REPUBLIC OF ESTONIA (BANKING AND CÜRBENCY BEFOBM) …The net proceeds of the loan were therefore to...

24

[Distributed to the Council and the Members of the League.] C. 186. M. 60. 1928. ii (F. 514.) Geneva, August 3rd, 1928. LEAGUE OF NATIONS REPUBLIC OF ESTONIA (BANKING AND CÜRBENCY BEFOBM) 7 % LOAN, 1927 FIRST ANNUAL REPORT BY THE TRUSTEE covering the period from June 15lh, 1927, to June 30th , 1928. I ntroduction . In conformity with the decision of the Council of September 15th, 1927. I have the honour to submit to the Council of the League of Nations my first annual report as Trustee for the " Republic of Estonia (Banking and Currency Reform) 7 % Loan. 1927 ”, it may be useful to give in this first report a somewhat detailed description of the execution of the scheme and of the duties of the Trustee. The essential features of the Estonian banking and currency reform, on which the Estonian Government and the financial experts of the League had already been working for some time, are contained in the Protocol signed at Geneva on December 10th. 1926. by the Estonian Minister of Finance, and approved by the Council on the same day. As provided for in this Protocol, the following laws were passed by the Estonian Parliament early in May 1927. viz., (1) the Eesti Pank Statutes Law, (2) the Monetary Law of Estonia, (3) the Law to terminate the Issue of Treasury and " Change ” Notes, and (4) the Foreign Loan Law 1. Thereupon, it was permissible to open negotiations for the loan which was to be issued under the auspices of the League and which was to produce an effective net yield of £1.350,000. F oreign L oan . The agreements for the loan, after submission to the Chairman of the Financial Committee for approval, were signed on June 15th, 1927, with representatix es of the British and American issuing houses, viz.. the British Foreign and Colonial Corporation, associated with the Midland Bank. London, and Messrs. Hallgarten & Co., New York. The British portion of the loan was £700.000 (of wdiich £200.000 were placed in Llolland, in the form of sterling bonds), and the American portion $4,000,000, or approximately £821,912. The loan bears interest at 7 per cent, and the issue price in both countries was 941 per cent, from which there had to be deducted the commissions and underwriting charges of the issuing houses, amounting, for the London issue, to 5 per cent and for the American portion to 5^ per cent. The net amount thus receivable by the Government was, in the case of the former, per cent, and in that of the latter, 89J per cent. At these respective net prices, the total yield of the loan, stated in terms of British currency, was about £1,361,600, which was duly paid on July 1st, 1927. The loan is to be repaid in forty years by an accumulative sinking fund of | per cent, to be employed half-yearly in the purchase of bonds below par, or in their amortisation by drawings at par. One of the clauses of the General Bond for the loan deserves special mention. Article 14 fcl) °f that document lays down that " the Government will not, so long as any of the bonds remain outstanding, permit the Statutes of the Bank of Issue as at present constitut ed to be altered in any manner which, in the opinion of the Financial Committee of the League of Nations, might te conducive to the depreciation of Estonian currency in terms of English or United States of America currency ”. 1 For the text of these laws, see document C.2*27.M.89.19*27.11. 5,1 N. i.OoO (F.) 825 (A,) 8/28. — Imp, Réunies, Chambéry. Publications of the League of Nations II, ECONOMIC AND FINANCIAL 1928. II. 42.

Transcript of REPUBLIC OF ESTONIA (BANKING AND CÜRBENCY BEFOBM) …The net proceeds of the loan were therefore to...

[ D i s t r i b u t e d to the Council and the Members of th e League.]

C. 186. M. 6 0 . 1928. i i(F. 514.)

Geneva, A ugus t 3rd, 1928.

L E A G U E OF N A TIO N S

REPUBLIC OF ESTONIA (BANKING AND CÜRBENCY BEFOBM)

7 % LOAN, 1927

FIRST ANNUAL REPORT BY THE TRUSTEE

covering the period from J u n e 15lh, 1927, to J u n e 3 0 th , 1928.

I n t r o d u c t i o n .

In conform ity w ith th e decision of th e Council of Sep tem ber 15th, 1927. I have the honour to submit to th e Council of th e League of Nations m y first annua l re p o r t as T rustee for the " Republic of E s ton ia (Banking and Currency Reform) 7 % Loan. 1927 ” ,

i t m ay be useful to give in th is first re p o r t a som ewhat detailed description of the execution of the scheme and of th e duties of the Trustee.

The essential features of th e E ston ian ban k in g and currency reform, on which the Estonian Government a n d th e financial experts of th e League h a d a lready been w orking for some time, are contained in th e P rotocol signed a t Geneva on Decem ber 10th. 1926. b y th e Estonian Minister of F inance, and approved by th e Council on th e same day.

As p rovided for in th is Protocol, th e following laws were passed b y th e Eston ian Parliam ent early in May 1927. viz., (1) th e Eesti P a n k S ta tu te s Law, (2) th e M onetary Law of Estonia,(3) the Law to te rm in a te th e Issue of T reasu ry and " Change ” Notes, and (4) th e Foreign Loan Law 1. Thereupon, it was permissible to open negotia tions for th e loan which was to be issued under the auspices of th e League and which was to produce an effective n e t yield of £1 .350,000.

F o r e i g n L o a n .

The agreem ents for th e loan, a f te r submission to th e C hairm an of th e F inancial Committee for approval, were signed on J u n e 15th, 1927, w ith representatix es of th e B ri t ish and American issuing houses, viz.. th e Brit ish Foreign and Colonial Corporation, associated with the Midland Bank. London, and Messrs. H a llgar ten & Co., New York. The Brit ish portion of the loan was £700.000 (of wdiich £200.000 were placed in Llolland, in th e form of sterling bonds), and the American portion $4,000,000, or ap p rox im a te ly £821,912.

The loan bears in te res t a t 7 per cent, and th e issue price in b o th countries was 941 per cent, from which th e re h ad to be deducted th e commissions and underw rit ing charges of th e issuing houses, am ounting , for th e L ondon issue, to 5 per cent and for th e Am erican portion to 5^ per cent. The n e t a m o u n t th u s receivable b y th e G overnm en t was, in th e case of th e former,

per cent, and in t h a t of th e la tter , 89J per cent. A t these respective net prices, th e to ta l yield of th e loan, s ta ted in te rm s of Brit ish currency, was ab o u t £1,361,600, which was duly paid on J u ly 1st, 1927. The loan is to be repaid in fo r ty years b y an accum ulative sinking fund of | per cent, to be employed half-yearly in th e pu rchase of bonds below par, or in the ir amortisation b y drawings a t par.

One of th e clauses of th e General B ond for the loan deserves special mention. Article 14 fcl) °f that docum ent lays down t h a t " th e G overnm ent will not, so long as an y of the bonds remain outstanding, p erm it th e S ta tu te s of th e B a n k of Issue as a t p resen t cons t i tu t ed to be altered in any manner which, in th e opinion of th e F inancia l Com m ittee of th e League of Nations, m ight te conducive to th e deprecia tion of E s ton ian currency in te rm s of English or United Sta tes of America currency ” .

1 For the text of these laws, see document C.2*27.M.89.19*27.11.

5,1 N. i.OoO (F.) 825 (A,) 8/28. — Imp, Réunies, Chambéry.

Publications of the League of Nations

II, E C O N O M IC A N D FIN A N C IA L

1928. II. 42.

o __

W ith th e issue of th e loan, th e duties of th e T rus tee began. These duties fall into two p a r ts :

(a) The supervision of th e em ploym en t of th e loan proceeds ;

(b ) The contro l of th e assigned revenues.

Sir W alte r J . I ’. Williamson. C.M.G., who was no m in a ted by th e Council as AdvLev to th e Eesti Pank . has been ac t ing th ro u g h o u t as m y rep resen ta t ive in th e carrying out of m y duties as Trustee .

It is w ith pleasure t h a t I t a k e th is o p p o r tu n i ty of th a n k in g Sir W a l te r W illiamson publicly for his va luab le and in te ll igent collaboration.

T h e E m p l o y m e n t o f t h e L o a n P r o c e e d s .

In accordance w ith Article I, sub 5, of th e Protocol, th e yield of th e loan was paid into a special account under th e control of th e Trustee .

Article IX' provides t h a t th e loan m a y be employed and t h a t th e T rus tee shall p i mit p ay m en ts , on ly for th e following two purposes :

(1) " The p a y m e n t b y th e E s to n ian G overnm en t to th e B a n k of Issue of an am o u n t equiva len t to one million pounds sterling, in exchange for long-term assets of th e Bank.

(2) “ The applica t ion by th e Eston ian G overnm ent of th e balance of the loan for th e es tab lishm en t of a m ortgage ins t i tu te .

The n e t proceeds of th e loan were therefore to be divided into two portions, viz., £1,000,000, to be a l lo t ted to th e Eesti P a n k in p a y m e n t of a corresponding va lue of long-term loans to be t ransfe rred to a new M ortgage B a n k to be c reated for th e purpose, and £350,000 to be given to t h a t in s t i tu t io n as capita l . I t was also prov ided t h a t th e new S ta tu te s of th e Eesti Pank should become opera t ive as soon as i t had received th e above-m entioned sum of £1,000,000. and t h a t th e M onetary Law an d th e L aw to t e rm in a te th e Issue of T reasury and 11 Change ” Notes were to come in to force s im ultaneously w ith th e Eest i P a n k S ta tu te s .

I t will th u s be seen t h a t th e es tab l ishm ent of th e Mortgage B an k was th e last, and an essential, link in th e chain of en ac tm en ts requ ired to ca r ry o u t th e scheme of financial reform. I t accordingly becam e th e ta s k of th e G overnm ent, a f te r th e re tu rn of th e Minister of Finance from London, to fram e th e requ ired S ta tu te s and p resen t th e m to Parl iam en t .

P end ing th e i r enac tm en t , which it was hoped m ig h t b e effected in t im e to allow of the entire scheme coming in to force by th e beg inn ing -of Decem ber 1927, th e G overnm en t issued

ins truc t ions to th e Eesti P a n k in J u ly 1927. u n d e r th e a u th o r i ty of th e S ta tu te s th en in force, to p repare deta iled lists of i ts d iscounts , loans, and advances, divided in to th e th ree categories ind ica ted in t h e re p o r t of th e F inancia l Com mittee , d a ted Decem ber 8th, 1926, viz., (a) items of a long-dated cha rac te r to be transfe rred to th e G overnm ent, for even tua l t ransfe r to the M ortgage B a n k ; (b) i tem s to rem a in on th e books of th e Ees t i P a n k u n d er th e Government guaran tee , to th e a m o u n t of ap p ro x im a te ly Ekr. 15 million, represen ting credits which, though m ore liquid t h a n those referred to above, wrere still m ain ly long-term in charac ter , an d (c) items of a sh o r t - te rm cha rac te r which conformed to th e new S ta tu te s of th e B ank . T he Government a t th e sam e t im e ap p o in ted a represen ta t ive , who w as to re p o r t to th e Minister of F i n a n c e

regard ing groups (a ) an d (b) above, an d fu r th e r in s truc ted th e B an k t h a t th e entire classification w as to be ap p ro v ed by th e Adviser. T he B a n k was, a t th e sam e time, d i r e c t e d

gradua l ly to b r ing its opera t ions in to conform ity w ith th e New S ta tu te s , as set for th in Article 51 thereof, w ith a view to th e i r final adop t ion by Decem ber 1st. 1927.

The M ortgage B an k S ta tu te s w ere p resen ted to P a r l iam en t early in November, but it speedily becam e evident t h a t th e re w as a considerable am o u n t of dissatisfaction on th e part of th e New Sett le rs (one of th e G o v e rn m en t groups) regard ing th e powers of th e B an k to gran t the p a r t ic u la r ty p e of loans in w hich th e y were in terested , viz.. loans to th e smaller farmers who h av e li t t le or no real p ro p e r ty to offer as security . Certain of th e opposition par ties also raised th e poin t t h a t P a r l iam e n t had n o t been given sufficient in fo rm ation as to th e n a tu re of the assets to be t ransfe rred to th e G overnm en t b y th e Eesti P an k . A m otion was proposed to ap p o in t a special Commission to re -exam ine th e S ta tu te s of th e Mortgage Bank and to rep o r t to P a r l ia m e n t on th e n a tu re of t h e above-m en tioned assets.

T he G overnm ent, while a t firs t opposed to th e a p p o in tm e n t of th is Commission, eventually agreed to accept it if a sho r t t im e-l im it was fixed for its labour ; b u t th is th e proposers of the motion declined to accept. I t was accordingly carried in its original form, and th e Government thereupon resigned on N o vem ber 23rd, 1927. b u t continued in office in conform ity with local cons t i tu t iona l practice, pend ing th e form ation of a new G overnm ent.

As it was now ev iden t t h a t th e reform scheme could not come in to force by the beginning of D e c e m b e r as originally contem pla ted , th e G overnm ent issued a new set of instructions to the Eesti P a n k on N ovem ber 25th . 1927. According to these instructions , operations by th e Bank in respect of group (a) of th e classification were res tr ic ted to item s in regard to which there were prior unfulfilled obligations, or to operations approved b y th e G overnm ent representative, while, as regards group (b ) , t h e B an k was d irec ted to p repare liquidation schemes for each i tem in agreem ent with th e G o v e rn m en t represen ta t ive , p rovid ing for th e settlement of th e loan as speedily as th e circum stances of th e d eb to r rendered possible. Cases where th e liquidation ex tended beyond th ree years were to be referred to th e Government. Finally, th e ins truc t ions laid down t h a t th e B an k might, up to December 31st, 1927. g rant loans, etc.. u n d e r i ts existing S ta tu te s , to be classified under group (c), b u t only with the approval of th e Adviser.

P a s s in g of Mortgage B a n k Statutes.

The special Commission appo in ted by P a r l iam e n t im m edia te ly proceeded to carry out the duties imposed upon it. an d shortly after th e new G overnm en t had been formed (December 12th . the revised S ta tu te s were again p resen ted and were passed on Decem ber 16th (see Appendix II).

As m igh t be expected, th e principal change m ade by th e Commission and agreed to by Parliament, was a provision to allow of loans being g ran ted b y th e B a n k to individuals on personal security only. These loans, however, m a y n o t be m ad e o u t of its cap ita l or out of the money received from th e foreign loan. T he effect of th is prohib it ion will be tha t, in practice, such loans will be given a lmost en tire ly in th e form of debentures , which m ust be placed somewhere, an d t h a t i t will fall m ain ly on th e G overnm en t to t a k e th em up. unless the Bank can find o ther purchasers. The Eesti P an k will only be able to do so if th e debentures are guaranteed by th e G overnm ent. E ven so. the a m o u n t will be limited. In th e first place, the Eesi i Pan k is allowed by Article 51 (12) of its S ta tu te s to inves t in securities of. or guaranteed by, the Government, hav ing a m a tu r i ty up to five years, to an am o u n t n o t exceeding iis paid-up capital (Ekr. 5 millions). Secondly, th e Mortgage B an k will have to reckon with the competition of th e L and B ank, which has recen tly issued a series of five-year bonds for th is very purpose.

The only w ay in which th e B an k can give these loans in cash from its own funds will be out of sums repaid by o th e r borrowers ; b u t in so far as these o th e r borrowers are corporations, firms or persons whose deb ts hav e been tak e n over from th e Eesti P an k for adm inis tra t ion on Government account, i t will rest w ith th e G overnm en t to decide (as prov ided for in th e S ta tu tes of Lie M ortgage B ank) w h e th e r th e recoveries shall be paid over to th e Governm ent in cash or in debentures . If th e la t te r course is agreed to. i t will be an indirect w ay of financing these loans th ro u g h th e G overnm ent.

Releases by Trustee.

:n th e m ean tim e, in an t ic ipa t ion of th e passing of these S ta tu te s , a r rangem en ts had been mac: between th e G overnm en t an d th e T rus tee for th e release of t he £1,000,000 on J an u a ry 1st, 192". T he p a y m e n t to th e Eesti P a n k was effected on t h a t date . T he w ork of handing over the assets to be transfe rred to th e Mortgage B ank , an d th e docum ents re la ting thereto, has sine : been prac t ica l ly completed .

The £350,000 ea rm ark ed for th e Mortgage B an k were released on F eb ru a ry 27th, 1928, after receipt by th e T ru s tee of an officially certified t ran s la t io n of its S ta tu te s (Appendix II).

Ne w U n i t of C u r r e n c y .

nder th e M onetary Law. which also cam e in to force on J a n u a r y 1st. a new unit of currency ^as been established, viz., th e “ kroon divided into 100 cents, th e kroon having a \ a lu e equivalent to th e correspond ing Scandinavian unit , viz.. 18.16 to th e sovereign, and 1 cent bein': equal to 1 E es t im ark . th e previous unit. As th e p a r va lue of th e kroon approxim ates very closely to a h u n d red t im es t h a t a t which th e E es t im ark has been m ain ta ined foi a considerable period (an average of abou t 1,820 to th e £), th e final stabilisation of the Estonian currency has- been effected w ith o u t a n y dislocation.

— 4 —

A m a l g a m a t i o n o f N o t e I s s u e s .

In conform ity w ith th e provisions of th e Law to te rm in a te th e Issue of Treasury and Change ” Notes ( the la t te r also a G overnm en t emission), b o th no te issues have been

t e r m in a te d , and th e T reasury n o te issue has been am algam ated w ith t h a t of th e Eesti Pank. w ith th e exception of notes of 100 m ark s denom ination . These, toge ther w ith th e “ Change notes of 25 m arks , rem ain in circulation for th e t im e being as subsidiary money, w ith values of 100 and 25 cents respectively, un ti l replaced by coins of th e cents denom inations to be issued b y th e S ta te under th e M onetary Law. T he va lue of th e no te issues so transfe rred to the E es t i P a n k has been paid for b y th e G overnm ent, to the ex ten t of Kroons 5,000,000 in gold, and th e balance b y a corresponding cancellation of th e B a n k ’s deb t to th e Government in respect of th e G overnm en t special deposit w i th th e Bank.

S t a t e S a v i n g s B a n k .

As th e n ew S ta tu te s of th e Eesti P a n k p roh ib i t i t from paying in terest on deposits, a

Savings B an k has been created for th e express purpose of receiving sums from small depositors. This b an k commenced operations on J a n u a r y 1st. 1928— th e m ax im u m limit for a deposit on cu r ren t account by an ind iv idual being Ekr. 2,000, and t h a t for an ins t i tu t ion , Ekr. 5 . 000.

T he Minister of F inance has th e r ig h t to increase th e aforesaid limits on condition tha t , in such case, th ree m o n th s ’ notice m u s t be given for w ithdraw als . T he Minister of Finance is also em pow ered to prescribe conditions and periods for fixed deposits.

T he direction of th e S ta te Savings B an k is en t ru s ted to a Board of five members, presided over b y th e D ep u ty Minister of F inance, th e technical m an a g em en t being in th e hands of the Eesti Pank .

T he Board of Directors has sanctioned th e following ra te s of in terest, w ith th e approval of th e Minister of F inance :

C urren t accounts ...........................................................4 i per cent.F ixed deposits for periods of less t h a n one year . . 5 ,,F ixed deposits for one yea r ..............................................5§ ,,

G o v e r n m e n t D e p o s i t s L a w .

In connection w ith th e above-m entioned prohib it ion aga inst th e giving of in terest by the Eest i P a n k on deposits, a law was passed in N ovem ber 1 9 2 7 to p e rm it th e Minister of Financeto pu rchase out of var ious monies deposited w ith th e G overnm ent a t th e Eesti Pank , the bonds and deben tures of E s to n ian M ortgage B ank , and public securities and these guaran teed by the S ta te , up to th e am o u n t of 8 0 per cent of such deposits. In th e case of bonds or debentures not so guaran teed , a m a x im u m limit of 15 per cen t is fixed.

This law is n o t applicable to th e cu r ren t funds of th e T reasury , deposited with the Eesti P an k . I ts object is no t only to enable some in te re s t to be earned on funds deposited with the G overnm ent, b u t to p rovide th e m eans b y which th e S ta te will assist in creat ing a market for th e bonds and deben tu res m entioned .

The Assigned Revenues.

In conform ity w ith the Protocol, the excise duties on (a) tobacco, (b) beer, (c) mulches and o th e r m inor articles have been assigned as security for th e B ank ing and Currency Reform 7 % 1 9 2 7 Loan (Article II , sub 1). T he service of t h a t loan— to g e th e r w ith th e service of a small loan of £ 1 3 0 , 0 0 0 ra ided in 1 9 2 6 — has a first charge on th ese revenues (Article II , sub 2)

W ith regard to th e assigned revenues, th e T rus tee has th e following duties :

(1) T he assigned revenues are, as and w hen collected, paid in to a special account under th e control of th e T rus tee or his rep resen ta t iv e (Article I I I , sub 2).

(2) T he T rus tee has to re im burse to th e E s to n ia n G o v ern m en t any balance o n the accoun t n o t re ta inab le under th e P rotocol or th e loan c o n tra c t (Article II I ,

(3) T he consent of th e T rus tee is requ ired for th e use of th e assigned r e v e n u e s as securi ty for any new loan (Article I. sub 3).

(4) T he T rus tee has th e r ig h t to ve to any m easure of th e E s ton ian G o v e r n m e n t

which, in his opinion, would diminish th e va lu e of th e assigned revenues and thus th rea ten th e security of th e bondholders T he E s to n ian G overnm ent has the right to appeal to th e Council aga inst an y decision of th e T rus tee on th is point (Article II- sub 4).

— 5 —

(5) If th e yield of th e assigned revenues falls below 150 per cent of th e service of the loan, th e T rus tee m a y dem and t h a t additional revenues shall be assigned. Here again, th e E s to n ian G overnm ent has th e right to appeal to th e Council ( Article II. sub 5).

To these s t ipula tions of th e Protocol various detailed provisions, which n e e d n o t be repeated here, are added in th e General Bond, w ith regard to th e forw arding of monies by th e Trustee for th e p a y m e n t of th e service of th e loan, th e action to be tak e n in th e case of default, etc.

During th e period under review in th is report , th e adm in is t ra t ion of th e assigned revenues, which was carried o u t for m e b y Sir W a l te r Williamson, has n o t given rise to any difficulty.

Sir W alte r Williamson w atches th e Special Blocked A ccount into which th e assigned excise revenues are paid, and sees t h a t th e whole am o u n t a t credit of th e account is remitted at the beginning of each m o n th to t h e Midland B ank, London, and H allgar ten & Co., New York— the remittances being m ade in th e ra tio 700 : 822, representing th e portions of the loan raised in the two countries. As soon as the am oun ts required for each half-year ending J u n e 30th and December 31st have been th u s paid, th e fu r th e r credits to th e Blocked Account are released to th e G overnm ent, less the sum payab le in th e half-year to th e Royal Exchange Assurance, London, in respect of th e loan m entioned above of £130,000 tak e n in 1926 for t h e purchase of ra ilw ay m ater ia l in G reat Britain .

By th e te rm s of th is loan, th e G overnm ent under took no t to create an y specific fixed mort gagé charge or o th e r encum brance on an y of th e E s to n ian S ta te revenues for th e purpose of securing any7 o ther loan w ith o u t at th e same t im e creating a fixed m ortgage charge or o th e r like encumbrance to secure th e pay m e n t of th is loan. The Trus tee has accordingly en tered into a deed with th e lenders, u n d e r tak in g t h a t he will not a t any t im e release to th e G o v ern m en t any part of th e monies from t im e to t im e s tand ing a t th e credit of th e Special Blocked Account unies s. prior to such release, he is satisfied th a t th e p ay m e n ts to be m ad e to t h e lenders in respect of th is loan have been, or will be, du ly prov ided for.

The Trustee is furnished m o n th ly by th e Eesti P ank . where th e accoun t is kept, with a statement of th e sums credited during th e m o n th in respect of th e several assigned revenues, the amounts re m it ted during th e m onth , th e sums re ta ined in connection w ith the loan of £130.000, and th e balance, if any. This balance is released by th e Adviser, acting as the Trustee's represen ta tive , a f te r all pay m en ts chargeable to th e Blocked A ccount have either been made or re ta ined for fu tu re paym ent.

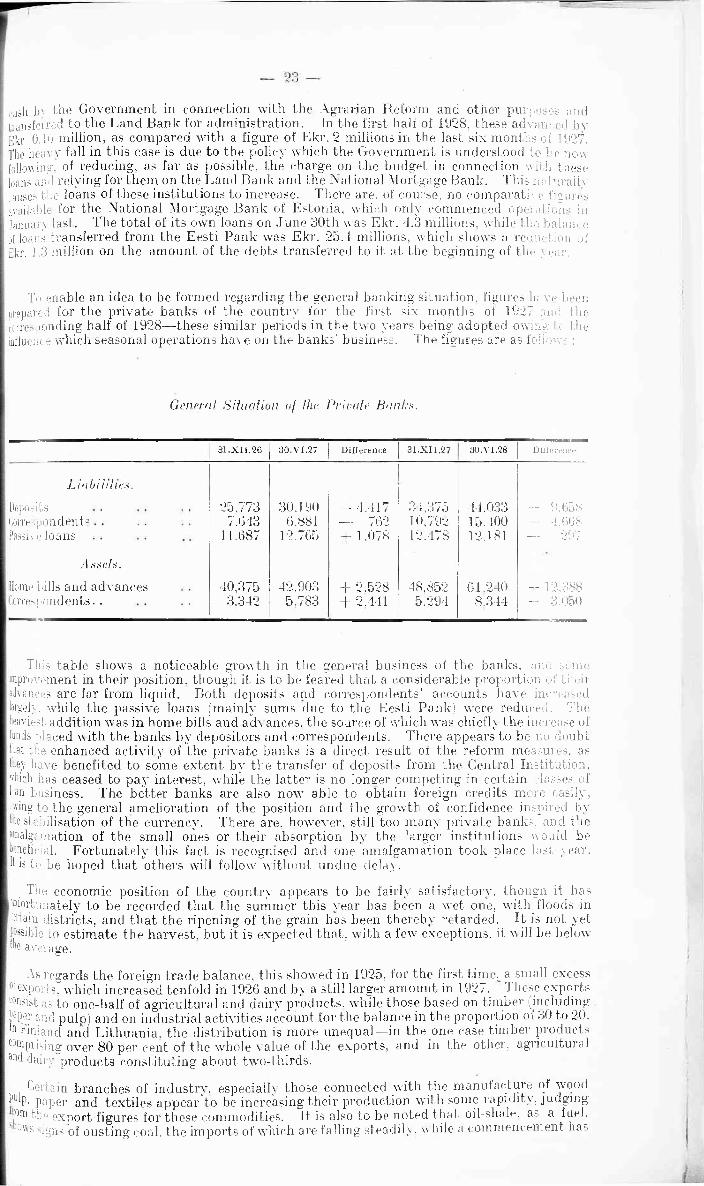

In A ppendix I. figures are given of th e yield of th e excise revenues assigned to the service of the In terna tional Loan of 1927 for th e th i rd an d four th q u a r te rs of t h a t year, and the first and second quar te rs of 1928, as also th e rem it tances-m ade there from for th e service of the loan for the second half of 1927 and th e first half of 1928. The yield for each of th e above-mentionedfour quarters represents th e following app ro x im a te percentages of one-quarter of the annualsum necessary for th e service of th e loan, as com pared w ith th e 150 per cent required by the Protocol :

1927 % 1928 %

T hird q u a r te r . . . . 270 F ir s t q u a r te r . . . . 242F o u r th ....................... 225 Second ........................252

In order to enable th e Council to follow th e financial resu lts of th e bank ing and m onetary reform accomplished in E ston ia under th e auspices of th e League of Nations. I have requested the Adviser of th e Eesti P a n k to dra f t a no te on th e developm ent of th e financial situation during the period covered by th is report . This no te forms A ppendix I I I .

( S igned) A . J a n s s e n .

Appendix I.

Y IE L D OF A S S IG N E D E X C IS E D U T IE S

f o r T h i r d a n d F o u r t h Q u a r t e r s o f 1 9 2 7 , a n d F i r s t a n d S e c o n d Q u a r t e r s o f 1928.

1. VII. to 30. IX. 1927.

1. X. to 31. XII.1927.

1. I. to 31. III.1928.

1. IV. to 30. VI,1928.

Tobacco ........................................B e e r .................................................M a t c h e s ........................................Wines, brandy, liqueursY e a s t .................................................Cigarette-cases and paper

1,122,198.37 220.912.50

8,750.— 42,653.20

6,975.— 11,717.50

907,552.25 157.200.—

8.750.— 67,949.55 34,170.—

9,478.90

969,688.92189,375.—

8,797.5068,871.9017,148.7510,174.25

1,021.838.69 207.705 —

13,279.- 64,463.15

9,508.30

1,413,206.57 1.185,100.70 1.264,056.32 1.316,8*4.14

Remittances to London and New York.

F o r service of loan for second half of 1927 :

To London : £26,450.To New Y ork : $151,000.

representing equivalent of Ekr. 1.047.904.54.

F o r service of loan for firs t half of 1 9 2 8 :

To London : £26,400.To New Y o rk : $1 5 0 ,0 0 0 .

rep resen ting eq u iva len t of E kr . 1,039,977.11.

Appendix II.

[Translation.]

S T A T U T E SOF T H E N A T IO N A L M O R TG A G E B A N K OF E S T O N IA

(PIKALAENU PANK)

[State Advertiser , December 30th, 1927, No. 115.)

P A R T I.— G E N E R A L P R O V I S IO N S .

Article I .

The object of th e National Mortgage B an k of E s ton ia (hereinafter called “ the Bank ’’) is to grant aga inst th e pledge of im movable p ro p e r ty or ships, or o ther securities, long-term loans for E s ton ian agriculture, industry , sh ipping a n d buildings, to municipalities and other institu tions and enterprises, and to co-operative organisations.

By v irtue of th e provisions of these S ta tu tes , th e re shall be handed over to th e B ank :

(1) The loans and claims to be transferred to th e G overnm ent in conformity w ith Article 82 of the S ta tu te s of th e Eest i P an k ; and

(2) Three hun d red and fifty th o u san d pounds sterl ing ou t of the S ta te Foreign L oan of 1927.

Article 2.

The B ank has th e r igh ts of a juridical person. I t is liable w ith its assets for obligations incurred and for possible losses.

Article 3.

The seat of th e B ank shall be a t Tallinn, and its activities shall extend th ro u g h o u t the Republic. The B an k m a y open branches and agencies when so decided b y the Government.

Article 4.

The B ank shall have a seal bearing th e R epublican coat-of-arms, surrounded by the Bank’s style.

Article 5.

All com m unica tions addressed to the B ank, as well as correspondence rela ting to its activities, shall be ex em p t from s tam p du ty .

P A R T I I .— F U N P S O F T H E B A N K .

Article 6.

A sum of five million krones shall be a llo tted from the S ta te Foreign Loan of 1927 to Serve as th e capita l of the B ank. The B an k m ay utilise no t m ore th a n th ree million krones °f this capital for buying its own bonds and th e deben tu res p rov ided for in Article 61 (2) of these S ta tu tes , or for g ran ting loans, while tw o million krones m u s t be invested in public securities or those guaran teed b y th e Governm ent. T he losses of th e B ank, which canno t be covered out of th e reserve fund (Article 7), shall be m e t from th e capital.

Article 7.

The reserve fund, destined to provide for the in teres t on, and redem ption of, th e B ank s bonds and debentures , as well as to m ee t possible losses (if th e cu rren t receipts are insufficient *or that purpose), shall be bu ilt up from th e n e t profits of th e B ank until the fund am ounts0 not less th a n th e capital. The reserve fund shall be invested inviolably in public

securities or those g u a ran teed b y the G overnm ent.

_ 8 —

P A R T I I I .— B U S I N E S S OF T H E BANK.

1. G e n e r a l R e g u l a t i o n s .

Article 8.

The B an k m a y ca rry ou t the following transac tions :

(1) G ra n t long-term loans in cash or in its bonds or debentures,

(a ) Secured by m ortgages on im m ovable p ro p e r ty of an y kind, such asland, buildings, factories and works (Articles 10-33) ;

(b) Secured by m ortgages on ships (Article 34) ;(c) To self-governing bodies on th e security of a G overnm ent guarantee

(Article 40) ;

(2) G ra n t loans for fixed periods of six m o n th s to five years on miscellaneous securities (Article 35) ;

(3) Accept from th e G overnm en t or from other ins t i tu t ions or persons, for the ir own account, th e m an ag em en t and collection of funds, as well as of loans to, and o ther claims against, th i rd par ties ;

(4) Issue bonds in single series of a m a tu r i ty n o t over tw e n ty years or under five years, e i ther in krones or in foreign currency. T he m anner , to ta l amount, denom inations and dates of th e issue of th e bonds shall be fixed b y th e Board of Directors, whose resolutions are sub jec t to confirm ation b y th e Government ;

(5) Issue debentures in krones or in foreign currency ;(6) B uy or sell for its own accoun t public bonds or those guaranteed by the

G overnm en t or, w ith th e consent of th e Minister of Finance, bonds of Estonian credit in s t i tu t ions n o t so g u a ran teed ;

(7) U n d e r tak e th e sale of its bonds and debentures in th e open market for accoun t and b y order of borrowers, charging a commission to be fixed b y the Bank's B oard of D irectors ; and

(8) Carry o u t such o ther operations as m a y be necessary for th e successful t ransac t ion of its legit imate business.

Article 9.

The G overnm en t will issue general ins tructions to th e B an k regard ing th e ex ten t of certain classes of business, as well as th e scope of its operations b y branches of economic activity.

2. L o a n s s e c u r e d b y I m m o v a b l e P r o p e r t y .

Article 10.

The B an k gran ts loans of a m a tu r i ty n o t exceeding tw e n ty years secured by mortgages on real p ro p e r ty of a n y k ind s i tua ted w ith in th e boundar ies of the Republic, such as land, buildings, works and factories, if these can serve as a hy p o th ec a ry pledge according to the existing laws.

T he m ortgaged buildings and appur tenances m u s t be insured against fire c o n f o r m a b ly

to the provisions of P a r t IV of these S ta tu tes .

Article 11.

Loans m a y be g ran ted up to 50 per cen t of th e assessed value of the real p roperty to be pledged, w i th a m in im u m of E kr . 500, w hereby th e B a n k is given a prior mortgage on the p ro p e r ty as security. Debts, if any, encum bering th e real p ro p e r ty to be pledged shall be paid ou t of th e loan gran ted , or all th e creditors of th e borrow er shall p e rm it th e B ank to have p r io r i ty for its claims over th e debts inscribed in the ir nam e, so t h a t th e B a n k shall, in the even t of the calling-in of th e loan, enjoy, in an y case, prior r igh ts according to these Statutes.

Excep tions to this provision are p e rm it ted onlyr in th e case of S ta te and municipal taxes a n d o ther public burdens, as well as of irredeem able servitudes and burdens, whose value is de te rm ined b y th e B oard of D irectors— th e am o u n t of the loan being correspondingly reduced,

Article 12.

Real p ro p e r ty owned b y several co-proprietors shall be accepted as a pledge only as an indivisible whole and w ith th e consent of all th e owners.

9 —

Article 13.

When applying for a loan on th e pledge of real p roperty , th e borrower shall address himself in w ri t ing to th e B a n k ’s M anagem ent, subm itt ing :

(1) A copy of th e en try in th e Register of th e L an d R eg is tra t ion Office relating to the said real p ro p e r ty ;

(2) A certificate by the fire-insurance com pany, recording the valuation of the buildings insured, th e date of va lua tion and the insurance prem ium ;

(3) A deta iled p lan of th e land, buildings, works or factories, evidence as to the am o u n t of S ta te and m unicipal taxes, and inform ation regarding th e activities (of the undertak ing) in former years ; and

(4) A s ta te m e n t of th e required a m o u n t of th e loan.

Simultaneously, th e borrower shall pay a sum to m ee t th e p re lim inary expenses, according to a tariff fixed by th e Board of Directors and published in th e State Advertiser. If the applicant’s request is n o t g ran ted , half the a m o u n t will be refunded to him, b u t no t if he receives the loan or fails to take it.

Article 14.

Should the loan be sanctioned, the app lican t shall h an d to th e B an k a bond of indebtedness for the sanctioned am o u n t of th e loan, se t t ing for th t h a t :

(1) The p ro p e r ty to be m ortgaged an d its appur tenances rem ain as a pledge to the B an k for th e loan received, th e in teres t thereon, and all expenses in connection therewith , including fire-insurance prem ia ;

(2) H e is liable to th e Bank, in addit ion , w ith his whole p ro p e r ty up to the final p ay m e n t of th e loan received ; and

(3) H e unconditionally subm its to th e provisions of th e B a n k ’s S ta tu tes and th e lawful regula tions of th e M anagement.

He shall also p resent an insurance policy covering fire risks on his real p roperty and appurtenances, for an am o u n t fixed according to th e provisions of Article 68 of these Statutes.

Article 15.

When the loan is taken , the M anagem ent will send the bo rrow er’s bond of indebtedness to the local L an d R egis tra t ion Office for inscrip tion of the m ortgage rights and for due endorsement of the bond.

Article 16.

The borrower shall p ay to th e B an k for th e loan, half-yearly in advance, th e interest, th e amortisation in s ta lm e n t and an a m o u n t to cover th e B a n k ’s expenses a t th e ra te fixed by the Board of Directors— th e paym en ts being calculated, in th e first instance, from th e date of the granting of th e loan, and subsequen tly for a complete half-year. An initial charge not exceeding 1 per cent of th e loan is m ade to cover th e B a n k ’s expenses in connection with the valuation of th e p ro p e r ty and the pr in t ing of th e bonds.

The afore-mentioned sums are payable to th e B an k half-yearly in advance on or before ■June 30th and Decem ber 31st, in cash, in draw n bonds or in coupons due for paym ent.

Article 17.

If th e loan is g ran ted in bonds, th e borrower has the r igh t a t any t im e to repay it in whole or in part, in am oun ts equal to the smallest denom ination of a bond or multiples thereof. The repayment or par tia l redem ption is effected in bonds, w ith th e coupons and talons a ttached , hcase of full r e p a y m en t of th e loan.it- is permissible to p ay in cash any odd am ount, if this does ]i,-,t, exceed half the smallest denom ination of a bond ; otherwise, th e am o u n t shall be Paid with a bo n d — th e B ank refunding th e difference in cash. Loans g ran ted in cash m ay a t anY time be also repaid in cash.

Article 18.

If the deb to r does no t m ake his p aym en ts to the Bank, including insurance premium, on due date, th e B an k shall impose a fine a t the ra te of 1 per cent per mensem of the am o u n t1 Ue part of a m o n th being reckoned as a full m o n th ; if th e y are no t discharged within Ihree months, th e B an k shall proceed to collect th e am o u n t due, together with all expenses.

— 10 —

Article 19.

The B ank m a y ex tend the p a y m e n t of debts or o ther obligations only in case the borrower is in t e m p o ra ry difficulties owing to fire or o th er disaster. In such cases, and also in that of the dea th of th e owner of th e real p roperty , th e B oard of Directors m ay ex tend up to three years th e te rm of th e n ex t tw o p ay m e n ts due, div iding th em into equal half-yearly instalments and m a y reduce, or wholly remit, th e fine for t h e delay.

Article 20.

If the borrow er has not paid his dues during th e periods prescribed in Articles 18 and 70 of these S ta tu te s , and has no t applied for a prolongation, or if th e Board has refused his application, th e M anagem ent shall im m edia te ly proceed to collect th e loan, and for this purpose shall app ly to th e com p e ten t Court to have th e pledged real p ro p e r ty p u t up to public auction, s ta t in g th e am o u n t of th e claim and p resenting evidence that, th e real property is pledged to th e Bank. The Court will decide th e m a t t e r w i th o u t sum m oning the debtor, m ere ly on th e notice of th e B ank , an d will have th e real p ro p e r ty p u t up for sale in the manner laid down in Articles 1845 to 1888 of th e Civil P rocedure Code, tak in g into consideration th e special provisions of these S ta tu te s . If th e M anagem ent so requests, th e Court will also arrange for th e income from the real p ro p e r ty to be placed under d is t ra in t w i th o u t waiting for th e te rm prescribed in Article 1861 of th e Civil P rocedure Code.

T he provisions of th is and th e following articles do n o t res tr ic t th e B a n k ’s r igh t, according to th e general laws, to collect its loan also from a n y o ther real or m ovable property 4 the debtor.

Article 21.

If th e borrower is declared b a n k ru p t , or if th e o ther creditors dem and a public auction of th e real p ro p e r ty pledged to the Bank, th e co m p e te n t Court or bailiff shall notify the Bank accordingly. T he claims of th e B ank, secured b y m ortgages on real p roperty , are to be satisfied a p a r t from th e b a n k r u p tc y proceedings. The B an k m ust , previous to the d a te of sale, notify to th e com pe ten t Court its to ta l claim, as well as th e assessed value of th e p roperty to be sold. T he notice m u s t be accom panied by a certificate of th e L a n d R eg is t ra t ion Office that th e real p ro p e r ty to be sold b y auc t ion is pledged to th e B an k as securi ty for its loan.

Article 22.

O u t of th e proceeds of th e sale of the pledged p ro p e r ty there shall be paid, before satisfying th e B a n k ’s claims, th e wages and hea l th- insurance p aym en ts of th e w orkm en and servants, as provided for in Article 1890 of th e Civil P rocedure Code.

Article 23.

T he bailiff shall no t ify to the owner th e am o u n t of th e B a n k ’s claim an d th e application to hold a public auc tion. H e shall perform all acts prescribed in Articles 1095 an d 1849 of the Civil P rocedure Code w i th o u t w a it ing for th e te rm provided for b y the said articles- The a n n o u n cem en t regard ing th e public auction, and all o ther a r rangem en ts therefor, snail be m ad e w he ther there is a n v ag reem ent between the tw o parties regard ing th e t im e and manner of the auc t ion or not.

Article 24.

T he real p ro p e r ty to be sold b y auc tion shall be a t ta c h ed and valued by th e ba: onlvif so reques ted by th e M anagem ent of the Bank. T he M anagem ent has also th e r ig h t to demand th e seizure of the d e b to r ’s m ovable p rope rty , an d its sale s im ultaneously w ith his real property and its appur tenances .

Article 25.

T he public auc t ion shall be notified in th e Stale Advertiser a t least two m o n th s b e f o r e the appo in ted date . If no v a lu a t io n was m ad e u n d er Article 24, th e notice m u s t contain, besides

th e d a te requ ired by Article 1147 (1) to (3), (6) and (8), an d Article 1869 of th e Civil P r o c e d u r e

Code, also th e assessed value of the real p ro p e r ty on which the loan was gran ted .

— 11 —

Article 26.

The borrower has th e r igh t to pay his debt, including fine and expenses incurred by the Bank on his account, before th e com m encem ent of the auction, or if th is has no result, before the second auction, and th u s free th e p ro p e r ty from sale.

Article 27.

After receiving from th e bailiff th e notice regard ing the p u t t in g up of th e real property to public auction, th e M anagem ent of th e B a n k shall notify th e com pe ten t Court of any changes in the particulars m en tioned in Articles 20 and 21 of these S ta tu tes , or which m ay occur between the presen ta t ion of th e final account a n d the da te of the sale.

Article 28.

No m a t te r on whose dem and th e auc tion is held, th e b idding for th e real property pledged to th e B ank shall, a t th e first auction, always s ta r t , a t lowest, a t an a m o u n t calculated to cover the d eb t registered in favour of th e B ank, including all claims to da te for interest, insurance premia, fines, cour t fees, and expenses in connection with th e sale, as well as all State and municipal taxes and liabilities which have preference over th e registered debt of the Bank. A n y person desirous of t ak in g p a r t in the b idd ing m u s t deposit 10 per cent of the initial bid as security . If th e highest b idder fails to p a y th e purchase money, including legal fees, within th e t im e provided for in Article 1874 of th e Civil P rocedure Code, th e money deposited or collected shall be used, in th e m anner prescribed in Article 1890 of the Civil Procedure Code, in p a y m e n t of liabilities, cour t fees, an d expenses of sale which have preference over the B a n k ’s claim according to th e Civil Procedure Code, of o ther expenses incurred by the Bank on the accoun t of th e debtor, and in par t ia l r e p ay m en t of th e am o u n t due to the Bank.

Article 29.

Should th e first auc t ion yield no result, a second auc tion shall be held no t earlier th an one month thereafte r , which must, be specifically announced in th e Stale Advertiser a t least three weeks previously. If th e sale takes place on th e dem and of th e B ank, th e second auction must s ta r t a t an am o u n t covering a t least th e claims hav in g prior i ty to those of the B ank : otherwise, th e b idd ing m u s t s t a r t a t an am o u n t n o t less t h a n t h a t prov ided for in Article 1885 of the Civil P rocedure Code. Persons wishing to ta k e p a r t in this b idding m u s t pay in a deposit equal to t h a t a t th e first auction, and this is to be dealt w ith as prescribed for the said auction. A t th e second auc t ion the B ank m a y bid. b u t only up to an am o u n t covering its own claims and those hav ing priority there to . In any case, a t the second auction, the property put up for sale will be definitely assigned to th e h ighest bidder.

Article 30.

The buyer m u s t sett le th e B a n k ’s claim a t th e office of th e B an k w ith in fourteen days (if the price b id is no t less t h a n th e am o u n t fixed according to Article 28), unless the Management of th e B an k consents to t ransfer to his nam e th e whole or a p a r t of the debt encumbering th e real p roperty .

As evidence of th e se t t lem en t of the debt, th e B an k shall issue a special certificate to the buyer for p resen ta t ion to the Court. In th is certificate there shall be precisely stated the amounts transferred and paid, so t h a t th e Court m a y deduc t th em from th e purchase price.

Article 31.

If the claim of th e B an k is no t fully covered b y th e sale of th e real property, theManagement shall ta k e im m edia te steps to satisfy the claim from o ther p ro p e r ty of the debtor.

Article 32.

In case th e real p ro p e r ty pledged as securi ty comes in to th e possession of th e Bank (Article 29), th e M anagem ent shall endeavour to sell i t w i th o u t loss to the Bank, and in the meantime to ob ta in some income from the p roperty . I t s sale m u s t be effected no t iater th a n tw o years a f te r it. has been registered in th e n am e of th e Bank. This period may be extended in individual cases for a fu r th e r two years, w i th the approval of the Government on each occasion. The B ank m a y not keep such p roperty except in cases where it is ind ispensably necessary for the conduc t of th e business of th e Bank, and where the decision to keep it is tak e n in conform ity w ith Article 79 (3).

In case of purchase, th e B an k shall be ex e m p t from reg is tra tion fees and s tam p d u ty ifit sells the acquired p ro p e r ty w ith in two years of its being inscribed in the B ank 's name, or "within four years if the G overnm en t has extended th e period in accordance with the first Paragraph of th is Article (32).

— 12 —

Article 33.

Additional loans on real p roperty , a lready bu rdened up to th e limit prescribed in Article 11, m a y be g ran ted only in cases where, on a new assessment, th e value of the property and appur tenances has increased, or where a t least one-fifth of th e original am o u n t of the debt has been paid.

3 . L o a n s a g a i n s t P l e d g i n g o f S h i p s .

Article 34.

The B an k gran ts loans aga inst m ortgages of E s to n ian ships, effected in accordancew ith th e provisions of th e L aw for R eg is tra t ion of Ships.

In g ran tin g such loans, th e provisions of these S ta tu te s regard ing loans secured on real p ro p e r ty shall apply , w ith th e following m odifications and addit ions :

(1) The am o u n t of th e loan shall n o t exceed 50 per cen t of the assessed valuein the case of steel ships, and 40 per cen t in t h a t of wooden ships ;

(2) The d u ra t io n of th e loan shall n o t exceed fifteen y7ears for steel sh ips , and te n years for wooden ships ;

(3) T he pledged ship m u s t be insured against accident or loss, an d th e insurance policy or covering certificate h a n d e d over to th e Bank. The deb to r m ust notify th e B an k in case of dam age ; and

(4) W h en app ly ing for the loan, there shall be p resen ted a copy of the entry in th e R eg is tra t ion Office regard ing th e vessel, in fo rm ation as to its pr ice , and an y o ther docum ents specified by th e B o ard of Directors of th e Bank.

4 . L o a n s a g a i n s t V a r i o u s S e c u r i t i e s .

Article 3 5 .

The B an k m a y g ra n t f ixed-term loans (Article 8 (2)) aga inst th e following securities :

(1) F ixed in terest-bearing public securities or those g u a ran teed b y th e Government, or approved b y th e Minister of F inance as sufficiently secure, up to 8 0 per cent of the ir m a rk e t va lue ;

(2) Precious m eta ls and articles m ad e therefrom , up to 8 0 per cent of the value of th e m eta l ;

(3) Bills an d bonds of indebtedness secured b y goods, m ater ia ls , agricultural p la n t and o ther m ovables , up to 6 0 per cent of their value. Im aginab le divisions of m ovable property7 of co-owners ca n n o t be accepted as security ;

(4) Bills a n d bonds of indebtedness secured by7 m ortgages, p rovided these latter, toge ther w ith prior m ortgages, if any , do n o t b u rd en th e property7 concerned to an ex te n t greater th a n 5 0 per cent of its assessed va lue ;

(5) G uaran tees of such credit in s t i tu t io n s as are approved by the Minister of F inance ;

(6) Bonds of indebtedness of co-operative c red it ins t i tu t ions , which are secured by similar bonds signed by m em bers who have received loans from institutions and which are g u a ran teed by a t least tw o solvent persons, sub jec t to the proviso t h a t loans to ind iv idual m em bers shall n o t exceed tw o th o u san d krones, and those to m em ber co-operatives five th o u sa n d krones. T he co-operative credit institutions m ay , w ith th e permission of th e B ank , change th e bonds of indebtedness serving as security7, w hen necessary ; and

(7) Bills a n d bonds of indeb tedness bearing, besides the s ignature of the drawer, the endorsem ent or g u a ran tee -endorsem en t of a t least two solvent persons, p ro v id e d

t h a t no loan to any ind iv idual shall exceed two th o u san d krones.

Article 36.

The B an k m a y also g ra n t f ixed-term loans (Article 35). redeem able by instalm ents—the in te re s t on th e deb t being ca lcula ted for th e t im e th e m oney is actually7 a t th e disposal of the borrower.

— 13 —

Article 37.

The B ank m a y n o t g ran t loans on the miscellaneous securities enum era ted in Article 35 1) to (7) from its cap ita l or from funds transferred to it ou t of th e S ta te Foreign Loan of 1927.

Article 38.

The movables p ledged to th e B an k in conform ity w ith Article 35 (3) of these Statutes may remain in th e possession of th e deb to r to keep and to use ; changes in the component parts and value of th e m ovable p ro p e r ty m a y only be m ad e w ith th e consent of the Bank, In such cases, an an n o u n cem en t shall be inserted in th e State Advertiser, a t the expense of the debtor, regard ing th e pledges and the ir release, and a notice to t h a t effect pu t up in a conspicuous position w ith in the place or room where th e pledged p rope r ty is k ep t ; corresponding labels shall be affixed to ind iv idual objects, if possible, to ind icate t h a t th ey have been pledged".

Pledged m ovables in regard to which all th e above-m entioned formalities have been complied w ith are considered to be “ dead-pledges ” (Faustp fand), and these cannot be seized in satisfaction of claims of th i rd parties, nor can th ey form p a r t of th e b a n k ru p t 's estate, if the debtor is declared insolvent, before the B a n k ’s loan, including in teres t and o ther additional liabilities, is paid. The a l ienation of pledged m ovables and the pledging of them to other persons are void if th e objec ts were du ly labelled as such, or if th e alienation took place in a room or place where th e re la tive notice was p u t up.

A debtor, his p roxy or se rvan t who alienates or pledges, w i th o u t the permission of the Bank, the pledged p ro p e r ty left in th e possession of th e deb to r shall be punishable, as prescribed by law, for dispersing and appropr ia t ing property7 in t ru s t .

Article 39.

If th e value of the pledged p ro p e r ty diminishes, th e deb tor shall present additional securities for an equal am o u n t or repays a corresponding p a r t of th e loan. If th is is no t done, or if the loan or th e due p a r t of i t is no t paid a t date, th e B ank shall im mediately proceed to collect th e loan. To th is end th e B ank is entitled, a t its discretion, for th e purpose of the collection, e ither to sell th e pledged property7 or, if i t sees fit, to recover th e deb t from other property7 of th e debtor. B y th e adop tion of one course of action, the B an k does not lose the right to tak e th e o th er course later.

The sale of pledged m ovable p ro p e r ty shall be effected by order of th e Management without recourse to th e Court. P ro p e r ty which is n o t quoted on th e E xchange shall be sold by public auction, whereas goods so quoted m a y be sold by th e M anagem ent w ith o u t an auction, on the basis of th e quo ta t ion . If th e a m o u n t realised from th e sale is in excess of the claim of the Bank, th e surplus shall be credited to th e d e b to r ’s account.

fhe deb tor has no r ig h t to m ake claims aga inst th e B a n k for losses incurred owing to delay in selling th e pledged property7, or to th e B a n k ’s choice of da te and place of sale.

Article 40.

The B an k may7, on th e gu a ran tee of th e G overnm ent, g ra n t loans to self-governing bodies in debentures or o u t of th e proceeds of th e sam e (Article 61 (2)), for periods up to twenty years.

5 . A d m i n i s t r a t i o n o f F u n d s a n d L o a n s o n A c c o u n t o f t h e G o v e r n m e n t .

Article 41.

Loans and claims t ransferred from th e Eesti P a n k to th e G overnm ent, in conformity with Article 82 of th e Eest i P a n k S ta tu tes , shall be h anded over to th e B ank for administration, together w ith all securities and documents.

In dealing w ith th e loans and claims so handed over, th e B an k shall appear before th ird parties w ith all the r ights and obligations, in so far as they7 are no t modified by these S ta tutes, which belonged to, or m igh t belong to, th e Eesti Pank . and which arise out of these loans and claims as well as from th e securities behind th em and th e lease and other contracts connected therew ith .

The Eesti P a n k shall, where necessary, convey b y deed th e documents relating to the above loans and claims directly7 to th e nam e of th e Bank. The consent of the contracting parties—the debtors and th e guaran to rs— is no t required for th e transfer. The transfer deeds ajid endorsements are ex em p t from s tam p duty7,

— 14 —

Article 42.

The B a n k has th e r igh t to tak e over loans and claims from th e G overnm en t account to its own account, on the securities and in th e m an n e r prescribed b y these S ta tu tes , paying to th e G o v e rn m en t a corresponding sum in its deben tu res (Article 61 (1)) or in cash ; th e Bank m a y also g ra n t fresh loans aga inst au thorised securities, in clearance of th e Government account.

If th e Board of Directors of th e B an k considers a loan or claim to be adequa te ly secured, and th e business of th e borrow er to be in a sound condition, i t has th e r ig h t to decide to ta k e over th e loan or claim from th e G overnm ent account to t h a t of th e Bank, even if the existing securities and a n y sup p lem en ta ry ones which the borrower m a y be able to present, or the ra t io betw een the va lue of th e securities and th e am o u n t of th e loan, do not conform to th e provisions of these S ta tu te s . In such case, however, the B an k an d th e borrower must agree specifically as to th e d a te by which th e la t te r shall p resen t addit ional securities, in order t h a t th e ra tio prescribed b y these S ta tu te s , between th e value of th e securities and th e amount of th e debt, shall be established. If the deb to r does no t adhere to th e agreed date, the debt, or the p a r t of it. m u s t be collected.

Article 43.

If th e B an k does n o t find i t possible to tak e over on its own accoun t a par ticu lar loan or claim from th e G overnm en t account, or to g ran t a new loan in full se t t lem en t of t h a t of the G overnm ent, aga inst th e existing securities an d an y sup p lem en ta ry ones which the debtor m ay be able to present, he shall be given the oppo rtu n i ty , w ith in a t im e to be fixed b y the B ank , to propose a financial in s t i tu t ion w hich is p repared to ta k e over th e debt In such case, th e B a n k m ay , up o n th e re ques t of th e financial in s t i tu t ion ta k in g over th e loan, if i t considers the position of th e in s t i tu t ion to be satisfactory , g ran t i t a loan aga inst securities which com ply w ith the provisions of these S ta tu te s ; in case of need, th e B ank m a y allow the re laxat ions m en tioned in Article 42 in regard to th e securities. The re p ay m en t of the loan shall be effected, a t la test , w ith in tw e n ty years by annua l instalm ents.

Article 44.

Loans and claims n o t t a k e n over, b y the B a n k or b y o ther financial institu tions shall rem ain under the m an a g e m e n t of th e B an k for account of th e G overnm ent, toge ther w ith all securities.

T he B an k m u s t endeavour, in th e first place, to ascerta in w h e th e r th e enterprises to which th e said loans ap p e r ta in still possess v i ta l i ty . If it appears t h a t an en terprise cannot he so regarded— being o v e rbu rdened w ith debts or for some o ther reason— th e B ank shall be obliged to proceed im m edia te ly to l iqu ida te th e loan.

The l iqu ida tion shall be effected according to a fixed scheme, w ith a v iew to saving the S ta te from loss. . If i t is n o t possible to find a purchaser for th e p ro p e r ty of th e enterprise in l iquidation, th e B a n k m ay , w ith th e express permission of th e Governm ent, acquire the p ro p e r ty for th e t im e being on behalf of th e S ta te . I t will be th e d u ty of th e B ank to manage acquired properties, ta k in g care t h a t the ir value does n o t diminish, and, w ith th e consent of the G overnm ent, to sell th e m w hen a purchaser is forthcoming.

Article 45.

If th e B oard of Directors of th e B an k takes th e view t h a t th e difficulties of th e position of th e enterprise are of a t e m p o ra ry na tu re , th e B a n k m ay, w ith th e express permission of th e G overnm ent, defer th e l iqu ida t ion of th e loans or claims wholly or par tly .

The permission of th e G o v e rn m en t is to be given for no t more th a n one year, separately for each enterprise , and the G o v e rn m en t m ay , after consideration of th e B a n k ’s rep o r t regarding th e enterprise , renew th e permission, if necessary, for n o t m ore th a n one yea r each time.

If th e en terprise has n o t been able w ith in five years to develop to such an ex ten t th a t the B an k or some o ther financial in s t i tu t ion deems it possible to ta k e over th e loan or claim in question on its own account, and p ar t icu la r ly if th e enterprise is no t able to p ay th e interest on its d e b t regularly , th e B an k shall proceed to l iqu ida te th e loan or claim in th e manner set fo r th in th e preceding Article.

Article 46.

The m an a g em en t and sale of securities of loans or claims tak e n over for a d m i n i s t r a t i o n

on the s t ren g th of Article 41. and sums received from these securities, are subject I- the provisions of Articles 20 to 32, 69 an d 70 of these S ta tu te s .

Pledges of m ovab le p ro p e r ty serving as secu r i ty for loans tak e n over for management are sub jec t to Articles 38 and 39 of these S ta tu te s .

The B oard of D irectors of the B an k shall decide, on th e basis of th e general instructions of the G overnm en t , th e a r ran g em en ts for insuring th e pledges securing th e administered i>»ans aga inst fire and o th er dam age, as well as the conditions of th e loans and th e mann r of adm in is te r ing them .

The B a n k has th e r ig h t to p e rm it th e renewal an d exchange of existing securities agams ■ o thers of no t less th a n th e sam e value. The writing-off of irrecoverable debts and claims, as well as agreem ents w ith deb tors an d g u a ran to rs regard ing th e reduction of interest an principal for th e purposes of rehab il i ta t ion , shall be decided by th e B oard of D i r e c t o r s of t e B ank , sub jec t to conf irm ation by th e G overnm ent.

- 15 —

Article 47.

The Bank m a y p a y to the G overnm en t in its debentures (Article 61 (1)) th e sums received in payment of loans and claims ta k e n over for ad m in is t ra t ion in accordance with Article 41 of these S ta tu tes , to an am o u n t an d subject to such conditions as are fixed by th e Government.

Article 48.

On th e proposal of th e Minister of Finance, th e G overnm en t has th e r ig h t to hand over to the B ank for m an a g em en t o th er claims and funds of the S ta te , subject to conditions to be decided by th e G overnm ent.

Article 49.

In m anag ing th e loans and claims tak en over for adm in is t ra t ion , as well as th e corresponding securities, and in selling th e securities, th e B ank shall act in its own name, bu t for account of the Governm ent.

The B ank is n o t liable w ith its assets for these claims, and the accounts of th e transactions shall be k ep t separa te ly from those of o ther t ran sac t io n s of th e Bank.

The B an k will receive such rem unera t ion for th e m an a g e m en t of the loans, claims and funds tak e n over for adm in is t ra t ion , in accordance w ith th e preceding articles, as m ay be fixed by th e G overnm ent.

Article 50.

The B an k shall su b m it to th e G overnm en t an nua l ly a full report on each m anaged loan, on dates prescribed by th e G overnm ent.

6 . B o n d s a n d D e b e n t u r e s o f t h e B a n k .

Article 51.

The bonds issued by th e B a n k m u s t be fully secured b y m ortgage deeds on pledged real property (Articles 10, 11 and 14) and on ships (Article 34) of a t least th e same nominal value and the same ra te of in terest. If th e cover has diminished th ro u g h rep ay m en ts or for other reasons, and th e im m ed ia te w ithd raw al from circulation of a corresponding am o u n t of bonds is not feasible, th e B an k m u s t keep, ins tead of th e w a n tin g m ortgage deeds, a corresponding sum in cash or in th e bonds m en tioned in Article 8 (6).

W ith th e permission of th e G overnm en t th e B an k m a y tem pora ri ly , until mortgage deeds can be procured, issue bonds which are secured by either cash or the bonds m entioned in Article 8 (6).

The aggregate of bonds in circulation, and of th e deben tures m entioned in Article 61 of these S ta tu tes , shall no t exceed ten t imes th e to ta l of the capita l and reserve funds of the Bank.

Article 52.

The bonds are to be issued consecutively num bered , an d to bearer, w ith interest dates January 2nd an d J u ly 1st. On the dem and of holders, th e bonds m ay be registered in their names. Coupons an d bonds to bearer change h an d s by simple delivery, while, in the case of registered bonds, th e t ransfe r entries have to be m ad e b y the M anagem ent of th e Bank.

Article 53.

The ra te of in te res t of issued bonds can be changed only w ith th e assent of th e Minister of Finance— th e M anagem ent of the B an k public ly announcing, a t least six m onths before the conversion, t h a t th e holders of the bonds have to p resen t th e m to th e Bank on the date Mentioned in th e notice, and to s ta te w he the r th e y agree to exchange their bonds on the da te of conversion for bonds bearing a lower ra te of in terest, or w he ther th ey wish th e nominal amount of th e bonds to be paid to th e m in cash.

Article 54.

From th e da te m en tioned in th e announcem ent, the bonds shall cease to bear interest. T h e y shall be w i th d ra w n from circulation, cancelled and paid if presented with in ten years, after which d a te th e y will be regarded as lapsed and forfeited to the Bank.

— 16 —

Article 55.

The p a y m e n t of th e nom inal va lue of, and th e in teres t on, bonds is g u a ran teed by mortgages of the pledged real p ro p e r ty and ships, b y p ay m e n ts by th e debtors to w hom loans have been g ra n te d aga inst th e pledging of real p ro p e r ty an d ships, and, if these are n o t sufficient, then — rank ing equal w ith o ther liabilities of th e B a n k — b y th e whole of th e B a n k ’s assets.

The m ortgages of im m ovab le p ro p e r ty and ships pledged to th e B ank, which serve as securi ty for th e issued bonds, m a y be used to m ee t o th e r liabilities of th e B a n k only if all th e bonds are redeemed, or if th e sum requ ired for the ir p a y m e n t is set a p a r t in cash or in public securities or those g u a ran teed by th e G overnm ent.

Article 56.

The w ith d raw al of bonds from circulation, to be u n d e r ta k en by th e M anagem ent of the B ank , shall be effected once a y ea r in December, by drawings, and th e nom inal value of the d raw n bonds will be paid w ith in ten years, beg inning from th e following J u ly 1st, after which d a te th e bonds will be regarded as lapsed an d forfeited to th e B ank. The bonds drawn cease to bear in teres t from th e d a te fixed for the ir redem ption . T hey m u s t be presented for re p ay m en t w ith all coupons for th e preceding period a t ta c h e d — otherwise the value of the missing coupons will be deduc ted from th e am o u n t repaid.

Article 57.

The bonds, w i th a coupon-sheet for te n years and its renew al ta lon, shall be printed in th e form sanc tioned b y th e Minister of F inance , w hereon th e denom ination , rate of in teres t, d a te of issue an d p ro jec t of am o rt isa t io n are n o ted . T he bonds shall bear the s ignatures of th e P res iden t an d of two Managers, and will be bound in a book and cut out in consecutive order.

Article 58.

The B a n k shall redeem every year, by drawings, bonds of corresponding series of a nominal am o u n t equal to n o t less t h a n th e am ort isa t ion p a y m e n ts m ad e b y th e debtors and th e amounts of loans repa id before due date , and shall also cancel bonds acquired b y it. Bonds drawn for red em p tio n and cancellation will be paid b y th e B a n k on p resenta t ion .

Article 59.

The d raw ing an d des truc t ion of bonds shall t a k e place publicly, in th e presence of three rep resen ta t ives of th e B an k a n d one of th e M inistry of F inance.

Article 60.

A list of the nu m b ers of th e d raw n bonds shall be published in th e State Advertiser, m ention ing th e da te when in te res t p ay m e n ts will te rm ina te . These lists will also be procurable a t th e B ank.

Article 61.The B a n k h a s eth e r ig h t to issue deben tures :

(1) Of a m a tu r i t y up to Ju ly 1st, 1967, aga ins t th e port ion of th e Foreign L oan received b y th e B ank, less th e a m o u n t destined to serve as its cap ita l (Article 6). and also against th e loans and claims of th e Ees t i P a n k transfe rred b y th e G o v e r n m e n t

and ta k e n over b y th e B an k for its own account ; these deben tures are exem pt from s ta m p d u ty ;

(2) Of a m a tu r i ty u p to tw e n ty years, for th e g ran tin g of th e loans m e n t i o n e d

in Article 40 of these S ta tu te s an d for o ther t ran sac t io n s admissible b y t h e said S ta tu te s ;

(3) Of a m a tu r i ty up to five years, for th e g ra n t in g of th e loans mentioned in Article 35 ; th e am o u n t of th e last d eben tu res in c irculation is no t to exceed the total of th e capita l and reserve funds of th e B ank.

Article 62.

All th e deben tu res issued u n d er subsections (1) and (3) of th e preceding Article (61) n ru s t

be fully covered b y loans secured e i ther by m ortgages of real p ro p e r ty (Articles 10, 11 and 13) ,

or of ships (Article 34), or b y th e miscellaneous securities m en tioned in Article 35 of these Sta tu te s .

The debentures issued under sub-section (2) of Article 61 m u s t be fully covered by the o-uarantee of th e G overnm ent.

If the cover is reduced th ro u g h rep ay m en ts of l o a n s or for o ther reasons, a n d if the immediate w ithdraw al from circulation of a corresponding am o u n t of debentures is not feasible, the B a n k m u s t hold, in s tead of th e w an ting securities, a corresponding am o u n t of ca sh or of the bonds m entioned in Article 8 (6) of these S ta tu tes .

Article 63.

The in terest and am ort isa t ion charges on deben tures issued to th e G overnm ent in paym ent (Article 61 (1)) will be fixed a t th e sam e ra te , and will be payab le on th e same dates, as for the State Foreign L oan of 1927.

The G overnm ent is empowered to reduce th e above-m entioned ra te of interest if it deems this necessary in th e in te res t of th e economic life of th e co u n try — tak in g into consideration the position of th e m oney m arke t .

These deben tu res are subject to th e provisions of Articles 52 to 54, 56, and 58 to 60 of these S ta tu tes .

Article 64.

The due dates for th e coupons, th e procedure for am ortisa t ion and conversion, and other conditions apply ing to debentures issued on th e g u aran tee of th e G overnm ent (Article 61 (2)), are fixed a t th e t im e of issue by th e B oard of Directors of th e Bank, sub ject to confirmation by the Governm ent.

Article 65.

The shor t - te rm deben tures (Article 61 (3)) m a y be inscribed or to bearer, and with or without coupons. T he p a y m e n t of in terest, th e procedure for am ortisa t ion and conversion, and other conditions apply ing to these deben tu res are fixed a t th e t im e of issue by the Board of Directors of the B an k , su b jec t to conf irm ation by th e G overnm ent,

Article 66.

Persons guilty of forgery of bonds and debentures will be punished, as prescribed by law, for th e forging of m o n e ta ry tokens.

Article 67.

The bonds an d deben tu res of th e B ank m a y be accepted as security for all contracts concluded with, and obligations to, S ta te inst itu t ions . T hey m a y also be utilised for the investment of funds of orphans, trus tees , in s t i tu t ions of self-governing bodies and of societies.

P A R T IV.—C U S T O D Y OF P L E D G E D R E A L P R O P E R T Y A N D IN S U R A N C EOF P L E D G E S A G A I N S T I,OSS.

Article 68.

All real p ro p e r ty and appur tenances pledged to th e Bank, and o ther p roperty which m igh t be destroyed b y fire or o ther cause, m u s t be insured aga inst loss, in the B a n k ’s name, in insurance com panies regarded b y th e B ank as reliable. T h e insured am oun t m us t be at least 50 per cent h igher th a n th e B a n k ’s loan, or up to double the a m o u n t thereof, if the Board of Directors so decides. If th e borrower does n o t p resent a renewal receipt to the Bank at least fifteen days before th e expiry of th e policy, th e B an k will insure the pledged property lor account of th e borrower, who m u s t p ay th e cost n o t la ter th a n a t th e time the next payment is due on th e loan. Otherwise th e B an k will proceed to call in the whole loan.

Article 69.

The borrower m u s t always keep in good order th e real p ro p e r ty pledged to th e Bank, and must carry out, w ith in th e t im e fixed, such necessary repairs to buildings as are demanded by the M anagem ent or its representa tive . The borrower shall also produce evidence to show that th e insurance com pany is fully liable during th e repairs.

The B an k will supervise th e fulfilment of the requ irem ents mentioned in the previous paragraph, th ro u g h the Assessing Commission, which m u s t inspect the pledged property at least once a yrear and subm it a repo r t thereon.

— 18 —

Major rebuildings of pledged p ro p e r ty m ay only be u n d er ta k en with th e consent of the Bank ; otherwise th e B an k has the r igh t to prohibit th e m and to call in th e loan.

Article 70.

If i t appears t h a t th e value of the pledged p ro p e r ty has d iminished in comparison with th e v a lu a tio n a t th e t im e of g ran ting th e loan, th e M anagem ent of th e B ank m a y demand from th e borrower addit ional securities or m a y call in a p a r t of th e loan before its maturity, If the deb tor does not re p ay th e p a r t of th e loan dem anded by th e M anagem ent w ith in the t im e fixed, th e M anagem ent has th e r igh t to proceed to collect th e whole loan in the manner prov ided for in Article 20 of these S ta tu tes .

Article 71.

In case of fire or o th e r damage, th e insurance com pany will p ay th e B ank for the loss sus ta ined on p resen ta t ion of th e insurance policy.

Article 72.

If th e pledged p ro p e r ty is entirely destroyed, or if th e rem a in ing p a r t does not secure th e loan, th e whole debt, or a p a r t of it, will be covered by th e am o u n t received on th e insurance policy.

Article 73.

If th e p a r t of th e p ro p e r ty un to u ch e d by th e dam age fully covers th e loan of the Bank, and if i t "is im m edia te ly in sured aga inst dam age in conform ity w ith the provisions of Article 68. th e B an k m a y release to th e borrower-owner th e a m o u n t paid by th e insurance company.

Article 74.

If th e insurance co m p an y is n o t liable for th e damage, b y th e te rm s of its s ta tu tes and the conditions of the insurance policy, th e B an k m a y proceed to collect th e loan and to seii the pledged properties for th is purpose.

P A R T V.— A S S E S S M E N T OF P L E D G E D P R O P E R T Y .

Article 75.

T he v a lu a tio n of p ro p e r ty to be pledged to th e B an k shall be m ad e on th e basis of the d a ta supplied by th e owner, and in accordance w ith th e instruct ions for v a lua tion prepared b y th e M anagem ent of th e B an k an d sanc tioned by th e Board of Directors.

T he Assessing Commission, toge ther w ith experts called in to a t ten d , if necessary, shall inspect on th e spot th e p ro p e r ty to be pledged, com pare its v a lu a t io n w ith t h a t of the fire- insurance com pany , m ak e a n o te of th e differences and d raw up a full an d detailed description of the p ro p e r ty on th e form prescribed in th e instructions. This description will also serve as th e basis for fu tu re inspections.

Article 76.

At th e va lua tion , th e income from th e land, buildings, works, factories and ships shall in th e first place, be ta k e n into account, as set forth in th e annua l reports and other inform ation , and th e Assessing Commission will assess i t w ith th e help of th e ex p e r t s . In addition , th e realisation va lue of th e land, buildings, works, factories and ships, and other income which th e app lican t for th e loan receives or m igh t receive from th e real property, will be ta k e n into consideration.

Article 77.

The said inform ation , checked in th e afore-inentioned m anner , toge ther w ith th e full descrip tion p rep a red as laid down in th e instruct ions, th e va lua tion , and th e resolution of the Assessing Commission, shall be su b m itted to th e M anagem ent of th e B ank , which will lay them before th e Board of Directors , w ith i ts own opinion, for approval . T he la t te r m ay decrease the assessed value , re fer it back for r e v a lu a t io n or refuse t o g ra n t th e loan, b u t i t m a y m no c ircum stances increase th e assessed value contrary7 to the reso lu t ion of th e Assessing Commission.

19 —

P A R T VIy»=—M A N A G E M E N T OF T H E B U S IN E S S OF T H E BA N K .

Article 78.

The B ank shall be subject to th e G overnm ent, th ro u g h th e Minister of Finance. The treneral m an ag em en t of th e affairs of th e B an k is in th e hands of th e B oard of Directors, consisting of th e P res iden t , no m in a ted by th e G overnm ent for a period of five years, his Deputy, and seven o ther Directors, no m in a ted by th e G overnm ent for th ree years on the proposal of th e Minister of Finance. If a D irector retires before his time, a new one shall be appointed in th e same m anner to fill his place for th e rem a inder of his te rm of office. During the first two years, th ree Directors, chosen by lot. shall re tire every year, after which the Directors shall re tire in accordance w ith th e ir length of service. Betir ing Directors m ay be renominated.

The Directors are responsible for th e perform ance of their duties in like m anner to S ta te officials. T hey receive no salary, pension or subsistence m oney. Their daily allowances, and the travelling expenses connected w ith th e perform ance of the ir duties, as well as remuneration for a t ten d a n ce a t Board meetings, shall be fixed by the. G overnm ent on the proposal of th e Minister of F inance.

Article 79.

A quorum of th e B oard of Directors shall be const i tu ted when not less th a n five Directors and the P res iden t or his D ep u ty are present. Decisions will be ad op ted by a simple majority of votes. In case of equa l i ty of votes, th e P res iden t shall have a casting one. If the President disagrees w ith a n y resolution, he has th e r ig h t to suspend its operat ion and submit it for decision to th e G overnm en t th ro u g h the Minister of Finance.