newmont mining PDAC

29

Slide 1 Providing an Alternative Providing an Alternative Strategic Capital Source Strategic Capital Source for Juniors for Juniors Paul Brink Director Newmont Capital PDAC, March 7, 2007 PDAC, March 7, 2007

-

Upload

finance37 -

Category

Economy & Finance

-

view

157 -

download

3

Transcript of newmont mining PDAC

Slide 1

Providing an Alternative Providing an Alternative Strategic Capital Source Strategic Capital Source

for Juniorsfor JuniorsPaul BrinkDirector

Newmont Capital

PDAC, March 7, 2007PDAC, March 7, 2007

Slide 2

Cautionary Statement

Cautionary Statement This presentation contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, that are intended to be covered by the safe harbor created by such sections. Such forward-looking statements include, without limitation, (i) statements regarding value or future distributions of investments, (ii) estimates regarding timing of future development, construction and production activities; (iii) statements regarding future exploration results; and (iv) estimates of reserves and statements regarding replacement of reserves. Where the Company expresses or implies an expectation or belief as to future events or results, such expectation or belief is expressed in good faith and believed to have a reasonable basis. However, forward-looking statements are subject to risks, uncertainties and other factors, which could cause actual results to differ materially from future results expressed, projected or implied by such forward-looking statements. For a discussion of risks and other factors, see the Company’s 2006 Annual Report on Form 10-K, which is on file with the Securities and Exchange Commission, as well as the Company’s other SEC filings. The Company does not undertake any obligation to release publicly revisions to any “forward-looking statement,” to reflect events or circumstances after the date of this news release, or to reflect the occurrence of unanticipated events, except as may be required under applicable securities laws.

Slide 3

Agenda

Newmont CapitalNewmont Capital

Investment RationaleInvestment Rationale

Technical SupportTechnical Support

Select TransactionsSelect Transactions

Transaction DriversTransaction Drivers

Slide 4

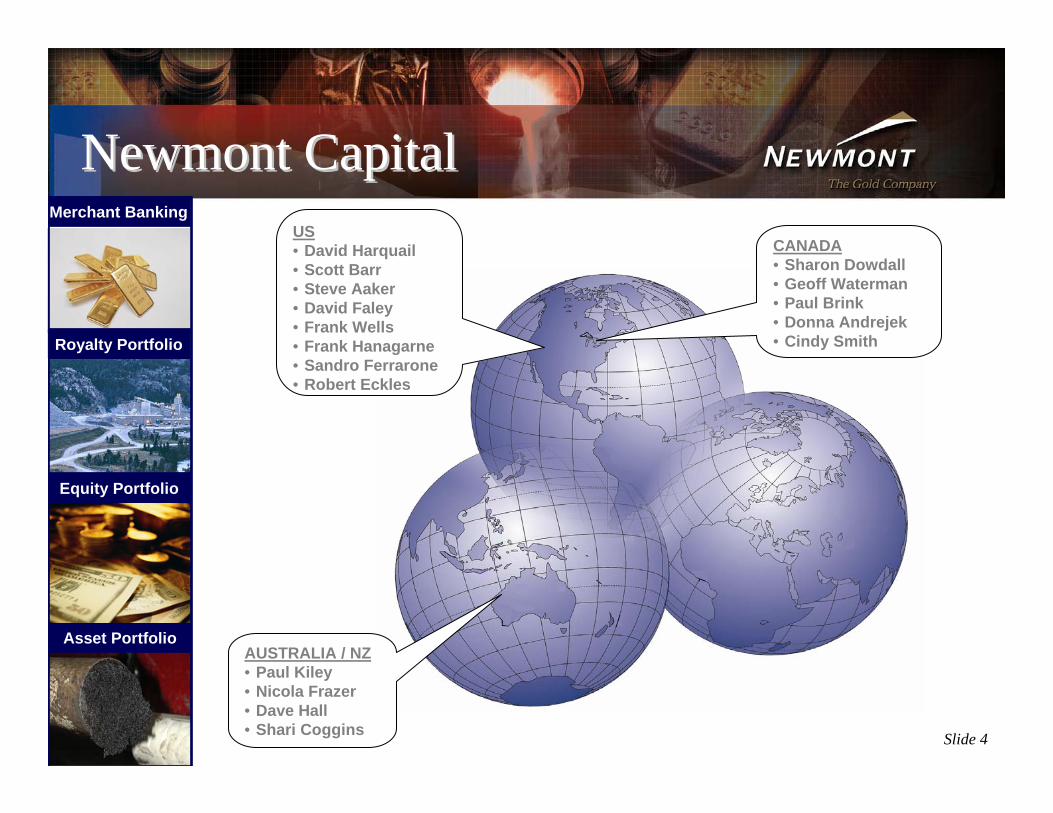

Newmont CapitalNewmont CapitalUS• David Harquail• Scott Barr• Steve Aaker• David Faley• Frank Wells• Frank Hanagarne• Sandro Ferrarone• Robert Eckles

CANADA• Sharon Dowdall• Geoff Waterman• Paul Brink• Donna Andrejek• Cindy Smith

AUSTRALIA / NZ• Paul Kiley• Nicola Frazer• Dave Hall• Shari Coggins

Merchant Banking

Asset Portfolio

Royalty Portfolio

Equity Portfolio

Slide 5

Oil and Gas57%

Gold28%

PGMs11%

Other4%

Royalty PortfolioRoyalty Portfolio

Royalty revenues by SourceYear to Date – 31 December 2006

Royalty stream of $90–$100million/yr

GoldGold PGMPGM

US US USUS

IndonesiaIndonesia

AustraliaAustralia

Canada Canada

Oil and GasOil and Gas Base MetalBase Metal

CanadaCanada USUS

OtherOther

Dominican RepublicDominican Republic

Active Royalties and Other RevenueActive Royalties and Other Revenue

Slide 6

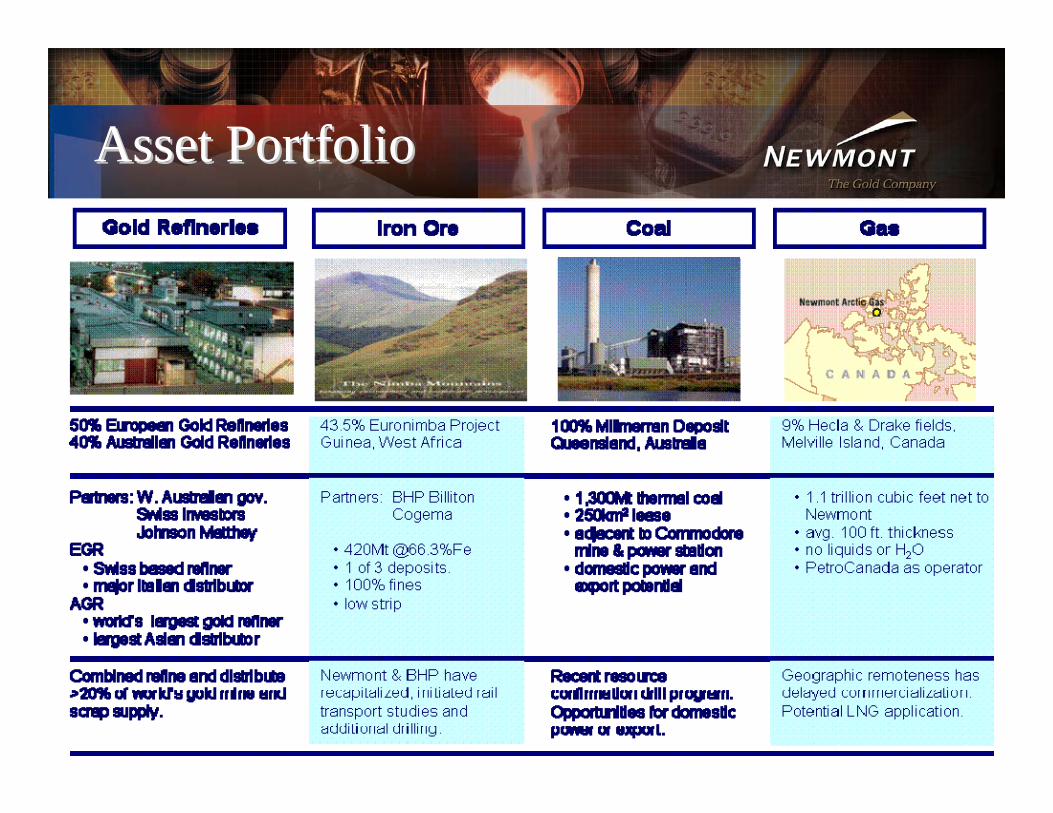

Asset PortfolioAsset Portfolio

Slide 7

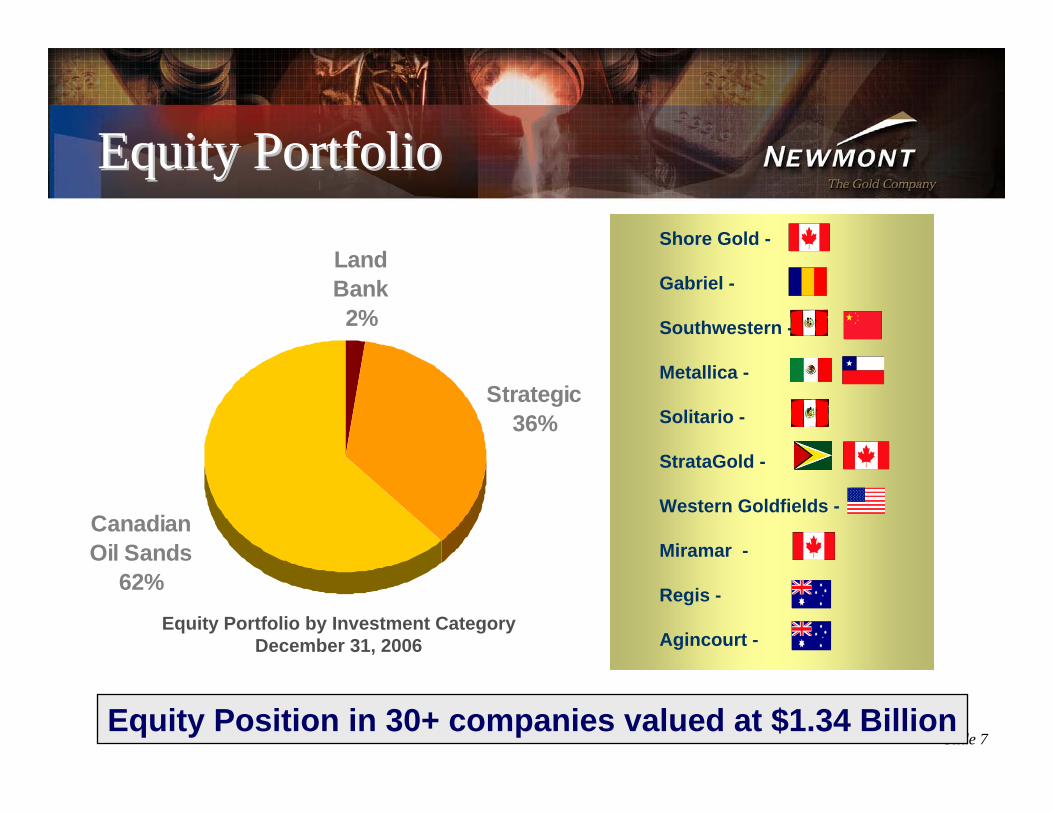

Land Bank2%

Strategic36%

Canadian Oil Sands

62%

Equity PortfolioEquity Portfolio

Equity Portfolio by Investment CategoryDecember 31, 2006

Shore Gold -

Gabriel -

Southwestern -

Metallica -

Solitario -

StrataGold -

Western Goldfields -

Miramar -

Regis -

Agincourt -

Equity Position in 30+ companies valued at $1.34 Billion

Slide 8

Agenda

Newmont CapitalNewmont Capital

Investment RationaleInvestment Rationale

Technical SupportTechnical Support

Select TransactionsSelect Transactions

Transaction DriversTransaction Drivers

Slide 9

Investment Rationale

Invest in properties Invest in properties that have the that have the potential to be core potential to be core assets in Newmontassets in Newmont’’s s portfolioportfolio

Nevada Peru

Indonesia

GhanaAustralia/ New Zealand

Slide 10

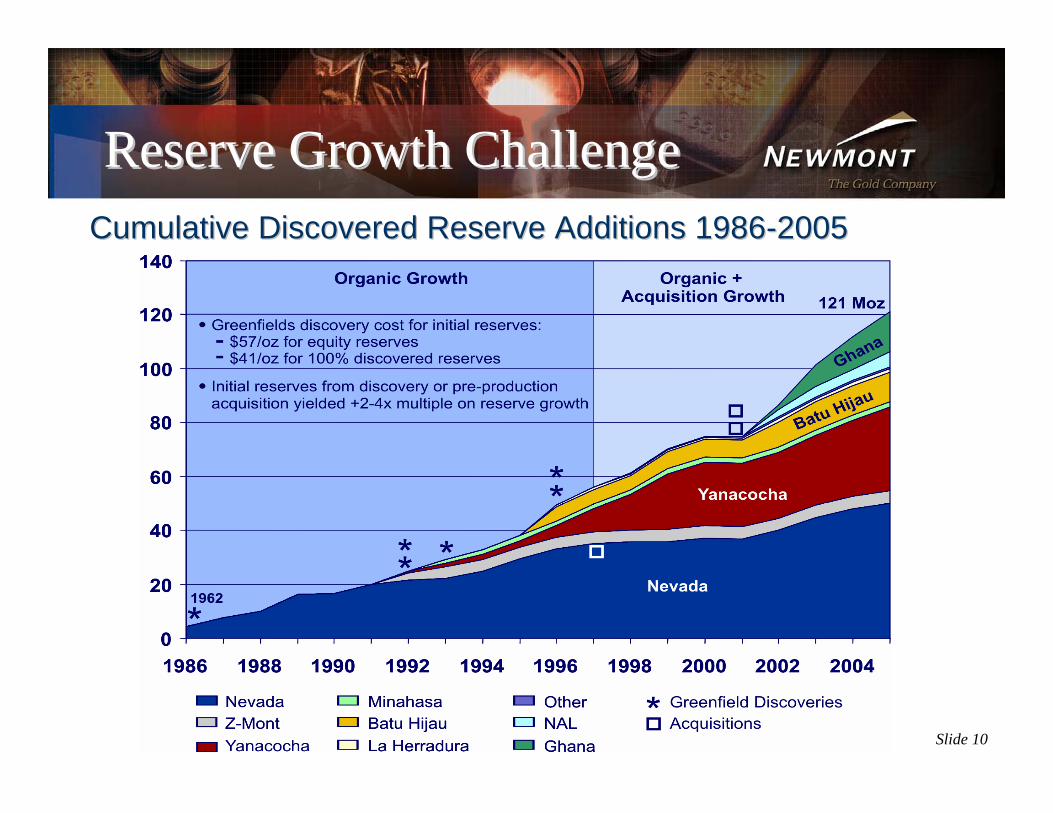

Cumulative Discovered Reserve Additions 1986Cumulative Discovered Reserve Additions 1986--20052005

Reserve Growth ChallengeReserve Growth Challenge

Slide 11

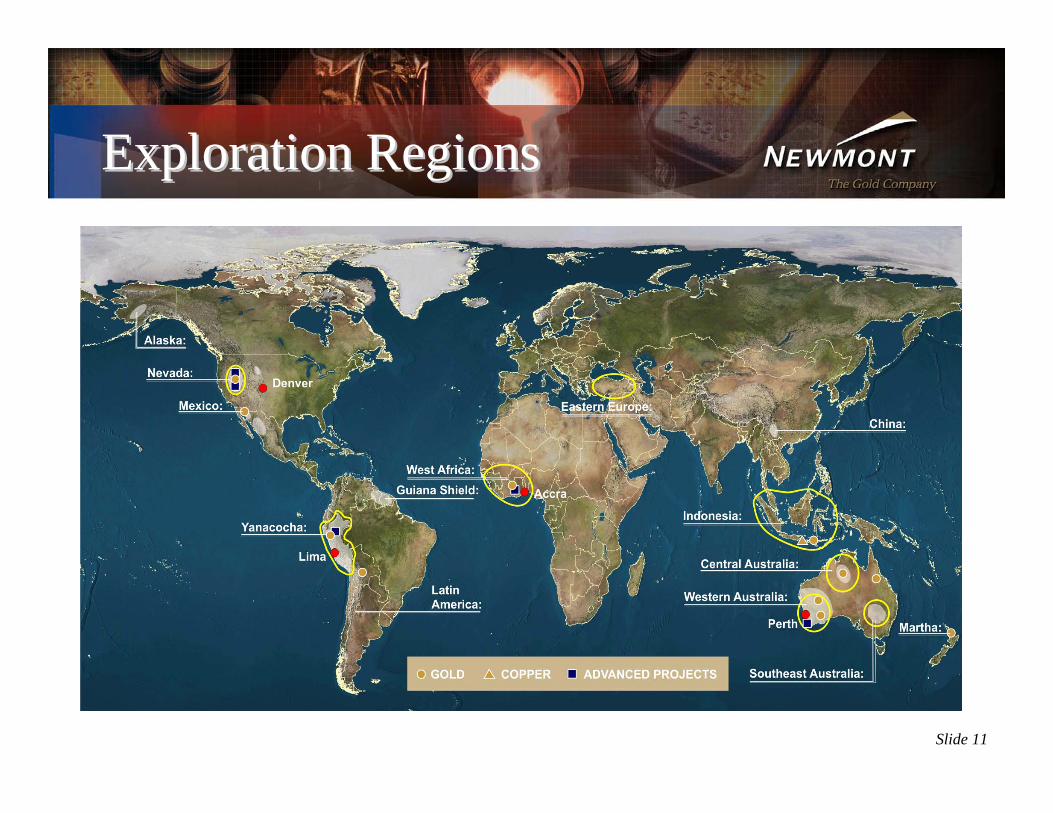

Exploration RegionsExploration Regions

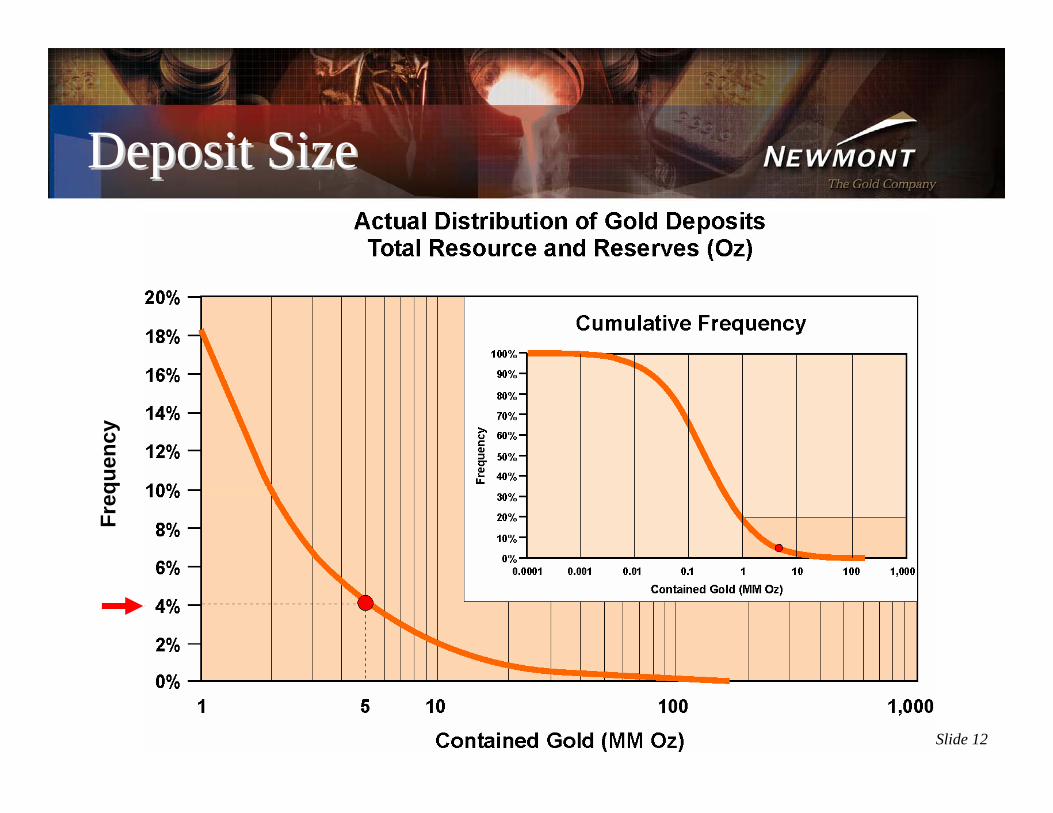

Slide 12

Freq

uenc

y

Deposit SizeDeposit Size

Slide 13

Priorities:

• Orogenic deposits, such as mesothermal shear hosted and vein deposits

• Sedimentary rock hosted gold deposits in Nevada and elsewhere

• Quartz-pebble conglomerate hosted deposits outside of South Africa

• Alkalic related deposits

Where we already hold prospective lands we include Arc related deposits:

• Porphyry copper-gold

• Epithermal vein styles

Exploration EnvironmentsExploration Environments

Slide 14

Agenda

Newmont CapitalNewmont Capital

Investment RationaleInvestment Rationale

Technical SupportTechnical Support

Select TransactionsSelect Transactions

Transaction DriversTransaction Drivers

Slide 15

Exploration Support

WorldWorld--class Exploration Teamclass Exploration Team•• 325 Geoscientists325 Geoscientists

•• Global Exploration Solutions Group:Global Exploration Solutions Group:-- Geophysicists, Geochemists, Remote SensingGeophysicists, Geochemists, Remote Sensing

Exploration Technologies/ToolsExploration Technologies/Tools•• Proprietary Airborne Geophysics (NewTEM2)Proprietary Airborne Geophysics (NewTEM2)

•• Proprietary BLEG Analysis at InProprietary BLEG Analysis at In--House LabHouse Lab

Slide 16

Exploration TeamSteve Enders, Steve Enders, Global Head of Global Head of

ExplorationExploration

David Groves, David Groves, Africa/EuropeAfrica/Europe

Lewis Teal, Lewis Teal, South AmericaSouth America

Ken Paul, North Ken Paul, North AmericaAmerica

Brian Levet Brian Levet Asia PacificAsia Pacific

Regional Exploration Regional Exploration ManagersManagers

Exploration Business Exploration Business DevelopmentDevelopment

Jeff HuspeniJeff Huspeni

Patrick Patrick HighsmithHighsmith

Grigore Simon,Grigore Simon,

GreenfieldGreenfield

Leroy Schutz,Leroy Schutz,

BrownfieldBrownfield

Slide 17

Technologies

Innovative Process TechnologiesInnovative Process Technologies

•• BIOPROBIOPRO®® –– BiooxidationBiooxidation

•• NN22TECTEC®® –– FlotationFlotation

•• Pressure OxidationPressure Oxidation

•• ATS ATS –– Ammonium Ammonium ThiosulphateThiosulphate

Slide 18

Technical Services

100 Technical Services Staff Globally:

• Met and Tech (45staff) • Mining and Resource

Development (40 staff)• Evaluations staff (12 staff)

Services Provided:• Development Geology• Metallurgical Testing• Project Evaluations• Mine Engineering & Planning• Process Design

MalozemofMalozemof Technical Center, Technical Center, Denver (80 staff)Denver (80 staff)

Unmatched ability to solve complex problemsUnmatched ability to solve complex problems

Slide 19

Agenda

Newmont CapitalNewmont Capital

Investment RationaleInvestment Rationale

Technical SupportTechnical Support

Select TransactionsSelect Transactions

Transaction DriversTransaction Drivers

Slide 20

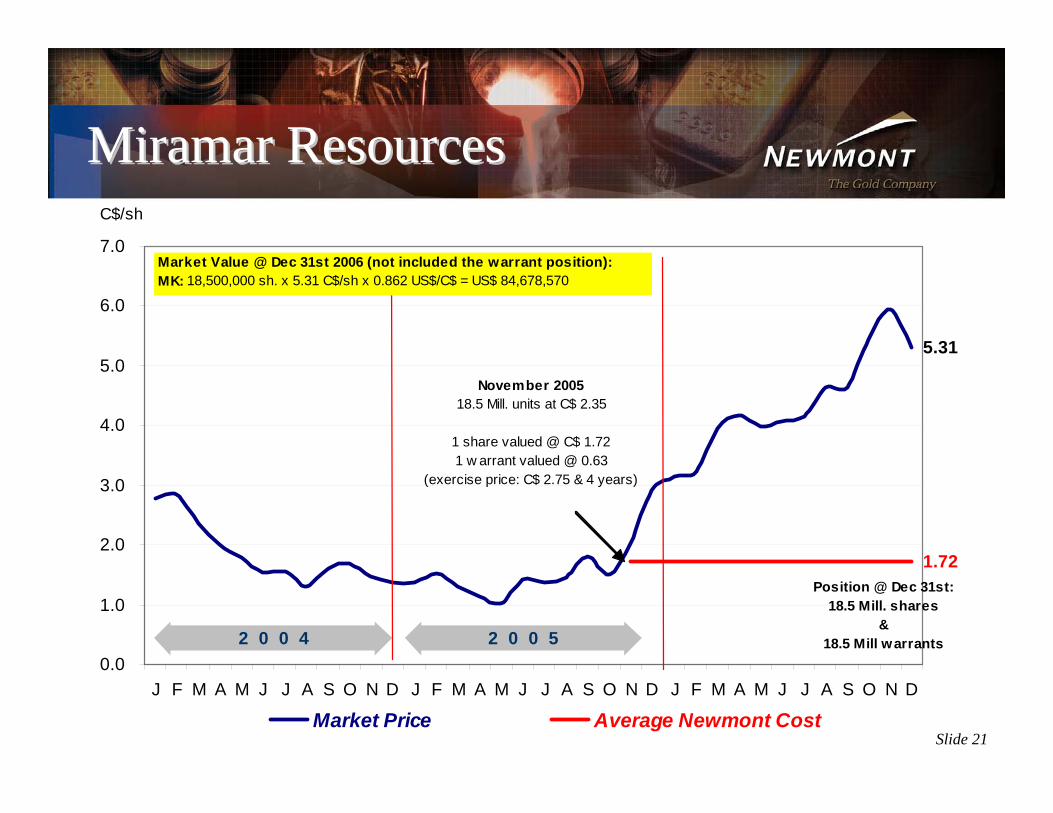

+8m ounce Hope Bay project in NunavutOP/UG operationMajor production by 2013 (500-800k oz) Low costs (<$300/oz), simple metallurgy.

Miramar ResourcesMiramar Resources

Slide 21

Miramar ResourcesMiramar Resources

5.31

1.72

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D

C$/sh

Market Price Average Newmont Cost

2 0 0 4 2 0 0 5

November 200518.5 Mill. units at C$ 2.35

1 share valued @ C$ 1.721 w arrant valued @ 0.63

(exercise price: C$ 2.75 & 4 years)

Position @ Dec 31st:18.5 Mill. shares

&18.5 Mill warrants

Market Value @ Dec 31st 2006 (not included the warrant position):MK: 18,500,000 sh. x 5.31 C$/sh x 0.862 US$/C$ = US$ 84,678,570

Slide 22

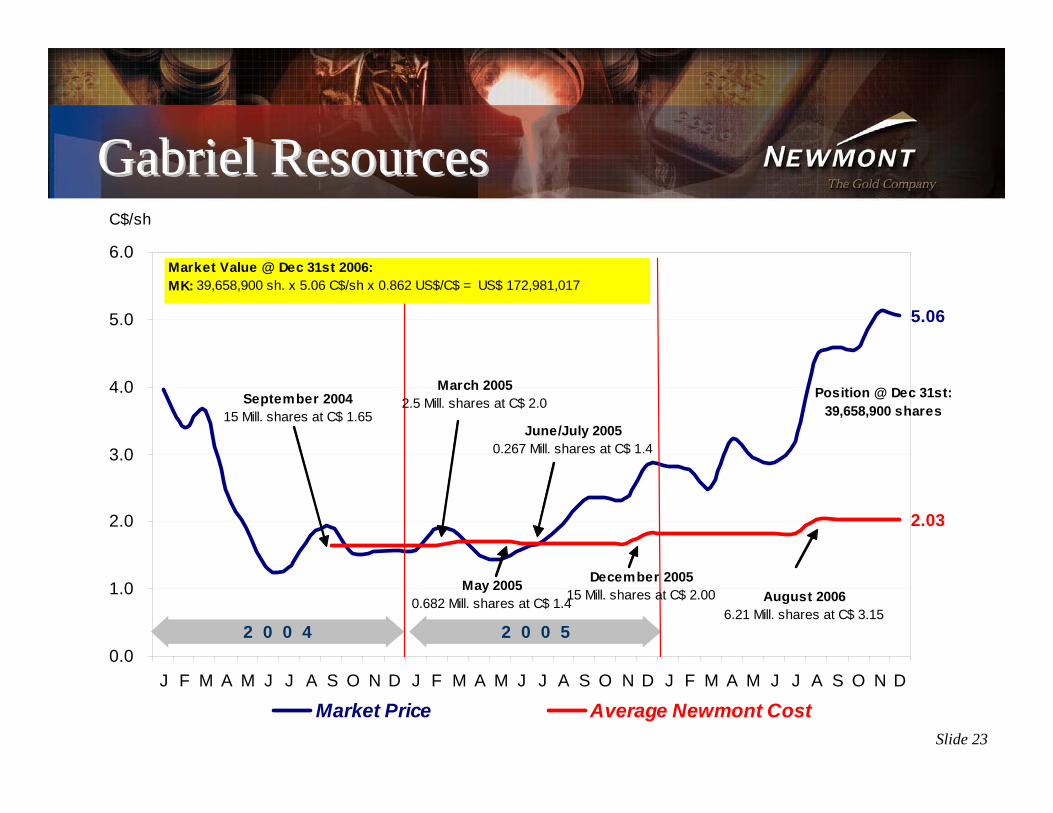

10m+ ounce RosiaMontana project in RomaniaLarge OP operation$120m + invested in feas. & reloc.Permitting and relocation underway

Gabriel ResourcesGabriel Resources

Slide 23

Gabriel ResourcesGabriel Resources

5.06

2.03

0.0

1.0

2.0

3.0

4.0

5.0

6.0

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D

C$/sh

Market Price Average Newmont Cost

2 0 0 4 2 0 0 5

September 200415 Mill. shares at C$ 1.65

March 20052.5 Mill. shares at C$ 2.0

May 20050.682 Mill. shares at C$ 1.4

December 200515 Mill. shares at C$ 2.00

June/July 20050.267 Mill. shares at C$ 1.4

Position @ Dec 31st:39,658,900 shares

August 20066.21 Mill. shares at C$ 3.15

Market Value @ Dec 31st 2006:MK: 39,658,900 sh. x 5.06 C$/sh x 0.862 US$/C$ = US$ 172,981,017

Slide 24

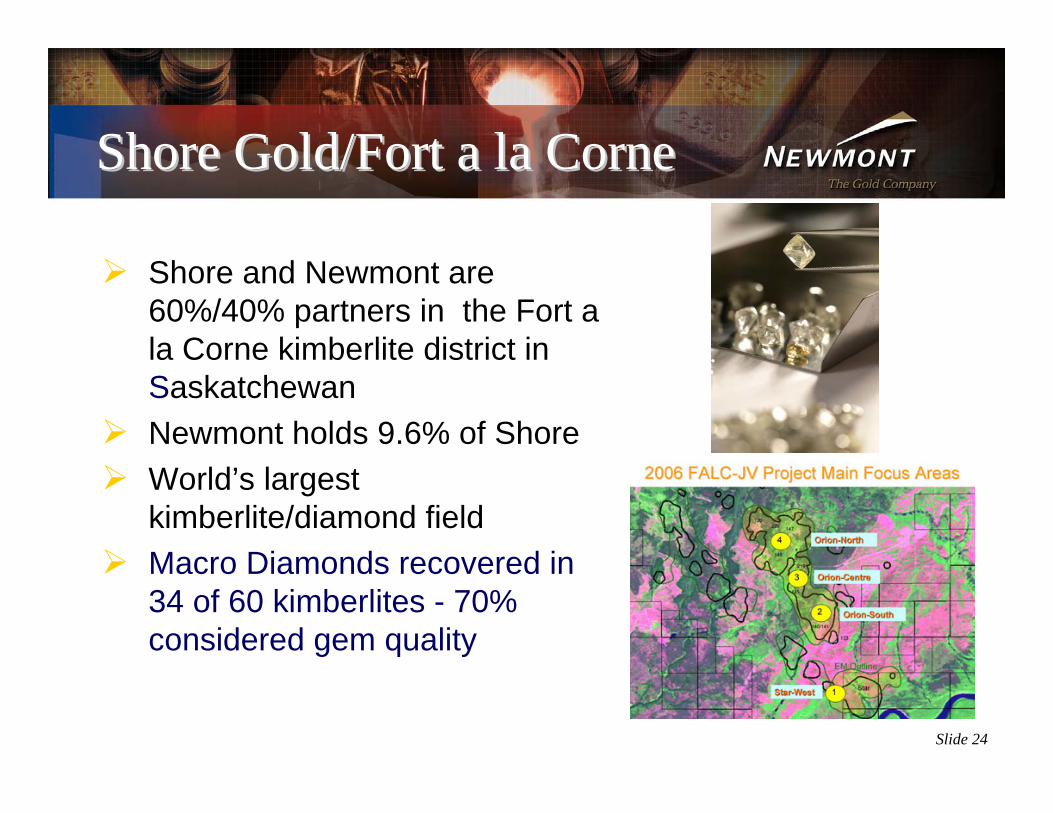

Shore Gold/Fort a la CorneShore Gold/Fort a la Corne

Shore and Newmont are 60%/40% partners in the Fort a la Corne kimberlite district in Saskatchewan Newmont holds 9.6% of ShoreWorld’s largest kimberlite/diamond fieldMacro Diamonds recovered in 34 of 60 kimberlites - 70% considered gem quality

Slide 25

StratagoldStratagold

StrataGold owns the Tassawiniprospect in Guyana and Dublin Gulch in BC.

Oct. ‘04 Newmont invested C$4m private placement to establish strategic alliance

Alliance subsequently expanded to 1m acre Barama JV with Newmont potential to 70%

April ’06 – Newmont invested additional $2.6m and representative appointed to BOD

Slide 26

Agenda

Newmont CapitalNewmont Capital

Investment RationaleInvestment Rationale

Technical Support Technical Support

Select TransactionsSelect Transactions

Transaction DriversTransaction Drivers

Slide 27

Property positions/equity investments

Private placements/public offerings

Not limited to at market deals

Due diligence

Public and private company transactions

TSX/ASX/AIM/AMEX

Creative Merchant BankingCreative Merchant Banking

Slide 28

Endorsement of a strategic investor

Technical support of the industry leading exploration/mining and metallurgical team

Potentially avoid brokerage fees

Flexible transaction structures with creative merchant bankers

Benefit of the experience of a senior operating partner

Partner of ChoicePartner of Choice

Slide 29

Thank YouThank You

Paul BrinkDirector

Newmont Capital(416) 480 6495