Report as of September 30, 2009 - centrotherm.de & Wafer Solar cell & Module ... (23% by 2020)...

37

Report as of September 30, 2009 November 11, 2009 Silicon & Wafer Solar Cell & Module Thin Film Semiconductor

Transcript of Report as of September 30, 2009 - centrotherm.de & Wafer Solar cell & Module ... (23% by 2020)...

Silicon & Wafer

Solar cell & Module

Thin film module

Semiconductor

Report as of September 30, 2009November 11, 2009

Silicon & Wafer

Solar Cell & Module

Thin Film

Semiconductor

2© centrotherm photov oltaics AG Report as of September 30, 2009

Disclaimer

We have exercised utmost care in the preparation of this presentation. It contains

forecasts and/or information relating to forecasts. Forecasts are based on facts,

expectations, and/or past figures. As with all forward-looking statements, forecasts are

connected with known and unknown uncertainties, which may mean the actual result

deviates significantly from the forecast. Forecasts prepared by third parties, or data or

evaluations used by third parties and mentioned in this communication, may be

inappropriate, incomplete, or falsified. We cannot assess whether information,

evaluations, or forecasts made by third parties are appropriate, complete, and not

misleading. To the extent that information in this presentation has been taken from third

parties, or these provide the basis of our own evaluations, such use is made known in this

report. As a result of the above-mentioned circumstances, we can provide no warranty

regarding the correctness, completeness, and up-to-date nature of information taken, and

declared as being taken, from third parties, as well as for forward-looking statements,

irrespective of whether these derive from third parties or ourselves.

Rounding differences may arise.

3© centrotherm photov oltaics AG Report as of September 30, 2009

Contents

2. Highlights

3. Financial Results

4. Outlook

5. Appendix

1. centrotherm photovoltaics at a Glance

4© centrotherm photov oltaics AG Report as of September 30, 2009

centrotherm photovoltaics at a Glance

Silicon & Wafer Solar cell & Module Thin film

� Technology and equipment supplier for PV industry

� Market-leading player of turnkey crystalline solar cell production lines

� Competitive advantages:

� Leading in technology

� Unique offering over full PV value chain

� Lowest cost of ownership solutions

Technology &

Equipment

Key Figures 2007 2008

Employees: 178 1,050

Sales: € 166 million € 375 million

EBIT: € 21 million € 43 million

Business

Divisions

Semiconductor &

Microelectronics

Turnkey Production Plants - Turnkey Lines - Key Equipment - Services

5© centrotherm photov oltaics AG Report as of September 30, 2009

PV Markets

USA:

� Biggest mid-term PV market

potential

� Strong support of renewable energy and PV market & industry

by President Obama

Germany:

� Biggest PV market 2009 >2GW

� New government will keep EEG

and further support PV� Most established PV market

India:

� 20GW installation till 2020� Strong PV support by

government

� Huge emerging PV market

China:

� Biggest PV production

� Strong PV subsidy programs

(Golden Sun, Solar Roofs Program,…)

� 2 GW PV installation till 2011

Japan:

� Longest PV market history

� New PV roof-top program

France:

� Strong support of BIPV (highest PV subsidies with 0.60 €/kWh)

� Further support of renewable

energy generation (23% by 2020)

Spain:

� Biggest market 2008 with 2.5 GW

� Introduction of 500 MW cap has

reduced global PV-market

significantly, but good long term outlook and established PV-

market

Italy:

� Potential of fast growing PV

market (strong public support)

� More governmental support and

less bureaucracy for PV approval needed

6© centrotherm photov oltaics AG Report as of September 30, 2009

Strategy 2010+ - Silicon & Wafer

� Silicon prices stabilizing -> Target production costs: < 20 €/kg by end 2011

� CTN assumption: Future demand coming from countries with new subsidy PV programs -> They will install polysilicon production (e.g. Ukraine)

� centrotherm photovoltaics has aligned product portfolio to new Chinese polysiliconmanufacturer requirements

� Expansion investments as future growth driver

� Focus on sustainable products and technology (e.g. VGR)

� Focus on expansion business by cost reduction of 10-20%:

� Extended basic engineering concept

� Single equipment with highest performance parameters

� Fully integrated factory

� Upgrade of existing facilities

Market Trends

Product / Technology Strategy

7© centrotherm photov oltaics AG Report as of September 30, 2009

Strategic Focus: Cost Reduction and Sustainability

Polysilicon Ingoting Wafering

Interface Optimization

~ 12…..15 %

Interface Optimization

~ 5…..10 %

Saving potential

OpEx (€/kg)

Scope of

performance

TCS synthesis unitReactor & Converter

Vent gas recovery

Crystallization

furnaceWire saw

Up to 30%

(relative)

in process section saving

Saving

potential ~ 40-50% in

3-5 years

~ 20 % ~ 10 %

8© centrotherm photov oltaics AG Report as of September 30, 2009

Market Focus: Chinese Polysilicon Regulations

� Output more than 3.000 t/a yes

� Limited area / factory site <6ha/kt yes (Basic engineering)

yes, modified reactor

� Vent gas recovery ratio: yes

Efficiency of the total recovery system

� 98,5% (SiCl4)

� 99% (HCl, H2)

New Chinese requirements for polysilicon projects centrotherm Technology / Equipment

� Maximal power consumption for solar grade deposition < 60 kWh/kg

9© centrotherm photov oltaics AG Report as of September 30, 2009

Strategy 2010+ - Solar Cell & Module

� Increasing investments in solar parks

� Increasing capacity utilization rates of solar cell & wafer producers

� First signs of price stabilization

� Increasing demand since exhibition in Hamburg in September 2009

� centrotherm photovoltaics working at full capacity until spring 2010

� Shorter order cycles

� Focus on highest efficiency

� Selective emitter technology

� Direct plasma process

� Focus on De-Engineering (“Minimal concept”)

� Interdependency between solar cell & module

� Module technology with customized modules

� M&A analysis on wet chemistry & automation equipment (Europe, Asia, USA)

Market Trends

Product / Technology Strategy

10© centrotherm photov oltaics AG Report as of September 30, 2009

- Guaranteed performance parameters like in all centrotherm turnkey

factories (Yield, throughput, certified module, project schedule)

- Guaranteed, very competitive module power, in combination with FlexLine + cell technology (Selective emitter)

- Cell structure and process flow optimized for high module power

- Low CoO, e.g. by optimization of consumables (Pastes, etc.)

Integrated Solar Cell & Module Approach

Integrated solar cell and module factory

11© centrotherm photov oltaics AG Report as of September 30, 2009

Strategy 2010+ - Thin film

� Future demand for thin film modules coming from solar parks and buildings

� Thin film technology under price pressure

� Only high efficiency thin film is competitive on the market

� Focus on sustainable products and technology

� Focus on highest efficiency -> CIGS with highest potential

� In general production costs must come below level

of solar cell module production costs

Market Trends

Product / Technology Strategy

12© centrotherm photov oltaics AG Report as of September 30, 2009

Contents

2. Highlights

3. Financial Results

4. Outlook

5. Appendix

1. centrotherm photovoltaics at a Glance

13© centrotherm photov oltaics AG Report as of September 30, 2009

Highlights

Continuing sales and earnings growth

� Sales: € 374.7 million (+ 58.1%)

� EBITDA: € 50.7 million (+62.3%)

� EBIT: € 35.5 million (+16.8%)

New offices in Blaubeuren are near completion

Shanghai – Registered office of third Asian sales & service company

14© centrotherm photov oltaics AG Report as of September 30, 2009

Crystallization furnace

Product Updates

New version of crystallization

furnace

� Higher performance output

(7.5 MWp per year)

� Shorter process cycles

(average: ~56 hours)

� Substantial less process

variations

POCl3Diffusion furnace Thin film module from own R&D production line

New generation of tube furnaces for

diffusion and oxidation

� 25% greater capacity

� Simplified automation

� More streamlined design

New Turnkey-Line FlexLine Plus with

patented selective emitter technology

Efficiencies:

� Mono-Si:18%

� Multi-Si: 16.6%

Silicon & Wafer Solar cell & Module Thin film

Achievement of 13% efficiency

at pilot line

� Patented production

process translates to

competitive advantages

� Pilot line enables efficient

technology transfer to

production

� Efficiencies of up to 12% for

turnkey lines expected

15© centrotherm photov oltaics AG Report as of September 30, 2009

Research and Development

Research and development expenses 9M 2009: € 19.4 million R&D ratio: 5.2%

Intensifying our R&D activities in Constance

Silicon & Wafer Solar cell & Module Thin film

R&D Expenses:

R&D Activities:

€ 6.1 million € 7.8 million(including semiconductors of € 0.4 million)

€ 5.5 million

� Further productivity

improvements of

crystallization furnace

� Design of new CVD

reactors and high pressure converter completed

� FlexLine Plus with

selective emitter front side

technology shows efficiency of >18%

� Development of new back side technology started

� Development of CVD

equipment with higher

throughput

� Development of new

analytics “in situ XRD”

� Efficient process transfer

from pilot line to production

line

� Cell efficiency of 13% realized in laboratory

16© centrotherm photov oltaics AG Report as of September 30, 2009

Project Status - Abstract (1)

Silicon & Wafer:

Delivery completed

Preparation of installationChinaConfidential

Move in / EquipmentTaiwanTaiwan Polysilicon

Corporation

Ramp-upChinaShaanxi

Project executed (FAT)ChinaAsia Silicon

Preparation of deliveryChinaConfidential

Preparation of deliveryUkraineConfidential

Preparation of deliveryChinaConfidential

StatusCountryProject

17© centrotherm photov oltaics AG Report as of September 30, 2009

Project Status - Abstract (2)

Hyundai Heavy Industries Co., Ltd. in South Korea

Solar cell & Module:

� Solar cell turnkey production plant up and running

� Capacity: 250 MW

� Enabling industrial entry into photovoltaics market

Thin film:

� Commissioning of first CIGS turnkey production

line at Asian customer in progress

� New CIGS module manufacturing process

established

� “First Module Out” expected by the end of 2009Sunshine PV in Taiwan

18© centrotherm photov oltaics AG Report as of September 30, 2009

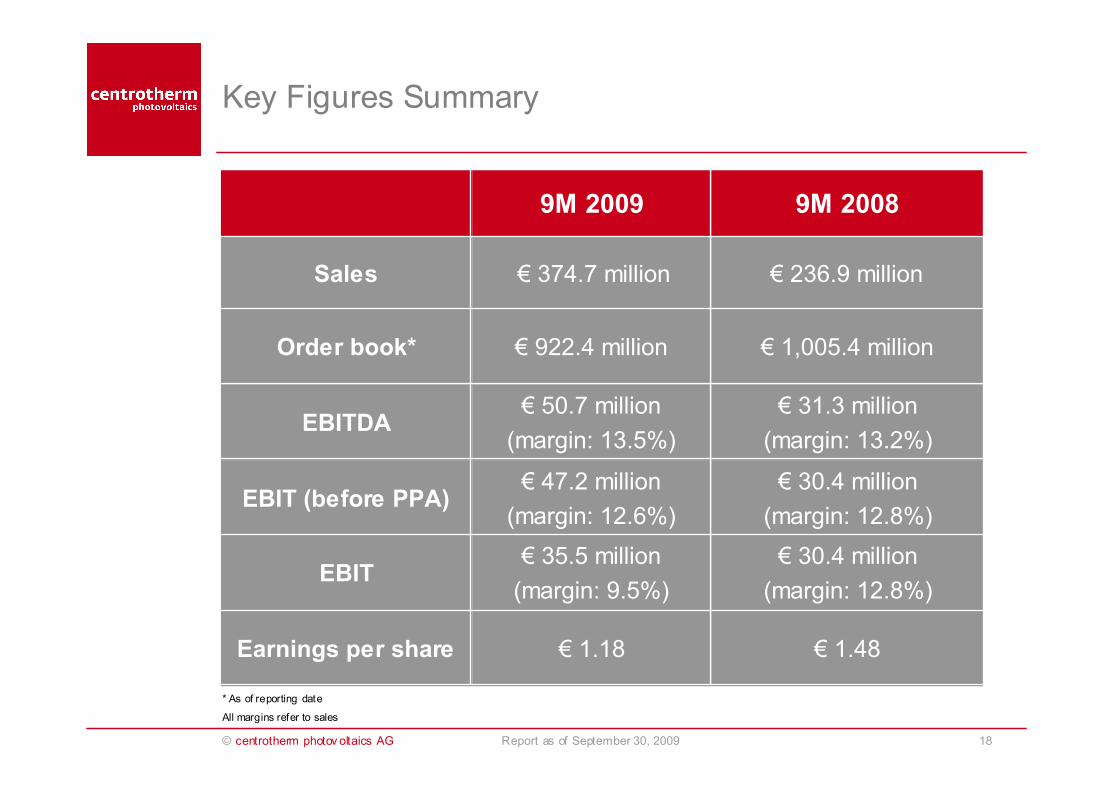

Key Figures Summary

€ 30.4 million

(margin: 12.8%)

€ 47.2 million

(margin: 12.6%)EBIT (before PPA)

€ 31.3 million

(margin: 13.2%)

€ 50.7 million

(margin: 13.5%)EBITDA

€ 1.48€ 1.18Earnings per share

€ 30.4 million

(margin: 12.8%)

€ 35.5 million

(margin: 9.5%)EBIT

€ 1,005.4 million€ 922.4 millionOrder book*

€ 236.9 million€ 374.7 millionSales

9M 20089M 2009

* As of reporting date

All margins refer to sales

19© centrotherm photov oltaics AG Report as of September 30, 2009

Contents

2. Highlights

3. Financial Results

4. Outlook

5. Appendix

1. centrotherm photovoltaics at a Glance

20© centrotherm photov oltaics AG Report as of September 30, 2009

Update on Order Book as of September 30, 2009

1,005 990

1,256

1,010922

0

200

400

600

800

1,000

1,200

1,400

Development of Order Book

in m

illion €

Order book contains:

� Silicon & Wafer: 8 orders

(capacity: 21,700 tonnes)

� Solar cell & Module: 22 turnkey lines

(capacity: 905 MWp)

� Thin film: 2 turnkey lines

(capacity: 80 MWp)

09/08 12/08 03/09 06/09 09/09

Split by Business Segments

Order intake Q3 2009: € 41.2 million, thereof:

� Solar cell & Module: € 28.9 million

� Silicon & Wafer: € 6.6 million

� Thin film: € 5.7 million

Total:

€ 922 million

Silicon & Wafer:€ 661 million (71.6%)

Thin film:

€ 92 million (10.0%) Solar cell & Module:

€ 169 million (18.4%)

21© centrotherm photov oltaics AG Report as of September 30, 2009

Stability of Order Book as of September 30, 2009

Split by Project Classification

A-projects: Orders under transaction

B-projects: Secured by prepayments / LC‘s

C-projects: Firm orders

Total:

€ 922 million

B-projects

€ 95 million

A-projects

€ 455 million

C-projects

€ 372 million

13

59

61

7972

370

36

232

0

100

200

300

400

500

600

700

Solar cell Thin film Silicon

C-projects

B-projects

A-projects

169

661

92

Split by Project Classification Per Segment

in m

illion €

Solar cell &

Module

Thin film Silicon &

Wafer

22© centrotherm photov oltaics AG Report as of September 30, 2009

Sales and Total Output

133.1

110.596.8

72.567.7

131.0

0

40

80

120

160

200

Q1 Q2 Q3

236.9

374.7

0

50

100

150

200

250

300

350

400

450

9M 2008 9M 2009

397.0

243.7

0

50

100

150

200

250

300

350

400

450

9M 2008 9M 2009

Sales

+58.1%

in m

illion €

Total Output

+ 62.9%

2008 2009

136.8 134.5125.7

97.6

78.168.0

0

40

80

120

160

200

Q1 Q2 Q3

2008 2009

in m

illion €

in m

illion €

in m

illion €

+28.8%

+14.2%

23© centrotherm photov oltaics AG Report as of September 30, 2009

Sales Breakdown by Region

Asia

301.8 (80.5%)

Germany

31.6 (8.4%)

Rest of Europe

24.4 (6.5%)

Rest of World

16.9 (4.6%)

Total:

374.7

in mill ion €

Export Quota: 91.6%

Asia

98.4 (89.0%)

Germany

3.1 (2.8%)

Rest of Europe

3.0 (2.7%)

Rest of World

6.0 (5.5%)

Total:

110.5

in mill ion €

Export Quota: 97.2%

9M 2009 Q3 2009

Trend: Increasing share of Asian market

24© centrotherm photov oltaics AG Report as of September 30, 2009

Sales Breakdown by Product

9M 2009

Turnkey Production

Lines

169.1 (45.1%)Single

Equipment

172.3 (46.0%)

Service & Replacement

15.7 (4.2%)

Other

2.7 (0.7%)

Total:

374.7

Consulting & Engineering

14.9 (4.0%)

Q3 2009

Turnkey Production

Lines

54.3 (49.1%)

Single Equipment

46.5 (42.1%)

Service & Replacement

6.0 (5.4%)

Other

0.4 (0.4%)

Total:

110.5

Consulting & Engineering

3.3 (3.0%)

in mill ion € in mill ion €

25© centrotherm photov oltaics AG Report as of September 30, 2009

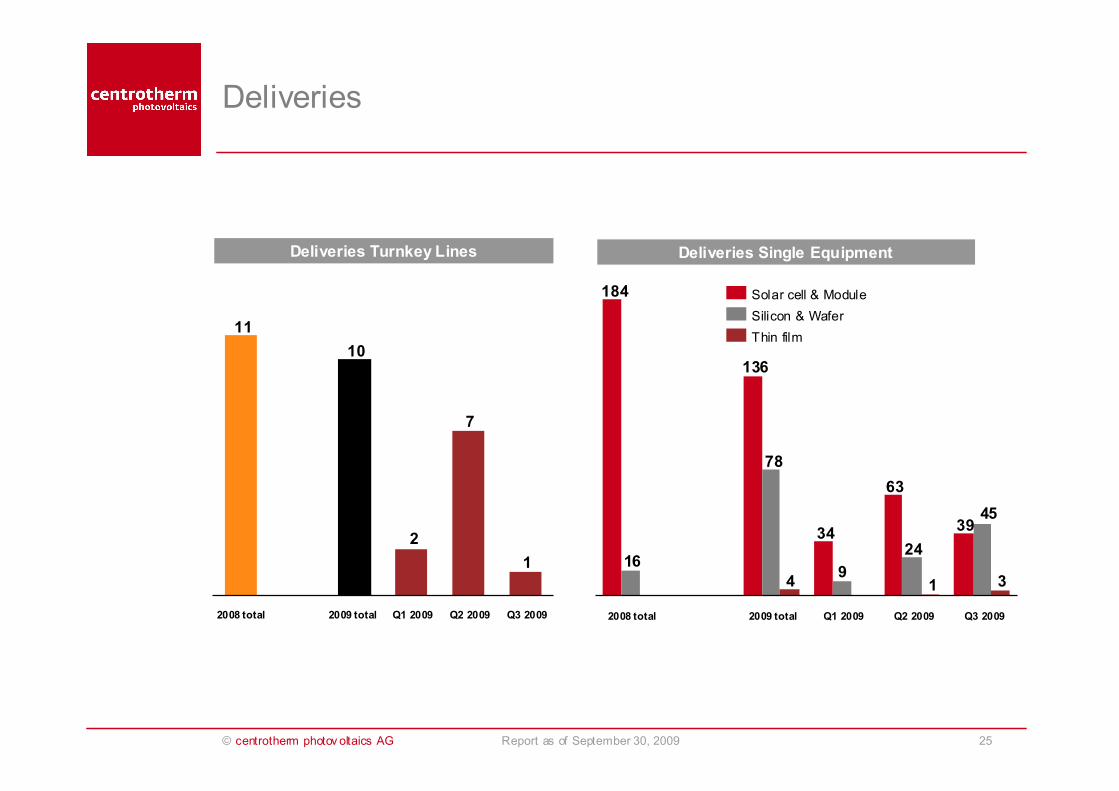

Deliveries

Deliveries Turnkey Lines Deliveries Single Equipment

1

7

2

10

11

Q3 2009Q2 2009Q1 20092008 total

39

63

34

136

184

45

24

9

78

16

314

Q3 2009Q2 2009Q1 20092009 total2008 total

Silicon & Wafer

Solar cell & Module

Thin film

2009 total

26© centrotherm photov oltaics AG Report as of September 30, 2009

Material and Personnel Expenses

88.9 86.578.6

49.6

73.4

59.6

0

20

40

60

80

100

Q1 Q2 Q3

182.6

254.0

67.8%

77.1%

0

40

80

120

160

200

240

280

9M 2008 9M 2009

0%

20%

40%

60%

80%

15.5

46.0

12.3%

6.6%

0

10

20

30

40

50

60

70

80

9M 2008 9M 2009

0%

2%

4%

6%

8%

10%

12%

14%

* referring to sales

Material Expensesin m

illion €

material expensesratio*

Personnel Expenses

14.516.1

15.3

3.9

6.55.1

0

4

8

12

16

20

Q1 Q2 Q3

personnel expenses ratio*

in m

illion €

in m

illion €

in m

illion €

2008 2009

2008 2009

27© centrotherm photov oltaics AG Report as of September 30, 2009

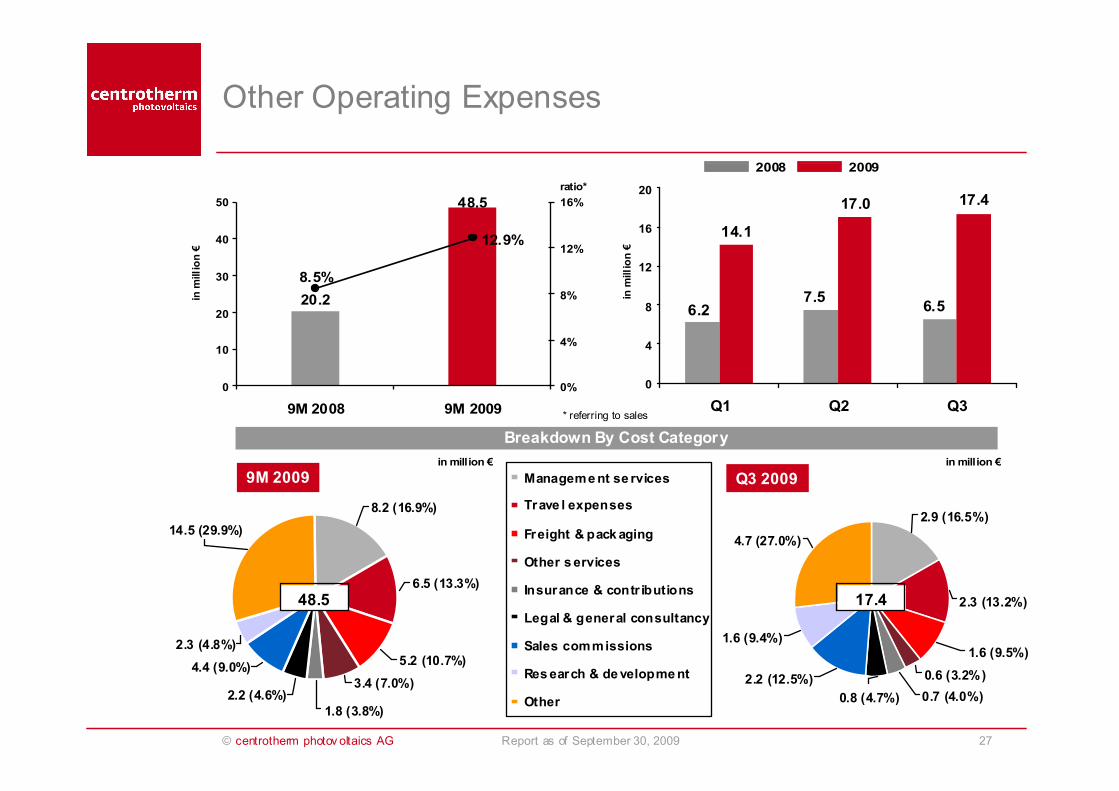

Other Operating Expenses

20.2

48.5

12.9%

8.5%

0

10

20

30

40

50

9M 2008 9M 2009

0%

4%

8%

12%

16%

14.1

17.0 17.4

7.56.56.2

0

4

8

12

16

20

Q1 Q2 Q3* referring to sales

Breakdown By Cost Category

ratio*in m

illion €

in m

illion €

2008 2009

8.2 (16.9%)

6.5 (13.3%)

5.2 (10.7%)

3.4 (7.0%)

14.5 (29.9%)

2.3 (4.8%)

4.4 (9.0%)

2.2 (4.6%)

1.8 (3.8%)

Management se rvices

Trave l expenses

Freight & packaging

Other services

Insurance & contr ibutions

Legal & general consultancy

Sales commissions

Research & development

Other

9M 2009 Q3 2009

2.9 (16.5%)

0.8 (4.7%)

0.6 (3.2%)

2.3 (13.2%)

1.6 (9.5%)

0.7 (4.0%)

2.2 (12.5%)

1.6 (9.4%)

4.7 (27.0%)

48.5

in million €in million €

17.4

28© centrotherm photov oltaics AG Report as of September 30, 2009

EBITDA and EBIT

31.3

50.7

13.5%13.2%

0

10

20

30

40

50

60

9M 2008 9M 2009

0%

4%

8%

12%

16%

20%

19.5

16.2 15.0

8.7

12.510.1

-2

2

6

10

14

18

22

26

30

Q1 Q2 Q3

EBITDAin m

illion €

in m

illion €

EBIT m

argin

Margins refer to sales

* before purchase price allocations

2008 2009

30.4

35.5

9.5%

12.8%

0

10

20

30

40

50

9M 2008 9M 2009

0%

2%

4%

6%

8%

10%

12%

14%

14.7

11.19.7

8.5

12.0

9.9

0

4

8

12

16

20

Q1 Q2 Q3

EBIT

in m

illion €

in m

illion €

EBIT m

argin

12.6%*

2008 2009

8.8%

13.5%12.9%

12.4%

29© centrotherm photov oltaics AG Report as of September 30, 2009

Consolidated Net Income

Consolidated Net Income and Earnings Per Share

25.023.7

6.7%

10.0%

0

5

10

15

20

25

30

35

40

9M 2008 9M 2009

0%

2%

4%

6%

8%

10%

12%

10.5

7.3 7.26.2

9.28.4

0

4

8

12

16

Q1 Q2 Q3

in m

illion €

in m

illion €

net income margin

Margin refers to sales

2008 2009

1.48

1.18

0.0

0.4

0.8

1.2

1.6

9M 2008 9M 2009

Earnings Per Share

in €

in €

2008 2009

0.50

0.34

0.520.57

0.390.34

0.0

0.2

0.4

0.6

0.8

1.0

Q1 Q2 Q3

9.5%6.5%

30© centrotherm photov oltaics AG Report as of September 30, 2009

Segmental Information (in Million €)

18.0 12.8

136.3

0

20

40

60

80

100

120

140

160

Sales EBITDA EBIT

2.9

48.0

-1.1

-10

0

10

20

30

40

50

Sales EBITDA EBIT

9.2 7.5

56.5

0

10

20

30

40

50

60

Sales EBITDA EBIT

Silicon & Wafer Solar cell & Module* Thin film

1.8

21.2

-10

-5

0

5

10

15

20

25

Sales EBITDA EBIT

2.20.5

32.9

0

10

20

30

40

Sales EBITDA EBIT

29.9 23.9

190.4

0

40

80

120

160

200

Sales EBITDA EBIT

Margin refers to sales

* Including other

3.5

13.2% 13.2%9.4%

16.4% 13.3%

15.7% 12.5%

6.7% 1.4%16.6% 8.4%

6.0% -2.3%

9M 2009 9M 2009 9M 2009

Q3 2009 Q3 2009 Q3 2009

31© centrotherm photov oltaics AG Report as of September 30, 2009

Balance Sheet

� Equity Ratio: 44.2%

� Liquidity: € 165.2 million

776.7

Total Assets

776.7

Total Equity and Liabilities

296.3

Non-current Assets

ther eof:

Securities

88 .0

343.2

Equity

370.9

Current Liabilities

62.6

Non-current Liabilities480.4

Current Assets

thereof:

Advanced payments

received

162 .3

Balance Sheet as of September 30, 2009 Balance Sheet as of December 31, 2008

665.8

Total Assets

665.8

Total Equity and Liabilities

273.0

Non-current Assets

thereof:

Securities

93.9

318.2

Equity

278.8

Current Liabilities

68.8

Non-current Liabilities392.7

Current Assets

thereof:

Advanced payments

received

158.9

32© centrotherm photov oltaics AG Report as of September 30, 2009

Cash Flow

33.2 35.8

-5.0

68.7

-20

0

20

40

60

80

100

120

-9.7

-3.7

-12

-10

-8

-6

-4

-2

0

Total Cash Flow

101.9

Cash Flow from Operating Activities

30.8

-105.6

-40.6

-120

-100

-80

-60

-40

-20

0

Cash Flow from Investment Activities

9M 2008

0.00.00

20

40

60

80

100

120

140

9M 2008 9M 2009

Cash Flow from Financing Activities

9M 2009NWC = Changes in Net Wor king Capital

EBT = Earnings Befor e Taxes

9M 20099M 2008

in m

illion €

In m

illion €

in m

illion €

in m

illion €

9M 2008 9M 2009

33© centrotherm photov oltaics AG Report as of September 30, 2009

Contents

2. Highlights

3. Financial Results

4. Outlook

5. Appendix

1. centrotherm photovoltaics at a Glance

34© centrotherm photov oltaics AG Report as of September 30, 2009

Outlook 2009 and Objectives 2010

2009 Outlook - confirmed

� Double-digit growth

� Sales: EUR 500 - 550 million

� Further increase in EBITDA

Objectives 2010

� Gaining further market shares

� Market launch of new, innovative products

� Strong focus on R&D activities

� Intensifying “Performance Plus”- Program

35© centrotherm photov oltaics AG Report as of September 30, 2009

Contents

2. Highlights

3. Financial Results

4. Outlook

5. Appendix

1. centrotherm photovoltaics at a Glance

36© centrotherm photov oltaics AG Report as of September 30, 2009

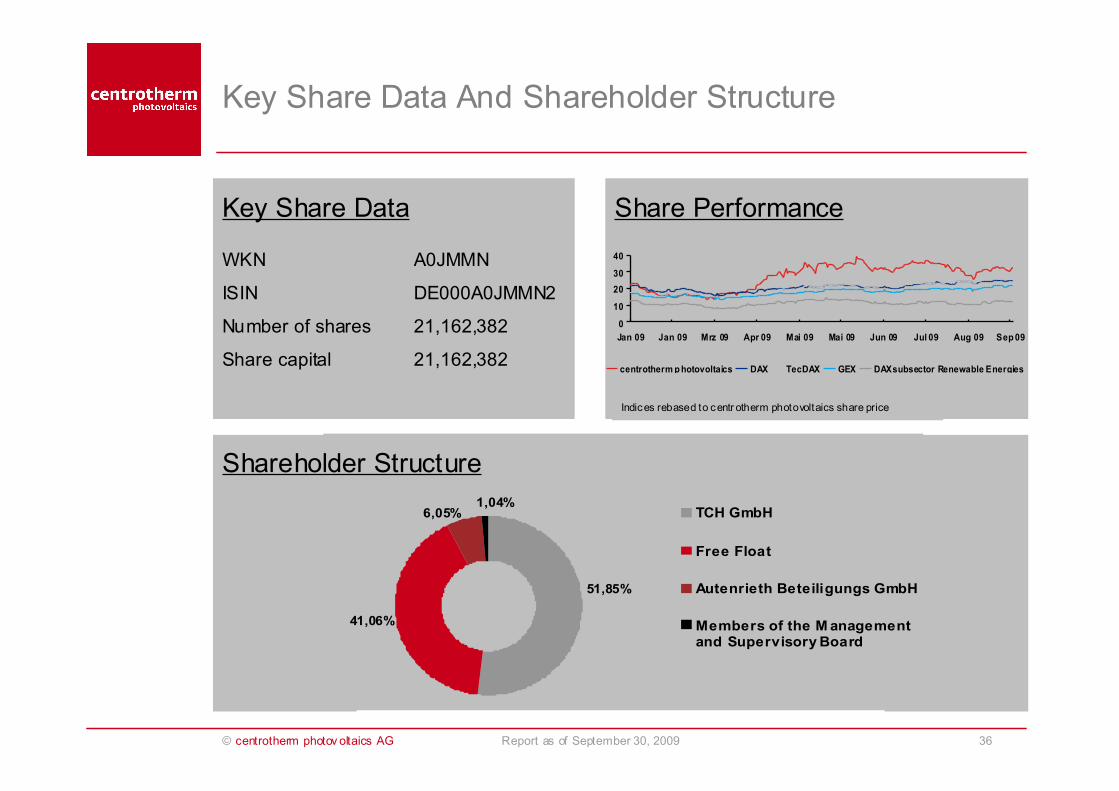

Key Share Data And Shareholder Structure

6,05%

41,06%

51,85%

1,04%TCH GmbH

Free Float

Autenrieth Beteiligungs GmbH

Members of the Managementand Supervisory Board

Key Share Data

WKN A0JMMN

ISIN DE000A0JMMN2

Number of shares 21,162,382

Share capital 21,162,382

0

10

20

30

40

Jan 09 Jan 09 Mrz 09 Apr 09 Mai 09 Mai 09 Jun 09 Jul 09 Aug 09 Sep 09

centrotherm photovoltaics DAX TecDAX GEX DAXsubsector Renewable Energies

Shareholder Structure

Share Performance

Indices rebased to centr otherm photovoltaics share price

37© centrotherm photov oltaics AG Report as of September 30, 2009

Contact

centrotherm - continuing innovations

Contact: Saskia Schultz-Ebert

Investor Relations

centrotherm photovoltaics AG

Johannes-Schmid-Strasse 8

89143 Blaubeuren

Tel +49 (0)7344 9188-890

Fax +49 (0)7344 9189-389