Payments imps

38

1 Payment Systems & IMPS Chintan Patel B.E(Comp) ; MBA(Finance) 26-Apr-2013

-

Upload

chintan123 -

Category

Documents

-

view

136 -

download

3

Transcript of Payments imps

1

Payment Systems & IMPS

Chintan PatelB.E(Comp) ; MBA(Finance)

26-Apr-2013

2

Agenda

Payment SystemsExisting Payment Systems – ECS, NEFT & RTGSMobile Payments – IMPS

Modes of Transfer & Various Use cases Process Flow Advantages & Disadvantages Comparison with other payments

Future PaymentsEmerging Trends

3

Payment Systems

Definition: Financial system supporting transfer of funds from payers to payee/s.

Role:

Payment systems to provide safe, efficient, affordable, easily accessible and robust payment services

Payment systems help in the smooth flow of money in the economy thus increasing the liquidity in the hands of the customer enhancing his purchasing capacity

Payment systems would also help minimize cases of fraud, use of counterfeit notes and black

money

4

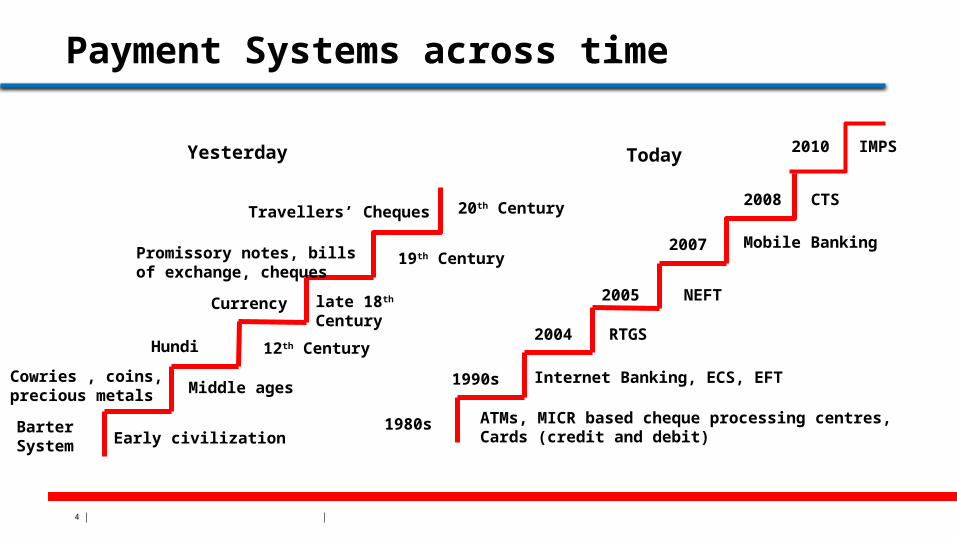

Payment Systems across time

Yesterday Today

Barter System Early civilization

Cowries , coins, precious metals Middle ages

Hundi 12th Century

late 18th CenturyCurrency

19th CenturyPromissory notes, bills of exchange, cheques

Travellers’ Cheques 20th Century

1980s ATMs, MICR based cheque processing centres, Cards (credit and debit)

1990s Internet Banking, ECS, EFT

2004

2005

2007

2008

RTGS

NEFT

Mobile Banking

CTS

2010 IMPS

5

Payment Systems – Stakeholders

RBI

NPCI

CCILBanks

RetailCustomers

CorporateCustomers

SMECustomers

6

Classification

Indian Payments

Retail

Paper Based

Cheque -MICR Demand Draft

Electronic Based

ECS NEFTCheque

Truncation system

Mobile Based

IMPS

Large Value Systems

Paper Based Electronic Based

RTGS

7

Global PaymentsUse of payment instruments by non-banks: total number of transactions, 2010 (Millions, total for the year)

Source: Data is from the Bank for International Settlements’ Statistics

8

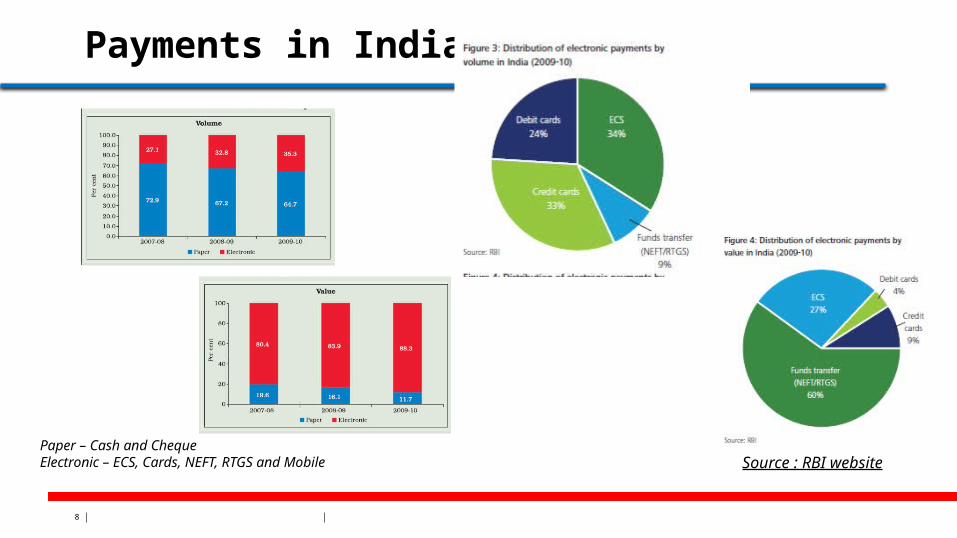

Payments in India

Paper – Cash and ChequeElectronic – ECS, Cards, NEFT, RTGS and Mobile Source : RBI website

9

Electronic Clearing Service (ECS)

It was introduced by RBI Provided an alternative method of effecting bulk transaction Avoided need for issuing and handling paper instrument User has to submit the mandate to the bank. (E.g.: MICR -Cancelled Cheque) No Transaction limit

There are two types of ECS:

ECS – Debit - There is multiple debit from vast section of people and corresponding single credit entry. E.g.: Bill payment

ECS - Credit - Electronic fund transfer from one account to many transactions transfers. E.g.: Salary Payment

10

Real Time Gross Settlement (RTGS)

Introduced by RBI in 2004 RTGS systems are managed by RBI.Transfer anywhere within India. Funds for > Rs 2 lakh to be transferred through RTGS. Lower funds cannot be

transferred . Upper Transaction limit set by individual bank. Payment instruction handled individually. Payment is final and irrevocable and the receiver can utilize the funds immediately RTGS Timings:

Weekdays : 9:15 AM to 4:15 PM Saturday : 9:15 AM to 1:15 PM ; No settlement on Sundays and Holidays

Service Charge applicable to customer Steps for Transaction : Register Payee & Transfer Funds

11

National Electronic Funds Transfer System (NEFT)

It was launched by RBI in 2005 It permits to transfer funds of lower value. Neither lower limit nor upper limit Transfer anywhere within India Operate on a deferred net settlement (DNS) basis which settles transactions in

batches. NEFT Timings:

Weekdays: 12 times every hour from 8:00 AM to 7:00 PM Saturday : 6 times every hour from 8:00 AM to 1:00 PM No transfer on Sundays and Holidays

Service Charge is applicable to the Customer Steps for Transaction : Register Payee & Transfer Funds

12

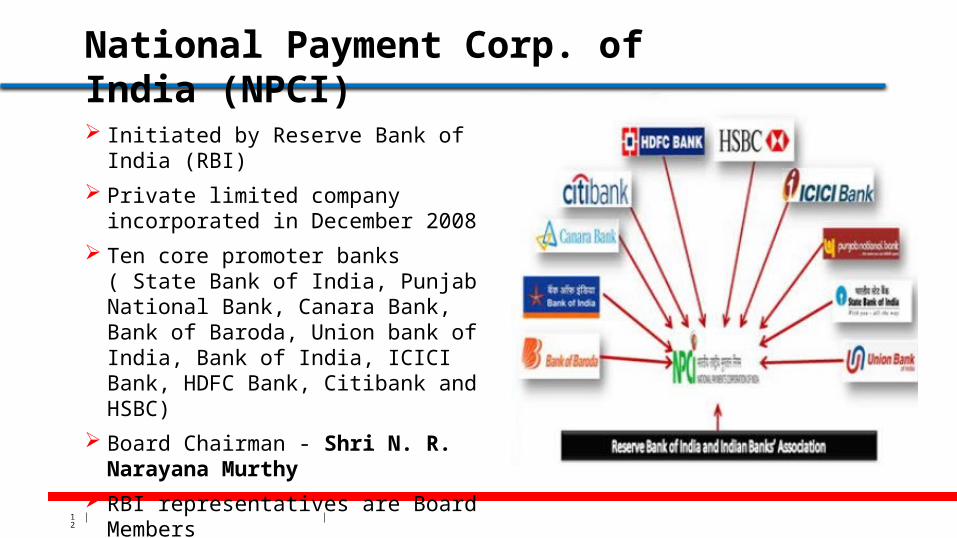

National Payment Corp. of India (NPCI)

Initiated by Reserve Bank of India (RBI)

Private limited company incorporated in December 2008

Ten core promoter banks ( State Bank of India, Punjab National Bank, Canara Bank, Bank of Baroda, Union bank of India, Bank of India, ICICI Bank, HDFC Bank, Citibank and HSBC)

Board Chairman - Shri N. R. Narayana Murthy

RBI representatives are Board Members

13

InterBank Mobile Payment Service (IMPS)

Initiated by NPCI along with 4 Member banks – SBI, Bank of India, Union Bank of India and ICICI Bank

Launched on 22nd November 2010

Service available to Public

To participate in IMPS, Banks should have approval from RBI

Available with 54 Banks

14

Objective of IMPS

Make a Mobile as Channel

Available – 24 X 7 X 365

No more sharing of bank account details

Instant

Payment – Simple, convenient

Time & cost saving

Safe & Secure

Immediate Confirmation

Use existing payments infrastructure (existing ATM networks)

15

Advantages of Mobile Channel

Mobile phone is a universal device 900+ million connections and growing most Indian families have access to one

It is a two way communication device Unlike cards Multiple level of security possible

Multi-mode communications SMS, Internet, USSD and Voice Even the semi-literate and illiterate people find it easy to use

Enables transactions in-person and remotely

16

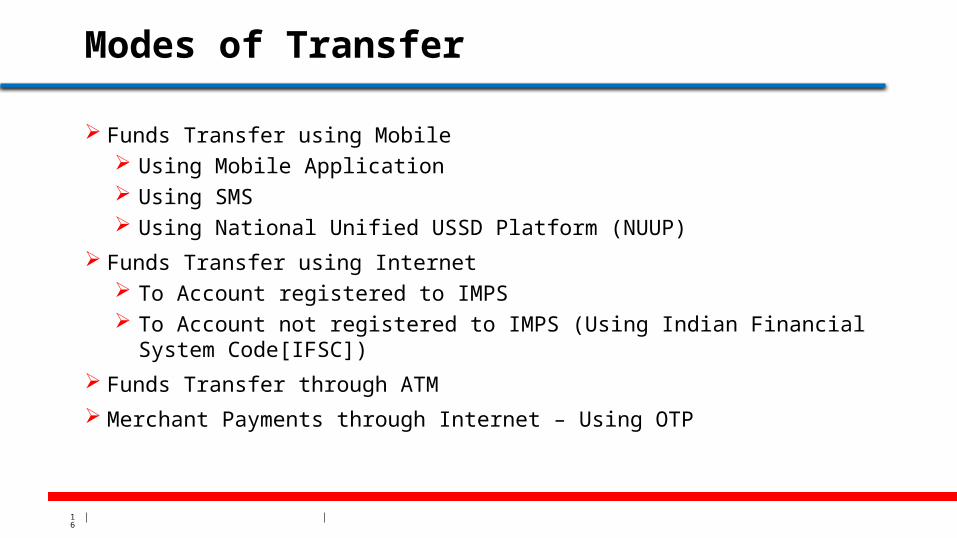

Modes of Transfer

Funds Transfer using Mobile Using Mobile Application Using SMS Using National Unified USSD Platform (NUUP)

Funds Transfer using Internet To Account registered to IMPS To Account not registered to IMPS (Using Indian Financial System Code[IFSC])

Funds Transfer through ATM

Merchant Payments through Internet – Using OTP

17

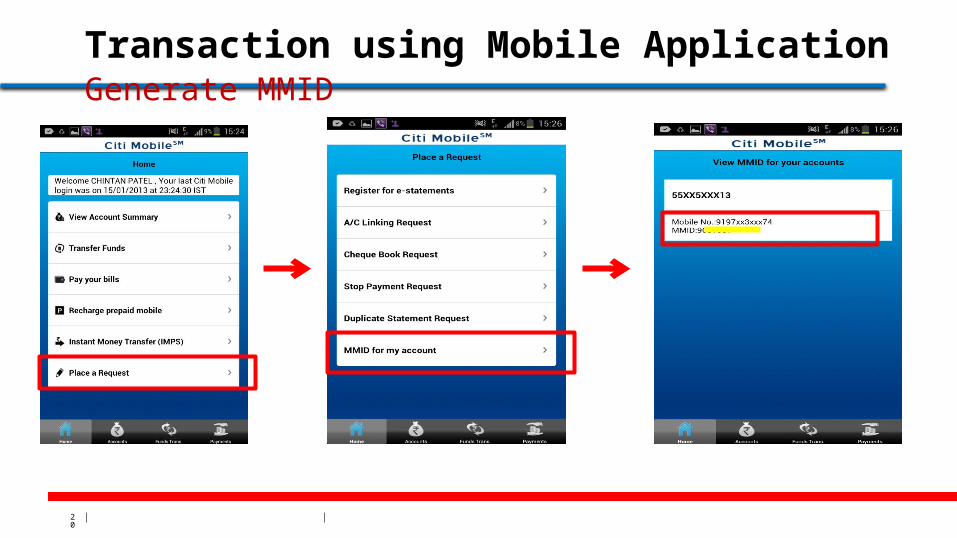

Steps for Transaction

Registration of Remitter – Generate MMIDMMID (Mobile Money Identifier) is 7-digit number, to be issued by

the Bank. Unique number for every associated account

Registration of Beneficiary – Generate MMIDFunds Transfer

Login to Mobile Banking Application or Send SMSEnter Beneficiary MMID, Beneficiary Mobile Number & AmountFunds Transferred ImmediatelyRemitter & Beneficiary receives confirmation

18

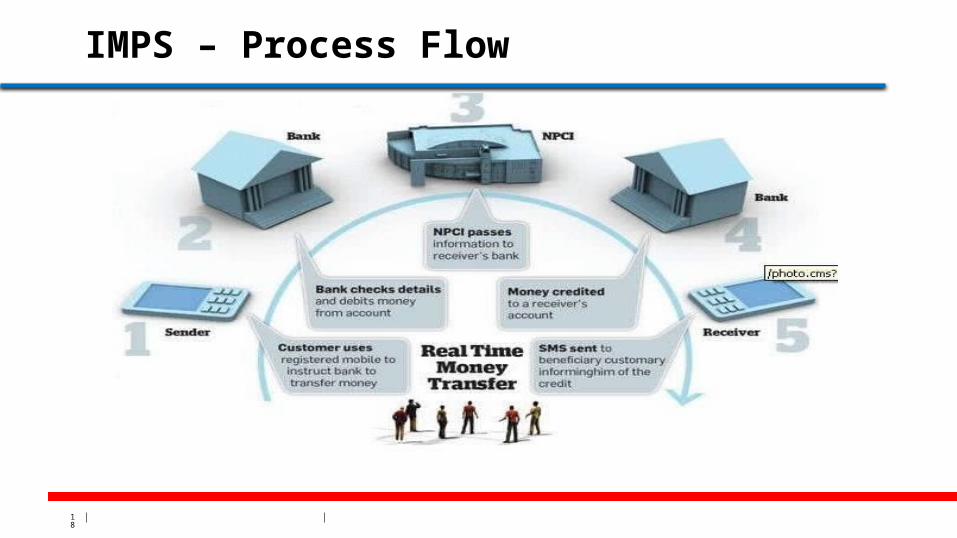

IMPS – Process Flow

19

Demonstrate IMPS

Account Holder A wants to transfer funds

Citi Bank Account ICICI Bank AccountIMPS

20

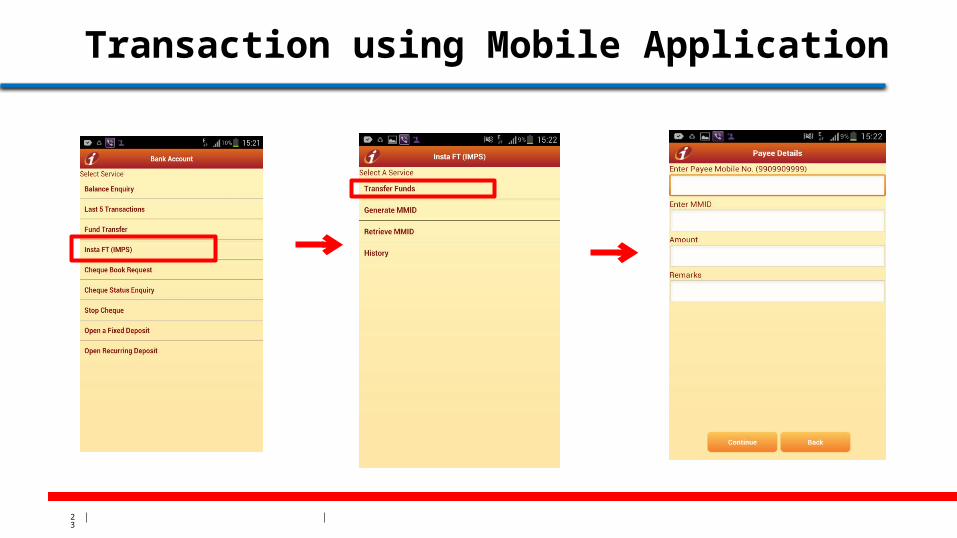

Transaction using Mobile ApplicationGenerate MMID

21

Transaction using Mobile ApplicationGenerate MMID

22

Transaction using Mobile Application

23

Transaction using Mobile Application

24

Transaction using SMS

25

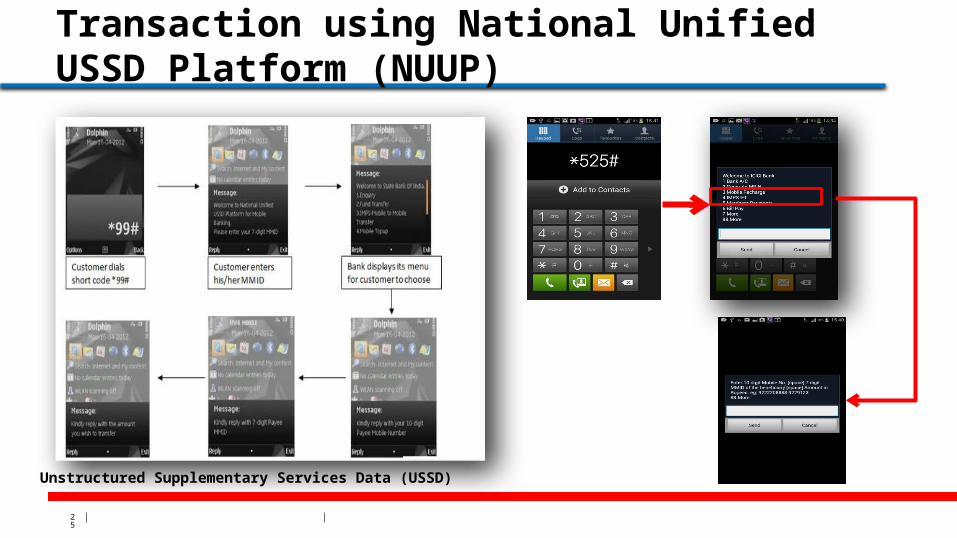

Transaction using National Unified USSD Platform (NUUP)

Unstructured Supplementary Services Data (USSD)

26

Transaction using Internet

27

Merchant Payments

28

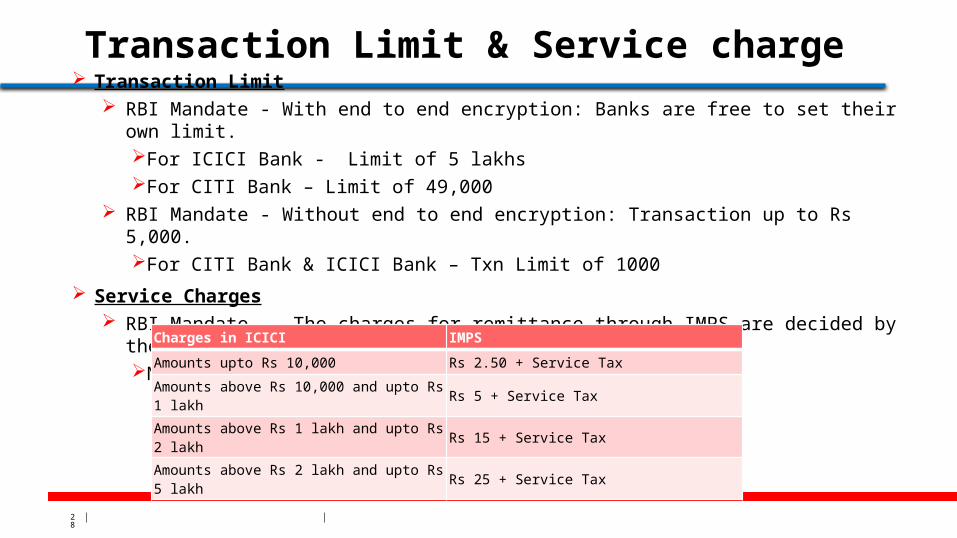

Transaction Limit & Service charge Transaction Limit

RBI Mandate - With end to end encryption: Banks are free to set their own limit.For ICICI Bank - Limit of 5 lakhsFor CITI Bank – Limit of 49,000

RBI Mandate - Without end to end encryption: Transaction up to Rs 5,000.For CITI Bank & ICICI Bank – Txn Limit of 1000

Service Charges RBI Mandate - The charges for remittance through IMPS are decided by the individual banks

No Charges in Citibank

Charges in ICICI IMPS

Amounts upto Rs 10,000 Rs 2.50 + Service Tax

Amounts above Rs 10,000 and upto Rs 1 lakh Rs 5 + Service Tax

Amounts above Rs 1 lakh and upto Rs 2 lakh Rs 15 + Service Tax

Amounts above Rs 2 lakh and upto Rs 5 lakh Rs 25 + Service Tax

29

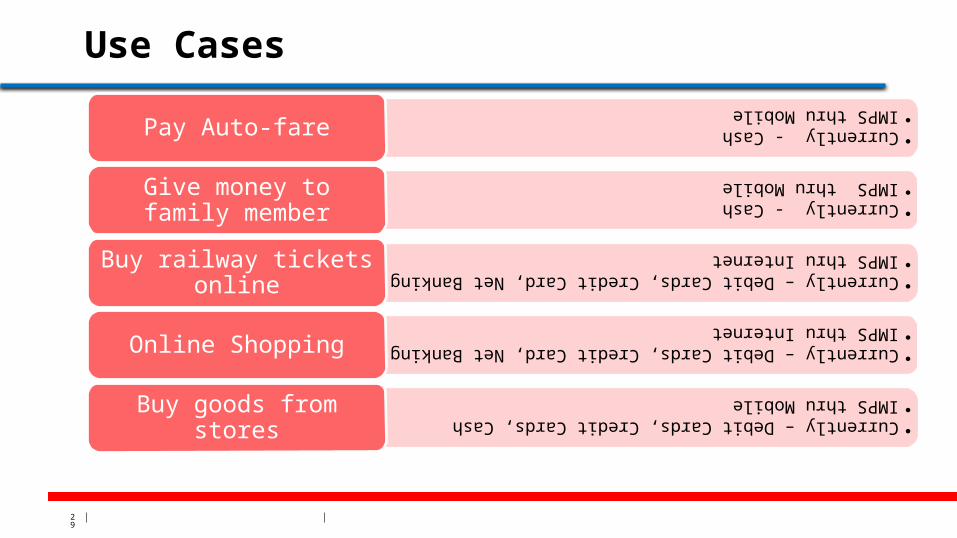

Use Cases

•Currently - Cash

•IMPS thru Mobile

Pay Auto-fare

•Currently - Cash

•IMPS thru Mobile

Give money to family member

•Currently – Debit Cards, Credit Card, Net Banking

•IMPS thru Internet

Buy railway tickets online

•Currently – Debit Cards, Credit Card, Net Banking

•IMPS thru Internet

Online Shopping

•Currently – Debit Cards, Credit Cards, Cash

•IMPS thru Mobile

Buy goods from stores

30

Use-cases

•Currently - NEFT, RTGS, Cheque, Demand-Drafts

•IMPS thru Mobile or Internet

Transfer Funds

•Currently - Cash

•IMPS thru Mobile

Buy vegetables

•Currently – Debit Cards, Credit Card, Net Banking

•IMPS thru Internet

Pay Mobile Bills online

•Currently – Debit Cards, Credit Cards, Cash, Cheque

•IMPS thru Mobile

Pay Mobile Bills at store

•Currently – Cash

•IMPS thru Mobile

Pizza Delivery

31

Pros and ConsAdvantages Disadvantages

Instantaneous

Available all the time

Without using any

additional device such

as Cards, POS

Multiple Channels

available such as Mobile

Application, SMS, USSD

etc

Dependent on Mobile

device

Mobile service is not

quick and not reliable

32

Comparison with other payments

IMPS NEFT RTGS

Time to Process Instantaneous Operates every one hour Instantaneous

Availability 24 X 7 X 365 Available in working hours Available in working hours

Restriction on Amount

Maximum 5 Lakh Maximum 5 Lakh > 2 LakhMaximum 5 Lakh

Service Charge Tiered Charges Tiered Charges Tiered Charges

Geographic spread Supported by 54 Banks 78,000 enabled bank branches

78,000 enabled bank branches

Channels Mobile – SMS, Mobile Application, USSDInternet

Internet, Branch Internet, Branch

Reliability Low due to Mobile Service High High

33

Comparision with other payments

Source : RBI website

34

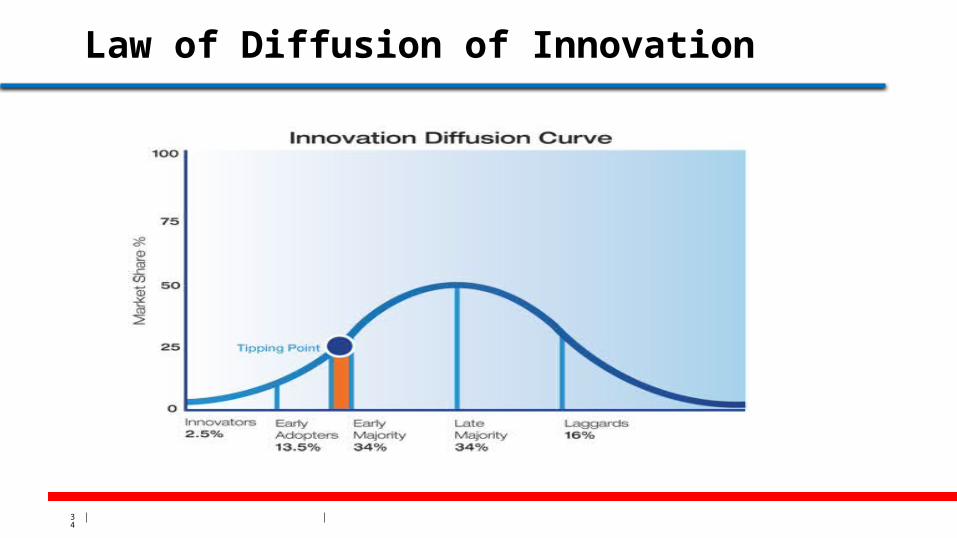

Law of Diffusion of Innovation

35

Future PaymentsMobile Wallets

Mobile Voice Banking Mobile Voice Banking System which authenticates voice input with the help of caller id and

biometric voice authorisation and validates registered users

36

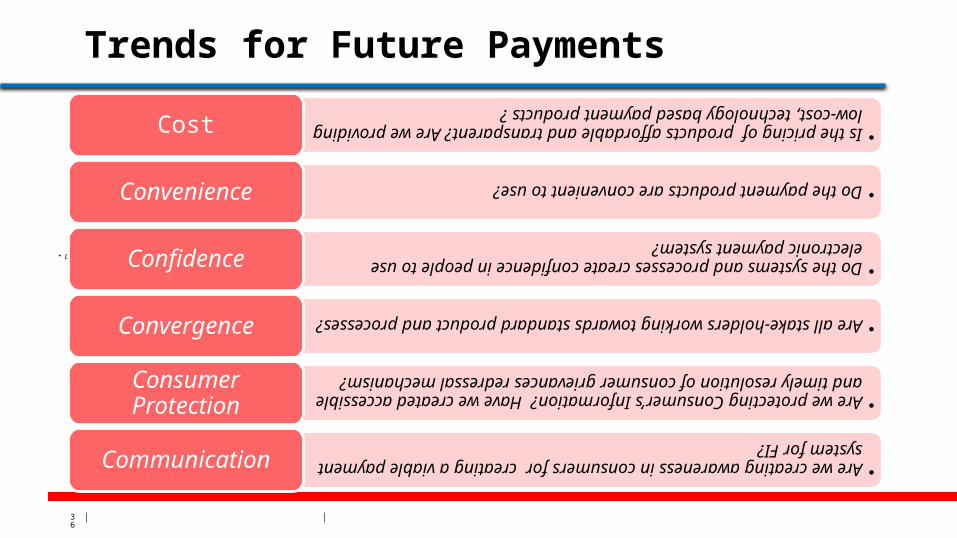

Trends for Future Payments

• Do the payment products are convenient to use?

•Is the pricing of products affordable and transparent? Are we providing low-cost, technology based payment products ?

Cost

•Do the payment products are convenient to use?

Convenience

•Do the systems and processes create confidence in people to use electronic payment system?

Confidence

•Are all stake-holders working towards standard product and processes?

Convergence

•Are we protecting Consumer’s Information? Have we created accessible and timely resolution of consumer grievances redressal mechanism?

Consumer Protection

•Are we creating awareness in consumers for creating a viable payment system for FI?

Communication

37

Innovate to Win

“An innovation is more than just a great idea…. innovation requires attention to other people: what they value and what they will adopt. It must contribute to transformation in a society and be adopted by users.”

38

Thank You

Any Questions?

![GSM Association Unrestricted Official Document: IR · specifications, OMA IMPS v1.2 [3] was published in January 2005. Nowadays most major mobile phone manufacturers include OMA IMPS](https://static.fdocuments.in/doc/165x107/5f95008be538da7f524d5bb7/gsm-association-unrestricted-official-document-ir-specifications-oma-imps-v12.jpg)