Reading - Amazon S3 · 2. Global Overview of Services Outsourcing4 Global outsourcing of services...

29

1st Reading November 26, 2008 16:38 WSPC/172-SER 00305 The Singapore Economic Review, Vol. 53, No. 3 (2008) 1–29 © World Scientific Publishing Company INDIA AND SERVICES OUTSOURCING IN ASIA RUPA CHANDA Indian Institute of Management, Bannerghatta Road Bangalore 560076, India This paper examines India’s role in services outsourcing within Asia. It provides a brief overview of the global as well as Indian services outsourcing industry. The core section examines India’s relationship with other Asian countries such as China, the Philippines, Vietnam, and Malaysia in service outsourcing. It examines the extent to which these countries pose a competitive challenge to India and concludes that at this time, India is far ahead although it is likely to face growing competition as its costs rise. The paper highlights the need to move beyond this comparative paradigm and to examine the complementary and collaborative opportunities that exist between India and other Asian countries in services outsourcing. It concludes that there is considerable scope for such synergies and that India and other Asian countries can form different parts of a larger regional or global delivery model. Regional and bilateral agreements within Asia can also facilitate this process. Keywords: Services; outsourcing; offshoring; information technology (IT); IT-enabled services; business process outsourcing. 1. Introduction Services outsourcing refers to the delegation of service activities to a third party, either onshore, or near shore, or offshore. Global outsourcing of services refers specifically to the offshoring of services, i.e., the delegation of service activities to another country. In recent years there has been rapid growth and scaling up of offshore outsourcing of services, involving a large number of countries and firms, and affecting a wide range of jobs and skill sets never before impacted by globalization. Several Asian countries are among the leaders in global outsourcing of services and have large and rapidly growing outsourcing industries. 1 India is the leading offshore destination for services outsourcing. It accounts for over 50% of the total value of work that is offshored in services. The outsourcing industry in India has been growing at around 40%–50% per annum over the past decade. More than 50% of Fortune 500 companies currently outsource a wide range of services to India. 2 The outsourcing industry is playing an important role in India’s integration with world markets and in its recent economic performance. This paper examines the role played by India in services outsourcing, globally and specifically within Asia. Section 2 provides a brief global overview of services outsourcing. 1 See AT Kearney, 2004. 2 NASSCOM (2005). 1

Transcript of Reading - Amazon S3 · 2. Global Overview of Services Outsourcing4 Global outsourcing of services...

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

The Singapore Economic Review, Vol. 53, No. 3 (2008) 1–29© World Scientific Publishing Company

INDIA AND SERVICES OUTSOURCING IN ASIA

RUPA CHANDA

Indian Institute of Management, Bannerghatta RoadBangalore 560076, India

This paper examines India’s role in services outsourcing within Asia. It provides a brief overviewof the global as well as Indian services outsourcing industry. The core section examines India’srelationship with other Asian countries such as China, the Philippines, Vietnam, and Malaysia inservice outsourcing. It examines the extent to which these countries pose a competitive challenge toIndia and concludes that at this time, India is far ahead although it is likely to face growing competitionas its costs rise. The paper highlights the need to move beyond this comparative paradigm and toexamine the complementary and collaborative opportunities that exist between India and other Asiancountries in services outsourcing. It concludes that there is considerable scope for such synergies andthat India and other Asian countries can form different parts of a larger regional or global deliverymodel. Regional and bilateral agreements within Asia can also facilitate this process.

Keywords: Services; outsourcing; offshoring; information technology (IT); IT-enabled services;business process outsourcing.

1. Introduction

Services outsourcing refers to the delegation of service activities to a third party, eitheronshore, or near shore, or offshore. Global outsourcing of services refers specifically tothe offshoring of services, i.e., the delegation of service activities to another country. Inrecent years there has been rapid growth and scaling up of offshore outsourcing of services,involving a large number of countries and firms, and affecting a wide range of jobs and skillsets never before impacted by globalization.

Several Asian countries are among the leaders in global outsourcing of services and havelarge and rapidly growing outsourcing industries.1 India is the leading offshore destinationfor services outsourcing. It accounts for over 50% of the total value of work that is offshoredin services. The outsourcing industry in India has been growing at around 40%–50% perannum over the past decade. More than 50% of Fortune 500 companies currently outsourcea wide range of services to India.2 The outsourcing industry is playing an important role inIndia’s integration with world markets and in its recent economic performance.

This paper examines the role played by India in services outsourcing, globally andspecifically within Asia. Section 2 provides a brief global overview of services outsourcing.

1See AT Kearney, 2004.2NASSCOM (2005).

1

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

2 The Singapore Economic Review

Section 3 discusses recent trends in India’s services outsourcing industry and highlights itsmain characteristics as well as its facilitators and constraints. Section 4 discusses India’srelationship with Asian countries in services outsourcing from a comparative as well ascomplementary perspective, based on secondary as well as primary sources.3

2. Global Overview of Services Outsourcing4

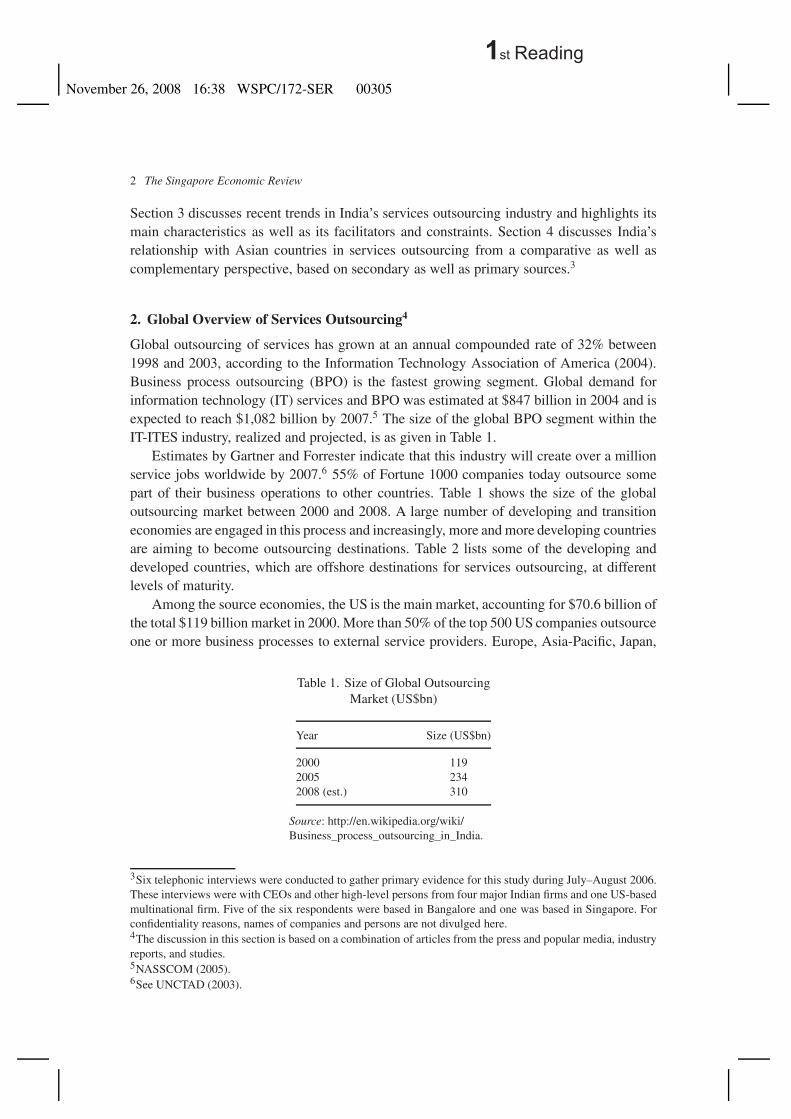

Global outsourcing of services has grown at an annual compounded rate of 32% between1998 and 2003, according to the Information Technology Association of America (2004).Business process outsourcing (BPO) is the fastest growing segment. Global demand forinformation technology (IT) services and BPO was estimated at $847 billion in 2004 and isexpected to reach $1,082 billion by 2007.5 The size of the global BPO segment within theIT-ITES industry, realized and projected, is as given in Table 1.

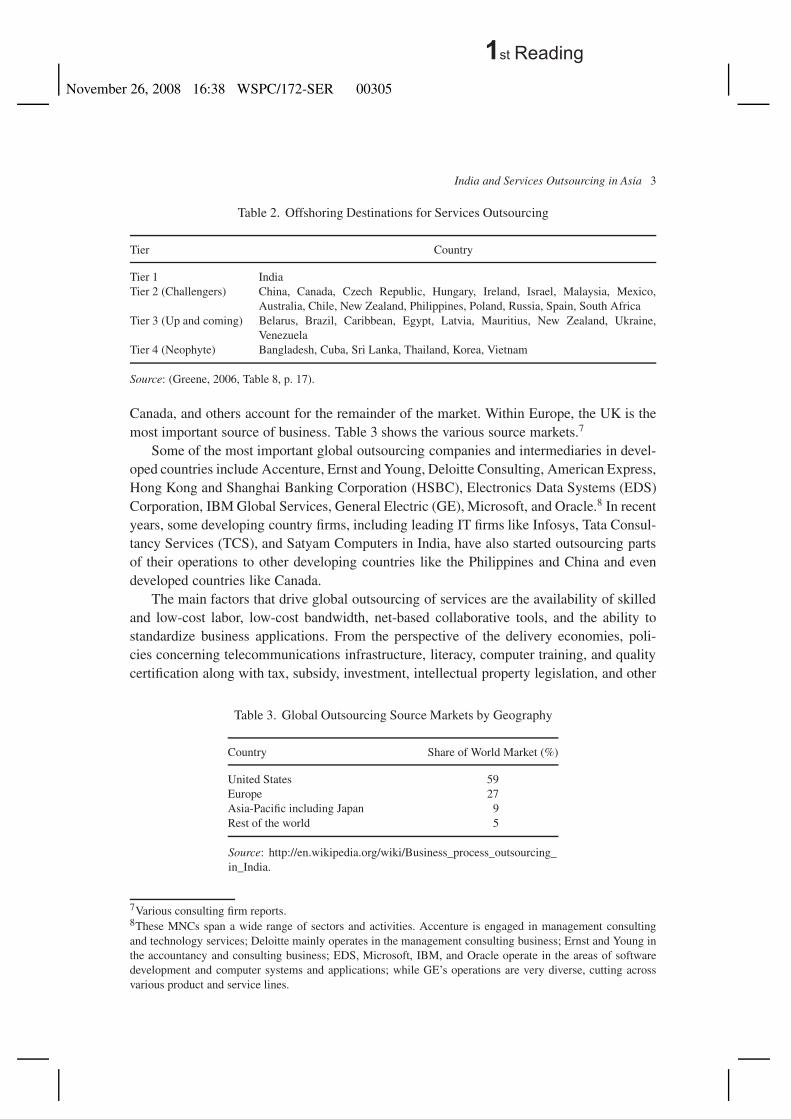

Estimates by Gartner and Forrester indicate that this industry will create over a millionservice jobs worldwide by 2007.6 55% of Fortune 1000 companies today outsource somepart of their business operations to other countries. Table 1 shows the size of the globaloutsourcing market between 2000 and 2008. A large number of developing and transitioneconomies are engaged in this process and increasingly, more and more developing countriesare aiming to become outsourcing destinations. Table 2 lists some of the developing anddeveloped countries, which are offshore destinations for services outsourcing, at differentlevels of maturity.

Among the source economies, the US is the main market, accounting for $70.6 billion ofthe total $119 billion market in 2000. More than 50% of the top 500 US companies outsourceone or more business processes to external service providers. Europe, Asia-Pacific, Japan,

Table 1. Size of Global OutsourcingMarket (US$bn)

Year Size (US$bn)

2000 1192005 2342008 (est.) 310

Source: http://en.wikipedia.org/wiki/Business_process_outsourcing_in_India.

3Six telephonic interviews were conducted to gather primary evidence for this study during July–August 2006.These interviews were with CEOs and other high-level persons from four major Indian firms and one US-basedmultinational firm. Five of the six respondents were based in Bangalore and one was based in Singapore. Forconfidentiality reasons, names of companies and persons are not divulged here.4The discussion in this section is based on a combination of articles from the press and popular media, industryreports, and studies.5NASSCOM (2005).6See UNCTAD (2003).

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

India and Services Outsourcing in Asia 3

Table 2. Offshoring Destinations for Services Outsourcing

Tier Country

Tier 1 IndiaTier 2 (Challengers) China, Canada, Czech Republic, Hungary, Ireland, Israel, Malaysia, Mexico,

Australia, Chile, New Zealand, Philippines, Poland, Russia, Spain, South AfricaTier 3 (Up and coming) Belarus, Brazil, Caribbean, Egypt, Latvia, Mauritius, New Zealand, Ukraine,

VenezuelaTier 4 (Neophyte) Bangladesh, Cuba, Sri Lanka, Thailand, Korea, Vietnam

Source: (Greene, 2006, Table 8, p. 17).

Canada, and others account for the remainder of the market. Within Europe, the UK is themost important source of business. Table 3 shows the various source markets.7

Some of the most important global outsourcing companies and intermediaries in devel-oped countries include Accenture, Ernst and Young, Deloitte Consulting, American Express,Hong Kong and Shanghai Banking Corporation (HSBC), Electronics Data Systems (EDS)Corporation, IBM Global Services, General Electric (GE), Microsoft, and Oracle.8 In recentyears, some developing country firms, including leading IT firms like Infosys, Tata Consul-tancy Services (TCS), and Satyam Computers in India, have also started outsourcing partsof their operations to other developing countries like the Philippines and China and evendeveloped countries like Canada.

The main factors that drive global outsourcing of services are the availability of skilledand low-cost labor, low-cost bandwidth, net-based collaborative tools, and the ability tostandardize business applications. From the perspective of the delivery economies, poli-cies concerning telecommunications infrastructure, literacy, computer training, and qualitycertification along with tax, subsidy, investment, intellectual property legislation, and other

Table 3. Global Outsourcing Source Markets by Geography

Country Share of World Market (%)

United States 59Europe 27Asia-Pacific including Japan 9Rest of the world 5

Source: http://en.wikipedia.org/wiki/Business_process_outsourcing_in_India.

7Various consulting firm reports.8These MNCs span a wide range of sectors and activities. Accenture is engaged in management consultingand technology services; Deloitte mainly operates in the management consulting business; Ernst and Young inthe accountancy and consulting business; EDS, Microsoft, IBM, and Oracle operate in the areas of softwaredevelopment and computer systems and applications; while GE’s operations are very diverse, cutting acrossvarious product and service lines.

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

4 The Singapore Economic Review

policies that shape the overall business environment for outsourcing, are very important indetermining a country’s attractiveness as an outsourcing destination.

Initially, outsourcing was largely limited to long-term ongoing support for IT infras-tructure, such as the maintenance, delivery, and management of IT functions by businesseswhose core operations were not related to IT, such as manufacturing companies. Moreover,initially, this outsourcing was mostly done on-site and was not offshored. However, withtechnological advancements and deregulation of the telecommunications sector around theworld, and the subsequent expansion of bandwidth and fall in connection costs, the range ofoperations that can not only be outsourced but also offshored, has grown significantly.

Today, global outsourcing in services involves an ever-increasing range of sectors, activ-ities, and skill requirements. These include, for instance, data entry and data mining services;on-line and telemarketing services; back-office corporate functions like accounting, payrollprocessing, billing, collections, benefits administration, travel, logistics, purchase and dis-bursement, and human resource management; technical support and help desk services likesoftware code writing, IT maintenance, and applications development; and complex busi-ness processes such as content development, design, research, and analytical and advisoryservices.9 Table 4 highlights the main industry verticals in global services outsourcing.

Companies are leveraging global outsourcing both horizontally across different servicelines and vertically across different segments within a service line. Also, as more and moreservices are provided remotely across borders and the range and complexity of servicesexpands, the boundaries between sectors and activities are increasingly getting blurred.

According to Forrester Research (2002), offshoring is expected to grow by 30%–40%per year over the next five years. The number of US jobs that will be outsourced to low-costcountries is projected to grow to 3.3 million by 2015, accounting for $136 billion in wages. Itis expected that 473,000 jobs from the IT industry alone will be offshored by 2015.10 Globalexpenditures on IT-enabled business process outsourcing services are projected at $165billion for sales activities, $163 billion for legal services, and $123 billion for engineeringand research and development services in 2006.11 Gartner projects that over the next two

Table 4. Global Outsourcing Market by Industry

Industry Shares (%)

Information technology 43Financial services 17Communication (telecom) 16Consumer goods/services 15Manufacturing 9

Source: http://en.wikipedia.org/wiki/Business_process_outsourcing_in_India.

9See Business Week (2003).10McKinsey Global Institute (2003).11Economic Times (12 June 2003).

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

India and Services Outsourcing in Asia 5

Table 5. Number of US Jobs Projected to be Offshored to Low-Wage Countries

Occupational Category 2005a 2010 2015 Difference 2005–2015

Life, physical, and social sciences 4,000 16,000 39,000 35,000Legal 20,000 39,000 79,000 59,000Art, design, entertainment, sports, medical 8,000 15,000 30,000 22,000Management 34,000 106,000 259,000 225,000Business operations 91,000 176,000 356,000 265,000Computer and mathematics 181,000 322,000 542,000 524,000Architecture and engineering 46,000 93,000 191,000 145,000Sales and related 38,000 97,000 218,000 180,000Office and administrative support 410,000 815,000 1,600,000 1,190,000

Total 830,000 1,700,000 3,300,000 2,570,000

Source: Forrester Research Inc. (2002).aThese were projected employment numbers for 2005, based on earlier studies.

years, 40% of the US’ top 1,000 companies will outsource one or more service projectsoverseas and that 30% of the large US companies will outsource IT services and managecertain business process via offshore vendors. A big offshore push is expected around 2010once there is standardization of global white-collar sourcing practices.

Demographic imperatives will also drive services outsourcing in future. According tothe US Bureau of Labor Statistics projections, there will be an estimated 167.75 million jobsin the US in 2010 but only 157.72 million workers available, and thus a shortage of some10 million workers.12 Table 5 shows the estimated number of US jobs that will be offshoredin various areas and disciplines to developing countries like India, China, Mexico, and thePhilippines, between 2005 and 2015.

To the extent that many services can be intermediated and physically disengaged from thefirm location and labor imports cannot make up for this entire gap, much of this shortage willbe met in future by outsourcing contracts to low-cost developing countries. This trend willbe further abetted by growing pressures on companies to be globally competitive, coupledwith manpower shortages in the developed world, the deregulation of services, especiallytelecommunication services in developing countries, and technological improvements.

3. Overview of Services Outsourcing in India

The rapid growth of India’s services sector in the post-reform era has played a critical role inthe country’s emergence as one of the fastest growing economies in the world in recent years.India’s services sector grew at an average annual rate of 9% during the 1990s. The share ofthe services sector in India’s GDP has risen consistently over the years, with an average shareof 52% between 2000–2001 and 2005–2006.13 The contribution of services to India’s tradeand FDI flows has also grown over the past decade, facilitating India’s integration with the

12Economic Times (9 June 2003).13World Bank (2004).

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

6 The Singapore Economic Review

world economy. Between 2000 and 2005, India’s services exports grew at an average annualrate of 33%, much above the world average for this period and faster than its merchandiseexports.14 The share of services in India’s total trade has risen to 30%.15 According to a2004 World Bank study on India’s service sector, India’s revealed comparative advantage inservices has risen significantly during the 1990s, especially in the area of business services(which includes IT and IT-enabled services). As a result, India has succeeded in raising itspenetration of world markets more rapidly in the case of services than for goods.

3.1. ITES-BPO sector in India: key trends and features

The ITES-BPO segment is one of four segments within the IT industry (the others beinghardware, IT, and engineering services and software products). The most dynamic growtharea in India’s services trade has been information technology (IT) and ITES (which includesBPO services). The total Indian market for IT-ITES was estimated at $36.3 billion in 2005–2006, roughly 4.8% of GDP according to the industry body, NASSCOM. The industry’sshare in India’s total services exports has grown from only 10% in 1995–1996 to around40% today, and India’s share in the world market for IT services (including BPO) has risenfrom 1.7% in 2003–2004 to 2.3% in 2004–2005 and further to an estimated 2.8% in 2005–2006.16 There has been a significant shift towards offshore as opposed to on-site provisionof IT services. From only 5% of IT services being provided offshore in 1990/1991, the shareof offshore IT services increased to 71% by 2004–2005.17

Both the IT services and the ITES-BPO segments have grown rapidly over the pastdecade. IT services exports grew at over 50% in the 1990s. Within the IT industry, theITES-BPO segment registered growth rates of 48% and 37% in 2004–2005 and 2005–2006,respectively. This segment is expected to register a turnover of $30 billion by 2010 and itsshare in GDP is expected to rise to 7% by 2008. The ITES-BPO segment is also highlyexport-oriented, with exports constituting over 95% of total revenues (exports plus domesticsales). Its share in total IT exports has grown from 6.5% in 1998–1999 to 29% in 2003–2004and is expected to reach 57% by 2007, thus constituting the most important component of ITexports.18 It is, however, becoming increasingly difficult to differentiate between the varioussegments of the IT industry, including the ITES-BPO and the engineering services segments,and thus statistics in this sector are subject to many classification problems. Figure 1 showsthe revenue trends for the various segments of India’s IT industry and the growing importanceof the ITES-BPO segment.

Table 6 shows revenue trends in the BPO segment during the 1999–2006 period. India’sIT-ITES exports are highly concentrated in a few countries. The US is the most important

14IBEF (www.ibef.org). Between 1995 and 2000, while India’s services exports grew nearly six times fasterthan world services exports (23.2% compared to 3.7%, respectively), its merchandise exports grew at only 1.4times the annual average growth rate for world exports of goods (5.4% compared to 3.9%, respectively).15Hindu Business Line (11 April 2006).16IBEF (www.ibef.org).17Asia Institute Research Series (2006), Chart 4, p. 5.18NASSCOM (2006).

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

India and Services Outsourcing in Asia 7

2.93.9

4.855.9

6.9

3.4

5.2

7.2

10.4

13.5

17.5

0

2

4

6

8

10

12

14

16

18

20

2004 2005 2006E

Engineering Services & S/w Products Hardware ITES-BPO IT Services

Figure 1. Revenue Growth for Major Sources in the Indian IT Industry (US $ billion)

Source: NASSCOM (2006).

Table 6. Business Process OutsourcingRevenues, 1999–2006 (millions of US$s)

Year Revenue ($ million) Percent change

1999–2000 5652000–2001 930 652001–2002 1,495 612002–2003 2,500 672003–2004 3,600 312004–2005∗ 5,200 442005–2006∗ 7,300 40

Source: Economic Times, NASSCOM.Note: (*) estimates.

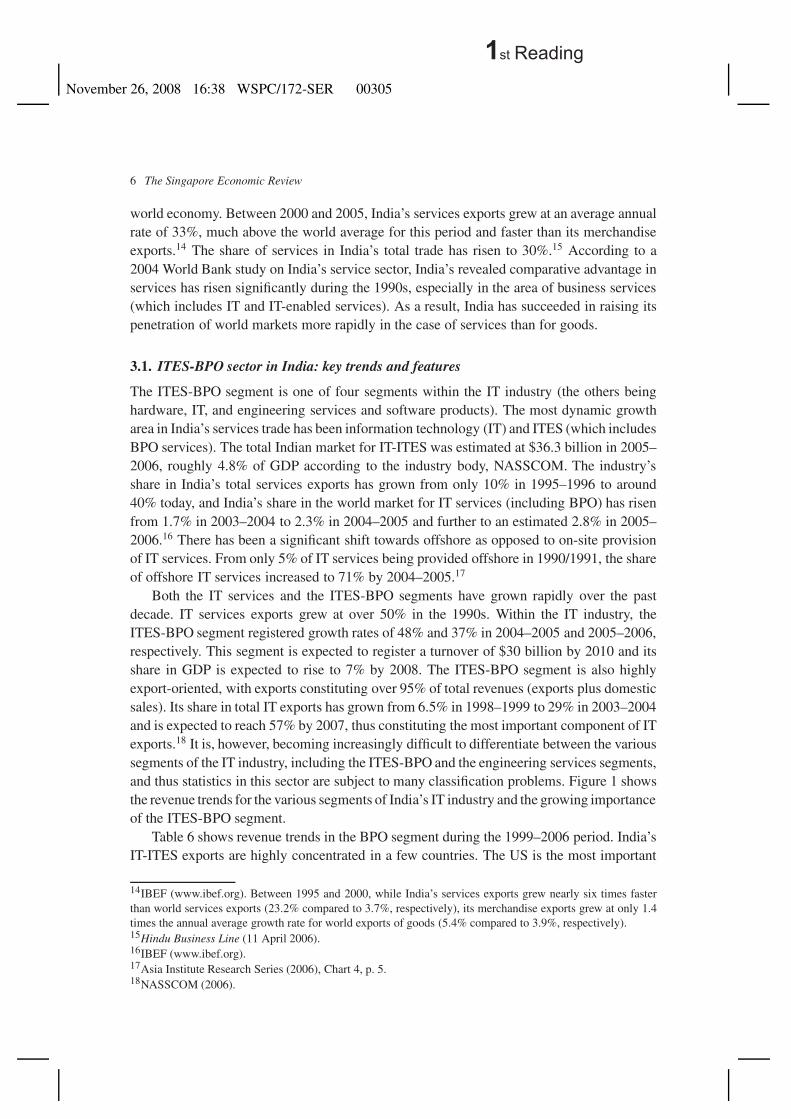

market, followed by the UK (14%). For activities such as contact services (call-center ser-vices), the US accounts for close to 80% of such exports, followed by the UK at 17%, andother markets which account for only 5%. Table 7 provides the values and shares of India’sIT-ITES exports to various markets.

There has also been significant growth in employment in the industry, with the numberof employees rising from about 40,000 in 2000 to over 300,000 by 2005. The employmenttrends in the IT and ITES-BPO industries are shown in Figure 2.

3.1.1. Characteristics of the industry

India is engaged in all kinds of services outsourcing, across a wide range of service lines andactivities. These include customer services, call-center activities, finance and administration,content development, and back-office billing and payment services, among others. Table 8summarizes the various processes currently outsourced to India.

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

8 The Singapore Economic Review

Table 7. India’s IT-ITES Exports by Destination Country, 2003–2004 and2004–2005 (millions of US$ and percent shares)

2003–2004 2004–2005

Share (%) Value Share (%) Value

America 69.4 8884 68.4 12,107Brazil 0.01 1 NA NACanada 1.1 143 0.9 159Mexico 0.01 1 NA NAUSA 68.2 8725 66.5 11,769Rest of America 0.1 13 1 178Asia, Oceania & Middle-East 7.4 943 8 1416Australia 0.8 105 0 139China 0.1 15 0.1 24Hong Kong 0.2 26 NA NAJapan 3 385 2.8 500Singapore 1.8 227 1.7 300South Korea 0.2 23 0 7Rest of Asia 1.3 161 2.6 460Europe 22.6 2894 23.1 4093UK 14.5 1857 14 2478Germany 2.8 354 2.3 400France 0.5 65 0.4 72Italy 0.1 12 NA NAFinland 0.5 61 NA NASweden 0.6 76 0.6 100Netherlands 1 129 1.4 250Switzerland 0.7 91 0.7 120Rest of Europe 1.9 249 3.8 673Others 0.6 81 0.5 90GRAND TOTAL 100 12,800 100 17,705

Source: NASSCOM (2006).

The bulk of ITES-BPO exports in India today are derived from customer services(call-center) and back-office financial and administrative services and essentially high-volume but low-value work, which does not require specialized skill sets. There is,however, a gradual shift in revenue composition towards more sophisticated and higherend services in India’s outsourcing industry, often called knowledge process outsourc-ing (KPO) activities. Examples of KPO services include activities such as risk anal-ysis, business research, equity research, balance sheet analysis and risk modeling forfirms, contract research in development of new molecules, clinical research trials, med-ical image processing and diagnostics, and editorial selection and publishing, to namea few. This trend towards KPO services is being driven by the setting up of R&D cen-ters by MNCs like IBM, GE, Motorola, Texas Instruments, and Cisco Technologies. Theresearch and development outsourcing market in India is expected to grow from $1.3billion (2003) to $9.1 billion (2010) and is estimated to have the potential to generate

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

India and Services Outsourcing in Asia 9

Figure 2. Employment in IT, ITES-BPO, 2000–2005 (Thousands of Employees)

Source: Deutsche Bank Research (2005, Chart 7, p. 4).

Table 8. Processes Outsourced to India

Segment Processes Outsourced

Customer care Call centers (inbound and outbound), telesales and telemarketing, web sales, helpdesks (electronic and voice), clerical support, data entry, word processing, massemailing, contact centers, IT and technical support help desks, e-CRM,collections, market research, customer phone support, warranty registration,catalog sales, order fulfillment, up-selling and cross-selling, customerrelationship management

Healthcare Medical transcription, medical billing and coding, healthcare services, medicalanimation, teleradiology, clinical services

Finance Accounting and accountancy services, billing and payment services, back-officefinance processing, banking processing, sales ledger, general nominal ledgeraccounting, financial reporting, customer supplier processing, documentmanagement, legal services, transaction processing, equity research support,accounts receivable, accounts payable, cost accounting, payroll andcommissions, stock market research, mortgage processing, credit change cardprocessing, check processing

Human resources Personnel administration, hiring and recruiting, training and education, records andbenefits payment administration, payroll services health benefits administration,401(k) administration, pension fund administration, retention, labor relations

Payment services Credit card and debit card services, check processing services, loan processing,electronic data interchange

Content development Engineering and design services, automation programming, digitization, animation,network management, biotech research, application development andmaintenance, web and multimedia content development, e-commerce

Administration Tax processing, claims processing, asset management, document management, legaland medical transcription, translation

Source: Greene (2006, Table 7, p. 18).

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

10 The Singapore Economic Review

Figure 3. Composition of India’s Business Process Outsourcing Exports (% shares), 2004–2005

Source: Deutsche Bank Research (2005).

200,000 plus jobs by 2010.19 Thus, the potential to move up the value chain remainslarge. Figure 3 highlights the shares of various activities that are currently outsourced toIndia.

Various business models are in operation in India’s services outsourcing industry. Theseinclude captive offshore centers of foreign multinationals, collaborative arrangements, andthird-party outsourcing to independent Indian firms. The pure captive model consists ofthe setting up of an internal cost center or a 100% subsidiary company to execute offshorebusiness process or IT services exclusively for the parent company. Firms such as GE, ANZand American Express have set-up captive subsidiaries in India, which perform servicesexclusively for them. There are also captive partnership models which consist of strategicalliances with Indian providers for implementing support services like infrastructure set-up, recruitment, and training. At the other end, there is the pure outsourcing business modelwhere work is outsourced to independent Indian companies who serve many different clients.These include Indian firms like Infosys, Wipro, and Cognizant, which undertake servicesoutsourcing on large and small scale, for multiple clients around the globe. In between thesetwo extremes are mixed business models where foreign and domestic firms engage in a jointventure or collaborative arrangement. Some of these companies are engaged exclusively inoutsourcing operations, while others (typically the larger firms) are engaged in a variety ofBPO and non-BPO operations (typically other IT services and production activities). As theindustry matures, there is a trend away from captive models towards the other models ofoutsourcing.

19http://www.indiainbusiness.nic.in/india-profile/ser-infotech.htm.

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

India and Services Outsourcing in Asia 11

The services outsourcing industry in India is highly concentrated geographically in afew cities. The main locations are the National Capital Region (NCR which includes Delhi,Gurgaon, and Noida), Bangalore, Mumbai, Hyderabad, and Chennai. The availability ofhuman resources and quality of physical infrastructure as well as presence of educationaland research institutions have been key determinants in the emergence of these cities aspremier outsourcing locations in the country. Increasingly, there are a number of second tiercities where companies are starting to spread their operations mainly because of the humanresource and infrastructural bottlenecks that are emerging in first tier locations given therapid growth of this industry.

3.2. Facilitating factors

A variety of factors have helped India’s services outsourcing industry. The single most impor-tant factor is the large pool of computer-literate and English-speaking persons available in thecountry. It is estimated that India has 2 million college graduates, 0.3 million postgraduates,200,000–250,000 (by some estimates 350,000) engineers, and 2,000 MBAs per year.20 Indiahas over 270 universities and 2,400 colleges, and several institutes of international repute.Thus, it has scalability in offshore services operations, which few countries other than Chinapossess. India is likely to sustain this human resource base advantage given its age structure.With a median age of 24.9 years and with a population pyramid where almost 15% of itspopulation is under 15 and 65% is between 15 and 64 years of age, India is well-placedto provide the human resource requirements of a growing services outsourcing industry.21

However, as the educationally less equipped Northern states have higher fertility rates whilethe higher literacy Southern and Western states have lower fertility rates, the demographicdividend need not automatically translate into sustained competitive advantage in future.There needs to be concomitant investment in education and employability of skills acrossstates in India to reap this demographic dividend.

Coupled with such scale are low labor costs. Labor costs are one-tenth to one-fifth ofthat for US IT workers. While an IT services professional costs between $50,000 to $70,000per year in the US and Germany, he costs only $6,000–$8,000 in India.22 A study by Datamonitor shows that per hour wages for customer care (telemarketing and other voice-basedcustomer service) operations in India are only 10%–12% of the cost of similar operationsin the UK. According to a Deutsche Bank paper, despite additional expenses incurred byoffshoring client firms due to investments in infrastructure, management costs, and localadaptation, among other costs, the large labor cost differentials permit savings of 20%–40%from offshoring to India.23

Another important facilitating factor has been the presence of a well-established, maturedomestic IT sector. As illustrated earlier, India’s IT industry has experienced rapid growth.

20http://www.thehindubusinessline.com/life/2006/07/21/stories/2006072100310100.htm (published 21 July2006).21https://www.cia.gov/cia/publications/factbook/geos/in.html.22Businessworld (2006).23See Deutsche Bank Research (2005, Chart 5, p. 4).

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

12 The Singapore Economic Review

Since the mid-1980s, there has been growing demand for engineers and software personnelfrom companies in the United States. Indian IT companies provided software programmers,coders, and software developers to US companies for on-site services.24 Thus, while Chinaestablished itself as a manufacturing hub for hardware, India became known for softwareservices. Many Indian IT companies acquired international quality certification and wereable to work on large-value contracts.25 Indian IT companies demonstrated their ability tohandle complex operations and a wide range of application skills. With advances in informa-tion and communication technology and the growing possibilities for performing many ofthese same services offshore, Western companies started establishing offshore developmentcenters in India. Indian IT companies were also able to get offshore contracts given theirdemonstrated experience and previous client networks. Hence, in the early stages, the bulkof services outsourcing to India was in IT outsourcing. The presence of big Indian play-ers such as TCS, Wipro, and Infosys helped give India a first mover advantage in servicesoutsourcing. In addition, the spurt in demand for IT experts (software programmers, spe-cialists, network architects, and consultants) around 2000 due to the Y2K problem, coupledwith cost imperatives of Western companies, also contributed to the growth in offshoring toIndia.

Government policies have also helped the growth of India’s services outsourcing indus-try. The government has provided many incentives in terms of liberal tax treatment (taxholidays, reduction on sales tax on software and hardware, exemptions from payment ofentry tax on all capital goods used for the business for specified periods), subsidies forsetting up establishments (direct subsidies on fixed capital investment), and setting up ofSoftware Technology Parks (STPI) and dedicated zones with provision of physical infras-tructure to firms within these zones.26 The government has also allowed private entities toset up software parks in the country, such as the ITPL in Bangalore.27 The government hasalso had very liberal FDI policies with regard to the form and extent of foreign equity par-ticipation (allowed up to 100% and all forms of establishment being permitted), and veryliberal trade policies for imports of telecom, computer equipment, and other import items inthis sector, with very low or zero import duties. There have also been manpower and humanresource initiatives (training in soft skills, exemption from restrictive labor laws preventingfemale employment on night shifts, flexible hours). Deregulation of the telecommunicationssector and improvements in telecom infrastructure have been particularly helpful. Liberal-ization of telecom services has led to falling connectivity costs, low-cost bandwidth, and thedevelopment of a large telecom network with good satellite and cable communication links,123,000 kilometers of fiber optic cables. Growing competition in the provision of internetand telephony services has led to rapid growth of around 20% per year in this sector andimproved quality of services.28

24http://www.dqindia.com/content/20years/102122306.asp.25India leads in the number of IT companies which have the highest level Capability Maturity Model certification.26http://www.stpn.soft.net/html/about_us.html.27http://www.intltechpark.com/about_itpark/about_itpark.htm.28ISI Emerging Markets (2006).

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

India and Services Outsourcing in Asia 13

There are other factors that have helped in the growth of India’s services outsourcingindustry. India has a time zone advantage, as it is possible to get tasks completed in Indiawhile business is closed in the West, thus allowing for 24/7 operations. The presence ofan active industry association, the National Association of Software Services Companies(NASSCOM), has also helped the Indian services outsourcing industry. NASSCOM hashelped lobby the government for favorable policies in showcasing the industry to clientcompanies and countries, and in interacting with overseas business interests to secure marketaccess for Indian companies. Another important contributor has been the Indian diaspora,especially in the US. There were estimated to be over a million Indians residing in the US in2001. Indians form the second largest group of doctoral candidates in the US. The share offirms in the Silicon Valley that have been set up by Indians has risen from 3% in the 1980sto 10% between 1995 and 2000. This diaspora has played an important role in bringingbusiness to India, either through direct outsourcing to Indian companies, with which manyof these non-resident Indians have previously worked or interacted, or by influencing theirmanagement in setting up offshore subsidiaries in India and often returning to head theseoperations. It is estimated that returning Indians set up 95% of firms in Bangalore’s SoftwareTechnology Parks. Thus, the usual brain gain, diaspora network effects have been strong inIndia’s services outsourcing industry.

Given India’s many advantages, both inherent and policy-induced, it is today the leadingdestination for global services outsourcing, as shown in the 2004 AT Kearney rankings ofthe top 20 global offshoring destinations.29 The main differentiator for India is people skillsand availability where it scores much better than all other countries. India’s scores on theother two attributes are broadly comparable to those of other countries and any deficienciesare greatly outweighed by its human resource advantage.

3.3. Emerging challenges

Although India is expected to remain the main offshoring destination in the near future,several constraints are emerging which could erode India’s competitiveness. On the humanresource front, two kinds of problems are beginning to affect the industry. One is the growingshortage of skilled and quality manpower, especially in the first tier cities. There is anestimated demand for 20,000–25,000 graduates per year in the National Capital Region andfor 17,000–20,000 graduates per year in Bangalore. Such a demand is becoming increasinglydifficult to fill as only 20%–25% of graduates are found to be employable with the given skillsets.30 According to some industry experts, if one takes into account quality considerations,then the number of Indian engineering graduates would fall considerably.

There is also a dearth of persons with specialized and domain knowledge skills in someof the emerging knowledge process outsourcing (KPO) segments. Also, notwithstanding the

29Kearney (2004, Figure 1, p. 2).30http://www.thehindubusinessline.com/life/2006/07/21/stories/2006072100310100.htm (published 21 July2006).

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

14 The Singapore Economic Review

large pool of English-speaking persons in India, the quality of this English is variable andbeyond the first tier cities, there are problems with accent neutralization and fluency.

A second problem on the human resource front relates to attrition, which is in the range of25%–40%, and in some cases as high as 60%. While such rates are lower than in developedcountries (where attrition may be as high as 60% or more), the high rate of turnover imposeshuge costs on firms, especially since firms have to invest in training their employees in bothgeneral as well as project-specific skills. Attrition is partly due to the poaching of employeesby outsourcing firms from each other in their attempt to meet the growing need for fluentEnglish-speaking and technically qualified manpower. It is also a result of employees movingfrom one firm to another within the outsourcing industry or to other areas in search of a bettercareer path.

The inability to meet the growing demand for quality manpower coupled with attritionhas resulted in wage increases to the tune of 10%–15% per year. According to a study byIndia Outsource, the average annual salary for an entry-level software developer in India hasrisen by 13% a year, from $4,082 in 2000 to $6,628 in 2004. Salaries of mid-level managershave risen by 23% per year over the same period, from $13,385 to $31,131.31 It must benoted, however, that the wage growth is also in part a reflection of the industry’s verticalmovement towards higher-end and more specialized operations in India.

Infrastructural bottlenecks are also starting to plague the Indian outsourcing industry,in particular, lack of office space and rising rental costs and real estate prices in first tiercities. According to a McKinsey report, the asking rate for new office space is 25 millionsquare feet per year and there is a need to set up office space equivalent to several existingoutsourcing hubs (five more Gurgaons and seven Punes, two current offshore locations inIndia). Such physical infrastructural constraints are putting cost pressures on the industry.Transport infrastructure, including roads, airlines and railways, have not been able to keepup with the spillovers of growth in the ITES and IT industry.32 All these problems do pose anissue for firms looking to expand within India as they are debilitating factors to improvementsin quality and growth in quantity for service providers.

Regulatory constraints are also present, particularly with regard to data protection legis-lation. The country lacks a national data protection law and all matters relating to consumerdata privacy and confidentiality are handled at the B2B level. Given recent cases of datatheft and fraud in some outsourcing firms, there is growing pressure from overseas clientsand the industry association to put in place a national data protection act, especially as theindustry moves into IP-sensitive operations.

There is growing recognition within industry and the government that policies arerequired to strengthen the human resource base, attune skill sets to the needs of indus-try, develop appropriate regulatory and legal frameworks, and introduce measures whichimprove employee retention and career development. For example, NASSCOM is partner-ing with the All India Council for Technical Education to address the curriculum needs

31http://indiaoutsource.livejournal.com/2006/01/05/.32http://www.cfo.com/article.cfm/5674512/c_5676923?f=insidecfo.

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

India and Services Outsourcing in Asia 15

of the industry and has signed a MOU with the University Grants Commission. Industrybodies have also been discussing non-poaching agreements among the larger Indian out-sourcing firms to stem employee attrition. There is also an emerging view that Indian firmsneed to diversify their outsourcing operations and move up the value chain, given increasedcompetition at the lower end from other developing countries. There is concern within theindustry that unless some of these constraints, especially the human resource constraints, areaddressed, India may not be able to sustain its competitiveness in global services outsourcing.

4. India’s Role as an Offshore Destination in Asia

India’s presence within Asia as a services outsourcing destination can be examined alongvarious dimensions. The first is from a comparative perspective — how India compareswith other Asian countries, and in particular, with China on parameters such as quality, cost,availability of requisite manpower, government policies, and other such contributing factors.The second is from a complementary perspective, i.e., how Western and Asian multinationalsas well as Indian companies can complement the skill sets and advantages that India haswith those in other Asian countries, how India fits within the regional and global deliverymodel of services outsourcing for Western and Asian multinationals, and how other Asiancountries fit within the regional and global delivery model of Indian BPO and ITES firms.

4.1. A comparative perspective

According to the AT Kearney 2004 rankings, six out of the top 20 offshore destinationsshown in the AT Kearney 2004 rankings are in Asia. These are India, China, Malaysia,Philippines, Thailand, and Vietnam, in order of attractiveness. Emerging BPO providerslike Bangladesh, Thailand, Vietnam, and Cambodia perform activities such as basic dataentry, conversion, and digitization. Bangladesh is a host to medical transcription services.Digitial Divide Data Company based in Phnom Penh, Cambodia provides outsourced dataservices for business and public customers both at home and abroad and has performed thedigitization of Harvard University’s archives.33 Several Asian countries are also engagedin more sophisticated outsourcing activities. For example, Philippines is host to outsourcedwork by some 8,000 foreign companies covering services such as graphic design, architec-tural blueprints, telemarketing, accounting, and software code writing, given its large poolof low-cost, high-quality professionals in these different fields.34 It is also host to captivecall-centers for several US-based MNCs. Singapore serves as an Asia-Pacific hub for compa-nies like ABB for provision of remote IT support and infrastructure services. China is a keyproduct development center for GE, Intel, Microsoft, Phillips, and other electronics giants,for hardware design and embedded software. Service providers in Singapore are engagedin leading-edge functions like remote robotics management, healthcare, and genetic diag-nostics. Although India is clearly the leading country, it is facing growing competition fromother countries in Asia.

33UNCTAD (2003).34AT Kearney (2004).

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

16 The Singapore Economic Review

4.1.1. India versus China

The main competitor for India within the Asian region is China. Like India, China has alarge talent pool, with 1.6 million engineering graduates and 9.6 million young professionalgraduates.35 China also has a well-developed domestic IT industry, which is able to engagein outsourced IT operations. China is also capable of tapping the voice-based outsourcingmarket from Japanese and Korean firms, given its linguistic and cultural affinity to thosemarkets. The Chinese government, like the Indian government, has played a supportive rolein developing the outsourcing industry. China has invested over $5 billion in education soas to attune skill sets to the needs of the outsourcing industry and to be able to tap the voice-based business from the US and Europe.36 It has also established technology parks similarto those in India, and is also trying to develop second tier cities like Xian, Nanjing, Dalianand Guangzhou, alongside first tier cities like Shanghai and Beijing.

However, China lags far behind India in the availability of English-speaking capabilities.According to Evaluserve analysis (the latter being a KPO firm in India), in terms of sheernumbers and not taking into account quality considerations, China had only 18,000 ITESprofessionals compared to 144,000 in India in 2002, and by 2006, China will have 66,000ITES professionals compared to over 500,000 in India. The existing human resource basewithin the IT/ITES industry as a whole is expected to be around 970,000 in China in 2006compared to nearly 1.8 million in India.37 In terms of the number of new entrants into theIT industry, India surpasses China by nearly two times. In addition, there are also qualityissues with the available manpower in China (as in the case of India), coupled with problemsof attrition, and a dearth of middle and project management skills. Also, unlike India’sIT industry, the Chinese IT industry lacks international quality certification, is much morefragmented, and is relatively weak on the software side (though it is stronger in the hardwaresegment).

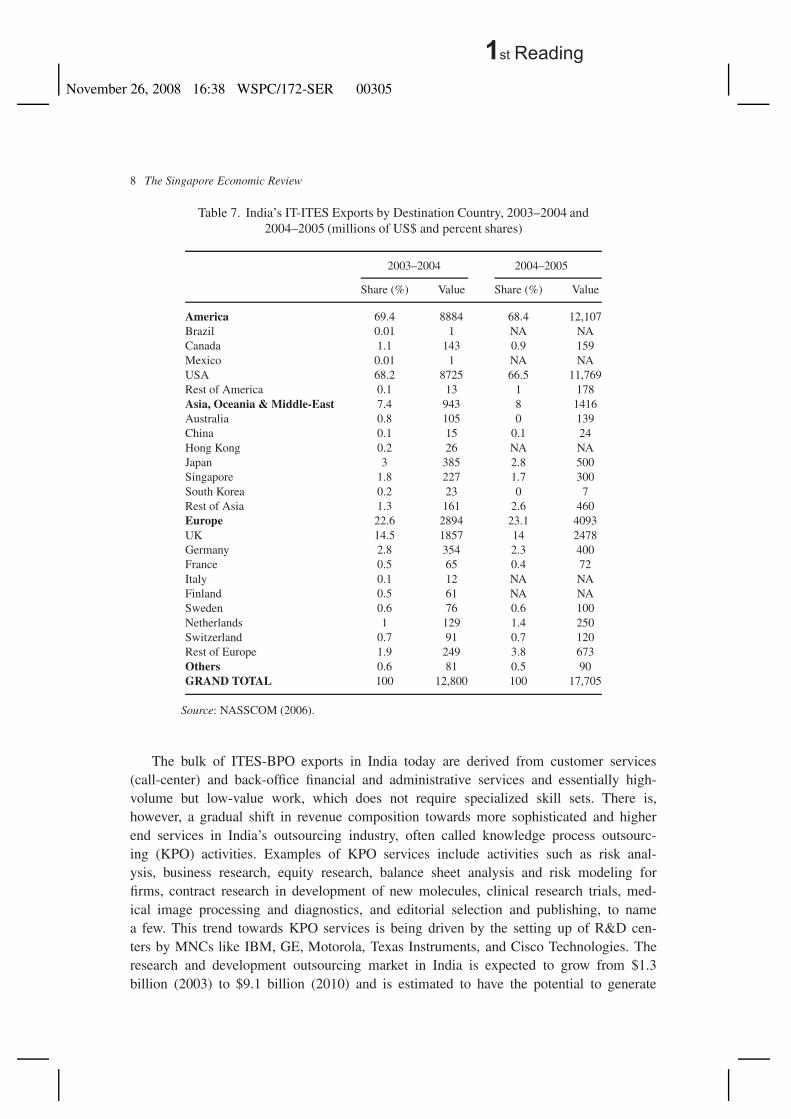

China’s ITO and BPO sectors are well-poised for growth but lag far behind India’s inrevenue terms. Revenues from BPO in China have grown from $490 million in 2002 to $977million in 2005, and are projected to rise to $1.4 billion by 2007. Revenues from ITO havegrown from $645 million to $934 million between 2002 and 2005 and are projected to riseto $1.7 billion by 2007. While this growth is substantial, the Chinese outsourcing industry isstill a fraction of the market size in India, where BPO services alone were estimated at over$6 billion in 2005 and are expected to grow to over $20 billion by 2007. Most outsourcingcompanies in China are very small and the industry is very fragmented. Thus, India is muchmore competitive and able to tap a larger share of the growing global offshoring market.Figure 4 illustrates the size of the IT and business process outsourcing markets in Chinabetween 2002 and 2007.

The services outsourcing industry in China is also quite different from India’s in termsof its geographic orientation. Its main markets are Japan and Hong Kong, while the US

35Farrell and Grant (2005).36http://infotech.indiatimes.com/articleshow/1710732.cms (6 July 2006).37Presentation by Evaluserve, an Indian KPO firm.

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

India and Services Outsourcing in Asia 17

490

645

574

705

802

705

977

934

1173

1252

1404

1730

0

500

1000

1500

2000

2500

3000

3500

2002 2003 2004 2005 2006 2007

BPO ITO

29%

17%

Figure 4. ITO and BPO Market Size in China, US$ Million and CAGR % (2002–2007)

Source: Lewis (2005, Figure 2, p. 12).

2%15%

13%

55%

15%

Taiwan Others US Japan Hong Kong

Figure 5. Offshore Outsourcing by Geography (2004)

Source: NeoIT (2005), Figure 2, p. 3.

accounts for a much smaller share of its exports, indicating clearly China’s limitationsin getting English-language based business. Figure 5 illustrates the market orientation ofChina’s outsourcing industry.

In terms of content also, the Chinese outsourcing industry differs from India’s. Thereare captive operations by Asian (mainly in Dalian area) and non-Asian multinationals inChina and there is very little independent work done by Chinese outsourcing companies.The bulk of the industry’s revenues are from the IT and telecom outsourcing segments (47%),reflecting China’s strengths in the IT hardware and telecom areas, followed by banking andfinancial services outsourcing (11%), and to a very limited extent voice-based operations.38

China is not as well-placed as India to cater to the growing business process outsourcingmarket. It is in a better position to do outsourcing work that relates to its manufacturing

38Details on the geographic orientation and composition of the Chinese outsourcing industry were obtainedfrom NeoIT (2005).

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

18 The Singapore Economic Review

capabilities, as in IT and telecom and related engineering and design services. To the extentthat English-speaking countries such as the US and the UK are likely to remain the mainclient countries for offshore services in the near future (although the Asia-Pacific market isexpected to grow), China will not be able to easily tap the growing voice-based BPO segment.

Overall, the main factor which will constrain China from challenging India’s leadingposition in IT and BPO services is talent, where according to industry experts, there is alooming shortage notwithstanding China’s large stock of graduates and engineers. A recentstudy by the McKinsey Global Institute found that there are several problems with theexisting talent pool in China. Apart from lack of knowledge of English, other problemsinclude poor communication skills; lack of practical orientation in the education system andthus graduates who are ill-equipped for analytical and process-oriented work; the limitednumber of quality higher education institutions and the relatively small number of world-class graduates in selected occupations such as finance, engineering, and accounting; lowmobility of the Chinese workforce within the country; and the high demand for talent fromthe rest of the economy given the fast growing domestic market. As a result, according tothis study, the pool of young engineers actually suitable for work in multinationals in Chinais just 160,000, and for eight other occupations (engineers, finance workers, accountants,quantitative analysts, generalists, life science researchers, doctors, nurses, and support staff),only 3% of the existing pool can be considered for generalist service positions. India alsohas a younger population with 65% of its population being less than 30 years old, whileChina does not have as large a base at the younger level and has a faster ageing populationthan India.39 Discussions with outsourcing firms, both Indian and multinational, indicate thatalthough China has scale, it is not in a position to overtake India in the near future in servicesoutsourcing mainly due to human resource reasons. Other factors that constrain the Chineseoutsourcing industry’s growth are the perceived weakness of China’s intellectual propertyregime which affect the offshoring of sensitive tasks to China, the country’s fragmentedoutsourcing and IT industries, and the lack of an industry association.

Thus, China contends with India mainly in terms of scale. But the two countries do notreally compete that extensively for business segments or markets at present. Their competi-tion is largely limited to the IT outsourcing segment and to non-voice areas like engineeringservices. However, as China invests more in English-language training and India attemptsto move into higher-end and specialized areas where language capabilities may be less of abarrier, it could pose more of a challenge to India.

4.1.2. India versus the Philippines40

The Philippines is the other main competitor for India within Asia. Although the Philippinesdoes not have the kind of scale that India possesses, it has a relatively large human resource

39http://www.sinomedia.net/eurobiz/v200409/outsourcing0409.html (published September 2004), and Farrelland Grant (2005).40Much of the discussion in this section is based on NeoIT reports, AT Kearney reports, and the PhilippinesDepartment of Trade and Industry sources.

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

India and Services Outsourcing in Asia 19

pool. The country has a skilled labor force of 29 million. There are some 350,000 universityor college students and 15,000 technical students graduating each year. There are 70,000IT or computer science graduates, 35,000 engineering graduates, and 100,000 commerce orbusiness administration graduates. There is also a high degree of English proficiency in thePhilippines and a high degree of cultural affinity with the US, thus making it easy to impartforeign accent and technical capabilities and to teach American speech and mannerisms,making it an ideal offshore destination for contact services. The education system is patternedon that in the US and there is a large number of reputed higher education institutions. Thecountry is highly cost competitive with agent costs at 20% of those in the US, contactcenter management costs around half those of the US, and total variable costs being one-third of the US. The country is also strategically located in the ASEAN region, coupledwith good infrastructure, including an expanding domestic telecommunications network,declining cost of internet bandwidth (falling by as much as 70% in the last four years), stablepower supply, and special IT parks and economic zones for outsourcing providers. Thegovernment has played a proactive role in promoting the industry, through tax incentives,provision of infrastructure, and liberal trade and investment policies.

Given these advantages, ITES-BPO services have grown rapidly in the Philippines.From a mere hundred million in revenues in the end 1990s, revenues grew to $2 billionin 2005 and are projected to grow to around $12 billion over the next five years. Annualturnover growth has been over 20% in recent years, according to the Philippines BusinessProcessing Association. In 2005, there were over 1,000 companies engaged in outsourcingin the Philippines, providing employment to over 130,000 workers. Over 90% of exportearnings from services outsourcing are derived from the US market.

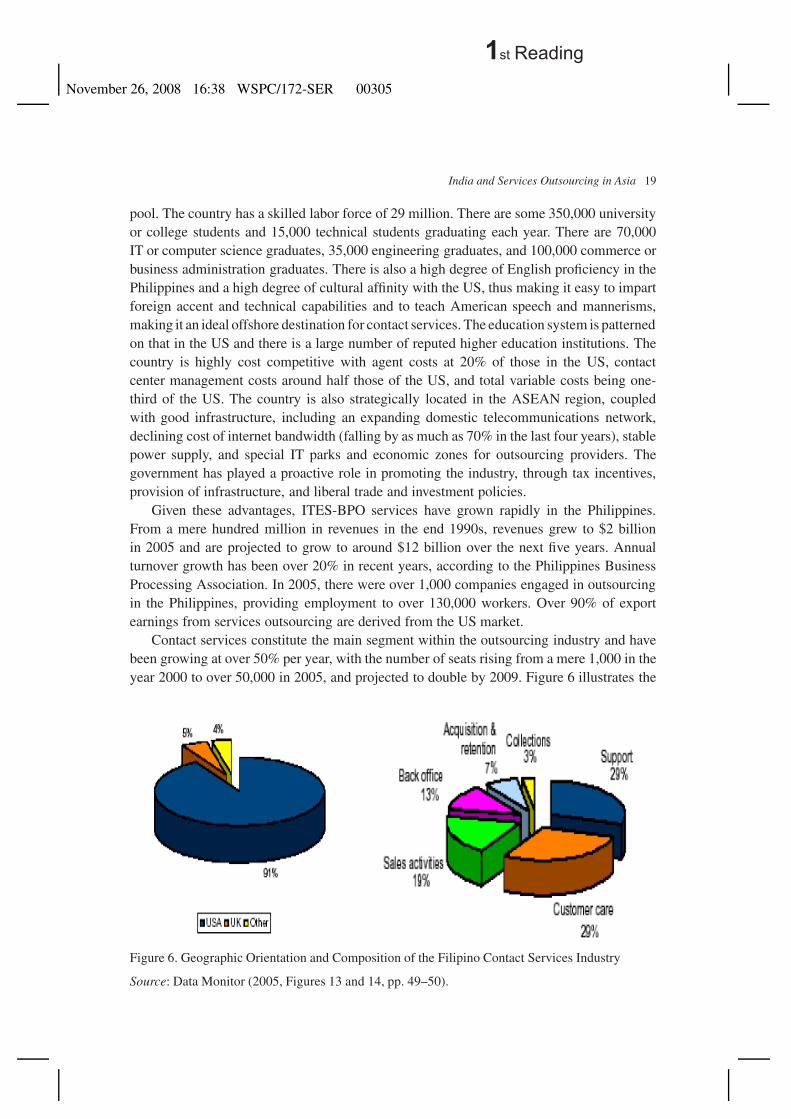

Contact services constitute the main segment within the outsourcing industry and havebeen growing at over 50% per year, with the number of seats rising from a mere 1,000 in theyear 2000 to over 50,000 in 2005, and projected to double by 2009. Figure 6 illustrates the

Figure 6. Geographic Orientation and Composition of the Filipino Contact Services Industry

Source: Data Monitor (2005, Figures 13 and 14, pp. 49–50).

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

20 The Singapore Economic Review

importance of the US for the Filipino contact services outsourcing industry and the variousactivities undertaken within this segment.

The Philippines is known for some other capability areas as well. These include anima-tion; transcription services; data search and conversion services; integration and analysis;engineering and design services; back-office operations like finance; accounting; and humanresources; and core IT services like website, software and applications, development, and sys-tems design. The Philippines has earned a reputation for high-quality animation outsourcing,at 15%–30% lower costs than in client countries.41 The country has a particular advantage inthe area of financial and accountancy services, given its large number and international qual-ity professionals in this area and the presence of the big four global accounting firms (PWC,KPMG, Deloitte, and E&Y) in the country. Some 2,500–3,000 Certified Public Accountantsgraduate per year. The sector adheres to international standards such as GAAP and IAS andfollows accounting norms in the US, Japan, and Europe. More generally, there is affinity withthe US in terms of legal and business practices and work ethics, making it easy for foreignfirms to outsource financial and accounting-related business processes to the Philippines.

Thus, in terms of current content and orientation, the Philippines is a closer competitor toIndia than China. Both India and the Philippines provide offshore services mainly to the USmarket, followed by the UK, given their English language skills. Both are engaged at variouslevels of the value chain within the outsourcing industry, though India has larger volume andvalue of operations at all levels, a much bigger IT outsourcing segment given its mature ITindustry and reputation in software services, and more high-end KPO-type services than thePhilippines. The two countries compete mainly in the call-center segment for US business.But as the CEO of a US-based multinational noted, the Philippines is oversaturated withcall-center work and has the limitation of being excessively concentrated in Manila, and isnot attractive from a disaster recovery or political stability point of view.

4.1.3. Other Asian countries

Apart from China and the Philippines, the only other country that could be a potentialcompetitor to India is Malaysia. The country has English-speaking manpower, good telecomand IT infrastructure, and government policies which facilitate the setting up of specialIT corridors like Putrajaya and Cyberjaya, for establishment of high-tech companies andoffshore activities. However, it cannot compete with India on scale or labor costs.

Singapore also has a large pool of professional manpower with multilingual capabilities,estimated at about 108,000, who could work in the services outsourcing industry.42 However,Singapore’s labor costs are high and again in terms of scale, its talent pool is not comparableto that of India. Where some of these other Asian countries have an edge over India isphysical infrastructure. Surveys also indicate that countries like Singapore are attractiveoffshore destinations for IP-sensitive operations as they have strong IP legislation, strictenforcement mechanisms, and good litigation procedures in case of data fraud and theft.

41See Department of Trade and Industry (2005).42http://www.ida.gov.sg/idaweb/media/PressRelease_LeadStory_Main.jsp?leadStoryId=L160&versionId=2.

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

India and Services Outsourcing in Asia 21

Some other Asian countries such as Vietnam are in a position to tap into the Japanese andKorean markets — markets that India has not been able to penetrate much due to languagebarriers. Vietnam, however, is so far limited to low-end transactional work. Other countries inSouth Asia have several limitations. Sri Lanka is a potential offshore location in this region,but it lacks scale and is limited to the Colombo area. Bangladesh has English languagecapabilities and scale but has problems of disaster recovery, political instability, and poorinfrastructure. According to the CEO of one US-based multinational, Pakistan is potentiallya good offshore destination, but is unattractive due to political instability.

4.1.4. Comparative aspects between India and other countries in services outsourcing

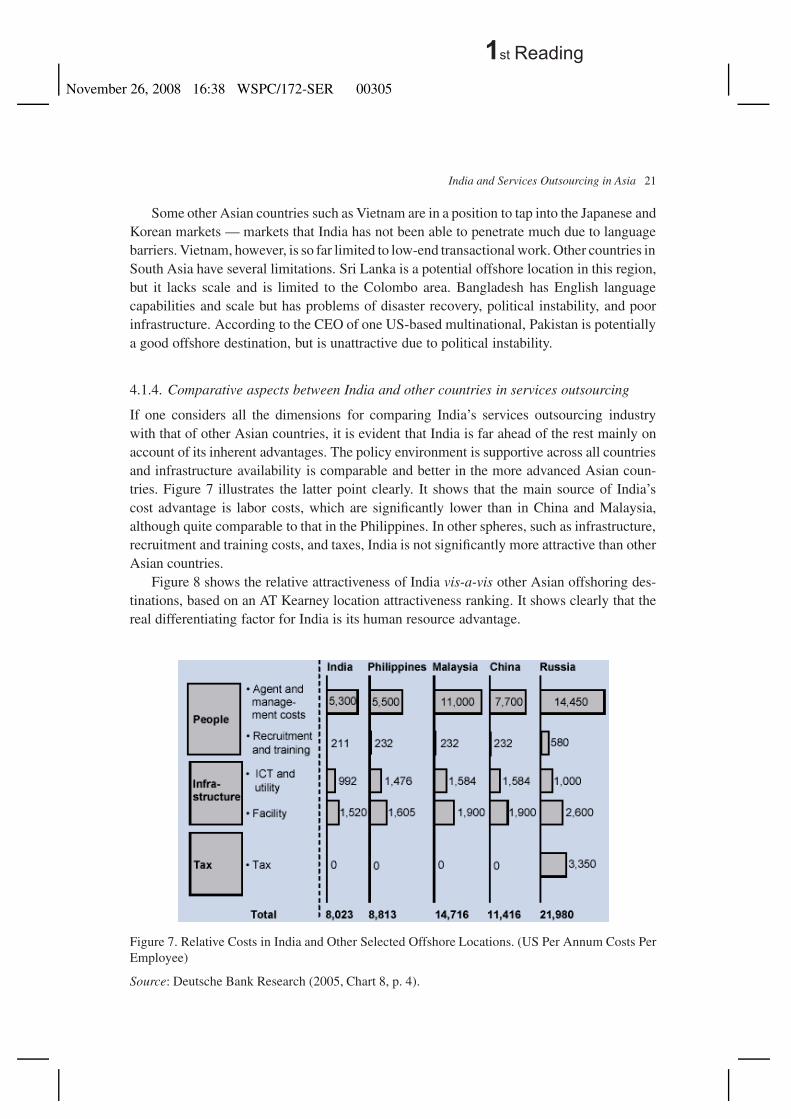

If one considers all the dimensions for comparing India’s services outsourcing industrywith that of other Asian countries, it is evident that India is far ahead of the rest mainly onaccount of its inherent advantages. The policy environment is supportive across all countriesand infrastructure availability is comparable and better in the more advanced Asian coun-tries. Figure 7 illustrates the latter point clearly. It shows that the main source of India’scost advantage is labor costs, which are significantly lower than in China and Malaysia,although quite comparable to that in the Philippines. In other spheres, such as infrastructure,recruitment and training costs, and taxes, India is not significantly more attractive than otherAsian countries.

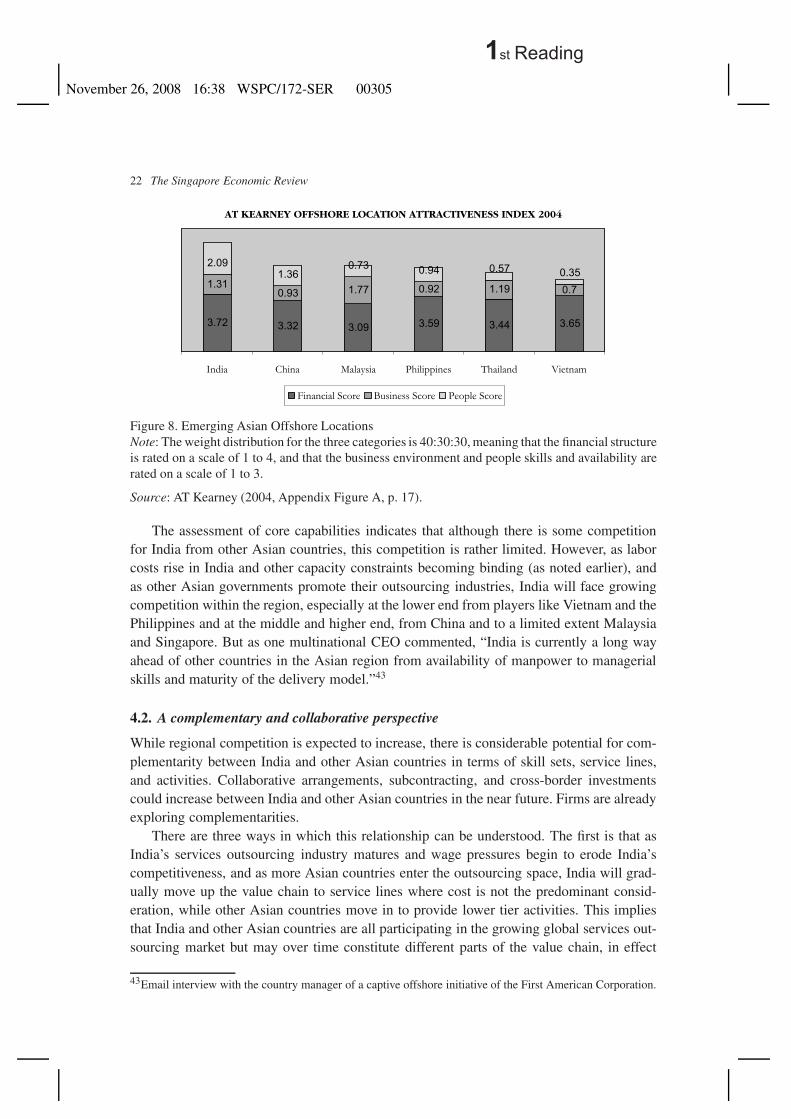

Figure 8 shows the relative attractiveness of India vis-a-vis other Asian offshoring des-tinations, based on an AT Kearney location attractiveness ranking. It shows clearly that thereal differentiating factor for India is its human resource advantage.

Figure 7. Relative Costs in India and Other Selected Offshore Locations. (US Per Annum Costs PerEmployee)

Source: Deutsche Bank Research (2005, Chart 8, p. 4).

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

22 The Singapore Economic Review

AT KEARNEY OFFSHORE LOCATION ATTRACTIVENESS INDEX 2004

3.72 3.32 3.09 3.59 3.44 3.65

0.93 1.77 0.92 1.19 0.7

2.091.36

0.73 0.94 0.57 0.351.31

India China Malaysia Philippines Thailand Vietnam

Financial Score Business Score People Score

Figure 8. Emerging Asian Offshore LocationsNote: The weight distribution for the three categories is 40:30:30, meaning that the financial structureis rated on a scale of 1 to 4, and that the business environment and people skills and availability arerated on a scale of 1 to 3.

Source: AT Kearney (2004, Appendix Figure A, p. 17).

The assessment of core capabilities indicates that although there is some competitionfor India from other Asian countries, this competition is rather limited. However, as laborcosts rise in India and other capacity constraints becoming binding (as noted earlier), andas other Asian governments promote their outsourcing industries, India will face growingcompetition within the region, especially at the lower end from players like Vietnam and thePhilippines and at the middle and higher end, from China and to a limited extent Malaysiaand Singapore. But as one multinational CEO commented, “India is currently a long wayahead of other countries in the Asian region from availability of manpower to managerialskills and maturity of the delivery model.”43

4.2. A complementary and collaborative perspective

While regional competition is expected to increase, there is considerable potential for com-plementarity between India and other Asian countries in terms of skill sets, service lines,and activities. Collaborative arrangements, subcontracting, and cross-border investmentscould increase between India and other Asian countries in the near future. Firms are alreadyexploring complementarities.

There are three ways in which this relationship can be understood. The first is that asIndia’s services outsourcing industry matures and wage pressures begin to erode India’scompetitiveness, and as more Asian countries enter the outsourcing space, India will grad-ually move up the value chain to service lines where cost is not the predominant consid-eration, while other Asian countries move in to provide lower tier activities. This impliesthat India and other Asian countries are all participating in the growing global services out-sourcing market but may over time constitute different parts of the value chain, in effect

43Email interview with the country manager of a captive offshore initiative of the First American Corporation.

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

India and Services Outsourcing in Asia 23

complementing one another regionally to offer a bundle of services to client companies.Discussions with several Indian IT-ITES majors indicate that India itself will play a role increating this segmentation, as all major Indian companies engaged in outsourcing work arelooking at developing global delivery models so as to leverage the advantages of countriesaround the world, in terms of their talent pool, proximity to clients, capabilities, infrastruc-ture, etc. They see themselves as gradually moving up the value chain as this global networkdevelops, with other countries stepping in to provide other parts of the value chain.

The second aspect of this relationship is that Indian firms and outsourcing firms in otherAsian countries fulfill different kinds of needs in the industry and are capable of tappingdifferent markets, skill sets, and competencies. Hence, client companies from the US, Japan,UK, and other important source countries for offshoring business are simultaneously basingtheir operations in India as well as in Asian countries but using these different markets foroffshoring different kinds of service activities, so as to ultimately get access to a wider rangeof offshore services. Along the same lines, Indian companies are also beginning to basesome of their operations in other Asian countries in order to tap new markets, new servicelines, to overcome emerging constraints and skill gaps within the Indian industry, and forother strategic reasons.

The third aspect of the complementary relationship between India and other Asian coun-tries is that firms are entering into cross-border collaborations such as joint ventures andtraining arrangements so as to learn from each other. This is particularly the case betweenIndian and Chinese firms.

Differences in demographic trends between India and other Asian countries will alsocreate opportunities for complementarity in outsourcing. As the latter experience rapidlyageing populations and India’s population remains young and productive over the next fewdecades, services outsourcing by Asian companies in Japan and Korea to India is likely toincrease.

4.2.1. Complementarity in the value chain

Secondary evidence supported by discussions with firms suggest that as India’s services out-sourcing industry matures and develops the capabilities to handle more complex operations,it will progress into more specialized and domain knowledge-intensive services. The growthof segments such as knowledge process outsourcing and engineering services outsourcing(also discussed earlier) is an indication of this transition. In contrast, most of the other Asianoffshoring markets are engaged in lower-end services such as medical transcription, dataentry, and conversion-type services. Even in the IT outsourcing segment, India has beengradually moving up the value chain towards application-oriented and consulting serviceswhere the maturity of its IT industry has played a role. In contrast, other Asian countries pri-marily provide routine software development and maintenance-type services or do not havea sufficiently mature IT industry to enter into IT outsourcing. First-mover advantage of theIndian IT and ITES industry coupled with labor market wage and manpower dynamics forlower-end outsourcing work in India, and growing competition in lower tier work from otherAsian countries, are the main reasons for this value chain segmentation that is emerging.

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

24 The Singapore Economic Review

In several of the firm interviews, CEOs noted that their companies are increasinglyfocusing on high-value work. They also noted that the gradual shift up the value chain ischanging the dynamics of job migration as Indian companies will increasingly move theirlow-end offshore work to emerging low-cost countries within the region, and multinationalswill also offshore more of their lower tier activities to these emerging markets and higher-endwork to India. The discussions, however, revealed that given the lack of scalability in mostother Asian markets, India would still continue to be present in all segments of the valuechain as it would be difficult for multinationals or Indian companies to set up large and easilyscalable operations for lower tier work in these emerging destinations within Asia. Thus,while service line differentiation is increasingly emerging in the future, India will continueto dominate the offshore business on account of the inherent demographic advantages it hasover other locations.

4.2.2. Indian firms exploring complementarities in Asian countries

The majority of evidence seems to support this second form of complementarity as drivingthe relationship between India and other Asian countries in services outsourcing. The bestexample of this relationship is provided by Indian firms which are beginning to outsourceto and setting up offshore subsidiaries in some Asian countries, either to directly provideservices from those bases to their clients or to use these overseas operations as part of a largerglobal or regional strategy. Major Indian firms such as Infosys, Satyam, TCS, Wipro, andHTMT are already engaging with other Asian countries, mainly through the establishment oftheir own subsidiaries and offices in these markets. This is being termed reverse outsourcing,where developing countries like India are outsourcing to other markets.

Indian firms are outsourcing or setting up offices in other Asian countries for variousreasons. They include the need to: (i) enter into new services and markets; (ii) enhance serviceofferings in different languages such as Japanese and Korean; (iii) broaden vertical focus;(iv) exploit near shore opportunities; (v) enlarge the pool of talent and skills available andovercome wage, quality, and attrition pressures in the domestic market; (vi) improve visibilityand marketing through international presence; (vii) ensure a disaster recovery mechanismin case of natural calamities or other emergencies and de-risk their operations; (viii) havea front-end interface for overseas clients in other countries; and (ix) provide services withspecial focus on overseas markets.

The two main markets for regional expansion within Asia are China and the Philippines.For example, Evaluserve, a firm engaged in knowledge process outsourcing, has opened acenter in Shanghai to provide Business Research and Investment Research services withspecial focus on the Chinese and Asian markets for its Western clients. The establishment ofthis center is aimed at helping Evaluserve understand the Chinese market better by enablinglocal interface with Chinese companies and foreign companies working in China, given thestrong interest of many of its clients in the Chinese market. An Evaluserve manager notedthat it is difficult to understand the nuances of overseas markets and keep in touch withdevelopments unless one is physically present in those markets. Likewise, another Indiancompany, HTMT Solutions, has set up a subsidiary in the Philippines as part of its strategy

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

India and Services Outsourcing in Asia 25

to expand its voice business, given the competitive contact services segment in that country.The latter is a case of trying to overcome competitive pressures in the voice business bylocating operations in competing nations like the Philippines and using the resource baseavailable there to grow the company’s business. Spectramind, a subsidiary of one of the bigfour Indian IT-ITES firms, Wipro for has set up a 1,000 person call-center in the formerClark Air Base, north of Manila.44 The aim of the bigger Indian companies is to reorganizeand globalize their operations, which includes a regional component, through establishmentof subsidiaries and acquisition of companies, in order to stay ahead of their nearest rivals,China and the Philippines, by leveraging the capabilities of those markets.

The discussions with management of various outsourcing companies indicated the par-ticular significance of China for Indian companies. Interviews with the management of majorIndian companies like Wipro and TCS revealed that China plays an important role in theirglobal and regional delivery models. China’s significance is because it has scale and enablesIndian companies to expand their global operations, because it enables companies to diver-sify geopolitical risk by diversifying offshoring locations and enables Indian companies toleverage local capabilities to address the regional requirements of multinational clients whohave an interest in the Asia-Pacific and Chinese market, because it helps Indian companiesgain visibility and get additional business from multinationals based in countries like Chinato India as well as tap the growing offshore business available in China from MNCs (whichlocal companies are not yet in a position to capture), and because it enables Indian compa-nies to leverage capabilities in East Asian languages to capture the offshore business fromJapanese and Korean companies.

Some of the interviews also revealed the scope for linking the manufacturing operationsof many Asian companies in China and elsewhere in Asia with the capabilities of some ofthe major Indian outsourcing companies in higher-end services outsourcing like engineeringdesign. The prospects for expanding engineering services outsourcing from companies suchas Fujitsu, Hitachi, and LG, which are good at new product development and also engage incontract manufacturing within the region, were stressed. In this respondent’s view, growingcompetitive pressures on Japanese, Korean, and Taiwanese companies would necessarilyresult in greater offshoring of manufacturing-related support services either directly to Indiaor to Indian companies located in markets like China. Thus, the presence of Indian companiesthrough operations in China could enable them to tap into manufacturing-related servicesoutsourcing activities.

4.2.3. Collaborative arrangements in outsourcing and allied areas45

The presence of complementarities between India and other countries also creates opportu-nities for collaboration and joint ventures, especially between India and China in verticalsrequiring a combination of hardware and software capabilities, as several of the inter-views revealed. For example, it was pointed out that Indian companies can contribute to

44Rudolph (2004, p. 2).45This discussion is mainly based on an Evaluserve presentation.

1st Reading

November 26, 2008 16:38 WSPC/172-SER 00305

26 The Singapore Economic Review

the computer-aided design, computer-aided manufacturing, and embedded systems designfor the Chinese semiconductor, IT, and electronics equipment manufacturing companies.Chinese companies can in turn tap the Indian domestic hardware market. The two countriestogether can exploit other Asia-Pacific markets, such as the North Asian markets, as alreadydiscussed. Indian training companies such as NIIT and Aptech are providing technical train-ing and Indian companies are also providing management training to Chinese professionals.

Huawei technologies, which is a China-based networking company, is a good exampleof a collaborative arrangement between the two countries. The company set up a center inBangalore in 2000 to conduct software research and development work. Around $14 millionworth of projects were outsourced by this center to majors like Infosys and Wipro, amongothers, in 2001. As noted by the Chief Operating Officer of Huawei, the primary reasonfor setting up this center was to leverage the software development skills in India. CDCOutsourcing, which is a unit of Chinadotcom, has a joint venture with vMoksha Technologies,an Indian software firm. The joint venture was set up to strengthen CDC’s outsourcingcapability in Asia and to broaden its IT outsourcing services to global clients, especially in thedeveloped countries, and thus to provide higher-quality, low-cost services. The joint ventureinvolves the use of CDC’s software development capabilities and vMoksha’s relationshipwith global companies. The venture has offshore development centers in Bangalore andShanghai, with marketing offices in customer markets for front-end services.

4.2.4. Role of bilateral and regional agreements

India is increasingly considering regional and bilateral agreements that cover services. Theseagreements could potentially help India in exploiting the complementarities and collabora-tive opportunities in outsourcing discussed above. For example, the Indo-Singapore Com-prehensive Economic Cooperation Agreement (CECA), which came into effect on 1 August2005, is India’s first broad-based agreement, covering goods, services, investment, intellec-tual property rights, and economic cooperation in various areas. The CECA is an integralcomponent of India’s Look East Policy and has implications for bilateral relations in the IT-ITES sector. For example, the CECA has reduced the withholding tax on royalties and feesfor technical services from 15% to 10%, which will benefit Indian IT companies providingservices to Singapore. Several steps have been taken to facilitate the cross-border move-ment of professionals between the two countries, which could have a bearing on outsourcingas temporary movement of service providers is often needed between the client and hostcountry and between offices of a delivery company, to support outsourcing operations. TheCECA is expected to boost the outsourcing of service activities from Singapore to India andthe setting up of subsidiaries by Indian IT-ITES companies in Singapore.46

Interviews with management of various Indian and multinational companies indicatedthree main benefits arising from such bilateral agreements. The first benefit is double taxationavoidance and tax incentives, which helps companies avoid being double-taxed on theirworldwide income. A second benefit is the access to larger resource pools and facilitation of

46See Chanda (2005b).

1st Reading