

Opening Date 2018

THE BRIDGE

Developer Oxley

GFA 30000 sq m

Opening Date 2017

AEON PHNOM PENH 2

Developer Aeon

GFA TBC sq m

Opening Date TBC

NAGACITY WALK

Developer NagaCorp

GFA 15800 sq m

Opening Date 2017

42

VIETNAM RETAIL MARKET

Approximately 40 retail developments in Yangon

MYANMAR RETAIL MARKET OVERVIEW

South

Outer City

East

Outer City

North

Outer City

West

Outer City

Inner City

Down Town

Shopping centre

Department stores

Hypermarket

Supermarket

43

VIETNAM RETAIL MARKET

EXISTING PROJECTS IN YANGON MYANMAR

DAGON shopping CENTER

Mixed-use development

Developer Dagon International

Retail GFA 15000 sqm

Completion 2011

Junction Square

Shopping center

Developer STD

Retail GFA 30000 sqm

Completion 2012

TAW WIN CENTER

Shopping center

Developer

Retail GFA 45000 sqm

Completion 2011

44

VIETNAM RETAIL MARKET

PIPELINE PROJECTS IN YANGON MYANMAR

Myanmar Center

Mixed-use development

Developer Hoang Anh Gia Lai

(Vietnam)

Retail GFA 54000 sqm

Completion Q22015 (Retail)

Junction City

Landmark

Mixed-used development

Developer SPA Yoma Group

Retail GFA 38000 sqm

Completion 2016

Hotel Shopping mall Offices

Developer Shwe Taung Group

Retail GFA 53333 sqm

Completion 2016

RETAILER REPRESENTATION - ASIA

RETAILER ANALYTICS

46

VIETNAM RETAIL MARKET

CBRErsquos Retailer Analytics platform allows clients to

ASSESS AND SELECT THE

MOST PROFITABLE

TRADING LOCATIONS

DELIVER THE MOST

PROFITABLE STORE

We are the only real estate advisor who can bring together knowledge and data

on consumer demographics market size retailer activity turnover potential and

real estate affordability This combination allows us to provide you with the most

accurate assessment of profitability and viability at country city and store level

Our ability to model and review the largest number of retail destinations across

Asia means that we can identify unexpected locations and opportunities for you

We also use local knowledge of future retail developments to spot locations

which will become attractive in the longer term

Because our Retailer Representation team works hand-in-hand with our agency

teams throughout Asia we can ensure our country city and street level

recommendations are truly deliverable Once decisions have been made on the

target destinations our Asia Retailer Representation team will work with our

market leading agents to negotiate and deliver the best stores on the best terms

IDENTIFY LATENT

OPPORTUNITIES ACROSS

A BROAD GEOGRAPHY

BENEFITS TO YOU

47

VIETNAM RETAIL MARKET

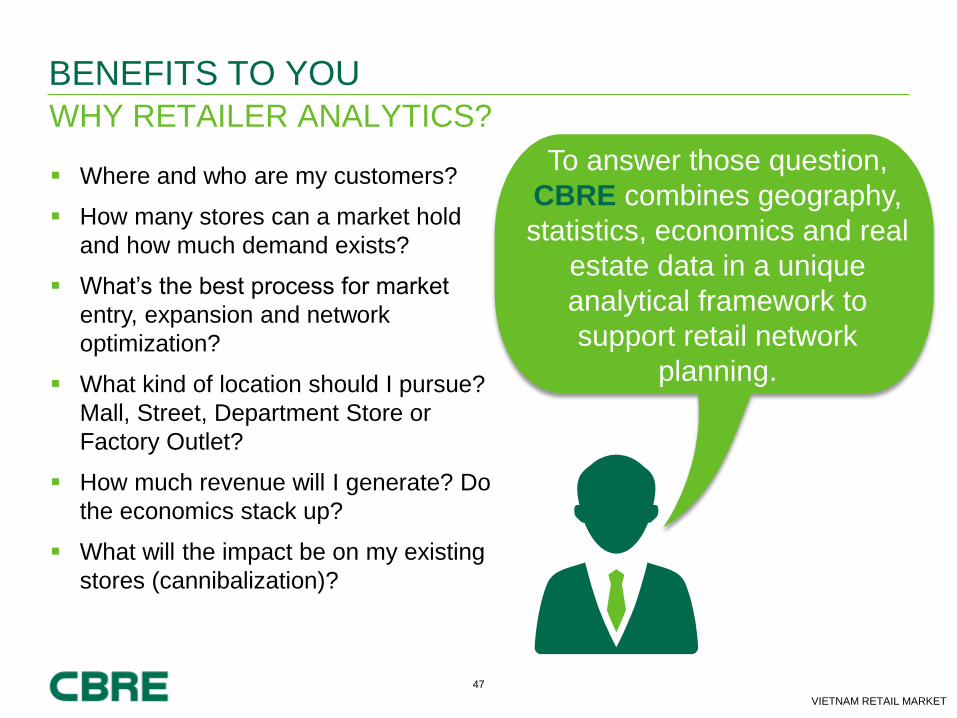

To answer those question

CBRE combines geography

statistics economics and real

estate data in a unique

analytical framework to

support retail network

planning

Where and who are my customers

How many stores can a market hold

and how much demand exists

Whatrsquos the best process for market

entry expansion and network

optimization

What kind of location should I pursue

Mall Street Department Store or

Factory Outlet

How much revenue will I generate Do

the economics stack up

What will the impact be on my existing

stores (cannibalization)

WHY RETAILER ANALYTICS

BENEFITS TO YOU

48

VIETNAM RETAIL MARKET

CBRE can provide clients a comprehensive strategy solution

for market entry and expansion existing store evaluations

and site selection The process is thorough putting our

clients in the best position for success throughout Asia

Country and city level

strategies

CBRE will recommend

executable strategies

and achievable locations

with the highest turnover

potential

Local agent insights

existing network

evaluation impact

analysis and new location

forecasting

DEVELOP OVERALL

STRATEGY

DRILL DOWN TO

MARKET LEVEL

SITE SELECTION

WHY RETAILER ANALYTICS

OUR APPROACH

49

VIETNAM RETAIL MARKET

WHY RETAILER ANALYTICS

MARKET ANALYTICS

RETAIL LANDSCAPE MARKET OVERVIEW

CATCHMENT MODELING + SALES DRIVERS + DEMAND AND SALES FORECASTING +

COMPETITOR BENCHMARKING

+

CBRE RECOMMENDATIONS

ACQUISITION AND STRATEGY MANAGEMENT

METHODOLOGY

50

VIETNAM RETAIL MARKET

PART I Market Overview and Retail Landscape

51

VIETNAM RETAIL MARKET

RETAILER ANALYTICS ndash PART I

MACRO ANALYSIS

DEMOGRAPHIC

TRANSPORT AND

INFRASTRUCTURE

UNIQUE CITY FEATURES

MARKET OVERVIEW

52

VIETNAM RETAIL MARKET

COMPETITOR MAPPING

GAP ANALYSIS

(identify market gaps for

further investigation)

COMPETITOR amp

ADJACENCY

(count per retail centre)

REAL ESTATE ANALYSIS

(rents landlords supply

pipeline sales densities)

RETAILER ANALYTICS ndash PART I RETAIL LANDSCAPE

GAP ANALYSIS Competitors Location Adjacencies Existing stores

53

VIETNAM RETAIL MARKET

Part 2 Market Analytics amp Competitor Benchmarking

PART II Market Analytics

54

VIETNAM RETAIL MARKET

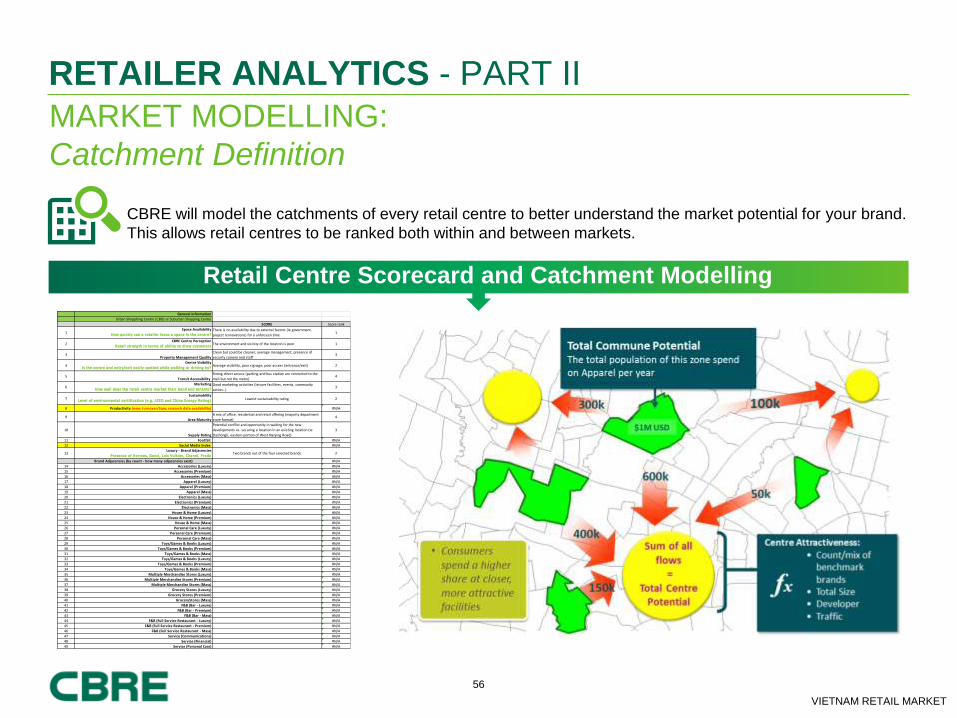

RETAILER ANALYTICS - PART II

MARKET MODELLING

Retail Centre Catchment Definition

CBRE will model the catchments of every retail centre to better understand the market potential

for your brand This allows retail centres to be ranked both within and between markets

Demand

Model current and future national

demand to census zones and correlate

to demographic socio-economic

characteristics

Supply

Assemble data to measure the size

and profile of every Retail Centre and

the fit with the client brand

Gravity model

Calibrate CBRErsquos Gravity Model to

replicate real world interactions

between Demand and Supply

METHODOLOGY

55

VIETNAM RETAIL MARKET

RETAILER ANALYTICS - PART II

MARKET MODELLING

Market Potential and Market Share

Market Potential and Market Share

Ho Chi Minh Retail Demand

at commune level

CBRE will model consumer demand to city district and commune administrative boundaries

to better understand where demand exists throughout Vietnam

56

VIETNAM RETAIL MARKET

RETAILER ANALYTICS - PART II

MARKET MODELLING

Catchment Definition

CBRE will model the catchments of every retail centre to better understand the market potential for your brand

This allows retail centres to be ranked both within and between markets

Retail Centre Scorecard and Catchment Modelling

General Information

Urban Shopphing Centre (CBD) or Suburban Shopping Centre

SCORE Score rank

1Space Availability

How quickly can a retai ler lease a space in the centreThere is no availability due to external factors (Ie government

project rennovations) for a unforseen time1

2CBRE Centre Perception

Retai l strength in terms of abi l i ty to draw customersThe environment and vicinity of the location is poor 1

3Property Management Quality

Clean but could be cleaner average management presence of

security camera and staff3

4Centre Visibility

Is the centre and entryexit easi ly spotted whi le walking or dr iving by Average visibility poor signage poor access (entranceexit) 2

5Transit Accessibility

Strong direct access (parking and bus station are connected to the

mall but not the metro)4

6Marketing

How wel l does the retai l centre market their band and tenantsGood marketing activities (leisure facilities events community

actionhellip)3

7Sustainability

Level of environmental certi fication (eg LEED and China Energy Rating) Lowest sustainability rating 2

8 Productivity (new turnoverSqm research data availability) NA

9Area Maturity

A mix of office residential and retail offering (majority department

store format)4

10

Supply Rating

Potential conflict and opportunity in waiting for the new

developments vs securing a location in an existing location (Ie

Dazhongli eastern portion of West Nanjing Road)

3

11 Footfall NA

12 Social Media Index NA

13Luxury - Brand Adjacencies

Presence of Hermes Gucci Luis Vuitton Chanel PradaTwo brands out of the four selected brands 2

Brand Adjacencies (by count - how many adjacencies exist) NA

14 Accessories (Luxury) NA

15 Accessories (Premium) NA

16 Accessories (Mass) NA

17 Apparel (Luxury) NA

18 Apparel (Premium) NA

19 Apparel (Mass) NA

20 Electronics (Luxury) NA

21 Electronics (Premium) NA

22 Electronics (Mass) NA

23 House amp Home (Luxury) NA

24 House amp Home (Premium) NA

25 House amp Home (Mass) NA

26 Personal Care (Luxury) NA

27 Personal Care (Premium) NA

28 Personal Care (Mass) NA

29 ToysGames amp Books (Luxury) NA

30 ToysGames amp Books (Premium) NA

31 ToysGames amp Books (Mass) NA

32 ToysGames amp Books (Luxury) NA

33 ToysGames amp Books (Premium) NA

34 ToysGames amp Books (Mass) NA

35 Multiple Merchandise Stores (Luxury) NA

36 Multiple Merchandise Stores (Premium) NA

37 Multiple Merchandise Stores (Mass) NA

38 Grocery Stores (Luxury) NA

39 Grocery Stores (Premium) NA

40 GroceryStores (Mass) NA

41 FampB (Bar - Luxury) NA

42 FampB (Bar - Premium) NA

43 FampB (Bar - Mass) NA

44 FampB (Full Service Restaurant - Luxury) NA

45 FampB (Full Service Restaurant - Premium) NA

46 FampB (Full Service Restaurant - Mass) NA

47 Service (Communications) NA

48 Service (Financial) NA

49 Service (Personal Care) NA

57

VIETNAM RETAIL MARKET

RETAILER ANALYTICS - PART II

CBRE works with

international clients to

understand what drives

sales in existing

locations to aid future

expansion

POTENTIAL DRIVERS OF SALES

COMPLEMENTARY

RETAILERS

FUTURE GROWTH

TO 2020 (GDP)

TOTAL MARKET SIZE

(SPEND)

OF

PROFESSION

OF MOST

AFFLUENT

GROUP

MALEFEMALE

COMPETING

RETAILERS

REVENUE DRIVERS

CASE STUDIES For luxury retailers we have worked with in Asia drivers often relate to

purchasing power and complimentarycompeting adjacencies rather

than market size or sheer volume of people

For a mid-market fashion brand in Malaysia the presence of those

aged 10-19 was important as this was the target market for the brand In

this case footfall was also essential because of the high volume of sales

required for what was an inexpensive product

For an upper-mid market watch retailer in the Taiwan we found that

sales were driven by those aged 25-44 years of age Additionally

affluence was a factor as well as market size and the presence of key

footfall drivers

58

VIETNAM RETAIL MARKET

RETAILER ANALYTICS - PART II

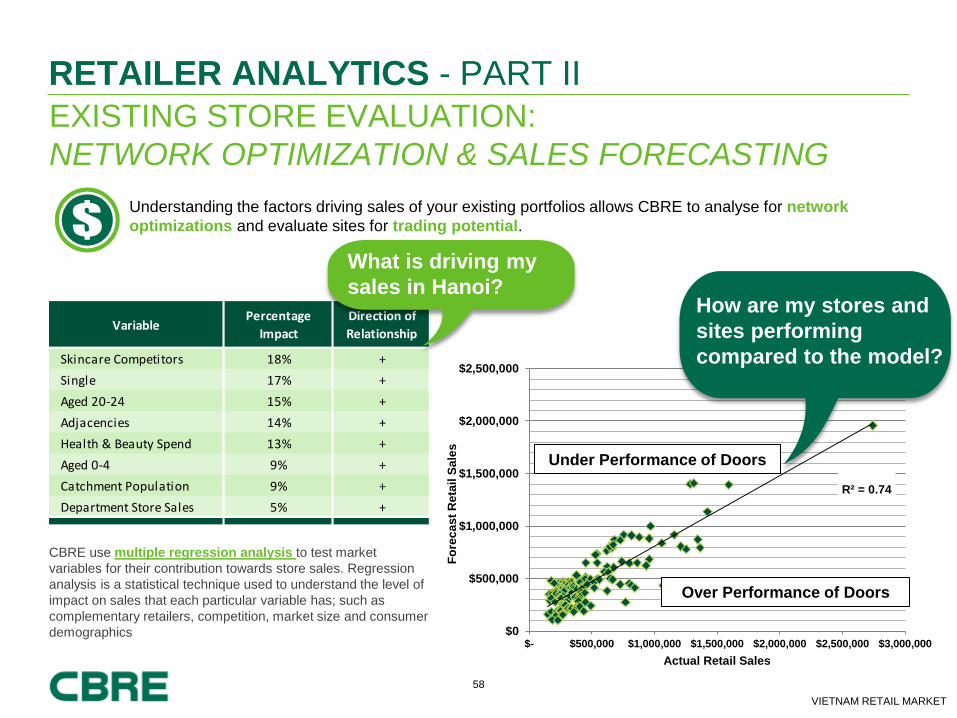

EXISTING STORE EVALUATION

NETWORK OPTIMIZATION amp SALES FORECASTING

VariablePercentage

Impact

Direction of

Relationship

Skincare Competitors 18 +

Single 17 +

Aged 20-24 15 +

Adjacencies 14 +

Health amp Beauty Spend 13 +

Aged 0-4 9 +

Catchment Population 9 +

Department Store Sales 5 +

Over Performance of Doors

Under Performance of Doors

Understanding the factors driving sales of your existing portfolios allows CBRE to analyse for network

optimizations and evaluate sites for trading potential

What is driving my

sales in Hanoi

Rsup2 = 074

$0

$500000

$1000000

$1500000

$2000000

$2500000

$- $500000 $1000000 $1500000 $2000000 $2500000 $3000000

Fo

rec

as

t R

eta

il S

ale

s

Actual Retail Sales

How are my stores and

sites performing

compared to the model

Under Performance of Doors

Over Performance of Doors

CBRE use multiple regression analysis to test market

variables for their contribution towards store sales Regression

analysis is a statistical technique used to understand the level of

impact on sales that each particular variable has such as

complementary retailers competition market size and consumer

demographics

59

VIETNAM RETAIL MARKET

RETAILER ANALYTICS - PART II

Retailer X Store Profitability

Models

Retailer X Store Profitability

Models

COUNTRY A COUNTRY X

TOWN B TOWN Y

Year 1 Year 1

Annual Turnover $750257 Annual Turnover $849958

Gross Profit $430493 Gross Profit $491915

Annual Rent + Rates $87037 Annual Rent + Rates $269266

Payroll $85875 Payroll $128798

Other Costs $49659 Other Costs $54283

Total Costs $222571 Total Costs $452348

Contribution $207922 Contribution $39567

Contribution as Turnover 28 Contribution as Turnover 5

CBRE uses cost

modelling to show

retailers what

operating costs will

apply and how this

impacts upon margin

Rent

Business rates

Cost of goods

Shipping

Head office costs

Advertisingmarketing costs

SALES FORECASTING

THE IMPACT OF RENT ON MARGIN

COSTS ASSESSED

Service charge

Employment costs

60

VIETNAM RETAIL MARKET

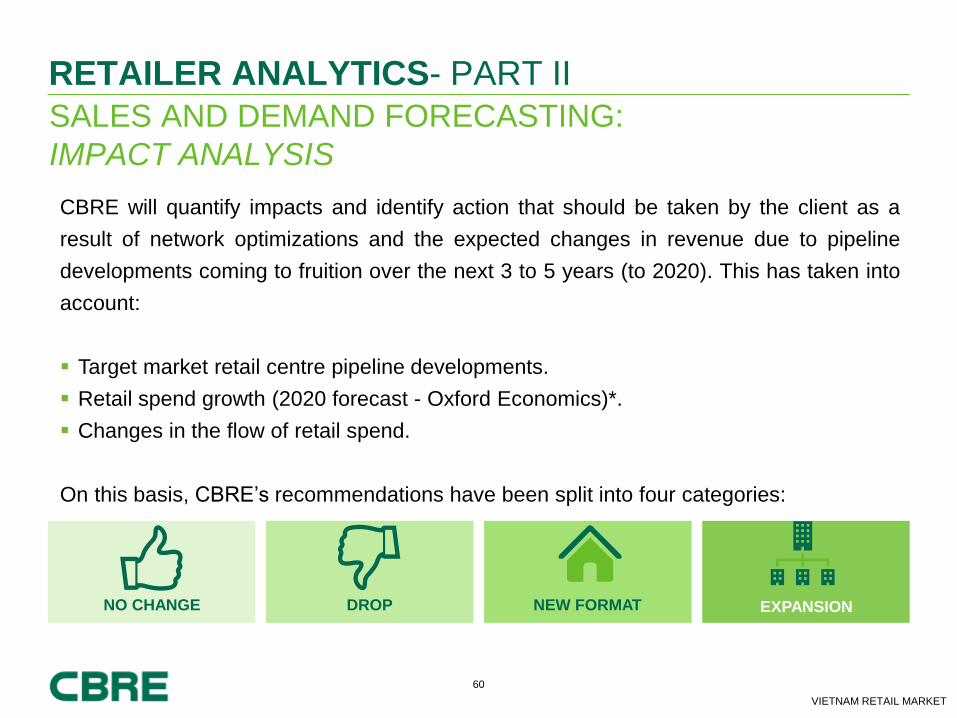

RETAILER ANALYTICS- PART II

SALES AND DEMAND FORECASTING

IMPACT ANALYSIS

NO CHANGE

CBRE will quantify impacts and identify action that should be taken by the client as a

result of network optimizations and the expected changes in revenue due to pipeline

developments coming to fruition over the next 3 to 5 years (to 2020) This has taken into

account

Target market retail centre pipeline developments

Retail spend growth (2020 forecast - Oxford Economics)

Changes in the flow of retail spend

On this basis CBRErsquos recommendations have been split into four categories

DROP NEW FORMAT EXPANSION

61

VIETNAM RETAIL MARKET

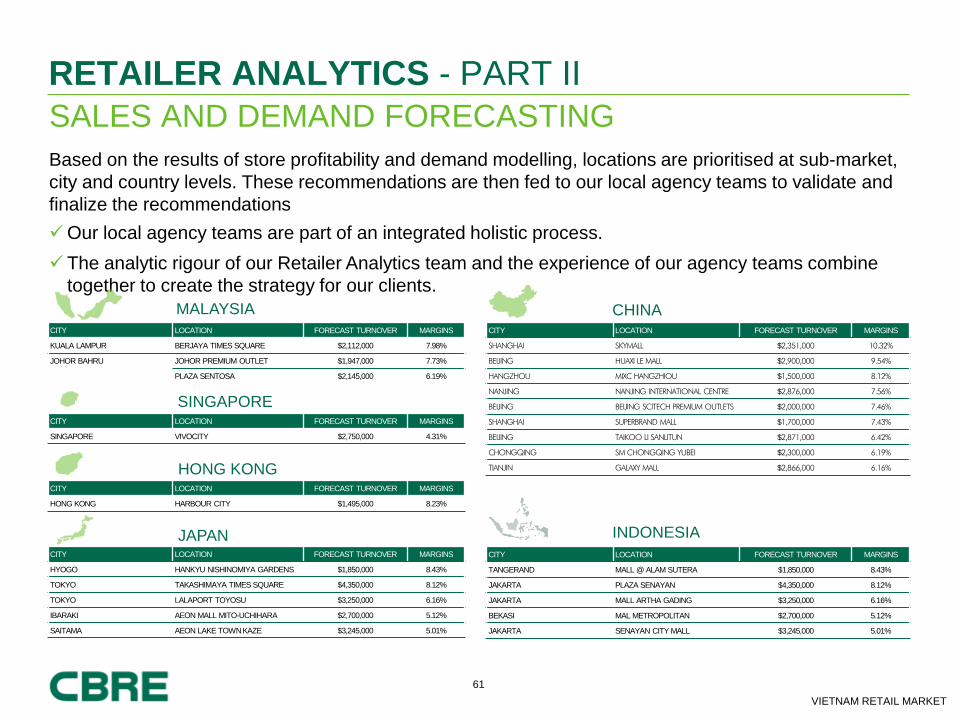

RETAILER ANALYTICS - PART II

Based on the results of store profitability and demand modelling locations are prioritised at sub-market

city and country levels These recommendations are then fed to our local agency teams to validate and

finalize the recommendations

Our local agency teams are part of an integrated holistic process

The analytic rigour of our Retailer Analytics team and the experience of our agency teams combine

together to create the strategy for our clients

CITY LOCATION FORECAST TURNOVER MARGINS

KUALA LAMPUR BERJAYA TIMES SQUARE $2112000 798

JOHOR BAHRU JOHOR PREMIUM OUTLET $1947000 773

PLAZA SENTOSA $2145000 619

CITY LOCATION FORECAST TURNOVER MARGINS

SINGAPORE VIVOCITY $2750000 431

CITY LOCATION FORECAST TURNOVER MARGINS

HONG KONG HARBOUR CITY $1495000 823

MALAYSIA

SINGAPORE

HONG KONG

CITY LOCATION FORECAST TURNOVER MARGINS

HYOGO HANKYU NISHINOMIYA GARDENS $1850000 843

TOKYO TAKASHIMAYA TIMES SQUARE $4350000 812

TOKYO LALAPORT TOYOSU $3250000 616

IBARAKI AEON MALL MITO-UCHIHARA $2700000 512

SAITAMA AEON LAKE TOWN KAZE $3245000 501

JAPAN

CITY LOCATION FORECAST TURNOVER MARGINS

SHANGHAI SKYMALL $2351000 1032

BEIJING HUAXI LE MALL $2900000 954

HANGZHOU MIXC HANGZHIOU $1500000 812

NANJING NANJING INTERNATIONAL CENTRE $2876000 756

BEIJING BEIJING SCITECH PREMIUM OUTLETS $2000000 746

SHANGHAI SUPERBRAND MALL $1700000 743

BEIJING TAIKOO LI SANLITUN $2871000 642

CHONGQING SM CHONGQING YUBEI $2300000 619

TIANJIN GALAXY MALL $2866000 616

CHINA

CITY LOCATION FORECAST TURNOVER MARGINS

TANGERAND MALL ALAM SUTERA $1850000 843

JAKARTA PLAZA SENAYAN $4350000 812

JAKARTA MALL ARTHA GADING $3250000 616

BEKASI MAL METROPOLITAN $2700000 512

JAKARTA SENAYAN CITY MALL $3245000 501

INDONESIA

SALES AND DEMAND FORECASTING

62

VIETNAM RETAIL MARKET

COMPETITORSrsquo RENTS

COMPETITOR BENCHMARKING

RETAILER ANALYTICS ndash PART II

COMPETITORSrsquo SALES ANALYSIS +

CBRE will provide competitor

benchmarking in the recommended

centres as an additional quantifier

of performance

63

VIETNAM RETAIL MARKET

PART III CBRE RECOMMENDATIONS

64

VIETNAM RETAIL MARKET

RETAILER ANALYTICS - PART III

The recommendation will assess the strongest retail markets evaluating existing and

future real estate The projects will be prioritized by country city and submarket

3 to 5 year growth or optimization strategy Recommendations by submarket

Mapping of target projects with relevant location and positioning

RECOMMENDATION

65

VIETNAM RETAIL MARKET

PART IV SOLUTIONS FOR EVERY RETAILER

66

VIETNAM RETAIL MARKET

RETAILER ANALYTICS

SOLUTIONS FORhellip

Market Entry

Market Overview

Retail Landscape

Market and Catchment Modeling

Demand Analysis and Sales Drivers

Market Potential

Competitor Benchmarking

Benefits

Understanding of the target market macro-economy

Understanding of rents landlords supply pipeline and

sales densities

Understanding of the competitive landscape and

competitor penetration

Understanding of market demand for brands and

categories

Achievable recommendations and locations with the

highest revenue potential

Achievable 3 to 5 year growth strategy

Benefits

Understanding of the target market macro-economy

Understanding of rents landlords supply pipeline and

sales densities

Understanding of the competitive landscape and

competitor penetration

Understanding of available demand for brands and

categories

Impact Analysis ndash Competitor Sales and Pipeline

Sales Forecasting based on a sound statistical

approach

Achievable 3 to 5 year growth strategy

Market Expansion amp Optimization

Market Overview

Retail Landscape

Competitor and Adjacency Impact Analysis

Market and Catchment Modeling

Sales Impact Analysis

Existing Store Assessment

Network Optimization

Sales Forecasting

Pipeline Impact Analysis

Competitor Benchmarking

67

VIETNAM RETAIL MARKET

Case Studies

CBRE CLIENTS

For more information please contact

Michael Ruby Head of Asia Retailer Analytics CBRE Asia T +852 2820 2916

Email michaelrubycbrecomhk

Joel Stephen Head of Retailer Representation

CBRE Asia T +852 2820 2803

Email joelstephencbrecomhk

Richard Leech MRICS Executive Director Retail Services CBRE South East Asia

Hang Vu Senior Manager Retail Services CBRE Vietnam

T +84 912 573 130

Email richardleechcbrecom

T +84 903 012 175

Email hangvucbrecom

CAMBODIA MARKET

MYANMAR MARKET

Trang Tran Senior Manager Retail Services

CBRE Vietnam T +84 912 486 399

Email trangtrancbrecom

Laszlo Fulop Senior Retail Consultant Retail Services

CBRE Vietnam T +84 972 058 444

Email laszlofulopcbrecom

Michael Vong Retail Consultant Retail Services

CBRE Vietnam +84 917 294 834

michaelvongcbrecom

LAOS MARKET

69

VIETNAM RETAIL MARKET BANGLADESH | CAMBODIA | INDONESIA | LAO PDR | MYANMAR | SINGAPORE | THAILAND

| VIETNAM

RETAIL LEGAL UPDATE VIETNAM CAMBODIA AND LAO PDR

5 FEBRUARY 2015

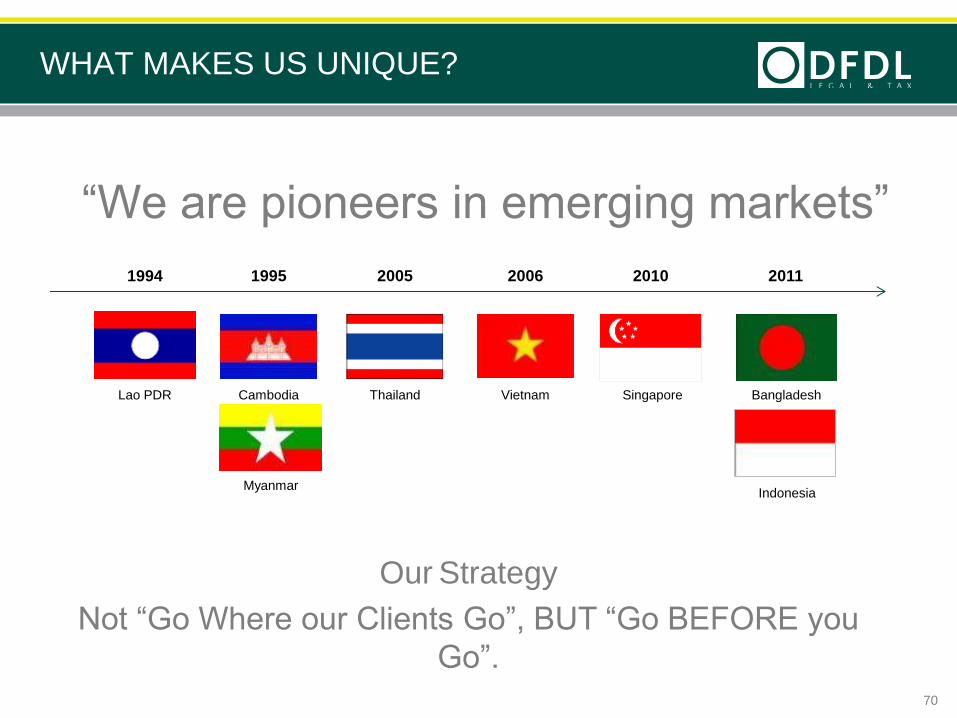

WHAT MAKES US UNIQUE

ldquoWe are pioneers in emerging marketsrdquo

2011 1994 2010 2006 1995 2005

Singapore Bangladesh

Indonesia

Lao PDR Cambodia

Myanmar

Thailand Vietnam

Our Strategy

Not ldquoGo Where our Clients Gordquo BUT ldquoGo BEFORE you

Gordquo

70

71

Part 1

Key Legal Regulations

VIETNAM

Key news laws are expecting to boost the retail industry in Vietnam

ndash Law on Investment

ndash Law on Enterprises

ndash Law on Real Estate Business and Law on Housing

The new laws will enter into force on 1st July 2015

Decree 23 of the Government dated 12 February 2007

Circular 08 of the Ministry of Industry and Trade (ldquoMOITrdquo) on trading

activities (including retail business)

72

VIETNAM

Circular 34 of the MOIT entered into force in February 2014 it

ndash announces the schedule for implementation of foreign companiesrsquo

trading activities

ndash replaces Decision 10 on the same subject which was issued in 2007

As of 1 January 2015 pursuant to the ASEAN Trade in Goods

Agreement (ATIGA) 10000 merchandise items coming from ASEAN

member countries are free of custom barriers (import tax reduced to

0)

73

CAMBODIA

The Civil Code of 2007

The 2011 Law on implementation of certain provisions of Civil Code

Law on Investment dated 4 August 1994 (as amended 4 February

2003)

Law on Commercial Enterprises dated 19 June 2005

The 2001 Land Law

74

LAOS PDR

Investment Promotion Law 02NA dated 08 July 2009

Decree on the Implementation of the Investment Promotion Law

119PM dated 20 April 2011

Decision regarding Businesses on Retail and Wholesale Trade

0977MOIC ITD dated 18 May 2012

Enterprise Law ( 46NA 26 December 2013)

Decree on Document Registration 52PM dated 13 March 1993

Notification 1489 regarding Categories of Goods and Investment

ratio open to foreign investors for investment in the Establishment of

import business units for wholesales in the Lao PDR dated 20 July

2012

75

76

Part 2

Selected key issues in retail

77

VIETNAM

VIETNAM-MARKET ACCESS TO TRADERS

Direct investment (100 foreign owned or joint venture) or Indirect

investment (franchise nominee-proxies Structure)

Definition of ldquoretailingrdquo the activity of selling [purchased] goods

directly to final customers

Definition of ldquooutletrdquo a unit owned by an enterprise for the purpose of

conducting retailing activities

Permitted goods retail of all legally imported and domestically

produced products (except tobacco pharmaceuticals crude oil

processed oil books newspapers magazines precious stones etc)

78

VIETNAM-MARKET ACCESS TO TRADERS CONTrsquoD

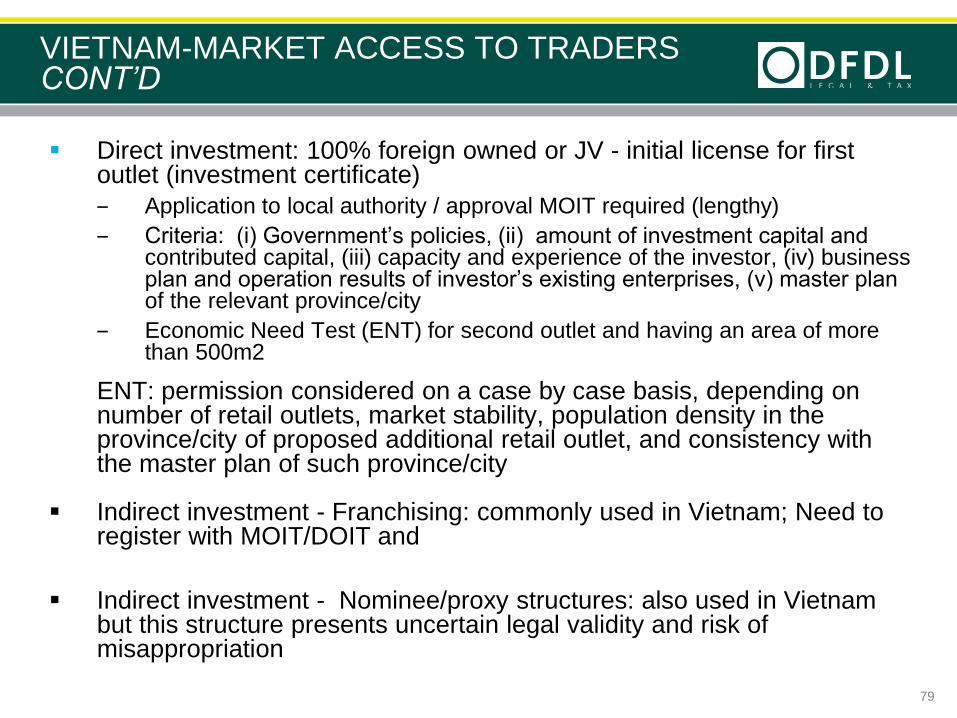

Direct investment 100 foreign owned or JV - initial license for first outlet (investment certificate)

‒ Application to local authority approval MOIT required (lengthy)

‒ Criteria (i) Governmentrsquos policies (ii) amount of investment capital and contributed capital (iii) capacity and experience of the investor (iv) business plan and operation results of investorrsquos existing enterprises (v) master plan of the relevant provincecity

‒ Economic Need Test (ENT) for second outlet and having an area of more than 500m2

ENT permission considered on a case by case basis depending on number of retail outlets market stability population density in the provincecity of proposed additional retail outlet and consistency with the master plan of such provincecity

Indirect investment - Franchising commonly used in Vietnam Need to register with MOITDOIT and

Indirect investment - Nomineeproxy structures also used in Vietnam but this structure presents uncertain legal validity and risk of misappropriation

79

VIETNAM-PROTECTION OF INTELLECTUAL PROPERTY (IP)

Adopt and implement a strategy

Protect trademarks domain names designs sensitive information

Obtain from your local partners to protect your and their IP

Practical issues ndash protect your brand consumers rights understand

and anticipate rumors know and work with local authorities and

restrictions on advertisement

80

VIETNAM-MARKET ACCESS TO DEVELOPERS

Lease land from the State or infrastructure developer

Necessity to undertake a land due diligence to make sure the land

location is appropriate

Approval in principle on the project location

Conditions to develop a real estate project such as master plan

architecture design compliance

Land Use Right granted in compliance with the Investment Certificate

81

82

CAMBODIA

CAMBODIA-SECTORAL OVERVIEW

No specific sectorial legal framework

Freehold or leasing

No specific land use type with respect to certificates of titlezoning

classification

Several draft laws draft lawamendments to the Law on Investment

Draft Sub-Decree on Urbanization of the capital city towns and

urban areas Draft Law on Construction Draft Law on Environment

Impact Assessment Draft Consumer Protection Law and Draft E-

Commerce Law

83

CAMBODIA-MARKET ACCESS TO TRADERS

Trading of goods 100 foreign owned entity possible

Food and beverage ndash restaurants cafes bakeries etc 100

foreign owned entity possible

Franchising ndash possible (and common) but no specific franchise law

yet in Franchising is governed mainly by the provisions of the Civil

Code

Registration of trademark possible (including exclusive trademark

licensing right) under the Law on Marks Trade Names and Acts of

Unfair Competition

84

CAMBODIA-PROTECTION OF IP

bull Trademark law is the most developed intellectual property system

but enforcement remains problematic due to nascent (but

developing) legal infrastructure and government authority resources

bull Protection of patents industrial designs and models are less

developed but government authority understanding and international

interest grows year on year

bull Risk local company registers marks although it is not the rightful

owner

bull Strategy first register trademark in Cambodia regardless of any

presence in Cambodia Proactive vigilance by IP proprietor of

infringement is key

85

CAMBODIA-MARKET ACCESS TO DEVELOPERS

Joint Venture with no more than 49 foreign capital can own land

Landholding structuring possible (different classes of shares +

protection documents + mortgage)

Alternative long term lease up to 50 year-term It is required to be

registered with Cadastral authorities to be enforceable against third

parties

86

87

LAOS PDR

LAOS-MARKET ACCESS TO TRADERS

ldquo Retail Sale Businessrdquo means the final stage of the business of

goods distribution to individuals or households for consumption

ldquoWholesale Businessrdquo means a goods distribution business to people

or legal entities for the purpose of further production wholesale or

retail

The 2012 Retail Decision states that Retail Sales Business is

reserved only for Lao citizens

88

LAOS-MARKET ACCESS TO TRADERS CONTrsquoD

For Retail Sales Business foreign individuals and legal entities are

only permitted to

conduct the distribution of goods within the Lao PDR through

distributors or franchisees of Lao nationality residing in Lao

PDR or

Invest or enter into a joint venture for the construction of new

forms of modern sales establishments for business units which

are to be reserved for trading such as hypermarkets

supermarkets shopping centers or malls in accordance with the

Investment Promotion Law and related laws and regulations

89

LAOS-PROTECTION OF IP

Registration of industrial property at Ministry of Science and

Technology

IP includes patents petty patents industrial designs trademarks

trade names trade secrets etc

Owner of IP enjoys the benefits derived from the IP transfer all or

part of their IP rights to other person by sale exchange lease or

assignment permit other persons to seek benefits over all or part of

the IP bequeath and assign the rights in the IP to other person and

protect the IP from violation by other parties

Strategy first register trademark in the Lao PDR regardless of any

presence in the Lao PDR

90

LAOS-MARKET ACCESS TO DEVELOPERS

Land ownership is not an option

Land lease possible

30 years from private owners

50 years from the Government (concessions)

75 years in specific economic zones and special economic

zones

Under 2009 Investment Promotion Law foreign-invested entities with

a minimum of USD 500000 equity investment may hold ldquoland use

rightsrdquo but not fully implemented

91

LAOS-STRUCTURING OPTIONS

Supply Chain Management Contract Under this structure a foreign

owned entity provides supply chain management services to a locally

owned entity These may include the lease or sub-lease of retail or

wholesale premises contractual licensing of intellectual property

licensed rights to IT systems and marketing methodologies

warehousing accounting and administrative services The fees payable

to the supply chain management services may be structured so that they

mirror what the foreign entity might have earned by way of dividends had

it been entitled to enjoy equity participation in the locally owned entity

Investing in SEZ The foreign owned supply chain if incorporated in a

Special Economic Zone (ldquoSEZrdquo) in the Lao PDR will be eligible for

significant tax benefits and may also obtain an exemption from the

wholesale and retail restrictions described above

92

THANK YOU

93

Tran Thi Vu Hanh Partner Vietnam

Deputy Managing Director Ho Chi Minh City Office

hanhtrandfdlcom

94

VIETNAM RETAIL MARKET

Excellence middot Creativity middot Trust Since 1994

BANGLADESH | CAMBODIA | INDONESIA | LAO PDR | MYANMAR | SINGAPORE | THAILAND | VIETNAM

wwwdfdlcom

2

VIETNAM RETAIL MARKET

Vietnam Market Overview

Market Trends

Other Indochina Markets Updates

Retailer Analytics

Legal updates on Retail Real Estate

CONTENT

VIETNAM MARKET OVERVIEW

4

VIETNAM RETAIL MARKET

APAC Real GDP Growth (2014-2015) vs Long Term Average

VIETNAM GDP GROWTH ndash REGIONrsquoS 2ND BEST

0

2

4

6

8

10

12

Vie

tna

m

Ind

one

sia

Ind

ia

Thaila

nd

Sou

th K

ore

a

Sin

ga

po

re

Hong

Kon

g

Ja

pa

n

Chin

a

New

Ze

ala

nd

Austr

alia

Phili

ppin

es

Taiw

an

Ma

laysia

Y-o

-Y R

ea

l G

DP

Gro

wth

(

)

2014F 2015F Average 2004 - 2013

Improvement in

geopolitical

pressure

China slow down -

knock-on effect

Source CBRE Research Oxford Economics December 2014

The chart does not tell this Group markets in

Export driven

Improvement in geopolitical tension

China slowdown ndash knock-on effect on commodity-export markets like Australia and New Zealand

Japan growth is minimal

Recovery in export on the

back of stronger global

demand

Oil price

drops

SLOWING IMPROVING

Election in

2016

5

VIETNAM RETAIL MARKET

OIL PRICES GETTING INCREDIBLY CHEAP

Oil had been getting stronger since 2009 2010 but then declined significantly since mid-2014

Crude oil price

Good consequences

Stronger consumptions due to lower industrial

input and logistics costs (-3 approx)

Lower construction cost

Lower building operating cost (service charge)

Bad consequences

Weakening VNDUSD

Falling oil world prices would slash Vietnamrsquos

state budget by around US$3 billion

But just a minimal impacts against VND

(Sufficient USD reserves surplus trade balance

robust FDI low inflation)

6

VIETNAM RETAIL MARKET

0

5

10

15

20

25

2007 2008 2009 2010 2011 2012 2013 2014

Inte

rest ra

te (

)

Average CPI (y-o-y) Rediscounting rate Refinancing rate Lending rate Deposit rate

FUNDING GETTING CHEAPER

Source Vietnamese General Statistical Office

Interest Rates and Inflation

Lending rate for the first 12 months

bull Techcombank 949

bull Vietcombank 799

bull ACB 89

7

VIETNAM RETAIL MARKET

Turnover continues to increase whilst growth continues to slow

RETAILS amp SERVICES TURNOVER

0

8

16

24

32

40

0

500

1000

1500

2000

2500

3000

35002

00

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4P

Gro

wth

Ra

te (

)

Tu

rno

ve

r (T

rilli

on

do

ng

)

Retails and Services Turnover Retails and Services Turnover Growth

8

VIETNAM RETAIL MARKET

Strong supply from Hanoi market

RETAIL MARKET UPDATE

Source CBRE Vietnam Q2 2014

Retail supply by city (NLA lsquo000 sqm)

0

200

400

600

800

1000

1200

HCMC Hanoi HCMC Hanoi HCMC Hanoi HCMC Hanoi HCMC Hanoi HCMC Hanoi

2011 2012 2013 2014 2015F 2016F

Re

tail

su

pp

ly b

y c

ity (

NL

A lsquo0

00

sq

m)

9

VIETNAM RETAIL MARKET

0

200

400

600

800

1000

1200

Beiji

ng

She

nzhe

n

Ban

gkok

New

De

lhi

Kua

la L

um

pur

Gua

ngzh

ou

Hano

i

Sha

ngh

ai

Ma

nila

Mu

mb

ai

Sin

ga

po

re

Me

lbou

rne

Ho

Chi M

inh C

ity

Tokyo

Sydn

ey

Ade

laid

e

Brisb

an

e

Hong

Kon

g

Ja

kart

a

Auckla

nd

Pert

h

Taip

ei

De

ve

lop

me

nt

Pip

elin

e (

lsquo00

0 s

qm

)

2015F

APAC Development Pipeline

RETAIL MARKET UPDATE

Source CBRE Research Q4 2014

10

VIETNAM RETAIL MARKET

Softer rents but vacancy still up

Source CBRE Vietnam Q4 2014

AVERAGE ASKING RENT

(US$smmonth)

VACANCY RATE

()

2014

Q4

Q3

Q2

Q1

2013

Q4

Q3

Q2

Q1

2012

Q4

Q3

Q2

Q1

2011

Q4

Q3

Q2

Q1

NON-CBD CBD

050100150 0 50 100 150

-3

3

9

15

21

-40000

0

40000

80000

120000

160000

2010 2011 2012 2013 2014

Va

ca

ncy R

ate

(

)

Net A

bso

rptio

n (

sm

)

Net Absorption (sm) Vacancy

HANOI MARKET PERFORMANCE 2014

11

VIETNAM RETAIL MARKET

Consistent performance for the last eight quarters

HOCHIMINH CITY PERFORMANCE 2014

Source CBRE Vietnam Q4 2014

AVERAGE ASKING RENT

(US$smmonth)

VACANCY RATE

()

2014

Q4

Q3

Q2

Q1

2013

Q4

Q3

Q2

Q1

2012

Q4

Q3

Q2

Q1

2011

Q4

Q3

Q2

Q1

NON-CBD CBD

050100150 0 50 100 150

0

4

8

12

16

20

-20000

0

20000

40000

60000

2011 2012 2013 2014

Va

ca

ncy R

ate

(

)

Net A

bso

rptio

n (

sm

)

Net absorption Vacancy rate

12

VIETNAM RETAIL MARKET

HANOI

NEW SUPPLY IN 2014

LOTTE MART

(Mipec Tower)

Dong Da District

GFA 27000 sm

Opened Q12014

Shopping Centre amp Department Store

LOTTE

DEPARTMENT STORE

Ba Dinh District

GFA 21480 sm

Opened Q32014

Trang Tien Plaza reopening

Add more FampB

More affordable brands

ALMAZ by Vingroup

Convention ndash FampB ndash Retail amp Entertainment Center

Long Bien District

GFA 25 ha

Opened Q42014

13

VIETNAM RETAIL MARKET

HoChinhMinh City

NEW SUPPLY IN 2014

AEON MALL

TAN PHU CELADON

Tan Phu District

GFA 42100 sm

Anchor Aeon Mart Aeon

department store CGV Dream

Games

Opened Q12014

Shopping Centre amp Department Store

AEON MALL

BINH DUONG CANARY

Binh Duong

GFA 62100 sm

Anchor Aeon Mart Aeon

department store CGV Play

Time

Opened Q42014

LOTTE MART CONG HOA

Tan Binh District

GFA 10000 sm

Anchor Lotte mart Lotte Cinema

Wall Street English California

Fitness

Opened Q42014

14

VIETNAM RETAIL MARKET

Hanoi

UPCOMING RETAIL DEVELOPMENT

AEON MALL HANOI

bull Long Bien district

bull GFA 108000 sm

bull 4 floors

bull Under construction

bull Expected to open

Q4 2015

Expect to open in 2015

HOA BINH GREEN CITY

bull Hai Ba Trung District

bull GFA 25000 sm

bull 4 floors

bull Opened on Jan 31st

bull Offering free rentals in

perpetuity

HO GUOM PLAZA

bull Ha Dong District

bull GFA 23400 sm

bull 5 floors

bull Completed Open

for lease

bull Anchor tenants

Tran Anh CGV

bull Expected to open

(fully) Q2 2015

VINCOM NGUYEN CHI

THANH

bull Dong Da District

bull GFA 44500 sm

bull Under construction

bull Expected to open Nov

2015

15

VIETNAM RETAIL MARKET

Ho Chi Minh City

UPCOMING RETAIL DEVELOPMENT

Expect to open in 2015

VINCOM THU DUC

Thu Duc District

GFA 27860 sm

Expected to open Feb 8

2015

SC VIVOCITY

District 7

GFA 62000 sm

Expected to open April 2015

PEARL PLAZA

Binh Thanh District

GFA 20000 sm

Expected to open July 2015

THAO DIEN PEARL

District 2

GFA 20000 sm

Expected to open July 2015

16

VIETNAM RETAIL MARKET

METRO LINE NO 1 AND RETAIL PROJECTS

Taken in front of Rex Hotel on Jan 7 2015

Vinhomes Central Park

Thao Dien Pearl

The Vista An Phu

Vincom MegaMall Masteri Thao Dien

Cantavil Premier

The Estella Heights

NEW EASTERN BUS STATION

LONG BINH DEPOT

The One

Union Square Tax Plaza

Saigon Center

17

VIETNAM RETAIL MARKET

Retailing hospots across APAC ndash strong activities in Hanoi

RETAIL MARKET UPDATE

HANOI

27 ENTRIES

18

VIETNAM RETAIL MARKET

Hanoi amp HCMC Markets

NEW RETAIL ENTRIES IN 2014

Ho Chi Minh City

Hanoi

MORE TO COMEhellip

MARKET TRENDS

20

VIETNAM RETAIL MARKET

Vingrouprsquos movements in retail sector

LOCAL PLAYERS EXPAND

VINCOM MEGAMALL THAO

DIEN

GFA 100000 sm

Expected completion 2015

VINCOM

NGUYEN CHI

THANH

GFA 44500 sm

25 Shopping Centers in 2015 - HCMC HANOI BAC NINH

VIET TRI DA NANG CAN THO BIEN HOA AN GIANG

HAI PHONG hellip

To open 100

supermarkets and

1000 convenience

stores in the next

3 years

VINCOM

DA NANG

GFA 31000 sm

VINCOM

CAN THO 2

GFA 14500 sm

MampA activity by Vingroup

13 supermarkets and convenience

stores with ~ 40000 sm retail area

VINCOM MEGAMALL

TRUONG CHINH -

HCMC

GFA 100000 sqm

To invest US$166 million

hellip

21

VIETNAM RETAIL MARKET

Mostly Asian retailers Korea Japanhellip

AND FOREIGNERS TOO

Expanded to Dong Nai and Da Nang

Opened Lotte Mart Binh Duong and Phan Thiet

bull Bought Pico

bull Opened Lotte Department Store in Hanoi

2008

2012

2013

2014 2020

To open

60 super-

markets

in

Vietnam

Ministop Trung Nguyen (25 share)

Aeon Mall HCMC

Aeon Mall Binh Duong

Aeon Mall Hanoi

20 hypermarkets

2011

1 2014

11 2014

2015

2020

Already successfully acquired a 30ndash

stake in Fivimart (operates 20 stores

in Hanoi) amp a 49 stake in Citimart

(runs 27 stores mainly in HCMC)

Opened first store in HCMC

22

VIETNAM RETAIL MARKET

hellipand Thailand

AND FOREIGNERS TOO

BJCrsquos Bs Mart bought 94 Family marts in Vietnam

aim to expand to 300 stores by 2018

BJC acquires Metro Vietnam for

US$879 million incl 19 distribution

centers and related real estate

Central Grouprsquos Robins Department

Store in Hanoi and HCMC

Central Group buys 49 stake in Nguyen Kim

49 51

Target gt 50 stores in 2019

23

VIETNAM RETAIL MARKET

DEPARTMENT STORE

2005

2013 - 2014

Robins Department Store

Diamond Plaza

Parkson Department

Store

2015 - 2016

Vingroup

Department

store

1999

Lotte Department Store

Takashimaya

Source Google Images

24

VIETNAM RETAIL MARKET

AFFORDABLE RETAIL

SAIGON SQUARE 3

District 3 HCMC

GFA 3100 sm

Opened 1 Jan 2015

HUNG VUONG SQUARE

District 5 HCMC

GFA 9500 sm

Opened 31 Dec 2014

More Bazaar emerged Supermarket

AEON CITIMART

Go Vap District HCMC

Opened Jan 2015

Rent-free Shopping Center

V+ Shopping Center ndash Hoa Binh

Green City

Minh Khai Street Hai Ba Trung District Hanoi

GFA 25000 sqm

Open 31st Jan 2015

Lower number of SKUrsquos

Rental free for all store selling ldquoMade-in-Vietnamrdquo

products

25

VIETNAM RETAIL MARKET

76

24 Shopping center

High Street

FampB is increasingly dominant with 47

Tenants enquiries by preferences 2014

High Street stores are still highly

preferred by retailers

Tenants enquiries by categories 2014

of enquiries

Source CBRE Vietnam Q4 2014

FampB

Fashion

Accessories

Education

Cosmetics

Furniture

Others

Source CBRE Vietnam Q4 2014

Source CBRE Vietnam Q4 2014

High-end restaurants moving out

More casual FampB moving in

FOOD amp BEVERAGE Steady demand ndash New Entries - Expansion

26

VIETNAM RETAIL MARKET

FOOD amp BEVERAGE DESTINATIONS

Crescent Lake

ndash D7 HCMC

West Lake Hanoi

Almaz ndash Long Bien

Dist Hanoi

Source Google Images

27

VIETNAM RETAIL MARKET

ESTABLISHED amp EMERGING RETAIL NODES IN HANOI

West Lake

Korean Town ndash Trung Hoa Nhan Chinh Old Quarter

Source Google Images

28

VIETNAM RETAIL MARKET

UNCONVENTIONAL RETAIL IN HCMC

CBD Location

Cheaper rent

New concept young cool

Word of Mouth

Roof-top beer Club

Upstairs Cafeacute Fashion store ndash In small allyrsquos

Cinema in 4-star Hotel

Source Google Images

29

VIETNAM RETAIL MARKET

Therersquos enough of the pie for everyone

ONLINE SHOPPING

Foreigner Players keep investing Rocket

Internet (Lazadavn Zaloravn Lamidovn)

701Search (ChoTotvn)

More Big Local Players to join market

VinEcom (Vingroup) Sendo (FPT) VCCorp

24h

Contribution from services providers

online payment shipping

Support from Government Vietnam E-

commerce and Information Technology

Agency ndash Ministry of Industry and Trade

Individual sellers mostly through

Facebook Instagram

30

VIETNAM RETAIL MARKET

Shopping center landlords must understand the needs thoroughly

COMPETITION WILL INTENSIFYhellip

Source The New Age of the Asia Pacific Retail Market CBRE Research 2014

31

VIETNAM RETAIL MARKET

CBRE recommends shopping cente landlords four strategies

STRATEGIES FOR SUCCESS

Source The New Age of the Asia Pacific Retail Market CBRE Research 2014

32

VIETNAM RETAIL MARKET

CBRE recommends retailers adapt their online strategy

WHAT SHOULD LANDLORDS DO TO CATCH THE TREND

Big data is here to help Use existing data provided by

customers to formulate a

more tailored strategies to

enhance overall shopping

experience

Create simple and useful apps 35 of survey

respondents admitted

to have never been

using mobile

applications

designed specifically for shopping

centers For most app users simplicity

and ease of use is critical

Build your brand Holding special events at shopping centers may

not generating additional sales however they

are the key to crafting a mallrsquos brand and image

BRAND

OTHER INDOCHINA MARKETS UPDATES

34

VIETNAM RETAIL MARKET

LAOS MARKET UPDATE - VIENTIANE

Home Ideal Talat Sao

Mall 1

Talat Sao

Mall 2 ASEAN

Mall

D Mart

Vientiane

New World

San Jiang

market

450

Vanthong

Plaza

Lane Xang

Arcade

Vanthong

Plaza

Vientiane

Centre

View Mall

That Luang

Plaza

TTTM

Nakhone Sup

Vientiane

Complex

(BIM)

World

Trade

Centre

Future projects Current projects

35

VIETNAM RETAIL MARKET

LAOS MARKET UPDATE ndash FUTURE SUPPLY

VIENTIANE CENTER Vientiane Laos

Complex of Office Shopping center amp Service

Apartments

Developer North Nong Chan

Development amp Commercial

Center Company Co Ltd Retail GFA 53333 sqm

Completion 2015

WORLD TRADE CENTER Vientiane Laos

Complex of Office Shopping center Residential amp

Hotel

Developer Lao International Development Co Ltd

Retail GFA 200000 sqm

Completion 2016

36

VIETNAM RETAIL MARKET

THAT LUANG PLAZA Vientiane Laos

Shopping center

Developer Chitchareune That Luang

Plaza Sole Co Ltd

Retail GFA 26880 sqm

Completion Q22016

VIENTIANE NEW WORLD Vientiane Laos

Complex of Business Center

Shopping center amp Residential

Developer CAMCE

Retail GFA 80000 sqm

Completion Q22016

LAOS MARKET UPDATE ndash FUTURE SUPPLY

37

VIETNAM RETAIL MARKET

CAMBODIA MARKET UPDATES ndash EXISTING SUPPLY

38

VIETNAM RETAIL MARKET

TK AVENUE

Developer TK Avenue Co

GFA 11000 sq m

Opening Date 2011

PARAGON

Developer Paragon

GFA 10000 sq m

Opening Date 1995

AEON PHNOM PENH

Developer Aeon

GFA 104000 sq m

Opening Date 2014

SORYA SHOPPING CENTER

Developer Canadia

GFA 40000 sq m

Opening Date 2003

CAMBODIA MARKET UPDATES ndash EXISTING SUPPLY

39

VIETNAM RETAIL MARKET

CAMBODIA MARKET UPDATES ndash EXISTING SUPPLY

VATTANAC TOWER

Developer Vattanac

GFA 7000 sq m

Opening Date 2014

NAGAWORLD

Developer NagaCorp

GFA 1055 sq m

Opening Date 1995

SOVANNA

Developer Canadia

GFA 25000 sq m

Opening Date 2008

YOUNG

Developer Young Co

GFA 28000 sq m

Opening date 2013

40

VIETNAM RETAIL MARKET

CAMBODIA MARKET UPDATE ndash FUTURE SUPPLY

LANDMARK

Developer HK Land

GFA 13000 sq m

Opening Date 2017

PARKSON PCC

Developer Hassan

GFA 70000 sq m

Opening Date 2016

41

VIETNAM RETAIL MARKET

CAMBODIA MARKET UPDATE ndash FUTURE SUPPLY

PARKSON LION CITY

Developer Lion Group

GFA 80000 sq m

Opening Date 2017

OLYMPIA CITY

Developer Canadia

GFA TBC sq m

Opening Date 2018

BPH TOWNCENTER

Developer Peng Huoth

GFA 143000 sq m

Opening Date 2018

THE BRIDGE

Developer Oxley

GFA 30000 sq m

Opening Date 2017

AEON PHNOM PENH 2

Developer Aeon

GFA TBC sq m

Opening Date TBC

NAGACITY WALK

Developer NagaCorp

GFA 15800 sq m

Opening Date 2017

42

VIETNAM RETAIL MARKET

Approximately 40 retail developments in Yangon

MYANMAR RETAIL MARKET OVERVIEW

South

Outer City

East

Outer City

North

Outer City

West

Outer City

Inner City

Down Town

Shopping centre

Department stores

Hypermarket

Supermarket

43

VIETNAM RETAIL MARKET

EXISTING PROJECTS IN YANGON MYANMAR

DAGON shopping CENTER

Mixed-use development

Developer Dagon International

Retail GFA 15000 sqm

Completion 2011

Junction Square

Shopping center

Developer STD

Retail GFA 30000 sqm

Completion 2012

TAW WIN CENTER

Shopping center

Developer

Retail GFA 45000 sqm

Completion 2011

44

VIETNAM RETAIL MARKET

PIPELINE PROJECTS IN YANGON MYANMAR

Myanmar Center

Mixed-use development

Developer Hoang Anh Gia Lai

(Vietnam)

Retail GFA 54000 sqm

Completion Q22015 (Retail)

Junction City

Landmark

Mixed-used development

Developer SPA Yoma Group

Retail GFA 38000 sqm

Completion 2016

Hotel Shopping mall Offices

Developer Shwe Taung Group

Retail GFA 53333 sqm

Completion 2016

RETAILER REPRESENTATION - ASIA

RETAILER ANALYTICS

46

VIETNAM RETAIL MARKET

CBRErsquos Retailer Analytics platform allows clients to

ASSESS AND SELECT THE

MOST PROFITABLE

TRADING LOCATIONS

DELIVER THE MOST

PROFITABLE STORE

We are the only real estate advisor who can bring together knowledge and data

on consumer demographics market size retailer activity turnover potential and

real estate affordability This combination allows us to provide you with the most

accurate assessment of profitability and viability at country city and store level

Our ability to model and review the largest number of retail destinations across

Asia means that we can identify unexpected locations and opportunities for you

We also use local knowledge of future retail developments to spot locations

which will become attractive in the longer term

Because our Retailer Representation team works hand-in-hand with our agency

teams throughout Asia we can ensure our country city and street level

recommendations are truly deliverable Once decisions have been made on the

target destinations our Asia Retailer Representation team will work with our

market leading agents to negotiate and deliver the best stores on the best terms

IDENTIFY LATENT

OPPORTUNITIES ACROSS

A BROAD GEOGRAPHY

BENEFITS TO YOU

47

VIETNAM RETAIL MARKET

To answer those question

CBRE combines geography

statistics economics and real

estate data in a unique

analytical framework to

support retail network

planning

Where and who are my customers

How many stores can a market hold

and how much demand exists

Whatrsquos the best process for market

entry expansion and network

optimization

What kind of location should I pursue

Mall Street Department Store or

Factory Outlet

How much revenue will I generate Do

the economics stack up

What will the impact be on my existing

stores (cannibalization)

WHY RETAILER ANALYTICS

BENEFITS TO YOU

48

VIETNAM RETAIL MARKET

CBRE can provide clients a comprehensive strategy solution

for market entry and expansion existing store evaluations

and site selection The process is thorough putting our

clients in the best position for success throughout Asia

Country and city level

strategies

CBRE will recommend

executable strategies

and achievable locations

with the highest turnover

potential

Local agent insights

existing network

evaluation impact

analysis and new location

forecasting

DEVELOP OVERALL

STRATEGY

DRILL DOWN TO

MARKET LEVEL

SITE SELECTION

WHY RETAILER ANALYTICS

OUR APPROACH

49

VIETNAM RETAIL MARKET

WHY RETAILER ANALYTICS

MARKET ANALYTICS

RETAIL LANDSCAPE MARKET OVERVIEW

CATCHMENT MODELING + SALES DRIVERS + DEMAND AND SALES FORECASTING +

COMPETITOR BENCHMARKING

+

CBRE RECOMMENDATIONS

ACQUISITION AND STRATEGY MANAGEMENT

METHODOLOGY

50

VIETNAM RETAIL MARKET

PART I Market Overview and Retail Landscape

51

VIETNAM RETAIL MARKET

RETAILER ANALYTICS ndash PART I

MACRO ANALYSIS

DEMOGRAPHIC

TRANSPORT AND

INFRASTRUCTURE

UNIQUE CITY FEATURES

MARKET OVERVIEW

52

VIETNAM RETAIL MARKET

COMPETITOR MAPPING

GAP ANALYSIS

(identify market gaps for

further investigation)

COMPETITOR amp

ADJACENCY

(count per retail centre)

REAL ESTATE ANALYSIS

(rents landlords supply

pipeline sales densities)

RETAILER ANALYTICS ndash PART I RETAIL LANDSCAPE

GAP ANALYSIS Competitors Location Adjacencies Existing stores

53

VIETNAM RETAIL MARKET

Part 2 Market Analytics amp Competitor Benchmarking

PART II Market Analytics

54

VIETNAM RETAIL MARKET

RETAILER ANALYTICS - PART II

MARKET MODELLING

Retail Centre Catchment Definition

CBRE will model the catchments of every retail centre to better understand the market potential

for your brand This allows retail centres to be ranked both within and between markets

Demand

Model current and future national

demand to census zones and correlate

to demographic socio-economic

characteristics

Supply

Assemble data to measure the size

and profile of every Retail Centre and

the fit with the client brand

Gravity model

Calibrate CBRErsquos Gravity Model to

replicate real world interactions

between Demand and Supply

METHODOLOGY

55

VIETNAM RETAIL MARKET

RETAILER ANALYTICS - PART II

MARKET MODELLING

Market Potential and Market Share

Market Potential and Market Share

Ho Chi Minh Retail Demand

at commune level

CBRE will model consumer demand to city district and commune administrative boundaries

to better understand where demand exists throughout Vietnam

56

VIETNAM RETAIL MARKET

RETAILER ANALYTICS - PART II

MARKET MODELLING

Catchment Definition

CBRE will model the catchments of every retail centre to better understand the market potential for your brand

This allows retail centres to be ranked both within and between markets

Retail Centre Scorecard and Catchment Modelling

General Information

Urban Shopphing Centre (CBD) or Suburban Shopping Centre

SCORE Score rank

1Space Availability

How quickly can a retai ler lease a space in the centreThere is no availability due to external factors (Ie government

project rennovations) for a unforseen time1

2CBRE Centre Perception

Retai l strength in terms of abi l i ty to draw customersThe environment and vicinity of the location is poor 1

3Property Management Quality

Clean but could be cleaner average management presence of

security camera and staff3

4Centre Visibility

Is the centre and entryexit easi ly spotted whi le walking or dr iving by Average visibility poor signage poor access (entranceexit) 2

5Transit Accessibility

Strong direct access (parking and bus station are connected to the

mall but not the metro)4

6Marketing

How wel l does the retai l centre market their band and tenantsGood marketing activities (leisure facilities events community

actionhellip)3

7Sustainability

Level of environmental certi fication (eg LEED and China Energy Rating) Lowest sustainability rating 2

8 Productivity (new turnoverSqm research data availability) NA

9Area Maturity

A mix of office residential and retail offering (majority department

store format)4

10

Supply Rating

Potential conflict and opportunity in waiting for the new

developments vs securing a location in an existing location (Ie

Dazhongli eastern portion of West Nanjing Road)

3

11 Footfall NA

12 Social Media Index NA