POLICY ON BIOMASS ENERGY TECHNOLOGY -...

54

Submitted to UNITED NATIONS INDUSTRIAL DEVELOPMENT ORGANIZATION Submitted by DEVELOPMENT ENVIRONERGY SERVICES LTD 819, Antriksh Bhawan, 22 Kasturba Gandhi Marg, New Delhi -110001 Tel.: +91 11 4079 1100 Fax : +91 11 4079 1101; www.deslenergy.com December 2016 Policy Advisory Services in Biomass Technology in Pakistan POLICY ON BIOMASS ENERGY TECHNOLOGY SECOND DRAFT Version 1

Transcript of POLICY ON BIOMASS ENERGY TECHNOLOGY -...

Submitted to

UNITED NATIONS INDUSTRIAL DEVELOPMENT ORGANIZATION

Submitted by

DEVELOPMENT ENVIRONERGY SERVICES LTD

819, Antriksh Bhawan, 22 Kasturba Gandhi Marg, New Delhi -110001 Tel.: +91 11 4079 1100 Fax : +91 11 4079 1101; www.deslenergy.com

December 2016

Policy Advisory Services in Biomass Technology in Pakistan

POLICY ON BIOMASS ENERGY TECHNOLOGY

SECOND DRAFT Version 1

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 2 of 54

DISCLAIMER

This report (including any enclosures and attachments) has been prepared for the exclusive use

and benefit of the addressee(s) and solely for the purpose for which it is provided. Unless we

provide express prior written consent, no part of this report should be reproduced, distributed or

communicated to any third party. We do not accept any liability if this report is used for an

alternative purpose from which it is intended, nor to any third party in respect of this report

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 3 of 54

ACKNOWLEDGEMENT

This document has been prepared for the United Nations Industrial Development Organization

(UNIDO) under the project title “Policy advisory services (Biomass Energy Conversion

technologies)” under the SAP ID 100333: “Promoting sustainable energy production and use for

biomass in Pakistan”.

Development Environergy Services Ltd. (DESL) acknowledges the support provided by the

following UNIDO officials:

Mr. Alois Mhlanga, Project Manager

Mr. Ali Yasir, National Project Manager, Sustainable Energy, Biomass - Pakistan

Mr. Masroor Ahmed Khan, National Project Manager, Sustainable Energy RE & EE

Study Team

Team Leader Dr. GC Datta Roy Team member(s) Mr. R Rajmohan, Biomass technology expert

Mr. Qazi Sabir, National expert

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 4 of 54

CONTENTS

1 BACKGROUND ................................................................................................................................... 8

2 STATUS QUO.................................................................................................................................... 10

2.1 MACRO PERSPECTIVE .......................................................................................................................... 10

2.2 ARE DEVELOPMENT PERSPECTIVES ........................................................................................................ 12

2.3 BIOMASS ENERGY POTENTIAL & MARKET ................................................................................................ 14

2.4 POLICY & REGULATORY INITIATIVES ........................................................................................................ 17

2.5 TARGET & ACHIEVEMENT..................................................................................................................... 20

2.6 SUMMARIZING .................................................................................................................................. 21

3 BARRIERS AND CHALLENGES ........................................................................................................... 22

3.1 RESOURCE AVAILABILITY & PRICE ........................................................................................................... 22

3.2 TECHNOLOGY & BUSINESS MODELS........................................................................................................ 23

3.3 POLICY & REGULATORY UNCERTAINTY .................................................................................................... 24

3.4 ACCESS TO FINANCE ............................................................................................................................ 25

3.5 SUMMARISING .................................................................................................................................. 25

4 GLOBAL CASE STUDIES ..................................................................................................................... 27

4.1 MACRO-PERSPECTIVE ......................................................................................................................... 27

4.2 ILLUSTRATIVE CASE STUDIES .................................................................................................................. 30

4.3 SUMMARISING .................................................................................................................................. 36

5 POLICY RECOMMENDATIONS .......................................................................................................... 39

5.1 BASIC FRAMEWORK ............................................................................................................................ 39

5.2 HARMONIZATION OF INSTITUTIONAL PROCESSES ....................................................................................... 40

5.3 PROGRAM PLANNING .......................................................................................................................... 40

5.4 FISCAL & MONETARY INCENTIVES .......................................................................................................... 41

5.5 REGULATIONS ................................................................................................................................... 42

5.6 PROJECT FINANCING ........................................................................................................................... 43

5.7 PROJECT DEVELOPMENT ...................................................................................................................... 44

5.8 SUMMARIZING .................................................................................................................................. 45

ANNEX I- BIOMASS RESOURCES AVAILABILITY ......................................................................................... 46

ANNEX-2 BUSINESS CASE EXAMPLES........................................................................................................ 52

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 5 of 54

LIST OF TABLES

TABLE 1: BIOMASS ENERGY ECONOMIC BENEFITS ....................................................................................................... 13

TABLE 2: LCOE POWER FROM DIFFERENT SOURCES .................................................................................................... 13

TABLE 3: AVAILABLE BIOMASS FOR ENERGY GENERATION............................................................................................. 14

TABLE 4: BIOMASS ENERGY POTENTIAL ESTIMATE ...................................................................................................... 15

TABLE 5: SUITABILITY OF TECHNOLOGIES FOR DIFFERENT MARKETS ................................................................................ 17

TABLE 6: ARE ACHIEVEMENT-2015 ....................................................................................................................... 21

TABLE 7: BARRIER ANALYSIS .................................................................................................................................. 25

TABLE 8: POLICIES IMPLEMENTED BY VARIOUS COUNTRIES ........................................................................................... 29

TABLE 9: FINANCIAL INCENTIVE SCHEMES IN CHINA .................................................................................................... 31

TABLE 10: FINANCIAL INCENTIVE ............................................................................................................................ 33

TABLE 11: BIOMASS POWER IN INDIA ...................................................................................................................... 34

TABLE 12: SUMMARY OF POLICIES IN SELECT COUNTRIES ............................................................................................. 37

TABLE 13: SOURCE OF INFORMATION FOR THE FEEDSTOCK FOR BIOMASS POWER GENERATION IN PAKISTAN.......................... 46

TABLE 14: SOURCE OF CROPS PRODUCED IN PAKISTAN ............................................................................................... 48

TABLE 15: CRR VALUES FROM DIFFERENT SOURCES ................................................................................................... 49

TABLE 16: CALCULATION OF ESTIMATED ANNUAL SURPLUS BIOMASS PRODUCTION ........................................................... 49

TABLE 17: CALCULATION OF ESTIMATED ANNUAL SURPLUS BIOMASS PRODUCTION ........................................................... 50

TABLE 18: WOOD BASED RESIDUE .......................................................................................................................... 50

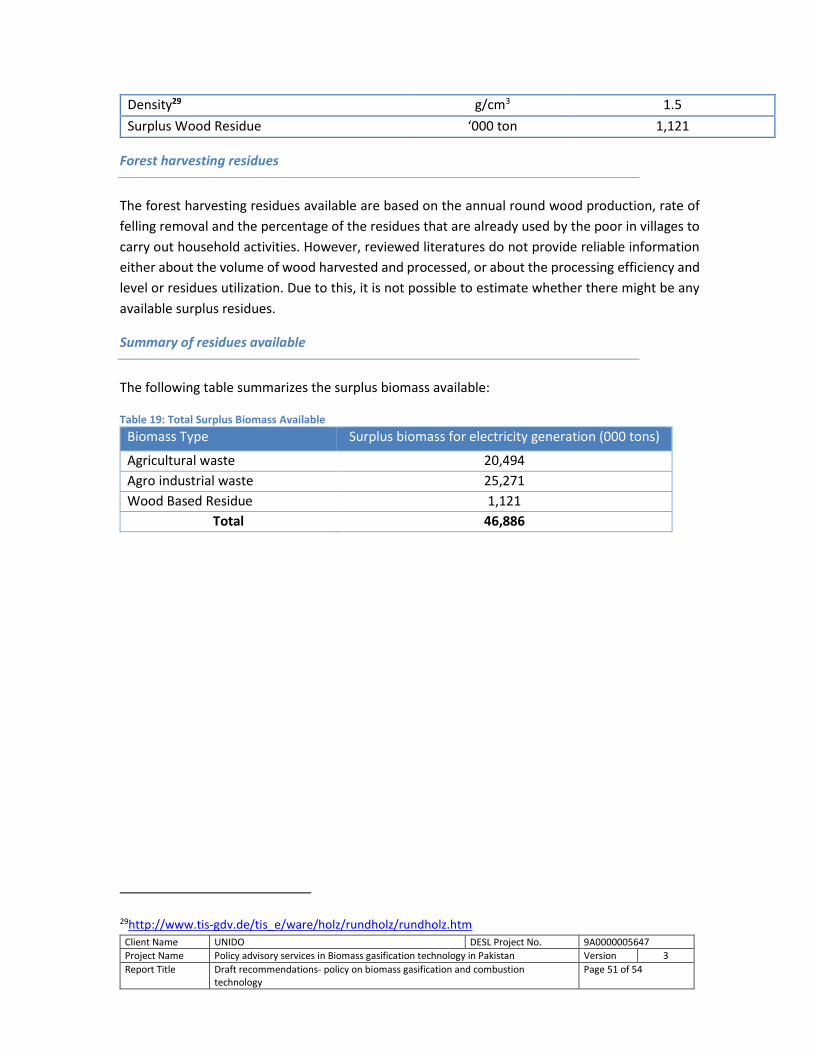

TABLE 19: TOTAL SURPLUS BIOMASS AVAILABLE ....................................................................................................... 51

LIST OF FIGURES

FIGURE 1: ENERGY MIX IN POWER GENERATION IN PAKISTAN ....................................................................................... 10

FIGURE 2: DISTRIBUTION OF UN-ELECTRIFIED VILLAGES IN PAKISTAN (2012) ................................................................... 11

FIGURE 3: DIFFERENT TYPES OF TECHNOLOGIES AVAILABLE FOR CONVERSION OF BIOMASS TO ENERGY .................................. 15

FIGURE 4: PROJECT DEVELOPMENT PATHWAY ........................................................................................................... 45

FIGURE 5: FEEDSTOCK FOR BIOMASS POWER GENERATION ........................................................................................... 46

FIGURE 6: SEQUENTIAL STEPS FOR THE ESTIMATION OF SURPLUS BIOMASS ...................................................................... 48

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 6 of 54

ABBREVIATIONS

ADB Asian Development Bank

AEDB Alternative Energy Development Board

AJK Azad Jammu & Kashmir

AMC Annual Maintenance Contract

ARE Alternative & renewable energy

BCT Biomass Combustion Technology

BET Biomass Energy Conversion Technologies

BGT Biomass Gasification Technology

CHP Combined heat and power

CDM Clean Development Mechanism

CHP Combined Heat & Power

CPP Captive power plant

CRR Crop Residue Ratio

DESL Development Environergy Services Ltd.

DISCOs Distribution Companies

DG Distributed generation

ESMAP Energy Sector Management Assistance Program

FBR Federal Board of Revenue, Government of Pakistan

FiT Feed in Tariff

GEF Global Environment Facility

GOP Government of Pakistan

GDP Gross Domestic Product

IA Implementation Agreement

IEA International Energy Agency

IEP Integrated Energy Plan

INR Indian Rupee

IPP Independent Power Plant

LNG Liquefied Natural Gas

LCOE Levelized cost of energy

MTDF Medium Term Development Framework

NEPRA National Electric Power Regulatory Authority

NGO Non-governmental organization

NTDC National Transmission and Dispatch Company

O&M Operation & Maintenance

PLF Plant Load Factor

PKR Pakistan Rupee

PPA Power Purchase Agreement

PPIB Private Power and Infrastructure Board

PPP Public private partnership

R&D Research and Development

RE Renewable Energy

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 7 of 54

RET Renewable energy technology

REC Renewable Energy Certificate

RPS Renewable Portfolio Standards

SME Small & Medium Enterprises

SRO Statutory Notification

THB Thai Baht

USC US cents

USD US Dollar

UNFCCC United Nations Framework Convention on Climate Change

UNIDO United Nations Industrial Development Organization

VAT Value Added Tax

WAPDA Water and Power Development Authority

UNITS OF MEASUREMENTS

Parameters UOM Kilo Calorie kCal Kilo Watt kW

Kilo Watt Hour kWh

Mega Watt MW Giga Watt Hour GWh

Thousand Metric Ton ‘000t

Tons per year TPY

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 8 of 54

1 Background With a large population of over 182 million1 and a rapidly developing economy, Pakistan’s energy

needs are potentially huge. The country, historically a net energy importer, is confronting

perpetual energy shortages as its economy and population grow. Pakistan is facing a demand-

supply gap of 4,500 to 5,500 MW2. The stability of the power system is being maintained by

resorting to load shedding, often extending to 12 to16 hours2. A large number of industries in

Pakistan are currently dependent on liquid fuels for meeting their electricity and heating needs.

Universal energy access is also a major issue in the country. Over 20,920 villages in the country are

yet to be electrified3. Government of Pakistan (GOP) has identified alternative and renewable

energy (ARE) as one of the options for bridging the demand supply gap. ARE resources would also

help in diversifying the resource base. Pakistan plans to add a minimum of 9,700 MW of renewable

energy generation capacity by 2030 as per the Medium Term Development Framework (MTDF)4.

GOP has initiated number of policy and institutional measures for promoting ARE technologies in

the different sectors of economy.

Ninety percent (90%) of the entrepreneurs in the industrial sector classified under the SME sector

account for 80% of the employment outside of agriculture and contribute over 40% of the

country’s GDP5. Shortage of energy, more specifically power has been having major impact on their

operation and global competitiveness. Large numbers of these units depend upon expensive and

polluting diesel generation units for meeting their power requirement. Industries such as rice mills,

wood processing mills, brick kilns etc also require heat energy. They are often burning fossil

fuel/biomass in inefficient ways. SMEs are now looking for alternative ways for improving their

energy security based on locally available energy resources, such as biomass and deployment of

efficient biomass-energy conversion technologies (BET). Such technologies have been successfully

deployed in a large number of countries such as China, India, Thailand, etc.

UNIDO with funding support from GEF is working with GOP or promoting efficient and market

based biomass energy technologies (BET, excluding biological processes) in industries in Pakistan.

Preparation of a set of policy recommendations for promoting BET in industries is a component of

the UNIDO program for which DESL has been contracted as Consultant through an international

competitive bidding process.

The objectives of the consulting assignment are two fold, viz. review of the current policies on ARE

and recommendations on specific measures for promoting BET and preparation of a draft on

1 World Bank Data for 2013 2 National Power Policy 2013, Government of Pakistan 3 Energy Access Assessment Punjab (Pakistan), ADB, December 2014 4 Policy for development of renewable energy for power generation, Government of Pakistan, 2006 5 TOR of the present project

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 9 of 54

technical quality standards for BET for sustainable performance of such technologies (imported as

well as locally manufactured) in the country.

The Consultant has carried out desk as well as field studies, including individual interactions with

a few stakeholders in order to understand the current scenario, BET opportunities and

development challenges. The first drafts on ‘quality standards’ and ‘policy recommendations’ have

been prepared based on the findings of these studies. The draft report on quality standards has

been submitted.

This report has been prepared on policy recommendations and structured under the following

sections:

Status quo

Barriers & challenges

Global review-successful case studies

Policy recommendations

The section ‘status quo’ has been prepared highlighting the current energy scenario and the GOP’s

policy initiatives for promotion of ARE technologies. The potential of BET has been assessed based

on the data available from the recently concluded study on biomass availability in the country.

Overall achievement against the set target indicates very low level of diffusion of ARE technologies

in the country. A number of barriers & challenges have been identified based on review of the

various policy documents, published papers and articles on BET market in Pakistan and informal

interaction with few stakeholders. Review of case studies on BET proliferation in China, India and

Thailand has helped in identifying specific institutional and policy measures that can help Pakistan

in overcoming the barriers and challenges. Specific policy recommendations have been prepared

taking into consideration the existing policies for promotion of ARE and lessons learned from

successful implementation of BET in the above-cited countries.

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 10 of 54

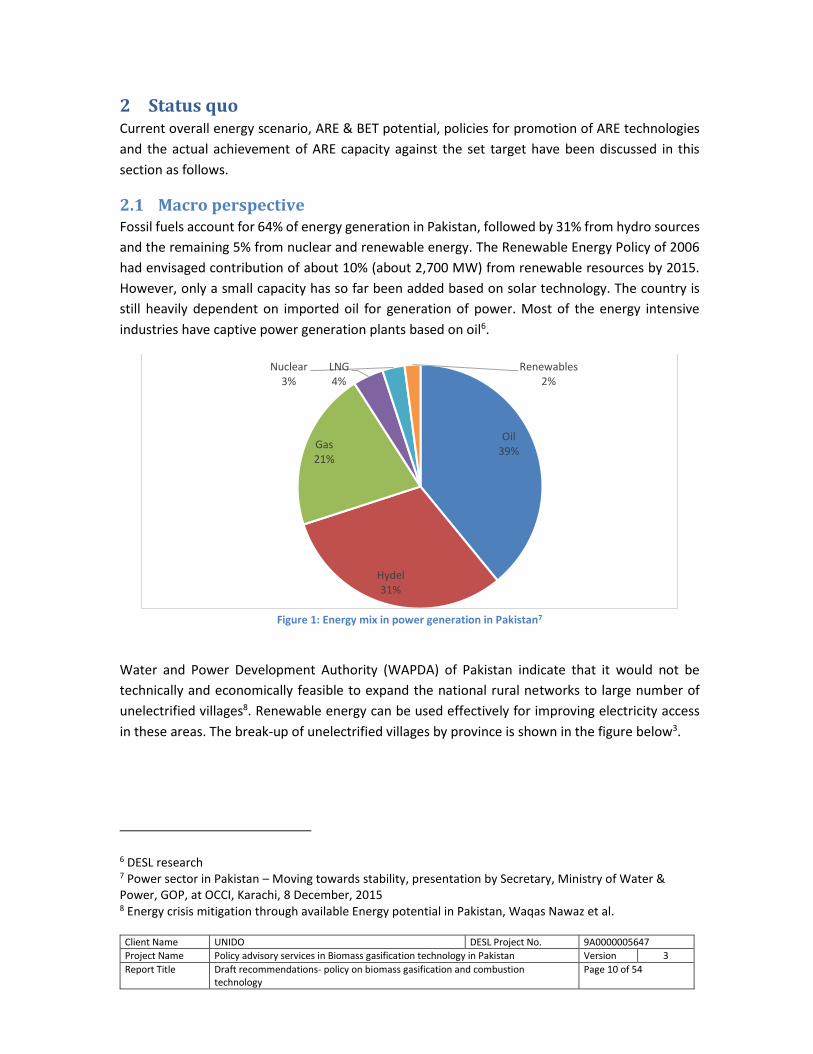

2 Status quo Current overall energy scenario, ARE & BET potential, policies for promotion of ARE technologies

and the actual achievement of ARE capacity against the set target have been discussed in this

section as follows.

2.1 Macro perspective Fossil fuels account for 64% of energy generation in Pakistan, followed by 31% from hydro sources

and the remaining 5% from nuclear and renewable energy. The Renewable Energy Policy of 2006

had envisaged contribution of about 10% (about 2,700 MW) from renewable resources by 2015.

However, only a small capacity has so far been added based on solar technology. The country is

still heavily dependent on imported oil for generation of power. Most of the energy intensive

industries have captive power generation plants based on oil6.

Figure 1: Energy mix in power generation in Pakistan7

Water and Power Development Authority (WAPDA) of Pakistan indicate that it would not be

technically and economically feasible to expand the national rural networks to large number of

unelectrified villages8. Renewable energy can be used effectively for improving electricity access

in these areas. The break-up of unelectrified villages by province is shown in the figure below3.

6 DESL research 7 Power sector in Pakistan – Moving towards stability, presentation by Secretary, Ministry of Water & Power, GOP, at OCCI, Karachi, 8 December, 2015 8 Energy crisis mitigation through available Energy potential in Pakistan, Waqas Nawaz et al.

Oil39%

Hydel31%

Gas21%

LNG4%

Nuclear3%

Renewables2%

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 11 of 54

Figure 2: Distribution of un-electrified villages in Pakistan (2012)

Similarly, high cost of power is adversely affecting the competitive position of the SME industries.

The cost of generation from diesel based system is touching over PKR 35.94/kWh against about

PKR 18.75/kWh for the cheaper alternative based on local gas. Government has set a target of

reducing the cost of generation to about USC 10/kWh by 2017 by moving towards cheaper fuel

including locally available coal and biomasses2.

Pakistan is richly endowed with renewable resources. Opportunities for solar energy exist in

Punjab province; wind energy in Sind and Balochistan provinces; Hydropower in north of Pakistan;

while bio-energy in all provinces. The federal government and some of the provincial governments

have been working on development and implementation of appropriate market conditions for

promoting renewable energy. The Quaid-e-Azam Solar Park in Punjab province is a major

accomplishment of these developmental efforts. Many of the development challenges such as

development of technology and local capacity, appropriate tariff, access and cost of finance and

other regulatory issues remain largely unresolved.

In case of BET, there is additional challenge of lack of information on availability of resources and

technology. The recently published biomass atlas with support from ESMAP would help in reducing

the information gap. Similarly, the feasibility studies carried out on application of biomass

gasification technologies (BGT) in rice mills and wood processing in Punjab province in the recent

past would help in specifically target the industries for promotion of BET.

With proper policy and coordinated actions from various institutions engaged in development of

power and renewable energy sectors in Pakistan, it would be possible to rapidly develop the ARE

market including market for BET in the country.

Sindh, 77%, 77%

Balochistan, 17%, 17%

Punjab, 3%, 3% KPK, 3%, 3%

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 12 of 54

2.2 ARE development perspectives Pakistan is abundantly endowed with renewable resources including solar, wind, biomass and

others. Until recently, reliable data and information on resource availability was not available.

AEDB with support from bilateral and multilateral agencies have undertaken survey of solar, wind

and biomass resources in the country. The survey work has been completed and data are being

processed for finalizing the resource estimate. Biomass atlas has been very recently released. This

would help in assessment of BET potential in the country. Meanwhile, some idea can be had from

the following macro level information on the renewable energy potential in the country.

The policy makers in Pakistan have long recognized the need for development of ARE. Benefits are

well acknowledged, more so considering the resource rich and energy starved situation. The

integrated energy plan 2009-2022 (IEP) has highlighted the following benefits from development

of ARE technologies in Pakistan9.

Energy security & independence

Diversity of supplies

Social cohesion (by deployment in remote, off-grid areas)

Environmental benefits

Job creation

Growth of local engineering industry

Image-building of the country as a socially conscious / responsible nation

Similarly, the policy for development of renewable energy for power generation 2006 (RE policy)

has also highlighted role of ARE technology in enhancing:

Energy security

Economic development

9 Integrated Energy Plan-EAC, Ministry of Finance, GOP, March 2009

Text box 1: Renewable resource potential

Wind: 340,000 MW (Theoretical)* 1760 MW in pipeline and abundant potential for development

Solar: 2,900,000 MW (Theoretical)*

Hydro (small/mini) 3,000 MW (Approx.)

Bagasse Cogeneration: 2,000 MW (Approx.)

Waste to Energy: 1,000 MW (Approx.)

Geothermal Studies underway

Alternative Fuels Potential being determined *Initial macro level assessment by NREL, USA in 2006

AEDB-June 2015

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 13 of 54

Social development &

Environmental improvement

The following table illustrates the magnitude of potential impact of BET system on local economic

and social development in a resource rich and energy starved country, estimated based on a case

study from India10.

Table 1: Biomass energy economic benefits

Particulars Million PKR /year Remarks

Rural income-biomass sale & employment

230,000 INR 1,500 -2,000/T of biomass (Fuel sale plus logistics); 2 to 4 man days/year/T of biomass

Fuel substitution-Agri pumps 140,000 Estimates by Petroleum Planning and Analysis Cell of Diesel consumption in agri pumps in India

Fuel substitution-lighting 140,000 NSSO Survey of kerosene based lighting in India

Carbon monetized 40,000 Corresponding to around 200 million tCO2eq

Reduction in utility T&D loss Not quantified -

Reduction in health cost Not quantified -

Total 550,000

The levelised cost of energy from BET system often provides the least cost solution as would be

seen from the following table assessed for India10.

Table 2: LCOE power from different sources

Technology LCOE-delivered electricity (PKR/kWh)

Small Hydro 7.2

Biomass 8.95-11.72

Wind 9.5

Solar PV 31.56

Diesel 33.41

Greater use of indigenous biomass resources can help diversify Pakistan’s energy mix and reduce

the country’s dependence on any single source, particularly imported fossil fuels, thereby

militating against supply disruptions and price fluctuation risks.

When properly assessed for their externalities, BET options can become economically competitive

with conventional supplies, on at least cost basis. This is particularly true for the more difficult,

10 Draft Biomass energy roadmap-Ministry of New and Renewable Energy, Government of India, 2011

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 14 of 54

remote, and under developed areas, where biomass can also have the greatest impact and the

avoided costs of conventional energy supplies can be significant.

Local environmental and health impacts of unsustainable and inefficient traditional biomass fuels

and fossil fuel -powered electricity generation can be largely circumvented through clean, BET

alternatives. Similarly, displaced greenhouse gas emissions carry significant global climate change

benefits, towards which Pakistan has pledged action under the UN Framework Convention on

Climate Change (UNFCCC) including, recently ratifying the Paris Climate Change Agreement.

2.3 Biomass energy potential & market

2.3.1 Availability of biomass resources

Pakistan is richly endowed with biomass resources, though overall energy potential is yet to be

scientifically determined. Biomass (other than habitat and animal wastes) resources are generated

from agricultural, agro industrial and forestry operations. The main constituents from the different

sources are:

Agricultural-Stalk, straws & trashes

Agro-industrial-Bagasse, paddy husks & shells

Forestry-Wood chips, barks & trims and river side greens

Methodologies for assessment of available surplus from the different sources are now well

established. Data on actual production of crops, crop residue ratio and current uses of the residues

are used for determination of surplus biomass from the agriculture. Generation of agro-industrial

residues such as husk and wood chips can be computed taking into account the actual production

and the normative residue generation ratios. It would be necessary to carry out primary survey for

assessment of availability of riverside green and statistical information on production of this may

not be available.

Energy Sector Management Assistance Program (ESMAP) of the World Bank has carried out

detailed resource mapping for wind, solar and biomass resources. DESL has estimated the available

surplus biomass, which can be utilized for energy production taking into account production

estimates in the ESMAP report and applying various validation factors based on DESL project

experiences. The following table shows the estimate of available biomass for power generation.

Table 3: Available biomass for energy generation

Biomass type Availability (000 tons)

Agricultural waste 20,494

Agro industrial waste 25,271

Wood Based Residue 1,121

Total 46,886

This estimate has been determined taking into account the information available from the biomass

atlas and the methodology used by DESL for assessment of surplus biomass for energy. Details are

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 15 of 54

provided at Annex-I. This methodology can be used by AEDB and prospective developed of BET

projects for assessment of biomass availability in a particular project area and configuration of the

plant capacity.

2.3.2 Biomass energy conversion technologies

Following chart shows different types of technologies for conversion of biomass to different forms

of energy.

Figure 3: Different types of technologies available for conversion of biomass to energy

In the context of the current project, combustion and gasification are more relevant. Almost all

types of biomasses can be utilised as fuel in the combustion based projects. Woody biomass such

as husks and wood chips are good fuel for gasification. Some of the semi woody biomass such as

corncobs and corn stalks can also be used for gasification. Leafy biomass such as straw and stalks,

on the other hand, would have to be densified (pellets) for gasification.

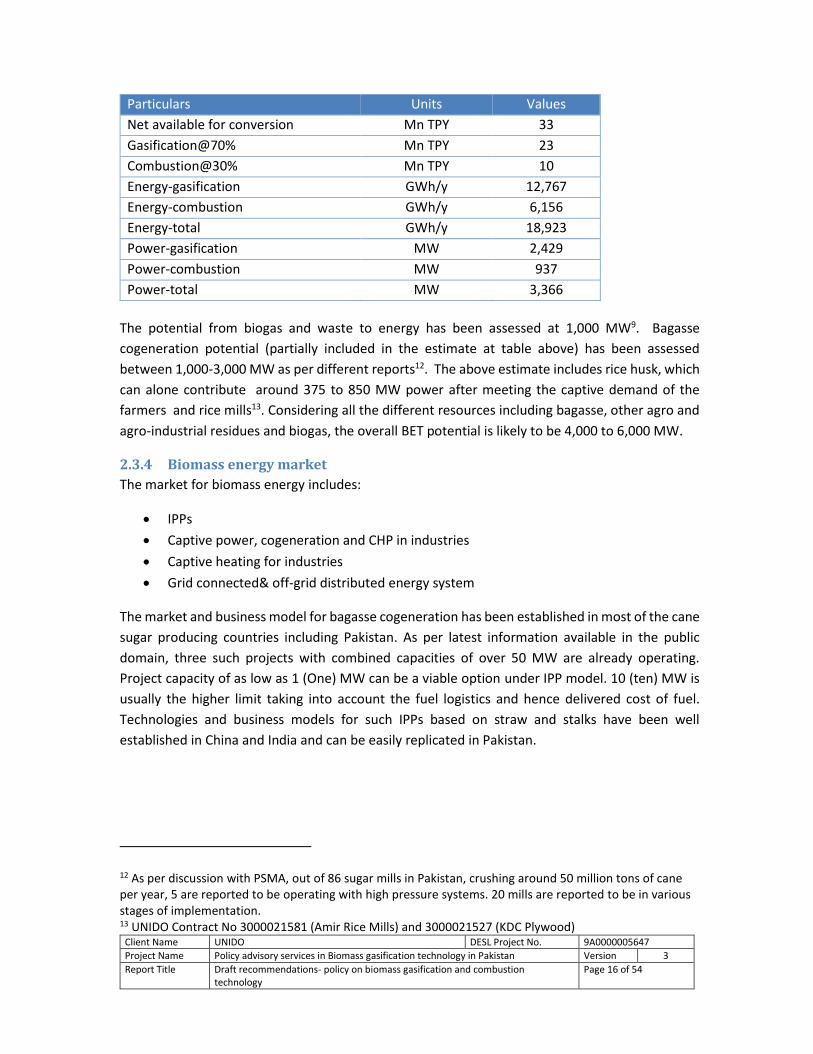

2.3.3 Biomass energy potential

The energy conversion potential has been assessed considering the following assumptions11:

Harvesting & logistics efficiency: 70%

GCV: 4,000 kCal/kg on dry basis: 3,000 kCal/kg on as received basis

Specific fuel consumption-gasification: 1.8 kg/kWh on as received basis

Specific fuel consumption-combustion: 1.6 kg/kWh on as received basis

Average plant load factor-gasification: 60%

Average plant load factor-combustion: 75%

Assuming a ratio of 70:30 between gasification and combustion overall potential has been

estimated as shown in the following table.

Table 4: Biomass energy potential estimate

Particulars Units Values

Biomass surplus estimate Mn TPY 47

Harvesting, logistics efficiency Factor 0.7

11 DESL database on BET projects

Technologies for biomass to energy

Biochemical Conversion

Anaerobic Digestion

Ethanol Fermentation

Lignocellulosic Conversion

Thermochemical Conversion

CombustionBiomass

GasificationBiomass Pyrolysis

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 16 of 54

Particulars Units Values

Net available for conversion Mn TPY 33

Gasification@70% Mn TPY 23

Combustion@30% Mn TPY 10

Energy-gasification GWh/y 12,767

Energy-combustion GWh/y 6,156

Energy-total GWh/y 18,923

Power-gasification MW 2,429

Power-combustion MW 937

Power-total MW 3,366

The potential from biogas and waste to energy has been assessed at 1,000 MW9. Bagasse

cogeneration potential (partially included in the estimate at table above) has been assessed

between 1,000-3,000 MW as per different reports12. The above estimate includes rice husk, which

can alone contribute around 375 to 850 MW power after meeting the captive demand of the

farmers and rice mills13. Considering all the different resources including bagasse, other agro and

agro-industrial residues and biogas, the overall BET potential is likely to be 4,000 to 6,000 MW.

2.3.4 Biomass energy market

The market for biomass energy includes:

IPPs

Captive power, cogeneration and CHP in industries

Captive heating for industries

Grid connected& off-grid distributed energy system

The market and business model for bagasse cogeneration has been established in most of the cane

sugar producing countries including Pakistan. As per latest information available in the public

domain, three such projects with combined capacities of over 50 MW are already operating.

Project capacity of as low as 1 (One) MW can be a viable option under IPP model. 10 (ten) MW is

usually the higher limit taking into account the fuel logistics and hence delivered cost of fuel.

Technologies and business models for such IPPs based on straw and stalks have been well

established in China and India and can be easily replicated in Pakistan.

12 As per discussion with PSMA, out of 86 sugar mills in Pakistan, crushing around 50 million tons of cane per year, 5 are reported to be operating with high pressure systems. 20 mills are reported to be in various stages of implementation. 13 UNIDO Contract No 3000021581 (Amir Rice Mills) and 3000021527 (KDC Plywood)

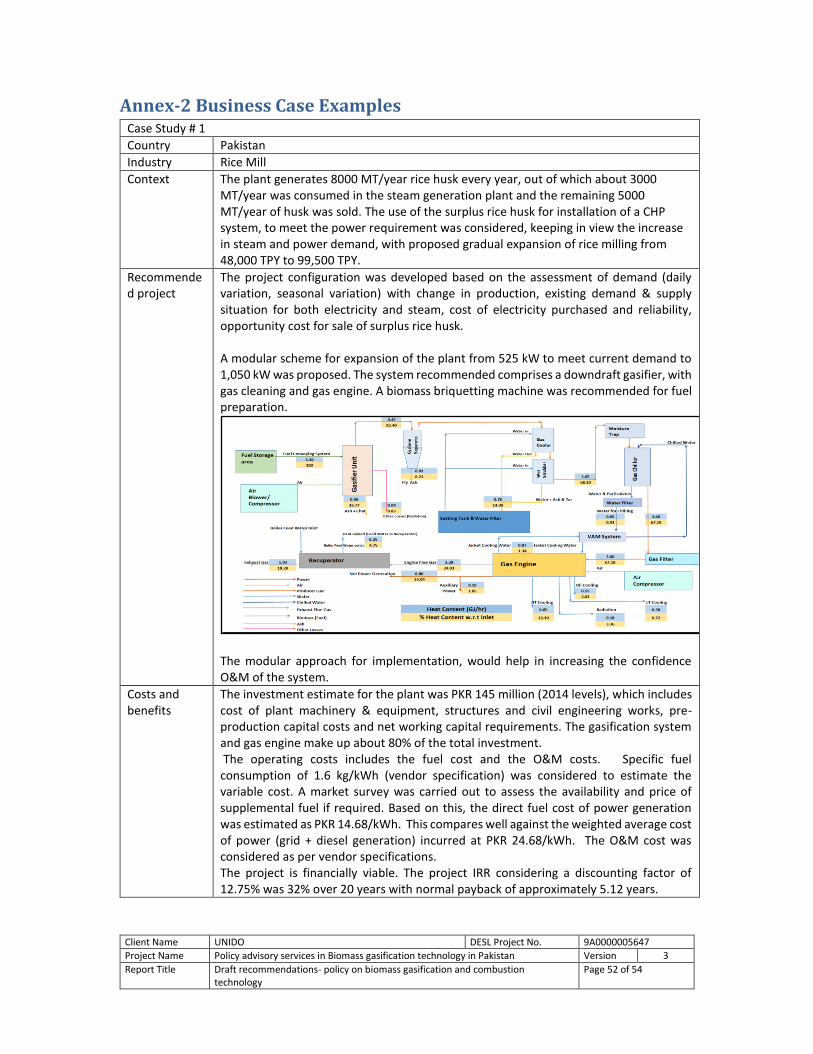

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 17 of 54

The energy demand for SME industries like rice mills, plywood-processing industries in Pakistan

were evaluated by the consultant under a previous assignment from UNIDO13. The following

project modules were identified as feasible option based on gasification technology.

Rice milling industry: 25 kW -1,050 kW

Plywood industry: 100 kW – 300 kW

Electricity demand for villages has been assessed considering average 50-60 households per village

and electricity consumption of 50 to 120 kWh/day14. The capacity of a BGT system to suit their

requirements has been estimated to range from 25 to 75 kW. Thus, the BET market is likely to be

quite diverse in nature with individual project capacities ranging from 25 kW to over 1 MW and

based on both combustion and gasification technologies.

Table 5: Suitability of technologies for different markets

Market segment Typical size of power demand (kW) Technology suitability

Independent power plants Minimum size for BCT 1 MW BCT

Industries (Captive power demand)

Rice mill – 25 - 1,050 kW Plywood Industry – 100 - 300 kW

BGT & BCT

Un-electrified villages 25-75 kW/village BGT

In the short-term period, it is expected that the uptake of the BGT/BCT technologies would take

place in the industries generating biomass resources (like rice mills, wooden furniture/plywood

industry etc.). Diffusion of BGT for rural distributed generation (DG) system on the other hand may

take time and would be largely governed by support from the government and the NGO

community and rural energy supply companies, which may get formed with fund support from

global donor communities.

2.4 Policy & regulatory initiatives Policy makers in Pakistan have duly recognized the important role of renewable resources and ARE

technologies. This is evidenced by the continued development of the institutional and policy and

regulatory processes for promoting ARE technologies. Some of the key initiatives include:

NEPRA Act-1997

Policy for development of renewable energy for power generation-2006

Bagasse cogeneration policy-2008

Integrated energy plan-2009-2022

AEDB Act-2010

14 Energy Access Assessment Punjab (Pakistan), ADB, December 2014 and “Electrification of villages: A

case study of Mastung village near Quetta (Pakistan)”, Syed Zafar Ilyas, S.M. Nasir and S. M. Raza,

Research Gate, April 2015

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 18 of 54

Provisions in the Finance Act-2015

2.4.1 Institutional mechanism

The roles and responsibilities of the various players involved in developing the energy system in

the country and promotion of ARE technologies have been clearly defined in the various Acts &

policy documents. These are briefly summarized as follows.

Ministry of Water & Power

The federal Ministry of Water and Power is the GOP’s executive arm for all issues relating to

electricity generation, transmission & distribution, pricing, regulation, and consumption in the

country. It exercises this function through its various line agencies as well as relevant autonomous

bodies. It also serves to coordinate and plant the nation’s power sector, formulate policy and

specific incentives, and liaise with provincial governments on all related issues.

National Electric Power Regulatory Authority

The National Electric Power Regulatory Authority (NEPRA) was established under an act of the

Parliament (Regulation of Generation, Transmission and Distribution of Electric Power Act, 1997,

also known as the ‘NEPRA Act’) to function as an independent regulator and ensure a transparent,

competitive, commercially oriented power market in Pakistan.

The authority’s main functions include, inter alia, issuing licenses for generation, transmission and

distribution of electric power; establishing and enforcing standards to ensure quality, safety and

proper accounting of operation and supply of electric power to consumers; approving investment

and power acquisition programs of the utility companies; and determining tariffs for bulk

generation and transmission and retail distribution of electric power.

Alternative Energy Development Board

Alternative Energy Development Board (AEDB) is the sole representing agency of the Federal

Government. AEDB was established in May 2003 with the main objective to facilitate, promote

and encourage development of renewable energy in Pakistan and with a mission to introduce

Alternative and Renewable Energies (AREs) at an accelerated rate. The administrative control of

AEDB was transferred to Ministry of Water and Power in 2006.

AEDB is tasked with implementing government policies and plans, developing projects, promoting

local manufacturing, creating awareness and facilitating technology transfer, channeling

international assistance, and coordinating all associated activities as the national facilitating

agency for development of renewable energy in the country.

Private Power Infrastructure Board

The Private Power and Infrastructure Board (PPIB) was created in 1994 as "one window facilitator"

to promote private sector participation in the power sector of Pakistan. PPIB facilitates investors

in establishing private power projects and related infrastructure, executes Implementation

Agreement (IA) with project sponsors and issues sovereign guarantees on behalf of the

Government of Pakistan.

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 19 of 54

Provincial and AJK Agencies

Provincial and Azad Jammu and Kashmir (AJK) governments support the implementation of

renewable energy projects within their geographical jurisdiction. In most of the provinces,

institutional structure is well established and working on target oriented programs. Some of these

programs are initiated at the province level or in collaboration with the AEDB.

Power Utilities

Electricity utilities in Pakistan comprise four generating companies (Southern, Central, Northern,

and Lakhra), WAPDA Hydel wing and ten separately corporatized distribution companies (DISCOs:

Lahore, Gujranwala, Faisalabad, Islamabad, Multan, Peshawar, Hyderabad, Quetta, Sukkur and

Tribal Areas) serving different regions of Pakistan and a private integrated company, the Karachi

Electric Supply Corporation (KESC), serving the Karachi metropolitan area.

2.4.2 Transparency in regulations

Establishment of NEPRA and promulgation of NEPRA Act 1997 has cleared the pathway for

regulation of the power sector in the country in a transparent manner. Promulgation of AEDB Act

2010 has further clarified the processes for regulation of the development of ARE technologies.

Regulatory processes have been well established for determination of tariff for different types of

ARE projects. Feed-in-tariffs for smaller scale solar PV projects have been notified by the NEPRA.

Utilities are now mandated for purchase of all the energies available from the renewable

resources. Regulations on grid connectivity, wheeling and banking of power too have been

notified. Net metering has been notified for solar PV projects.

Monetary & fiscal incentives

The integrated energy plan, 2009-20229 had recommended creation of an alternative energy fund

and development of soft financing scheme for ARE projects. It also recommended incentives to the

provincial, city and local governments for development of ARE projects.

Text box 2: Regulations & incentives

Resource Risk is not shifted to Project Sponsor

Guaranteed Electricity purchase

Grid provision is the responsibility of the Power Purchaser

Protection against political risk & change in law

Attractive Tariffs – Cost Plus and Upfront Tariff Regimes

Guaranteed Return on investment is between 17% to 18% (IRR)

No Import Duties on Equipment

Zero Sales Tax

No Income Tax / withholding tax / turnover tax

Convertibility of PKR into USD

AEDB-June 2015

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 20 of 54

The Renewable Energy Policy, 2006 foresees that a market would be developed in the long run for

ARE technologies, which would be competitive against the conventional energy projects on their

own merits. However, in the shorter term it provides for incentives consisting of:

Risk mitigation against resource uncertainty (particularly for wind projects)

Production incentives beyond benchmark output

Facilitating monetization of carbon

Payment securitization by the Government of Pakistan for the private sector investors

Permitting generating companies to issue corporate bonds

Permitting issuance of share at discounts to equity investors/venture capitals

ARE technologies have also been exempted from custom duty, sales tax, income tax

including turnover tax and withholding tax on imports.

The Financing Act 2015 provides for duty free import of large number of equipments and

components for development of ARE projects in the Solar, Wind & Geothermal segments. It also

provides for concessional duty for some equipment such as harvesting, threshing and storage

equipments, which are normally required for larger scale BET projects. The Act also provides for

inclusion of any other item approved by AEDB & concurred by FBR.

Repatriation of equity and dividends are freely allowed subject to approval of State Bank of

Pakistan.

2.4.3 Project development alternatives

Policy on development of projects under different modes (IPP, grid connected CPPs, off-grid CPPs

& other projects) has been clearly outlined in the RE policy 2006. Currently, only IPPs require

licensing from government. The policy also provides for de-licensing of small-scale projects (<5

MW for small hydro and <1 MW net export for others).

Development options for IPPs too have been well structured under the solicited and unsolicited

categories. AEDB has been empowered to provide one-window facility for project development

and regulatory powers for the same subject to approval of the rules from the Government.

The integrated energy plan envisages initiatives from public sector for development of pilot and

demonstration projects as well as off-grid projects for rural electrification. AEDB too has been

empowered for setting up such projects on its own or through PPP models.

Procedure and processes for bid evaluation, selection and implementation of bid projects have

been established and several projects already implemented.

2.5 Target & achievement The Integrated Energy Plan 2009-22 envisaged achieving 12% of the energy pie from the renewable

resources by 2012 and induction of 17,400 MW power to the grid from solar and wind power by

2022. The policy for development of renewable energy for power generation (2006) had fixed a

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 21 of 54

more modest target of 9,700 MW by 2030 in the medium term framework. As against these

targets, about 400 MW projects have been set up by 2015 contributing to about 1.6% of the overall

installed capacity.

Table 6: ARE achievement-2015 Source MW GWh % (MW) % (GWh)

Hydro 7,115 32,074 28.3% 33.50%

Thermal 16,600 58,177 66.1% 60.77%

Nuclear 987 4,996 3.9% 5.22%

ARE

Wind 256 457 1.0% 0.48%

Solar 100 26 0.4% 0.03%

Bagasse 51 NA 0.2% NA

Total 25,109 95,730 100% 100%

ARE-total 407 483 1.6% 0.5%

2.6 Summarizing It can be concluded that large number of policy and regulatory measures have been initiated for

development of the ARE technologies in the country. The institutional framework is also there for

development of the sector. The focus of the various measures so far has been solar and wind. Even

for solar and wind, actual achievement so far is very small compared to the potential. The biomass

energy is yet to make a beginning. The current scenario in Pakistan is not unique. Almost all

countries have faced similar situations in the initial phase of development due to number of

barriers faced against development of market for ARE technologies. Some of the barriers are

universal and some country specific. It becomes critically important to identify such barriers in an

ongoing manner and take action for overcoming the same.

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 22 of 54

3 Barriers and challenges Major barriers & challenges are faced in developing market for ARE technologies, more so for BETs

due to number of real and perceived risks such as:

Resource availability & price

Untested technology & business models

Policy & regulatory uncertainty

BET projects are also considered less attractive by Bankers/Equity & Venture funds due to several

factors such as:

Lower scalability

Smaller project investment size

Higher cost of transaction for loan processing

Major financing barriers are therefore, faced by BET project developers.

For Pakistan, these issues have to be contextualized better for development of targeted policy

and regulatory measures for promotion of BETs.

3.1 Resource availability & price Risk profile of a biomass project varies widely depending upon the biomass sourcing option and

quantitative requirement. It is negligible for bagasse cogeneration project as the entire quantity of

resources is available from internal operation. This would be somewhat true for rice mills so long

the entire requirement is met from the internal milling operation. For smaller village projects too,

the risk is low as the requirement can be mostly met locally, though pricing issues could arise. For

the IPPs, on the other hand, this risk is high as the entire quantity of fuel is sourced from outside

and mostly through informal arrangement. Seasonality of availability of agricultural residues poses

Text box 3: Financing barrier

Different RETs have different degrees of exposure to the various identified barriers and risks.

Barriers are created by underdeveloped financial markets. Examples of barriers include lack of long-

term loans, high financing costs, high transaction costs, and poorly capitalized developers.

Risks refer to the high risks and costs of RETs. They include cost competitiveness, technology risks,

regulatory risks specific to making RETs competitive, and resource risks. The paper considers how

well different financing instruments address different barriers and risks. The list of instruments

covered includes grants, equity, debt, asset-backed classes, guarantees, and insurance as well as

more targeted categories such as results-based financing, carbon financing, and small-scale project

financing.

Financing renewable energy-World Bank/Climate investment funds

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 23 of 54

yet another challenge. The requirement for the entire year has to be procured in a short time

during the harvesting season and stored for utilization during the whole year.

Almost the entire quantity of paddy husks and wood chips are being currently utilized in boilers

and furnaces in the SME industries in Pakistan. Surplus from these sources can be generated only

by improving efficiencies of the existing systems. Opportunities for the same exist but would

require investment in upgradation.

Plentiful straws and stalks are available. Harvesting and logistics management systems for these

would have to be developed. In absence of an existing market, farmers are unlikely to make

investment for this. IPP projects would have to therefore, take into account investment in fuel

management system in addition to the power plants. This would potentially increase the risk

profile of the projects.

IPPs therefore, face multiple risks such as availability, management of logistics, price escalation

and storage degradation. The Consultants has prepared and submitted a separate report on

biomass management and pricing.

3.2 Technology & business models Biomass combustion technologies for fuels such as paddy husk and wood chips are matured and

large numbers of such plants are operating all over the world. SME industry in Pakistan too is using

these fuels in low-pressure boilers, though at much lower efficiencies. Gasification technology for

wood chips is well established. Technology for gasification of husks has also been developed and

numbers of such plants are operating in China, India, and Thailand. Technology for stalk gasification

has been developed mainly in China. Very large numbers of rural energy projects are being

operated for supply of heat and a few supplying both heat and power.

Technology for energy production from straw is still going through the learning curve. The first

such commercial project on straw outside of Europe was developed in India about a decade back.

Few such projects are operating mostly in the northern States of Punjab and Haryana. In the recent

past, China has made rapid stride in developing straw firing technology. Large numbers of such

projects with individual capacity ranging from 8 to 12 MW have been operating successfully in

paddy and wheat growing provinces11.

Strong collaboration between the research & development institutions and the local

manufacturing industries with support from Governments has been mainly responsible for success

in developing such technologies in China, India & Thailand. Such collaboration arrangements have

also helped in developing local capacity for servicing such projects, one of the key condition

precedents for sustainability of operation.

Business models for IPPs have been well established in Pakistan. It should be possible to replicate

the same for BET based IPPs too. However, such models do not exist for other types of projects.

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 24 of 54

This would require development of technical and financial capacities of all the stakeholders

involved in promoting and developing BET businesses.

Rural distributed generation projects would face even more challenges as have been experienced

in India. Some of the major issues that have to be addressed are:

Ownership models

Operation models

Regulations

Pricing of resources & delivered energy

Affordability

Willingness to pay

Cash flow

3.3 Policy & regulatory uncertainty Review of the policy and regulatory framework indicates existence of few gaps that have to be

addressed for faster diffusion of ARE & BET. Tariff issue may remain as the single most important

regulatory barrier. Government seems to have the final say in determination of tariff as would be

seen from the following provision of the NEPRA Act 1997 on power of the NEPRA.

Section 7 (3) (a)

“Determine tariff, rates, charges and other terms and conditions for supply of electric power

services by the generation, transmission and distribution companies and recommend to the Federal

Government for notification”.

Similarly, the provincial Governments have been empowered to notify tariff for projects

implemented within the jurisdiction of Provinces.

Feed-in-tariff (FiT) has been notified only for small-scale solar and bagasse cogeneration projects.

Transparent guideline of process of tariff determination and regulations are yet to be established.

This issue would be even more complex for BET projects. Regulators would find it difficult to

determine the fuel prices for BET projects in absence of a formal market for biomass resources

AEDB Act 2010 does not provide enough administrative and financial power to the Board for

promoting ARE technologies. AEDB can as best play the role of a facilitator. IPP project developers

would have to go through the existing procedures and processes applicable for conventional

projects. Developers of small-scale BET projects would find it extremely difficult and cumbersome

to go through such processes for getting various permits and clearances. Historically, power

purchase agreements are reported to be abruptly terminated, and developers would like all

uncertainties about reliability of agreements to be removed.

The mechanisms for inter-institutional coordination have not been articulated in the relevant

documents. This concern has been highlighted in the IEP document-“If a Ministry of Energy cannot

be formed then a high powered body with legislative powers, authority and necessary

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 25 of 54

empowerment and resources should be established at the earliest to drive Pakistan’s energy

development in the right direction and in the most optimum way possible”.

It has also been highlighted that most of the institutions involved in developing the ARE market do

not have adequate capacity to undertake the policy development and implementation related

activities.

3.4 Access to finance BET project developers in Pakistan would find it difficult to finance such projects even if all the

policy and regulatory aspects are addressed. This has been the experience in both China and India

in the initial development stages.

The IEP9 had made several recommendations for creating an enable environment for financing of

such projects. These included both financing and market mechanisms such as:

Financing mechanisms

o Alternative energy fund for setting up pilot projects & soft financing of

demonstration & R&D projects

o Monetary incentives to provincial, city and local governments for RET projects

Market instruments

o RET obligation for utilities

o RPS for DISCOs

o Mandatory use of feasible RET projects in the Government & public sector

buildings

AEDB Act has also provision for implementation of projects by AEDB on its own or in partnership

with private sector. These policy- intents are yet to be converted to implementable action

agenda.

3.5 Summarising DESL has been involved in policy related as well as project development work in the BET domain

globally including in China and India. The potential impact of the barriers discussed above on the

implementation front has been assessed for Pakistan as shown in the following table.

Table 7: Barrier analysis

Parameters Off-Grid rural electrification using BGT

IPP using BCT

Captive power generation using BGT

Resources (Biomass)

Availability & certainty

Medium High Medium

Technology

Availability High Low High

Service High Low Medium

Business models

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 26 of 54

Parameters Off-Grid rural electrification using BGT

IPP using BCT

Captive power generation using BGT

Price of electricity/tariff

High High Low

Cash flow High Medium Low

Policy & regulatory

Processes High High Low

Regulatory Low High Low

Access to finance High High Medium

Historically, every country has faced similar barriers. The following section of the report provides

a highlight on how different strategies have been adopted all over the globe for addressing such

barriers and challenges.

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 27 of 54

4 Global case studies

4.1 Macro-perspective Global renewable energy markets have grown rapidly in the past decade. Renewable energy

provided an estimated 19.1% of global final energy consumption in 20134. This growth has been

driven by supportive national and local policies. Declining costs have also played a significant role

in the expansion of renewable energy deployment in recent years. The global policy landscape has

driven the expansion of renewable energy technologies by attracting investment and creating

markets that have brought about economies of scale and supported technology advances.

Since 2004, the number of countries promoting renewable energy with direct policy support has

nearly tripled, from 48 to over 140, and an ever-increasing number of developing and emerging

countries are setting renewable energy targets and enacting support policies. The most commonly

used policies and their scope in brief are as followsError! Bookmark not defined.:

Resource mapping: Use of technology for real time mapping of available energy resources

Regulatory instruments

o Feed-in premium: a type of feed-in policy, where producers of electricity from

renewable sources sell electricity at market prices, and a premium is added to the

market price to compensate for higher costs and, thus, to mitigate the financial risks

of the production from renewables.

o Feed-in tariff: the basic form of feed-in policies, where a minimum price (tariff) per

unit (normally kWh or MWh) is guaranteed over a stated fixed-term period when

electricity can be sold and fed into the electricity network, normally with priority and

guaranteed grid access and dispatch.

o Net metering: a regulated arrangement in which utility customers who have installed

their own generating systems pay only for the net electricity delivered from the utility

(total consumption minus on-site self-generation).

o Mandate/obligation: a measure that requires designated parties (consumers,

suppliers, generators) to meet a minimum, and often gradually increasing, target for

renewable energy, such as a percentage of total supply or a stated amount of capacity.

Market instruments o Renewable energy certificate (REC): a certificate awarded to certify the generation of

one unit of renewable energy (typically 1 MWh of electricity, but also less commonly

of heat).

o Renewable energy target: an official commitment, plan or goal set by a government

(at the local, state, national or regional level) to achieve a certain amount of renewable

energy by a future date.

o Renewable portfolio standard (RPS): an obligation placed by a government on a utility

company, group of companies or consumers to provide or use a predetermined

minimum renewable share of installed capacity, or of electricity or heat generated or

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 28 of 54

sold;” RPSs often include tradable certificates, and they are referred to as tradable

green certificates (TGC systems) in Europe

Monetary & fiscal incentives

o Capital subsidy: a subsidy that covers a share of the upfront capital cost of an asset

(such as a solar water heater).

o Fiscal incentive: an economic incentive that provides individuals, households or

companies with a reduction in their contribution to the public treasury via income or

other taxes, or with direct payments from the public treasury in the form of rebates or

grants.

o Investment tax credit: a taxation measure that allows investments in renewable

energy to be fully or partially deducted from the tax obligations or income of a project

developer, industry, building owner, etc.

o Production tax credit: a taxation measure that provides the investor or owner of a

qualifying property or facility with an annual tax credit based on the amount of

renewable energy (electricity, heat or biofuel) generated by that facility.

A study on ‘Taxes, incentives for renewable energy’ by KPMG describes the taxes and incentives

provided by various countries around the world to promote renewable energy from wind, solar,

biomass, geothermal and hydropower. These policies also support other areas such as increased

energy efficiency, smart-grid management, bio-fuels, carbon capture systems and storage

technologies. It includes an introduction about global trends in renewable energy, a summary of

investments in renewable energy, and a brief outline of renewable energy promotion policies in

the countries.

[The policies implemented by the countries are classified into five sections, High Income Countries,

Upper Middle Income, Lower Middle Income, Low income countries along with policies in six South

Asian Countries. This is based on World Bank’s classification of world's economies on the estimates

of gross national income (GNI) per capita for the previous year that determines the lending

eligibility. As of 1 July 2015, low-income economies are defined as those with a GNI per capita of

$1,045 or less in 2014; middle-income economies are those with a GNI per capita of more than

$1,045 but less than $12,736; high-income economies are those with a GNI per capita of $12,736

or more. Lower-middle-income and upper-middle-income economies are separated at a GNI per

capita of $4,125.]

The incentives to deploy renewable technologies depend in part on a country’s socio-economic

situation. Industrialized and emerging economies may be keen to de-carbonize their energy system

or to improve energy security. Least Developed Countries, whilst sharing such motivations, are

likely to be more concerned with improving human development, which involves increasing rates

of energy access. Many Least Developed Countries have deployed RETs as a cost-effective means

of electrifying parts of their territory

The following table encloses the policies implemented by various countries:

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 29 of 54

Table 8: Policies implemented by various countries15

Type of Incentive No. of countries with full/partial (% of population) High

Income Countries

(43)

Upper Middle Income

Countries (41)

Lower Middle Income

Countries (30)

Low Income

Countries (24)

South Asian

Countries (6)

Pakistan

Renewable energy targets

41 (95%) 34 (83%) 25 (83%) 17 (71%) 6 (100%) Yes

Regulatory Policies

Feed-in-tariff/ premium payment

27 (63%) 21 (53%) 16 (53%) 5 (21%) 4 (67%) Yes

Electric utility quota obligation/RPS

16 (37%) 6 (15%) 6 (20%) 1 (4%) 2 (33%)

Net Metering 17 (40%) 13 (32%) 13 (43%) 0 (0%) 3 (50%) Yes

Tradable REC 20 (47%) 3 (7%) 3 (10%) 0 (0%) 1 (17%)

Tendering 21 (49%) 18 (44%) 13 (43%) 3 (13%) 3 (50%)

Heat obligation/ mandate

10 (23%) 5 (12%) 3 (10%) 1 (4%) 1 (17%)

Biofuels obligations/ mandate

29 (67%) 18 (44%) 9 (30%) 7 (29%) 2 (33%)

Fiscal incentives and public financing

Capital subsidy or rebate

28 (65%) 13 (32%) 11 (37%) 6 (25%) 4 (67%)

Investment or production tax credits

15 (35%) 11 (27%) 9 (30%) 2 (8%) 2 (33%)

Reductions in sales, energy, CO2, VAT and other taxes

28 (65%) 24 (59%) 20 (67%)

19 (79%) 3 (50%)

Energy production payment

9 (21%) 5 (12%) 6 (20%) 2 (8%) 2 (33%)

Public investment, loans or grants

25 (58%) 21 (51%) 12 (40%) 9 (38%) 5 (83%)

15KPMG:Taxes, incentives for renewable energy, 2014

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 30 of 54

At least 164 countries had renewable energy targets.

At least 145 countries had renewable energy support policies in place.

Low income, lower middle income as well as upper middle-income countries feature

fastest policy uptake during the last decade.

4.2 Illustrative case studies Development in China, India and Thailand has been taken up for more detailed analysis for their

relevance for developing BET in Pakistan.

4.2.1 China

China leads the world in total non-hydropower renewable energy capacity, with 70 GW installed

nation-wide (excluding hydropower) by the end of 2011. The incredible growth of China’s

renewable energy sector is due in large part to intentional and calculated action and will on part

of the government. Government of China has catalyzed the development by undertaking several

actions in parallel. Major interventions include setting a legal framework through the 2006

renewable energy law, articulating time-bound goals on RE deployment including diversifying its

energy mix, developing technology and manufacturing base, remunerative tariffs and payment of

fair price to the biomass producers.

In 2005, the government sent a clear signal that renewable energy development was a priority by

setting a target of 30GW of renewable energy by 2020. More recently in 2011, after far surpassing

its 30GW target, the government has reconfirmed its dedication by increasing the number of its

technology specific installation targets.

Text box 4: Biomass power in China

Based on the medium- to long-term development planning of renewable energy, Chinese Central

People’s Government has proposed the development goals for biomass power generation: by

2010, its installed capacity would be 5.5 GW (equivalent to generating capacity of 27.28 billion

kWh); by 2020, its installed capacity will be 30 GW (equivalent to generating capacity of 148.8

billion kWh). According to the “12th Five-Year Plan” of renewable energy, the development goal of

biomass power generation capacity has been determined, to be 13 GW during the next 5 years

(2010–2015). Based on the target of the planning, biomass power generation is more popular than

photovoltaic power generation in China In April 2011, the Ministry of Finance People’s Republic of

China (MFPRC), the National Energy Bureau (NEB) and the Ministry of agriculture of the People’s

Republic of China (MAPRC) together issued the “Interim Measures on assistance fund management

of green energy demonstration counties”. According to the Interim Measures, all of the “green

energy demonstration counties” will be subsidized with a total of $ 3.9 million, mainly for biogas

generation, biomass power generation projects and so on. According to the goal of “building 200

green energy demonstration counties by 2015”, biomass industry will receive a huge investment of

more than $ 3.1 billion.

Development goal of China’s 30 GW Biomass power-Science direct, Sept 2013

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 31 of 54

Technology development is a thrust area in the BET program in China. Every province has a

technical institute dedicated to development of technologies for conversion of locally available

biomasses and transfer of these technologies to the manufacturing companies. This has helped

China to become the most advanced technology supplier for BETs including for combustion,

gasification and waste-to-energy technologies. Financial incentive has been used as a strong policy

tool by China as would be seen from the following table.

Table 9: Financial incentive schemes in China

Year Law & Regulation Project

1999 Notice on issues of further supporting the development of renewable energy

Infrastructure loan for power generation projects of renewable energy which are arranged by bank

2% Finance discount

2006 Renewable Energy Law

Projects of poor profitability and strong public welfare. The projects in the guiding catalogue for industrial development of national renewable energy or the item meeting the credit qualifications

Free funding ; Interest payment on loans (interest rate<3%)

2009 Circular Economy Promotion Law of the People’s Republic of China

Comprehensive utilization and development of straw and gas

Establishing the relevant special fund for developing circular economy

Snapshot of the various components of China’s policy is as under:

Administrative

Mandatory market share (MMS): The National Development & Reform Commission

(NDRC) introduced mandatory market share (MMS, or “renewable portfolio standards”. In

regions served by centralized power grids, the share of power generation form non-hydro

renewable sources should reach 1% of the total by 2010 and 3% by 2020 according to the

plan.

Renewable Energy Targets: Significantly increased renewable energy targets would be set

for grid companies to provide more incentives to purchase renewable electricity.

The National Energy Administration (NEA) was given the responsibility of monitoring

compliance on a monthly basis.

Fiscal/Monetary

Government financial support for renewable energy projects: The Chinese government

also supports renewable energy projects by providing financial subsidies. Financial

funds/allowance: Special funds are made available to facilitate the development of

renewable energy relating to the following activities:

Client Name UNIDO DESL Project No. 9A0000005647

Project Name Policy advisory services in Biomass gasification technology in Pakistan Version 3

Report Title Draft recommendations- policy on biomass gasification and combustion technology

Page 32 of 54

o Scientific and technical research, standardization processes and model

engineering projects

o Renewable energy projects in rural and pastoral areas

o Construction of stand-alone electricity generation system in remote areas and

islands

o Renewable energy resource surveys, evaluation and construction of information

systems

o Localization of manufacturing facilities used in the renewable energy sector.

Financial subsidies for the development of “Model County for Green Energy” program for

the following qualified projects in rural areas:

o Concentrated provision of methane gas projects

o Biomass gasification projects

o Biomass briquette projects

o Other projects that develop and utilize renewable energies

o Rural energy service system.

China is encouraging local renewable equipment manufacturers through a range of tax

exemptions as well as direct financial support

Corporate Income Tax (CIT): A reduced CIT rate of 15 percent is granted to qualified

advanced and new technology enterprises.

The Clean Development Mechanism (CDM) Fund is exempted from CIT on some

specific Income

Regulatory

Tariff based support mechanisms for power generation from renewable energy sources:

Two main methods have been adopted—competitive tendering (government-guided

pricing; an auction mechanism) and FiTs (government-fixed pricing).

Market mechanism

Renewable energy certificates would be used to track the fulfillment of targets, but the

certificates had not yet been made tradable.

4.2.2 India

India has made rapid stride in developing renewable energy with over 28GW of installed capacity