Next Generation TV Panel Technology and Market Trends 2020

31

From Technologies to Markets © 2020 From Technologies to Markets © 2020 Next Generation TV Panel Technology and Market Trends 2020 – Market and Technology Report 2020 Sample

Transcript of Next Generation TV Panel Technology and Market Trends 2020

From Technologies to Markets

© 2020

From Technologies to Markets

© 2020

Next Generation TV Panel

Technology and Market Trends 2020

–Market and Technology

Report 2020

Sample

2

About the authors

Companies cited in this report

Comparisons with 2019 report

Acronyms

Context

Objective of the report

Content

Structure of the report

Glossary 16

o LCD basics

o LCD vs OLED

o Panels vs TVs

o Panel substrate generation and size

o Display resolutions

Executive summary 23

Context 76

o Emerging TV features

o Advanced TV features: 2020 status

o Volume and revenue by price band

Market forecast - Supply and demand analysis 83

o Looking back at 2019

o Recent events

o LCD panel price trends

o LCD capacity attrition:Who fills the vacuum?

o 2019-2021 LCD capacity scenario

o China Subsidies

o China won the LCD TV battle

o China LCD strategy: Not a first!

o 2018-2024 TV panel area capacity forecast by technology

o 2018-2024 TV panel area capacity forecast by region

o 2018-2024 TV panel area capacity forecast by company

o 2018-2024 TV panel area capacity forecast by fab generation

o Covid-19 impact overview

o Covid-19 impact: Macro-economic Data

o Covid-19 impact: Demand Side

o 2018-2026 TV sets volume forecast- Size breakdown

o 2018-2026 TV panels area forecast – Size breakdown

o 2018-2026 TV sets forecast – Technology breakdown

o 2018-2024 supply vs demand analysis

o Conclusions:A shifting industry landscape

Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

TABLE OF CONTENTS

Part 1/6

3

Competitive landscape - Company strategies 112

o Overview of TV panel makers fab locations

o TV panel maker market share (volumes)

o AU Optronics (TW)

o BOE (CN)

o CEC Panda (CN)

o TCL CSOT (CN)

o HKC (CN)

o Foxconn / Innolux / Sakai Display / SIO (TW/JP/CN)

o LG display (KR)

o Samsung (KR)

Technology landscape 141

o Many technologies

o LCD and OLED

o Scorecards

o Evolution

o New self emissive technologies

LCD upgrades 149

Quantum dot enhancement films (QDEF) 150

o What is a quantum dots

o Photo-luminescent vs electro-luminescent

o LCD display structure

o Benefits

o Implementations

o QD films: Structure and requirements

o Quantum dot film price evolution

o Perovskite

o Quantum dot films SWOT

o Supply chain status and trends

o Other players

Narrowband phosphors 166

o Notch filters

o Narrowband phosphors

o PFS - Possible limitations

o Desired phosphor improvement

o Other solutions: Bandpass filters

MiniLED backlights 172

o Introduction: LCD backlight dimming

o Local dimming – Evolution

o Dimming zones and number of LEDs

o Examples: 75” 2019-2020 commercial models

o Local dimming challenges

o Increasing the number of leds

o From FALD to miniLED backlights

o MiniLED benefits

Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

TABLE OF CONTENTS

Part 2/6

4

o MiniLED key design elements

o LED type and die size

o Circuit board types

o Assembly

o Challenges

o Driving: Passive Or active matrix

o Illustration: A 4576 zone passive matrix backlight

o Transition to active matrix?

o MiniDrivers and MOSFET transistors

o MiniLED TV examples

o Number of zones vs LEDs

o TCL miniLED timeline

o Power consumption

o Summary: Design and performance trade offs for miniLED BLU

o Example of 75” miniLED BLU cost structure projections

o 75” TV cost comparison: WOLED vs miniLED LCD

o Conclusions

o Supply chain – Key players

o MiniLED SWOT

Dual cell LCD 206

o Overview

o Cost

o Discussion

o Examples

o Power consumption

o Status & timeline

o Discussion

o Dual cell SWOT

OLED 216

o AMOLED display structure

o RGB OLED

o White OLED (WOLED)

o Top emission / Bottom emission

o OLED materials

o OLED emitter materials: Front runners

o Inkjet printed RGB OLED

o OLED materials for inkjet printing

o Inkjet printing tools for display manufacturing

o Inkjet printing: Potential cost benefits

o RGB inkjet vs WOLED evaporation process comparison

o Inkjet printed RGB TV prototypes

o Inkjet printed RGB OLED – Key players and supply chain

o JOLED: First to volume manufacturing

o JOLED Prototypes and commercial panels

o Status

o RGB OLED SWOT

Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

TABLE OF CONTENTS

Part 3/6

5

QD-OLED 235o From QD color filters to Qd-OLED

o Benefits and challenges

o Example: QD materials

o Status

o QD-Materials

o QD-OLED SWOT

QNED 243o Timeline

o Frontend: Nanorod fabrication

o Nanorod structure and dimensions

o Backend: QNED display structure & assembly

o QNED vs QD-OLED

o QNED vs “standard” microLED

o QNED: The third path?

o Challenges

o Status

o QNED SWOT

Summary: OLED company strategies 255

Electroluminescent quantum dots (EL-QD) 261o Introduction

o Potential benefits vs RGB OLED

o Challenges

o EL-QD material status

o Hybrid OLED/Electroluminescent QD

o Status and major players

o Electroluminescent QD SWOT

MicroLED 271

o Potential benefits

o Assembly

o Challenges

o The assembly challenge

o Major types of microLED transfer and assembly processes

o The die size challenge

o Implications for performance and manufacturability

o MicroLED industry status

o Intellectual property activity trends

o Leading applicant ranking

o Trends per company type

o Panel makers

o Supply chain overview

o Supply chain requirements and maturity level

o TV: Blurring the frontier between TV and videowalls

o MicroLED TV: Sony, Samsung and LG

Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

TABLE OF CONTENTS

Part 4/6

6

o Samsung designs

o Challenges for tiled displays

o Scenario for MicroLED Adoption in TV

o Possible disruption: QNED

o MicroLED SWOT

Manufacturing synergies between the various emerging TVtechnologies 291

o Quantum dot patterning

o Inkjet printing

o Alternative to inkjet printing: Organic vapor jet printing

o TFT backplane

TV features 302

Large panels 303

o Size vs price

o Generation 8.5 substrate cuts

o Generation 10.5 substrate cuts

o List of G10.X Fabs

o Options for large panels

o Multi modal glass cut

o Examples of Gen 8.5 and 10.5 multi mode glass cut

o “Jumbo” TV: 90” and above

o MicroLED modular displays

o Laser TV (short throw projectors)

8K 320

o Panel size, viewing distance and field of view

o Angular resolution

o Illustration: 85” TV

o Is 8K needed?

o Current challenges for 8K: Building the plane while flying?

o Illustration: Bandwidth

o Current challenges for 8K

o Content availability for different platforms

o Upscaling

o 8K challenges for LCD: Power consumption

o 8K challenges for LCD:TFT and drivers

o 8K challenges For OLED:Top and bottom emission

o 8K adoption trends

o 8K association

o TV panel resolution forecast 2018-2026

o Comparison against previous forecast

o 8K breakdown by panel size 2018-2026

o Discussion

o Key players: Panel and TV brands

Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

TABLE OF CONTENTS

Part 5/6

7

Better pixels: Contrast and color 341

o The “better pixel”

o The UHD Alliance

Wide color gamut 345

o Color gamut: standard LED LCD TVs

o UHD Alliance requirements

o ColorVolumes

o Status: Emitter types

o Wide color gamut technology benchmark

o OLED resonant micro-cavities

o Color gamut performance of commercially available TV

o Performance of commercially availableTV: Color gamut

o Performance of commercially availableTV: Color volume

o Quantum dot film and narrowband phosphor adoption

o Major TV makers’ wide color gamut technologies

o Wide color gamut forecast and technology breakdown 2018-2026

o Discussions: Possible disruptions

High Dynamic Range 363

o High Dynamic Range (HDR)

o Viewers’ preference

o UHD Alliance requirement

o Transfer function

o Tone mapping - Signal delivery

o Major HDR delivery standard

o HDR ecosystem – 2020 update

o Challenges for display

o Examples

o OLED vs LCD

o Summary

o HDR vs HDR compatible

o HDR TV volume forecast 2018-2026

Discussion 381

o Contrast or color?

o Trends

o The best of both worlds?

o OLED and LCD

o Emerging self emissive technologies

o Technology roadmap for High-End TV

o Conclusions

Yole Développement presentation 400

Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

TABLE OF CONTENTS

Part 6/6

8Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

ABOUT THE AUTHORS

Biographies & contacts

EricVirey, PhD.

Eric Virey, PhD. serves as a Principal Display Market and Technologies Analyst within the Photonics, Sensing & Display division at Yole Développement (Yole).

Eric has spoken in more than 50 industry conferences over the last 10 years and has been interviewed or quoted in multiple media including: The Wall Street Journal, CNN, Fox News, CNBC, Bloomberg, Financial Review, Forbes, Technology Review, etc.

Prior to joining Yole, Eric held R&D, engineering, manufacturing and marketing positions with Fortune 500 Company Saint-Gobain in France and the United States. Eric received a PhD in Optoelectronics from the National Polytechnic Institute of Grenoble. He is based in Portland, OR.

Contact: [email protected]

Zine Bouhamri, PhD.

As a Technology & Market Analyst, Displays, Zine Bouhamri, PhD is a member of the Photonics, Sensing & Display division at YoleDéveloppement (Yole).

Zine manages the day to day production of technology & market reports, as well as custom consulting projects. He is also deeply involved in the business development of the Displays unit activities at Yole.

Previously, Zine was in charge of numerous R&D programs at Aledia. During more than three years, he developed strong technical expertise as well as a detailed understanding of the display industry. He is author and co-author of several papers and patents. Zine holds an Electronics Engineering Degree from the National Polytechnic Institute of Grenoble (France), one from the Politecnico di Torino (Italy), and a Ph.D. in RF & Optoelectronics from Grenoble University (France).

Contact: [email protected]

99

Apple, Asus, AU Optronics, Avantama, BOE, CEC Panda, Changelight, Changhong, CHOT, CNC, CSOT,

Cynora, Dolby, Dupont, eFun, Efonlong, Eizo, Electech, eLux, Epileds, Epistar, Excellence Opto, Exciton,

Flanders Scientific, Foxconn, Funai, GE/Current, Haier, Hansol, Harvatek, HC Semitek, Hisense, Hitachi

Chemical (AKA Showa Denko Materials), HKC, HongLi, Huawei, Innolux, Intematix, JOLED, Kateeva,

KDX, Kinglight, Konka, Kulicke & Soffa, Kyulux, Lextar, LG Display, Loewe, Lumenari, MnTech, Nanjing

Tech, Nanoco, Nanophotonica, Nanosys, Nationstar, Nexdot, NHK, Nichia, Nitto Kolon, Panasonic,

Philips, PixelDisplay, Playnitride, Quantum Materials, Refond, Rohinni, Sakai Display (SDP/SIO), Samsung

Display, Samsung Visual Display , Sanan, Semes, Sharp, ShineOn, Skyworth, Sony, Sumitomo Chemical,

Taiwan Nanomaterials, TCL, Tianma, Toshiba, TPV, Unijet, Universal Display, Vestel, Vizio, Wahong, X-

Celeprint / Xdisplay (XDC), Xiaomi, and more.

Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

COMPANIES CITED IN THIS REPORT

10Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

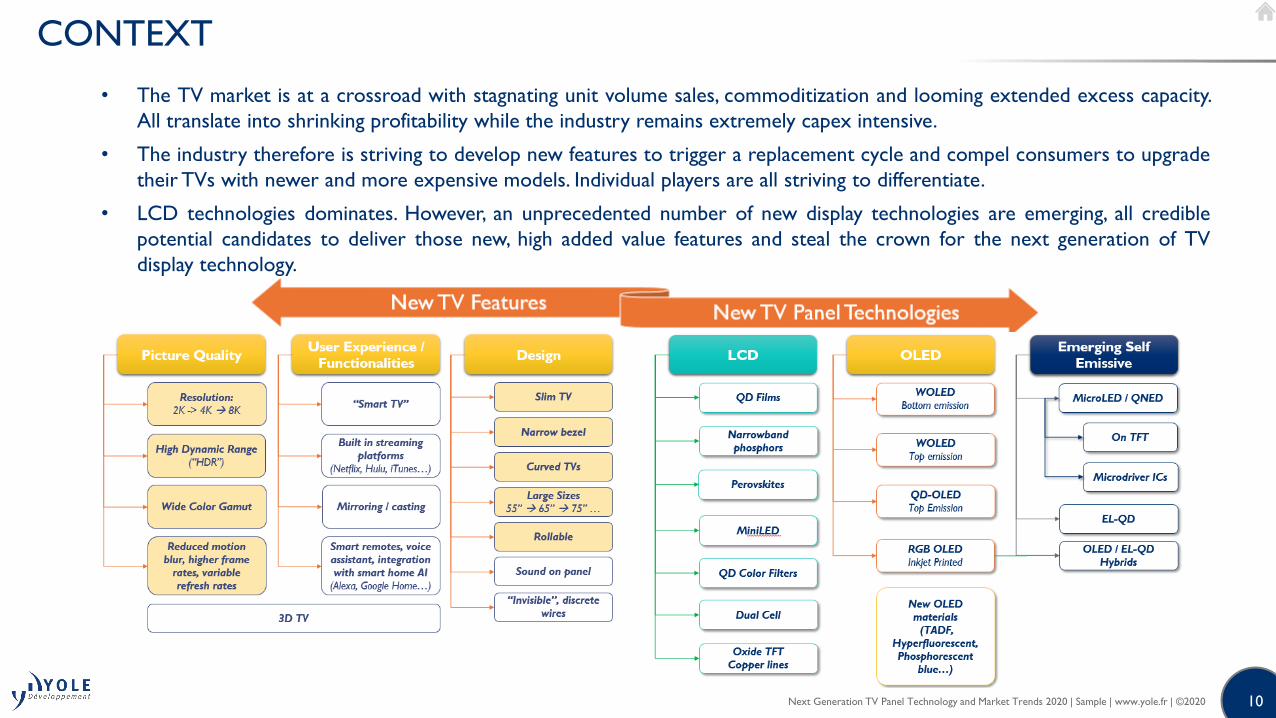

CONTEXT

• The TV market is at a crossroad with stagnating unit volume sales, commoditization and looming extended excess capacity.

All translate into shrinking profitability while the industry remains extremely capex intensive.

• The industry therefore is striving to develop new features to trigger a replacement cycle and compel consumers to upgrade

their TVs with newer and more expensive models. Individual players are all striving to differentiate.

• LCD technologies dominates. However, an unprecedented number of new display technologies are emerging, all credible

potential candidates to deliver those new, high added value features and steal the crown for the next generation of TV

display technology.

11Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

OBJECTIVE OF THE REPORT

The objective of the report is to provide an update of the TV panel industry landscape (trends and forecast, supply and

demand…), present and analyze new TV features, understand which technologies are best positioned to deliver them, and

look at the intersections to understand the impact and possible strategies for panel makers

Present and analyze new TV features

expected to compel consumers to

upgrade their TV

Present and analyze emerging display

technologies and determine how well

positioned they are to serve each of the

new desired TV features

Analyze the intersection of new features and emerging technologies:

what are the implications in terms of panel makers’ strategies,

technological and manufacturing choices and impact on the supply chain.

Which are the best technologies? Who owns or champions them? Which ones will dominate ?

What manufacturing strategies are deployed by individual panel makers?

How can Korean and Chinese manufacturers defend against the rise of Chinese manufacturers?

What are the capacity constraints? Over-spending risks? Etc.…

TV panels market forecast by size and technology / supply and demand analysis / company strategies

12Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

CONTENT

Technologies

• Quantum Dot Films

• Quantum Dot Color filters

• Perovskite

• Narrowband phosphors

• Notch Filters

• Dual Cell LCD

• miniLED

• microLED and QNED

• WOLED

• RGB OLED

• QD-OLED

• EL-QD

TV features

For each:

Trends, adoption rates,

technology breakdown and volume

forecast.

Other analysis

• Large panel capacity

analysis and trends:

breakdown by technology,

company, substrate size

(fab generation), country [1].

• Key player strategies for

technology and

manufacturing.

• Large panel sizes

• Resolution: 4K → 8K

• Wide color gamut and color

volume.

• High dynamic range (black

levels and peak brightness,

HDR delivery).

• Not covered: 3D, refresh

rates

For each:

Detailed description, key

players, supply chain, SWOT

analysis.

[1]: Data from Yole display fab database.

13Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

SAMSUNG AND LG LCD EXIT RESTORES HEALTHIER SUPPLY DEMAND BALANCE

Samsung

+ LG

LCD exit

Together, LG Display and Samsung Display are expected to remove more than 50m m2 of panel start capacity.

BOE, CSOT and HKC are ramping up their recently built fabs, but no new investment is expected beyond HKC’s Gen 8.6 “H5”.

With OLED also ramping up more slowly than anticipated after LG postponed its G10.5 fab in Korea, the overall supply and demand balance

could become tight as soon as 2021.

May 2019 Forecast

14Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

2019-2021 LCD CAPACITY SCENARIO

XXX

- X m m2

XXX

- X m m2

XXX

+ X m m2

XXX

+ X m m2

XXX

-16.7m m2

XXX

+X m m2

XXX: +X m m2

Others: -X m2

XXX:

-X m m2

• Complete XXX and XX fabs ramp up: +XX million m2

• Complete XXX ramp up: XX million m2

• Assumes acquisition of CEC Panda XX fabs: + XXm m2

• Assumes acquisition of XXX fab : +XX million m2.

• Finish XXXXXXX fabs ramp. Build XX fab in XX.

• Stop XXXXX

• Keep XXXXXXXXXX

• XXXXXXXXXXX

• Assumes fab sold to XXXX

• Resume XXXXXXXXXXX

• Assumes XXXXXXXXXXXXX sold to XX

• e.g.: Panasonic exit LCD manufacturing

Minus

XXm

m2

Plus

XXm m2

Others: +X m m2

2019-2021

LCD variation:

-XX m m2

Zero sum game:

This scenario assumes that

…………………………

…………………………

…………………………

…………………………

…………………………

…………………………

…………………………

…………………………

…………………………

…………………………

…………………………

…………………………

…………………………

…………

1515

2018-2024 TV PANEL AREA CAPACITY FORECAST BY COMPANY

Chinese companies BOE and CSOT are set to dominate. Scenario assumes that CEC Panda fabsare acquired in late 2020 by CSOT.

Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

[1]: For G5 and G6: only fabs known to produce large panels are included in the total (most Gen 6 and below fabs are used for mobile applications, automotive, industrial and

other small size panels). SIO G10.5 fab in China counted as “Foxconn/sharp/Sakai.

1616

AN OVERALL FLAT TV MARKET

The TV market has been essentially flat since the end of the cathode ray tube replacement cycle at the beginning of the decade.

Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

• The TV market has been essentially flat since the end of the cathode ray tube replacement cycle. The industry faces

lower margins and slower growth. It needs ways to compel consumers to upgrade often fairly-recent flat panel TVs

and spend more on newer models.

• Through the past decade, a variety of design and technological improvements have been introduced. While some have

allowed TV makers to combat price erosion, none were disruptive enough to trigger a major replacement cycle akin

to the transition from CRT to flat panel. The industry must therefore keep developing more, new and compelling

features.

-

50

100

150

200

250

300

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 (F)

Mill

ion U

nits

Flat Panel Shipments

(Plasma, LCD, OLED only – Excludes Cathod Ray Tubes)

Resolution: 1k → 2k

(HD→ FHD)

LED backlight

(also enabled

thinner

displays)

3D TVs

Resolution:

2K → 4KCurved TV

HDR, Wide

Color Gamut

= UHD

Resolution:

8K

17Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

TV DEMAND TRENDS AND FORECAST BY FEATURE 2019-2026

Large size panels and adoption of new higher added value features will help the industry alleviate a massive margin crunch

[1]: per UHD alliance criteria

18Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

ADVANCED TV FEATURES: 2020 ADOPTION STATUS

Current and future industry battlegrounds

LED backlight

XXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

Emerging Growing Mature

XXXX

Slim:

OLEDXXXX

Adoption in 2020

(% of total TV sold annually)

Status

2019

2009

Curved TVs

3D TVs [2] ?

[2]: Possible come back in the long-term if glass-free

technology development successful.

20172014

2017

2006

2012

2014

20072006

Keys for the graph:

• Date = first introduction of the feature

• Highlighted: panel-technology-related (otherwise:

driven by TV set electronics and software)

• Adoption dynamic of the features:

2016

2014

2014

XXXX

50%

100%

0%

[1]: HDR compatible: accept HDR signal but panel technology doesn’t

allow proper reproduction per UHD consortium requirements

Fast growth

Slow growth, Stagnating

Decreasing

100%

2020

19Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

MANY TECHNOLOGIES COMPETING TO DELIVER ADVANCED FEATURES

Established On-RoadmapEarly-stage prod / Pilot In Development

Other

self-

emissive

&

projection

Note: curved arrows highlight synergies and commonalities between different emerging technologies

LCD

OLED

AKA XXX

20Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

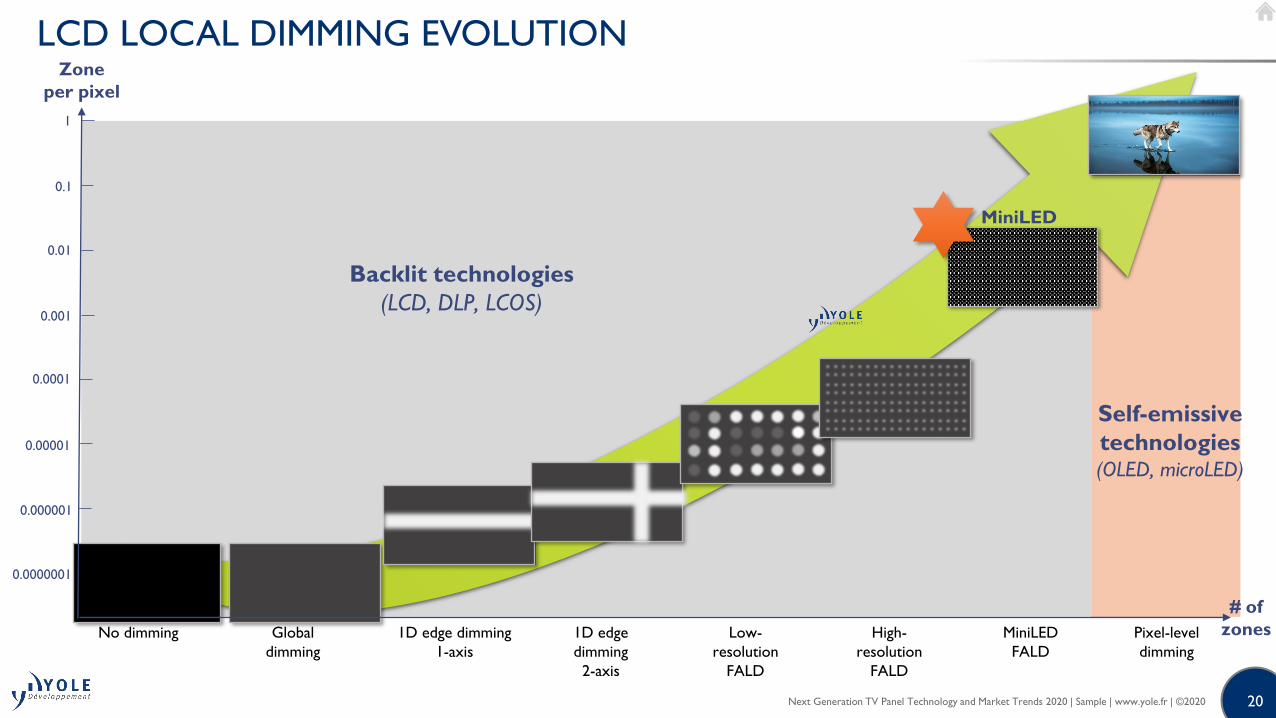

LCD LOCAL DIMMING EVOLUTION

1D edge dimming

1-axis

1D edge

dimming

2-axis

Low-

resolution

FALD

High-

resolution

FALD

Pixel-level

dimming

MiniLED

FALD

No dimming Global

dimming

# of

zones

Zone

per pixel

1

0.1

0.01

0.001

0.0001

0.00001

0.000001

0.0000001

Backlit technologies

(LCD, DLP, LCOS)

Self-emissive

technologies(OLED, microLED)

MiniLED

2121

TECHNOLOGY BREAKDOWN FORECAST

Entry level LCD keep dominating in term of volumes.

Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

2222

TV PANEL MAKER MARKET SHARE (VOLUMES)

XXXXXXXXXXXXXXXXXXXX

Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

2323

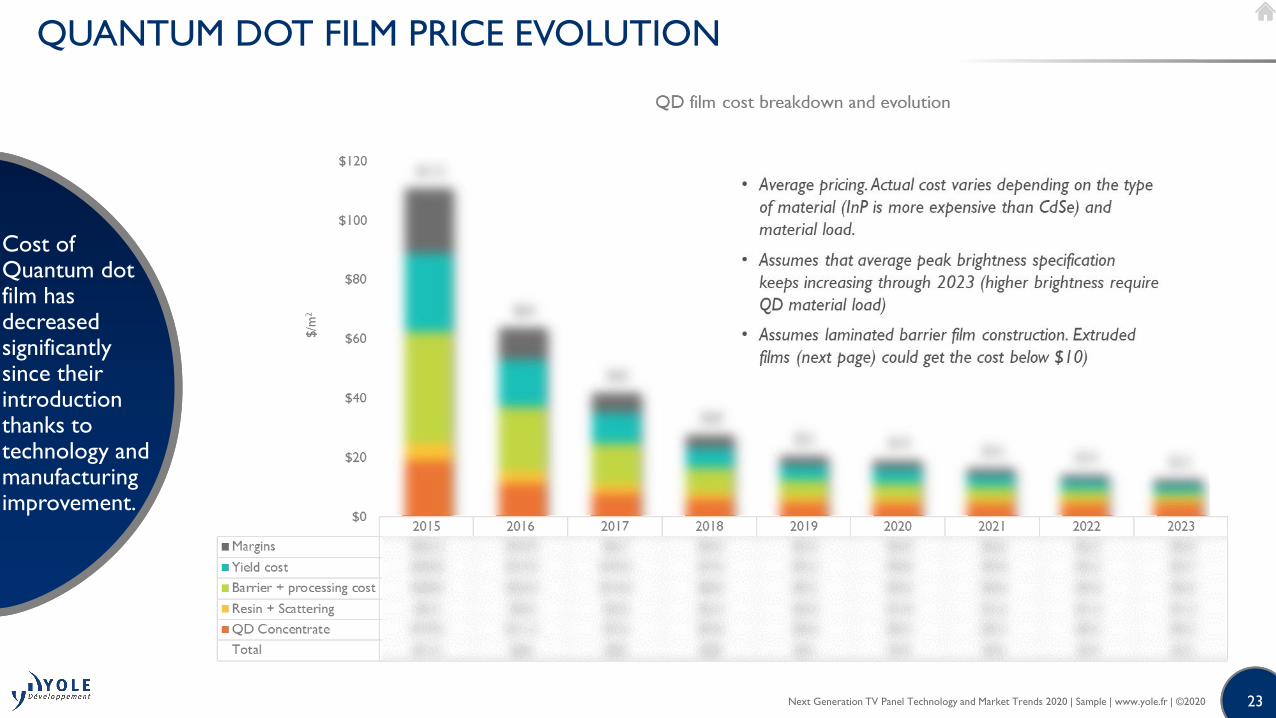

QUANTUM DOT FILM PRICE EVOLUTION

Cost of Quantum dot film has decreased significantly since their introduction thanks to technology and manufacturing improvement.

Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

24Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

ILLUSTRATIONS: NUMBER OF ZONES VS LEDS

The industry is far from having converged in term of design choices:

10k zones / 100k+ chips seem to be the end game to deliver OLED-like performance and good

efficiency, thermal management.

1 000

10 000

100 000

1 000 000

- 2 000 4 000 6 000 8 000 10 000 12 000

Num

ber

of LED

s

Number of Zones

2525

EXAMPLE OF 75” MINILED BLU COST STRUCTURE PROJECTIONS

With this architecture, the AM backplane, miniLEDs and the light management films in the BLU are the leading cost contributors. Other architectures could lead to different results (e.g.: mini--drivers)!

Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

[1]: reflector, DBEF etc.

[2]: drivers, frame, PCB strip for the FALD, flexible edge connectors etc.

Key hypothesis:

$XX

26Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

QNED FRONTEND FABRICATION: NANOROD PROCESS FLOW

2727

SAMSUNG MINI AND MICROLED DESIGNS

Samsung Visual Display is sending confusing messages by using 2 very distinct technologies and architectures and branding them both “MicroLED”.

Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

The Wall

miniLED

75” / 150”

microLED

1st year shown 2018 2019

Application Videowall/luxuryTV High end TV

Die size XX µm ~XX µm

Die supplier XX XX

Module material PCB LTPS TFT

Assembly Die bonder Proprietary mass transfer

Driving Passive matrix, discrete ICs Active matrix TFT

Individual module size XX mm XX

Individual module resolution XX XX

Pixel pitch 0.84 mm (30 PPI) 0.43 mm (59 PPI)

Display resolution

Depends on size:

146”=4K

292”: 8K

Depends on size:

75”: 4K

150”: 8K

2828

CURRENT CHALLENGES FOR 8K

The entire content production and delivery chain needs to define and adopt common standards and practices to enable improved image quality for all viewers.

Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

Content creation

Production -encoding

Distribution/ broadcasting

Display

• Digital cameras

• Editing

• Codecs (HEVC, VCC…)

• Connectivity (HDMI, DisplayPort,

wireless.)

• Streaming

• Blu-ray

• Broadcasting

• Set-top boxes

• TVs

• Tablets

• Laptops

• Smartphones

29Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

UHD ALLIANCE REQUIREMENTS

Content creation

Production -encoding

Distribution/ broadcasting

Display

The UHD Alliance adopted Rec. 2020 as a long-term, future-proof color standard for encoding and distribution and

the smaller digital cinema DCI P3 gamut to measure display reproduction capabilities.

BT. 2020 gamut with a 10-bit depth

(1,024 levels for each R,G,B primary,

for a total of more than 1B colors [1])

Must be able to handle signal encoded in BT2020

but minimum requirement for color reproduction is

90% of the DCI P3 gamut [2].

[1] Previous standard for HD TVs was 8 bits, i.e. 256 levels per primary, for a total of 16.8M colors.

[2] Requirement for professional displays used for content mastering is 100% of DCI P3 in order to ensures that colorists will see the content as shown in digital theatres.

Rec. 709:

Current HD

TV

DCI P3

BT2020

Mastering, encoding and distribution

Displays

30

Contact our

Sales Team

for more

information

30

Contact our

Sales Team

for more

information

MicroLED Displays 2019

Next Generation TV Panel Technology and Market Trends 2020 | Sample | www.yole.fr | ©2020

Yole Développement

MicroLED Displays – Intellectual Property Status & Landscape 2020

Next Generation 3D Displays 2019

Displays and optics for AR & VR 2020 (available in April 2020)

YOLE GROUP OF COMPANIES RELATED REPORTS

MiniLED Displays 2019

31About Yole Développement | www.yole.fr | ©2020

CONTACTS

FINANCIAL SERVICES

› Jean-Christophe Eloy - [email protected]

+33 4 72 83 01 80

› Ivan Donaldson - [email protected]

+1 208 850 3914

CUSTOM PROJECT SERVICES

› Jérome Azémar, Yole Développement -

[email protected] - +33 6 27 68 69 33

› Julie Coulon, System Plus Consulting -

[email protected] - +33 2 72 17 89 85

GENERAL

› Camille Veyrier, Marketing & Communication

[email protected] - +33 472 83 01 01

› Sandrine Leroy, Public Relations

[email protected] - +33 4 72 83 01 89

› General inquiries: [email protected] - +33 4 72 83 01 80

Western US & Canada

Steve Laferriere - [email protected]

+ 1 310 600 8267

Eastern US & Canada

Chris Youman - [email protected]

+1 919 607 9839

Europe and RoW

Lizzie Levenez - [email protected]

+49 15 123 544 182

Benelux, UK & Spain

Marine Wybranietz - [email protected]

+49 69 96 21 76 78

India and RoA

Takashi Onozawa - [email protected]

+81 80 4371 4887

Greater China

Mavis Wang - [email protected]

+886 979 336 809 +86 136 6156 6824

Korea

Peter Ok - [email protected]

+82 10 4089 0233

Japan

Miho Ohtake - [email protected]

+81 34 4059 204

Japan and Singapore

Itsuyo Oshiba - [email protected]

+81 80 3577 3042

Japan

Toru Hosaka – [email protected]

+81 90 1775 3866

Follow us on

REPORTS, MONITORS & TRACKS