Wild Rivers Coast Rural Tourism Studio Agritourism Presentation

Upload

dinhkhuongCategory

view

216download

2

Part 2A of Form ADV: Firm Brochure

Wild Rivers Financial Services LLC

16147 Hwy 101SPO Box 4790

Brookings, OR 97415

Telephone: 541-469-4080Email: [email protected]

Web Address: www.integrity-fp.com

03/15/2011

This brochure provides information about the qualifications and businesspractices of Integrity Financial Planners. If you have any questions about thecontents of this brochure, please contact us at 541-469-4080 [email protected]. The information in this brochure has not been approved orverified by the United States Securities and Exchange Commission or by anystate securities authority.

Additional information about Integrity Financial Planners also is available on theSEC’s website at www.adviserinfo.sec.gov. You can search this site by a uniqueidentifying number, known as a CRD number. Our firm's CRD number is140333.

Item 2 Material ChangesThe SEC adopted "Amendments to Form ADV" in July, 2010. This Firm Brochure, dated03/15/2011, is our new disclosure document prepared according to the SEC’s newrequirements and rules. As a state-registered investment adviser, our firm is required tocomply with the new reporting and filing requirements. As you will see, this document is anarrative that is substantially different in form and content, and includes some newinformation that we were not previously required to disclose.

After our initial filing of this Brochure, this Item will be used to provide our clients with asummary of new and/or updated information. We will inform you of the revision(s) based onthe nature of the updated information.

Consistent with the new rules, we will ensure that you receive a summary of any materialchanges to this and subsequent Brochures within 120 days of the close of our business’ fiscalyear. Furthermore, we will provide you with other interim disclosures about material changesas necessary.

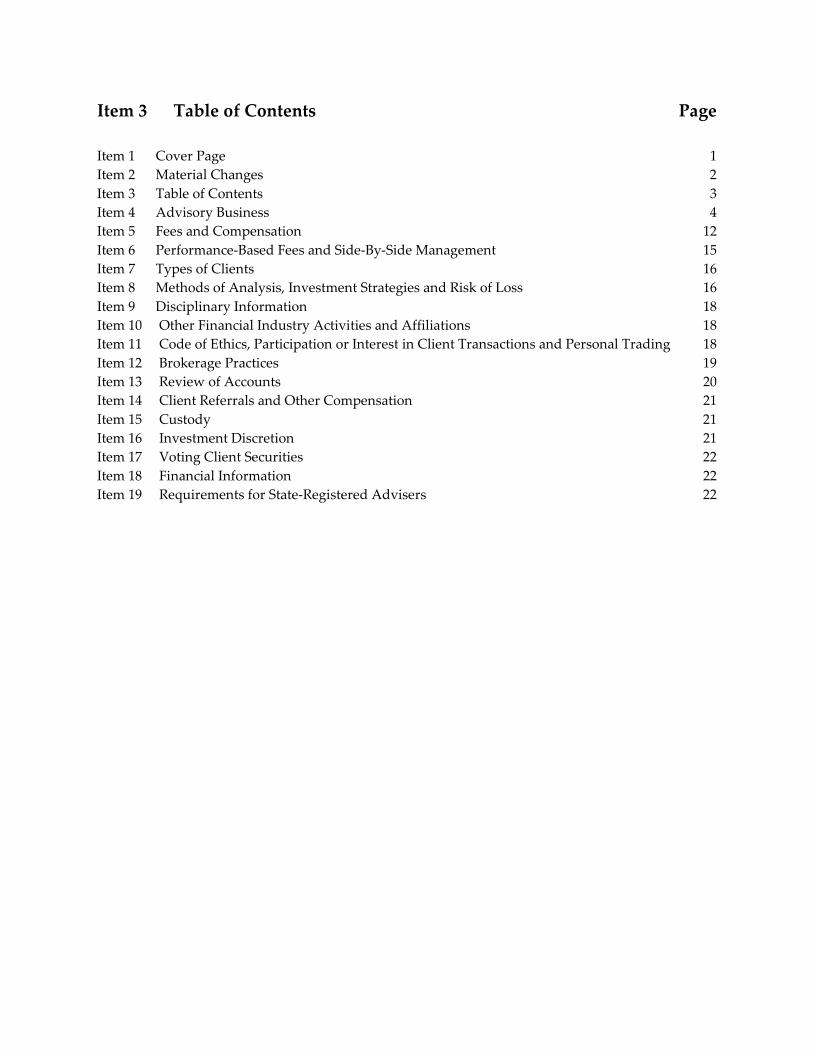

Item 3 Table of Contents Page

Item 1 Cover Page 1Item 2 Material Changes 2Item 3 Table of Contents 3Item 4 Advisory Business 4Item 5 Fees and Compensation 12Item 6 Performance-Based Fees and Side-By-Side Management 15Item 7 Types of Clients 16Item 8 Methods of Analysis, Investment Strategies and Risk of Loss 16Item 9 Disciplinary Information 18Item 10 Other Financial Industry Activities and Affiliations 18Item 11 Code of Ethics, Participation or Interest in Client Transactions and Personal Trading 18Item 12 Brokerage Practices 19Item 13 Review of Accounts 20Item 14 Client Referrals and Other Compensation 21Item 15 Custody 21Item 16 Investment Discretion 21Item 17 Voting Client Securities 22Item 18 Financial Information 22Item 19 Requirements for State-Registered Advisers 22

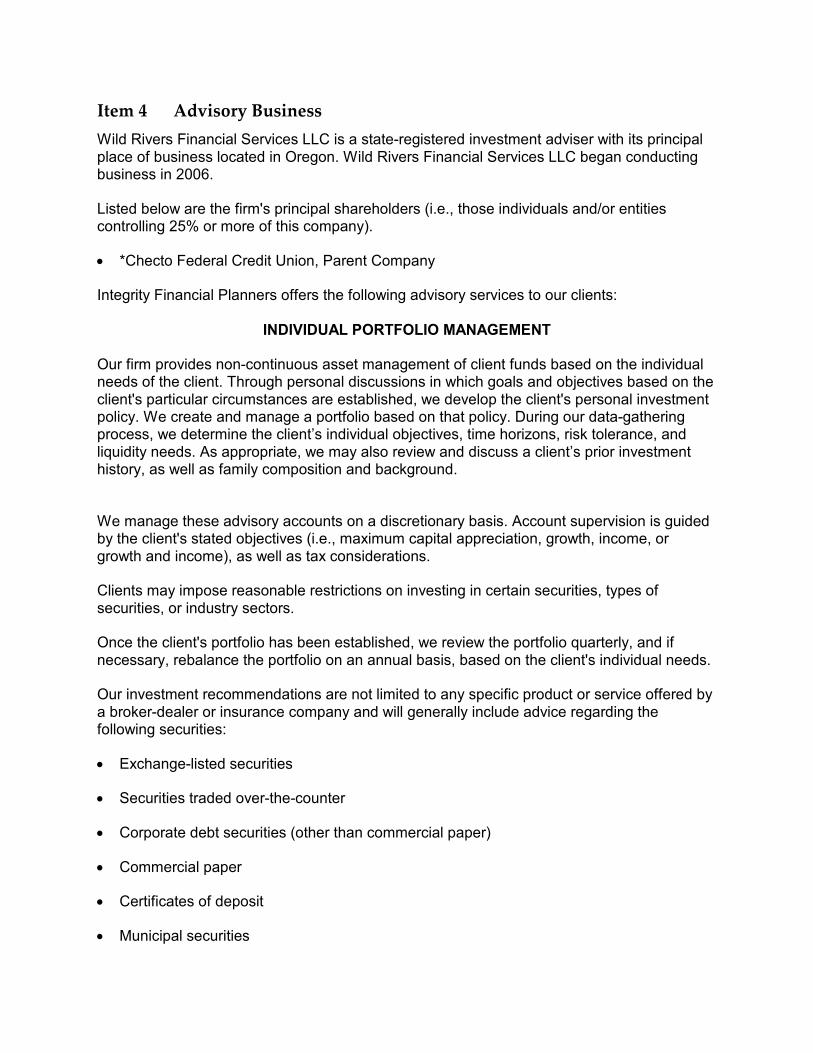

Item 4 Advisory BusinessWild Rivers Financial Services LLC is a state-registered investment adviser with its principalplace of business located in Oregon. Wild Rivers Financial Services LLC began conductingbusiness in 2006.

Listed below are the firm's principal shareholders (i.e., those individuals and/or entitiescontrolling 25% or more of this company).

*Checto Federal Credit Union, Parent Company

Integrity Financial Planners offers the following advisory services to our clients:

INDIVIDUAL PORTFOLIO MANAGEMENT

Our firm provides non-continuous asset management of client funds based on the individualneeds of the client. Through personal discussions in which goals and objectives based on theclient's particular circumstances are established, we develop the client's personal investmentpolicy. We create and manage a portfolio based on that policy. During our data-gatheringprocess, we determine the client’s individual objectives, time horizons, risk tolerance, andliquidity needs. As appropriate, we may also review and discuss a client’s prior investmenthistory, as well as family composition and background.

We manage these advisory accounts on a discretionary basis. Account supervision is guidedby the client's stated objectives (i.e., maximum capital appreciation, growth, income, orgrowth and income), as well as tax considerations.

Clients may impose reasonable restrictions on investing in certain securities, types ofsecurities, or industry sectors.

Once the client's portfolio has been established, we review the portfolio quarterly, and ifnecessary, rebalance the portfolio on an annual basis, based on the client's individual needs.

Our investment recommendations are not limited to any specific product or service offered bya broker-dealer or insurance company and will generally include advice regarding thefollowing securities:

Exchange-listed securities

Securities traded over-the-counter

Corporate debt securities (other than commercial paper)

Commercial paper

Certificates of deposit

Municipal securities

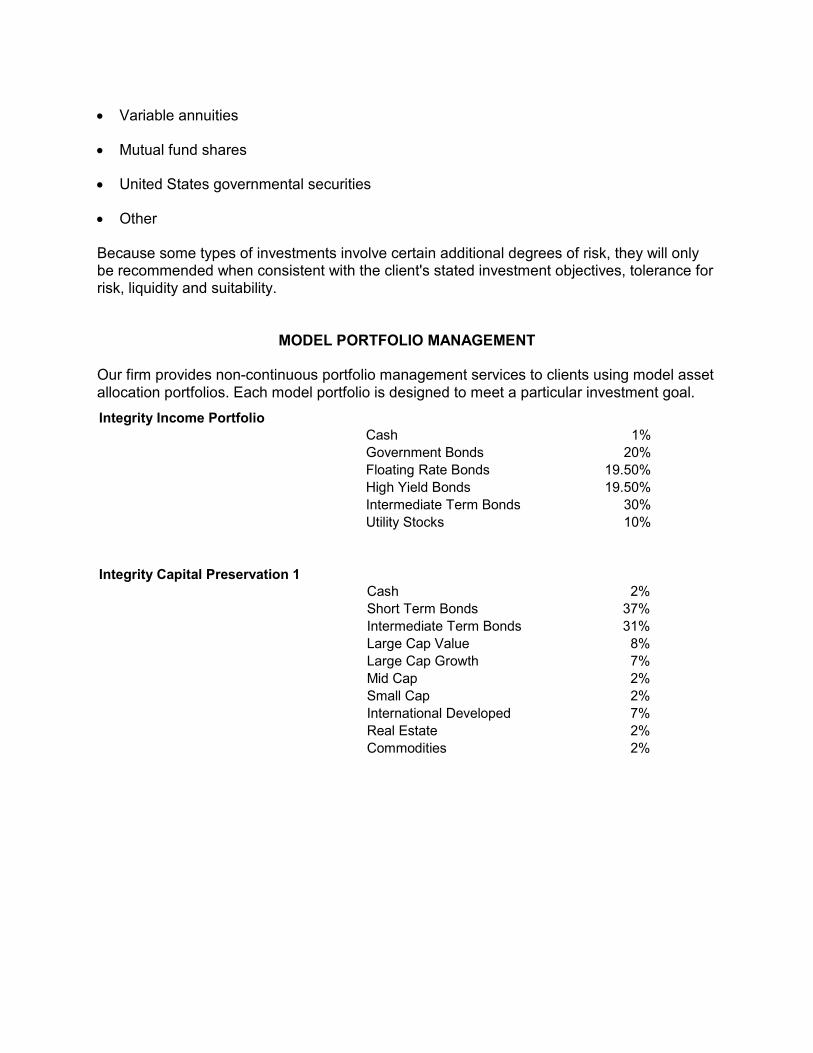

Variable annuities

Mutual fund shares

United States governmental securities

Other

Because some types of investments involve certain additional degrees of risk, they will onlybe recommended when consistent with the client's stated investment objectives, tolerance forrisk, liquidity and suitability.

MODEL PORTFOLIO MANAGEMENT

Our firm provides non-continuous portfolio management services to clients using model assetallocation portfolios. Each model portfolio is designed to meet a particular investment goal.Integrity Income Portfolio

Cash 1%Government Bonds 20%Floating Rate Bonds 19.50%High Yield Bonds 19.50%Intermediate Term Bonds 30%Utility Stocks 10%

Integrity Capital Preservation 1Cash 2%Short Term Bonds 37%Intermediate Term Bonds 31%Large Cap Value 8%Large Cap Growth 7%Mid Cap 2%Small Cap 2%International Developed 7%Real Estate 2%Commodities 2%

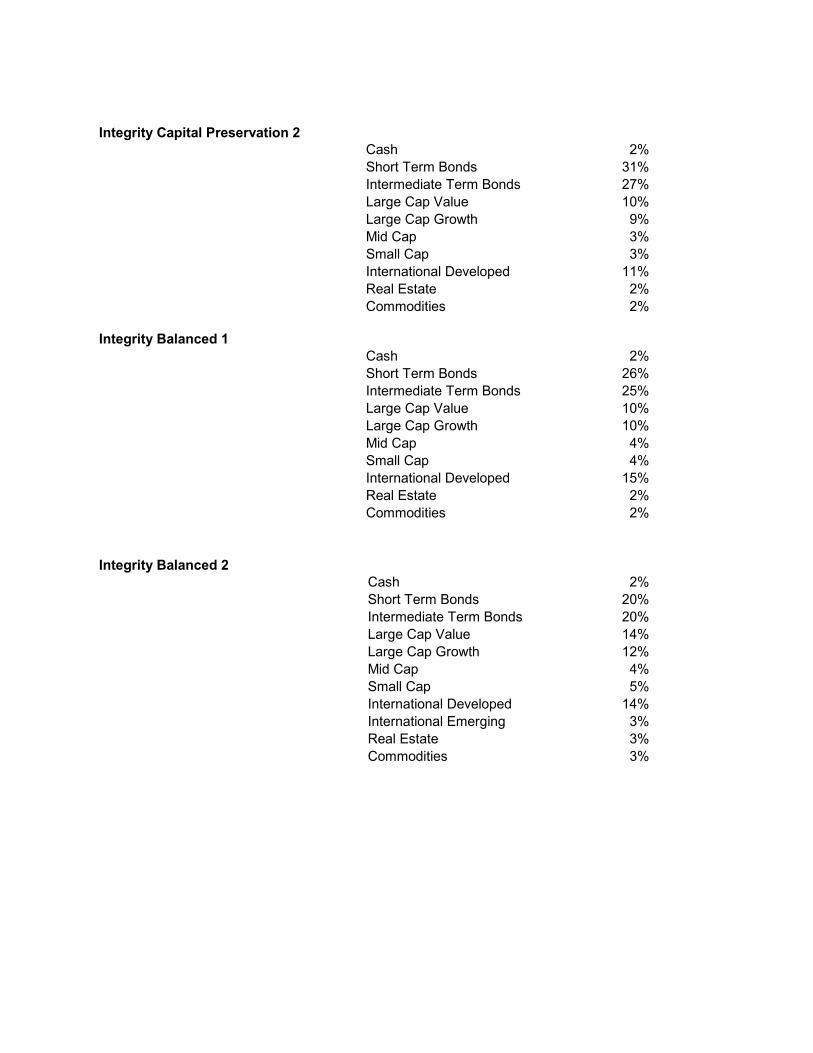

Integrity Capital Preservation 2Cash 2%Short Term Bonds 31%Intermediate Term Bonds 27%Large Cap Value 10%Large Cap Growth 9%Mid Cap 3%Small Cap 3%International Developed 11%Real Estate 2%Commodities 2%

Integrity Balanced 1Cash 2%Short Term Bonds 26%Intermediate Term Bonds 25%Large Cap Value 10%Large Cap Growth 10%Mid Cap 4%Small Cap 4%International Developed 15%Real Estate 2%Commodities 2%

Integrity Balanced 2Cash 2%Short Term Bonds 20%Intermediate Term Bonds 20%Large Cap Value 14%Large Cap Growth 12%Mid Cap 4%Small Cap 5%International Developed 14%International Emerging 3%Real Estate 3%Commodities 3%

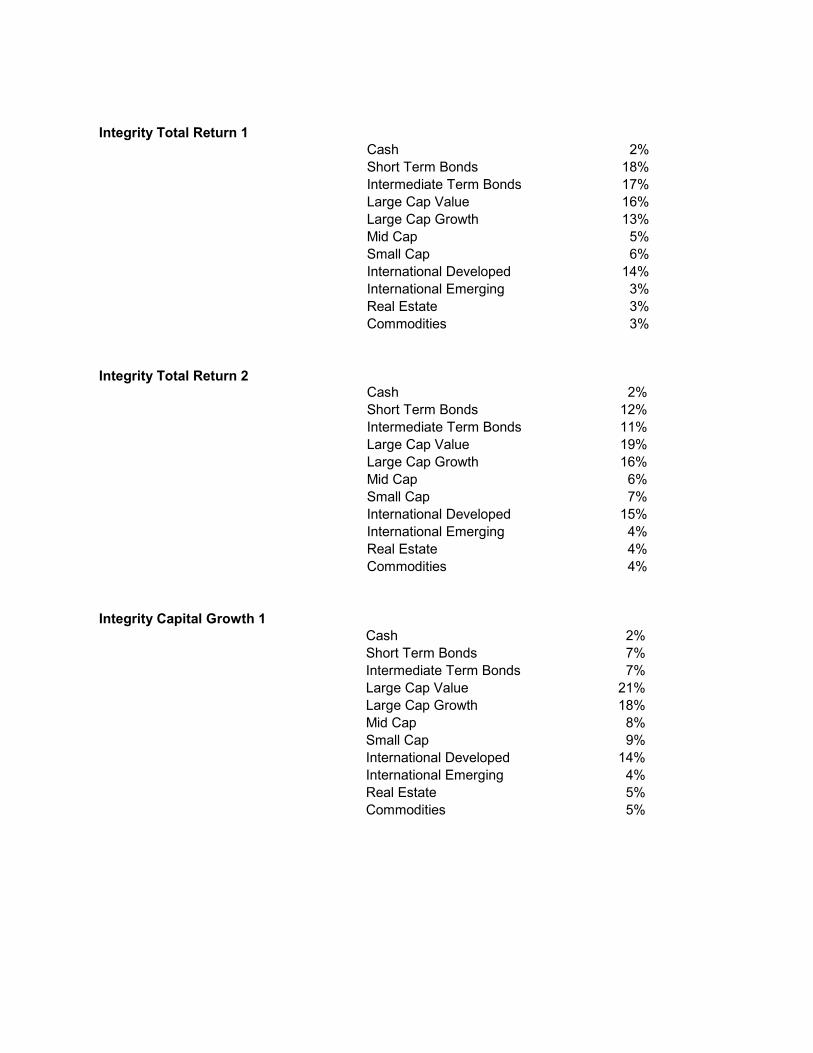

Integrity Total Return 1Cash 2%Short Term Bonds 18%Intermediate Term Bonds 17%Large Cap Value 16%Large Cap Growth 13%Mid Cap 5%Small Cap 6%International Developed 14%International Emerging 3%Real Estate 3%Commodities 3%

Integrity Total Return 2Cash 2%Short Term Bonds 12%Intermediate Term Bonds 11%Large Cap Value 19%Large Cap Growth 16%Mid Cap 6%Small Cap 7%International Developed 15%International Emerging 4%Real Estate 4%Commodities 4%

Integrity Capital Growth 1Cash 2%Short Term Bonds 7%Intermediate Term Bonds 7%Large Cap Value 21%Large Cap Growth 18%Mid Cap 8%Small Cap 9%International Developed 14%International Emerging 4%Real Estate 5%Commodities 5%

Integrity Capital Growth 2Cash 2%Short Term Bonds 3%Intermediate Term Bonds 3%Large Cap Value 23%Large Cap Growth 20%Mid Cap 9%Small Cap 10%International Developed 16%International Emerging 4%Real Estate 5%Commodities 5%

Through personal discussions with the client in which the client's goals and objectives areestablished, we initially determine whether the model portfolio is suitable to the client'scircumstances. Once we confirm suitability, the portfolio is managed based on the portfolio'sgoal, rather than on each client's individual needs. Clients, nevertheless, have the opportunityto place reasonable restrictions on the types of investments to be held in their account.Clients retain individual ownership of all securities.

We manage these advisory accounts on a discretionary basis. Account supervision is guidedby the client's stated objectives (i.e., maximum capital appreciation, growth, income, orgrowth and income), as well as tax considerations.

Once the client's portfolio has been established, we review the portfolio quarterly, and ifnecessary, rebalance the portfolio on an annual basis, based on the client's individual needs.

Through personal discussions with the client in which the client's goals and objectives areestablished, we determine if the model portfolio is suitable to the client's circumstances. Oncewe determine the suitability of the portfolio, the portfolio is managed based on the portfolio'sgoal, rather than on each client's individual needs. Clients, nevertheless, have the opportunityto place reasonable restrictions on the types of investments to be held in their account.Clients retain individual ownership of all securities.

Our investment recommendations are not limited to any specific product or service offered bya broker dealer or insurance company and will generally include advice regarding thefollowing securities:

Exchange-listed securities

Corporate debt securities (other than commercial paper)

Municipal securities

Mutual fund shares

United States governmental securities

Because some types of investments involve certain additional degrees of risk, they will onlybe implemented/recommended when consistent with the client's stated investment objectives,tolerance for risk, liquidity and suitability.

To ensure that our initial determination of an appropriate portfolio remains suitable and thatthe account continues to be managed in a manner consistent with the client's financialcircumstances, we will:

1. at least quarterly, contact each participating client to determine whether there have beenany changes in the client's financial situation or investment objectives, and whether theclient wishes to impose investment restrictions or modify existing restrictions;

2. be reasonably available to consult with the client; and

3. maintain client suitability information in each client's file.

FINANCIAL PLANNING

We provide financial planning services. Financial planning is a comprehensive evaluation of aclient’s current and future financial state by using currently known variables to predict futurecash flows, asset values and withdrawal plans. Through the financial planning process, allquestions, information and analysis are considered as they impact and are impacted by theentire financial and life situation of the client. Clients purchasing this service receive a writtenreport which provides the client with a detailed financial plan designed to assist the clientachieve his or her financial goals and objectives.

In general, the financial plan can address any or all of the following areas:

PERSONAL: We review family records, budgeting, personal liability, estate informationand financial goals.

TAX & CASH FLOW: We analyze the client’s income tax and spending and planning forpast, current and future years; then illustrate the impact of various investments on theclient's current income tax and future tax liability.

INVESTMENTS: We analyze investment alternatives and their effect on the client'sportfolio.

INSURANCE: We review existing policies to ensure proper coverage for life, health,disability, long-term care, liability, home and automobile.

RETIREMENT: We analyze current strategies and investment plans to help the clientachieve his or her retirement goals.

DEATH & DISABILITY: We review the client’s cash needs at death, income needs ofsurviving dependents, estate planning and disability income.

ESTATE: We assist the client in assessing and developing long-term strategies, includingas appropriate, living trusts, wills, review estate tax, powers of attorney, asset protectionplans, nursing homes, Medicaid and elder law.

We gather required information through in-depth personal interviews. Information gatheredincludes the client's current financial status, tax status, future goals, returns objectives andattitudes towards risk. We carefully review documents supplied by the client, including aquestionnaire completed by the client, and prepare a written report. Should the client chooseto implement the recommendations contained in the plan, we suggest the client work closelywith his/her attorney, accountant, insurance agent, and/or stockbroker. Implementation offinancial plan recommendations is entirely at the client's discretion.

We also provide general non-securities advice on topics that may include tax and budgetaryplanning, estate planning and business planning.

Exchange-listed securities

Securities traded over-the-counter

Corporate debt securities (other than commercial paper)

Commercial paper

Certificates of deposit

Municipal securities

Variable life insurance

Variable annuities

Mutual fund shares

United States governmental securities

Interests in partnerships investing in real estate

Interests in partnerships investing in oil and gas interests

Typically the financial plan is presented to the client within six months of the contract date,provided that all information needed to prepare the financial plan has been promptlyprovided.

Financial Planning recommendations are not limited to any specific product or service offeredby a broker-dealer or insurance company. All recommendations are of a generic nature.

AMOUNT OF MANAGED ASSETS

As of 12/31/2010, we were actively managing $31,466,667 of clients' assets on adiscretionary basis plus $1,282,916 of clients' assets on a non-discretionary basis.

Item 5 Fees and CompensationPORTFOLIO MANAGEMENT SERVICES FEES

The annualized fee for Portfolio Management Services will be charged as a percentage ofassets under management, according to the following schedule:

Assets Under Management Annual Fee$100,000 - $500,000 1.00%

$500,001 - $1,000,000 0.85% $1,000,001 - $2,000,000 0.55% $2,000,001 - $5,000,000 0.40% $5,000,001 and above Negotiable

Our fees are billed quarterly, in advance, at the beginning of each calendar quarter basedupon the value (market value or fair market value in the absence of market value), of theclient's account at the end of the previous quarter. Fees will be debited from the account inaccordance with the client authorization in the Client Services Agreement.

A minimum of $100,000 of assets under management is required for this service. Thisaccount size may be negotiable under certain circumstances. Integrity Financial Plannersmay group certain related client accounts for the purposes of achieving the minimum accountsize and determining the annualized fee.

Limited Negotiability of Advisory Fees: Although Integrity Financial Planners hasestablished the aforementioned fee schedule(s), we retain the discretion to negotiatealternative fees on a client-by-client basis. Client facts, circumstances and needs will beconsidered in determining the fee schedule. These include the complexity of the client, assetsto be placed under management, anticipated future additional assets; related accounts;portfolio style, account composition, reports, among other factors. The specific annual feeschedule will be identified in the contract between the adviser and each client.

We may group certain related client accounts for the purposes of achieving the minimumaccount size requirements and determining the annualized fee.

Discounts, not generally available to our advisory clients, may be offered to family membersand friends of associated persons of our firm.

MODEL PORTFOLIO MANAGEMENT FEES

The annualized fee for Model Portfolio Management Services will be charged as apercentage of assets under management, according to the following schedule:

Assets Under Management Annual Fee$100,000 - $500,000 1.00%

$500,001 - $1,000,000 0.85% $1,000,001 - $2,000,000 0.55% $2,000,001 - $5,000,000 0.40%

$5,000,001 and above NegotiableOur fees are billed quarterly, in advance, at the beginning of each calendar quarter basedupon the value (market value or fair market value in the absence of market value), of theclient's account at the end of the previous quarter. Fees will be debited from the account inaccordance with the client authorization in the Client Services Agreement.

A minimum of $100,000 of assets under management is required for this service. Thisaccount size may be negotiable under certain circumstances. Integrity Financial Plannersmay group certain related client accounts for the purposes of achieving the minimum accountsize and determining the annualized fee.

Limited Negotiability of Advisory Fees: Although Integrity Financial Planners hasestablished the aforementioned fee schedule(s), we retain the discretion to negotiatealternative fees on a client-by-client basis. Client facts, circumstances and needs will beconsidered in determining the fee schedule. These include the complexity of the client, assetsto be placed under management, anticipated future additional assets; related accounts;portfolio style, account composition, reports, among other factors. The specific annual feeschedule will be identified in the contract between the adviser and each client.

We may group certain related client accounts for the purposes of achieving the minimumaccount size requirements and determining the annualized fee.

Discounts, not generally available to our advisory clients, may be offered to family membersand friends of associated persons of our firm.

FINANCIAL PLANNING FEES

Integrity Financial Planners' Financial Planning fee will be determined based on the nature ofthe services being provided and the complexity of each client’s circumstances. All fees areagreed upon prior to entering into a contract with any client.

Our Financial Planning fees are calculated and charged on a fixed fee basis, typically rangingfrom $5,000 to $10,000, depending on the specific arrangement reached with the client.

We may request a retainer upon completion of our initial fact-finding session with the client;however, advance payment will never exceed $500 for work that will not be completed withinsix months. The balance is due upon completion of the plan.

Financial Planning Fee Offset: Integrity Financial Planners reserves the discretion toreduce or waive the hourly fee and/or the minimum fixed fee if a financial planning clientchooses to engage us for our Portfolio Management Services.

The client will be billed quarterly in advance based on our total estimated Financial Planningfees.

GENERAL INFORMATION

Termination of the Advisory Relationship: A client agreement may be canceled at anytime, by either party, for any reason upon receipt of 30 days written notice. As disclosedabove, certain fees are paid in advance of services provided. Upon termination of anyaccount, any prepaid, unearned fees will be promptly refunded. In calculating a client’sreimbursement of fees, we will pro rate the reimbursement according to the number of daysremaining in the billing period.

Mutual Fund Fees: All fees paid to Integrity Financial Planners for investment advisoryservices are separate and distinct from the fees and expenses charged by mutual fundsand/or EFTs to their shareholders. These fees and expenses are described in each fund'sprospectus. These fees will generally include a management fee, other fund expenses, and apossible distribution fee. If the fund also imposes sales charges, a client may pay an initial ordeferred sales charge. A client could invest in a mutual fund directly, without our services. Inthat case, the client would not receive the services provided by our firm which are designed,among other things, to assist the client in determining which mutual fund or funds are mostappropriate to each client's financial condition and objectives. Accordingly, the client shouldreview both the fees charged by the funds and our fees to fully understand the total amountof fees to be paid by the client and to thereby evaluate the advisory services being provided.

Wrap Fee Programs and Separately Managed Account Fees: Clients participating inseparately managed account programs may be charged various program fees in addition tothe advisory fee charged by our firm. Such fees may include the investment advisory fees ofthe independent advisers, which may be charged as part of a wrap fee arrangement. In awrap fee arrangement, clients pay a single fee for advisory, brokerage and custodial services.Client’s portfolio transactions may be executed without commission charge in a wrap fee

arrangement. In evaluating such an arrangement, the client should also consider that,depending upon the level of the wrap fee charged by the broker-dealer, the amount ofportfolio activity in the client’s account, and other factors, the wrap fee may or may notexceed the aggregate cost of such services if they were to be provided separately. We willreview with clients any separate program fees that may be charged to clients.

Additional Fees and Expenses: In addition to our advisory fees, clients are alsoresponsible for the fees and expenses charged by custodians and imposed by brokerdealers, including, but not limited to, any transaction charges imposed by a broker dealer withwhich an independent investment manager effects transactions for the client's account(s).Please refer to the "Brokerage Practices" section (Item 12) of this Form ADV for additionalinformation.

ERISA Accounts: Integrity Financial Planners is deemed to be a fiduciary to advisory clientsthat are employee benefit plans or individual retirement accounts (IRAs) pursuant to theEmployee Retirement Income and Securities Act (“ERISA”). As such, our firm is subject tospecific duties and obligations under ERISA and the Internal Revenue Code that includeamong other things, restrictions concerning certain forms of compensation. To avoidengaging in prohibited transactions, Integrity Financial Planners may only charge fees forinvestment advice about products for which our firm and/or our related persons do notreceive any commissions or 12b-1 fees, or conversely, investment advice about products forwhich our firm and/or our related persons receive commissions or 12b-1 fees, however, onlywhen such fees are used to offset Integrity Financial Planners' advisory fees.

Advisory Fees in General: Clients should note that similar advisory services may (or maynot) be available from other registered (or unregistered) investment advisers for similar orlower fees.

Limited Prepayment of Fees: Under no circumstances do we require or solicit payment offees in excess of $500 more than six months in advance of services rendered. Asstate-registered advisers are subject to the rules and regulations of their home state (i.e., thestate in which the firm maintains its principal place of business) these firms should reviewhome state requirements which may limit prepayment of fees in excess of $500.

Item 6 Performance-Based Fees and Side-By-Side ManagementIntegrity Financial Planners does not charge performance-based fees.

Item 7 Types of ClientsIntegrity Financial Planners provides advisory services to the following types of clients:

Individuals (other than high net worth individuals)

High net worth individuals

Charitable organizations

Corporations or other businesses not listed above

Item 8 Methods of Analysis, Investment Strategies and Risk of LossMETHODS OF ANALYSIS

We use the following methods of analysis in formulating our investment advice and/ormanaging client assets:

Charting. In this type of technical analysis, we review charts of market and security activityin an attempt to identify when the market is moving up or down and to predict when how longthe trend may last and when that trend might reverse.

Fundamental Analysis. We attempt to measure the intrinsic value of a security by lookingat economic and financial factors (including the overall economy, industry conditions, and thefinancial condition and management of the company itself) to determine if the company isunderpriced (indicating it may be a good time to buy) or overpriced (indicating it may be timeto sell).

Fundamental analysis does not attempt to anticipate market movements. This presents apotential risk, as the price of a security can move up or down along with the overall marketregardless of the economic and financial factors considered in evaluating the stock.

Technical Analysis. We analyze past market movements and apply that analysis to thepresent in an attempt to recognize recurring patterns of investor behavior and potentiallypredict future price movement.

Technical analysis does not consider the underlying financial condition of a company. Thispresents a risk in that a poorly-managed or financially unsound company may underperformregardless of market movement.

Cyclical Analysis. In this type of technical analysis, we measure the movements of aparticular stock against the overall market in an attempt to predict the price movement of thesecurity.

Asset Allocation. Rather than focusing primarily on securities selection, we attempt toidentify an appropriate ratio of securities, fixed income, and cash suitable to the client’sinvestment goals and risk tolerance.

A risk of asset allocation is that the client may not participate in sharp increases in aparticular security, industry or market sector. Another risk is that the ratio of securities, fixedincome, and cash will change over time due to stock and market movements and, if notcorrected, will no longer be appropriate for the client’s goals.

Mutual Fund and/or ETF Analysis. We look at the experience and track record of themanager of the mutual fund or ETF in an attempt to determine if that manager hasdemonstrated an ability to invest over a period of time and in different economic conditions.We also look at the underlying assets in a mutual fund or ETF in an attempt to determine ifthere is significant overlap in the underlying investments held in another fund(s) in the client’sportfolio. We also monitor the funds or ETFs in an attempt to determine if they are continuingto follow their stated investment strategy.

A risk of mutual fund and/or ETF analysis is that, as in all securities investments, pastperformance does not guarantee future results. A manager who has been successful may notbe able to replicate that success in the future. In addition, as we do not control the underlyinginvestments in a fund or ETF, managers of different funds held by the client may purchasethe same security, increasing the risk to the client if that security were to fall in value. There isalso a risk that a manager may deviate from the stated investment mandate or strategy of thefund or ETF, which could make the holding(s) less suitable for the client’s portfolio.

Risks for all forms of analysis. Our securities analysis methods rely on the assumptionthat the companies whose securities we purchase and sell, the rating agencies that reviewthese securities, and other publicly-available sources of information about these securities,are providing accurate and unbiased data. While we are alert to indications that data may beincorrect, there is always a risk that our analysis may be compromised by inaccurate ormisleading information.

INVESTMENT STRATEGIES

We use the following strategy(ies) in managing client accounts, provided that suchstrategy(ies) are appropriate to the needs of the client and consistent with the client'sinvestment objectives, risk tolerance, and time horizons, among other considerations:

Long-term purchases. We purchase securities with the idea of holding them in the client'saccount for a year or longer. Typically we employ this strategy when:

we believe the securities to be currently undervalued, and/or

we want exposure to a particular asset class over time, regardless of the currentprojection for this class.

A risk in a long-term purchase strategy is that by holding the security for this length of time,we may not take advantages of short-term gains that could be profitable to a client. Moreover,

if our predictions are incorrect, a security may decline sharply in value before we make thedecision to sell.

Short-term purchases. When utilizing this strategy, we purchase securities with the idea ofselling them within a relatively short time (typically a year or less). We do this in an attempt totake advantage of conditions that we believe will soon result in a price swing in the securitieswe purchase.

Item 9 Disciplinary InformationWe are required to disclose any legal or disciplinary events that are material to a client's orprospective client's evaluation of our advisory business or the integrity of our management.

Our firm and our management personnel have no reportable disciplinary events to disclose.

Item 10 Other Financial Industry Activities and AffiliationsOur firm and our related persons are not engaged in other financial industry activities andhave no other industry affiliations.

We are a registered investment adviser and a wholly owned subsidiary of Chetco FederalCredit Union, a national credit union that offers a broad spectrum of banking products andfinancial services to consumers, small businesses and commercial clients.

Where appropriate, Integrity Financial Planners and our employees may recommend thevarious investment and investment-related services of the Chetco Federal Credit Union to ouradvisory clients. Chetco Federal Credit Union and their employees may also recommend theadvisory services of our firm to their clients. The services provided by the Chetco FederalCredit Union are separate and distinct from our advisory services, and are provided forseparate and additional compensation. No Integrity Financial Planners client is obligated touse the services of any of the Chetco Federal Credit Union.

Item 11 Code of Ethics, Participation or Interest in Client Transactions andPersonal TradingOur firm has adopted a Code of Ethics which sets forth high ethical standards of businessconduct that we require of our employees, including compliance with applicable federalsecurities laws.

Integrity Financial Planners and our personnel owe a duty of loyalty, fairness and good faithtowards our clients, and have an obligation to adhere not only to the specific provisions of theCode of Ethics but to the general principles that guide the Code.

Our Code of Ethics includes policies and procedures for the review of quarterly securitiestransactions reports as well as initial and annual securities holdings reports that must besubmitted by the firm’s access persons. Among other things, our Code of Ethics also requires

the prior approval of any acquisition of securities in a limited offering (e.g., private placement)or an initial public offering. Our code also provides for oversight, enforcement andrecordkeeping provisions.

Integrity Financial Planners' Code of Ethics further includes the firm's policy prohibiting theuse of material non-public information. While we do not believe that we have any particularaccess to non-public information, all employees are reminded that such information may notbe used in a personal or professional capacity.

A copy of our Code of Ethics is available to our advisory clients and prospective clients. Youmay request a copy by email sent to [email protected], or by calling us at 541-469-4080.

Integrity Financial Planners and individuals associated with our firm are prohibited fromengaging in principal transactions.

Integrity Financial Planners and individuals associated with our firm are prohibited fromengaging in agency cross transactions.

Our Code of Ethics is designed to assure that the personal securities transactions, activitiesand interests of our employees will not interfere with (i) making decisions in the best interestof advisory clients and (ii) implementing such decisions while, at the same time, allowingemployees to invest for their own accounts.

Our firm and/or individuals associated with our firm may buy or sell for their personalaccounts securities identical to or different from those recommended to our clients. Inaddition, any related person(s) may have an interest or position in a certain security(ies)which may also be recommended to a client.

It is the expressed policy of our firm that no person employed by us may purchase or sell anysecurity prior to a transaction(s) being implemented for an advisory account, therebypreventing such employee(s) from benefiting from transactions placed on behalf of advisoryaccounts.

Item 12 Brokerage PracticesFor discretionary clients, Integrity Financial Planners requires these clients to provide us withwritten authority to determine the broker dealer to use. There are no commission costs thatwill be charged to these clients for these transactions.

Integrity Financial Planners does not have any soft-dollar arrangements and does not receiveany soft-dollar benefits.

As a matter of policy and practice, Integrity Financial Planners does not generally block clienttrades and, therefore, we implement client transactions separately for each account.Consequently, certain client trades may be executed before others, at a different price and/orcommission rate. Additionally, our clients may not receive volume discounts available toadvisers who block client trades.

Item 13 Review of AccountsPORTFOLIO MANAGEMENT SERVICES

REVIEWS: While the underlying securities within Individual Portfolio Management Servicesaccounts are continually monitored, these accounts are reviewed quarterly. Accounts arereviewed in the context of each client's stated investment objectives and guidelines. Morefrequent reviews may be triggered by material changes in variables such as the client'sindividual circumstances, or the market, political or economic environment.

These accounts are reviewed by: Charles Blozinski, CFP and Thomas Goodwin, CFP, EA.

REPORTS: In addition to the monthly statements and confirmations of transactions thatPortfolio Management Services clients receive from their broker-dealer, Integrity FinancialPlanners will provide annual reports summarizing account performance, balances andholdings.

MODEL PORTFOLIO MANAGEMENT SERVICES

REVIEWS: While the underlying securities within Model Portfolio Management Servicesaccounts are regularly monitored, these accounts are reviewed on a quarterly basis.Accounts are reviewed in the context of the investment objectives and guidelines of eachmodel portfolio as well as any investment restrictions provided by the client. More frequentreviews may be triggered by material changes in variables such as the client's individualcircumstances, or the market, political or economic environment.

These accounts are reviewed by: Charles Blozinski, CFP and Thomas Goodwin, CFP, EA.

REPORTS: In addition to the monthly statements and confirmations of transactions thatModel Portfolio Management Services clients receive from their broker-dealer, IntegrityFinancial Planners will provide annual reports summarizing account performance, balancesand holdings. These reports will also remind the client to notify us if there have been changesin the client's financial situation or investment objectives and whether the client wishes toimpose investment restrictions or modify existing restrictions.

FINANCIAL PLANNING SERVICES

REVIEWS: While reviews may occur at different stages depending on the nature and termsof the specific engagement, typically no formal reviews will be conducted for FinancialPlanning clients unless otherwise contracted for.

REPORTS: Financial Planning clients will receive a completed financial plan. Additionalreports will not typically be provided unless otherwise contracted for.

Item 14 Client Referrals and Other CompensationIt is Integrity Financial Planners' policy not to engage solicitors or to pay related ornon-related persons for referring potential clients to our firm.

It is Integrity Financial Planners' policy not to accept or allow our related persons to acceptany form of compensation, including cash, sales awards or other prizes, from a non-client inconjunction with the advisory services we provide to our clients.

Item 15 CustodyWe previously disclosed in the "Fees and Compensation" section (Item 5) of this Brochurethat our firm directly debits advisory fees from client accounts.

As part of this billing process, the client's custodian is advised of the amount of the fee to bededucted from that client's account. On at least a quarterly basis, the custodian is required tosend to the client a statement showing all transactions within the account during the reportingperiod.

Because the custodian does not calculate the amount of the fee to be deducted, it isimportant for clients to carefully review their custodial statements to verify the accuracy of thecalculation, among other things. Clients should contact us directly if they believe that theremay be an error in their statement.

Our firm does not have actual or constructive custody of client accounts.

Item 16 Investment DiscretionClients may hire us to provide discretionary asset management services, in which case weplace trades in a client's account without contacting the client prior to each trade to obtain theclient's permission.

Our discretionary authority includes the ability to do the following without contacting the client:

Determine the security to buy or sell; and/or

Determine the amount of the security to buy or sell

Clients give us discretionary authority when they sign a discretionary agreement with our firm,and may limit this authority by giving us written instructions. Clients may also change/amendsuch limitations by once again providing us with written instructions.

As previously disclosed in Item 4 of this brochure, our firm does not provide discretionaryasset management services.

Item 17 Voting Client SecuritiesAs a matter of firm policy, we do not vote proxies on behalf of clients. Therefore, although ourfirm may provide investment advisory services relative to client investment assets, clientsmaintain exclusive responsibility for: (1) directing the manner in which proxies solicited byissuers of securities beneficially owned by the client shall be voted, and (2) making allelections relative to any mergers, acquisitions, tender offers, bankruptcy proceedings or othertype events pertaining to the client’s investment assets. Clients are responsible for instructingeach custodian of the assets, to forward to the client copies of all proxies and shareholdercommunications relating to the client’s investment assets.

We may provide clients with consulting assistance regarding proxy issues if they contact uswith questions at our principal place of business.

Item 18 Financial InformationIntegrity Financial Planners has no additional no financial circumstances to report.

Under no circumstances do we require or solicit payment of fees in excess of $500 per clientmore than six months in advance of services rendered. Therefore, we are not required toinclude a financial statement.

Integrity Financial Planners has not been the subject of a bankruptcy petition at any timeduring the past ten years.

Item 19 Requirements for State-Registered AdvisersThe following individuals are the principal executive officers and management persons ofIntegrity Financial Planners:

Charles Richard Blozinski, President and CEO

Thomas George Goodwin, Vice President and CCO

Information regarding the formal education and business background for each of theseindividuals is provided in their respective Brochure Supplements.

Part 2B of Form ADV: Brochure Supplement

Charles Richard Blozinski97786 Hanscam Lane

Harbor, OR 97415541-661-4657

Integrity Financial Planners

Brookings, OR 97415

03/15/2011

This brochure supplement provides information about Charles Richard Blozinskithat supplements the Integrity Financial Planners brochure. You should havereceived a copy of that brochure. Please contact Thomas Goodwin if you didnot receive Integrity Financial Planners' brochure or if you have any questionsabout the contents of this supplement.

Additional information about Charles Richard Blozinski is available on the SEC’swebsite at www.adviserinfo.sec.gov

Item 2 Educational, Background and Business ExperienceFull Legal Name: Charles Richard Blozinski Born: 1956

Education

University of California Los Angeles; BA, Econimics; 1982

College of Marin; 1980

Business Experience

Wild Rivers Financial Services LLC d/b/a/ Integrity Financial Planners; Presidentand CEO; from 07/2006 to Present

Uvest Financial Services Group; Registered Representative; from 03/2005 to07/2006

Citicorp Investment Services; Financial Executive; from 11/2004 to 03/2005

Southtrust Securities; Registered Representative; from 07/1998 to 11/2004

Liberty Securities Corporation; Registered Representative; from 07/1998 to04/2000

Griffin Financial Services; Investment Officer; from 09/1997 to 07/1998

Designations

Charles Richard Blozinski has earned the following designation(s) and is in goodstanding with the granting authority:

Certified Financial Planner; CFP Board; 2002

Certified Financial Planner (CFP) designation

Initial Certification

To become certified, you are required to meet the following initial certificationrequirements:

Education - To take the CFP® Certification Examination, you will need to beknowledgeable in all of areas covered by the financial planning topic list. There arethree ways to complete the educational requirement: CFP Board-Registered

Programs, Challenge Status or Transcript Review. Candidates for certification musthave a bachelor's degree (or higher), or its equivalent, in any discipline, from anaccredited college or university in order to obtain CFP® certification. The bachelor’sdegree requirement is a condition of initial certification.

Examination - The CFP® Certification Examination assesses your ability to apply yourfinancial planning knowledge, in an integrated format, to financial planning situations.Combined with the education and experience requirements, it assures the public thatyou have met a level of competency appropriate for professional practice.

Experience - Because CFP® certification indicates to the public your ability to providefinancial planning without supervision, CFP Board requires you to have experience inthe financial planning process. Three years of full-time relevant personal financialplanning experience is required.

Ethics - To complete the CFP® Certification you must disclose whether you havebeen a party (or involved) in any criminal, civil, governmental, or self-regulatory agencyproceeding or inquiry. CFP® certification also requires you to agree to adhere to CFPBoard's Code of Ethics and Professional Responsibility, Rules of Conduct andFinancial Planning Practice Standards, and acknowledge CFP Board's right toenforce them through its Disciplinary Rules and Procedures.

Certification Renewal

Once you have been authorized to use the CFP® marks, you must meet CFP Board'srenewal standards to continue to use them. Your CFP® certification must be renewedevery two years. The renewal requirements include 30 hours of CE. The CErequirement includes 28 hours in the accepted financial planning topics and two hoursfrom a pre-approved program on CFP Board's Code of Ethics and ProfessionalResponsibility or Financial Planning Practice Standards.

Item 3 Disciplinary Information Charles Richard Blozinski has no reportable disciplinary history.

Item 4 Other Business ActivitiesA. Investment-Related Activities

1. Charles Richard Blozinski is not engaged in any otherinvestment-related activities.

2. Charles Richard Blozinski does not receive commissions, bonuses orother compensation on the sale of securities or other investment products.

B. Non Investment-Related Activities

Charles Richard Blozinski is not engaged in any other business or occupation that

provides substantial compensation or involves a substantial amount of his time.

Item 5 Additional Compensation Charles Richard Blozinski does not receive any economic benefit from a non-advisoryclient for the provision of advisory services.

Item 6 SupervisionSupervisor: Patricia McVay

Title: Chairman of the Board of Directors

Phone Number: 541-661-1894

Charles Richard Blozinski reports to the board of directors of Wild Rivers FinancialServices LLC on a monthly basis.These report include financial statements as well as activityreports on new clients, departing clients and any other reportable client activities. Allreportting is done on a cumulative activity basis, thereby protecting the privacy andconfidentiality of our individual relationships.

Additionally, the activities of Charles Richard Blozinski are monitored by the ChiefCompliance Officer of the firm on a daily basis.

Item 7 Requirements for State-Registered AdvisersA. Additional Disciplinary History

Charles Richard Blozinski has no reportable disipinary history.

B. Bankruptcy History

Charles Richard Blozinski has not been the subject of a bankruptcypetition.

Part 2B of Form ADV: Brochure Supplement

Thomas George Goodwin17184 S. Passley RoadBrookings, OR 97415

541-469-3138

Integrity Financial Planners

Brookings, OR 97415

03/15/2011

This brochure supplement provides information about Thomas George Goodwinthat supplements the Integrity Financial Planners brochure. You should havereceived a copy of that brochure. Please contact Thomas Goodwin if you didnot receive Integrity Financial Planners' brochure or if you have any questionsabout the contents of this supplement.

Additional information about Thomas George Goodwin is available on theSEC’s website at www.adviserinfo.sec.gov

Item 2 Educational, Background and Business ExperienceFull Legal Name: Thomas George Goodwin Born: 1958

Education

Boston University; MS, Computer Science; 1995

Rensselaer Polytechnic Institute; BS, Computer and Systems Engineering; 1980

Business Experience

Wild Rivers Financial Services LLC d/b/a Integrity Financial Planners; VicePresident and CCO; from 08/2006 to Present

Thomas Goodwin & Associates; Owner; from 01/2003 to 08/2006

MML Investor Services Inc.; Registered Representative/Financial Planner; from05/2002 to 08/2006

Goodwin Financial Group; Owner; from 04/2004 to 08/2006

MassMutual Financial Group; Agent/Financial Advisor; from 05/2002 to 03/2004

Jefferson Pilot Securities Corporation; Registeredd Representative; from 02/1999to 04/2002

Informed Resources, Inc.; Financial Planner; from 04/1999 to 04/2002

Designations

Thomas George Goodwin has earned the following designation(s) and is ingood standing with the granting authority:

Certified Financial Planner; CFP Board; 2005

Enrolled Agent; Internal Revenue Service; 2004

Certified Financial Planner (CFP) designation

Initial Certification

To become certified, you are required to meet the following initial certificationrequirements:

Education - To take the CFP® Certification Examination, you will need to beknowledgeable in all of areas covered by the financial planning topic list. There arethree ways to complete the educational requirement: CFP Board-RegisteredPrograms, Challenge Status or Transcript Review. Candidates for certification musthave a bachelor's degree (or higher), or its equivalent, in any discipline, from anaccredited college or university in order to obtain CFP® certification. The bachelor’sdegree requirement is a condition of initial certification.

Examination - The CFP® Certification Examination assesses your ability to apply yourfinancial planning knowledge, in an integrated format, to financial planning situations.Combined with the education and experience requirements, it assures the public thatyou have met a level of competency appropriate for professional practice.

Experience - Because CFP® certification indicates to the public your ability to providefinancial planning without supervision, CFP Board requires you to have experience inthe financial planning process. Three years of full-time relevant personal financialplanning experience is required.

Ethics - To complete the CFP® Certification you must disclose whether you havebeen a party (or involved) in any criminal, civil, governmental, or self-regulatory agencyproceeding or inquiry. CFP® certification also requires you to agree to adhere to CFPBoard's Code of Ethics and Professional Responsibility, Rules of Conduct andFinancial Planning Practice Standards, and acknowledge CFP Board's right toenforce them through its Disciplinary Rules and Procedures.

Certification Renewal

Once you have been authorized to use the CFP® marks, you must meet CFP Board'srenewal standards to continue to use them. Your CFP® certification must be renewedevery two years. The renewal requirements include 30 hours of CE. The CErequirement includes 28 hours in the accepted financial planning topics and two hoursfrom a pre-approved program on CFP Board's Code of Ethics and ProfessionalResponsibility or Financial Planning Practice Standards.

Enrolled Agent

An Enrolled Agent (or EA) is a tax professional recognized by the United Statesfederal government to represent taxpayers in dealings with the Internal RevenueService (IRS). To become an Enrolled Agent an applicant must pass the SpecialEnrollment Examination or present evidence of qualifying experience as an InternalRevenue Service employee. A background check, including a review of the applicant’stax compliance, is conducted. The IRS also requires Enrolled Agents to complete 72hours of continuing professional education every three years for recertification.

Item 3 Disciplinary Information Thomas George Goodwin has no reportable disciplinary history.

Item 4 Other Business ActivitiesA. Investment-Related Activities

1. Thomas George Goodwin is not engaged in any otherinvestment-related activities.

2. Thomas George Goodwin does not receive commissions, bonuses orother compensation on the sale of securities or other investment products.

B. Non Investment-Related Activities

Thomas George Goodwin is not engaged in any other business or occupationthat provides substantial compensation or involves a substantial amount of histime.

Item 5 Additional Compensation Thomas George Goodwin does not receive any economic benefit from a non-advisoryclient for the provision of advisory services.

Item 6 SupervisionSupervisor: Charles R. Blozinski

Title: President and CEO

Phone Number: 541-469-4080

Charles Richard Blozinski supervises and monitors the actions of Thomas GeorgeGoodwin on a daily basis as outlined in the firm's policies and procedures manual.

Item 7 Requirements for State-Registered AdvisersA. Additional Disciplinary History

Thomas George Goodwin has no reportable disciplinary history.

B. Bankruptcy History

Thomas George Goodwin has not been the subject of a bankruptcypetition.