PA Interfaith Power and Light

26

PLASTICS A TO Z FORUM FRACKING, CRACKING AND PLASTICS ECONOMICS, ALTERNATIVES AND SOLUTIONS PA Interfaith Power and Light July 19, 2021 Patricia M. DeMarco, Ph.D.

Transcript of PA Interfaith Power and Light

P L A S T I C S A T O Z F O R U MF R A C K I N G , C R A C K I N G

A N D P L A S T I C SE C O N O M I C S ,

A LT E R N AT I V E S A N D S O L U T I O N S

PA Interfaith Power and LightJuly 19, 2021

Patricia M. DeMarco, Ph.D.

THE MORAL IMPERATIVE

• Today we use plastic- a material designed to last forever - for products designed to be used for minutes

• “The future of all life now depends on us.”

• David Attenboro-Blue Planet II

2

Dan Clark/Planet PIX/ZUMA

PLASTIC EVERYTHING -

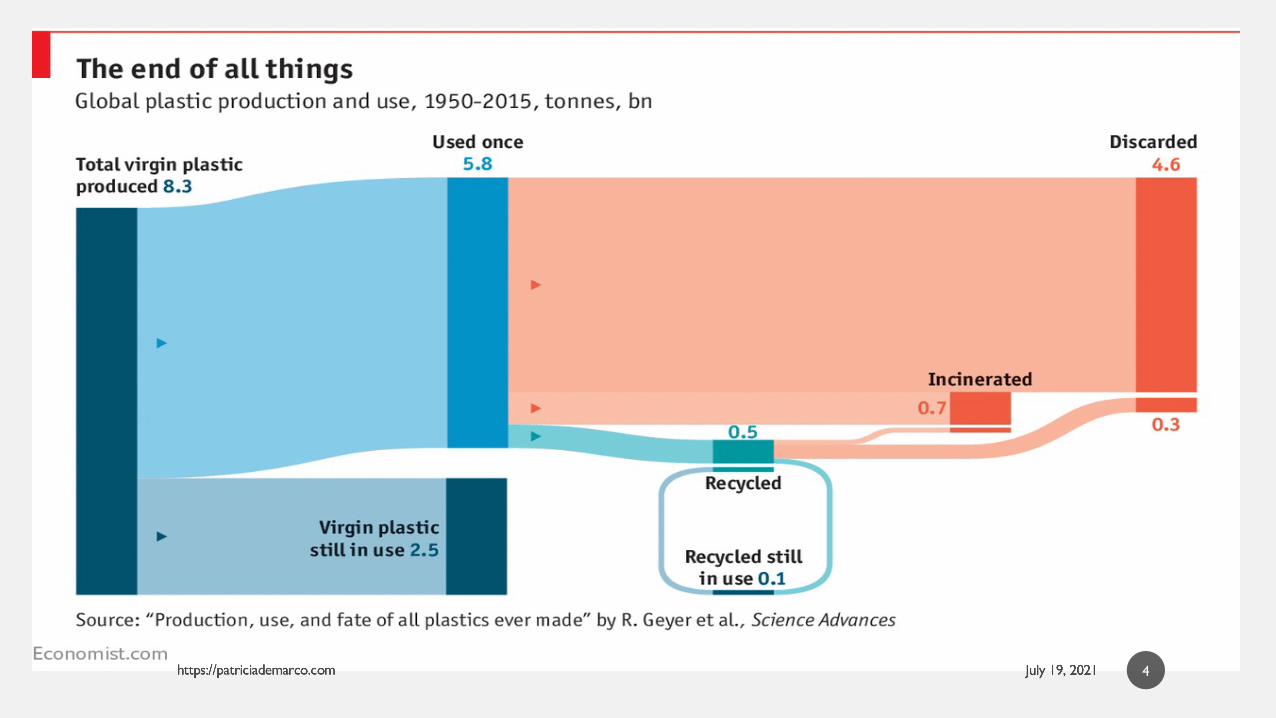

• Americans discard 33.6 million tons of plastic a year

• Only 6.5% of plastic is recycled

• And 7.7% is burned in trash to energy facilities

• China no longer accepting material with more than 1% contamination for recycling

• So, most of plastic waste is now destined for landfill

https://patriciademarco.com July 19, 2021 3

4

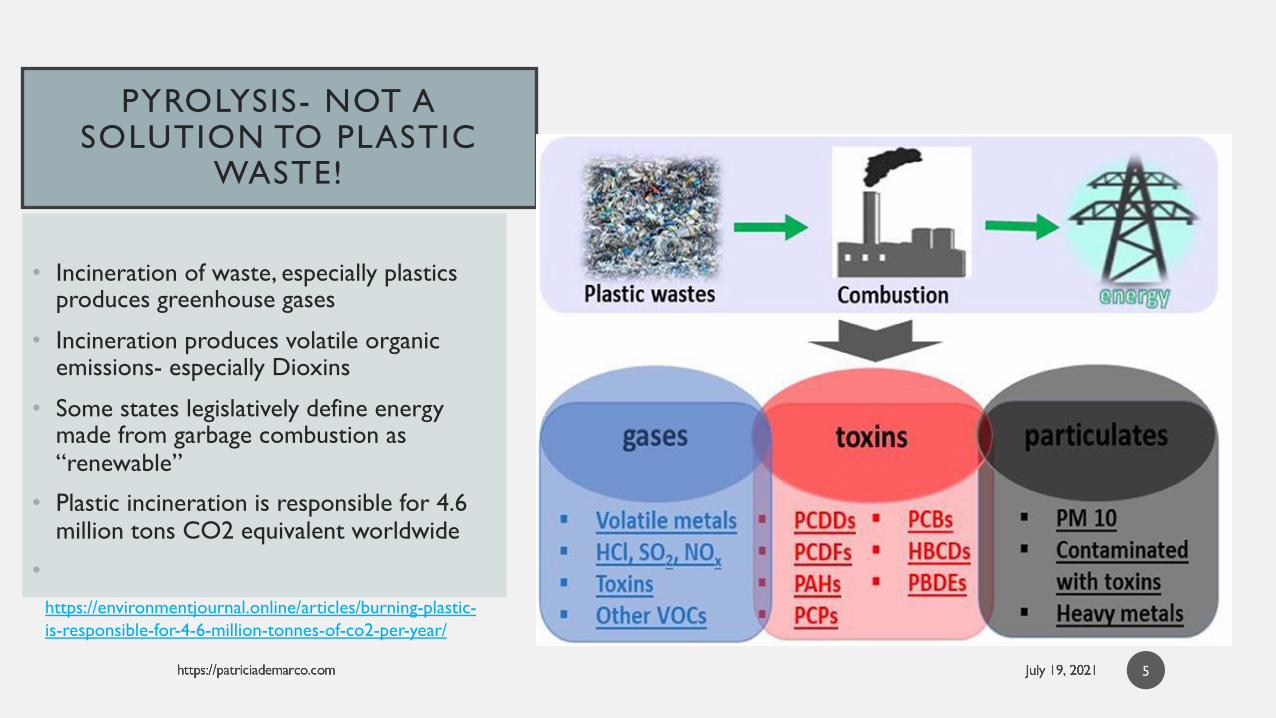

PYROLYSIS- NOT A SOLUTION TO PLASTIC

WASTE!

• Incineration of waste, especially plastics produces greenhouse gases

• Incineration produces volatile organic emissions- especially Dioxins

• Some states legislatively define energy made from garbage combustion as “renewable”

• Plastic incineration is responsible for 4.6 million tons CO2 equivalent worldwide

•

5

https://environmentjournal.online/articles/burning-plastic-is-responsible-for-4-6-million-tonnes-of-co2-per-year/

GREENHOUSE GAS EMISSIONS FROM

LANDFILL

6

https://ensia.com/features/methane-landfills/ https://www.epa.gov/lmop/basic-information-about-landfill-gas

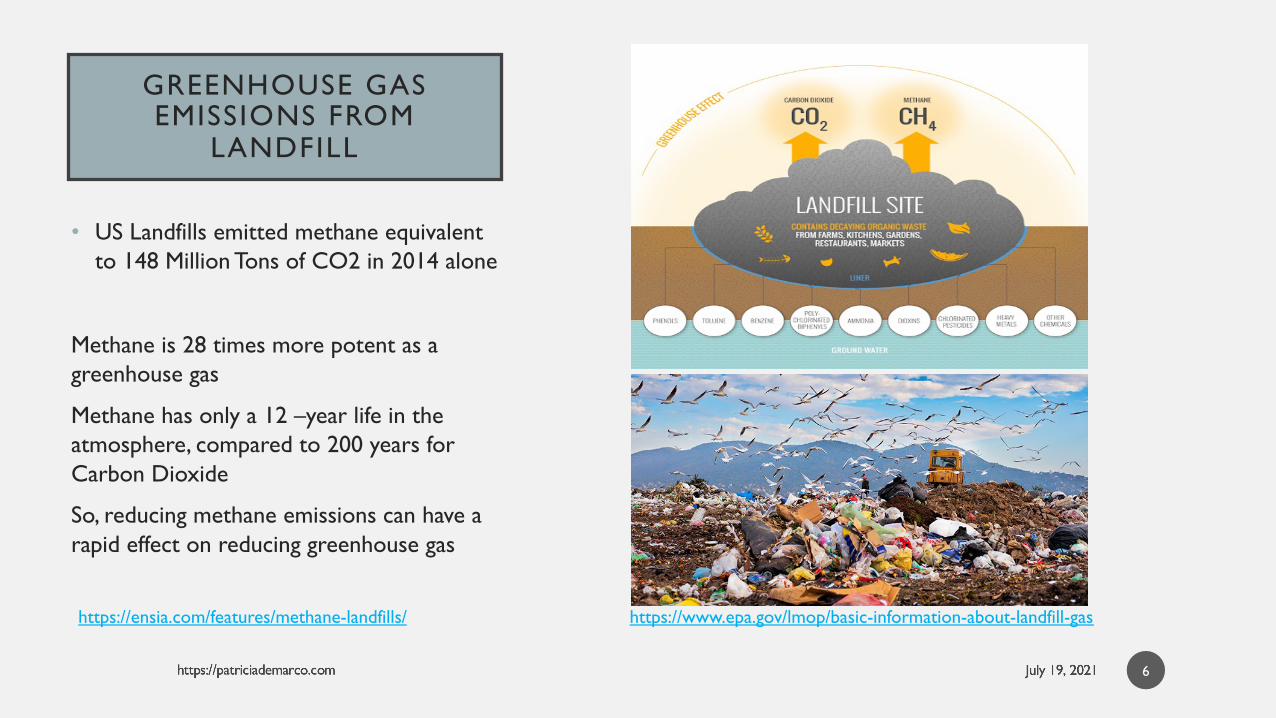

• US Landfills emitted methane equivalent to 148 Million Tons of CO2 in 2014 alone

Methane is 28 times more potent as a greenhouse gas

Methane has only a 12 –year life in the atmosphere, compared to 200 years for Carbon Dioxide

So, reducing methane emissions can have a rapid effect on reducing greenhouse gas

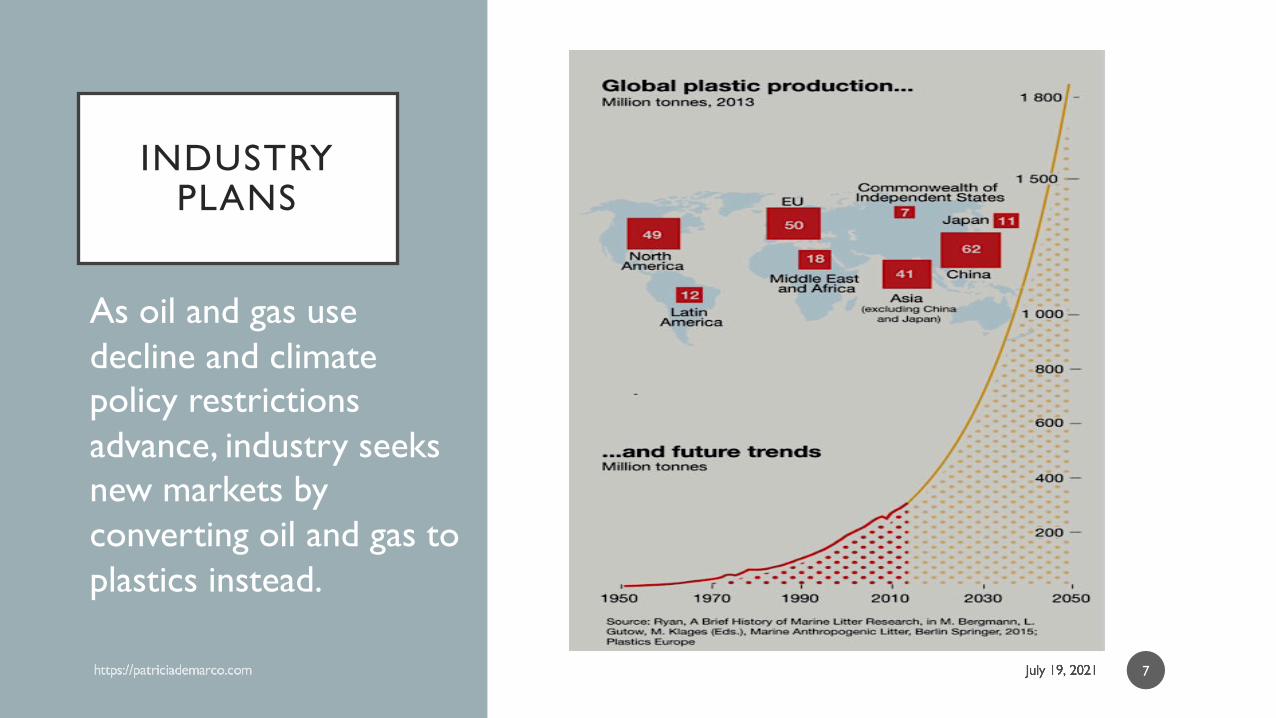

INDUSTRY PLANS

As oil and gas use decline and climate policy restrictions advance, industry seeks new markets by converting oil and gas to plastics instead.

7

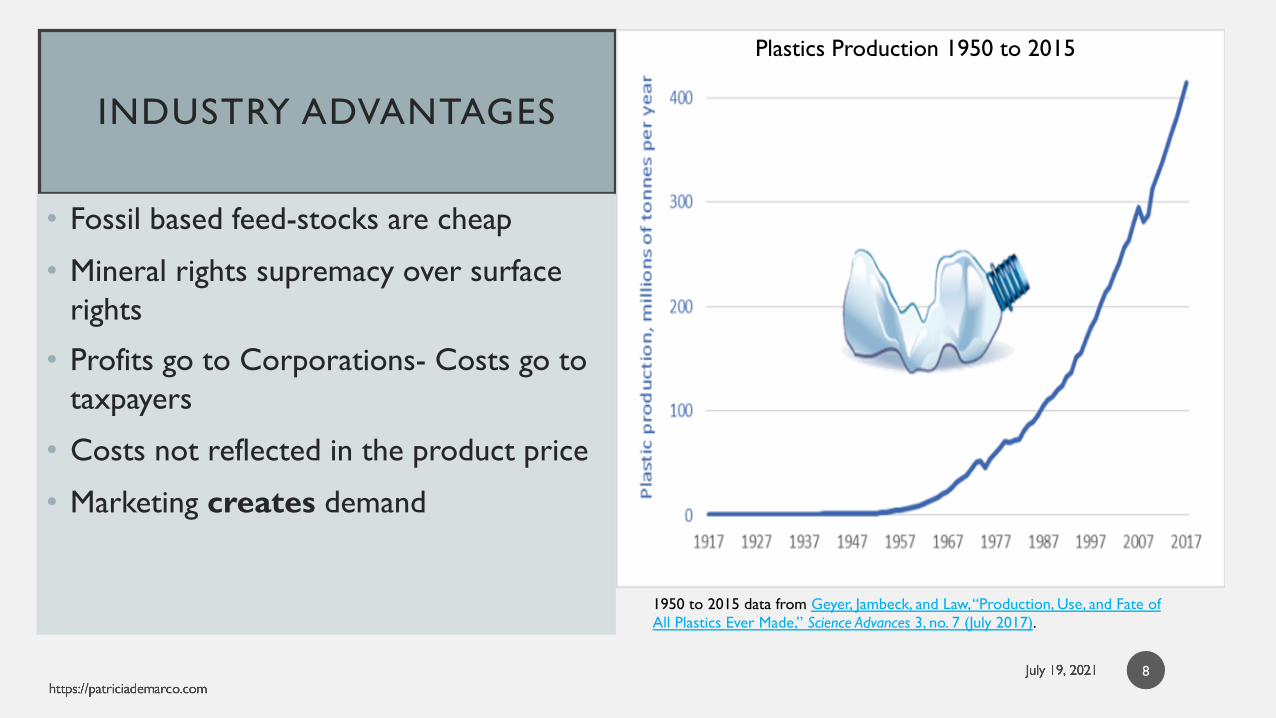

INDUSTRY ADVANTAGES

• Fossil based feed-stocks are cheap

• Mineral rights supremacy over surface rights

• Profits go to Corporations- Costs go to taxpayers

• Costs not reflected in the product price

• Marketing creates demand

1950 to 2015 data from Geyer, Jambeck, and Law, “Production, Use, and Fate of All Plastics Ever Made,” Science Advances 3, no. 7 (July 2017).

Plastics Production 1950 to 2015

8

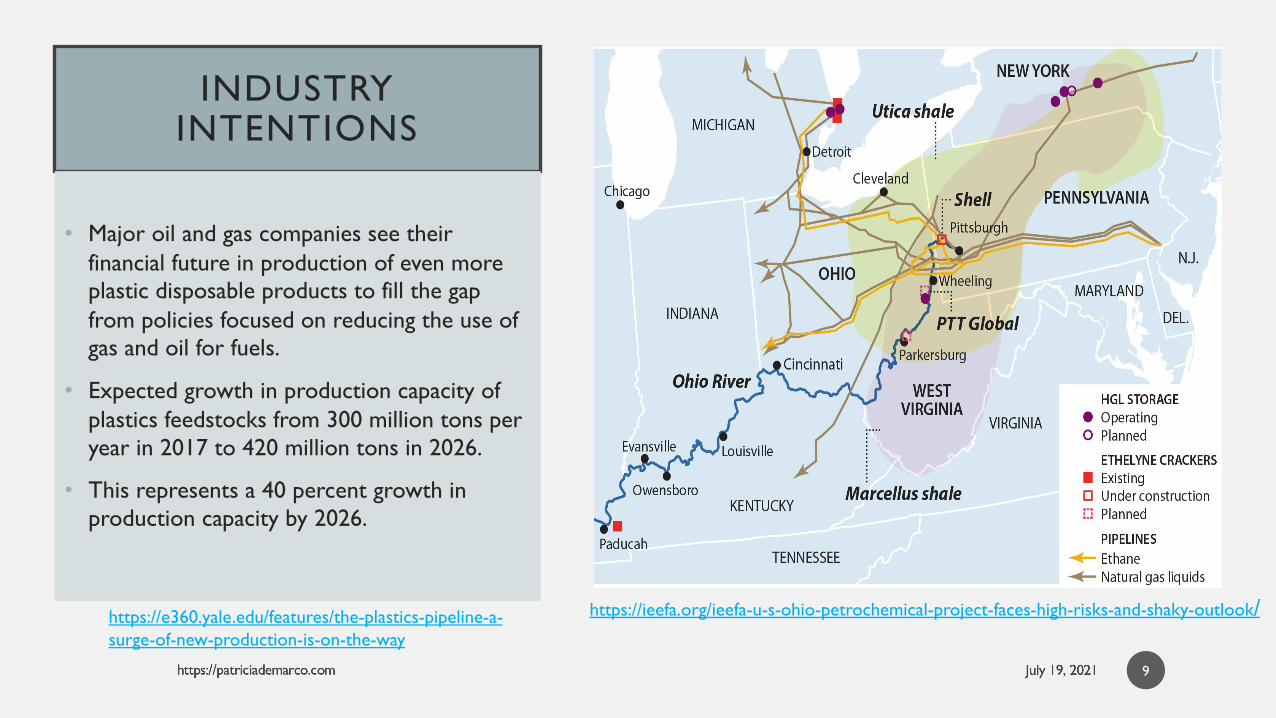

INDUSTRY INTENTIONS

• Major oil and gas companies see their financial future in production of even more plastic disposable products to fill the gap from policies focused on reducing the use of gas and oil for fuels.

• Expected growth in production capacity of plastics feedstocks from 300 million tons per year in 2017 to 420 million tons in 2026.

• This represents a 40 percent growth in production capacity by 2026.

https://e360.yale.edu/features/the-plastics-pipeline-a-surge-of-new-production-is-on-the-way

https://ieefa.org/ieefa-u-s-ohio-petrochemical-project-faces-high-risks-and-shaky-outlook/

9

INDUSTRY INTENTIONS

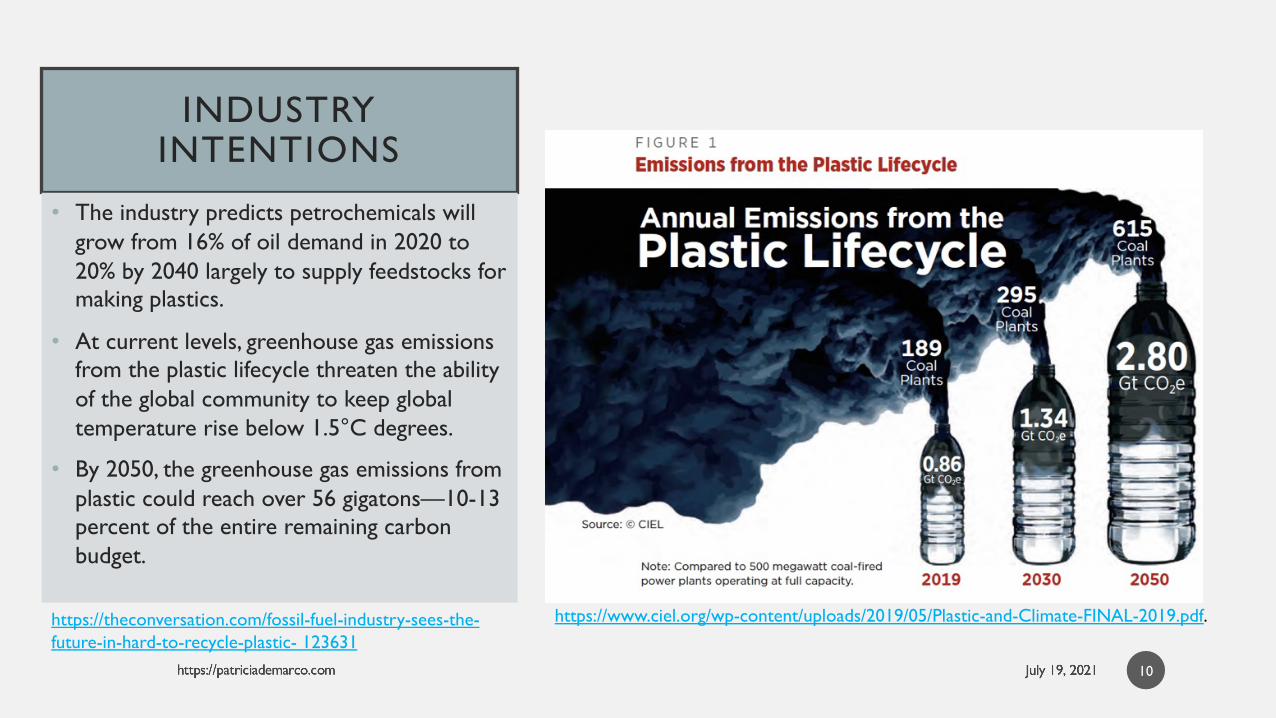

• The industry predicts petrochemicals will grow from 16% of oil demand in 2020 to 20% by 2040 largely to supply feedstocks for making plastics.

• At current levels, greenhouse gas emissionsfrom the plastic lifecycle threaten the ability of the global community to keep global temperature rise below 1.5°C degrees.

• By 2050, the greenhouse gas emissions from plastic could reach over 56 gigatons—10-13 percent of the entire remaining carbon budget.

https://theconversation.com/fossil-fuel-industry-sees-the-future-in-hard-to-recycle-plastic- 123631

https://www.ciel.org/wp-content/uploads/2019/05/Plastic-and-Climate-FINAL-2019.pdf.

10

ECONOMIC REALITY

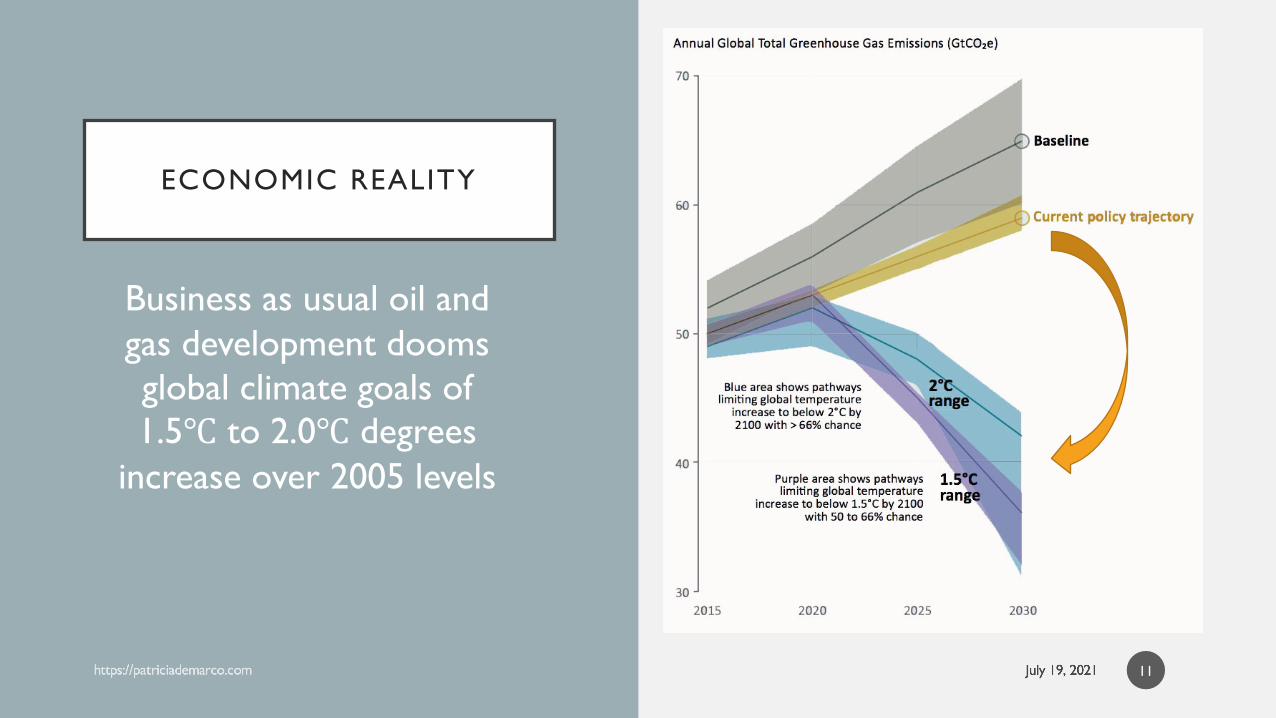

Business as usual oil and gas development dooms global climate goals of 1.5℃ to 2.0℃ degrees

increase over 2005 levels

11

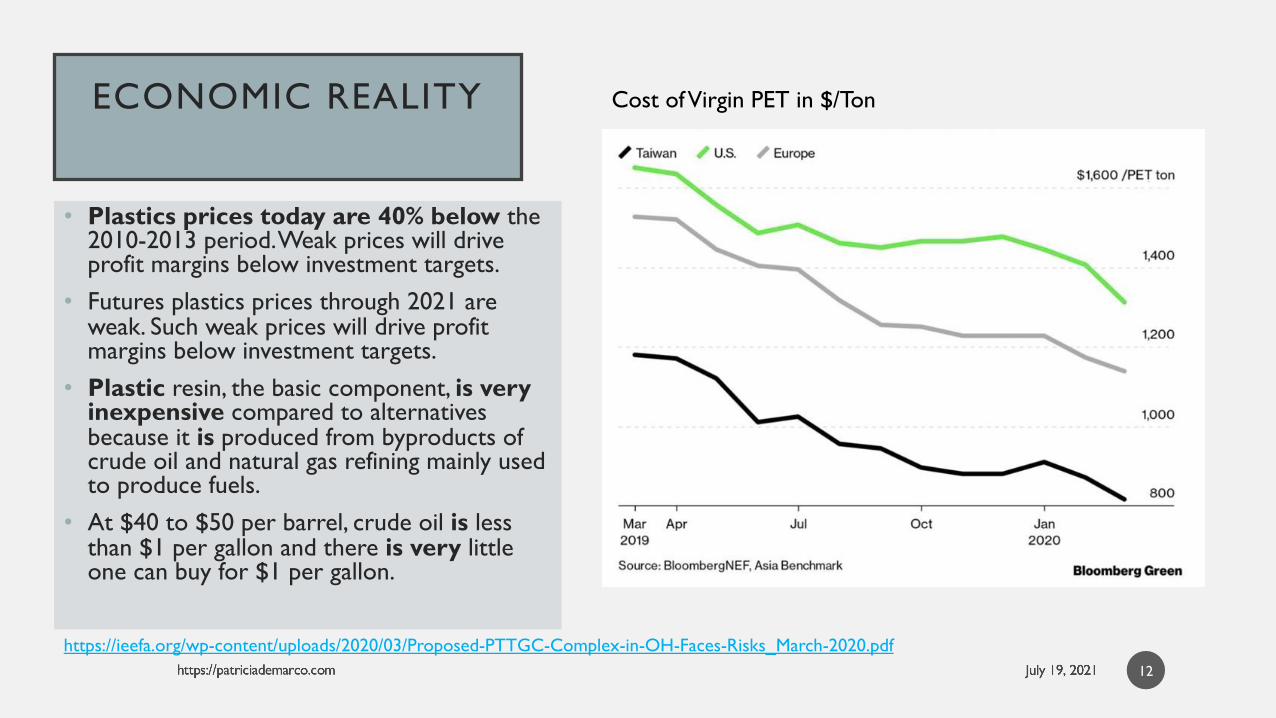

ECONOMIC REALITY

• Plastics prices today are 40% below the 2010-2013 period. Weak prices will drive profit margins below investment targets.

• Futures plastics prices through 2021 are weak. Such weak prices will drive profit margins below investment targets.

• Plastic resin, the basic component, is very inexpensive compared to alternatives because it is produced from byproducts of crude oil and natural gas refining mainly used to produce fuels.

• At $40 to $50 per barrel, crude oil is less than $1 per gallon and there is very little one can buy for $1 per gallon.

https://ieefa.org/wp-content/uploads/2020/03/Proposed-PTTGC-Complex-in-OH-Faces-Risks_March-2020.pdf

Cost of Virgin PET in $/Ton

12

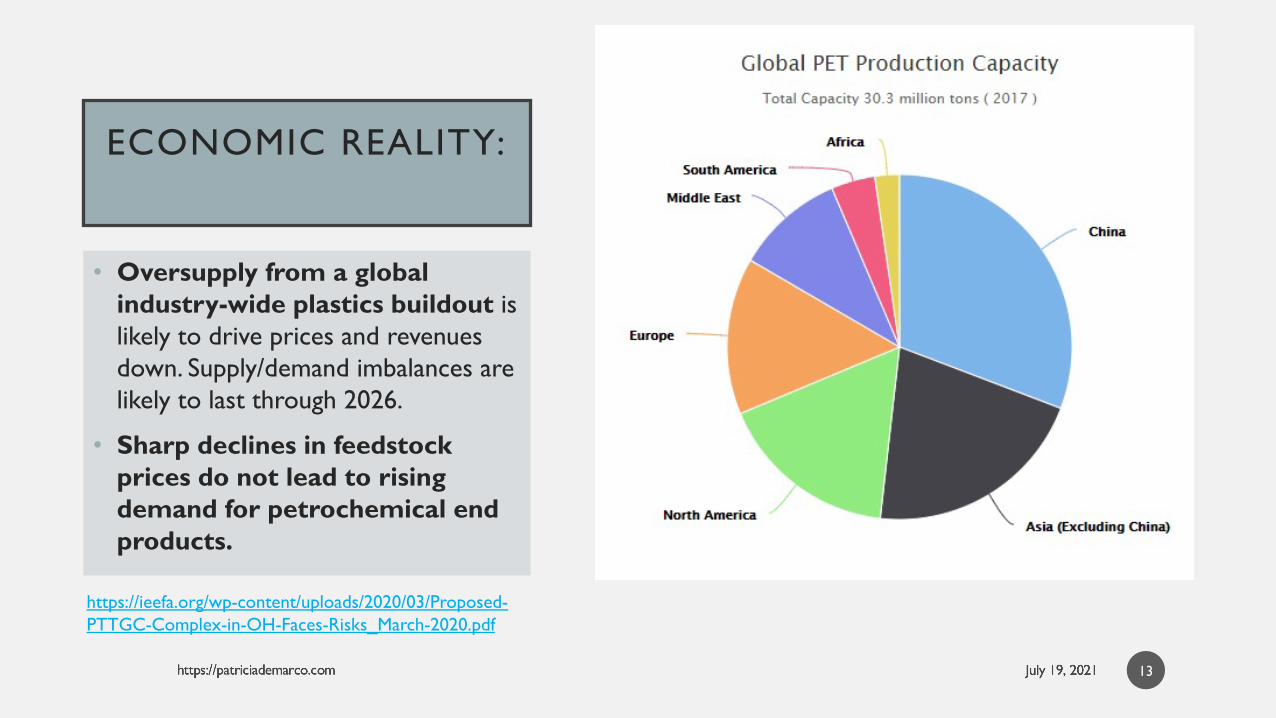

ECONOMIC REALITY:

• Oversupply from a global industry-wide plastics buildout is likely to drive prices and revenues down. Supply/demand imbalances are likely to last through 2026.

• Sharp declines in feedstock prices do not lead to rising demand for petrochemical end products.

https://ieefa.org/wp-content/uploads/2020/03/Proposed-PTTGC-Complex-in-OH-Faces-Risks_March-2020.pdf

13

ECONOMIC REALITY:OHIO CASE STUDY

• PTTGC faces stiff competition from major companies – ExxonMobil, Dow Chemical, Chevron ‒ that have existing relationships in the U.S. market.

• Any new project will face vigorous and perhaps devastating competition from existing domestic and global petrochemical operations.

https://ieefa.org/wp-content/uploads/2020/03/Proposed-PTTGC-Complex-in-OH-Faces-Risks_March-2020.pdf

PTTGC Petrochemical Complex: Unacceptable Risk for Investors and Ohio

14

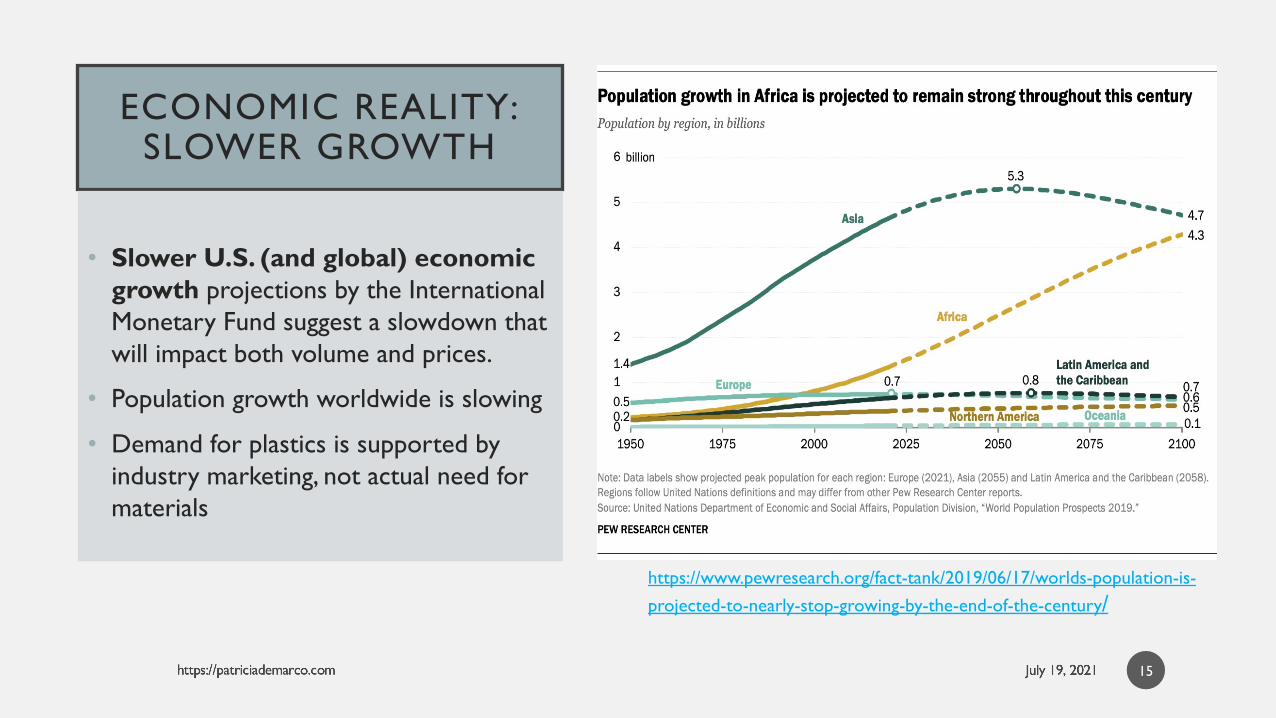

ECONOMIC REALITY:SLOWER GROWTH

• Slower U.S. (and global) economic growth projections by the International Monetary Fund suggest a slowdown that will impact both volume and prices.

• Population growth worldwide is slowing

• Demand for plastics is supported by industry marketing, not actual need for materials

https://www.pewresearch.org/fact-tank/2019/06/17/worlds-population-is-projected-to-nearly-stop-growing-by-the-end-of-the-century/

15

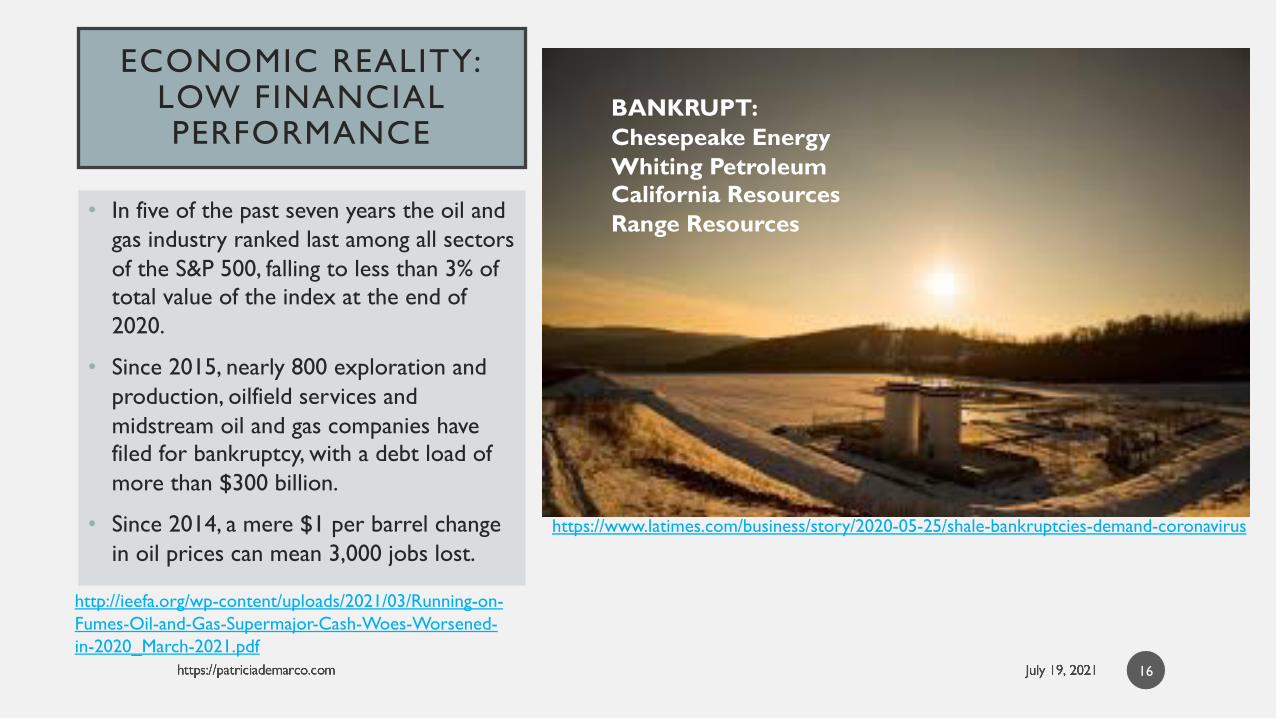

ECONOMIC REALITY:LOW FINANCIAL PERFORMANCE

• In five of the past seven years the oil and gas industry ranked last among all sectors of the S&P 500, falling to less than 3% of total value of the index at the end of 2020.

• Since 2015, nearly 800 exploration and production, oilfield services and midstream oil and gas companies have filed for bankruptcy, with a debt load of more than $300 billion.

• Since 2014, a mere $1 per barrel change in oil prices can mean 3,000 jobs lost.

https://www.latimes.com/business/story/2020-05-25/shale-bankruptcies-demand-coronavirus

BANKRUPT:Chesepeake EnergyWhiting PetroleumCalifornia ResourcesRange Resources

http://ieefa.org/wp-content/uploads/2021/03/Running-on-Fumes-Oil-and-Gas-Supermajor-Cash-Woes-Worsened-in-2020_March-2021.pdf

16

ECONOMIC REALITY:REGULATORY UNCERTAINTY• Uncertainty over federal government

policies add to the risk

• Investors are increasingly concerned with the financial risks from climate change - demanding climate action

• Half of fuel burned to generate heat for industrial processes, where natural gas, coal and oil are used, can be replaced with electrification.

• Competitive performance for wind, solar, battery and fuel cell technologies encourages regulatory support

https://ieefa.org/wp-content/uploads/2020/03/Proposed-PTTGC-Complex-in-OH-Faces-Risks_March-2020.pdf

Inflated balloons are seen during a Global Climate Strike, part of the “Fridays for Future” movement, in Cologne, Germany, November 29, 2019.

17

REUTERS/Thilo Schmuelgen

SOLUTIONS

• Public pressure for effective policy changes must continue and become even more urgent.

• Manufacturers must be held accountable for both production and disposal of plastic materials.

18

https://issuu.com/greenallianceuk/docs/returntosenderfull

Greenpeace activists stage a plastic spill at bottling plant in Austria asking coke to switch to reusable bottles instead of single-use. Banner says “Stop the plastic flood”

SOLUTIONS:END SINGLE-USE PLASTICS

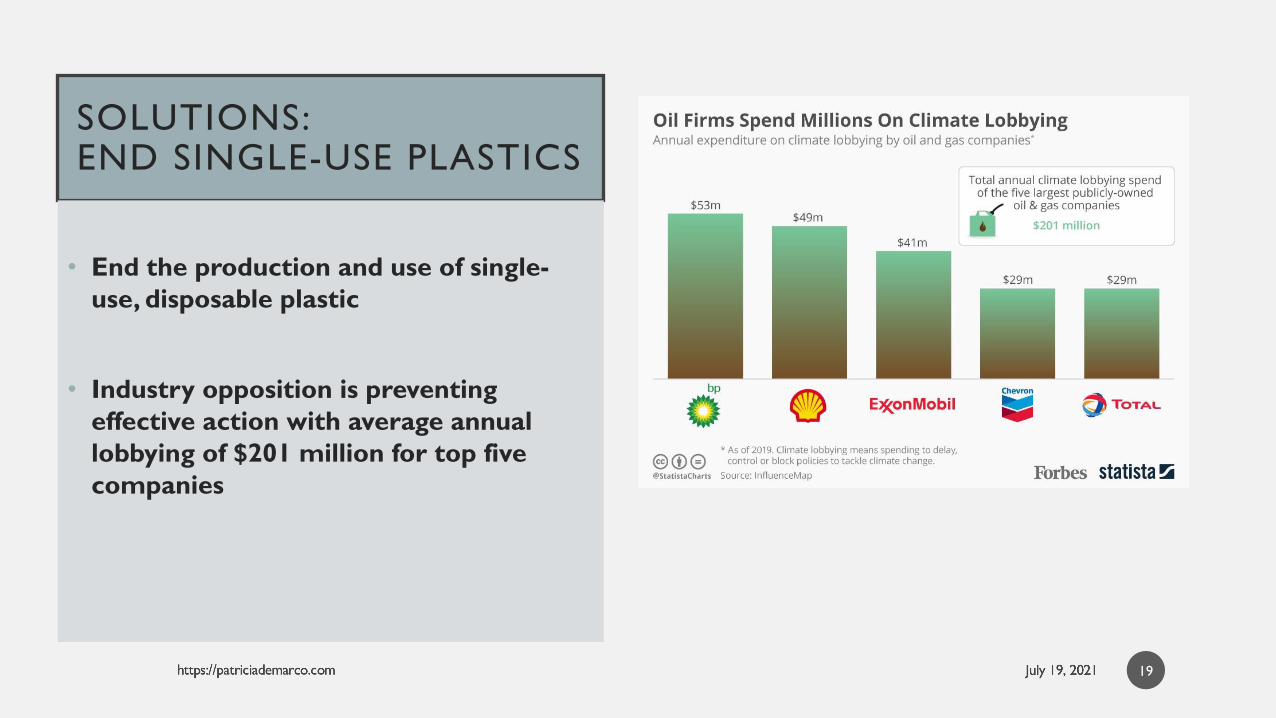

• End the production and use of single-use, disposable plastic

• Industry opposition is preventing effective action with average annual lobbying of $201 million for top five companies

19

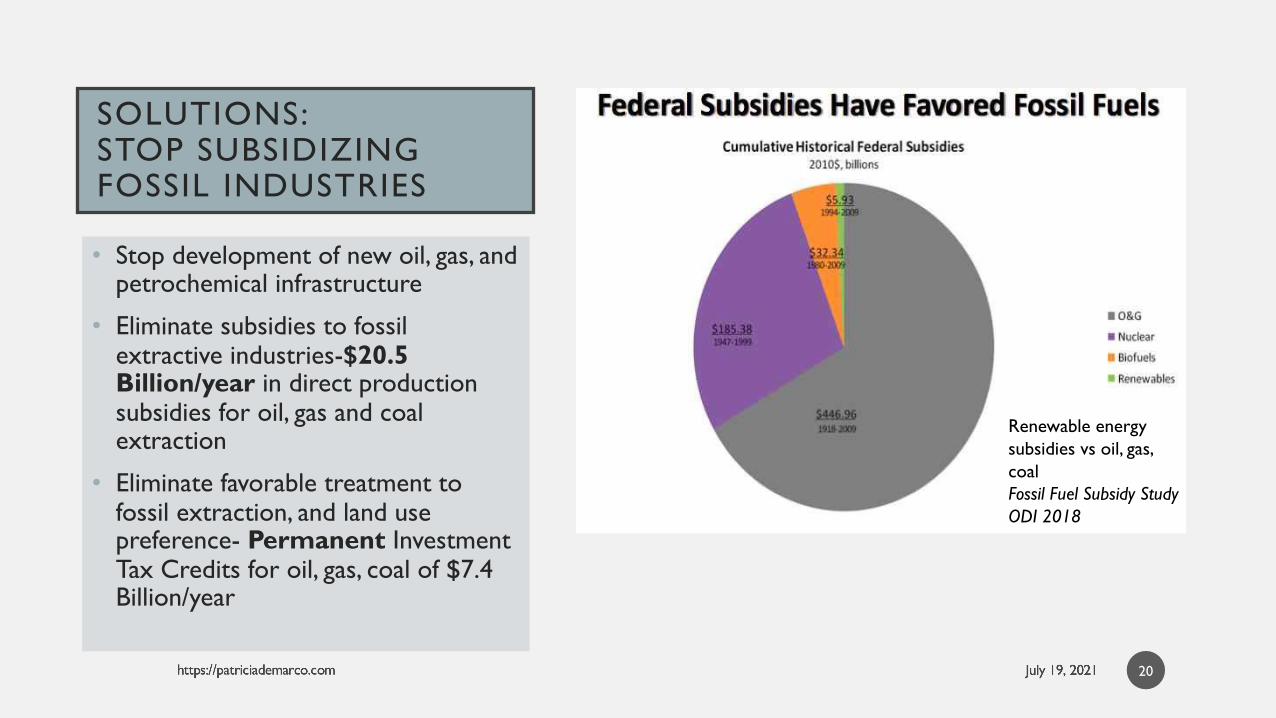

SOLUTIONS:STOP SUBSIDIZING FOSSIL INDUSTRIES

• Stop development of new oil, gas, and petrochemical infrastructure

• Eliminate subsidies to fossil extractive industries-$20.5 Billion/year in direct production subsidies for oil, gas and coal extraction

• Eliminate favorable treatment to fossil extraction, and land use preference- Permanent Investment Tax Credits for oil, gas, coal of $7.4 Billion/year

Renewable energy subsidies vs oil, gas, coalFossil Fuel Subsidy Study ODI 2018

20

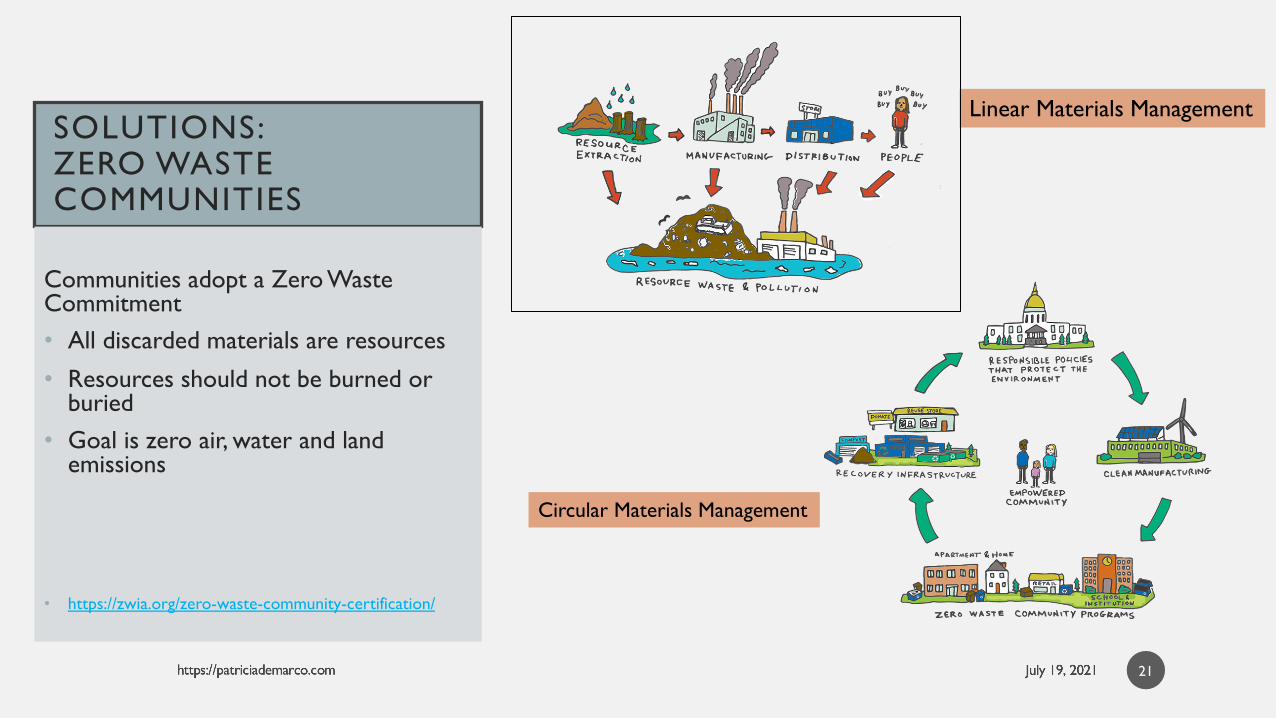

SOLUTIONS:ZERO WASTE COMMUNITIES

Communities adopt a Zero Waste Commitment • All discarded materials are resources

• Resources should not be burned or buried

• Goal is zero air, water and land emissions

• https://zwia.org/zero-waste-community-certification/

Linear Materials Management

Circular Materials Management

21

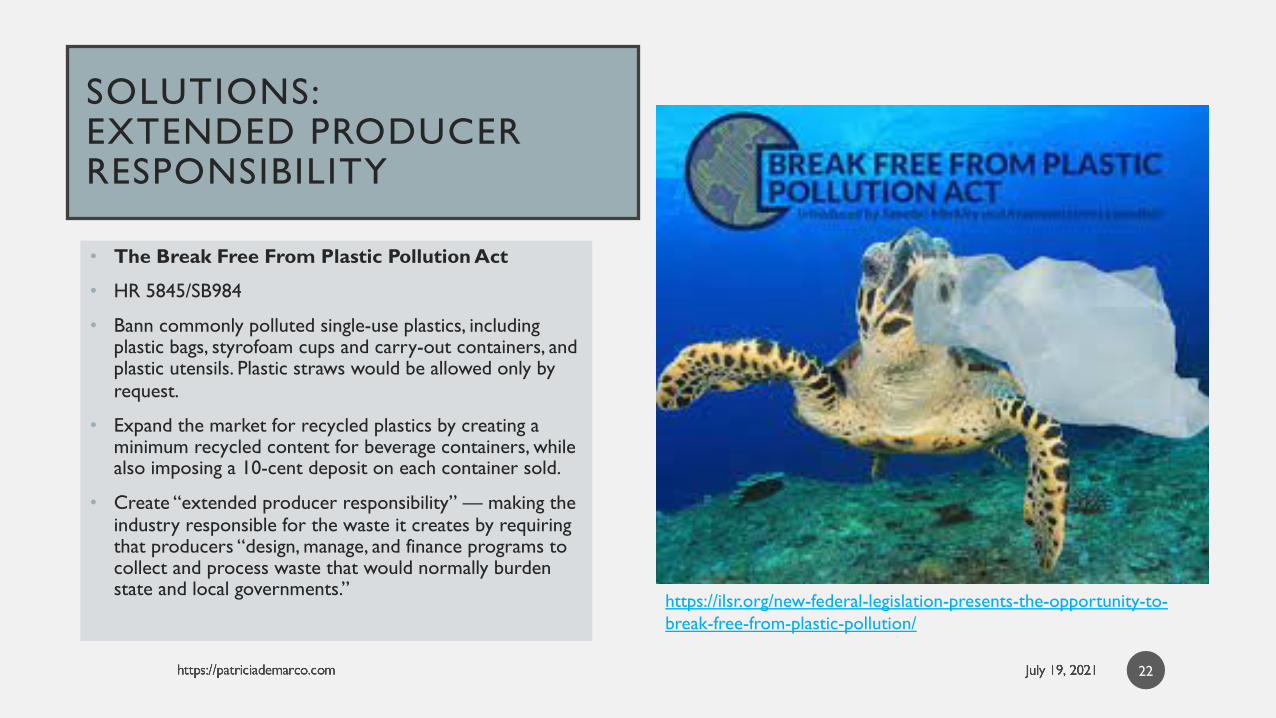

SOLUTIONS:EXTENDED PRODUCER RESPONSIBILITY

• The Break Free From Plastic Pollution Act

• HR 5845/SB984

• Bann commonly polluted single-use plastics, including plastic bags, styrofoam cups and carry-out containers, and plastic utensils. Plastic straws would be allowed only by request.

• Expand the market for recycled plastics by creating a minimum recycled content for beverage containers, while also imposing a 10-cent deposit on each container sold.

• Create “extended producer responsibility” — making the industry responsible for the waste it creates by requiring that producers “design, manage, and finance programs to collect and process waste that would normally burden state and local governments.”

https://ilsr.org/new-federal-legislation-presents-the-opportunity-to-break-free-from-plastic-pollution/

22

SOLUTIONS:CONNECT ALL FOSSIL INDUSTRYTO CLIMATE

• Adopt and Enforce ambitious targets to reduce greenhouse gas emissions from all sectors, including plastic production

• Nothing short of stopping the expansion of petrochemical and plastic production and keeping fossil fuels in the ground will create the surest and most effective reductions in the climate impacts from the plastic lifecycle.

https://greenbuildingelements.com/2012/10/18/zero-waste-systems/

23

BE AN EMPOWERED CONSUMER

USE your $$• Refuse-single-use items

• Reduce- Buy in bulk, substitute recyclable and non-toxic materials for non-recyclable

• Reuse- select refillable products; buy recycled materials-replace single-use items with reusable items-exchange toys, clothing, household décor

• Recycle- know the rules in your area and separate clean items

• Rot- compost food waste and organic material

USE your VOICE!• Advocate for policy changes at local, state and federal

level

24

https://www.learnz.org.nz/redvale181/bg-standard-f/the-5-r%27s-of-waste-management

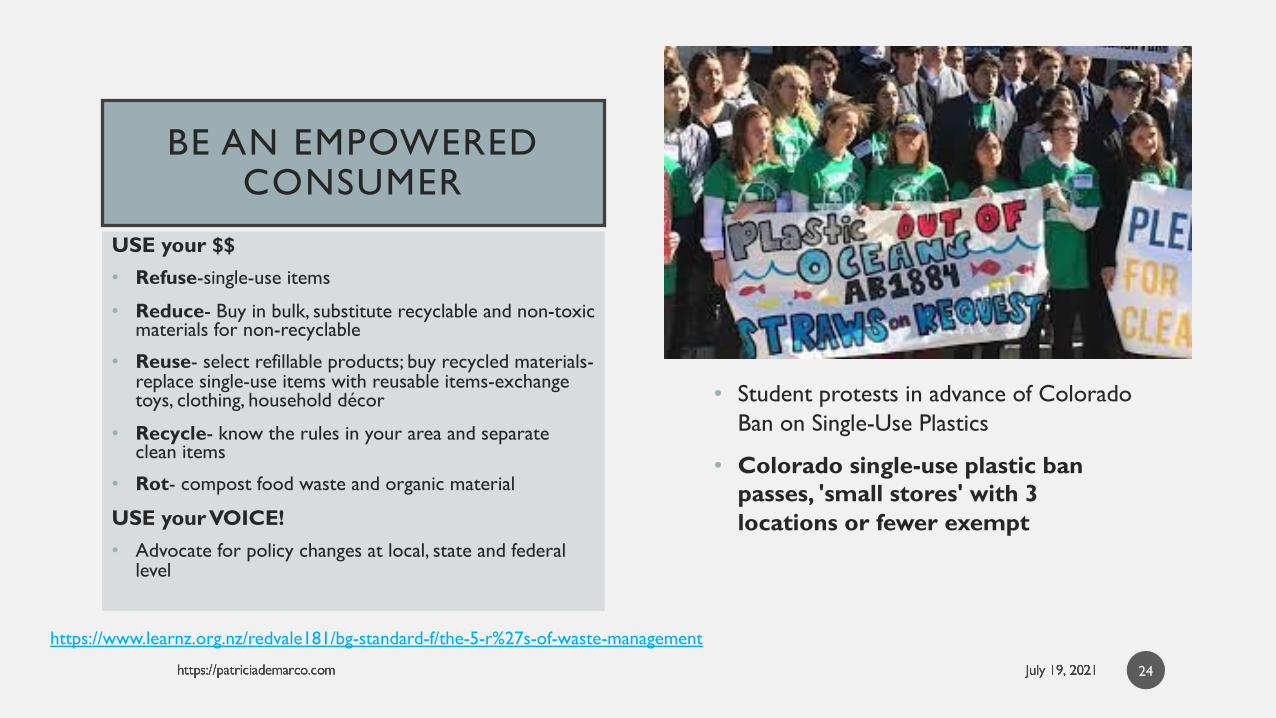

• Student protests in advance of Colorado Ban on Single-Use Plastics

• Colorado single-use plastic ban passes, 'small stores' with 3 locations or fewer exempt

THE MORAL IMPERATIVE:

THE LAWS OF NATURE ARE NOT NEGOTIABLE!

• Freedom without responsibility yields chaos. Hold manufacturers accountable for waste.

• Refuse…Reduce…Reus…Recycle…Rot (compost)

• “The road we have long been traveling is deceptively easy, a smooth superhighway on which we progress at great speed, but at its end lies disaster.” Rachel Carson –Silent Spring

25

THANK YOU!

• For more information visit my web site

• https://patriciademarco.com

• See my blog post: “Mending the Interconnected Web of Life- Endocrine Disruption and Global Plastic Pollution”

• https://patriciademarco.files.wordpress.com/2021/07/mending-the-interconnected-web-of-life-a-call-for-regulating-endocrine-disrupting-chemicals-2.pdf

26

Patricia M. DeMarco, Ph.D.Live in harmony with Nature!