PwC Tax Panel · BOI Board resolution - 19 Aug and 3 Oct 2014 The BOI under the new chairmanship of...

49

www.pwc.com/th 16 October 2014 Shangri-La Hotel 16th Annual Conference PwC Tax Panel Maximise Shareholder Value through Effective Tax Planning 2015

Transcript of PwC Tax Panel · BOI Board resolution - 19 Aug and 3 Oct 2014 The BOI under the new chairmanship of...

www.pwc.com/th

16 October 2014Shangri-La Hotel

16th Annual Conference

PwC Tax Panel

MaximiseShareholder Valuethrough EffectiveTax Planning 2015

PwC

Agenda

Section 1 - BOI – New Strategy and Investment Policy

Section 2 - Trends in Thai tax policy

2.1 Corporate income tax

2.2 Value added tax

Section 3 - Treasury centres

Slide 216 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

BOI – New Strategy and InvestmentPolicy

Slide 316 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

New BOI’s Structure

NPOC’s Announcement No. 100/2557: Transfer BOI be under thePrime Minister Office, as from 21 July 2014 (formerly under Ministry ofIndustry)

Slide 416 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

BOI Board resolution - 19 Aug and 3 Oct 2014

The BOI under the newchairmanship of the PM wasto implement the NewInvestment PromotionStrategy/Policy as from1 Jan 2015.

Slide 516 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

New Investment Strategy

- Promote investment to restructure Thai economy for

sustainable development and to overcome “Middle Income Trap”

- Promote competitiveness development and value creation ofindustrial sector

- Promote green industry or high technology driven to drive balancedand sustainable growth

- Promote new industrial clusters in the region to create newinvestment concentration

- Promote Thai overseas investment in order to increasecompetitiveness of Thai businesses

Slide 616 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Seven year plan – 2558-2564 (2015-2021)

- To respond to the 11th National Economic and Social DevelopmentPlan and Thailand’s Industrial Development Plan (2555-2559)

“To be more proactive with respect to the ASEAN EconomyCommunity (AEC) in 2015, Thailand needs to comply with itscommitments under various cooperation frameworks andstrengthen its resilience through development of its economic andsocial capital. In all aspects, the powerhouse of the country’s futuredevelopment will comprise knowledge, science, technology,innovation and creativity.”

- To cover the development to the 12th National Economic and SocialDevelopment Plan (2560-2564)

Slide 716 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Promoted Sectors

Sector

Agriculture

Minerals and Ceramics

Light Industry

Metal Products, Machinery andTransportation equipment

Electronics Industry andElectrical Appliances

Chemicals, Paper and Plastics

Services and Public Utilities

Slide 816 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

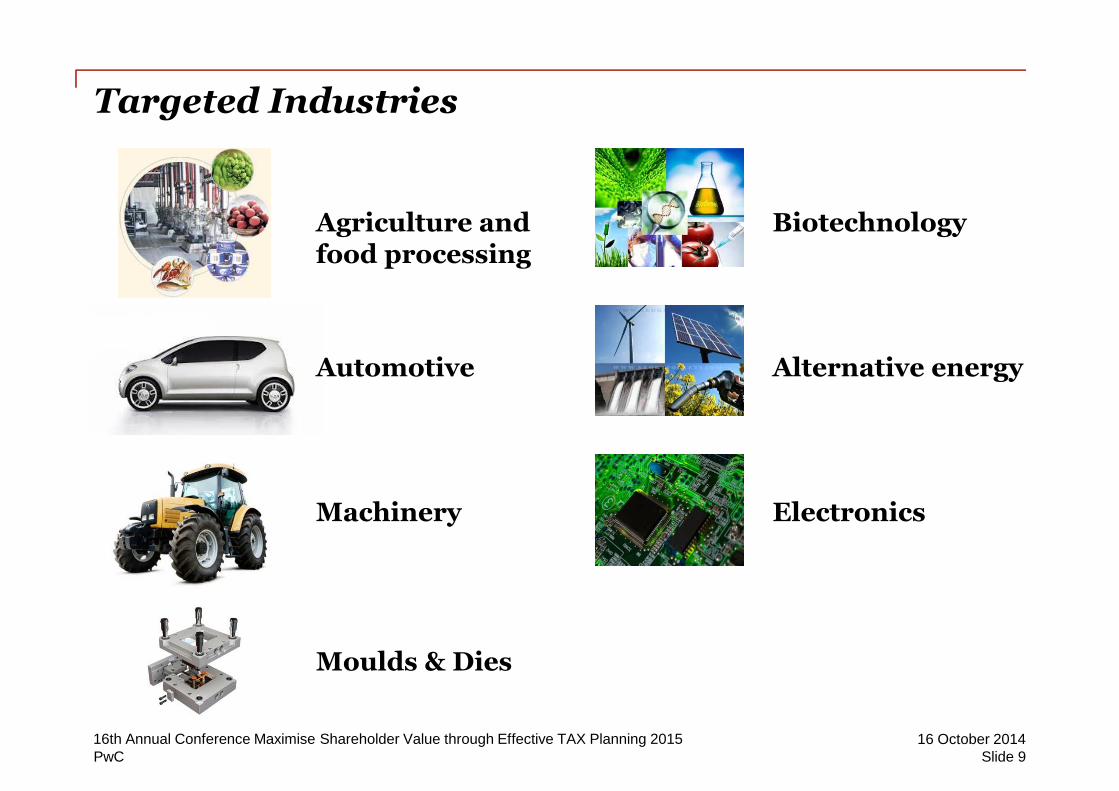

Targeted Industries

Agriculture andfood processing

Automotive

Machinery

Moulds & Dies

Biotechnology

Alternative energy

Electronics

Slide 916 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Remove IndustriesExample

Tea coffee snacks chocolate candy

Plastic packaging/Plastic consumer products

Hand tools and measuring tools

Slide 1016 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Reduce incentivesExample

Petrochemical

Pharmaceutical

Products

Tyres for vehicles

5 years CIT exemption

3 years CIT exemption

Engines forautomobiles

and motorcycles

Slide 1116 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Reasons/Objectives

Remove/Reduce Target

low value added high value added

low technology high technology

low complexity ofproduction process

innovation

environmental problems use of alternative energyand green energy

non-skilled labour intensive skilled labour

Slide 1216 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

New Strategy

“Change”

Broad-based investment promotion

Focused and prioritised investment promotion

(e.g. biotechnology, nanotechnology, advanced materialtechnology)

Slide 1316 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

New Strategy

Focus based Incentives

Activities that are highlyimportant for country’s economicrestructuring in order to stimulateinvestment and to be able tocompete with other countries.

CIT exemption- 8 years with cap/without cap- 5 years with cap- 3 years with cap

Activities that still need to bepromoted but not necessary to begranted CIT exemption.

Import duty exemption onmachinery and raw materials butnot CIT.

A

B

Slide 1416 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

New Strategy

Activity - based incentives

Merit-based incentives

Merit-based incentives

Invest in R&D (whether in-house,cooperation with educational or researchinstitution or donation to Technology andHuman Resources Development Fund)

The number of additional years of CITexemption depends on the percentage of R&Dexpenditure to revenue, e.g.:•1 % of gross sales or not less than 200 millionbaht - one additional year of CIT exemption

Spread the prosperity to the region –located the factory in provinces that have lessper capita income three years - additional ofCIT exemption or 50% CIT reduction for 5years

Projects located within industrialestates/promoted industrial zones - oneadditional year of CIT exemption

Examples

Slide 1516 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

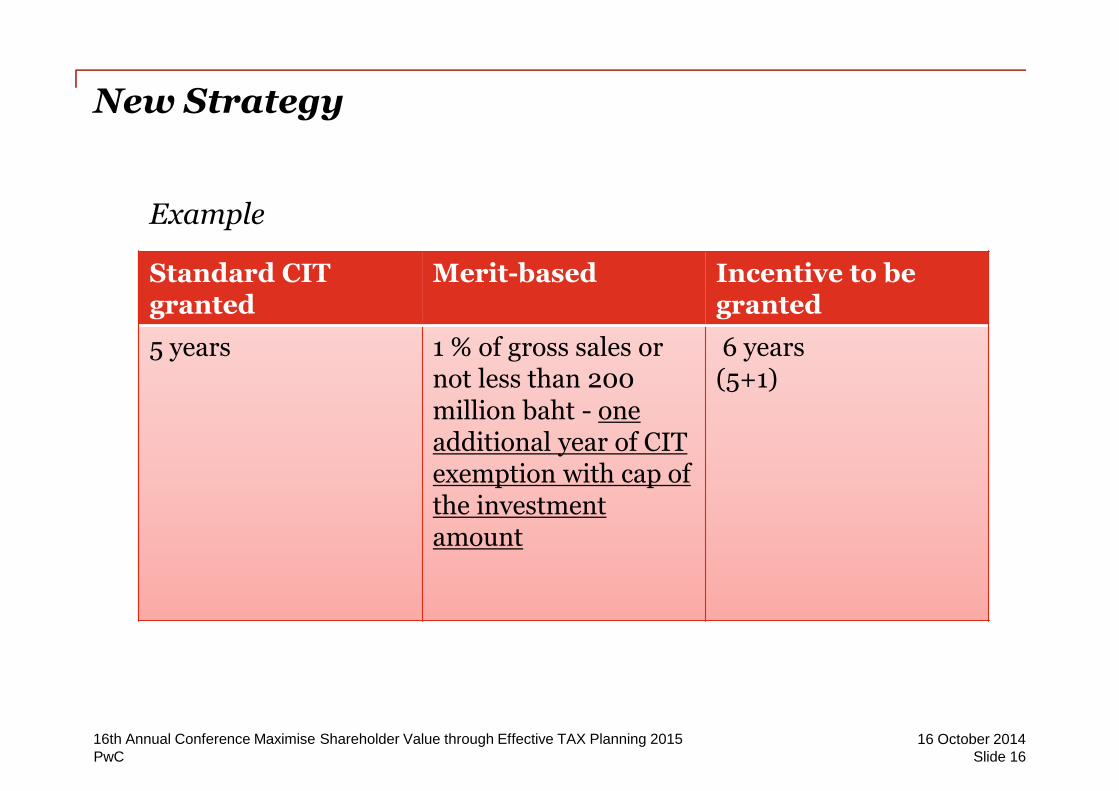

PwC

New Strategy

Standard CITgranted

Merit-based Incentive to begranted

5 years 1 % of gross sales ornot less than 200million baht - oneadditional year of CITexemption with cap ofthe investmentamount

6 years(5+1)

Example

Slide 1616 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

New Strategy

Zone-based investment promotion

New Regional Industrial Clusters

No base on zoning (1-3)

New Industrial Cluster ineach region or border area

- Food processing cluster

- Aerospace cluster

Slide 1716 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

New Strategy

Regulator

Facilitator

Facilitator

One-stop services

Support and facilitation

Reduce barriers

Slide 1816 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

New Strategy

- BOI will promote both inbound and outbound investment

Target countries

No. 1 Indonesia, Myanmar, Vietnam and Cambodia

No. 2 China, India and other ASEAN countries

No. 3 Middle East, South Asia and Africa

Slide 1916 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Trends in Thai tax policy

Slide 2016 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Agenda

Taxes to be reformed

Trends in Thai tax policy

• Corporate income tax

• Value added tax

Slide 2116 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Taxes to be reformed

• Customs duty

• Excise tax

• Inheritance tax

• Property tax

Slide 2216 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Trends in Thai tax policy - corporate income tax

Thailand . . . Overview

30.0%

23.5%

25.0%

35.0%

25.0%

30.0%

17.0%

25.0%

20.0% 20.0% 20.0%

25.0%24.0%

25.0% 25.0%

30.0%

17.0%

22.0%

15%

20%

25%

30%

35%

2010

2011

2012

2013

2014

2010 – 2014 ASEAN corporate income tax (CIT) rates

In 2013-2014, Thailand has the second lowest corporate tax rate in ASEAN whileSingapore is the first.

Slide 2316 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Trends in Thai tax policy - corporate income tax

Withholding tax

CIT 30% WHT 1% for transportation, insurance

2% for commissions

3% for service fees

5% for rental

CIT 20% ?WHT

Example Service fee 100

Profit 10

Tax 30% 3

WHT 3

No refund 0

Service fee 100

Profit 10

Tax 20% 2

WHT 3

Refund 1

Slide 2416 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

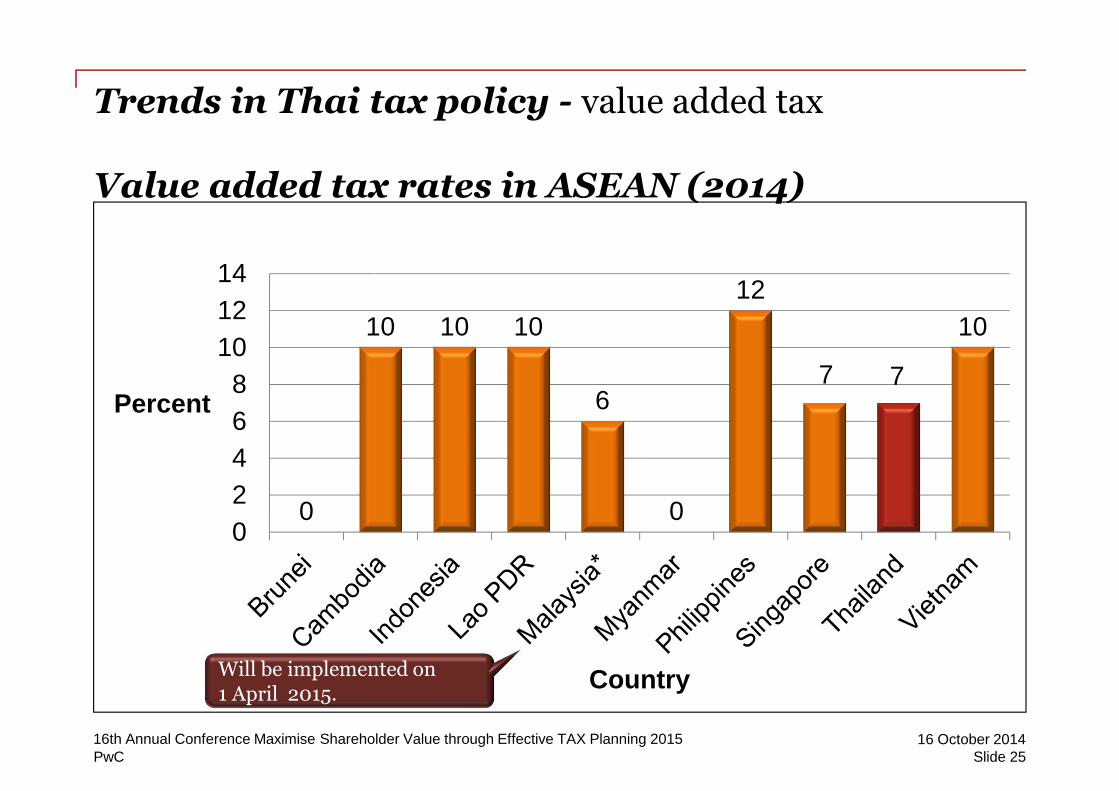

Trends in Thai tax policy - value added tax

Value added tax rates in ASEAN (2014)

0

10 10 10

6

0

12

7 7

10

0

2

4

6

8

10

12

14

Percent

Country

Chart Title

Will be implemented on1 April 2015.

Slide 2516 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Value added tax rates in Thailand and othercountries

8

5

7 7

5

7

0

1

2

3

4

5

6

7

8

9

Japan Nigeria Panama Singapore Taiwan Thailand

Percent

Country

Chart Title

Slide 2616 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Value added tax rates in European Union

20 21

25 24

20 1922

2321

0

5

10

15

20

25

30

Percent

Country

Chart Title

Slide 2716 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Almost all essential goods for living are exemptfrom VAT

Productionfactor (e.g.

fertiliser, fishmeal, animal

feed,pesticide) Animals, meat

(e.g. beef,pork, chicken,shrimp, fish)

Agriculturalproducts (e.g.

rice, corn,vegetablesand fruit)

Newspapers,magazines,textbooks

Governmentlottery, sale of

goods andprovision of

services by thegovernmentAll channels of

domestictransport

(land, sea, air)

Educationalservices ofgovernmentand private

entities

Healing andnursing

services bygovernmentand private

entities

Rental ofhouse/

immovableproperty

Businesseswith income

not exceedingTHB 1.8

million/year

The VAT burden falls moreheavily on middle classand the rich.

VAT VAT

VATThe poor

Slide 2816 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Treasury centres

Slide 2916 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Agenda

Section 3.1 : Treasury centres under Thailand roadmap

Section 3.2 : Treasury centres in Thailand

Section 3.3 : Top countries in Asia for setting up treasury centres

Section 3.4 : Development plan for treasury centres in Thailand

Slide 3016 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Treasury centres under Thailandroadmap

Slide 3116 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Treasury centres under Thailand roadmap

Priority area:

Treasury centre

Slide 3216 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Why dowe need atreasurycentre?

Slide 3316 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Costof funds

Financial

Efficiency

Why do we need a treasury centre?

In-house bank

Company A

Company B

Manage cash flows

Manage foreign exchange risk

Slide 3416 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Treasury centres in Thailand

Slide 3516 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Treasury centres in Thailand

Establishmentof corporate

treasury centres

Only 4 companieshave obtained atreasury centre

license

10 years !!!

2004

2014

Slide 3616 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Obstacles

Slide 3716 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Top countries in Asia for setting uptreasury centres

Slide 3816 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Top countries in Asia for setting up treasury centres

Tax package (10% CIT for 5-10 years,

WHT exemption)

Strong banking network

Wide DTA network

No tax on outbound activities

Proximity to China

Strong banking network

Newly-launched tax package

(70% income exemption for 5 years,

WHT exemption)

Islamic financial hub

Slide 3916 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Development plan for treasurycentres in Thailand

Slide 4016 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Development plan for treasury centres in Thailand

Cash pooling

Netting

Hedging

Slide 4116 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Should cash leakagebe solved with WHT

exemption?

Cash pooling

WHT refundable

SBT exemption

1% WHT on gross interest

Which rate shouldbe reasonable?

Interestrate

Should regulationson SBT exemption

be revised?

3

USD 300 loan

1

Company B

2

Company A

Slide 4216 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

ROH

Interest incomefrom relending is

subject to 10% CITunder ROH

Issue onmaintaining 50%

foreign service androyalty income

threshold

ROH

Disqualified!!!

Slide 4316 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Netting

Company A

Export of goods USD 100

1

Company B

Company C

USD 100

Slide 4416 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Hedging

• Revaluation of forward contract under Paw 68

• Allowing use of “mid rate”

Revaluation ofFX assets and

liabilities

• At the rate of 0.011%

SBT on

FX gains/

derivatives

Slide 4516 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

How to achieve goal?

CashPooling

Netting

Hedging

• Interest rate on relending

• WHT exemption

• SBT exemption on interest

• Netting / tax coupon

• Mid rate for FX translation

CITincentives

CITincentives

CITincentives

Slide 4616 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC Slide 4716 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

PwC

Contact

Peerapat PoshyanondaPartnerTel. +66 (0) 2344 [email protected]

Siripong SupakijjanusornPartnerTel. +66 (0) 2344 [email protected]

Somboon WeerawutiwongPartnerTel: +66 (0) 2344 [email protected]

Orawan FongasiraAssociate PartnerTel. +66 (0) 2344 [email protected]

Slide 4816 October 201416th Annual Conference Maximise Shareholder Value through Effective TAX Planning 2015

Thank you

© 2014 PricewaterhouseCoopers Legal & Tax Consultants Ltd. All rights reserved.'PricewaterhouseCoopers' and/or 'PwC' refers to the individual members of thePricewaterhouseCoopers organisation in Thailand, each of which is a separate andindependent legal entity. Please see www.pwc.com/structure for further details.