PDAC Media Conference - Slides

13

PDAC 2020 Stephen McIntosh – Group Executive Growth & Innovation 2 March 2020

Transcript of PDAC Media Conference - Slides

PDAC 2020Stephen McIntosh – Group Executive Growth & Innovation2 March 2020

©2020, Rio Tinto, All Rights Reserved

Cautionary statements

2

This presentation has been prepared by Rio Tinto plc and Rio Tinto Limited (“Rio Tinto”). By accessing/attending this presentation you acknowledge that you have read and understood the following statement.

Forward-looking statementsThis document, including but not limited to all forward looking figures, contains certain forward-looking statements with respect to the financial condition, results of operations and business of the Rio Tinto Group.These statements are forward-looking statements within the meaning of Section 27A of the US Securities Act of 1933, and Section 21E of the US Securities Exchange Act of 1934. The words “intend”, “aim”,“project”, “anticipate”, “estimate”, “plan”, “believes”, “expects”, “may”, “should”, “will”, “target”, “set to” or similar expressions, commonly identify such forward-looking statements.

Examples of forward-looking statements include those regarding estimated ore reserves, anticipated production or construction dates, costs, outputs and productive lives of assets or similar factors. Forward-lookingstatements involve known and unknown risks, uncertainties, assumptions and other factors set forth in this presentation.

For example, future ore reserves will be based in part on market prices that may vary significantly from current levels. These may materially affect the timing and feasibility of particular developments. Other factorsinclude the ability to produce and transport products profitably, demand for our products, changes to the assumptions regarding the recoverable value of our tangible and intangible assets, the effect of foreigncurrency exchange rates on market prices and operating costs, and activities by governmental authorities, such as changes in taxation or regulation, and political uncertainty.

In light of these risks, uncertainties and assumptions, actual results could be materially different from projected future results expressed or implied by these forward-looking statements which speak only as to thedate of this presentation. Except as required by applicable regulations or by law, the Rio Tinto Group does not undertake any obligation to publicly update or revise any forward-looking statements, whether as aresult of new information or future events. The Group cannot guarantee that its forward-looking statements will not differ materially from actual results. In this presentation all figures are US dollars unless statedotherwise.

DisclaimerNeither this presentation, nor the question and answer session, nor any part thereof, may be recorded, transcribed, distributed, published or reproduced in any form, except as permitted by Rio Tinto. By accessing/attending this presentation, you agree with the foregoing and, upon request, you will promptly return any records or transcripts at the presentation without retaining any copies.

This presentation contains a number of non-IFRS financial measures. Rio Tinto management considers these to be key financial performance indicators of the business and they are defined and/or reconciled in RioTinto’s annual results press release and/or Annual report.

Reference to consensus figures are not based on Rio Tinto’s own opinions, estimates or forecasts and are compiled and published without comment from, or endorsement or verification by, Rio Tinto. Theconsensus figures do not necessarily reflect guidance provided from time to time by Rio Tinto where given in relation to equivalent metrics, which to the extent available can be found on the Rio Tinto website.

By referencing consensus figures, Rio Tinto does not imply that it endorses, confirms or expresses a view on the consensus figures. The consensus figures are provided for informational purposes only and are notintended to, nor do they, constitute investment advice or any solicitation to buy, hold or sell securities or other financial instruments. No warranty or representation, either express or implied, is made by Rio Tinto orits affiliates, or their respective directors, officers and employees, in relation to the accuracy, completeness or achievability of the consensus figures and, to the fullest extent permitted by law, no responsibility orliability is accepted by any of those persons in respect of those matters. Rio Tinto assumes no obligation to update, revise or supplement the consensus figures to reflect circumstances existing after the date hereof.

©2020, Rio Tinto, All Rights Reserved3

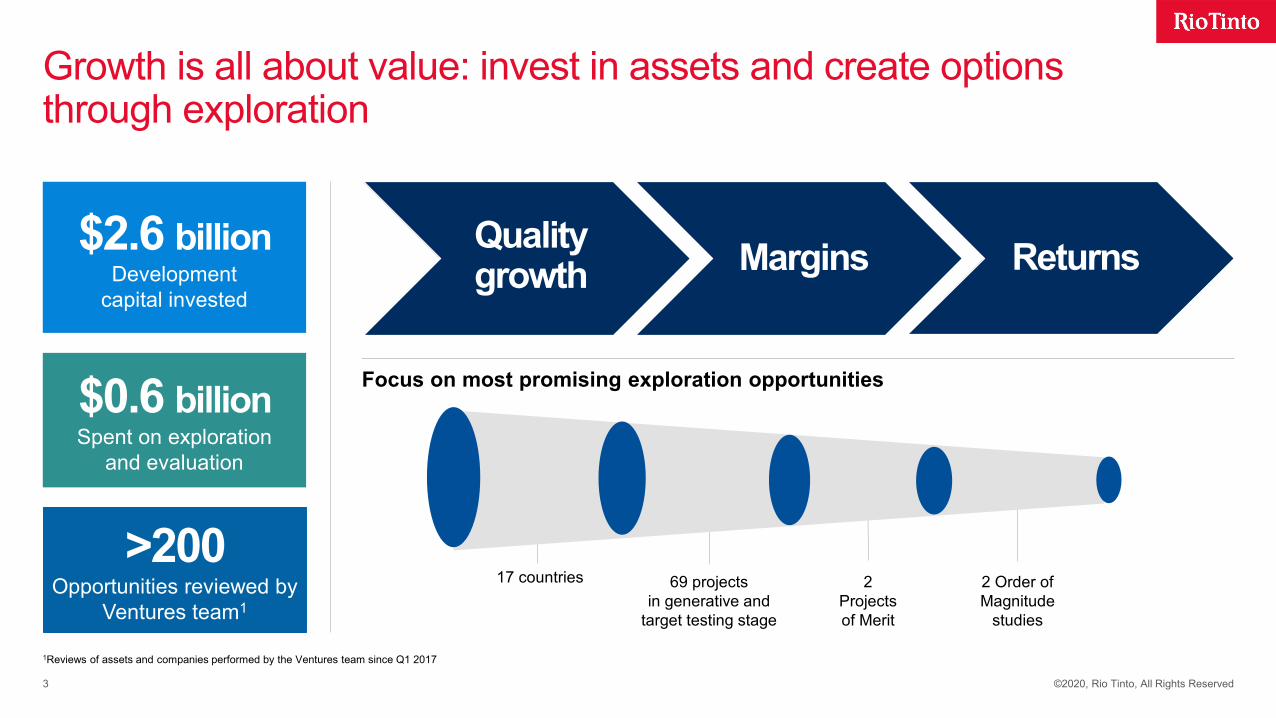

Growth is all about value: invest in assets and create options through exploration

17 countries 69 projectsin generative and

target testing stage

2 Projects of Merit

2 Order of Magnitude

studies

Focus on most promising exploration opportunities

$2.6 billionDevelopment

capital invested

$0.6 billionSpent on exploration

and evaluation

Quality growth Margins Returns

>200Opportunities reviewed by

Ventures team1

1Reviews of assets and companies performed by the Ventures team since Q1 2017

4

A truly global footprint – well funded and very active

©2020, Rio Tinto, All Rights Reserved

A truly global footprint – well funded and very active

* Active countries as at February 2020

Exploring for 7 different commodities across 17 countries* Targets tested Metres drilled (km)

Tenements / agreements

Active hectares (millions)

Copper

Bauxite

Minerals

Iron Ore

Greenfield

Brownfield

Uranium

Diamonds

Ni/PGE

54 6787

2017 2018 2019

89 97

230

2017 2018 2019

174261

157

2017 2018 2019

7.3 8.2 9.8

2017 2018 2019

5

7 decades of industry leading discovery performance

©2020, Rio Tinto, All Rights Reserved

1947

1950

1955

1956

1960

1962

1964

1968

1970

1975

1977

1980

1983

1990

1994

1999

2002

2004

2007

2008

2009

2011

2014

2015

2019

1986

1996

2006

2018

1947CanadaLac AllardIlmeniteKennecott

1955Australia

WeipaBauxite

1962AustraliaTom PriceIron OreCZP

1979AustraliaArgyleDiamondsCRAE

2002USA

ResolutionCopper

RTX

2004GuineaSimandou Iron OreRTX

2005Peru

La Granja Copper

RTX

2005Australia

CaliwinginaIron Ore

RTX

1968NamibiaRössing UraniumRTZ

1970Australia

Tarong (QLD) Coal

CRAE

1964PNG

PangunaCopperCRAE

1968PNGOK TediCopperKennecott

1960USA

SierritaCopper

Kennecott

2000Argen.PRCPotashRTX

Under Cover or +100m depth of mineralization

Rio Tinto current or formerly owned / operated or significant business potential

Divested

2012CanadaSaskatchewanPotashRTX

2008USA

TamarackNickel

RTX

2009SerbiaJadarLithiumRTX

2014AustraliaYandi Braid Iron OreRTX

2015AustraliaMTW / HV*CoalRTX

2008IndiaBunderDiamondsRTX

2018Australia

WinuCopper

RTX

1991Brazil

CorumbaIron ore

RTZ

1991PNGWafiGoldRTZ

1994Brazil

FortalezaNickel

RTZ

1994Aus.Hm. WellNickelCRAE

1956South AfricaPalaboraCopperRTZ

1972BrazilParagominasBauxiteRTZ

1983PNGLihirGoldKennecott

1986Australia

KintyreUranium

CRAE

1977Indonesia

KelianGold

CRAE

1996SpainL. CrucesCopperRTX

2007South AfricaChapudiCoalRTX

1996Lao PDR

SeponCopperCRAE

2004USAEagle Nickel

2004PeruConstanciaCopperRTX

1999Zimbabwe

MurowaDiamonds

RTX

1984Indonesia

Kaltim PrimaCoal

CRAE

2005TurkeyCopper

GoldRTX

2003Iran

S. GunayGoldRTX

2007TurkeyKazanTronaRTX

2008IndonesiaSulawesiNickelRTX

1953Canada

Elliot LakeUranium

RTZ

1982Brazil

Moro de OuroGoldRTZ

1996Canada

Diavik Diamonds

KEX

2008MozambiqueMutambaIlmeniteRTX

1955Australia

Mary KathleenUranium

RTMA

1956GuineaSangarediBauxiteAlcan

2011Brazil

AmargosaBauxite

RTX

1975Australia

Koodaideri BeddedIron Ore

CRAE

2006AustraliaTexas EastIron OreRTX

1972South AfricaRichards Bay IlmeniteRTZ

2009ChileEscondida EsteCopperRTX

2007ChilePampa Es.CopperRTX

2007Australia

CaliwinginaNth.

Iron OreRTX

2007Peru

MiradorCopper

RTX

1999PeruTia MariaCopperRTX

2006Peru

CoraniSilverRTX

1995PeruP.D.

PongoFe

1975USAFlambeauCopperKennecott

1990MadagascarQMMInd. MineralsRTZ

1993Australia

CenturyZinc

CRAE

1998Mexico

PenasquitoSilverRTX

2000PeruMina JustaCopperRTX

6

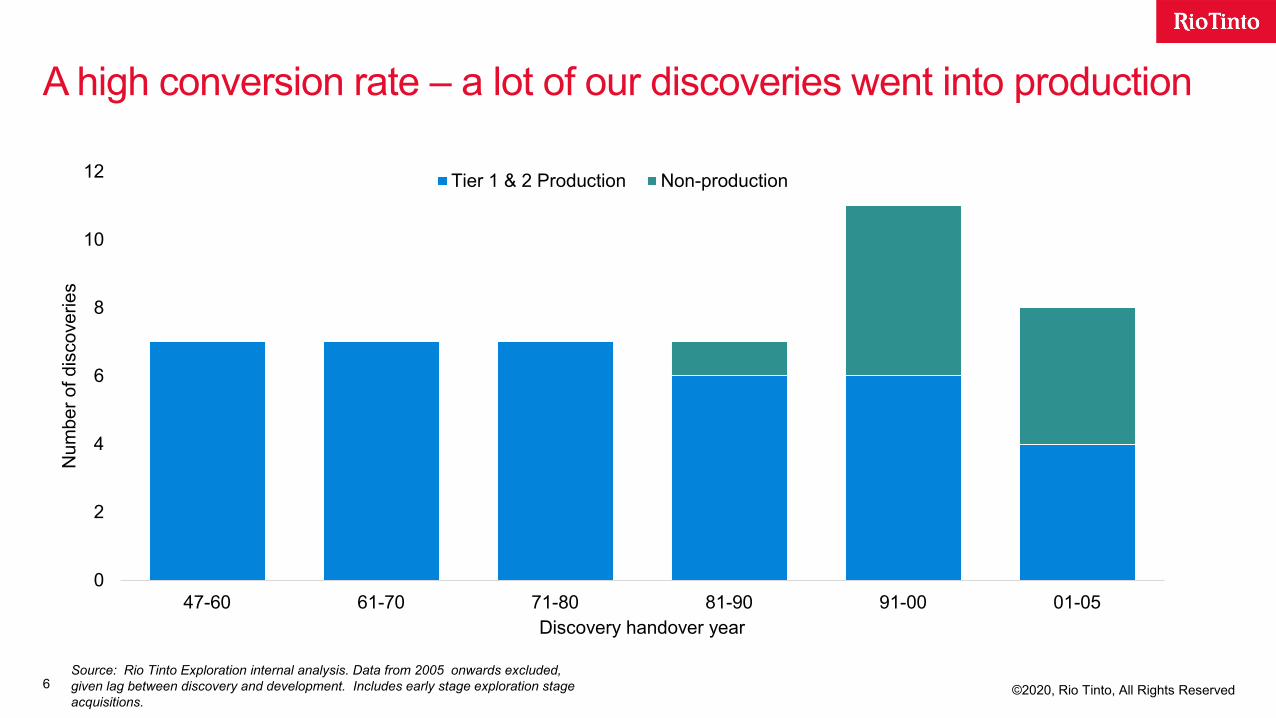

A high conversion rate – a lot of our discoveries went into production

©2020, Rio Tinto, All Rights ReservedSource: Rio Tinto Exploration internal analysis. Data from 2005 onwards excluded, given lag between discovery and development. Includes early stage exploration stage acquisitions.

0

2

4

6

8

10

12

47-60 61-70 71-80 81-90 91-00 01-05

Num

ber o

f dis

cove

ries

Discovery handover year

Tier 1 & 2 Production Non-production

7

The lost decade – the industry got busy being busy, but found less

©2020, Rio Tinto, All Rights Reserved

Industry success historically tied to spend

From ’94-’08 there was a fairly uniform trend for spend and discovery success

But then the industry got busy being busy – spending big and finding less

Note: Excludes bulk minerals (coal, iron ore, bauxite, phosphate and potash). Sources: MinEx Consulting July 2019 (discovery data) and SNL Dec 2018 (expenditure data)

0

5

10

15

20

25

30

0

10

20

30

40

50

60

70

80

'90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18Ex

plor

atio

n bu

dget

(201

8 U

S$b

real

)

Num

ber o

f dis

cove

ries

Tier 3 Tier 2 Tier 1 Exploration Spend

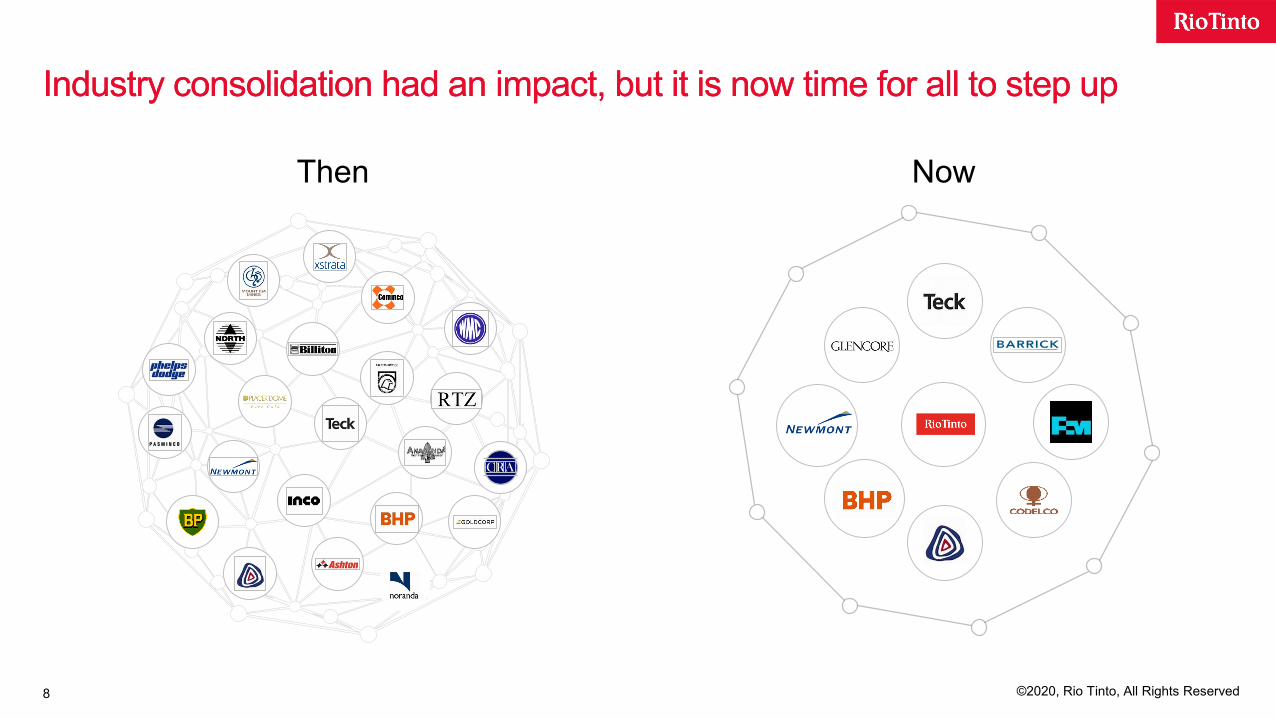

Industry consolidation had an impact, but it is now time for all to step up

CRA

©2020, Rio Tinto, All Rights Reserved8

Industry consolidation had an impact, but it is now time for all to step up

Then Now

9

Analytics and technology enabled exploration strategy

©2020, Rio Tinto, All Rights Reserved

+

Rapid application of new technologies

SearchAnalytics

ResearchPartnership

Drones Data in the fieldHyperspectral Imaging

Sophisticated proprietary tools & techniques

“Greenrocks” Geochronology& Fertility

Automated Mineralogy

New modelsPredictive Analytics

10

Rio Tinto has an excellent track record of effectively exploring beneath cover

©2020, Rio Tinto, All Rights Reserved

Industry discoveries are increasingly at depth – typically greater capital at risk for investment

Rio Tinto has an excellent track record of effectively exploring beneath cover

Source: MinEx Consulting March 2017

0

500

1,000

1,500

2,000

2,500

3,000

3,500

19201900 19601940 1980 2000 2020

Base Metals

GoldGold - South Africa

Copper

• Escondida Este

• Las Cruces• Mirador• Resolution

Iron ore

• Calawingina• Calawingina Nth• Yandi Braid

Other

• Jadar (Lithium)

• Kazan (Trona)• PRC (Potash)• Tamarack

(Nickel)

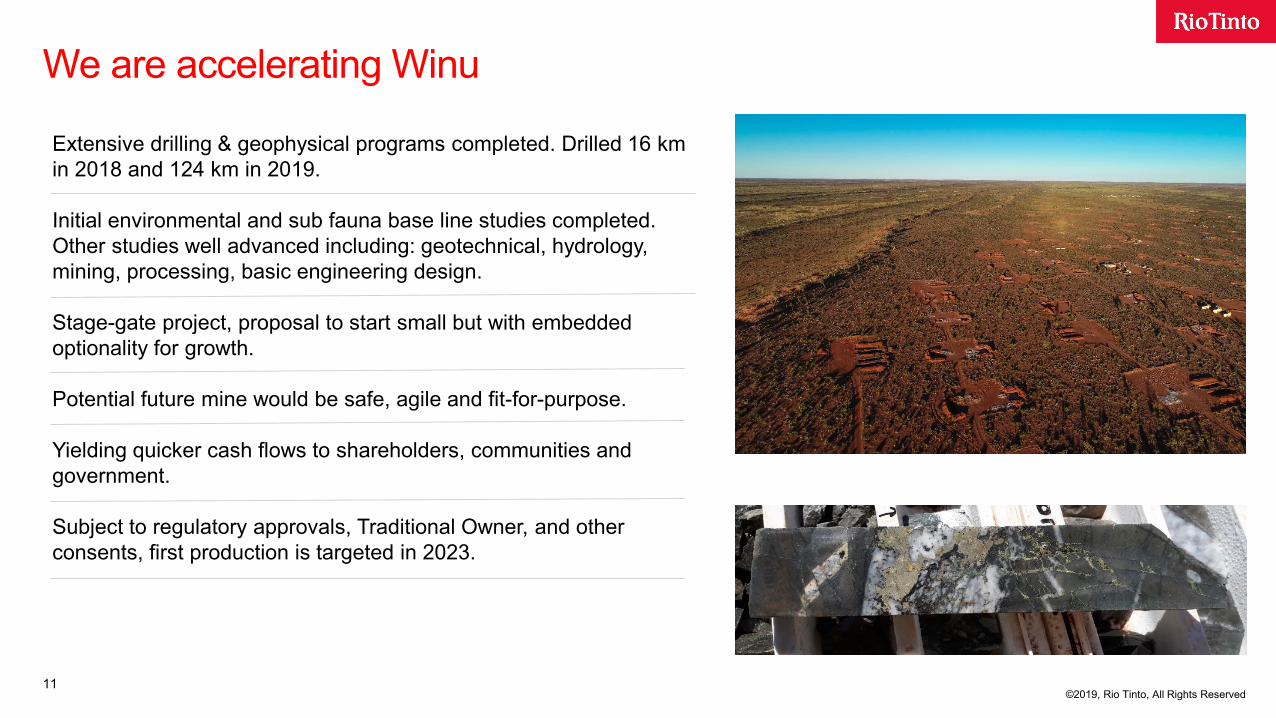

We are accelerating Winu

©2019, Rio Tinto, All Rights Reserved©2019, Rio Tinto, All Rights Reserved

Extensive drilling & geophysical programs completed. Drilled 16 km in 2018 and 124 km in 2019.

Initial environmental and sub fauna base line studies completed. Other studies well advanced including: geotechnical, hydrology, mining, processing, basic engineering design.

Stage-gate project, proposal to start small but with embedded optionality for growth.

Potential future mine would be safe, agile and fit-for-purpose.

Yielding quicker cash flows to shareholders, communities and government.

Subject to regulatory approvals, Traditional Owner, and other consents, first production is targeted in 2023.

11

©2020, Rio Tinto, All Rights Reserved12

Technology on show at FalCon

Not a typical site

Novel application of existing non-mining technology

Working with our partner to quickly identify the potential

FalCon diamond project - cutter crew changeover after reaching 228.4 metres depth

©2020, Rio Tinto, All Rights Reserved13

Best in class analytics & technology

Industry needs to crack the code on cover – Rio Tinto will play it’s part

Ready to partner globally