Presentation: Global Trade in Services: Fear, Facts, and ... Trade in Services: Fear, Facts, and ......

57

Global Trade in Services: Global Trade in Services: Fear, Facts, and Offshoring Fear, Facts, and Offshoring J. Bradford Jensen J. Bradford Jensen McDonough School of Business, Georgetown University McDonough School of Business, Georgetown University Peterson Institute for International Economics Peterson Institute for International Economics Peterson Institute for International Economics Peterson Institute for International Economics Georgetown Center for Business and Public Policy Georgetown Center for Business and Public Policy NBER NBER Otb 18 2011 Otb 18 2011 October 18, 2011 October 18, 2011

Transcript of Presentation: Global Trade in Services: Fear, Facts, and ... Trade in Services: Fear, Facts, and ......

Global Trade in Services: Global Trade in Services: Fear, Facts, and OffshoringFear, Facts, and Offshoring

J. Bradford JensenJ. Bradford Jensen

McDonough School of Business, Georgetown UniversityMcDonough School of Business, Georgetown University

Peterson Institute for International EconomicsPeterson Institute for International EconomicsPeterson Institute for International EconomicsPeterson Institute for International Economics

Georgetown Center for Business and Public Policy Georgetown Center for Business and Public Policy

NBERNBER

O t b 18 2011O t b 18 2011October 18, 2011October 18, 2011

Why?

Retail trade12%

Transportation and warehousing

3%

Wholesale trade5%

Manufacturing10%

Services50%

Mining0%

Utilities0%

Construction5%

0%

Federal Government2%

State and Local Government12%

Source: 2007 Economic Census, Census of Governments and 2006 Occupational Employment Survey

Why?

Retail trade12%

Transportation and warehousing

3%

Business Services25%

Wholesale trade5%

$56,000$56,000

Manufacturing10%

$46,000$46,000

Construction5%

Utilities0% Mining & Ag. Personal Services

Federal Government2%

State and Local Government12%

0%1%

Personal Services25%

Source: 2007 Economic Census, Census of Governments and 2006 Occupational Employment Survey

Why?

NAICS Code SectorEmployment

2007

Share of Total Employment

2007

Employment Growth

1997-200721 Mining 703 129 0 5% 38%21 Mining 703,129 0.5% 38%22 Utilities 632,432 0.5% -10%23 Construction 7,399,047 5.5% 31%31-33 Manufacturing 13,333,390 9.9% -21%42 Wholesale trade 6,295,109 4.7% 9%44-45 Retail trade 15,610,710 11.5% 12%48-49 Transportation and warehousing 4,435,760 3.3% 52%51-56 Business Services 33,430,809 24.7% 29%

51 Information 3,428,262 2.5% 12%52 Finance and insurance 6,562,546 4.9% 12%53 Real estate and rental and leasing 2,249,353 1.7% 32%54 Professional scientific and technical services 8 121 171 6 0% 51%54 Professional, scientific, and technical services 8,121,171 6.0% 51%55 Management of companies and enterprises 2,915,644 2.2% 11%56 Administrative and support and waste remediation services 10,153,833 7.5% 38%

61-81 Personal Services 34,595,857 25.6% 23%61 Educational services 562,210 0.4% 75%62 Health care and social assistance 16,859,513 12.5% 24%71 Arts entertainment and recreation 2 070 524 1 5% 30%71 Arts, entertainment, and recreation 2,070,524 1.5% 30%72 Accommodation and food services 11,587,814 8.6% 23%81 Other services (except public administration) 3,515,796 2.6% 8%

Federal Government 2,462,000 1.8% --State and Local Government 16,400,000 12.1% --

S U S CSource: U.S. Census Bureau

What is Trade in Services?What is Trade in Services?

• Modes of service trade:

• Mode 1 – Cross‐border provision, e.g. software produced in one region and shipped via internet to another region

• Mode 2 – Consumption abroad, e.g. consumer travels to resort to consume service

• Mode 3 – Commercial presence in foreign region, e.g. restaurant opens local branch to serve foreign demand

• Mode 4 – Temporary movement of natural persons, e.g. consultant travels to customer to deliver services

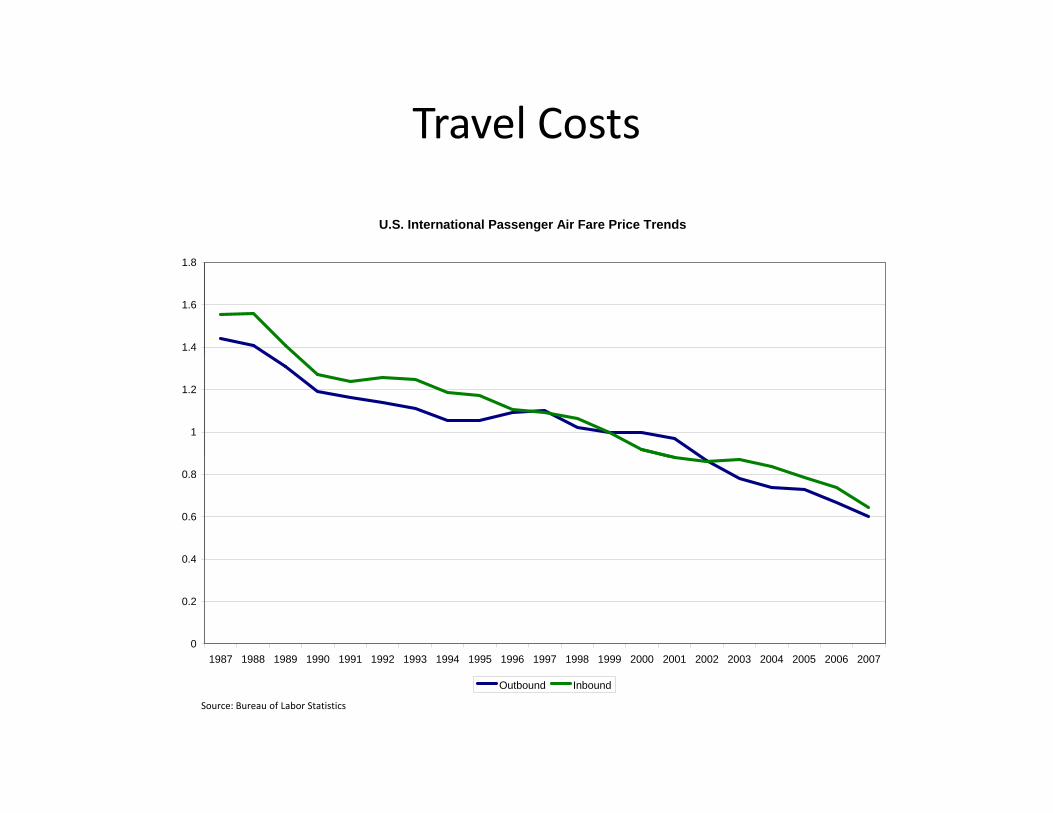

Travel Costs

U.S. International Passenger Air Fare Price Trends

1.4

1.6

1.8

1

1.2

0 4

0.6

0.8

0

0.2

0.4

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Outbound Inbound

Source: Bureau of Labor Statistics

Telecommunication CostsInternational Switched Services

Average Revenue per Minute

$1 00

$1.20

$0 60

$0.80

$1.00

$0 20

$0.40

$0.60

$0.00

$0.20

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Source: International Telecommunications Data, FCC, June 2009100

120

2 km

50 km

Index 1992 =100

Trends in leased line pricing (2 Mbits)

40

60

80

50 km

200 km

Source: OECD

0

20

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Internet Usage

Region Population Internet Users 2009 Penetration User Growth (2000-2009)Africa 975,330,899 54,171,500 6% 1100%Asia 3,780,819,792 657,170,816 17% 475%

World Internet Usage and Population Statistics

Europe 803,903,540 393,373,398 49% 274%Middle East 196,767,614 45,861,346 23% 1296%North America 337,572,949 251,290,489 74% 133%Latin America/Caribbean 581,249,892 173,619,140 30% 861%Oceania / Australia 34,384,384 20,783,419 60% 173%WORLD TOTAL 6 710 029 070 1 596 270 108 24% 342%WORLD TOTAL 6,710,029,070 1,596,270,108 24% 342%

Source: www.internetworldstats.com

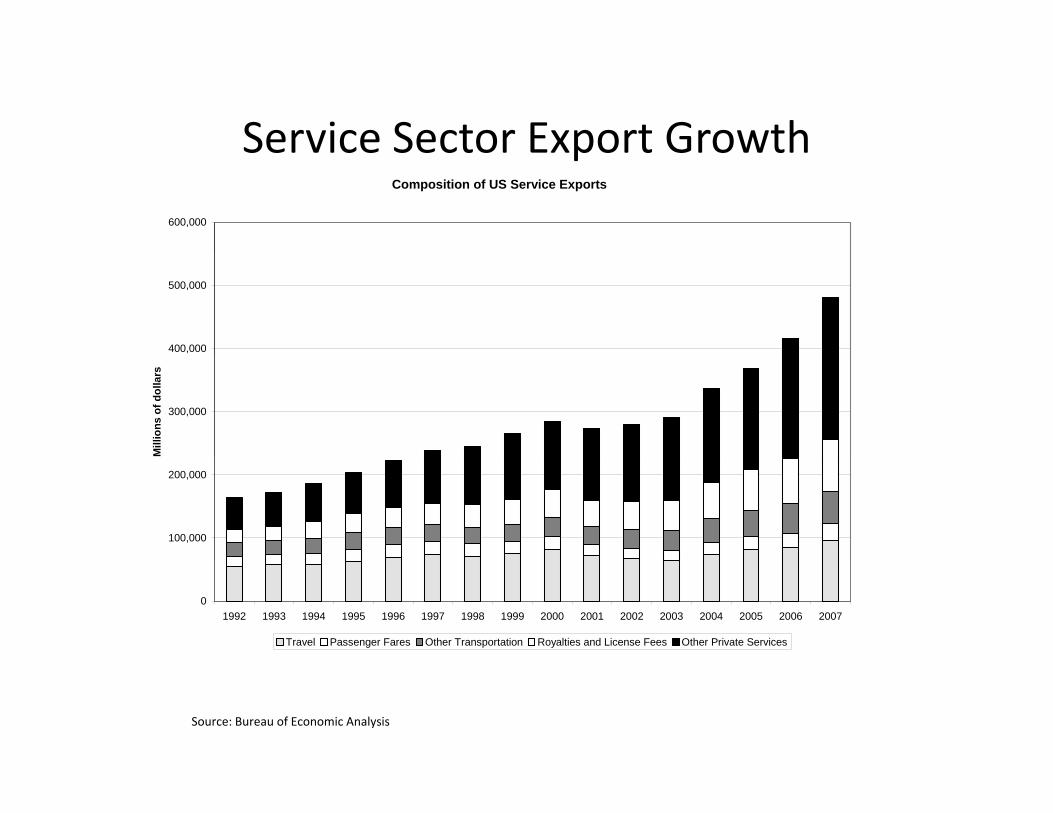

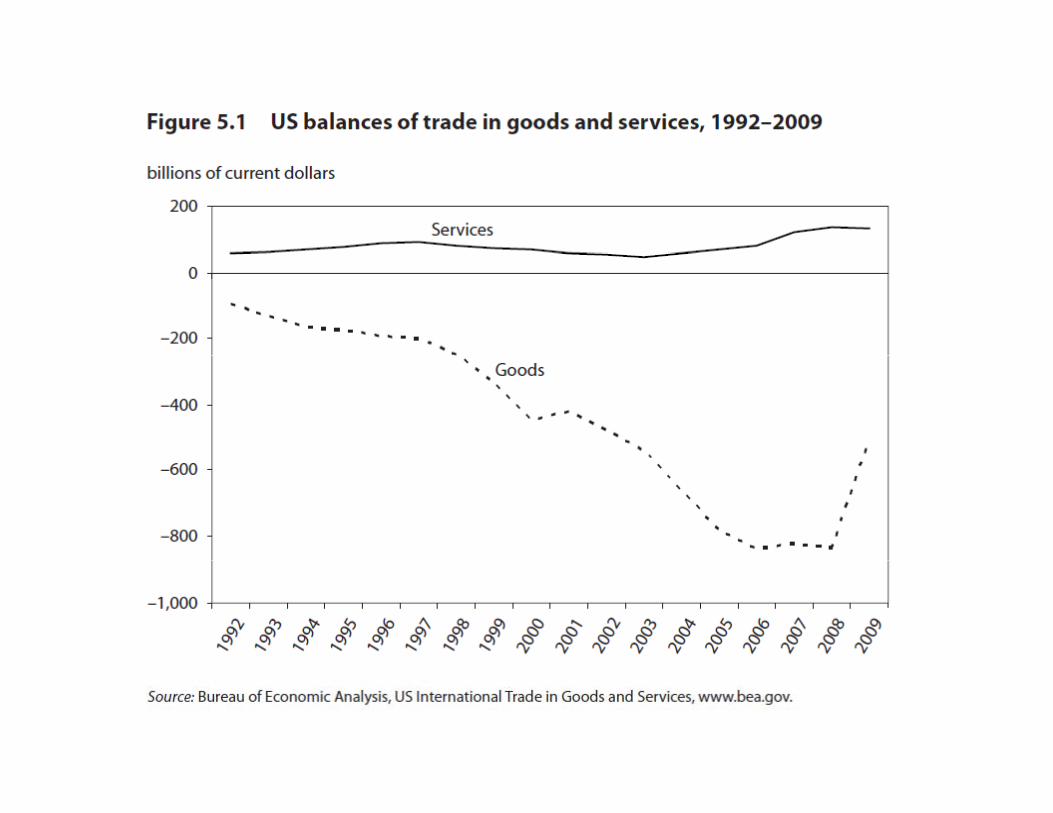

Service Sector Export GrowthService Sector Export GrowthComposition of US Service Exports

600,000

400,000

500,000

300,000

Mill

ions

of d

olla

rs

100,000

200,000

01992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Travel Passenger Fares Other Transportation Royalties and License Fees Other Private Services

Source: Bureau of Economic Analysis

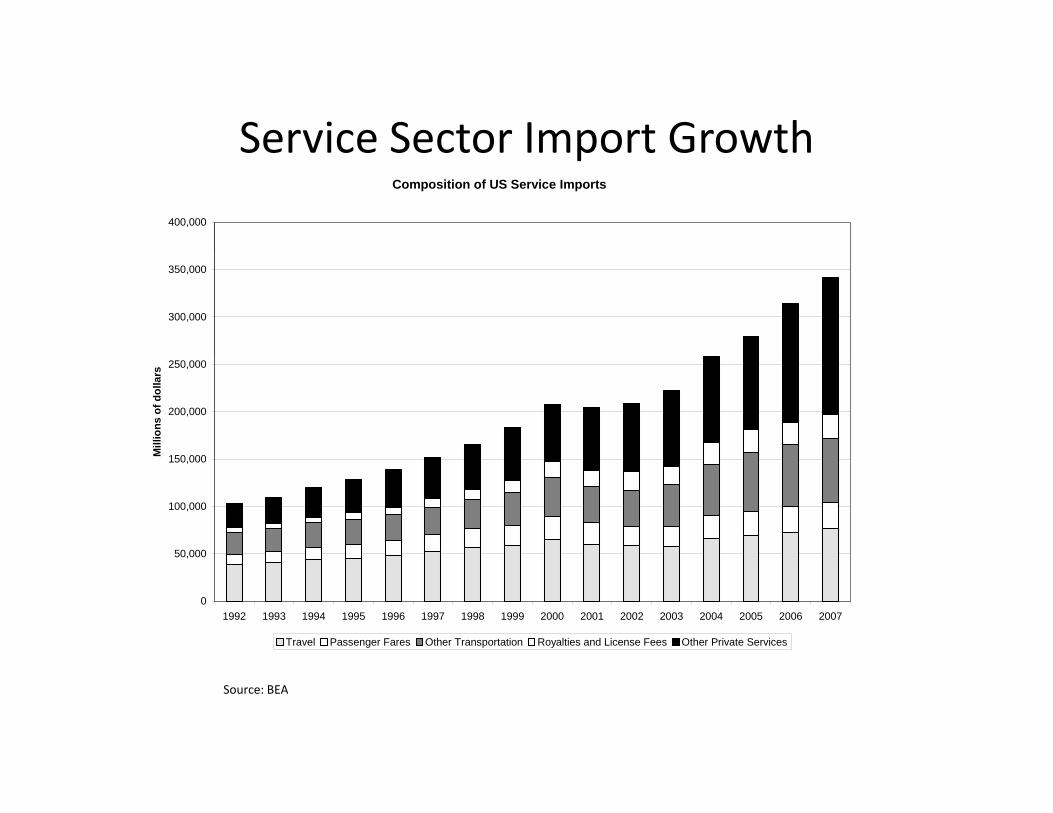

Service Sector Import GrowthService Sector Import GrowthComposition of US Service Imports

400,000

300,000

350,000

150 000

200,000

250,000

Mill

ions

of d

olla

rs

50,000

100,000

150,000

01992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Travel Passenger Fares Other Transportation Royalties and License Fees Other Private Services

Source: BEA

A closer look

2006Travel 2 ……………………………………………………………………Passenger fares 3 …………………………………………………………Other transportation……………………………………………………..Royalties and license fees………………………………………………Other private services 4 15………………………………………………

Education 5………………………………………………………………16Financial services 16……………………………………………………

Insurance services 6 ……………………………………………………Telecommunications 7…………………………………………………Business, professional, and technical services 16…………………

Computer and information services 8 16……………………………Management and consulting services 9Management and consulting services ……………………………Research and development and testing services 9………………Operational leasing 16…………………………………………………Other business, professional, and technical services 10 16………

Accounting, auditing, and bookkeeping services……………….Advertising……………………………………………………………

Data AvailableArchitectural, engineering, and other technical services………Construction …………………………………………………………Industrial engineering………………………………………………Installation, maintenance, and repair of equipment……………Legal services………………………………………………………

11Medical services 11…………………………………………………Mining 12………………………………………………………………Sports and performing arts…………………………………………Trade-related services 13……………………………………………Training services……………………………………………………Other 14Other …………...

Other services………………………………………………………….Film and television tape rentals……………………………………

Other…………………………………………………………………

2001Travel 2 ……………………………………………………………………

Data AvailablePassenger fares 3 ………………………………………………………Other transportation……………………………………………………..Royalties and license fees………………………………………………Other private services 4 15………………………………………………

Education 5………………………………………………………………16Financial services 16……………………………………………………

Insurance services 6 ……………………………………………………Telecommunications 7…………………………………………………Business, professional, and technical services 16…………………

Computer and information services 8 16……………………………Management and consulting services 9Management and consulting services ……………………………Research and development and testing services 9………………Operational leasing 16…………………………………………………Other business, professional, and technical services 10 16………Data Available

11Medical services 11…………………………………………………

Other services………………………………………………………….Film and television tape rentals……………………………………

Other…………………………………………………………………

1997Travel 2 ………………………………………………………………

Data AvailablePassenger fares 3 …………………………………………………Other transportation………………………………………………Royalties and license fees…………………………………………Other private services 4 15…………………………………………

Education 5…………………………………………………………16Financial services 16………………………………………………

Insurance services 6 ……………………………………………Telecommunications 7……………………………………………Business, professional, and technical services 16……………

Computer and information services 8 16………………………

Operational leasing 16…………………………………………Other business, professional, and technical services 10 16…Data Available

11Medical services 11……………………………………………

Other services……………………………………………………Film and television tape rentals………………………………

Other……………………………………………………………

1992Travel 2 ………………………………

Data AvailablePassenger fares 3 ……………………Other transportation…………………Royalties and license fees…………Other private services 4 15…………

Education 5…………………………

Insurance services 6 ………………Telecommunications 7……………

…

Data Available

11Medical services 11………………..

Other services………………………Film and television tape rentals

Other……………………………

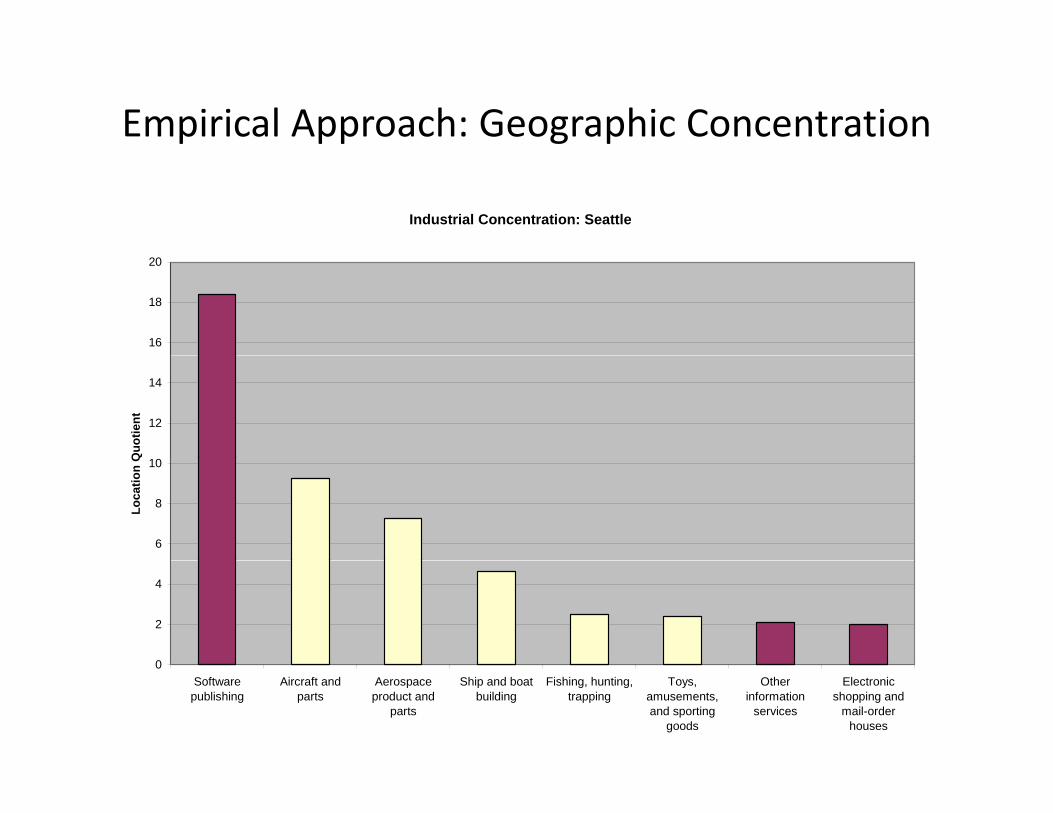

A new approach

Empirical Approach: Geographic Concentration

Industrial Concentration: Seattle

16

18

20

12

14

Quo

tient

6

8

10

Loca

tion

Q

0

2

4

0Aircraft and

partsAerospaceproduct and

parts

Ship and boatbuilding

Fishing, hunting,trapping

Toys,amusements,and sporting

goods

Empirical Approach: Geographic Concentration

Industrial Concentration: Seattle

16

18

20

12

14

Quo

tient

6

8

10

Loca

tion

Q

0

2

4

0Softwarepublishing

Aircraft andparts

Aerospaceproduct and

parts

Ship and boatbuilding

Fishing, hunting,trapping

Toys,amusements,and sporting

goods

Otherinformation

services

Electronicshopping and

mail-orderhouses

Geographic Concentration of Industries

Geographic Concentration of Industries

0.7

0.8

0.9

Mfg EMP –86% T

Ag/Min EMP –100% T

0.5

0.6

Coe

ffici

ent

Bus Svc EMP –70% Tradable

100% T

0.2

0.3

0.4

Gin

i C

Ed/Health EMP –98% N‐TOth Svc EMP –80% N‐T

0

0.1

0 100 200 300 400 500 600 700 800 900 1000

NAICS Industry

Ag Mining Utilities Construction Manufacturing Wholesale Retail Transportation Services Public Admin

Source: Jensen and Kletzer (2006)

Geographic Concentration of Occupations

Geographic Concentration of Occupations

0.7

0.8

0.5

0.6

ffici

ent

Comp/Math EMP –100% T

Scientific EMP –84% T

0 2

0.3

0.4

Gin

i Coe

f

Social Svc/Ed EMP –100% N-T

0

0.1

0.2

010 15 20 25 30 35 40 45 50 55 60

SOC Occupation

High-End Services Other Services Legal Other Services Production Related Military Specific

Mgt, Bus/Fin Ops, Arch/Eng EMP –65% T

Prod EMP – 80% N-T

New insights

Employment Shares for Tradable Industries

Manufacturing10%

Wholesale Trade

Ag, Forest, Fish1%

Retail Trade2%

Trans/Warehouse3%

2%

Business Services14%

Personal Services3%

Public Administration2%

Non-Tradable Industries63%

S A h ’ l l i 2007 A i C i SSource: Author’s calculations, 2007 American Community Survey

Tradable Services are Different

Worker Characteristics for Select Industries

Non-tradable Industry Tradable IndustryNumber of Workers 2,235,432 12,994,490Average Earnings $44,014 $49,952Share with B.A. 16% 24%

Manufacturing (NAICS 30s)

Share with B.A. 16% 24%Share with Advanced Degree 3% 7%Share in Tradable Occupations 26% 34%

Non-tradable Industry Tradable IndustryProfessional Services (NAICS 50s)

Non tradable Industry Tradable IndustryNumber of Workers 8,038,246 18,430,199Average Earnings $42,226 $66,454Share with B.A. 29% 50%Share with Advanced Degree 7% 17%Share in Tradable Occupations 31% 60%pSource: Author's calculations, 2007 American Community Survey

Source: Author’s calculations, 2007 American Community Survey

Tradable Services are Different

25%

Average Earnings Differentialswith Demographic, Industry, and Occupation Group Controls

20%

15%

5%

10%

0%All Workers Prof. Service Industries High-End Service Occupations

Non-tradable Industry, Tradable Occupation Tradable Industry, Non-tradable Occupation Tradable Industry, Tradable Occupation

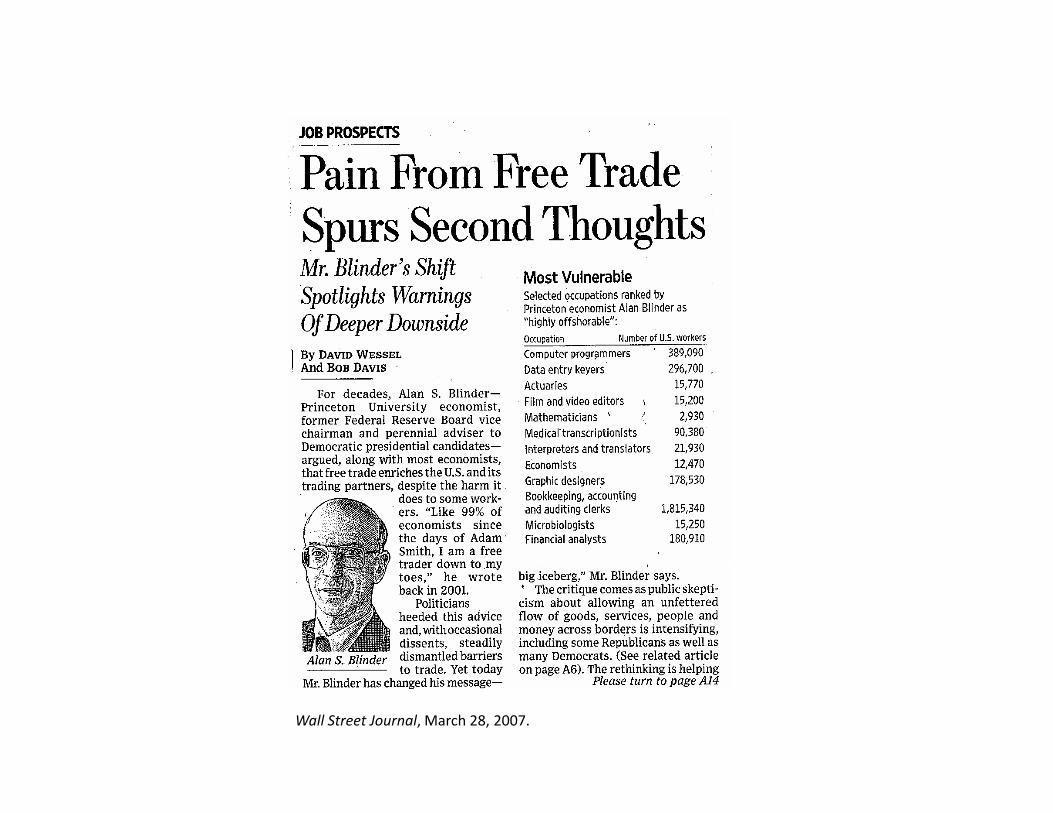

Cause for concern?

Wall Street Journal, March 28, 2007.

Factor Abundance: Education

Average Educational Attainment, 1985 Select Countries

12

14

U.S.

Australia, Canada

8

10

Year

s

Japan, Germany, U.K., Netherlands, BelgiumSouth Korea

Italy, France

4

6

China

India

IndonesiaBrazil

Mexico

0

2

0 5000 10000 15000 20000

GDP per Capita

Source: Educational Attainment, Barro and Lee and GDP per Capita, Penn World Tables v. 5

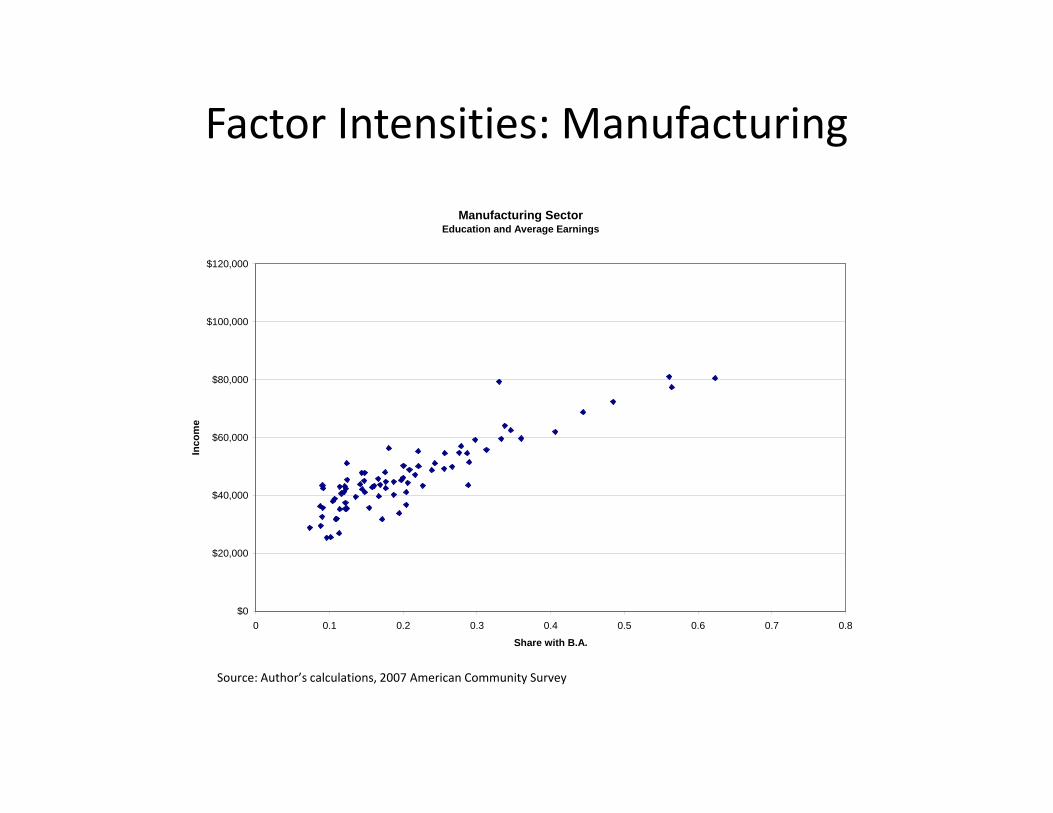

Factor Intensities: Manufacturing

Manufacturing Sector

Education and Average Earnings

$100,000

$120,000

$60,000

$80,000

Inco

me

$20,000

$40,000

$00 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8

Share with B.A.

Source: Author’s calculations, 2007 American Community Survey

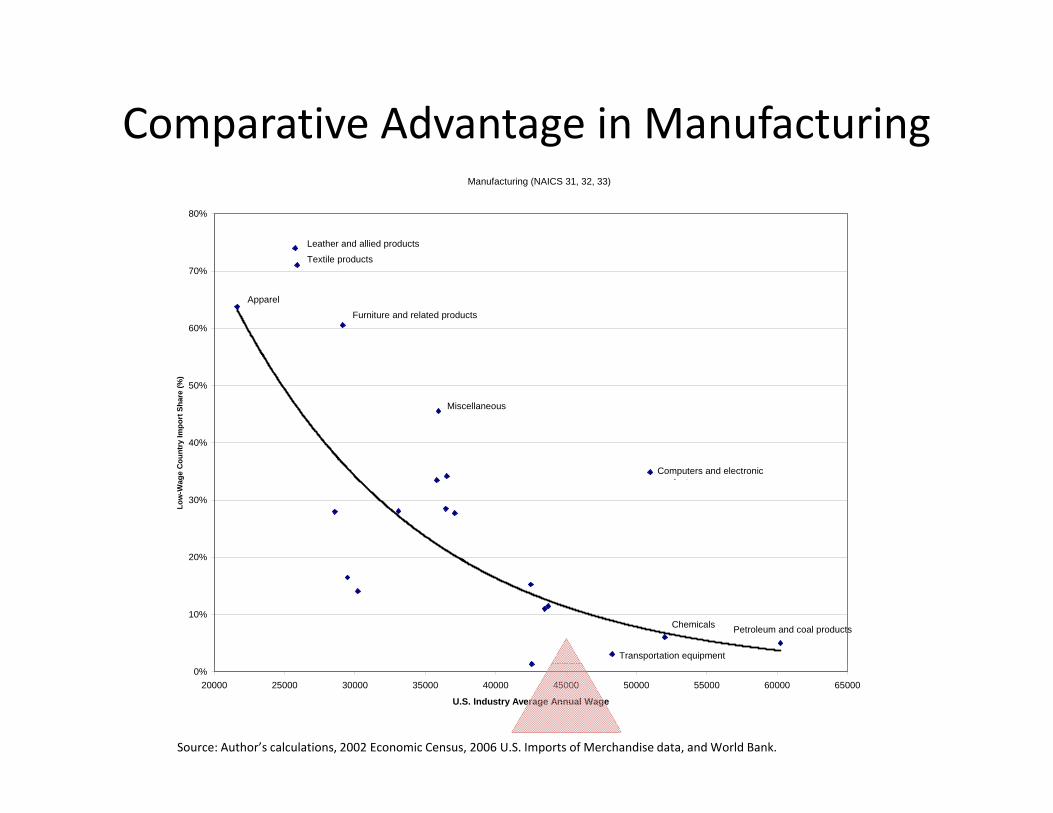

Comparative Advantage in Manufacturing

Manufacturing (NAICS 31, 32, 33)

80%

Leather and allied products

60%

70%Textile products

Apparel

Furniture and related products

40%

50%

untr

y Im

port

Sha

re (%

)

Miscellaneous

20%

30%

Low

-Wag

e C

ou

Computers and electronic d t

10%Petroleum and coal productsChemicals

Transportation equipment

0%20000 25000 30000 35000 40000 45000 50000 55000 60000 65000

U.S. Industry Average Annual Wage

Source: Author’s calculations, 2002 Economic Census, 2006 U.S. Imports of Merchandise data, and World Bank.

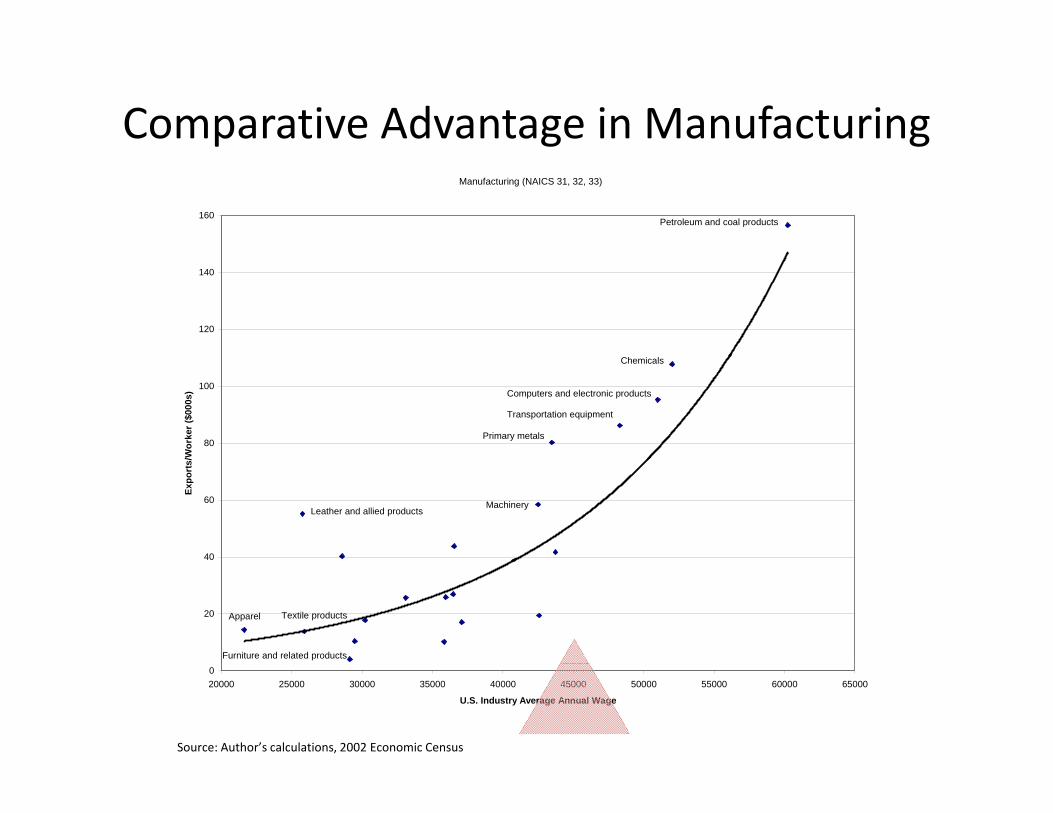

Comparative Advantage in Manufacturing

Manufacturing (NAICS 31, 32, 33)

160Petroleum and coal products

120

140

80

100

/Wor

ker (

$000

s)

Chemicals

Computers and electronic products

Transportation equipment

Primary metals

40

60

Expo

rts/

MachineryLeather and allied products

20 Textile productsApparel

Furniture and related products020000 25000 30000 35000 40000 45000 50000 55000 60000 65000

U.S. Industry Average Annual Wage

Source: Author’s calculations, 2002 Economic Census

Factor Intensities: Services

Service Sector

Education and Average Earnings

$100,000

$120,000

$60,000

$80,000

ncom

e

$20 000

$40,000

In

$0

$20,000

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8

Share with B.A.

Source: Author’s calculations, 2007 American Community Survey

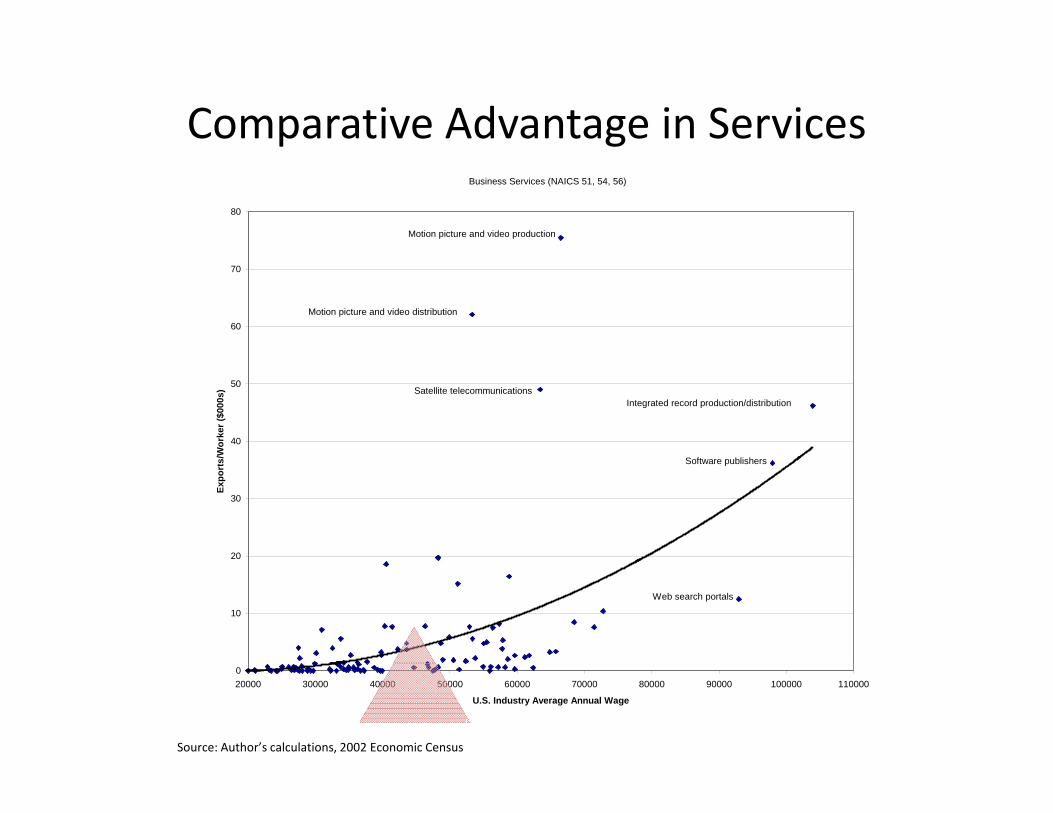

Comparative Advantage in Services

Business Services (NAICS 51, 54, 56)

80

Motion picture and video production

60

70

Motion picture and video distribution

40

50

/Wor

ker (

$000

s)

Integrated record production/distribution

S ft bli h

Satellite telecommunications

20

30

Expo

rts/ Software publishers

10

Web search portals

020000 30000 40000 50000 60000 70000 80000 90000 100000 110000

U.S. Industry Average Annual Wage

Source: Author’s calculations, 2002 Economic Census

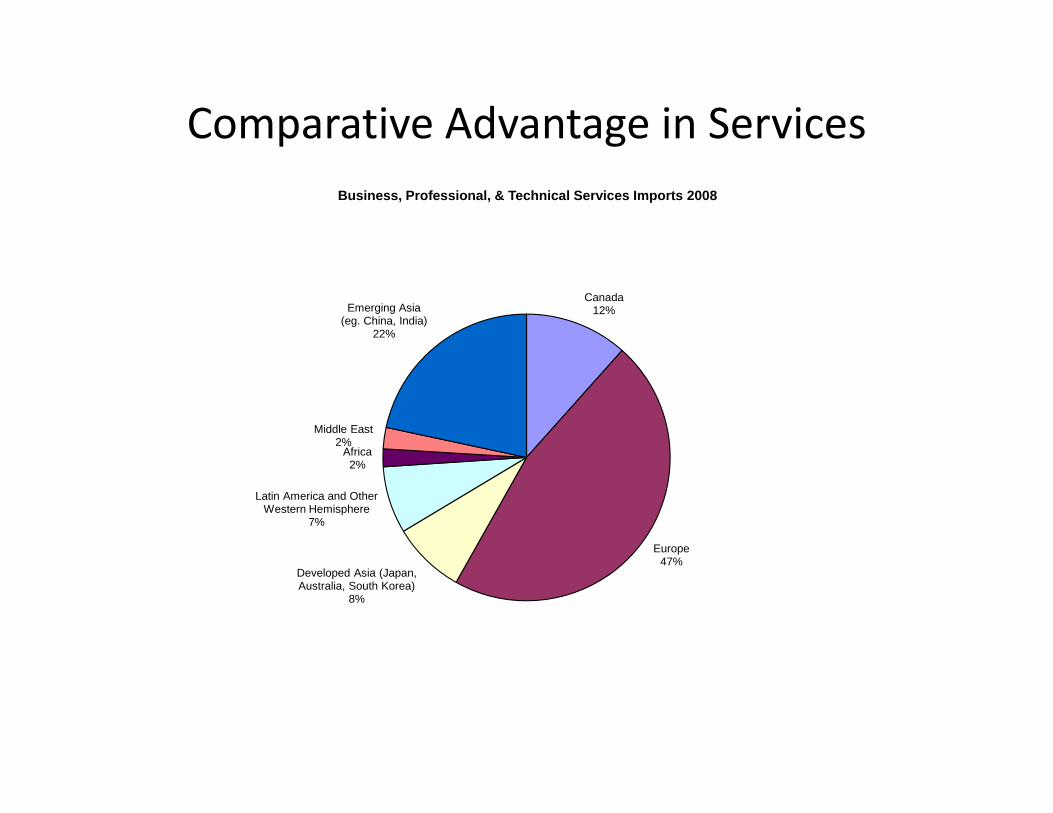

Comparative Advantage in ServicesBusiness, Professional, & Technical Services Imports 2008

Canada12%Emerging Asia

(eg. China, India)22%

Africa

Middle East2%

Europe47%

Latin America and Other Western Hemisphere

7%

2%

47%Developed Asia (Japan, Australia, South Korea)

8%

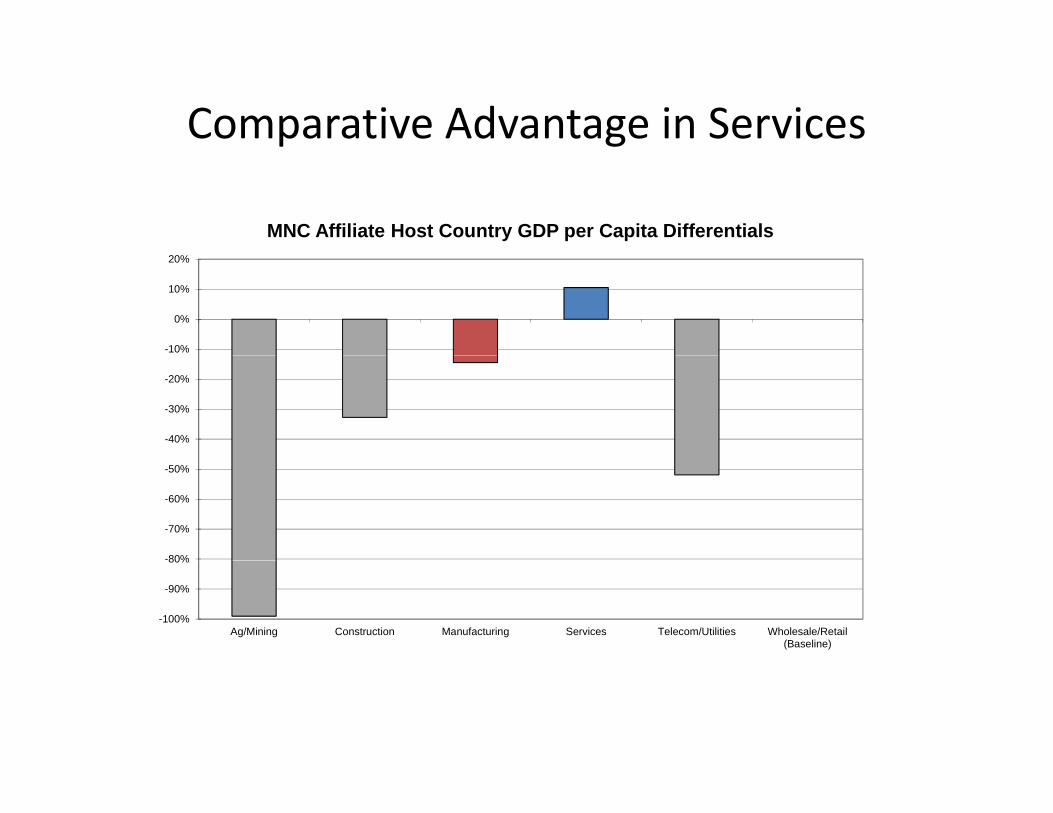

Comparative Advantage in Services

MNC Affiliate Host Country GDP per Capita Differentials

-10%

0%

10%

20%

-40%

-30%

-20%

-80%

-70%

-60%

-50%

-100%

-90%

80%

Ag/Mining Construction Manufacturing Services Telecom/Utilities Wholesale/Retail(Baseline)

Comparative Advantage in Services

50%

GDP per Capita Differences for Vertically Integrated Affiliates

30%

40%

10%

20%

‐10%

0%Manufacturing ‐‐ Vertically Integrated Services ‐‐ Vertically Integrated

‐40%

‐30%

‐20%

‐50%

0%

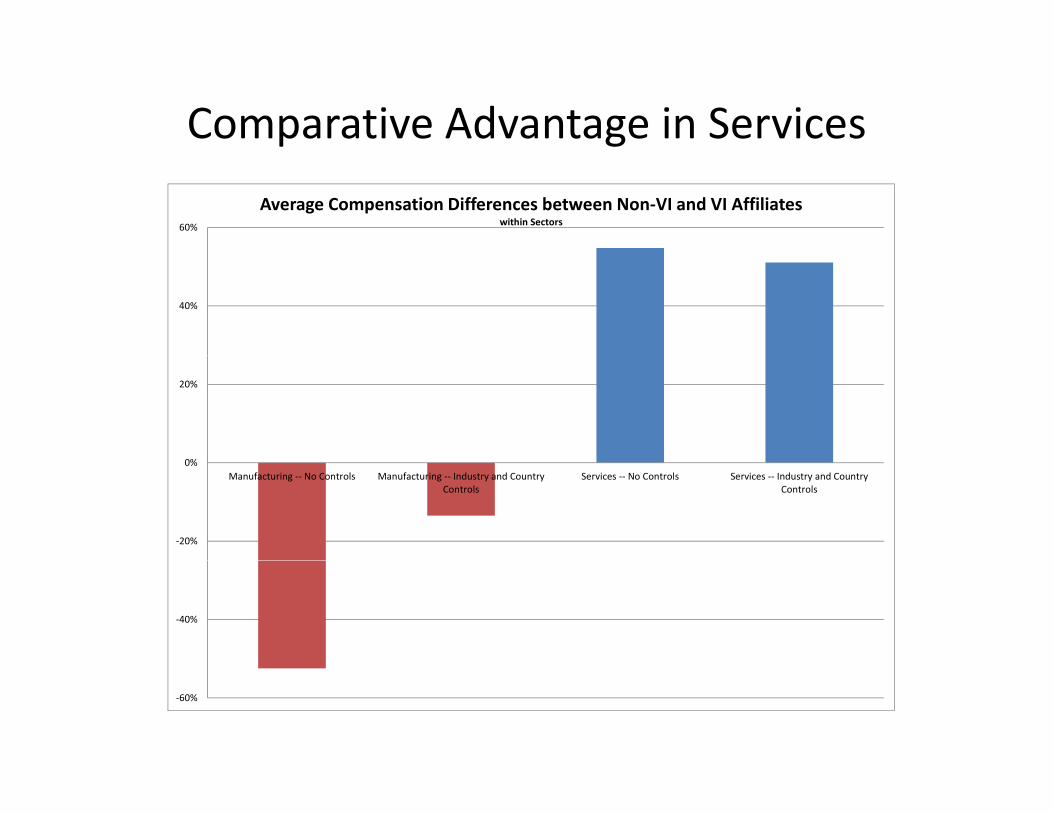

Comparative Advantage in Services

60%

Average Compensation Differences between Non‐VI and VI Affiliates within Sectors

40%

20%

‐20%

0%Manufacturing ‐‐ No Controls Manufacturing ‐‐ Industry and Country

ControlsServices ‐‐ No Controls Services ‐‐ Industry and Country

Controls

‐40%

‐60%

Opportunities?

Impediments to Trade in Services

11 7 illi

14.1 million

Total Employment

11.7 million

Probability of Exporting: 1/4 Probability of Exporting: 1/20

Even controlling for “tradability” i t bli h t h lfservice establishments half as

likely to export

For exporters, exports/sales ratios lower in business

Employmentt E t

6.5 million

ratios lower in business services than manufacturing

at Exporters

1.2 million

Manufacturing Business Services

Source: Author’s calculations from 2002 Economic Census; Manufacturing (NAICS Industries 31-33), Business Services (NAICS Industries 51, 54, 56)

Impediments to Trade in Services

• Requirements for and restrictions on commercial presence

• Economic needs tests• Quotas on number of producers• Requirements for local joint ventures• Licensing/accreditation• Regulation• Differential tax treatment• Government procurement practices

Impediments to Trade in Services

Source: Gootiiz and Mattoo (2009)

Labor Market Impact

Potential Labor Market Impact

100%

Tradable Manufacturing (NAICS 30s) Tradable Business Services (NAICS 50s)

70%

80%

90%

ent

40%

50%

60%

e of

Sec

tor E

mpl

oym

e

20%

30%

Shar

e

0%

10%

20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000 100,000 110,000 120,000 130,000

Industry Average Wage

Source: Author’s calculation using 2007 County Business Patterns data.

Labor Market Impact

8,000,000

Net Change in Employment, 1998‐2007 by Sector

6,000,000

2,000,000

4,000,000

of Jo

bs

0Business Services ‐

Non‐tradableBusiness Services ‐

TradableManufacturing ‐Non‐tradable

Manufacturing ‐Tradable

Personal Services Other

Num

ber o

‐4,000,000

‐2,000,000

‐6,000,000

Source: Jensen (2011), Author's calculations, County Business Pattern Data, 1998‐2007

Distribution of Tradable Service JobsTradable Business Service Industries Tradable Business Service Occupations

0.25

0.3

Share of Workforce in Low-wage Tradable Professional Service Industries

0.1

0.15

0.2

0

0.05

10 11 12 13 14 15 16 17

ln(Workforce)

Source: Author’s calculations, 2007 American Community Survey

Concluding Observations

Concluding Observation 1

• US has much to gain and risks limited dislocation from liberalization in services trade– Tradable services skill intensive

– US (still) relatively skill abundant

Concluding Observation 2

• Intellectual Property important for export intensive industries in US– Software

– Audio/visual arts

– Engineering servicesg g

Concluding Observation 3

• Large and fast growing economies impose high barriers to trade in services

Concluding Observation 4

• Huge infrastructure boom coming – big opportunity for tradable service firms/workers– $40 Trillion, most outside of US,

– Architecture, financing, engineering services, water treatment, project management services…

Concluding Observation 5

• These are likely to be (at least partially) government projects and large, fast‐growing economies are not participants in GPA– Interactions between GATS and GPA make liberalization difficult

– Should work with EU and other developed economies to liberalize

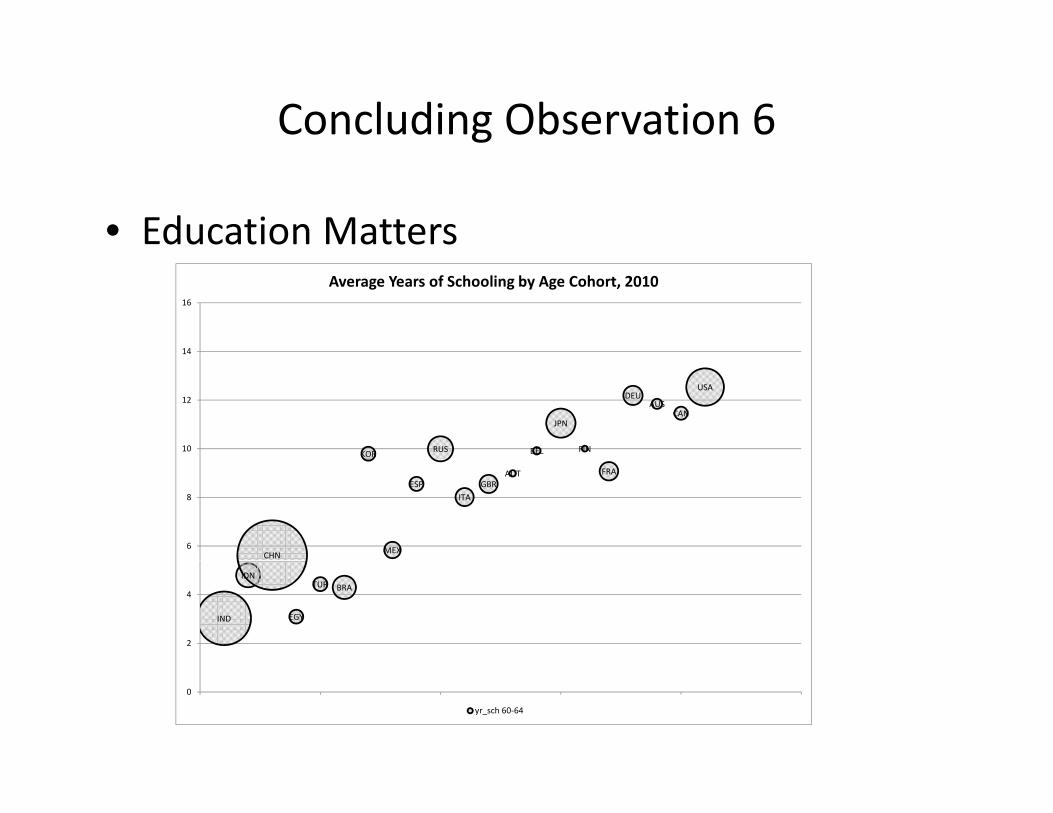

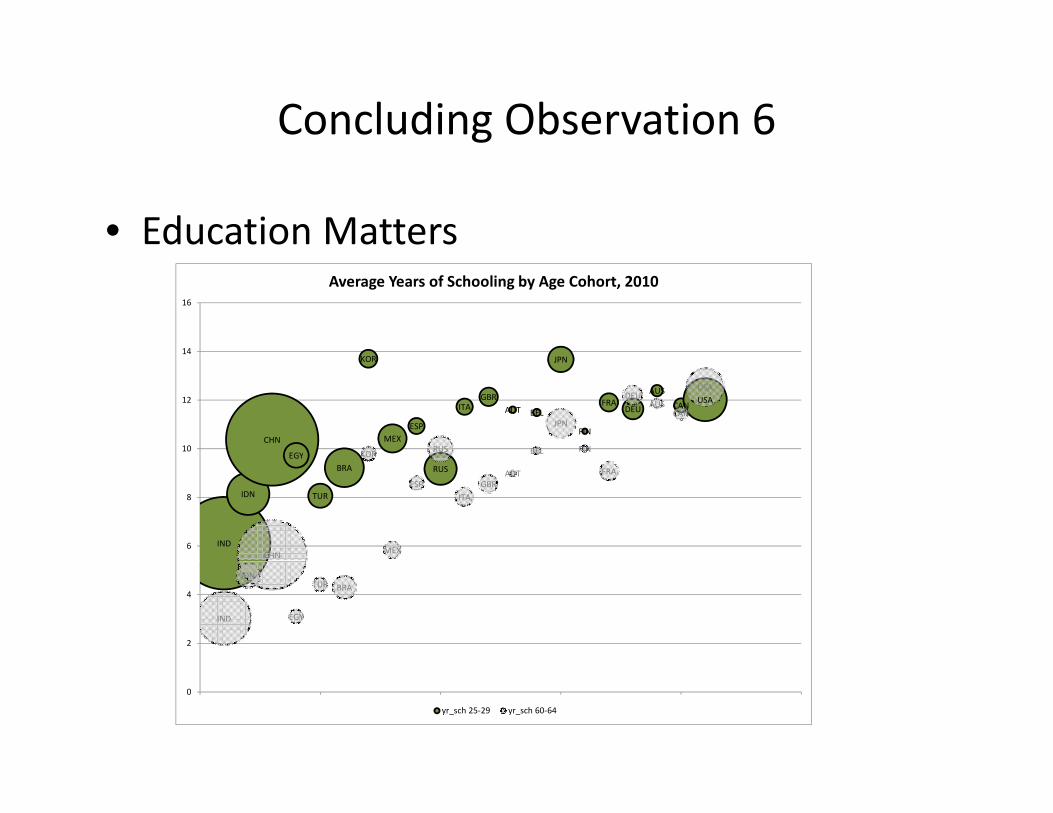

Concluding Observation 6

• Education Matters

14

16

Average Years of Schooling by Age Cohort, 2010

KOR RUS BEL

JPN

FIN

DEUAUS

CAN

USA

10

12

CHN MEX

ESPITA

GBRAUT FRA

6

8

IND

IDN

EGY

TUR BRA

2

4

0

yr_sch 60‐64

Concluding Observation 6

• Education Matters

14

16

Average Years of Schooling by Age Cohort, 2010

CHN

EGY

KOR

MEXESP

ITAGBR

AUT BEL

JPN

FIN

FRADEU

AUS

CANUSA

KOR RUS BEL

JPN

FIN

DEUAUS

CAN

USA

10

12

IND

IDN

EGY

TUR

BRA RUS

CHN MEX

ESPITA

GBRAUT FRA

6

8

IND

IDN

EGY

TUR BRA

2

4

0

yr_sch 25‐29 yr_sch 60‐64

What is the potential?

• Thought experiment:– Increase exports/sales ratio in tradable business services to same level as manufacturing

– Many reasons to question this number, but a place to start…

• “Back‐of‐the‐envelope” numbers:Additional Service Exports Jobsp

Empl Sales Exports Exports/ (.156 * $5T) (export sales/(sales/emp))(million) (trillion) (billion) Sales (trillion) (million)

Tradable Manufacturing 12 5 1000 0.200

T d bl B i S i 20 5 220 0 044 0 78 3 12Tradable Business Services 20 5 220 0.044 0.78 3.12

Policy Recommendations:

• The United States, in cooperation with other developed countries, should:should:

• push aggressively to open the large and fast‐growing markets to service trade.

• continue to push for improved intellectual property p p p p yprotections internationally.

• push for further liberalization of business services in the WTO. • strongly encourage large and fast‐growing countries to sign on

to the WTO government procurement agreement.

• The US should make access to a good primary, secondary, and t d d ti hi h ti l i itpostsecondary education a high national priority.

• The US should strengthen the social safety net for workers dislocated by trade and technological advancement.

• The US should collect better data on the service sector• The US should collect better data on the service sector.

Thank YouThank You