Offshore Wind Market and Economic Analysis Report 2013 · 2013-12-13 · Offshore Wind Market and...

143

Offshore Wind Market and Economic Analysis Annual Market Assessment Prepared for: U.S. Department of Energy Client Contact Michael Hahn, Patrick Gilman Award Number DE-EE0005360 Navigant Consulting, Inc. 77 Bedford Street Suite 400 Burlington, MA 01803-5154 781.270.8314 www.navigant.com October 17, 2013

Transcript of Offshore Wind Market and Economic Analysis Report 2013 · 2013-12-13 · Offshore Wind Market and...

Offshore Wind Market and Economic

Analysis

Annual Market Assessment

Prepared for:

U.S. Department of Energy

Client Contact Michael Hahn, Patrick Gilman

Award Number DE-EE0005360

Navigant Consulting, Inc.

77 Bedford Street

Suite 400

Burlington, MA 01803-5154

781.270.8314

www.navigant.com

October 17, 2013

Offshore Wind Market and Economic Analysis Page ii Document Number DE-EE0005360

U.S. Offshore Wind Market and Economic Analysis

Annual Market Assessment

Document Number DE-EE0005360

Prepared for: U.S. Department of Energy

Michael Hahn

Patrick Gilman

Prepared by: Navigant Consulting, Inc.

Bruce Hamilton, Principal Investigator

Lindsay Battenberg

Mark Bielecki

Charlie Bloch

Terese Decker

Lisa Frantzis

Jay Paidipati

Andy Wickless

Feng Zhao

Bruce

Navigant Consortium Member Organizations Key Contributors

American Wind Energy Association Jeff Anthony and Chris Long

Great Lakes Wind Collaborative Victoria Pebbles

Green Giraffe Energy Bankers Marie de Graaf, Jérôme Guillet, and Niels

Jongste

National Renewable Energy Laboratory Eric Lantz and Aaron Smith

Ocean & Coastal Consultants (a COWI company) Brent D. Cooper, P.E., Joe Marrone, P.E., and

Stanley M. White, P.E., D.PE, D.CE

Tetra Tech EC, Inc. Michael D. Ernst, Esq.

Offshore Wind Market and Economic Analysis Page iii Document Number DE-EE0005360

Notice and Disclaimer

This report was prepared by Navigant Consulting, Inc. for the exclusive use of the U.S. Department of

Energy—who supported this effort under Award Number DE-EE0005360. The work presented in this

report represents our best efforts and judgments based on the information available at the time this

report was prepared. Navigant Consulting, Inc. is not responsible for the reader’s use of, or reliance

upon, the report, nor any decisions based on the report. NAVIGANT CONSULTING, INC. MAKES NO

REPRESENTATIONS OR WARRANTIES, EXPRESSED OR IMPLIED. Readers of the report are advised

that they assume all liabilities incurred by them, or third parties, as a result of their reliance on the

report, or the data, information, findings and opinions contained in the report.

Neither the United States Government nor any agency thereof, nor any of their employees, makes any

warranty, express or implied, or assumes any legal liability or responsibility for the accuracy,

completeness, or usefulness of any information, apparatus, product, or process disclosed, or represents

that its use would not infringe privately owned rights. Reference herein to any specific commercial

product, process, or service by trade name, trademark, manufacturer, or otherwise does not necessarily

constitute or imply its endorsement, recommendation, or favoring by the United States government or

any agency thereof.

This report is being disseminated by the Department of Energy. As such, the document was prepared in

compliance with Section 515 of the Treasury and General Government Appropriations Act for Fiscal

Year 2001 (Public Law 106-554) and information quality guidelines issued by the Department of Energy.

Though this report does not constitute “influential” information, as that term is defined in DOE’s

information quality guidelines or the Office of Management and Budget's Information Quality Bulletin

for Peer Review (Bulletin), the study was reviewed both internally and externally prior to publication.

For purposes of external review, the study benefited from the advice and comments of a panel of

offshore wind industry stakeholders. That panel included representatives from private corporations,

national laboratories, and universities.

Offshore Wind Market and Economic Analysis Page iv Document Number DE-EE0005360

Acknowledgments

For their support of this report, the authors thank the entire U.S. Department of Energy (DOE) Wind &

Water Power Technologies Office, particularly Patrick Gilman and Michael Hahn.

Navigant would also like to thank the following for their contributions to this report:

Arnold Boezaart GVSU / Michigan Alternative and Renewable Energy Center

Guy Chapman Dominion

Ben Chicoski Energetics Incorporated

Sebastian Chivers PMSS

Fara Courtney U.S. Offshore Wind Collaborative

Steve Dever LEEDCo

Tim Downey Saint Lawrence Seaway Development Corporation (US DOT)

Patrick Fullenkamp Global Wind Network

Tom Graf Michigan DEQ

Lynn Gresock ARCADIS

Jeffrey Grybowski Deepwater Wind

Jeff Hammond Ecology and Environment, Inc.

John Hingtgen California Energy Commission

William Hurley The Glosten Associates, Inc.

Willett Kempton University of Delaware

Ben Maples NREL

Dennis Nielson DOSECC Exploration Services

Brian O'Hara Southeastern Coastal Wind Coalition

Doug Pfeister Offshore Wind Development Coalition

Eric Ritter LEEDCo

Jacques Roeth NYSERDA

Bob Schubert Siemens Energy Inc

Peter D. Stoklossa ThyssenKrupp Rothe Erde GmbH

Katarina Svabcikova Siemens Energy

Larry Viterna Nautica Windpower LLC

Carl Wegener Signal International, Inc.

Cliff Williams Orisol Energy

Greg Williams Bracewell & Guiliani, LLP

Paul Williamson Maine Wind Industry Initiative

Andy Zalay windfarm inc

Offshore Wind Market and Economic Analysis Page v Document Number DE-EE0005360

Table of Contents

Executive Summary ............................................................................................................... xiii

Section 1. Global Offshore Wind Development Trends ........................................................................ xiii Section 2. Analysis of Policy Developments ........................................................................................... xvi Section 3. Economic Impacts .................................................................................................................... xvii Section 4. Developments in Relevant Sectors of the Economy ............................................................ xvii

1. Global Offshore Wind Development Trends ............................................................. 1

1.1 Global Offshore Wind Development ................................................................................................ 3 1.2 U.S. Project Development Overview ................................................................................................ 5

1.2.1 Forecast Capacity and Completion Dates ......................................................................... 9 1.2.2 Notable Developments in Advanced-Stage Projects........................................................ 9 1.2.3 U.S. DOE Advanced Technology Demonstration Projects ............................................ 13

1.3 Capital Cost Trends .......................................................................................................................... 17 1.4 Market Segmentation and Technology Trends ............................................................................. 19

1.4.1 Depth and Distance from Shore ........................................................................................ 19 1.4.2 Plant Characteristics ........................................................................................................... 22 1.4.3 Turbine Trends .................................................................................................................... 23 1.4.4 Support Structure Trends .................................................................................................. 31 1.4.5 Electrical Infrastructure Trends ........................................................................................ 36 1.4.6 Logistical and Vessel Trends ............................................................................................. 39 1.4.7 Operations and Maintenance Trends ............................................................................... 43

1.5 Financing Trends ............................................................................................................................... 44 1.5.1 Rising Capital Requirements ............................................................................................. 44 1.5.2 Utility On-balance Sheet Financing .................................................................................. 44 1.5.3 Project Finance .................................................................................................................... 44 1.5.4 Multiparty Financing.......................................................................................................... 45 1.5.5 Importance of Government Financial Institutions ......................................................... 46 1.5.6 New Financing Sources ...................................................................................................... 46 1.5.7 Likely Financing Trends for Offshore Wind in the United States ................................ 47 1.5.8 Cape Wind Financing ......................................................................................................... 47

2. Analysis of Policy Developments ................................................................................ 48

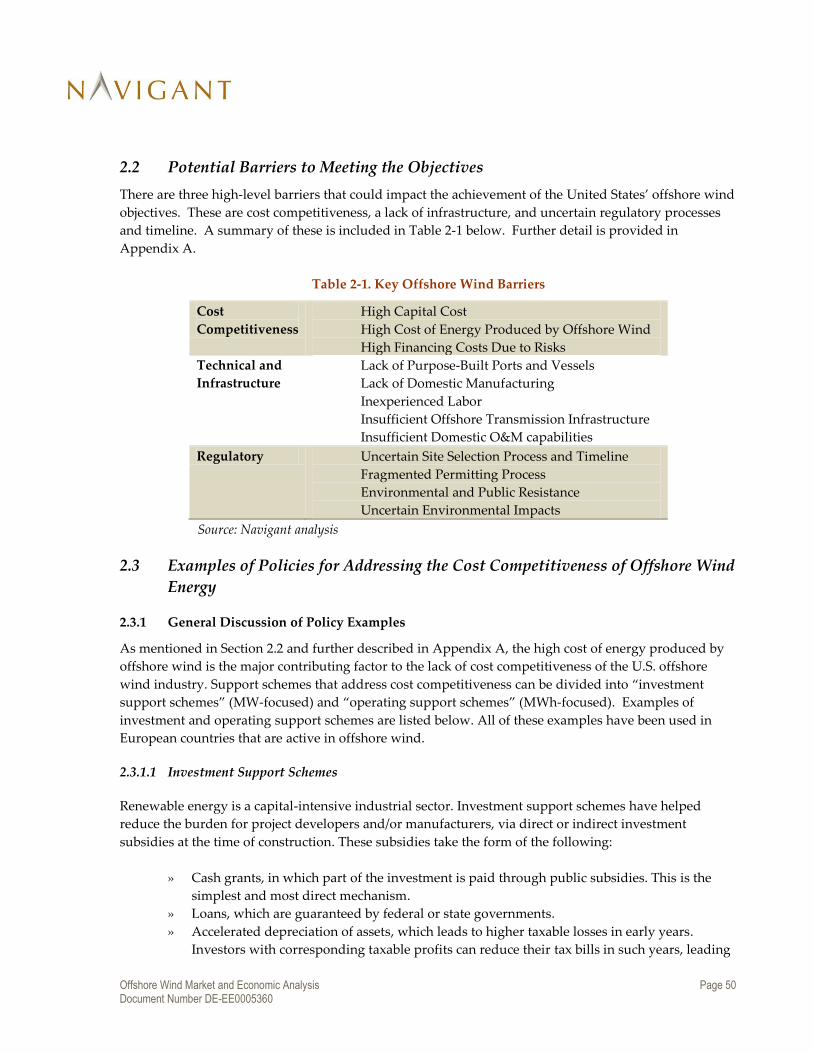

2.1 Offshore Wind Program Objectives ................................................................................................ 49 2.2 Potential Barriers to Meeting the Objectives ................................................................................. 50 2.3 Examples of Policies for Addressing the Cost Competitiveness of Offshore Wind Energy ... 50

2.3.1 General Discussion of Policy Examples ........................................................................... 50 2.3.2 Current U.S. and State Policies.......................................................................................... 51 2.3.3 Current Policies in Europe ................................................................................................. 60

2.4 Examples of Policies for Addressing Infrastructure Challenges ................................................ 67

Offshore Wind Market and Economic Analysis Page vi Document Number DE-EE0005360

2.4.1 General Discussion of Policy Examples ........................................................................... 67 2.4.2 Current U.S. and State Policies.......................................................................................... 72 2.4.3 Current Policies in Europe ................................................................................................. 73

2.5 Policies That Address Regulatory Challenges .............................................................................. 74 2.5.1 General Discussion of Policy Examples ........................................................................... 74 2.5.2 Current U.S. and State Policies.......................................................................................... 76 2.5.3 Current Policies in Europe ................................................................................................. 80

2.6 Summary ............................................................................................................................................ 81

3. Economic Impacts ........................................................................................................... 83

3.1 Summary ............................................................................................................................................ 83 3.2 Scope of Update................................................................................................................................. 83 3.3 Baseline Data Collection ................................................................................................................... 84

3.3.1 Online Survey ...................................................................................................................... 84 3.3.2 Phone Survey ....................................................................................................................... 85 3.3.3 JEDI Estimates ..................................................................................................................... 85

3.4 Results ................................................................................................................................................. 85

4. Developments in Relevant Sectors of the Economy ................................................ 87

4.1 Introduction ....................................................................................................................................... 87 4.2 Power Sector ...................................................................................................................................... 88

4.2.1 Change in Overall Demand for Electricity ...................................................................... 88 4.2.2 Change in the Country’s Nuclear Power Generation Capacity.................................... 89 4.2.3 Change in Natural Gas Prices ........................................................................................... 90 4.2.4 Change in the Country’s Coal-Based Generation Capacity .......................................... 91

4.3 Oil and Gas ......................................................................................................................................... 92 4.3.1 Change in Level of Offshore Oil and Gas Development ............................................... 92

4.4 Construction ...................................................................................................................................... 92 4.4.1 Change in Level of Construction Activity Using Similar Types of Equipment and/or

Raw Materials as Offshore Wind ...................................................................................... 92 4.5 Manufacturing ................................................................................................................................... 93

4.5.1 Change in Manufacturing of Products That Utilize Similar Types of Raw Materials

as Offshore Wind ................................................................................................................ 93 4.6 Telecommunications ......................................................................................................................... 94

4.6.1 Change in Demand for Subsea Cable-Laying Vessels ................................................... 94 4.7 Financial ............................................................................................................................................. 95

4.7.1 Change in the Cost of Capital ........................................................................................... 95

5. Conclusion ........................................................................................................................ 96

References .................................................................................................................................. 97

Appendix A. Potential Barriers to Offshore Wind Development in the U.S. ...... 101

Offshore Wind Market and Economic Analysis Page vii Document Number DE-EE0005360

A.1 Cost-Competitiveness of Offshore Wind Energy ....................................................................... 101 A.2 Infrastructure Challenges ............................................................................................................... 101 A.3 Regulatory Challenges ................................................................................................................... 102

Appendix B. Offshore Wind Policies in Selected U.S. States ................................. 104

B.1 California .......................................................................................................................................... 104 B.2 Delaware........................................................................................................................................... 104 B.3 Illinois ............................................................................................................................................... 105 B.4 Maine ................................................................................................................................................ 106 B.5 Maryland .......................................................................................................................................... 106 B.6 Massachusetts .................................................................................................................................. 107 B.7 Michigan ........................................................................................................................................... 108 B.8 New Jersey ....................................................................................................................................... 109 B.9 New York ......................................................................................................................................... 110 B.10 Ohio ................................................................................................................................................... 111 B.11 Rhode Island .................................................................................................................................... 111 B.12 Texas ................................................................................................................................................. 112 B.13 Virginia ............................................................................................................................................. 112

Appendix C. Offshore Wind Policies in Selected European Countries ................ 114

C.1 Denmark ........................................................................................................................................... 114 C.2 Germany ........................................................................................................................................... 116 C.3 The Netherlands .............................................................................................................................. 119 C.4 United Kingdom .............................................................................................................................. 122

Offshore Wind Market and Economic Analysis Page viii Document Number DE-EE0005360

List of Figures

Figure ES-1. Proposed U.S. Offshore Wind Energy Projects in Advanced Development Stages by

Jurisdiction and Project Size ...................................................................................................................................... Figure 1-1. Historical Growth of the Global Offshore Wind Market ................................................................. 3 Figure 1-2. Proposed U.S. Offshore Wind Energy Projects in Advanced Development Stages by

Jurisdiction and Project Size ...................................................................................................................................... Figure 1-3. Growth Trajectory for U.S. Offshore Wind Based on Forecast Construction Dates .................... 9 Figure 1-4. Map of BOEM Atlantic Wind Energy Areas ................................................................................... 11 Figure 1-5. Reported Capital Cost Trends for Global Offshore Wind Projects over Time ........................... 17 Figure 1-6. Offshore Wind Plant Capital Cost Breakdown ............................................................................... 18 Figure 1-7. Offshore Wind Plant Capital Cost Breakdown (without Construction Financing) ................... 19 Figure 1-8. Average Distance from Shore for Offshore Wind Projects over Time ......................................... 20 Figure 1-9. Depth and Distance from Shore for Global Offshore Wind Farms .............................................. 21 Figure 1-10. Global Offshore Wind Plant Capacities over Time ...................................................................... 22 Figure 1-11. Reported Capacity Factors for Global Offshore Wind Plants over Time .................................. 23 Figure 1-12. Average Turbine Size for Historic Global and Planned U.S. Offshore Wind Farms ............... 24 Figure 1-13. Global Offshore Wind Plant Hub Heights over Time ................................................................. 26 Figure 1-14. Global Offshore Wind Plant Rotor Diameter over Time ............................................................. 27 Figure 1-15. Share of Cumulative Installed Offshore Wind Capacity by Drive Train Configuration

(through 2012) ......................................................................................................................................................... 28 Figure 1-16. Offshore Wind Turbine Prototypes by Drivetrain Configuration and Year of First Offshore

Deployment ............................................................................................................................................................. 31 Figure 1-17. Substructure Types for Completed Offshore Wind Projects (through 2012) ............................ 32 Figure 1-18. Substructure Types for Completed Offshore Wind Projects by Year Installed ........................ 33 Figure 1-19. Array and Export Voltages for Offshore Wind Projects .............................................................. 38 Figure 2-1. Summary of Policies to Address Cost Competitiveness in Selected U.S. States ........................ 53 Figure 2-2. Site Selection and Leasing Policies in U.S. States ........................................................................... 77 Figure 3-1. Annual U.S. Employment Supported by the U.S. Offshore Wind Industry, 2012 Projection .. 83 Figure 3-2. Annual U.S. Economic Activity Supported by the U.S. Offshore Wind Industry, 2012

Projection ................................................................................................................................................................. 84 Figure 4-1. U.S. Retail Electricity Sales: 2002-2012 (million kWh) ................................................................... 89 Figure 4-2. U.S. Power Generation Capacity Additions by Fuel Type ............................................................ 90 Figure 4-3. Henry Hub Gulf Coast Natural Gas Spot Price 2007-2013 ............................................................ 91 Figure 4-4. Producer Price Index for Selected Commodities (2003-2012) ....................................................... 93 Figure 4-5. Rare Earth Criticality Matrices .......................................................................................................... 94 Figure 4-6. Federal Funds Effective Rate (%): January 2000 – July 2013 ......................................................... 95

Offshore Wind Market and Economic Analysis Page ix Document Number DE-EE0005360

List of Tables

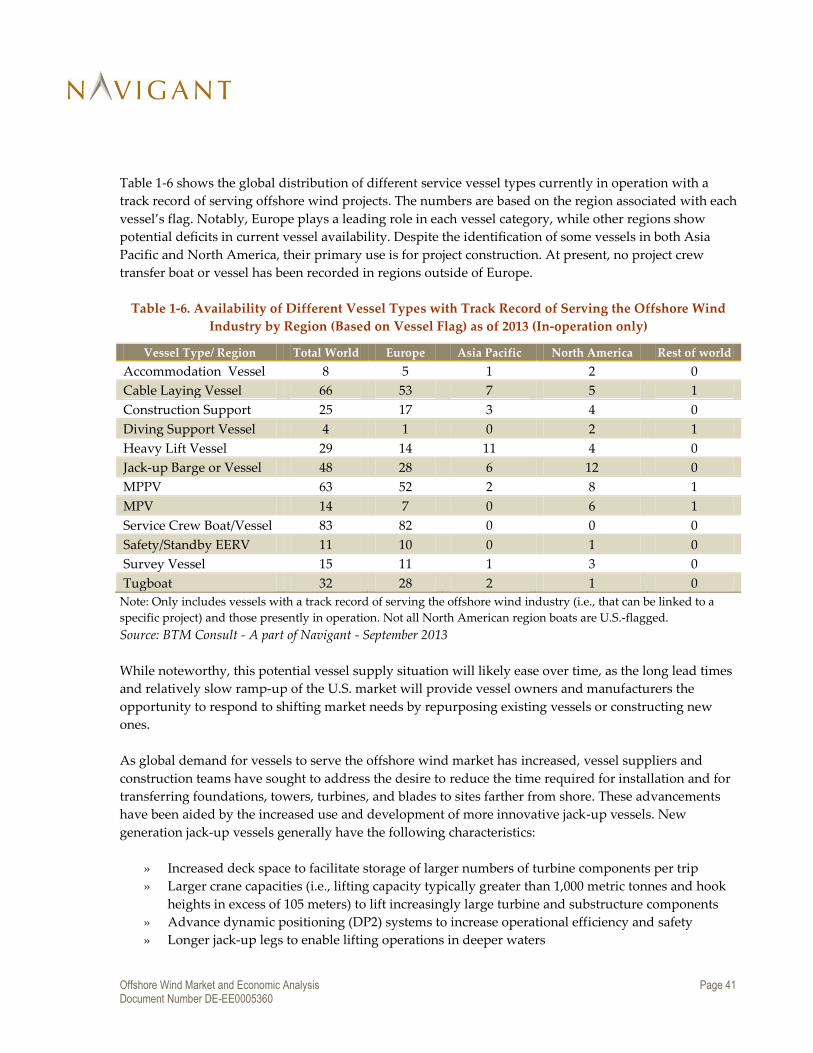

Table 1-1. Summary of Installed Global Offshore Capacity through 2012 ....................................................... 4 Table 1-2. Summary of Advanced-Stage U.S. Projects ........................................................................................ 7 Table 1-3. Segmentation of Wind Turbine Drivetrain Architectures ............................................................... 30 Table 1-4. Selected Offshore Wind Foundation Designs under Development .............................................. 35 Table 1-5. Vessel Types Required for Each Offshore Wind Project Phase ...................................................... 40 Table 1-6. Availability of Different Vessel Types with Track Record of Serving the Offshore Wind

Industry by Region (Based on Vessel Flag) as of 2013 (In-operation only) .................................................... 41 Table 2-1. Key Offshore Wind Barriers ................................................................................................................ 50 Table 2-2. Policies to Address Cost Competitiveness of Offshore Wind in Selected U.S. States ................. 54 Table 2-3. Renewable Energy Investment Support Schemes in Europe ......................................................... 60 Table 2-4. Offshore Wind Capacity Installed Under Support Schemes Used in Europe .............................. 63 Table 2-5. State-based Wind-focused Transmission Policies ............................................................................ 72 Table 2-6. Policies for Addressing Infrastructure Challenges in Europe ........................................................ 73 Table 2-7. Policies that Address Regulatory Challenges in Europe ................................................................. 80 Table 2-8. Offshore Wind Policy Examples and Developments ...................................................................... 81 Table 3-1. Estimated Employment and Investment in the U.S. Offshore Wind Industry ............................ 86 Table 4-1. Factors That Impact Offshore Wind ................................................................................................... 88

Offshore Wind Market and Economic Analysis Page x Document Number DE-EE0005360

Abbreviations

AC alternating current

ATD Advanced Technology Demonstration

AWC Atlantic Wind Connection

AWEA American Wind Energy Association

BOEM Bureau of Ocean Energy Management

BPU Board of Public Utilities

BTMU Bank of Tokyo-Mitsubishi UFJ (Japan)

CAISO California Independent System Operator

CBM condition-based maintenance

CEQ Council on Environmental Quality

CfD Contracts for Difference

COP Construction and Operations Plan

CREZ competitive renewable energy zone

CZMA Coastal Zone Management Act

DC direct current

DD Direct Drive

DEA Danish Energy Agency

DECC Department of Energy and Climate Change

(U.K.)

DNR Department of Natural Resources

DOE Department of Energy

EA environmental assessment

EERE Energy Efficiency & Renewable Energy

EEZ Exclusive Economic Zone (DK)

EIS environmental impact statement

EnWG New German Energy Act

EPA Environmental Protection Agency

EPAct Energy Policy Act of 2005 (U.S.)

ETI Energy Technologies Institute

EU European Union

EWEA European Wind Energy Association

FEPA Food and Environment Protection Act 1985

(U.K.)

FERC Federal Energy Regulatory Commission

FiT Feed-in Tariff

FONSI Finding of No Significant Impacts

FTE full-time equivalent

GBS gravity-based structure

GDP gross domestic product

GE General Electric

GIB Green Investment Bank (U.K.)

GLOW Great Lakes Wind

GLWC Great Lakes Wind Collaborative

GW gigawatt

GWEC Global Wind Energy Council

HVAC high-voltage alternating current

HVDC high-voltage direct current

IAPEME International Advisory Panel of Experts on

Marine Ecology

IOU investor-owned utility

IPP independent power producer

ISO independent system operator

ITC investment tax credit

JEDI Jobs & Economic Development Impact

kcmil thousand circular mils

kV kilovolt

kW kilowatt

LCOE levelized cost of energy

LEEDCo Lake Erie Energy Development Corporation

LIPA Long Island Power Authority

LNG liquefied natural gas

METI Ministry of Economy, Trade and Industry

(Japan)

MISO Midcontinent Independent System Operator

mmBTU million British thermal units

MMS Minerals Management Service

MOU Memorandum of Understanding

MW megawatt

MWh megawatt-hours

NEPA National Environmental Policy Act

NIP National Infrastructure Plan

NOAA National Oceanic and Atmospheric

Administration

NPS National Policy Statement (U.K.)

NREL National Renewable Energy Laboratory

NYPA New York Power Authority

O&M operations and maintenance

OCS Outer Continental Shelf

OEM original equipment manufacturer

Ofgem Office of the Gas and Electricity Markets

(U.K.)

OFTO offshore transmission owner

OREC offshore wind renewable energy credit

OTB Offshore Terminal Bremerhaven

OWEDA Offshore Wind Economic Development Act

PEA programmatic EA

Offshore Wind Market and Economic Analysis Page xi Document Number DE-EE0005360

PEIS programmatic EIS

PMDD permanent magnetic direct drive

PMG permanent magnetic generator

POU publicly owned utility

PPA power purchase agreement

PSC Public Service Commission

PTC production tax credit

PUC Public Utilities Commission

R&D research and development

REC Renewable Energy Credit

RFP request for proposal

RO Renewable Obligation

ROC Renewable Obligation Certificate

RPS renewable portfolio standard

RTO regional transmission organization

SAP site assessment plan

SCADA supervisory control and data acquisition

SEA Strategic Environmental Assessment (U.K.)

TCE The Crown Estate

TSO transmission system operator

UMaine University of Maine

USACE U.S. Army Corps of Engineers

USFWS U.S. Fish and Wildlife Service

WAB Wind Agency Bremerhaven

WEA Wind Energy Area

WRA wind resource area

Offshore Wind Market and Economic Analysis Page xii Document Number DE-EE0005360

Introduction

This report was produced on behalf of the Wind and Water Power Technologies Office within the U.S.

Department of Energy’s (DOE) Office of Energy Efficiency and Renewable Energy (EERE) as an award

resulting from Funding Opportunity Announcement DE-FOA-0000414, entitled U.S. Offshore Wind:

Removing Market Barriers; Topic Area 1: Offshore Wind Market and Economic Analysis.

The objective of this report is to provide a comprehensive annual assessment of the U.S. offshore wind

market. The report will be updated and published annually for a three-year period. The report was first

published in early 2013 covering research performed in 2012. This 2nd annual report focuses on new

developments that have occurred in 2013. The report will provide stakeholders with a reliable and

consistent data source addressing entry barriers and U.S. competitiveness in the offshore wind market.

The report was produced by the Navigant Consortium, led by Navigant Consulting, Inc. (“Navigant”).

Additional members of the Navigant Consortium include the American Wind Energy Association

(AWEA), the Great Lakes Wind Collaborative (GLWC), Green Giraffe Energy Bankers, National

Renewable Energy Laboratory (NREL), Ocean & Coastal Consultants (a COWI company), and Tetra

Tech EC, Inc.

Offshore Wind Market and Economic Analysis Page xiii Document Number DE-EE0005360

Executive Summary

The U.S. offshore wind industry is transitioning from early development to demonstration of

commercial viability. While there are no commercial-scale projects in operation or in the construction

phase, there are eleven U.S. projects in advanced development, defined as having either been awarded a

lease, conducted baseline or geophysical studies, or obtained a power purchase agreement (PPA). There

are panels or task forces in place in at least 13 states to engage stakeholders to identify constraints and

sites for offshore wind. U.S. policymakers are beginning to follow the examples in Europe that have

proven successful in stimulating offshore wind technological advancement, project deployment, and job

creation.

This report is the second annual assessment of the U.S. offshore wind market. It includes the following

major sections:

» Section 1: key data on developments in the offshore wind technology sector and the global

development of offshore wind projects, with a particular focus on progress in the United States

» Section 2: analysis of policy developments at the federal and state levels that have been effective

in advancing offshore wind deployment in the United States

» Section 3: analysis of actual and projected economic impact, including regional development and

job creation

» Section 4: analysis of developments in relevant sectors of the economy with the potential to affect

offshore wind deployment in the United States

Section 1. Global Offshore Wind Development Trends

There are approximately 5.3 gigawatts (GW) of offshore wind installations worldwide. The majority of

this activity continues to center on northwestern Europe, but development in China continues to

progress. In 2012, more than 1,100 megawatts (MW) of wind power capacity was added globally, with

the United Kingdom alone accounting for 756 MW of new capacity. The European market will continue

to grow rapidly over the next two years, with new and expanding projects likely to contribute a record-

setting 2,900 MW in 2013 alone (mostly in Germany and the United Kingdom).

Offshore Wind Market and Economic Analysis Page xiv Document Number DE-EE0005360

Since the last edition of this report, several potential U.S. offshore wind projects have achieved

notable advancements in their development processes. In addition to two Bureau of Ocean Energy

Management (BOEM) commercial lease auctions for federal Wind Energy Areas (WEAs), other later-

stage commercial-scale projects have made incremental progress toward starting construction. Eleven

U.S. projects, representing 3,824 MW, now lie in advanced stages of development.1 . A map showing the

announced locations and capacities of these advanced-stage projects appears in Figure ES-1.

Note: One potential project (the Deepwater Wind Energy Center) spans federal waters off the coasts of

Massachusetts and Rhode Island; this map splits its estimated 1,000-MW capacity between the two states.

Source: Navigant analysis

1 In this report, “advanced stage” includes projects that have accomplished at least one of the following three

milestones: received approval for an interim limited lease or a commercial lease in state or federal waters; conducted

baseline or geophysical studies at the proposed site with a meteorological tower erected and collecting data,

boreholes drilled, or geological and geophysical data acquisition system in use; or signed a power purchase

agreement (PPA) with a power off-taker. Note that each of these criteria represents a requisite step that a project will

take before it gains final approvals and reaches the construction phase. Simply having achieved one of these

milestones, however, does not guarantee that a project will ultimately move forward, and any two projects

qualifying as “advanced” may have made different levels of progress relative to one another.

Figure ES-1. Proposed U.S. Offshore Wind Energy Projects in Advanced Development Stages by

Jurisdiction and Project Size

Offshore Wind Market and Economic Analysis Page xv Document Number DE-EE0005360

On the demonstration-project front, the University of Maine, in partnership with the U.S.

Department of Energy (DOE), installed the United States’ first offshore wind turbine: a 1/8-scale pilot

turbine on a floating foundation. In addition, DOE awarded Advanced Technology Demonstration

(ATD) project grants in December 2012. The grants are intended to help address ongoing challenges and

cost barriers to offshore wind energy. The DOE will select up to three of these projects to receive

additional funding to help carry the projects through final design, fabrication, and installation.

Offshore wind power prices have generally increased over time. For projects installed in 2012 (for

which data was available), the average reported capital cost was $5,384/kW. These cost increases are a

function of several factors (e.g., a movement toward deeper-water sites and increased siting complexity);

however, potential technological advancements aim to help slow and eventually reverse the trend. In

addition to advancements in equipment and installation approaches, improved capacity factors may

help further mitigate increased capital costs through better energy capture and conversion.

The average nameplate capacity of offshore wind turbines installed globally each year has grown

from 2.9 MW in 2007 to 4.1 MW in 2012. This trend toward larger turbines will likely continue, driven

by advancements in materials, design, processes, and logistics, which allow larger components to be

built with lower system costs. The average turbine size for advanced-stage, planned projects in the

United States, however, is expected to range between 4 and 5 MW, indicating that the United States is

largely planning to utilize larger offshore turbines rather than smaller turbines that have previously been

installed in European waters.

Globally, offshore wind projects continue to trend further from shore into increasingly deeper

waters; parallel increases in turbine sizes and hub heights are contributing to higher reported

capacity factors. While the trend toward greater distances helps reduce visual impacts and public

opposition to offshore wind, it also requires advancements in foundation technologies and affects the

logistics and costs of installation and maintenance. On the positive side, the trend toward higher-

capacity machines combines with increasing hub heights and rotor diameters to allow projects to

improve energy capture by taking better advantage of higher wind speeds.

Approaches to drivetrain configurations continue to diversify in an effort to improve reliability and

reduce exposure to volatile supplies of the rare earth metals required for direct drive generators. The

high costs of addressing past turbine equipment failures in an offshore setting have encouraged

manufacturers and developers to continue seeking more robust drivetrain configurations. However,

recent interest in direct-drive turbines has been somewhat tempered by limited supply and price

volatility for several rare earth metals. As a result, several prototypes of machines employing alternate

drivetrain designs are expected to be tested in the next two to three years.

The general trend toward diversification of substructure types also continued in 2012 and 2013, as the

industry seeks to address deeper waters, varying seabed conditions, increasing turbines sizes, and the

increased severity of wind and wave loading at offshore wind projects. However, alternatives to the

monopile and gravity-based approaches have only seen limited deployment since 2009, with a total of

350 units installed through the end of 2012 (out of an overall 1,725 units globally). To date, only two full-

scale prototype floating foundations have been installed globally.

Offshore Wind Market and Economic Analysis Page xvi Document Number DE-EE0005360

Few new developments have occurred with regard to vessels, logistics, and the operations and

maintenance (O&M) of offshore wind farms since the previous edition of this report. In general,

increased turbine size, plant size, and distance from shore all have direct consequences on vessel

requirements and availability, as well as on O&M practices. These trends will add to the logistical

difficulties of maintaining offshore turbines, particularly as longer distances from shore increase the

challenges in accessing turbines due to weather conditions. The relatively slow ramp-up of the U.S.

market will likely provide developers ample opportunity to respond to shifting vessel and O&M needs.

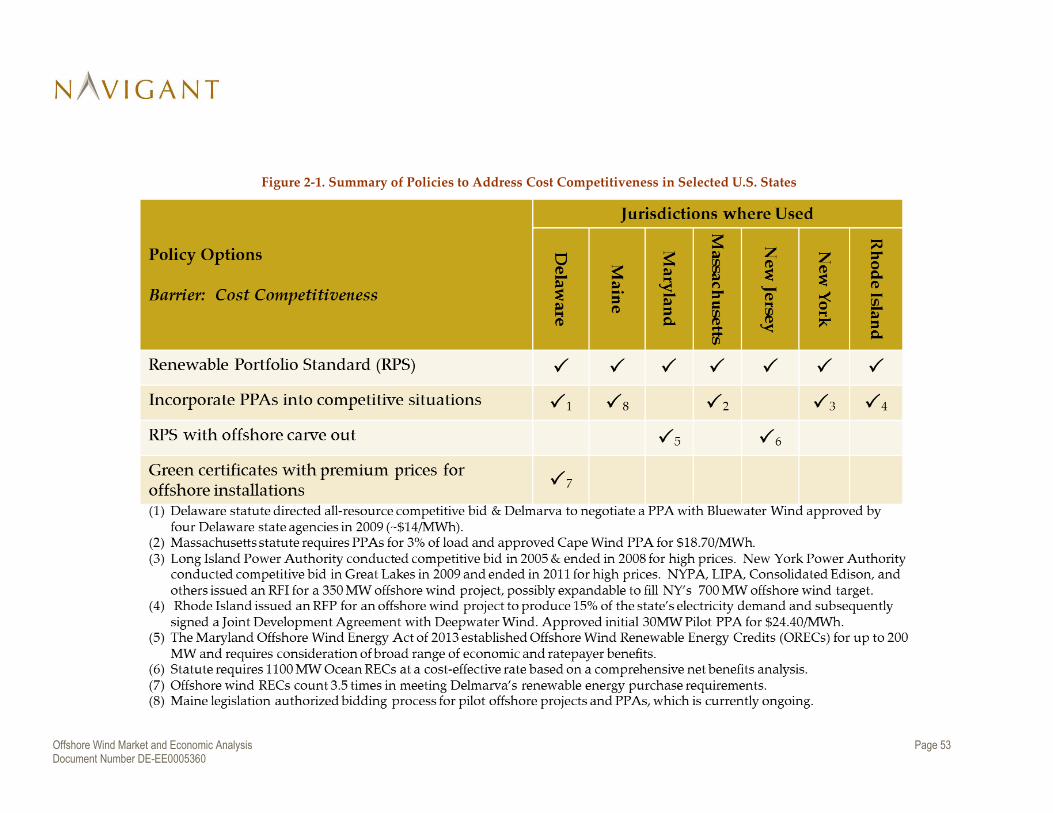

Section 2. Analysis of Policy Developments

U.S. offshore wind development faces significant challenges: (1) the cost competitiveness of offshore

wind energy;2 (2) a lack of infrastructure such as offshore transmission and purpose-built ports and

vessels; and (3) uncertain and lengthy regulatory processes. Various U.S. states, the U.S. federal

government, and European countries have used a variety of policies to address each of these barriers

with varying success.

For the U.S. to maximize offshore wind development, the most critical need continues to be

stimulation of demand through addressing cost competitiveness. In 2013, this critical need was

partially addressed through an extension of the U.S. Renewable Electricity Production Tax Credit (PTC),

the Business Energy Investment Tax Credit (ITC), and the 50 percent first-year bonus depreciation

allowance. In addition, the U.S. DOE announced seven projects that will receive up to $4 million each to

complete engineering and planning as the first phase of the Offshore Wind Advanced Technology

Demonstration Program. On the state level, the Maryland Offshore Wind Energy Act of 2013 established

Offshore Wind Renewable Energy Credits for up to 200 MW, requiring consideration of peak load price

suppression and limiting rate impacts.

Increased infrastructure is necessary to allow demand to be filled. Examples of transmission policies

that can be implemented in the short term with relatively little effort are to designate offshore wind

energy resources zones for targeted offshore grid investments, establish cost allocation and recovery

mechanisms for transmission interconnections, and promote utilization of existing transmission capacity

reservations to integrate offshore wind. In 2013, there were few tangible milestones in this area,

although long-term plans for offshore transmission projects such as the Atlantic Wind Connection and

the New Jersey Energy Link progressed steadily in their development efforts.

Regulatory policies cover three general categories: (a) policies that define the process of obtaining site

leases; (b) policies that define the environmental, permitting processes; and (c) policies that regulate

environmental and safety compliance of plants in operation. In 2013, BOEM held the first two

competitive lease sales for renewable energy in U.S. federal waters off the shores of Rhode Island and

2 The first two contracts for U.S. offshore wind reflect the higher costs by being priced at $187/MWh plus 3.5%

annual escalation for Cape Wind and $244/MWh plus 3.5% annual escalation for the Deepwater Wind Block Island

Wind Farm.

Offshore Wind Market and Economic Analysis Page xvii Document Number DE-EE0005360

Virginia. On the state level, Illinois passed the Lake Michigan Wind Energy Act, which requires the

Illinois DNR to develop a detailed offshore wind energy siting matrix for Lake Michigan.

Section 3. Economic Impacts

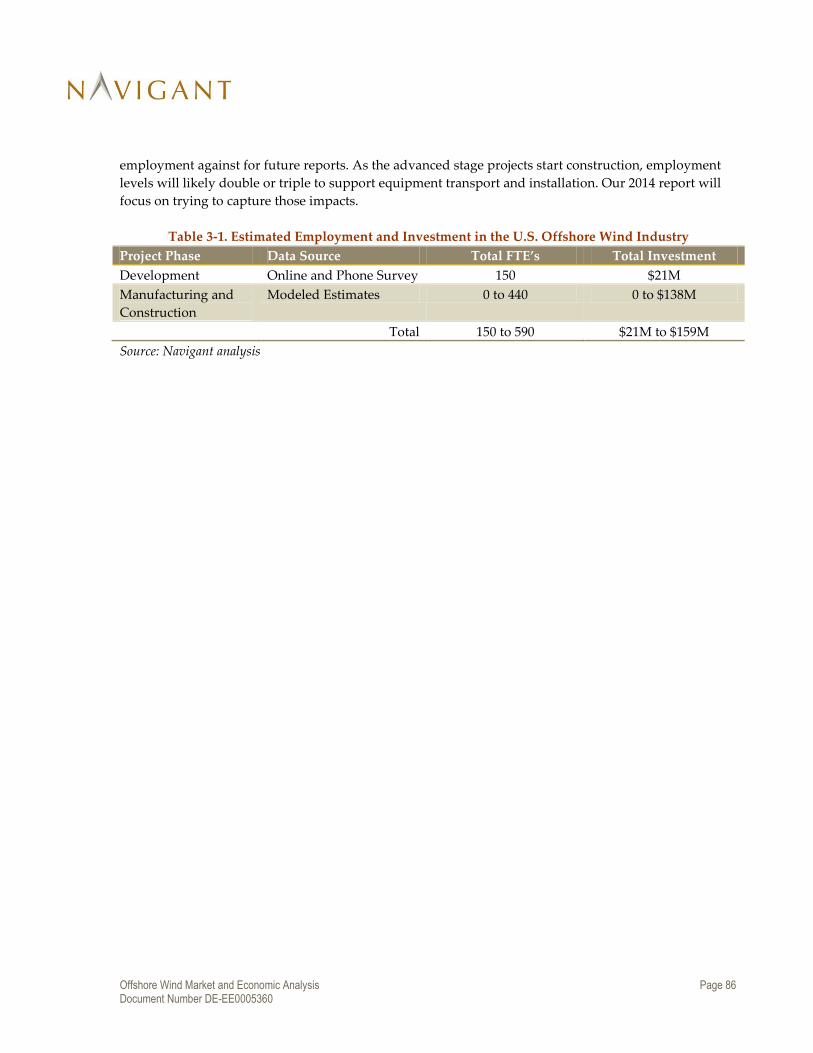

Current employment levels could be between 150 and 590 full-time equivalents (FTEs), and current

investment could be between $21 million and $159 million. The ranges are driven by Navigant’s

uncertainty about from where advanced-stage projects are sourcing components. As the advanced-stage

projects start construction, employment levels will likely double or triple to support equipment transport

and installation.

Section 4. Developments in Relevant Sectors of the Economy

The development of an offshore wind industry in the U.S. will depend on the evolution of other

sectors in the economy. Factors within the power sector, such as the capacity or price of competing

power generation technologies, will affect the demand for offshore wind. Factors within industries that

compete with offshore wind for resources (e.g., oil and gas, construction, and manufacturing) will affect

the price of offshore wind power.

Factors in the power sector that will have the largest impact include natural gas prices and the change

in coal-based generation capacity. As electricity prices have historically been linked to natural gas

prices, a decrease in prices of the latter can lead to a decrease in the price of the former. Natural gas

prices declined from above $4 per million British thermal units (MMBtu) in August 2011 to below

$2/MMbtu in April 2012, largely due to the supply of low-cost gas from the Marcellus Shale. Lower

resulting electricity prices can make investment in other power generation sources such as offshore wind

less economically attractive. However, natural gas prices have been rising steadily since then to

$3.72/MMbtu in October 20133 and may continue to rise with three new liquefied natural gas plants

recently approved.

In terms of coal, Navigant analysis reveals executed and planned coal plant retirements through 2017

that exceed 37 GW. As this capacity is removed from the U.S. electric generation base, it will need to be

replaced by other power generation resources, including but not limited to natural gas and offshore

wind. As such, continued coal plant retirements could increase the demand for offshore wind plants in

the United States.

3 U.S. Energy Information Administration Daily Energy Prices, October 16, 2013

(http://www.eia.gov/todayinenergy/prices.cfm).

Offshore Wind Market and Economic Analysis Page 1 Document Number DE-EE0005360

1. Global Offshore Wind Development Trends

Since last year’s report, additional progress has been made to develop commercial and demonstration-

scale projects in U.S. waters, including the installation of the nation’s first pilot-scale, offshore wind

turbine. The University of Maine’s 20-kilowatt (kW) turbine, resting atop a prototype floating

substructure, began generating power in early June 2013. At the commercial scale, some projects that

were in early planning stages last year have progressed to a more advanced stage, while other advanced-

stage projects have been placed on hold or abandoned altogether. These changes reflect the continuing

technology, market, and policy uncertainty surrounding offshore wind power development in the

United States. To help address the particular technical challenges of developing projects in the United

States, the U.S. Department of Energy (DOE) announced seven Advanced Technology Demonstration

grants in December 2012, three of which will be selected for additional funding following their initial

feasibility assessments.

As the U.S. market moves forward, it will continue to respond to and reflect the general trends occurring

in the global offshore wind market. Through 2012 and into 2013, offshore wind technology has

continued along historical trends. Turbine sizes and plant capacities have continued to grow, and water

depth and distances to shore have increased. As projects move further from shore, taller and larger

turbines may allow developers to take advantage of better and more sustained wind resources, thereby

increasing capacity factors. On the other hand, these deeper waters and longer distances present new

challenges and opportunities for foundations, drivetrains, installation logistics, and operations and

maintenance (O&M). Time will tell how well initial U.S. projects align with those global trends in light of

region-specific wind resource and seabed conditions.

This section presents an overview of the global offshore wind market and illustrates several of these

trends in more detail. This analysis draws upon an offshore wind project database compiled from

existing project databases and an ongoing review of developer announcements and industry news

coverage.4 Note that, for planned projects, this data relies primarily on developer projections and news

reports and that the status and details of projects under development are subject to change.

4The authors would like to acknowledge Navigant Research (formerly BTM Consult [BTM]), Green Giraffe Energy

Bankers, and the National Renewable Energy Laboratory (NREL) for their contributions of project information they

had previously collected. In addition, the team relied on publicly available information from the 4C Offshore Wind

Farm Database (4C Offshore 2013) and the Global Wind Energy Council (GWEC 2013).

Offshore Wind Market and Economic Analysis Page 2 Document Number DE-EE0005360

Summary of Key Findings – Chapter 1

» There are approximately 5.3 gigawatts (GW) of offshore wind installations worldwide.

» Several potential U.S. projects have achieved notable progress in the past year, with

eleven projects now in advanced stages of development.

» The average nameplate capacity of offshore wind turbines installed globally each year

has grown from 2.88 megawatts (MW) in 2007 to 4.03 MW in 2012.

» Globally, offshore wind projects continue to trend further from shore into increasingly

deeper waters, resulting in correspondingly higher capital costs. In parallel, however,

larger turbine sizes and hub heights are contributing to higher reported capacity factors.

» Approaches to drivetrain configurations continue to diversify in an effort to improve

reliability and reduce exposure to volatile supplies of the rare earth metals required for

direct drive generators.

» Global trends suggest that U.S. projects are likely to continue facing difficulties in

securing financing.

Offshore Wind Market and Economic Analysis Page 3 Document Number DE-EE0005360

1.1 Global Offshore Wind Development

Historically, the offshore wind market has primarily focused on northwest Europe; however, the Asian

market has shown signs of increasing activity over the past three years. In 2012, more than 1,100 MW of

wind power capacity was added globally, bringing the cumulative global total to 5,284 MW. The

majority of capacity additions occurred in European countries, with the United Kingdom alone

accounting for 756 MW of new capacity.5 Figure 1-1 summarizes the historical growth of the global

offshore wind market.

Figure 1-1. Historical Growth of the Global Offshore Wind Market

Note: Shows capacity in the year it was installed but not necessarily grid-connected. Includes commercial, test,

and intertidal projects.

Source: Navigant analysis of data provided by NREL and BTM

5 Various sources use different approaches for reporting annual capacity estimates. Navigant’s approach has

historically reported MW capacity installed in a particular year, regardless of whether it has been connected to the

grid. Other sources (e.g., the European Wind Energy Association [EWEA]) report MW capacity based on the year in

which it is connected to the grid. As a result, estimates of annual capacity additions may vary. For example, EWEA’s

estimate for 2011 European capacity additions shows 866 MW (EWEA 2012a), while BTM’s shows only 366 MW.

This is likely a result of 500 MW installed in 2010 not being connected to the grid until 2011.

Offshore Wind Market and Economic Analysis Page 4 Document Number DE-EE0005360

While capacity additions in 2012 represented a large increase over 2011, it failed to surpass the pace of

capacity additions in 2010. Much of the downturn from 2010 to 2011 can be attributed to the effects of the

global financial crisis, and while the upward trend has resumed annual additions continue to fall behind

prior expectations. In Asia, China continues to lead in terms of capacity, with 113 MW added in 2012 and

365 MW of cumulative capacity.6 While China previously announced plans to install 5 GW of offshore

wind by 2015 (Global Wind Energy Council [GWEC] 2013), it appears decreasingly likely that the goal

will be achieved, with only 222 MW of new capacity expected for 2013.7 Table 1-1 provides a summary of

the current global offshore market in number of projects, cumulative capacity, and number of turbines

by country.

Table 1-1. Summary of Installed Global Offshore Capacity through 2012

Region Country

Number of

Operational

Projects

Total Capacity

(MW)

Total Number of

Turbines Installed

Asia

China 13 365 138

Japan 5 28 16

South Korea 2 5 2

Europe

Belgium 3 380 91

Denmark 16 875 406

Finland 3 32 11

Germany 7 286 69

Ireland 1 25 7

Netherlands 4 247 128

Norway 1 2 1

Portugal 1 2 1

Sweden 5 164 75

United Kingdom 24 2,874 850

Total 85 5,284 1,795

Note: Includes commercial and test projects. Individual phases of projects at a single site may be counted as

separate projects.

Source: Navigant analysis of data provided by NREL and BTM

As shown in Table 1-1, the United Kingdom continues to lead the market, with 2,874 MW, more than

half of global installed capacity. The European market will continue to grow rapidly over the next two

years, with projects under construction in 2013 in Belgium, Denmark, Germany, Sweden, and the United

Kingdom. In fact, these new and expanding projects will likely contribute to a record-setting year, with

up to 2,900 MW expected to be installed before the end of 2013 (mostly in Germany and the United

Kingdom).

6 Notably, 251 MW of that capacity comprises inter-tidal projects, some of which were installed using methods more

similar to land-based wind farms. 7 As of September 2013.

Offshore Wind Market and Economic Analysis Page 5 Document Number DE-EE0005360

Apart from China’s 365 MW in the Asia region, Japan and South Korea have installed a combined 33

MW of demonstration-scale projects, with more under construction or planned. Like China, other Asian

countries have announced ambitious plans for growing their offshore wind markets. Taiwan has set a

target of 600 MW by 2020 and 3 GW by 2030, while the South Korean government set a target of 1.5 GW

by 2019, with an eventual goal of 2.5 GW (GWEC 2013).

Despite announced goals and targets, uncertainty around the political, economic, and supply-chain

factors influencing the global offshore wind market causes various forecasts and predictions for future

activity to range widely. Published forecasts for cumulative global offshore wind capacity range from

approximately 40 GW to more than 75 GW by 2022 (IHS Emerging Energy Research 2012; BTM 2012;

Douglas-Westwood 2013).

1.2 U.S. Project Development Overview

Since the last edition of this report, several potential U.S. offshore wind projects have achieved notable

advancements in their development processes. In addition to two BOEM commercial lease auctions for

federal Wind Energy Areas (WEAs), other, later-stage, commercial-scale projects have made incremental

progress toward starting construction. On the demonstration project front, the DOE awarded seven

Advanced Technology Demonstration (ATD) project grants in December 2012 that will help address

ongoing challenges and cost barriers to offshore wind energy. In addition, in June 2013, the University of

Maine (in partnership with the DOE) installed the United States’ first offshore wind turbine, a 1/8-scale

pilot turbine on a floating foundation. This section provides an overview of these and other updates to

U.S. offshore wind project developments.

The United States is still awaiting the installation of its first commercial-scale offshore wind project;

however, several developers continue to push forward on previously announced project plans. While

several dozen potential projects have been announced over the past five years, this report focuses on

those that have reached what Navigant considers to be an advanced stage of development. This

“advanced stage” includes projects that have accomplished at least one of the following three milestones:

» Received approval for an interim limited lease or a commercial lease in state or federal waters

» Conducted baseline or geophysical studies at the proposed site with a meteorological tower

erected and collecting data, boreholes drilled, or geological and geophysical data acquisition

system in use

» Signed a power purchase agreement (PPA) with a power off-taker

Note that each of these criteria represents a requisite step that a project will take before it gains final

approvals and reaches the construction phase. Simply having achieved one of these milestones,

however, does not guarantee that a project will ultimately move forward, and any two projects

qualifying as “advanced” may have made different levels of progress relative to one another.

In addition, some advanced-stage projects may be relatively inactive, with little evidence (or at least

public announcements) that they are continuing to progress their development plans. Conversely, some

projects that are making visible progress have yet to achieve any of the milestones that would categorize

them as advanced stage.

Offshore Wind Market and Economic Analysis Page 6 Document Number DE-EE0005360

A map showing the announced locations, capacities, and recent activities for each of eleven advanced-

stage projects appears in Figure 1-2.

Note: One potential project (the Deepwater Wind Energy Center) spans federal waters off the coasts of

Massachusetts and Rhode Island; this map splits its estimated 1,000-MW capacity between the two states.

Source: Navigant analysis

These eleven projects represent 3,842 MW of planned capacity. As shown in the figure, roughly two-

thirds of this potential capacity lies in federal waters (i.e., typically outside a three-nautical-mile state

boundary). Notably, this represents a reversed trend from two years ago, when a greater share of

advanced-stage planned capacity lied within state waters. This shift arose in part from developments in

federal leasing activities, as well as a refocusing of development efforts in Texas state waters (the federal

water boundary in Texas lies further out at nine nautical miles). Table 1-2 provides additional details

about each of the eleven advanced-stage projects, including nameplate capacity, number of turbines,

turbine make and model, turbine capacity, water depth and distance to shore, status notes, and an

estimated completion date.

Figure 1-2. Proposed U.S. Offshore Wind Energy Projects in Advanced Development Stages by

Jurisdiction and Project Size

Offshore Wind Market and Economic Analysis Page 7 Document Number DE-EE0005360

Table 1-2. Summary of Advanced-Stage U.S. Projects

Project Name (State)

Proposed

Capacity

(MW)

Turbines

(#)

Distance

to Shore

(Miles)

Average

Water

Depth (m)

Projected

Turbine

Model

Status Notes

Target

Completion

Dateb

Block Island Offshore

Wind Farm (Deepwater)

(RI)

30 5 3 22 Siemens SWT

6.0-120 (6 MW)a

National Grid has agreed to a 20-year PPA. U.S. Army

Corps of Engineers environmental studies completed.

Submitted final state and federal permit applications in

October 2012. Developers recently proposed an alternate

location for the project’s export cable at Scarborough State

Beach after a proposed landing was rejected by the Town

of Narragansett.

2015

Lake Erie Offshore Wind

Project (Great Lakes)

(OH)

27 9 7 18 Siemens SWT-

3.0-101(3 MW)

Lease signed with state of Ohio. Invited to negotiate

contract with DOE for an initial award under the Wind

and Water Power Program in 2012. Geotechnical surveys

completed. DOE ATD grant recipient.

2015

Fisherman's Energy:

Phase I (Atlantic City

Wind Farm)(NJ)

25 5 3 11.5 XEMC-Darwind

XD115 (5 MW)

Fully permitted. Completion date unclear after the New

Jersey Board of Public Utilities denied a settlement

agreement between Fisherman's and the NJ Division of

Rate Counsel over concerns about the project’s potential

ratepayer impacts (July 2013). DOE ATD grant recipient.

2015

Cape Wind Offshore

(MA) 468 130 10 10

Siemens SWT

3.6-107 (3.6

MW)a

Approved for federal waters; commercial lease offered in

April 2010. Commenced geotechnical and geophysical

survey operations in July 2012. PPA in place for 77.5% of

project's power through National Grid and NStar (with

contingency that construction begins by end of 2015).

2016

Dominion Virginia Power

- Virginia Offshore Wind

Technology Advancement

Project (VA)

12 2 23.5 26 Alstom Haliade

6 MW

In February 2013, Dominion submitted an unsolicited

research lease application for an area off the coast of

Virginia. In September 2013, the group was the winning

bidder in the second competitive lease sale for an adjacent

U.S. offshore wind area. DOE ATD grant recipient.

2017

Fisherman's Energy:

Phase II (NJ) 330 66 7 17.5

XEMC-Darwind

XD115 (5 MW)

Received a meteorological tower rebate from the state and

began baseline surveys in August 2009. Has interim lease

for initial assessment of wind farm feasibility.

2018

Offshore Wind Market and Economic Analysis Page 8 Document Number DE-EE0005360

Galveston Offshore Wind

(Coastal Point Energy)

(TX)c

150 55-75 7 14.5 XEMC-Z72-2000

(2-2.75 MW)

Has lease from Texas General Land Office. Announced

intention to install a 750-kW test turbine. 2018

Baryonyx Rio Grande

Wind Farms (North and

South) (TX)c

1000 100-200 7.8 20.5 Siemens SWT

6.0-120 (6 MW)a

Received lease from Texas General Land Office in 2009.

Army Corps of Engineers environmental studies

underway. DOE ATD grant recipient.

2019

Garden State Offshore

Energy Wind Farm (NJ) 350 58-70 20 27 (5 or 6 MW)

Awarded interim limited lease; began baseline surveys in

2009. State funding pulled in October 2012 because of

inaction. Launched state-of-the-art buoy to study offshore

weather conditions in November 2012.

2019

Deepwater Offshore Wind

Energy Center 1000 167-200 20 40 (5 or 6 MW)

In August 2013, Deepwater was the winning bidder in the

first competitive lease sale for a U.S. offshore wind area. 2019

NRG Bluewater's Mid-

Atlantic Wind Park (DE) 450 150 12.7 20 3 MW

Received one of the first U.S. offshore leases (non-

competitive) from BOEM in October 2012 as part of

"Smart from the Start" program; however, Delmarva had

canceled a PPA for 200 MW of the power. The project

website states that the project is officially on hold, and it is

unclear whether Bluewater will develop or sell the

project.

2020

a) These projects have committed to a specific turbine with a turbine supply agreement in place. All other stated turbines are based on developer statements and may change.

b) Dates shown in this table are based on developer statements and Navigant analysis; they may change based on permitting, leasing, surveying, and other activities.

c) Leasing and permitting requirements for projects in Texas state waters do not involve the Federal Energy Regulatory Commission (FERC) or the BOEM Minerals Management

Service and may move more quickly than projects in federal waters.

Source: Navigant analysis based on published project information, developer statements and media coverage

Offshore Wind Market and Economic Analysis Page 9 Document Number DE-EE0005360

1.2.1 Forecast Capacity and Completion Dates

According to developer statements, seven of the eleven projects have target completion dates before the

end of 2018, and developers for three of the projects——Block Island, Cape Wind, and Fisherman’s

Energy I—continue to compete to be the first commercial-scale offshore wind farm online in U.S. waters.

Given global historical trends, however, it is unlikely that all eleven of these projects will achieve these

targets, due to delays, cancelations, or other regulatory or market issues. Viewing these projects in the

context of these global trends and assumptions about their rates of completion, Navigant expects that the

initial growth of the U.S. offshore market would follow a trajectory like that shown in Figure 1-3,

assuming all eleven of these projects ultimately move forward.

Figure 1-3. Growth Trajectory for U.S. Offshore Wind Based on Forecast Construction Dates

Source: Navigant analysis of collected project data

In addition to these advanced-stage projects, the DOE-supported ATD projects will continue to make

progress over the next few years. Their smaller scale, receipt of targeted federal support, and state

support may facilitate their installation and make them among the first projects in U.S. waters. Section

1.2.3 describes these projects in more detail.

1.2.2 Notable Developments in Advanced-Stage Projects

This section briefly highlights some of the key developments and advancements that have occurred in

the development of U.S. offshore wind projects since the last edition of this report.

Offshore Wind Market and Economic Analysis Page 10 Document Number DE-EE0005360

1.2.2.1 BOEM Advancements and Leasing Activities

The BOEM continued to make steady progress on its Smart from the Start initiative to facilitate siting,

leasing, and construction of offshore wind energy projects on the Atlantic Outer Continental Shelf.8

Notably, in October 2012, it issued its first non-competitive commercial lease to NRG Bluewater

Delaware for the intended site of its 450-MW Mid-Atlantic Wind Park. However, as noted in Table 1-2,

NRG’s anticipated initial off-taker, Delmarva Power, had previously cancelled its PPA for the project. It

is yet unclear what steps, if any, NRG will take to move the project forward.

In 2013, BOEM also made significant progress in assessing the suitability of and interest in each of six

WEAs. Under the initiative, BOEM selected these areas for expedited assessments and planning to help

facilitate development of projects along the Atlantic Coast. Figure 1-4 shows the location of each of these

six areas.

8 See http://www.boem.gov/Renewable-Energy-Program/Smart-from-the-Start/Index.aspx

Offshore Wind Market and Economic Analysis Page 11 Document Number DE-EE0005360

Figure 1-4. Map of BOEM Atlantic Wind Energy Areas

Source: BOEM 2012

BOEM has made initial progress in each of these areas by engaging local stakeholders and government

agencies, issuing requests for interest and calls for information for commercial developers and initiating

environmental studies. In mid-2013, it held its first two competitive auctions and awarded leases for two

of these WEAs. On July 31, 2013, Deepwater Wind New England LLC submitted the winning bid for two

leases within the Rhode Island/Massachusetts WEA, and it subsequently signed the lease on September

20. On September 4, 2013, Virginia Electric and Power Company (doing business as Dominion Virginia

Power) won the second BOEM competitive lease for the Virginia WEA. Award of each lease enables the

lessee to move forward with its site assessment plans and subsequent construction and operations plans.

Offshore Wind Market and Economic Analysis Page 12 Document Number DE-EE0005360

Since the fall of 2012, BOEM has also received and responded to several unsolicited lease requests for

project sites related to three of the DOE ATD projects. Key activities include the following:

» In December 2012, BOEM issued a notice of no competitive interest for a previously submitted

(October 2011), unsolicited commercial lease submitted by Statoil for a site in Maine related to its

Hywind demonstration project.

» In February 2013, the Commonwealth of Virginia Department of Mines, Minerals and Energy

(DMME), in partnership with Dominion Virginia Power, submitted its second unsolicited

research lease request for an area related to the Dominion ATD project.

» In May 2013, Principal Power submitted an unsolicited application for a site in Oregon for its

WindFloat Pacific Pilot Project

See Section 1.2.3 for additional information on each of these ATD projects.

1.2.2.2 Cape Wind – Focus on Financing and Year-End Construction Start

The 468-MW Cape Wind Offshore wind project has continued to press forward despite its long history

of public comment, technical reviews, and legal challenges. A significant milestone for the project was

the Massachusetts Department of Public Utilities’ approval of Cape Wind’s PPA with NSTAR in

November 2012. The NSTAR PPA is for 27.5 percent of Cape Wind’s power that, when combined with

National Grid’s PPA for 50 percent, represents the majority of the project’s output. Subsequent attention

turned to solidifying financing for the project, and developers confirmed a $200 million investment from

PensionDanmark, a Danish pension fund, in July 2013. The project has also indicated tentative

commitments from the Bank of Tokyo-Mitsubishi UFJ (which is coordinating the project’s financing) and

Siemens (the projects’ turbine supplier), but specific dollar amounts are not confirmed. Notably, the

PensionDanmark investment is conditioned on Cape Wind securing the remainder of its $2.6 billion

financing and beginning construction by the end of 2013, which is the deadline for the project to take

advantage of the federal Investment Tax Credit (Lindsay 2013, McKenna 2013).

1.2.2.3 Fishermen’s Energy I (Atlantic City Wind Farm) – Subsidies, Costs and Rate Impacts

As one of the other more advanced offshore projects, Fishermen’s Energy Atlantic City Windfarm was

making encouraging progress before encountering a series of decisions in 2013 that have further delayed

the proposed 25-MW pilot project. As the project sought to qualify for New Jersey ratepayer-funded

subsidies, the New Jersey Division of Rate Counsel has opposed the project, citing concerns about the

potentially high costs to ratepayers (Johnson 2013). In an attempt to reach a settlement on the issue, the

developers submitted a filing to the Division in March 2013, which the Division subsequently accepted

and endorsed to the New Jersey Board of Public Utilities (BPU). In mid-July, however, the BPU rejected

the settlement, citing several specific objections related to potential ratepayer impacts and benefits

(Milford 2013). The BPU gave the developers an opportunity to respond to the objections, but at the time

this report was published, no further agreements had been announced. Later that month, the Division of

Rate Counsel filed a reply brief to the BPU's position, affirming that the project meets the “net benefits”

test required by the Offshore Wind Economic Development Act (OWEDA) and urging the BPU to move

ahead with the project. This issue remained unresolved as of this report’s publication.

Offshore Wind Market and Economic Analysis Page 13 Document Number DE-EE0005360

Notably, Fisherman’s Energy I is also one of the DOE’s ATD project grant recipients; details of the

technological innovations it hopes to demonstrate appear in Section 1.2.2.3.

1.2.2.4 Block Island – Navigating Public Opposition

The third later-stage, advanced U.S. project, Deepwater’s 30-MW Block Island Offshore Wind Farm,

faced increasing public scrutiny and opposition in 2013. The project has completed its U.S. Army Corps

of Engineers environmental studies, submitted its requisite permits, and secured a 20-year PPA from

National Grid. In August 2013, the developers adjusted their plans after failing to gain approval from the

Town of Narragansett for the sale of easements for the originally planned location of the project’s

transmission line. (Campbell 2013). As of this report’s publication, Deepwater had announced a

proposed alternate site for the cable to come ashore at Scarborough State Beach and was awaiting

approval from the State Properties Committee (Kuffner 2013).

1.2.3 U.S. DOE Advanced Technology Demonstration Projects

This section provides a brief overview of each of the seven projects that have received DOE ATD grants.

As previously stated, the DOE will provide up to $4 million to each project to complete initial

engineering, planning, and feasibility assessments. The DOE will then select up to three of the projects to

receive additional funding to help carry the projects through final design, fabrication, and installation.

Note that some of these projects meet Navigant’s advanced-stage project criteria and appear in Table 1-2.

1.2.3.1 New England Aqua Ventus I

The DeepCwind Consortium, a team led by the University of Maine (UMaine), has proposed a pilot

floating offshore wind farm of two 6-MW, direct-drive turbines on concrete, semi-submersible

foundations near Monhegan Island, Maine. As mentioned previously, the UMaine separately partnered

with the DOE to install and connect a 1/8-scale prototype floating turbine to the grid on June 13, 2013.

The 65-foot-tall prototype was designed and fabricated at UMaine; assembled at Cianbro's facility in

Brewer, Maine; and towed nearly 30 miles from Brewer to Castine, Maine, by the Maine Maritime

Academy. The prototype is anchored off the coast of Castine in approximately 24 meters of water and is

the first grid-connected offshore wind platform in the Americas.

The Consortium will use the data acquired during the deployment of the prototype to optimize the

design of UMaine's VolTurnUS floating turbines (patent pending). The VolTurnUS turbines utilize

floating concrete foundations that the Consortium anticipates will result in improvements to

commercial-scale production and provide offshore wind projects with a cost-effective alternative to

traditional fixed steel foundations. Once scaled to full size and incorporating economies of scale (based

on the number of turbines), the team hopes to reduce the cost of offshore wind to a point that it can

compete (without subsidies) with other forms of electricity generation.

On August 30, 2013, UMaine filed a bid with the Maine Public Utilities Commission (PUC) to provide

long-term power to the grid. As of this report’s writing, anticipated next steps were for the PUC staff to

review the proposal and request supplemental information prior to asking UMaine to develop a term

Offshore Wind Market and Economic Analysis Page 14 Document Number DE-EE0005360

sheet or contract. The PUC plans to decide whether to award UMaine a long-term contract before

December 31, 2013.

1.2.3.2 Hywind Maine

Statoil North America of Stamford, Connecticut, planned to deploy four 3-MW wind turbines on floating

spar buoy structures approximately 19 miles offshore in the Gulf of Maine in approximately 140 meters

of water. These spar buoys will be assembled portside (to help reduce installation costs versus

constructing offshore) in Boothbay Harbor, Maine, and then towed to the installation site to access the

Gulf of Maine's extensive deep water offshore wind resources. The Hywind Project follows Statoil's first

Hywind demonstration project off the coast of Norway; in 2009, Statoil installed a single 2.3 MW turbine

(with an 82-meter rotor diameter) on a spar buoy with 100-meter draft to test the effects of wind and

waves on a floating turbine. The project has produced 15 megawatt-hours (MWh) since startup in 2010.

In January 2013, the Maine PUC voted to support a term sheet for a 20-year PPA with Central Maine

Power Company. However, the project was placed on hold in July 2013 after new legislation created

uncertainty regarding the state's prior approval of the project. That approval had included the Maine

PUC’s agreement for the project to receive ratepayer-funded subsidies after Statoil submitted the only

bid in the state’s competitive process. In late June, the Maine legislature passed a bill that re-opened the

bidding process for the ratepayer subsidies and UMaine submitted a similar proposal for the Aqua

Ventus project. On October 15, 2013, citing increased uncertainty created by the change in legislation, as

well as more general schedule challenges, Statoil announced its intent to abandon the Hywind Maine

project and focus its floating offshore wind efforts on a proposed demonstration in Scotland.

1.2.3.3 Fisherman’s Energy I (Atlantic City Wind Farm)

As described in Section 1.2.2.3, Fishermen’s Energy proposes to install five 5-MW, direct-drive turbines

in state waters 2.8 miles off the coast of Atlantic City, New Jersey. The project will result in an advanced,

bottom-mounted foundation design and innovative installation procedures that aim to mitigate potential