OMMA Display 2011 -- Transformation of the Measurement Industry: How Much Can Be Attributed to M&A

24

Transformation of the Measurement Transformation of the Measurement Industry: How Much Can be Industry: How Much Can be Attributed to M&A? Attributed to M&A? November 7, 2011

-

Upload

linda-gridley -

Category

Business

-

view

601 -

download

1

Transcript of OMMA Display 2011 -- Transformation of the Measurement Industry: How Much Can Be Attributed to M&A

Transformation of the Measurement Transformation of the Measurement

Industry: How Much Can be Industry: How Much Can be

Attributed to M&A?Attributed to M&A?

November 7, 2011

2

Introduction

• Industry leaders today are facing a quickly changing landscape

- Rate of change in industry among the highest in all of digital technology

- Emergence of real time data collection and dissemination drivingtechnology deeper into today’s solutions

• Increasingly tough to compete with new, innovative entrants

- Growing channels and use cases bringing new players to the market

Unprecedented opportunity for new leaders to emerge

3

Snapshot of the Web 10 Years Ago

Social networks limited to forums, blogs, and chatrooms

41% of Americans using mobile phones (voice only)

Users spent seven hours per week online (email, news, chat)

143 million Americans (54%) using the Internet

Source: NTIA Source: Harris Interactive

Source: CTIA

4

Despite its Size, Online Advertising was Quite Underdeveloped

U.S. Online Advertising Revenue

($ in billions)

Source: IAB Internet Advertising Report, BusinessWeek

$7.1

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

2001

• Highly manual processes

• Little to no accurate measurement methodology

“…big advertisers still don't see the value of the Internet yet,"

Morgan Stanley analyst Michael Russell - July ’01

“… experts in the field now say that advertisers ought to forget about click-throughs… Online ads aren't meant only to spawn direct sales.. They're also for establishing or burnishing a brand…”

BusinessWeek – July ‘01

5

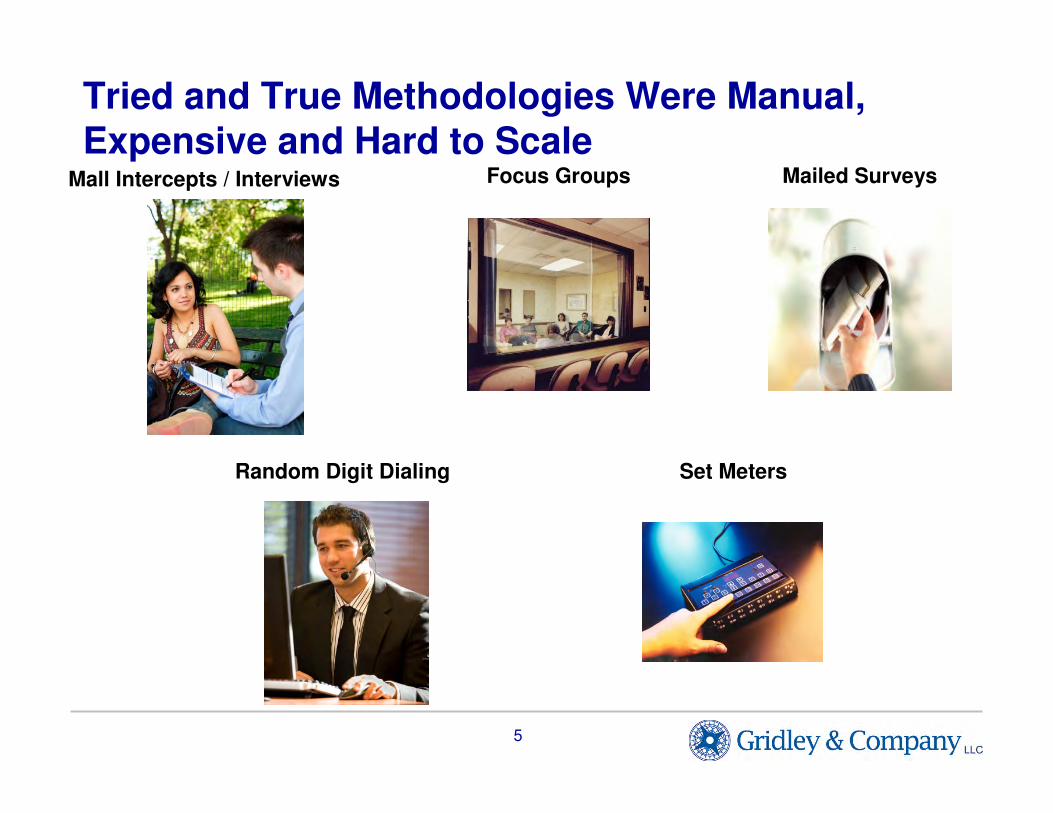

Tried and True Methodologies Were Manual, Expensive and Hard to Scale

Random Digit Dialing

Mall Intercepts / Interviews Focus Groups Mailed Surveys

Set Meters

6

The Web Quickly Developed Scale and Use

43%

79%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2000 2010

Doubling of U.S. Online Penetration

Radio

15%

Other

7%

Magazines

3%

TV | Video

39%

Newspaper

5%

Mobile

8%

Internet

23%

Time Spent on Internet + Mobile Approaching TV

Source: eMarketer

Avg. hrs spent per week ~7hrs ~13hrs

Source: ITU, Harris Interactive, comScore

7

Fundamental Shifts in Usage Are Driving Need for New Measurement Methodologies

~8x growth in U.S. eCommerce

($ in billions)

$25.8

$164.6

$0.0

$20.0

$40.0

$60.0

$80.0

$100.0

$120.0

$140.0

$160.0

$180.0

2000 2010

Source: U.S. Census Bureau

0%

23%

0%

5%

10%

15%

20%

25%

2001 2010

8%

61%

0%

10%

20%

30%

40%

50%

60%

70%

2005 2010

Introduction of the Smartphone

Social NetworkingCreating Information at Scale

Source: comScore Source: Pew Research

8

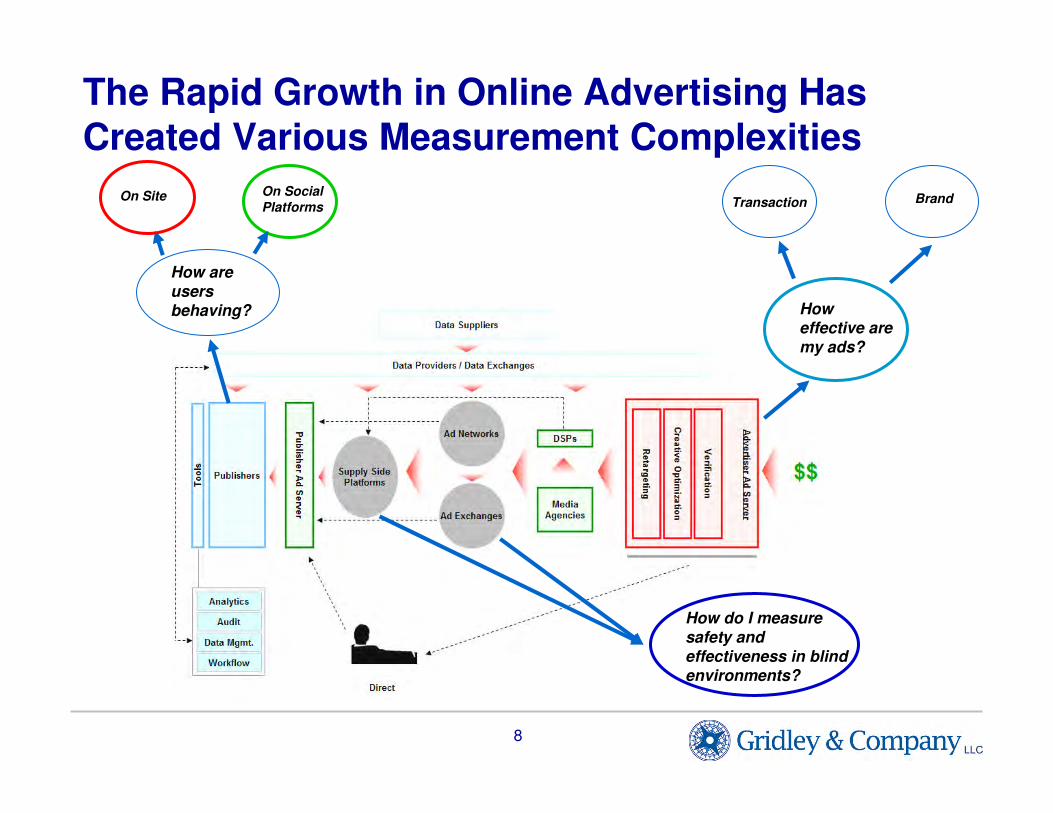

The Rapid Growth in Online Advertising Has Created Various Measurement Complexities

How effective are my ads?

BrandTransaction

How are users behaving?

How do I measure safety and effectiveness in blind environments?

On Site On Social

Platforms

9

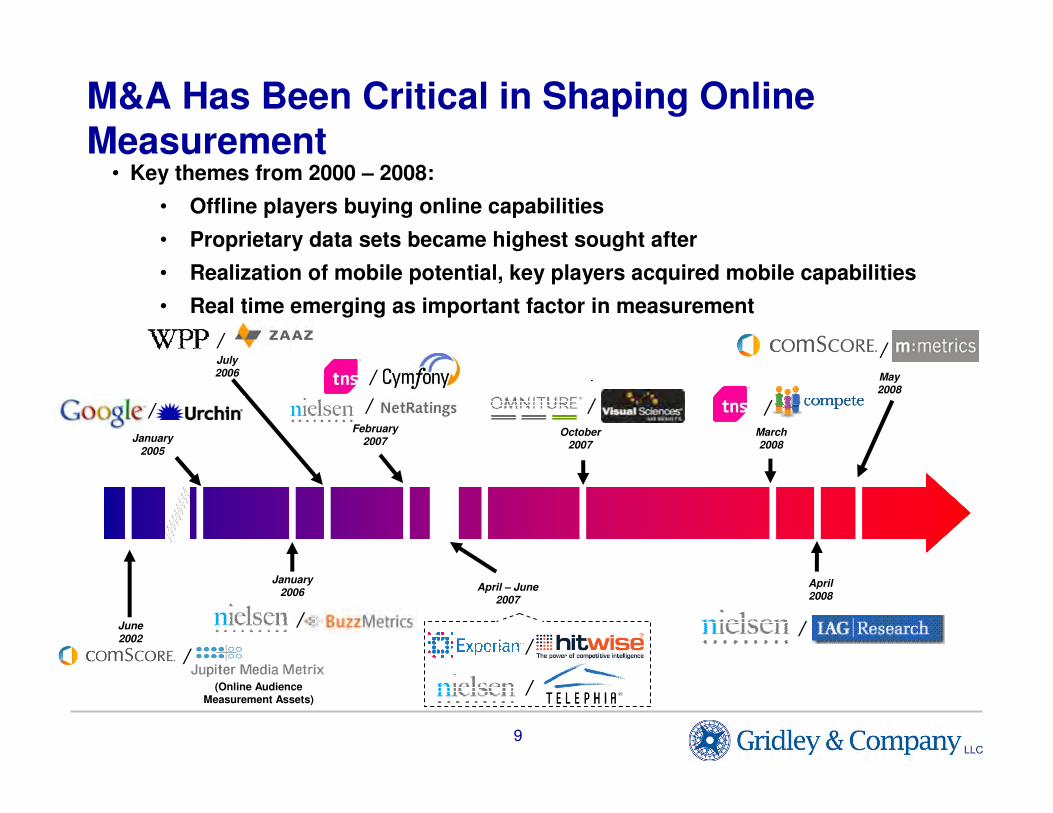

M&A Has Been Critical in Shaping Online Measurement

• Key themes from 2000 – 2008:

• Offline players buying online capabilities

• Proprietary data sets became highest sought after

• Realization of mobile potential, key players acquired mobile capabilities

• Real time emerging as important factor in measurement

January

2005

April – June2007

/

/

/(Online Audience Measurement Assets)

/

/

March2008

/February

2007

April 2008

May 2008

October 2007

/

/

January 2006

/June

2002

/July 2006 /

/

10

January2011

2010

Online advertising

overtakes newspapers in U.S. (source: eMarketer)

September

2009

/

June2010

/

July

2008Nielsen releases its

first quarterly “Three Screen Report”,

covering TV, Internet, and mobile

October2009

February 2010

September2010

February2011

April2011

March 2011

August2011

September

2011

/

/

/

/

/

/

/

/

/

• Key themes from 2009 – today:

• New entrants to the market with use cases beyond research – Adobe, IBM, Salesforce

• Measurement in real time environments – Social, RTB

• Measurement -> Data Analytics

M&A Has Been Critical in Shaping Online Measurement (cont’d)

/

11

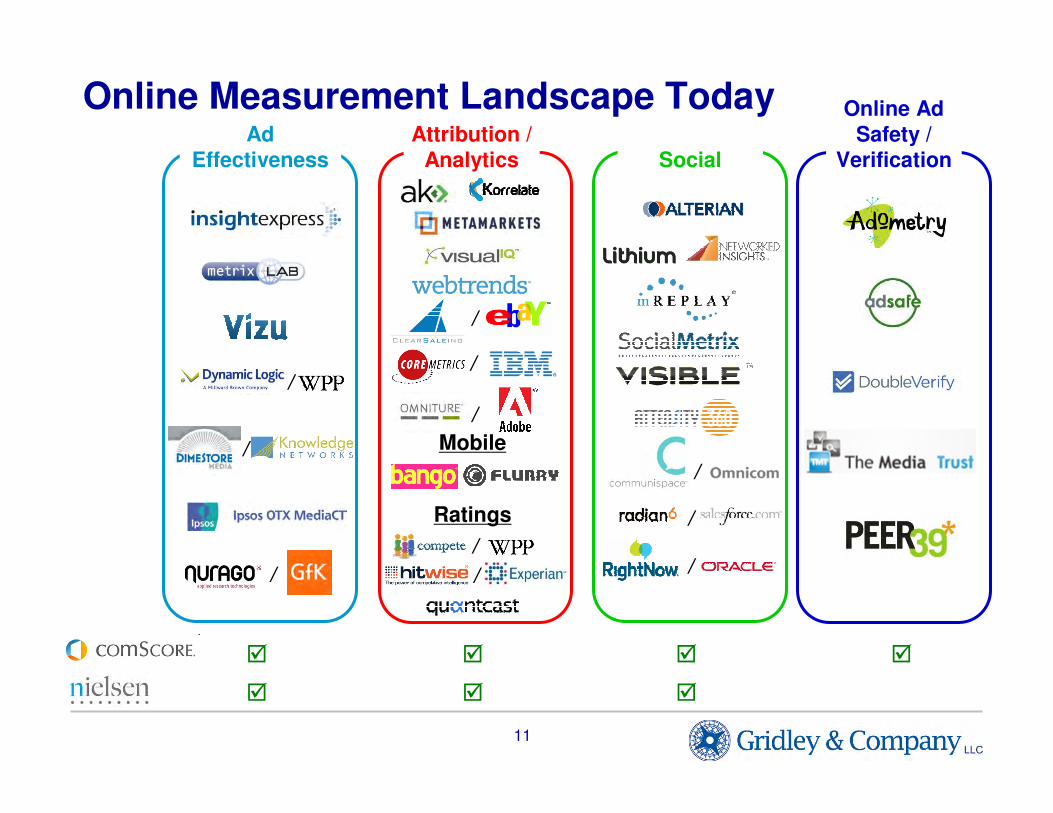

Online Measurement Landscape Today

/

Social

Online Ad Safety /

VerificationAttribution /

AnalyticsAd

Effectiveness

/

/

� �

� � �

/

� �

/

/

/

Ratings

/

/

/

Mobile

/

12

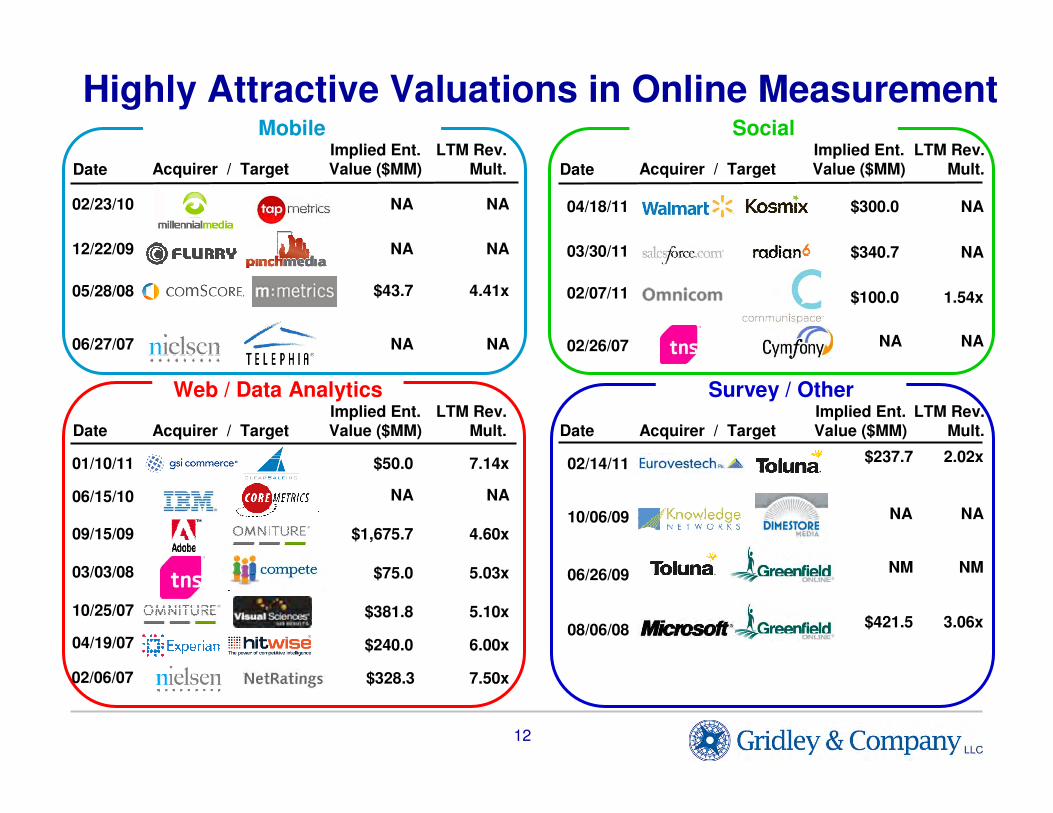

Highly Attractive Valuations in Online Measurement

Survey / OtherWeb / Data Analytics

Mobile

Acquirer / TargetDate

$100.0

$300.004/18/11

$340.703/30/11

Acquirer / TargetDate

$75.003/03/08

$240.004/19/07

$381.810/25/07

Acquirer / TargetDateImplied Ent. Value ($MM)

12/22/09 NA

Acquirer / TargetDate

$421.508/06/08

$43.705/28/08

$328.302/06/07

Implied Ent. Value ($MM)

LTM Rev.Mult.

LTM Rev.Mult.

LTM Rev.Mult.

Implied Ent. Value ($MM)

LTM Rev.Mult.

5.03x

6.00x

5.10x

NA

4.41x 1.54x

NA

NA

3.06x

7.50x

NA06/27/07 NA

NM06/26/09 NM

$1,675.709/15/09

NA

4.60x

NA

$237.702/14/11 2.02x

02/07/11

06/15/10

Social

02/26/07

Implied Ent. Value ($MM)

02/23/10 NA NA

10/06/09 NANA

NA NA

01/10/11 $50.0 7.14x

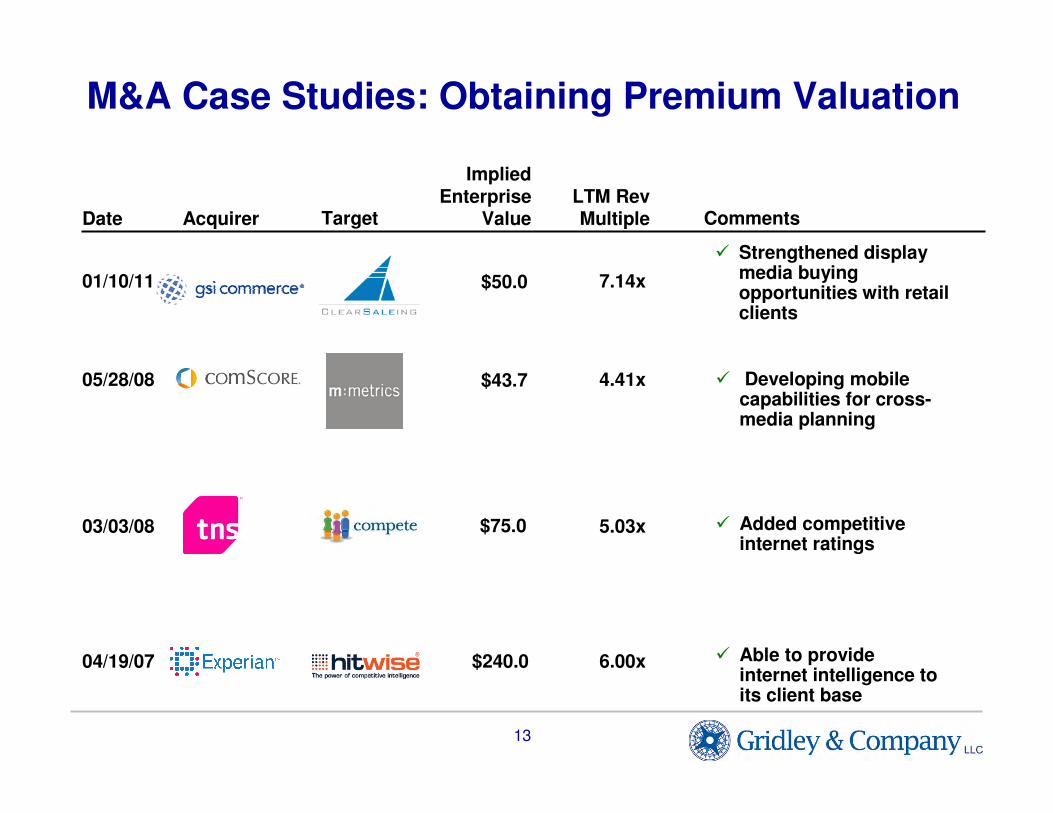

13

Acquirer

Implied Enterprise

Value Target LTM Rev MultipleDate

05/28/08

03/03/08

04/19/07

$43.7 4.41x

$75.0

$240.0 6.00x

5.03x

� Developing mobile capabilities for cross-media planning

� Added competitive internet ratings

� Able to provide internet intelligence to its client base

Comments

M&A Case Studies: Obtaining Premium Valuation

� Strengthened display media buying opportunities with retail clients

01/10/11 $50.0 7.14x

14

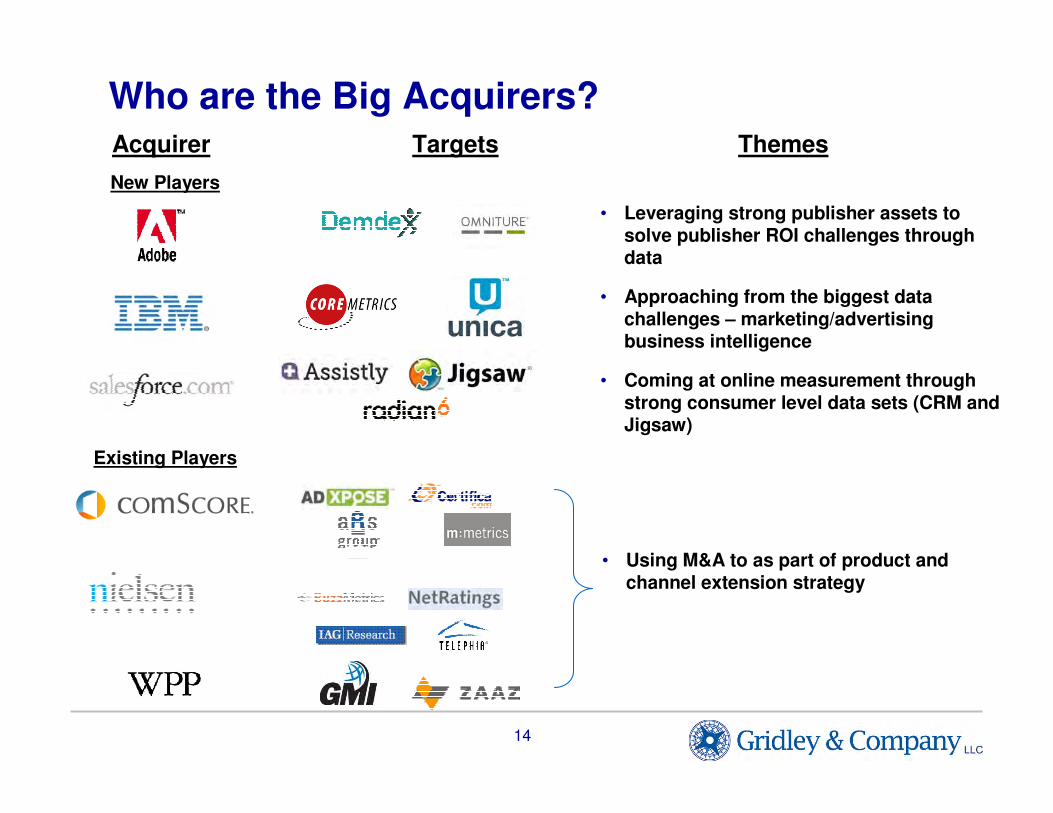

Who are the Big Acquirers?Acquirer Targets Themes

• Leveraging strong publisher assets to solve publisher ROI challenges through data

• Approaching from the biggest data challenges – marketing/advertising business intelligence

• Coming at online measurement through strong consumer level data sets (CRM and Jigsaw)

New Players

Existing Players

• Using M&A to as part of product and channel extension strategy

15

Measurement Technologies Will be Important to the Development of Real-Time Bidding

• Measurement of

quality and

effectiveness will

grow in importance

• Stigma of low quality

will further increase

importance of real

time measurement

technologies

Blind“Cookied”

Rapidly growing market > Majority of impressions still relatively anonymous

$353

$823

$380

$592

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2001 2010

U.S. Exchange Traded Media Spending in $MM

Source: Forrester

RTB

Non-RTB

16

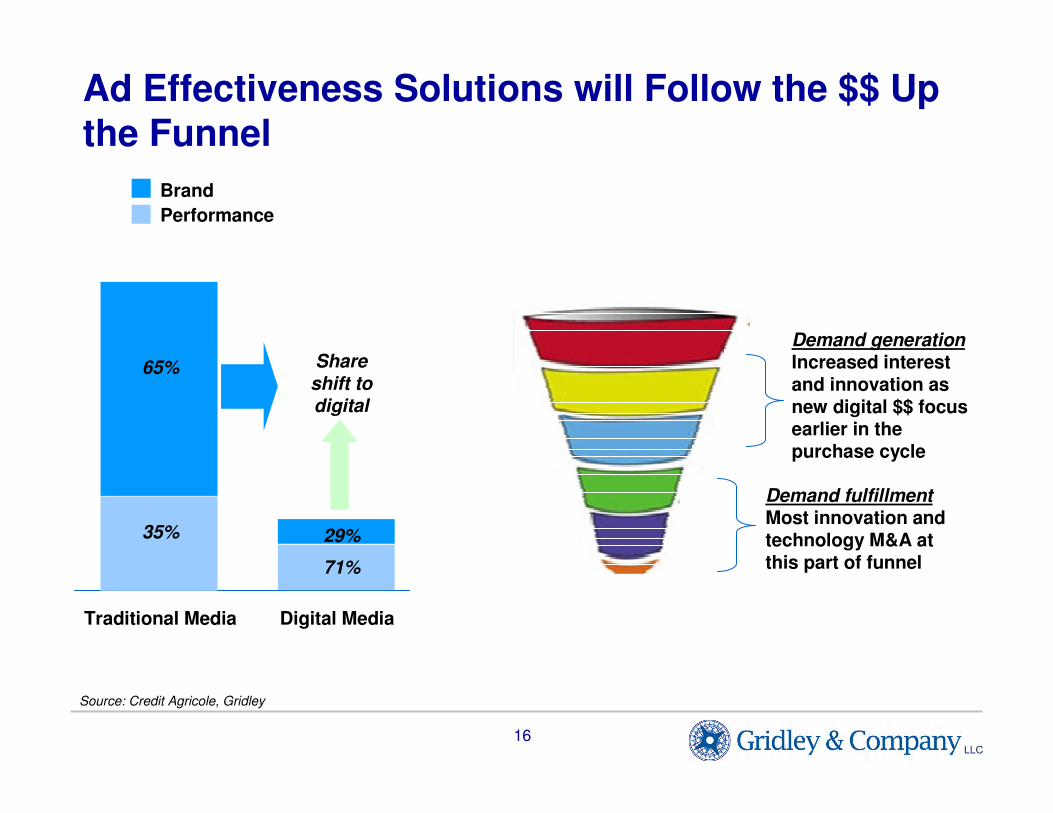

Ad Effectiveness Solutions will Follow the $$ Up the Funnel

65%

35%

71%

29%

Performance

Brand

Traditional Media Digital Media

Share shift to digital

Demand fulfillmentMost innovation and technology M&A at this part of funnel

Demand generationIncreased interest and innovation as new digital $$ focus earlier in the purchase cycle

Source: Credit Agricole, Gridley

17

Social will Challenge the Status Quo in Both Advertising and User Measurement

Coca-Cola

Example of Coke using Facebook to

elicit feedback on

bottle design

Example of Coke using Facebook to

elicit feedback on

bottle design

Massive audience

Massive audience

Facebook controls a large part of the adtech supply

(~30%)

Rest of the Web

Brands are going directly to its

consumers through Facebook

Source: Comscore Q1 estimates for U.S. Web, Facebook

Q1’11: 1.1 trillion impressions

18

Source: eMarketer

Tremendous Promise with Mobile Given Unique Characteristics

Computer

Newspapers, Magazines, Books

Snail Mail

Video Camera

Range Finder

Game Console

Alarm ClockMusic

Player

Credit Cards, Identity

Telephone

PDA

GPS, Maps,

Compass

Camera

Watch

29%

34%

5%

5%

16%

8%

Don’t know

Performed worse than expected

Performed as expected

Exceeded expectations

Haven’t measured

Far below expectations

ROI of Existing Mobile Marketing Campaigns

Measurement will be critical to achieve scale by marketers

Over 50% of campaigns lack any sort of measurement

19

Everything is Becoming Internet-Enabled

PC: 1990 - VoIP: 1999 - Mobile: 2008 - Tablet: 2010 - TV: 2012 ? Car: 2013?

Offline Online

• Growing interest from brand marketers to define ROI across channels

• Data integration becoming increasingly possible/seamless as world become internet-enabled

20

Convergence of Capabilities

• Becoming hard to determine who is competitive as separate disciplines converge

• Has major M&A implications

Mobile Social

Ad Effectiveness

Ad Safety / Verification

Users

21

Advice to the Audience – Private Companies

• Unprecedented opportunity for new leadership

• Clear, differentiated capabilities are key

• Buyers will pay premiums for market leaders and experienced teams

• Scale and successful client case studies are key

• Watch for new buyers to emerge

22

Advice to the Audience – Public Companies

• Traditional leaders – You are more vulnerable than you think

• Think strategically about innovation and M&A

• Tremendous value being created, competitive dynamics are changing

• Watch out for disruptive business models

23

Advice to the Audience – VC / PE Investors

• "Jump In – The Water's Fine"

• Be careful about amount of $ invested

• $250MM+ exits aren't easy!

• Look for new strategic buyers to emerge

• Different companies require different exit strategies

24

Questions?

Linda GridleyGridley & Company LLC

10 East 53rd Street, 24th FloorNew York, NY 10022

212.400.9720 tel

212.400.9717 faxTwitter: @gridleyco

www.gridleyco.com