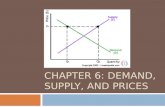

On the left side of the diagram we see the standard market. Equilibrium is at the point where the...

22

-

date post

21-Dec-2015 -

Category

Documents

-

view

216 -

download

1

Transcript of On the left side of the diagram we see the standard market. Equilibrium is at the point where the...

• On the left side of the diagram we see the standard market.

• Equilibrium is at the point where the quantity demanded is the same as the quantity supplied. Nothing new here!

$

0

$

0X q

d, p, mr

D

S

• On the right side we have the picture of just one firm of a great number of firms. It can be representative of all the others, since all are price takers: they simply accept the market price.

$

0

$

0X q

d, p, mrMC AC

Pure CompetitionPure Competition

• Note that in economics, costs include normal opportunity cost returns (e.g., market salaries and stock investments) for all factors of production.

• When all costs are covered, the firm is making a normal profit.

• A “pure” or “economic” profit is large enough to allow greater than market returns to factors or provide for net investment in the firm.

Characteristics of Pure Comp: Many firms, A homogenous product, and No barriers to exit and entrance. Entry is the automatic response to the profit incentive.

$

0

$

0X q

d, p, mr

Results? Efficiency. Easy market access (entry) denies long-term pure profit. D temporary NR entry S and price adjustment efficiency, since P=AC

$

0

$

0X q

d, p, mr

• The monopolist (compare to pure competition) is the only seller facing the industry-wide demand curve.

•The monopolist can often make profit by restricting output and raising the price. (Sliding to the left, back up the demand curve.)

0 Q

$

D=armr

acmc

• Here we see the monopolist maximizing profit by equating MC and MR.

•MC is the cost of selling 1 more unit. MR is the revenue from selling 1 more unit.

•We can gain no more revenue than by equating MC and MR. This can be seen by….

•How to maximize profits. Select the output and price that make TR as much greater than TC as possible.

Q* Q

TC

TR

NR

Note where TC and TR diverge, and, after Q*, converge. They are furthest apart at Q*.

Note the slopes ofTC and TR. They are MC and MR, and areequal at Q*.

$

• Oligopolies have a small number of firms (2 to 5 perhaps)

• “Few Sellers”

• Interdependence -- The battle for market share leads to uncertainty.

-- If an oligopolist tries to increase market share, what will be the competitors’ response? Price wars and non-price competition (through product differentiation).

•Many models are used to reflect the oligopoly situation, since there are many reactions to uncertainty.

0 Q

$

mr

mc

0 Q

$

Cartel TR Max with Π constraint

Min

• The many models of oligopoly, reflect differing reactions to uncertainty in different kinds of oligopoly industries.

•Where oligopolists collude to flee uncertainty and to secure greater profits, cartels may be formed.

0 Q

$

mr

mc

0 Q

$

Cartel TR Max with Π constrant

Min

•Otherwise, firms tend to avoid price wars and compete through product differentiation.

0 Q

$

acmc

• Several firms (10 to 20 perhaps): enough so no interdependence.

• Great importance of many retail items (even where production is on oligopoly basis) and for service firms.

0 Q

$

acmc

• Differentiation and product groups.

• Entry pushes D downward until AC just rests on the demand curve.

• Long-run profit can exist only if entry is blocked. This can be done through licensing.

•Notice that additional firms joining the product group (entry) will lead to a shifting of the demand curve downward or to the right. This works just as it does in pure competition.

With entry, S shifts out and the Firm’s D curve (price line) falls

With entry, S shifts out and the Firm’s D curve (price line) falls

With entry, D also fallshere until costs are just covered.

The competitive environment differs distinctly depending on which of these models holds for a given firm.

As Michael Porter has shown, there are extensive forces of competition confronting nearly all firms as part of their environment. These forces emanate from:

• firms in other industries offering substitute products,

• potential new entrants,

• buyers with monopsony power,

• suppliers of key inputs.