Power Sector Update - vid.investmentguruindia.com

16

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>. Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore. India Equity Research | Power May 1, 2020 Sector Update Power Refer to important disclosures at the end of this report Sharp decline in generation on low demand during lockdown CESC BUY CMP Target Price 656 698 Gujarat Industries Power BUY CMP Target Price 59 99 JSW Energy BUY CMP Target Price 45 73 NHPC BUY CMP Target Price 21 28 NTPC BUY CMP Target Price 95 120 Power Grid Corporation BUY CMP Target Price 162 220 This report is solely produced by Emkay Global. The following person(s) are responsible for the production of the recommendation: Anuj Upadhyay [email protected] +91 22 6624 2447 Power demand fell 8.2% yoy in Mar’20 amid lockdown: Power generation declined 8.2% yoy to 107.4.1bn units in Mar’20 as peak demand declined 23-25% during the lockdown in the country. Generation is expected to decline 32.2% yoy in Apr’20. PLF: PLF declined significantly across the coal segment in Mar’20 (-882 bps yoy to 53.5%) due to the fall in demand. However, PLF improved in 1) hydro (+101bps yoy to 27.3%) due to better water availability; 2) gas (+343bps yoy to 24.2%) to maintain grid stability; and 3) nuclear plants (+1,226bps yoy to 80.0%) due to better fuel availability in Mar’20. PLF in Apr’20 is expected to decline further across the coal segment due to a lack of significant industrial and commercial activity during the lockdown. Spot rates declined in Mar’20 but deficits remained flat: Both base and power deficits remained flat at 0.4% each in Mar’20 on yoy and mom basis. Merchant rates, however, declined by 21.1% yoy to Rs2.5/kWh in Mar’20 and further by 1.8% mom to Rs2.4/kWh in Apr’20 due to subdued power demand. EAP position: We continue to prefer regulated return entities such as NTPC, PGCIL, NHPC and CESC which remains largely immune to the low power offtake by the discoms as their fixed costs are recoverable on the basis of plant availability, and not load factor. Our view: The lockdown across the country led to a significant 23-25% decline in power demand and generation due to very low power offtake from commercial and industrial consumers (C&I) that account for ~40% of the total power demand. The demand, however, is expected to witness a gradual pick-up in the coming weeks with the onset of peak summers and also some relaxations in the green zone areas. In addition, in a move to revive the economy, government is planning to provide relaxations across the selected C&I segment which should increase power demand. Further, in order to provide relief to the financially burdened discoms, the Union Power Ministry (MoP) has made a proposal to PFC/REC to provide special loans to discoms to help them clear power generators’ outstanding bills of ~Rs906bn. These special concessional loans will be given for a period of 10-12 years, along with a moratorium on principal. The loans will be secured by state government guarantees. Relaxation is also provided to discoms in maintaining lower LCs for power procurement, with moratorium on interest and principal repayment to banks. This should partially offset the stress on discoms’ working capital due to subdued power demand and low revenue collection during the lockdown period. Gencos and transmission companies’ working capital would also be under stress due to delayed payment from discoms. The MoP’s direction to discoms for the payment of availability-based fixed charges has provided a significant relief to regulated entities such as NTPC, NHPC and PGCIL. We continue to prefer regulated entities like NTPC, NHPC, CESC and PGCIL who operates on a risk-averse regulatory business environment and earns fixed return on invested project equities. These companies can recover their entire fixed costs on an availability basis. Please see our sector model portfolio (Emkay Alpha Portfolio): Power (Page 3) Financial Snapshot (Consolidated) EPS (Rs) EV/EBITDA P/E FY20E FY21E FY20E FY21E FY20E FY21E CESC 70.7 71.4 9.1 8.4 9.3 9.2 Gujarat Industries Power 17.6 19.5 2.0 2.1 3.4 3.0 JSW Energy 5.4 6.0 4.9 3.8 8.2 7.4 NHPC 2.8 2.9 8.1 8.2 7.4 7.2 NTPC 11.8 12.2 8.4 8.1 8.0 7.8 Power Grid Corporation 21.4 22.2 7.2 6.7 7.6 7.3 Source: Company, Emkay Research

Transcript of Power Sector Update - vid.investmentguruindia.com

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>. Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

India Equity Research | Power

May 1, 2020

Sector Update

Power Refer to important disclosures at the end of this report

Sharp decline in generation on low

demand during lockdown

CESC BUY

CMP Target Price

656 698

Gujarat Industries Power BUY

CMP Target Price

59 99

JSW Energy BUY

CMP Target Price

45 73

NHPC BUY

CMP Target Price

21 28

NTPC BUY

CMP Target Price

95 120

Power Grid Corporation BUY

CMP Target Price

162 220

This report is solely produced by Emkay Global. The following person(s) are responsible for the production of the recommendation:

Anuj Upadhyay [email protected] +91 22 6624 2447

Power demand fell 8.2% yoy in Mar’20 amid lockdown: Power generation declined

8.2% yoy to 107.4.1bn units in Mar’20 as peak demand declined 23-25% during the

lockdown in the country. Generation is expected to decline 32.2% yoy in Apr’20.

PLF: PLF declined significantly across the coal segment in Mar’20 (-882 bps yoy to 53.5%)

due to the fall in demand. However, PLF improved in 1) hydro (+101bps yoy to 27.3%) due

to better water availability; 2) gas (+343bps yoy to 24.2%) to maintain grid stability; and 3)

nuclear plants (+1,226bps yoy to 80.0%) due to better fuel availability in Mar’20. PLF in

Apr’20 is expected to decline further across the coal segment due to a lack of significant

industrial and commercial activity during the lockdown.

Spot rates declined in Mar’20 but deficits remained flat: Both base and power deficits

remained flat at 0.4% each in Mar’20 on yoy and mom basis. Merchant rates, however,

declined by 21.1% yoy to Rs2.5/kWh in Mar’20 and further by 1.8% mom to Rs2.4/kWh in

Apr’20 due to subdued power demand.

EAP position: We continue to prefer regulated return entities such as NTPC, PGCIL,

NHPC and CESC which remains largely immune to the low power offtake by the discoms

as their fixed costs are recoverable on the basis of plant availability, and not load factor.

Our view: The lockdown across the country led to a significant 23-25% decline in power

demand and generation due to very low power offtake from commercial and industrial

consumers (C&I) that account for ~40% of the total power demand. The demand, however, is

expected to witness a gradual pick-up in the coming weeks with the onset of peak summers

and also some relaxations in the green zone areas. In addition, in a move to revive the

economy, government is planning to provide relaxations across the selected C&I segment

which should increase power demand. Further, in order to provide relief to the financially

burdened discoms, the Union Power Ministry (MoP) has made a proposal to PFC/REC to

provide special loans to discoms to help them clear power generators’ outstanding bills of

~Rs906bn. These special concessional loans will be given for a period of 10-12 years, along

with a moratorium on principal. The loans will be secured by state government guarantees.

Relaxation is also provided to discoms in maintaining lower LCs for power procurement, with

moratorium on interest and principal repayment to banks. This should partially offset the stress

on discoms’ working capital due to subdued power demand and low revenue collection during

the lockdown period. Gencos and transmission companies’ working capital would also be

under stress due to delayed payment from discoms. The MoP’s direction to discoms for the

payment of availability-based fixed charges has provided a significant relief to regulated

entities such as NTPC, NHPC and PGCIL.

We continue to prefer regulated entities like NTPC, NHPC, CESC and PGCIL who operates

on a risk-averse regulatory business environment and earns fixed return on invested project

equities. These companies can recover their entire fixed costs on an availability basis.

Please see our sector model portfolio (Emkay Alpha Portfolio): Power (Page 3)

Financial Snapshot (Consolidated)

EPS (Rs) EV/EBITDA P/E

FY20E FY21E FY20E FY21E FY20E FY21E

CESC 70.7 71.4 9.1 8.4 9.3 9.2

Gujarat Industries Power 17.6 19.5 2.0 2.1 3.4 3.0

JSW Energy 5.4 6.0 4.9 3.8 8.2 7.4

NHPC 2.8 2.9 8.1 8.2 7.4 7.2

NTPC 11.8 12.2 8.4 8.1 8.0 7.8

Power Grid Corporation 21.4 22.2 7.2 6.7 7.6 7.3

Source: Company, Emkay Research

Power India Equity Research | Sector Update

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>. Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

May 1, 2020 | 2

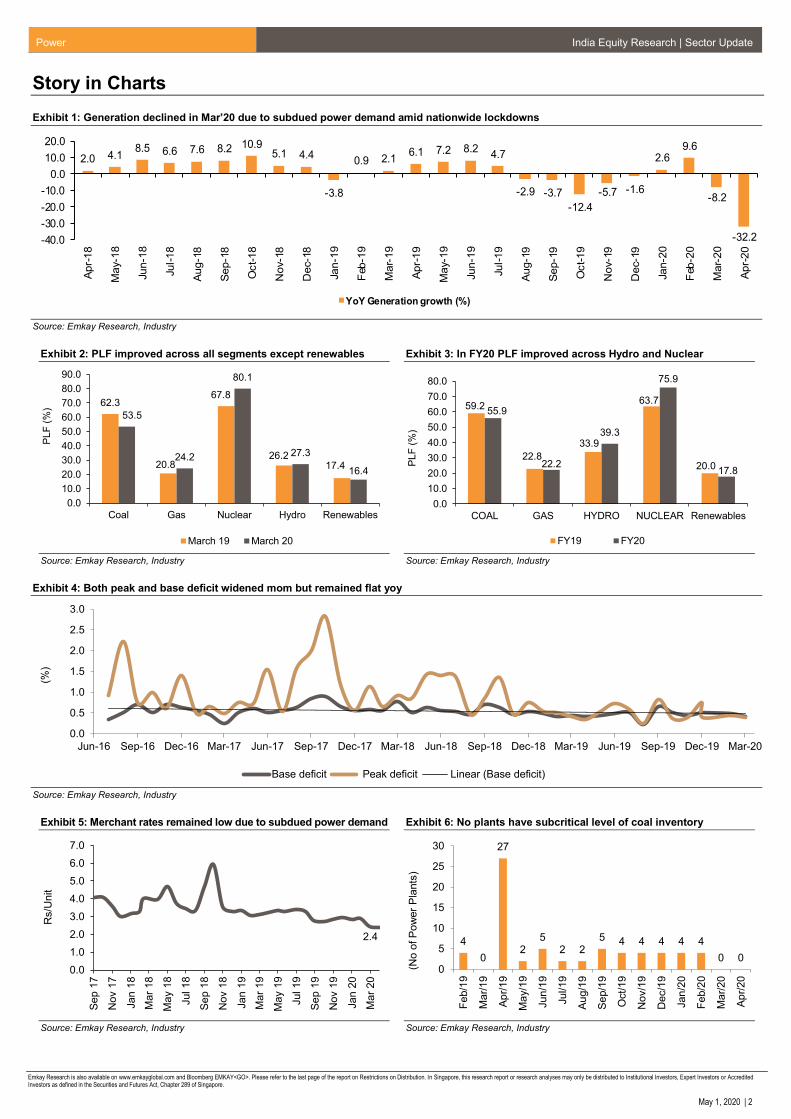

Story in Charts

Exhibit 1: Generation declined in Mar’20 due to subdued power demand amid nationwide lockdowns

2.0 4.18.5 6.6 7.6 8.2 10.9

5.1 4.4

-3.8

0.9 2.16.1 7.2 8.2

4.7

-2.9 -3.7

-12.4

-5.7 -1.6

2.69.6

-8.2

-32.2-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

Apr-

18

May-1

8

Jun-1

8

Jul-18

Aug-1

8

Sep-1

8

Oct-18

Nov-1

8

Dec-1

8

Jan-1

9

Feb-1

9

Mar-

19

Apr-

19

May-1

9

Jun-1

9

Jul-19

Aug-1

9

Sep-1

9

Oct-19

Nov-1

9

Dec-1

9

Jan-2

0

Feb-2

0

Mar-

20

Apr-

20

YoY Generation growth (%)

Source: Emkay Research, Industry

Exhibit 2: PLF improved across all segments except renewables

Source: Emkay Research, Industry

Exhibit 3: In FY20 PLF improved across Hydro and Nuclear

Source: Emkay Research, Industry

Exhibit 4: Both peak and base deficit widened mom but remained flat yoy

Source: Emkay Research, Industry

Exhibit 5: Merchant rates remained low due to subdued power demand

Source: Emkay Research, Industry

Exhibit 6: No plants have subcritical level of coal inventory

Source: Emkay Research, Industry

62.3

20.8

67.8

26.217.4

53.5

24.2

80.1

27.3

16.4

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Coal Gas Nuclear Hydro Renewables

PL

F (

%)

March 19 March 20

59.2

22.8

33.9

63.7

20.0

55.9

22.2

39.3

75.9

17.8

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

COAL GAS HYDRO NUCLEAR Renewables

PL

F (

%)

FY19 FY20

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jun-16 Sep-16 Dec-16 Mar-17 Jun-17 Sep-17 Dec-17 Mar-18 Jun-18 Sep-18 Dec-18 Mar-19 Jun-19 Sep-19 Dec-19 Mar-20

(%)

Base deficit Peak deficit Linear (Base deficit)8.46.9

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Se

p 1

7

Nov 1

7

Jan

18

Ma

r 18

Ma

y 1

8

Jul 18

Se

p 1

8

Nov 1

8

Jan

19

Ma

r 19

Ma

y 1

9

Jul 19

Se

p 1

9

Nov 1

9

Jan

20

Ma

r 20

Rs/U

nit

2.4 4

0

27

25

2 25 4 4 4 4 4

0 00

5

10

15

20

25

30

Fe

b/1

9

Ma

r/19

Ap

r/19

Ma

y/1

9

Jun

/19

Jul/19

Au

g/1

9

Se

p/1

9

Oct/19

Nov/1

9

Dec/1

9

Jan

/20

Fe

b/2

0

Ma

r/20

Ap

r/20

(No o

f P

ow

er

Pla

nts

)

Power India Equity Research | Sector Update

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>. Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

May 1, 2020 | 3

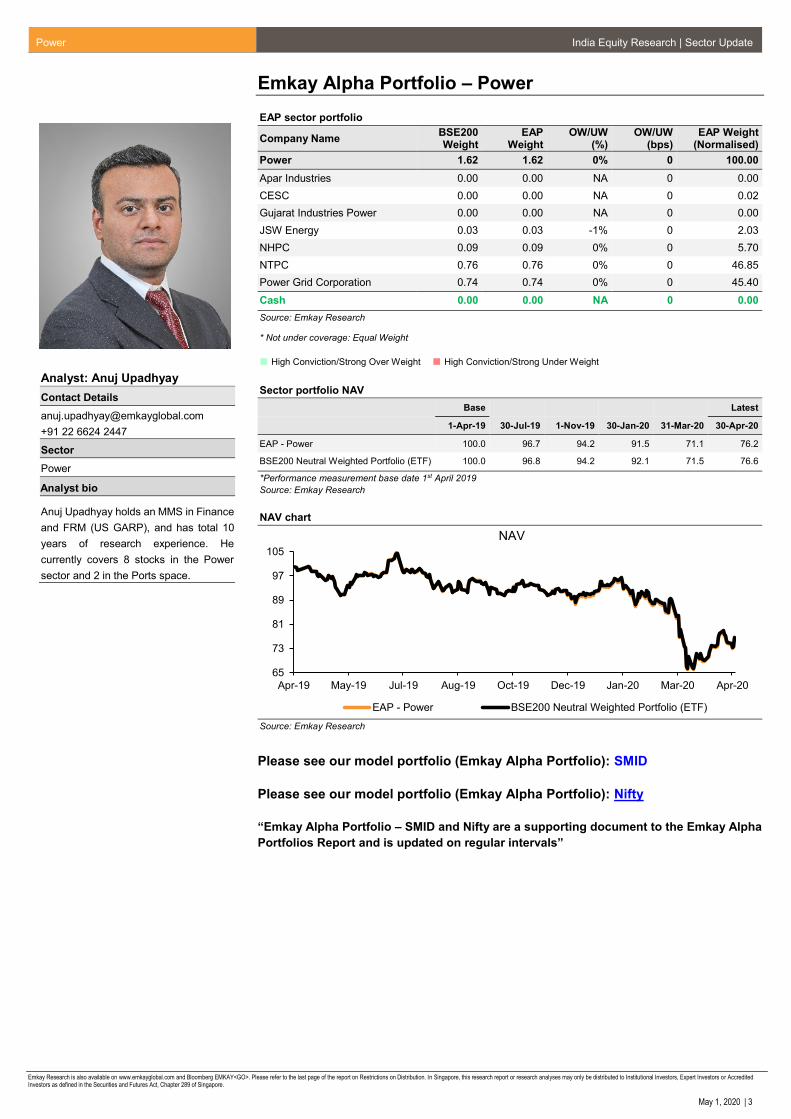

Emkay Alpha Portfolio – Power

EAP sector portfolio

Company Name BSE200 Weight

EAP Weight

OW/UW (%)

OW/UW (bps)

EAP Weight (Normalised)

Power 1.62 1.62 0% 0 100.00

Apar Industries 0.00 0.00 NA 0 0.00

CESC 0.00 0.00 NA 0 0.02

Gujarat Industries Power 0.00 0.00 NA 0 0.00

JSW Energy 0.03 0.03 -1% 0 2.03

NHPC 0.09 0.09 0% 0 5.70

NTPC 0.76 0.76 0% 0 46.85

Power Grid Corporation 0.74 0.74 0% 0 45.40

Cash 0.00 0.00 NA 0 0.00

Source: Emkay Research

* Not under coverage: Equal Weight

High Conviction/Strong Over Weight High Conviction/Strong Under Weight

Sector portfolio NAV

Base Latest

1-Apr-19 30-Jul-19 1-Nov-19 30-Jan-20 31-Mar-20 30-Apr-20

EAP - Power 100.0 96.7 94.2 91.5 71.1 76.2

BSE200 Neutral Weighted Portfolio (ETF) 100.0 96.8 94.2 92.1 71.5 76.6

*Performance measurement base date 1st April 2019

Source: Emkay Research

NAV chart

Source: Emkay Research

Please see our model portfolio (Emkay Alpha Portfolio): SMID

Please see our model portfolio (Emkay Alpha Portfolio): Nifty

“Emkay Alpha Portfolio – SMID and Nifty are a supporting document to the Emkay Alpha

Portfolios Report and is updated on regular intervals”

65

73

81

89

97

105

Apr-19 May-19 Jul-19 Aug-19 Oct-19 Dec-19 Jan-20 Mar-20 Apr-20

NAV

EAP - Power BSE200 Neutral Weighted Portfolio (ETF)

Analyst: Anuj Upadhyay

Contact Details

+91 22 6624 2447

Sector

Power

Analyst bio

Anuj Upadhyay holds an MMS in Finance

and FRM (US GARP), and has total 10

years of research experience. He

currently covers 8 stocks in the Power

sector and 2 in the Ports space.

Power India Equity Research | Sector Update

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>. Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

May 1, 2020 | 4

Generation, PLF and prices

Generation declined 8.2% yoy in Mar’20 but was flat on full-year basis

Generation in Mar’20 declined 8.2% yoy (incl. provisional figures for renewables) as overall

demand declined 9.1% yoy to 98.8bn units. Generation declined in coal (-12.3% yoy) and

renewables (-1.3% yoy), while it improved in gas (+16.6% yoy), hydro (+4.8% yoy) and nuclear

(+18.1% yoy). Provisional data indicates that generation is expected to decline 32.2% yoy in

Apr’20, with coal declining 39.2% yoy due to subdued demand from the C&I segment. On a full-

year basis generation has remained flat at 1,378bn units.

Exhibit 7: Generation remained flat on full-year basis

Source: CEA, Emkay Research

Exhibit 8: Generation declined across coal and RES in Mar’20

(12.3)

16.6 4.8 18.1

92.1

(1.3)

(20)

(10)

0

10

20

30

40

50

60

Coal Gas Hydro Nuclear Imports RES

(%)

Source: CEA, Emkay Research

During Mar’20, peak power demand improved yoy across states like J&K (+14% yoy),

Rajasthan (+14% yoy), Gujarat (+3%), Maharashtra (+7% yoy), AP (+14%), Karnataka

(+3%), Telangana (+23%), West Bengal (+5%) and Jharkhand (+4%).

Power generation, however, increased only in five states: Delhi (+76%), Chhattisgarh

(+8%), Tamil Nadu (+2%), Bihar (+14%) and Orissa (+18%).

Exhibit 9: State-wise generation and demand scenario on a monthly basis

76%-56%

-7%

0%

-68%-15%

-12%

-3%

8%-9%

-14%-10%

-23%

-2%-23%

2%-15%

14%-11%

18%

-17%

-6%

-3%

-2%14%

-13%

14%

-10%-5%

-10%

3%

-1%

7%

14%

3%-2%

-1%

23%-6%

4%

-6%5%

-80% -60% -40% -20% 0% 20% 40% 60% 80% 100%

Delhi

Haryana

HP

J&K

Punjab

Rajasthan

UP

Uttarakhand

Chhattisgarh

Gujarat

MP

Maharashtra

AP

Karnataka

Kerala

TN

Telangana

Bihar

Jharkhand

Orissa

WB

Demand growth YoY Generation growth YoY

Source: Emkay Research

117.0 107.4

1375.5 1378.3

0.0

200.0

400.0

600.0

800.0

1000.0

1200.0

1400.0

1600.0

March 19 March 20 YTDFY19 YTDFY20

(BU

s)

Power India Equity Research | Sector Update

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>. Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

May 1, 2020 | 5

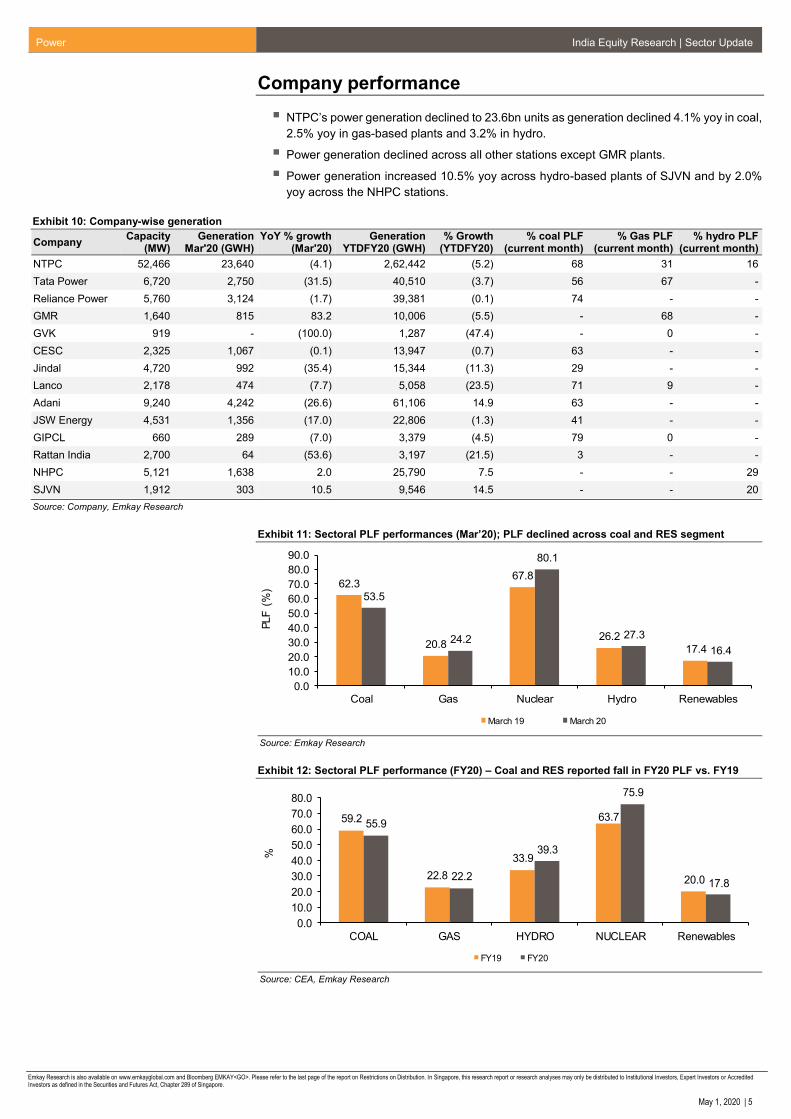

Company performance

NTPC’s power generation declined to 23.6bn units as generation declined 4.1% yoy in coal,

2.5% yoy in gas-based plants and 3.2% in hydro.

Power generation declined across all other stations except GMR plants.

Power generation increased 10.5% yoy across hydro-based plants of SJVN and by 2.0%

yoy across the NHPC stations.

Exhibit 10: Company-wise generation

Company Capacity

(MW) Generation

Mar'20 (GWH) YoY % growth

(Mar'20) Generation

YTDFY20 (GWH) % Growth

(YTDFY20) % coal PLF

(current month) % Gas PLF

(current month) % hydro PLF

(current month)

NTPC 52,466 23,640 (4.1) 2,62,442 (5.2) 68 31 16

Tata Power 6,720 2,750 (31.5) 40,510 (3.7) 56 67 -

Reliance Power 5,760 3,124 (1.7) 39,381 (0.1) 74 - -

GMR 1,640 815 83.2 10,006 (5.5) - 68 -

GVK 919 - (100.0) 1,287 (47.4) - 0 -

CESC 2,325 1,067 (0.1) 13,947 (0.7) 63 - -

Jindal 4,720 992 (35.4) 15,344 (11.3) 29 - -

Lanco 2,178 474 (7.7) 5,058 (23.5) 71 9 -

Adani 9,240 4,242 (26.6) 61,106 14.9 63 - -

JSW Energy 4,531 1,356 (17.0) 22,806 (1.3) 41 - -

GIPCL 660 289 (7.0) 3,379 (4.5) 79 0 -

Rattan India 2,700 64 (53.6) 3,197 (21.5) 3 - -

NHPC 5,121 1,638 2.0 25,790 7.5 - - 29

SJVN 1,912 303 10.5 9,546 14.5 - - 20

Source: Company, Emkay Research

Exhibit 11: Sectoral PLF performances (Mar’20); PLF declined across coal and RES segment

62.3

20.8

67.8

26.2

17.4

53.5

24.2

80.1

27.3

16.4

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Coal Gas Nuclear Hydro Renewables

PLF (

%)

March 19 March 20

Source: Emkay Research

Exhibit 12: Sectoral PLF performance (FY20) – Coal and RES reported fall in FY20 PLF vs. FY19

59.2

22.8

33.9

63.7

20.0

55.9

22.2

39.3

75.9

17.8

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

COAL GAS HYDRO NUCLEAR Renewables

%

FY19 FY20

Source: CEA, Emkay Research

Power India Equity Research | Sector Update

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>. Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

May 1, 2020 | 6

Deficit: Both peak and base deficits remained largely flat yoy and mom in Mar’20.

Exhibit 13: Peak and base deficits for Mar’20

0.4 0.4 0.4 0.4

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Base Defict Peak Deficit

% d

eficit

March-19 March-20

Source: CEA, Emkay Research

Exhibit 14: Region-wise base deficit and peak deficit (Mar’20)

Region %

Base Deficit Peak Deficit

Northern region (1.7) (1.3)

Western region 0.0 0.0

Southern region 0.0 0.0

Eastern Region 0.0 0.0

North Eastern region (2.2) (3.4)

All India (0.4) (0.4)

Source: CEA, Emkay Research

Exhibit 15: Deficit status of eight major states (Mar’20)

Major deficit states %

Base Deficit Peak Deficit

J&K (17.9) (20.0)

Bihar 0.0 0.0

AP 0.0 (0.1)

Karnataka 0.0 0.0

UP (1.1) 0.0

Telangana 0.0 0.0

Tamil Nadu 0.0 (0.1)

Kerala 0.0 0.0

Source: CEA, Emkay Research

Exhibit 16: Peak deficit and base deficit trend

0.0

0.5

1.0

1.5

2.0

2.5

3.0

May-

16

Jul-16

Sep-1

6

Nov-

16

Jan-1

7

Mar-

17

May-

17

Jul-17

Sep-1

7

Nov-1

7

Jan-1

8

Mar-

18

May-

18

Jul-18

Sep-1

8

Nov-1

8

Jan-1

9

Mar-

19

May-1

9

Jul-19

Sep-1

9

Nov-

19

Jan-2

0

Mar-

20

(%)

Base deficit Peak deficit

8.6.

Source: CEA, Emkay Research

Power India Equity Research | Sector Update

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>. Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

May 1, 2020 | 7

Spot rates: Merchant rates declined 21.2% yoy and by 15.7% mom to Rs2.5/unit in Mar’20.

Merchant rates have declined further by 1.8% mom and by 25.1% yoy to Rs2.4/unit in Apr’20

due to the significant drop in power demand amid nationwide lockdowns. Prices in the South

Zone declined 26.7% yoy to Rs2.53/unit in Apr’20 and by 20.9% yoy in other Zones.

Exhibit 17: Spot exchange rate on IEX

4.7

5.9

3.63.3 3.3

3.1 3.1 3.2 3.3 3.3 3.4 3.32.8 2.7 2.9 2.9 2.9 2.9

2.5 2.4

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Sep

18

Oct

18

Nov

18

Dec

18

Jan

19

Feb

19

Mar

19

Apr

19

May

19

Jun

19

Jul 1

9

Aug

19

Sep

19

Oct

19

Nov

19

Dec

19

Jan

20

Feb

20

Mar

20

Apr

20

Rs

/Un

it

Source: IEX, Emkay Research

Exhibit 18: Month-wise Zonal IEX average price trend

Zone Apr'20 Apr'19 YoY (%) Mar'20 MoM (%)

A1 2.53 3.19 -20.9 2.45 2.97

A2 2.53 3.19 -20.9 2.45 2.97

E1 2.53 3.19 -20.9 2.45 2.97

E2 2.53 3.19 -20.9 2.45 2.97

N1 2.53 3.19 -20.9 2.45 2.97

N2 2.53 3.19 -20.9 2.45 2.97

N3 2.53 3.19 -20.9 2.45 2.97

S1 2.53 3.44 -26.7 2.47 2.19

S2 2.53 3.46 -26.9 2.47 2.19

W1 2.53 3.19 -20.9 2.45 2.97

W2 2.53 3.19 -20.9 2.45 2.97

W3 2.53 3.19 -20.9 2.45 2.97

MCP 2.53 3.22 -21.6 2.46 2.85

Source: CEA, Emkay Research;

Fuel supply, prices: Production across coal mines improved by 5.3% on yoy basis to 90.3

mn tonnes in Mar’20, while coal dispatch was down by 6.9% yoy to 61.4mn tonnes. Coal

production at CIL mines increased by 6.5% yoy to 84.36 mn tonnes in Mar’20, while in

FY20 CIL produced 602.14mn tonnes of coal vs 608.1mn tonnes in FY19. Overall coal

production in FY20 has declined marginally by 0.8% yoy to 666.2mn tonnes.

Further, the outstanding dues of power generators to CIL stood at Rs138.4bn at the end of

Feb’20 vs. Rs124.2bn at the end of Jan’20.

Inventory at power stations continues to impress with zero plants facing sub-critical level of

inventory in Apr’20 vs. 27 in April’19, primarily due to the drop in demand.

Exhibit 19: Number of power plants facing sub-critical level of inventory (less than 7 days)

2825

1613

11

22

29

23

96

4

0

27

25

2 25 4 4 4 4 4

0 00

5

10

15

20

25

30

35

Apr-

18

May-

18

Jun-1

8

Jul-18

Aug-1

8

Sep-1

8

Oct-18

Nov-

18

Dec-

18

Jan-1

9

Feb

-19

Mar-

19

Apr-

19

May-

19

Jun-1

9

Jul-19

Aug-1

9

Sep-1

9

Oct-19

Nov-

19

Dec-

19

Jan-2

0

Feb

-20

Mar-

20

Apr-

20

(No o

f Pow

er Pla

nts

)

Source: CEA, Emkay Research

A1 - Tripura, Meghalaya, Manipur, Mizoram, Nagaland

A2 - Assam, Arunachal Pradesh

E1 - WB, Sikkim, Bihar, Jharkhand

E2 - Orissa

N1 - J&K, HP, Chandigarh, Haryana

N2 - UP, Uttaranchal, Rajasthan, Delhi

N3 - Punjab

S1 - AP, Telangana, Karnataka, Pondicherry (Yanam), South Goa

S2 - TN, Kerala, Pondicherry (Puducherry), Pondicherry (Karaikal), Pondicherry (Mahe)

W1 - MP

W2 - Maharashtra, Gujarat, Daman and Diu, Dadra and Nagar Haveli, North Goa

W3- Chhattisgarh

Power India Equity Research | Sector Update

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>. Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

May 1, 2020 | 8

As of April’20, coal stocks at 134 power plants increased by 60.6% yoy to 50.7mn tonnes

(97.7% domestic and 2.3% imported). Coal stock was also up by 12.7% mom due to better

coal supply and slowdown in demand which led to a rise in inventory levels.

Exhibit 20: Coal production and dispatch trend in Mar’20

-50.0

-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

- 10.0 20.0

30.0 40.0 50.0

60.0 70.0 80.0

90.0

Feb

-19

Mar-

19

Apr-

19

May-

19

Jun-1

9

Jul-19

Aug-1

9

Sep-1

9

Oct-19

Nov-

19

Dec-

19

Jan-2

0

Feb

-20

(%)

(Mn T

onnes)

Coal production Coal disp atch t o power sector Dispatch to Power Coal Pro duction

Source: CEA, Emkay Research

International coal prices (RB Index 6300 kcal) declined 8.8% yoy to US$65.5/tonne in

Mar’20 and by 14.1% mom. On a landed cost basis, however, it was down by only 0.5%

yoy at Rs4,932/tonne, primarily due to rupee depreciation. The HBA Index declined 19.7%

yoy to US$65.8/tonne in Apr’20 and by 25.9% yoy to US$67.1/tonne in Mar’20.

Exhibit 21: International coal price trend (RB Index 6300 kcal) Mar’20

0

20

40

60

80

100

120

Dec-

14

Mar-

15

Jun-1

5

Sep-1

5

Dec-

15

Mar-

16

Jun-1

6

Sep-1

6

Dec-

16

Mar-

17

Jun-1

7

Sep-1

7

Dec-

17

Mar-

18

Jun-1

8

Sep-1

8

Dec-

18

Mar-

19

Jun-1

9

Sep-1

9

Dec-

19

Mar-

20

($/tonne)

Source: Emkay Research,

Exhibit 22: International coal price trend (Indonesian coal - HBA index) April’20

0.00

40.00

80.00

120.00

Dec-

14

Apr-

15

Aug-1

5

Dec-

15

Apr-

16

Aug-1

6

Dec-

16

Apr-

17

Aug-1

7

Dec-

17

Apr-

18

Aug-1

8

Dec-

18

Apr-

19

Aug-1

9

Dec-

19

Apr-

20

($/tonne)

Source: Emkay Research

Power India Equity Research | Sector Update

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>. Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

May 1, 2020 | 9

Natural gas production declined 8.8% yoy and by 10.2% mom to 75.5 mmscmd in Feb’20.

Exhibit 23: Domestic natural gas production trend

70.0

75.0

80.0

85.0

90.0

95.0

Feb

-16

May-

16

Aug-1

6

Nov-1

6

Feb

-17

May-

17

Aug-1

7

Nov-

17

Feb

-18

May-

18

Aug-1

8

Nov-

18

Feb-1

9

May-

19

Aug-1

9

Nov-

19

Feb-2

0

(mm

scm

d)

Source: Emkay Research

Capacity: In Mar’20, 1,320 MW capacity was added across the Coal space (660 MW – NTPC

Khargone & 660 MW Suratgarh in Rajasthan) and 270 MW capacity was added across the

Renewable sector. Apart from this, 700 MW was retired in the coal sector during the month. In

FY20, 14GW of net capacity has been added, comprising Coal (4.4GW), Hydro (300MW) and

RES (9.4GW). Currently, the all-India installed capacity is 370GW.

Exhibit 24: Current capacity fuel mix

62.3

1.8

12.3

23.5

0

10

20

30

40

50

60

70

Thermal (Coal+gas) Nuclear Hydro RES

(%)

Source: CEA, Emkay Research

Exhibit 25: Upcoming plant capacity

State Project Name LOA Date Unit Cap. (MW) Org. Comm. Sched. Ant. COD

Bihar Barh STPP St-1 March-05 1 660 August-09 June-20

Bihar Nabinagar STPP January-13 2 660 July-17 June-20

Chhattisgarh Lara STPP November-12 2 800 September-17 July-20

Madhya Pradesh Gadarwara STPP March-13 2 800 September-17 July-20

Odisha Rourkela PP-II Expansion May-16 1 250 September-18 July-20

Uttar Pradesh Harduaganj Expn II September-15 1 660 November-19 July-20

Telangana Bhadradri TPP March-15 2 270 March-17 May-20

Karnataka Yelahanka CCPP November-15 1 370 February-18 May-20

Source: Emkay Research, Industry; As per CEA report

Outstanding dues of discoms: The outstanding dues of distribution companies to power

generating companies declined 3% mom to Rs906bn in Mar’20, while the overdue amount is

down by 1% mom to Rs798bn.

Power India Equity Research | Sector Update

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>. Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

May 1, 2020| 10

Exhibit 26: Discoms outstanding dues data

885 897 881 860 876 889929

906

713745 760 758 765 766

808 798

500

600

700

800

900

1000

Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20

Rs b

n

Outstanding Overdue O/S

Source: Emkay Research

Exhibit 27: Total gas consumption by top 10 power developers (MMSCMD)

Developer October-19 November-19 December-19 January-20 February-20 March-20

Torrent Power 4.8 5.17 3.89 2.53 4.37 4.49

NTPC 2.98 2.3 2.4 3.06 3.41 2.8

IPGPCL 3.39 2.95 2.86 2.59 2.67 2.57

ONGC 1.82 1.6 1.56 1.88 2.49 3.93

RGPPL 2.32 2.68 2.99 2.33 2.21 1.99

NEEPCO 2.18 2.24 2.18 1.38 2.17 1.67

MAHAGENCO 2.47 2.18 1.6 1.07 1.71 0.9

Puducherry ED 0.17 0.17 1.35 0.42 1.51 3.31

APGPCL 1.02 1.12 1.09 1.65 1.03 1.07

Lanco Power 1.2 1.14 1.21 0.76 0.95 0.47

Source: Emkay Research, Elekore

Exhibit 28: Gas Consumption by Power Sector (MMSCM/Day)

Category September-19 October-19 November-19 December-19 January-20 February-20

RLNG 11 8 9 8 7 8

DOMESTIC 20 19 20 19 19 19

Total 31 27 29 27 26 27

Source: Emkay Research, Elekore

DEEP Portal Tender Outcomes in Mar’20

Exhibit 29: GUVNL RA 02 – 500 MW tender

Buyer Period Tender

Quantum (MW)

Trader Source Supply

Quantum (MW)

Supply Time

Landed cos (Rs/kWh)t

GUVNL RA 02

1st April 2020 -30th April2020

500

Adani Enterprises

Torrent 50

00-24 hrs

3.16 TPTCL 100

Adani Power 350

1st May 2020 - 31st May 2020

500 Torrent 50

3.21 Adani Power 450

1st June 2020 - 30th June 2020

500 Torrent 50

3.25 Adani Power 450

Source: Emkay Research, Elekore

Exhibit 30: Tata Power RA 82

Bidder’s Name Tariff (Rs/kwh) Period of Supply Bidder Qty (MW) LoI

Essar Power 2.8 1st June 2020 - 30th June 2020 87

LoI Issued Adani Power 2.8 1st July 2020 - 31st July 2020 87

DB Power 2.8 1st Aug 2020 - 31st Aug 2020 87

Adani Power 2.8 1st Sept 2020 - 30th Sept 2020 87

Source: Emkay Research, Elekore

Power India Equity Research | Sector Update

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>. Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

May 1, 2020| 11

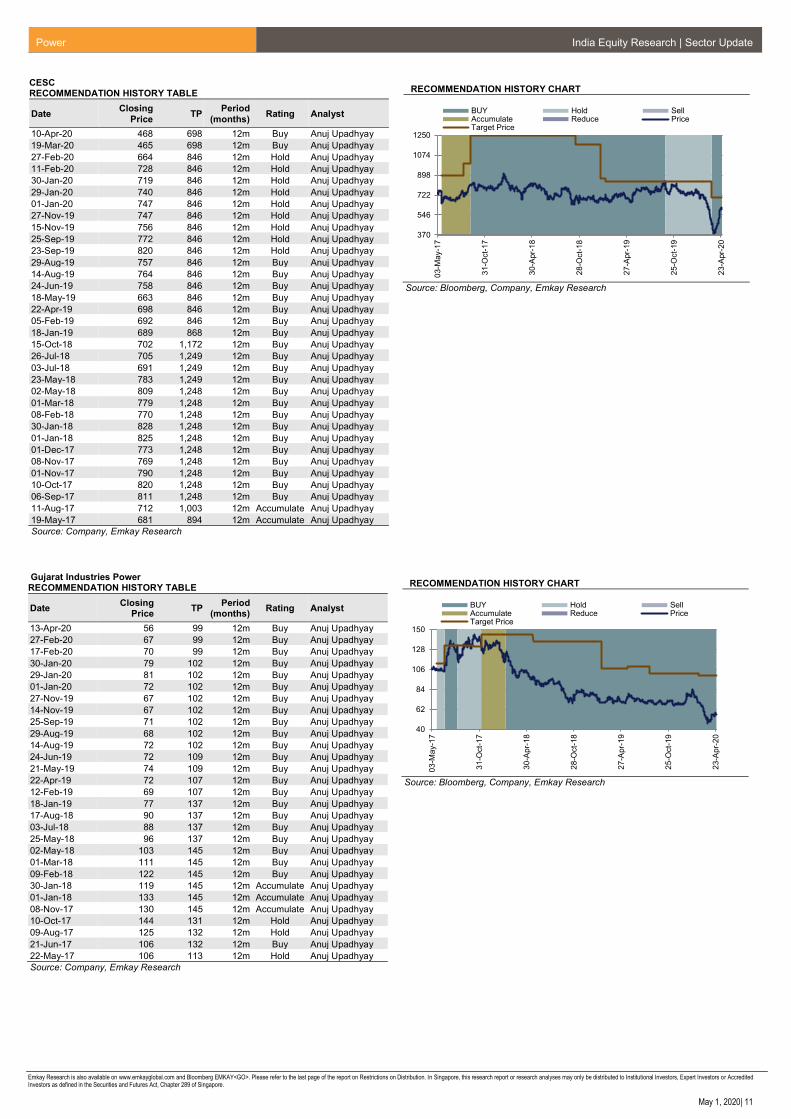

CESC RECOMMENDATION HISTORY TABLE

Date Closing

Price TP

Period

(months) Rating Analyst

10-Apr-20 468 698 12m Buy Anuj Upadhyay

19-Mar-20 465 698 12m Buy Anuj Upadhyay

27-Feb-20 664 846 12m Hold Anuj Upadhyay

11-Feb-20 728 846 12m Hold Anuj Upadhyay

30-Jan-20 719 846 12m Hold Anuj Upadhyay

29-Jan-20 740 846 12m Hold Anuj Upadhyay

01-Jan-20 747 846 12m Hold Anuj Upadhyay

27-Nov-19 747 846 12m Hold Anuj Upadhyay

15-Nov-19 756 846 12m Hold Anuj Upadhyay

25-Sep-19 772 846 12m Hold Anuj Upadhyay

23-Sep-19 820 846 12m Hold Anuj Upadhyay

29-Aug-19 757 846 12m Buy Anuj Upadhyay

14-Aug-19 764 846 12m Buy Anuj Upadhyay

24-Jun-19 758 846 12m Buy Anuj Upadhyay

18-May-19 663 846 12m Buy Anuj Upadhyay

22-Apr-19 698 846 12m Buy Anuj Upadhyay

05-Feb-19 692 846 12m Buy Anuj Upadhyay

18-Jan-19 689 868 12m Buy Anuj Upadhyay

15-Oct-18 702 1,172 12m Buy Anuj Upadhyay

26-Jul-18 705 1,249 12m Buy Anuj Upadhyay

03-Jul-18 691 1,249 12m Buy Anuj Upadhyay

23-May-18 783 1,249 12m Buy Anuj Upadhyay

02-May-18 809 1,248 12m Buy Anuj Upadhyay

01-Mar-18 779 1,248 12m Buy Anuj Upadhyay

08-Feb-18 770 1,248 12m Buy Anuj Upadhyay

30-Jan-18 828 1,248 12m Buy Anuj Upadhyay

01-Jan-18 825 1,248 12m Buy Anuj Upadhyay

01-Dec-17 773 1,248 12m Buy Anuj Upadhyay

08-Nov-17 769 1,248 12m Buy Anuj Upadhyay

01-Nov-17 790 1,248 12m Buy Anuj Upadhyay

10-Oct-17 820 1,248 12m Buy Anuj Upadhyay

06-Sep-17 811 1,248 12m Buy Anuj Upadhyay

11-Aug-17 712 1,003 12m Accumulate Anuj Upadhyay

19-May-17 681 894 12m Accumulate Anuj Upadhyay

Source: Company, Emkay Research

RECOMMENDATION HISTORY CHART

Source: Bloomberg, Company, Emkay Research

370

546

722

898

1074

1250

03

-Ma

y-1

7

31

-Oct-

17

30

-Apr-

18

28

-Oct-

18

27

-Apr-

19

25

-Oct-

19

23

-Apr-

20

BUY Hold SellAccumulate Reduce PriceTarget Price

Gujarat Industries Power RECOMMENDATION HISTORY TABLE

Date Closing

Price TP

Period (months)

Rating Analyst

13-Apr-20 56 99 12m Buy Anuj Upadhyay

27-Feb-20 67 99 12m Buy Anuj Upadhyay

17-Feb-20 70 99 12m Buy Anuj Upadhyay

30-Jan-20 79 102 12m Buy Anuj Upadhyay

29-Jan-20 81 102 12m Buy Anuj Upadhyay

01-Jan-20 72 102 12m Buy Anuj Upadhyay

27-Nov-19 67 102 12m Buy Anuj Upadhyay

14-Nov-19 67 102 12m Buy Anuj Upadhyay

25-Sep-19 71 102 12m Buy Anuj Upadhyay

29-Aug-19 68 102 12m Buy Anuj Upadhyay

14-Aug-19 72 102 12m Buy Anuj Upadhyay

24-Jun-19 72 109 12m Buy Anuj Upadhyay

21-May-19 74 109 12m Buy Anuj Upadhyay

22-Apr-19 72 107 12m Buy Anuj Upadhyay

12-Feb-19 69 107 12m Buy Anuj Upadhyay

18-Jan-19 77 137 12m Buy Anuj Upadhyay

17-Aug-18 90 137 12m Buy Anuj Upadhyay

03-Jul-18 88 137 12m Buy Anuj Upadhyay

25-May-18 96 137 12m Buy Anuj Upadhyay

02-May-18 103 145 12m Buy Anuj Upadhyay

01-Mar-18 111 145 12m Buy Anuj Upadhyay

09-Feb-18 122 145 12m Buy Anuj Upadhyay

30-Jan-18 119 145 12m Accumulate Anuj Upadhyay

01-Jan-18 133 145 12m Accumulate Anuj Upadhyay

08-Nov-17 130 145 12m Accumulate Anuj Upadhyay

10-Oct-17 144 131 12m Hold Anuj Upadhyay

09-Aug-17 125 132 12m Hold Anuj Upadhyay

21-Jun-17 106 132 12m Buy Anuj Upadhyay

22-May-17 106 113 12m Hold Anuj Upadhyay

Source: Company, Emkay Research

RECOMMENDATION HISTORY CHART

Source: Bloomberg, Company, Emkay Research

40

62

84

106

128

150

03

-Ma

y-1

7

31

-Oct-

17

30

-Apr-

18

28

-Oct-

18

27

-Apr-

19

25

-Oct-

19

23

-Apr-

20

BUY Hold SellAccumulate Reduce PriceTarget Price

Power India Equity Research | Sector Update

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>. Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

May 1, 2020| 12

JSW Energy RECOMMENDATION HISTORY TABLE

Date Closing

Price TP

Period

(months) Rating Analyst

13-Apr-20 41 73 12m Buy Anuj Upadhyay

27-Feb-20 60 73 12m Buy Anuj Upadhyay

18-Feb-20 66 73 12m Buy Anuj Upadhyay

05-Feb-20 62 73 12m Buy Anuj Upadhyay

30-Jan-20 64 74 12m Hold Anuj Upadhyay

29-Jan-20 66 74 12m Hold Anuj Upadhyay

01-Jan-20 69 74 12m Hold Anuj Upadhyay

27-Nov-19 74 74 12m Hold Anuj Upadhyay

03-Nov-19 70 74 12m Hold Anuj Upadhyay

25-Sep-19 64 74 12m Hold Anuj Upadhyay

29-Aug-19 67 74 12m Hold Anuj Upadhyay

06-Aug-19 68 74 12m Hold Anuj Upadhyay

24-Jun-19 67 74 12m Hold Anuj Upadhyay

17-May-19 67 74 12m Hold Anuj Upadhyay

22-Apr-19 71 73 12m Hold Anuj Upadhyay

31-Jan-19 67 73 12m Hold Anuj Upadhyay

18-Jan-19 68 73 12m Hold Anuj Upadhyay

27-Jul-18 67 73 12m Hold Anuj Upadhyay

03-Jul-18 64 73 12m Reduce Anuj Upadhyay

03-May-18 82 73 12m Reduce Anuj Upadhyay

02-May-18 82 76 12m Reduce Anuj Upadhyay

01-Mar-18 81 76 12m Reduce Anuj Upadhyay

06-Feb-18 83 76 12m Reduce Anuj Upadhyay

30-Jan-18 87 76 12m Reduce Anuj Upadhyay

01-Jan-18 91 76 12m Reduce Anuj Upadhyay

01-Dec-17 84 76 12m Reduce Anuj Upadhyay

01-Nov-17 85 76 12m Reduce Anuj Upadhyay

10-Oct-17 79 64 12m Hold Anuj Upadhyay

11-Aug-17 64 64 12m Hold Anuj Upadhyay

02-May-17 62 64 12m Hold Anuj Upadhyay

Source: Company, Emkay Research

RECOMMENDATION HISTORY CHART

Source: Bloomberg, Company, Emkay Research

30

44

58

72

86

100

03

-Ma

y-1

7

31

-Oct-

17

30

-Apr-

18

28

-Oct-

18

27

-Apr-

19

25

-Oct-

19

23

-Apr-

20

BUY Hold SellAccumulate Reduce PriceTarget Price

NHPC RECOMMENDATION HISTORY TABLE

Date Closing

Price TP

Period (months)

Rating Analyst

13-Apr-20 22 28 12m Buy Anuj Upadhyay

03-Mar-20 23 28 12m Buy Anuj Upadhyay

27-Feb-20 21 28 12m Buy Anuj Upadhyay

10-Feb-20 24 28 12m Buy Anuj Upadhyay

30-Jan-20 25 28 12m Buy Anuj Upadhyay

29-Jan-20 26 28 12m Buy Anuj Upadhyay

01-Jan-20 24 28 12m Buy Anuj Upadhyay

27-Nov-19 24 28 12m Buy Anuj Upadhyay

19-Nov-19 23 28 12m Buy Anuj Upadhyay

25-Sep-19 23 28 12m Buy Anuj Upadhyay

29-Aug-19 23 28 12m Buy Anuj Upadhyay

14-Aug-19 23 28 12m Buy Anuj Upadhyay

24-Jun-19 25 28 12m Hold Anuj Upadhyay

31-May-19 25 28 12m Hold Anuj Upadhyay

22-Apr-19 24 29 12m Buy Anuj Upadhyay

08-Feb-19 24 29 12m Buy Anuj Upadhyay

18-Jan-19 25 31 12m Buy Anuj Upadhyay

16-Dec-18 26 31 12m Buy Anuj Upadhyay

13-Aug-18 25 31 12m Buy Anuj Upadhyay

03-Jul-18 23 31 12m Accumulate Anuj Upadhyay

04-Jun-18 26 31 12m Accumulate Anuj Upadhyay

02-May-18 28 35 12m Buy Anuj Upadhyay

01-Mar-18 28 35 12m Buy Anuj Upadhyay

12-Feb-18 30 35 12m Buy Anuj Upadhyay

30-Jan-18 30 33 12m Buy Anuj Upadhyay

01-Jan-18 32 33 12m Buy Anuj Upadhyay

01-Dec-17 28 33 12m Buy Anuj Upadhyay

13-Nov-17 27 33 12m Buy Anuj Upadhyay

01-Nov-17 29 33 12m Accumulate Anuj Upadhyay

10-Oct-17 28 33 12m Accumulate Anuj Upadhyay

10-Aug-17 30 33 12m Accumulate Anuj Upadhyay

05-Jun-17 31 30 12m Hold Anuj Upadhyay

Source: Company, Emkay Research

RECOMMENDATION HISTORY CHART

Source: Bloomberg, Company, Emkay Research

10

16

22

28

34

40

03

-Ma

y-1

7

31

-Oct-

17

30

-Apr-

18

28

-Oct-

18

27

-Apr-

19

25

-Oct-

19

23

-Apr-

20

BUY Hold SellAccumulate Reduce PriceTarget Price

Power India Equity Research | Sector Update

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>. Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

May 1, 2020| 13

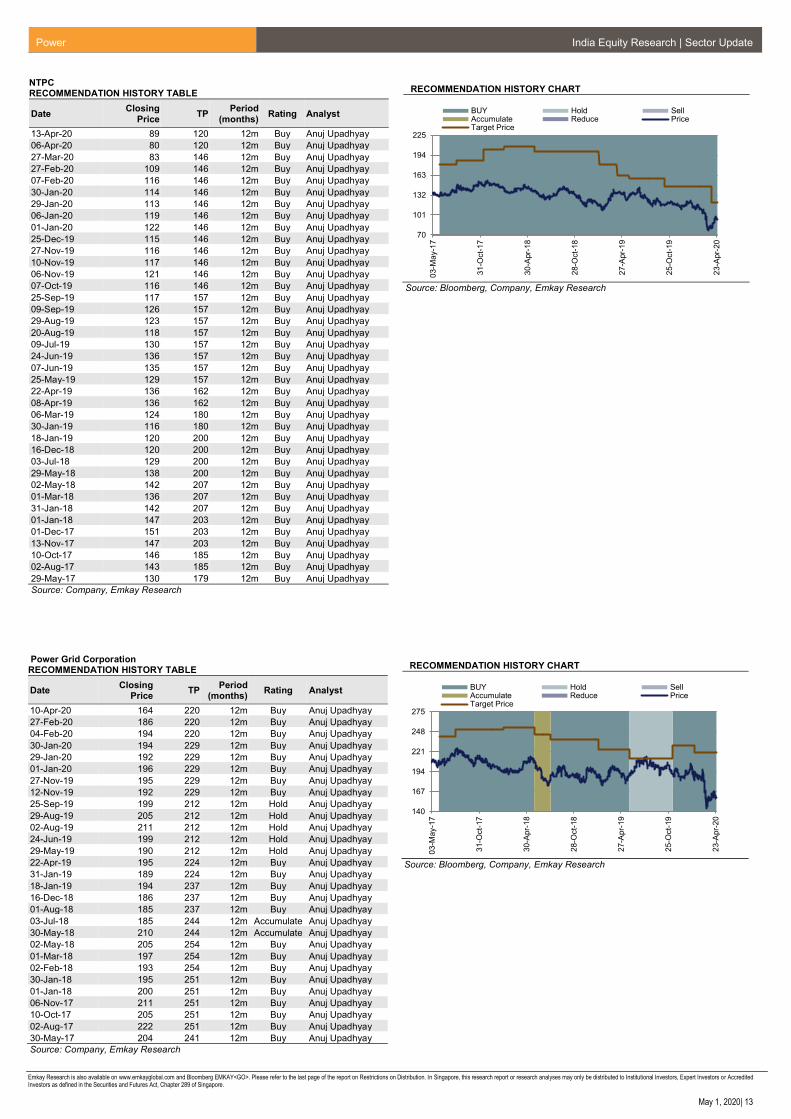

NTPC RECOMMENDATION HISTORY TABLE

Date Closing

Price TP

Period

(months) Rating Analyst

13-Apr-20 89 120 12m Buy Anuj Upadhyay

06-Apr-20 80 120 12m Buy Anuj Upadhyay

27-Mar-20 83 146 12m Buy Anuj Upadhyay

27-Feb-20 109 146 12m Buy Anuj Upadhyay

07-Feb-20 116 146 12m Buy Anuj Upadhyay

30-Jan-20 114 146 12m Buy Anuj Upadhyay

29-Jan-20 113 146 12m Buy Anuj Upadhyay

06-Jan-20 119 146 12m Buy Anuj Upadhyay

01-Jan-20 122 146 12m Buy Anuj Upadhyay

25-Dec-19 115 146 12m Buy Anuj Upadhyay

27-Nov-19 116 146 12m Buy Anuj Upadhyay

10-Nov-19 117 146 12m Buy Anuj Upadhyay

06-Nov-19 121 146 12m Buy Anuj Upadhyay

07-Oct-19 116 146 12m Buy Anuj Upadhyay

25-Sep-19 117 157 12m Buy Anuj Upadhyay

09-Sep-19 126 157 12m Buy Anuj Upadhyay

29-Aug-19 123 157 12m Buy Anuj Upadhyay

20-Aug-19 118 157 12m Buy Anuj Upadhyay

09-Jul-19 130 157 12m Buy Anuj Upadhyay

24-Jun-19 136 157 12m Buy Anuj Upadhyay

07-Jun-19 135 157 12m Buy Anuj Upadhyay

25-May-19 129 157 12m Buy Anuj Upadhyay

22-Apr-19 136 162 12m Buy Anuj Upadhyay

08-Apr-19 136 162 12m Buy Anuj Upadhyay

06-Mar-19 124 180 12m Buy Anuj Upadhyay

30-Jan-19 116 180 12m Buy Anuj Upadhyay

18-Jan-19 120 200 12m Buy Anuj Upadhyay

16-Dec-18 120 200 12m Buy Anuj Upadhyay

03-Jul-18 129 200 12m Buy Anuj Upadhyay

29-May-18 138 200 12m Buy Anuj Upadhyay

02-May-18 142 207 12m Buy Anuj Upadhyay

01-Mar-18 136 207 12m Buy Anuj Upadhyay

31-Jan-18 142 207 12m Buy Anuj Upadhyay

01-Jan-18 147 203 12m Buy Anuj Upadhyay

01-Dec-17 151 203 12m Buy Anuj Upadhyay

13-Nov-17 147 203 12m Buy Anuj Upadhyay

10-Oct-17 146 185 12m Buy Anuj Upadhyay

02-Aug-17 143 185 12m Buy Anuj Upadhyay

29-May-17 130 179 12m Buy Anuj Upadhyay

Source: Company, Emkay Research

RECOMMENDATION HISTORY CHART

Source: Bloomberg, Company, Emkay Research

70

101

132

163

194

225

03

-Ma

y-1

7

31

-Oct-

17

30

-Apr-

18

28

-Oct-

18

27

-Apr-

19

25

-Oct-

19

23

-Apr-

20

BUY Hold SellAccumulate Reduce PriceTarget Price

Power Grid Corporation RECOMMENDATION HISTORY TABLE

Date Closing

Price TP

Period (months)

Rating Analyst

10-Apr-20 164 220 12m Buy Anuj Upadhyay

27-Feb-20 186 220 12m Buy Anuj Upadhyay

04-Feb-20 194 220 12m Buy Anuj Upadhyay

30-Jan-20 194 229 12m Buy Anuj Upadhyay

29-Jan-20 192 229 12m Buy Anuj Upadhyay

01-Jan-20 196 229 12m Buy Anuj Upadhyay

27-Nov-19 195 229 12m Buy Anuj Upadhyay

12-Nov-19 192 229 12m Buy Anuj Upadhyay

25-Sep-19 199 212 12m Hold Anuj Upadhyay

29-Aug-19 205 212 12m Hold Anuj Upadhyay

02-Aug-19 211 212 12m Hold Anuj Upadhyay

24-Jun-19 199 212 12m Hold Anuj Upadhyay

29-May-19 190 212 12m Hold Anuj Upadhyay

22-Apr-19 195 224 12m Buy Anuj Upadhyay

31-Jan-19 189 224 12m Buy Anuj Upadhyay

18-Jan-19 194 237 12m Buy Anuj Upadhyay

16-Dec-18 186 237 12m Buy Anuj Upadhyay

01-Aug-18 185 237 12m Buy Anuj Upadhyay

03-Jul-18 185 244 12m Accumulate Anuj Upadhyay

30-May-18 210 244 12m Accumulate Anuj Upadhyay

02-May-18 205 254 12m Buy Anuj Upadhyay

01-Mar-18 197 254 12m Buy Anuj Upadhyay

02-Feb-18 193 254 12m Buy Anuj Upadhyay

30-Jan-18 195 251 12m Buy Anuj Upadhyay

01-Jan-18 200 251 12m Buy Anuj Upadhyay

06-Nov-17 211 251 12m Buy Anuj Upadhyay

10-Oct-17 205 251 12m Buy Anuj Upadhyay

02-Aug-17 222 251 12m Buy Anuj Upadhyay

30-May-17 204 241 12m Buy Anuj Upadhyay

Source: Company, Emkay Research

RECOMMENDATION HISTORY CHART

Source: Bloomberg, Company, Emkay Research

140

167

194

221

248

275

03

-Ma

y-1

7

31

-Oct-

17

30

-Apr-

18

28

-Oct-

18

27

-Apr-

19

25

-Oct-

19

23

-Apr-

20

BUY Hold SellAccumulate Reduce PriceTarget Price

Power India Equity Research | Sector Update

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>. Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

May 1, 2020| 14

Emkay Rating Distribution

Ratings Expected Return within the next 12-18 months.

BUY Over 15%

HOLD Between -5% to 15%

SELL Below -5%

Completed Date: 01 May 2020 19:54:03 (SGT) Dissemination Date: 01 May 2020 19:55:03 (SGT)

Sources for all charts and tables are Emkay Research unless otherwise specified.

GENERAL DISCLOSURE/DISCLAIMER BY EMKAY GLOBAL FINANCIAL SERVICES LIMITED (EGFSL): Emkay Global Financial Services Limited (CIN-L67120MH1995PLC084899) and its affiliates are a full-service, brokerage, investment banking, investment management and financing group. Emkay Global Financial Services Limited (EGFSL) along with its affiliates are participants in virtually all securities trading markets in India. EGFSL was established in 1995 and is one of India's leading brokerage and distribution house. EGFSL is a corporate trading member of Bombay Stock Exchange Limited (BSE), National Stock Exchange of India Limited (NSE), MCX Stock Exchange Limited (MCX-SX). EGFSL along with its subsidiaries offers the most comprehensive avenues for investments and is engaged in the businesses including stock broking (Institutional and retail), merchant banking, commodity broking, depository participant, portfolio management, insurance broking and services rendered in connection with distribution of primary market issues and financial products like mutual funds, fixed deposits. Details of associates are available on our website i.e. www.emkayglobal.com EGFSL is registered as Research Analyst with SEBI bearing registration Number INH000000354 as per SEBI (Research Analysts) Regulations, 2014. EGFSL hereby declares that it has not defaulted with any stock exchange nor its activities were suspended by any stock exchange with whom it is registered in last five years, except that NSE had disabled EGFSL from trading on October 05, October 08 and October 09, 2012 for a manifest error resulting into a bonafide erroneous trade on October 05, 2012. However, SEBI and Stock Exchanges have conducted the routine inspection and based on their observations have issued advice letters or levied minor penalty on EGFSL for certain operational deviations in ordinary/routine course of business. EGFSL has not been debarred from doing business by any Stock Exchange / SEBI or any other authorities; nor has its certificate of registration been cancelled by SEBI at any point of time. EGFSL offers research services to clients as well as prospects. The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report. Other disclosures by Emkay Global Financial Services Limited (Research Entity) and its Research Analyst under SEBI (Research Analyst) Regulations, 2014 with reference to the subject company(s) covered in this report EGFSL and/or its affiliates may seek investment banking or other business from the company or companies that are the subject of this material. Our salespeople, traders, and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed herein, and our proprietary trading and investing businesses may make investment decisions that may be inconsistent with the recommendations expressed herein. In reviewing these materials, you should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest including but not limited to those stated herein. Additionally, other important information regarding our relationships with the company or companies that are the subject of this material is provided herein. This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject EGFSL or its group companies to any registration or licensing requirement within such jurisdiction. Specifically, this document does not constitute an offer to or solicitation to any U.S. person for the purchase or sale of any financial instrument or as an official confirmation of any transaction to any U.S. person. Unless otherwise stated, this message should not be construed as official confirmation of any transaction. No part of this document may be used by private customers in United Kingdom. All material presented in this report, unless specifically indicated otherwise, is under copyright to Emkay. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of EGFSL . All trademarks, service marks and logos used in this report are trademarks or registered trademarks of EGFSL or its Group Companies. The information contained herein is not intended for publication or distribution or circulation in any manner whatsoever and any unauthorized reading, dissemination, distribution or copying of this communication is prohibited unless otherwise expressly authorized. Please ensure that you have read “Risk Disclosure Document for Capital Market and Derivatives Segments” as prescribed by Securities and Exchange Board of India before investing in Indian Securities Market. In so far as this report includes current or historic information, it is believed to be reliable, although its accuracy and completeness cannot be guaranteed.

This publication has not been reviewed or authorized by any regulatory authority. There is no planned schedule or frequency for updating research publication relating to any issuer.

Please contact the primary analyst for valuation methodologies and assumptions associated with the covered companies or price targets Disclaimer for U.S. persons only: This research report is a product of Emkay Global Financial Services Limited (Emkay), which is the employer of the research analyst(s) who has prepared the research report. The research analyst(s) preparing the research report is/are resident outside the United States (U.S.) and are not associated persons of any U.S. regulated broker-dealer and therefore the analyst(s) is/are not subject to supervision by a U.S. broker-dealer, and is/are not required to satisfy the regulatory licensing requirements of Financial Institutions Regulatory Authority (FINRA) or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject company, public appearances and trading securities held by a research analyst account. This report is intended for distribution to "Major Institutional Investors" as defined by Rule 15a-6(b)(4) of the U.S. Securities and Exchange Act, 1934 (the Exchange Act) and interpretations thereof by U.S. Securities and Exchange Commission (SEC) in reliance on Rule 15a 6(a)(2). If the recipient of this report is not a Major Institutional Investor as specified above, then it should not act upon this report and return the same to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any U.S. person, which is not the Major Institutional Investor. In reliance on the exemption from registration provided by Rule 15a-6 of the Exchange Act and interpretations thereof by the SEC in order to conduct certain business with Major Institutional Investors.

Power India Equity Research | Sector Update

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>. Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

May 1, 2020| 15

ANALYST CERTIFICATION BY EMKAY GLOBAL FINANCIAL SERVICES LIMITED (EGFSL) The research analyst(s) primarily responsible for the content of this research report, in part or in whole, certifies that the views about the companies and their securities expressed in this report accurately reflect his/her personal views. The analyst(s) also certifies that no part of his/her compensation was, is, or will be, directly or indirectly, related to specific recommendations or views expressed in the report. The research analyst (s) primarily responsible of the content of this research report, in part or in whole, certifies that he or his associate1 does not serve as an officer, director or employee of the issuer or the new listing applicant (which includes in the case of a real estate investment trust, an officer of the management company of the real estate investment trust; and in the case of any other entity, an officer or its equivalent counterparty of the entity who is responsible for the management of the issuer or the new listing applicant). The research analyst(s) primarily responsible for the content of this research report or his associate does not have financial interests2 in relation to an issuer or a new listing applicant that the analyst reviews. EGFSL has procedures in place to eliminate, avoid and manage any potential conflicts of interests that may arise in connection with the production of research reports. The research analyst(s) responsible for this report operates as part of a separate and independent team to the investment banking function of the EGFSL and procedures are in place to ensure that confidential information held by either the research or investment banking function is handled appropriately. There is no direct link of EGFSL compensation to any specific investment banking function of the EGFSL. 1 An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst. 2 Financial interest is defined as interest that are commonly known financial interest, such as investment in the securities in respect of an issuer or a new listing applicant, or financial accommodation arrangement between the issuer or the new listing applicant and the firm or analysis. This term does not include commercial lending conducted at the arm’s length, or investments in any collective investment scheme other than an issuer or new listing applicant notwithstanding the fact that the scheme has investments in securities in respect of an issuer or a new listing applicant.

COMPANY-SPECIFIC / REGULATORY DISCLOSURES BY EMKAY GLOBAL FINANCIAL SERVICES LIMITED (EGFSL):

Disclosures by Emkay Global Financial Services Limited (Research Entity) and its Research Analyst under SEBI (Research Analyst) Regulations, 2014 with reference to the subject company(s) covered in this report-: 1. EGFSL, its subsidiaries and/or other affiliates do not have a proprietary position in the securities recommended in this report as of May 1, 2020 2. EGFSL, and/or Research Analyst does not market make in equity securities of the issuer(s) or company(ies) mentioned in this Research Report Disclosure of previous investment recommendation produced: 3. EGFSL may have published other investment recommendations in respect of the same securities / instruments recommended in this research

report during the preceding 12 months. Please contact the primary analyst listed in the first page of this report to view previous investment recommendations published by EGFSL in the preceding 12 months.

4. EGFSL , its subsidiaries and/or other affiliates and Research Analyst or his/her relative’s does not have any material conflict of interest in the securities recommended in this report as of May 1, 2020.

5. EGFSL, its subsidiaries and/or other affiliates and Research Analyst or his/her relative’s does not have actual/beneficial ownership of 1% or more securities of the subject company at the end of the month immediately preceding the May 1, 2020

6. EGFSL, its subsidiaries and/or other affiliates and Research Analyst have not received any compensation in whatever form including compensation for investment banking or merchant banking or brokerage services or for products or services other than investment banking or merchant banking or brokerage services from securities recommended in this report (subject company) in the past 12 months.

7. EGFSL, its subsidiaries and/or other affiliates and/or and Research Analyst have not received any compensation or other benefits from securities recommended in this report (subject company) or third party in connection with the research report.

8. Securities recommended in this report (Subject Company) has not been client of EGFSL, its subsidiaries and/or other affiliates and/or and Research Analyst during twelve months preceding the May 1, 2020

Power India Equity Research | Sector Update

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>. Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

May 1, 2020| 16

RESTRICTIONS ON DISTRIBUTION

General This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

Australia This report is not for distribution into Australia.

Hong Kong This report is not for distribution into Hong Kong.

Indonesia This report is being distributed in Indonesia by PT DBS Vickers Sekuritas Indonesia.

Malaysia This report is not for distribution into Malaysia.

Singapore

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 16800306E) or DBSVS (Company Regn. No. 1860024G) both of which are Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd and/or DBSVS, may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an agreement under Regulation 32C of the financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 6327 2288 for matters arising from, or in connection with the report.

Thailand This report is being distributed in Thailand by DBS Vickers Securities (Thailand) Co Ltd.

United Kingdom

This report is disseminated in the United Kingdom by DBS Vickers Securities (UK) Ltd, ("DBSVUK"). DBSVUK is authorised and regulated by the Financial Conduct Authority in the United Kingdom.

In respect of the United Kingdom, this report is solely intended for the clients of DBSVUK, its respective connected and associated corporations and affiliates only and no part of this document may be (i) copied, photocopied or duplicated in any form or by any means or (ii) redistributed without the prior written consent of DBSVUK. This communication is directed at persons having professional experience in matters relating to investments. Any investment activity following from this communication will only be engaged in with such persons. Persons who do not have professional experience in matters relating to investments should not rely on this communication.

Dubai International Financial Centre

This research report is being distributed by DBS Bank Ltd., (DIFC Branch) having its office at units 608-610, 6th Floor, Gate Precinct Building 5, PO Box 506538, Dubai International Financial Centre (DIFC), Dubai, United Arab Emirates. DBS Bank Ltd., (DIFC Branch) is regulated by The Dubai Financial Services Authority. This research report is intended only for professional clients (as defined in the DFSA rulebook) and no other person may act upon it.

United Arab Emirates

This report is provided by DBS Bank Ltd (Company Regn. No. 196800306E) which is an Exempt Financial Adviser as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. This report is for information purposes only and should not be relied upon or acted on by the recipient or considered as a solicitation or inducement to buy or sell any financial product. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situation, or needs of individual clients. You should contact your relationship manager or investment adviser if you need advice on the merits of buying, selling or holding a particular investment. You should note that the information in this report may be out of date and it is not represented or warranted to be accurate, timely or complete. This report or any portion thereof may not be reprinted, sold or redistributed without our written consent.

United States

DBSVUSA did not participate in its preparation. The research analyst(s) named on this report are not registered as research analysts with FINRA and are not associated persons of DBSVUSA. The research analyst(s) are not subject to FINRA Rule 2241 restrictions on analyst compensation, communications with a subject company, public appearances and trading securities held by a research analyst. This report is being distributed in the United States by DBSVUSA, which accepts responsibility for its contents. This report may only be distributed to Major U.S. Institutional Investors (as defined in SEC Rule 15a-6) and to such other institutional investors and qualified persons as DBSVUSA may authorize. Any U.S. person receiving this report who wishes to effect transactions in any securities referred to herein should contact DBSVUSA directly and not its affiliate.

Other jurisdictions In any other jurisdictions, except if otherwise restricted by laws or regulations, this report is intended only for qualified, professional, institutional or sophisticated investors as defined in the laws and regulations of such jurisdictions.

Emkay Global Financial Services Ltd.

CIN - L67120MH1995PLC084899

7th Floor, The Ruby, Senapati Bapat Marg, Dadar - West, Mumbai - 400028. India

Tel: +91 22 66121212 Fax: +91 22 66121299 Web: www.emkayglobal.com