NestléFull Year Results 2007 Full Year Results Roadsho · 16 2007 full year results roadshow –...

66

2007 full year results roadshow – February 2008 Full Year Results Roadshow

Transcript of NestléFull Year Results 2007 Full Year Results Roadsho · 16 2007 full year results roadshow –...

2007 full year results roadshow – February 2008

Nestlé Full Year Results 2007

Name of chairman

Full Year Results Roadshow

2 2007 full year results roadshow – February 2008

Disclaimer

This presentation contains forward looking statements which reflect Management’s current views and estimates. The forward looking statements involve certain risks and uncertainties that could cause actual results to differ materially from those contained in the forward looking statements. Potential risks and uncertainties include such factors as general economic conditions, foreign exchange fluctuations, competitive product and pricing pressures and regulatory developments.

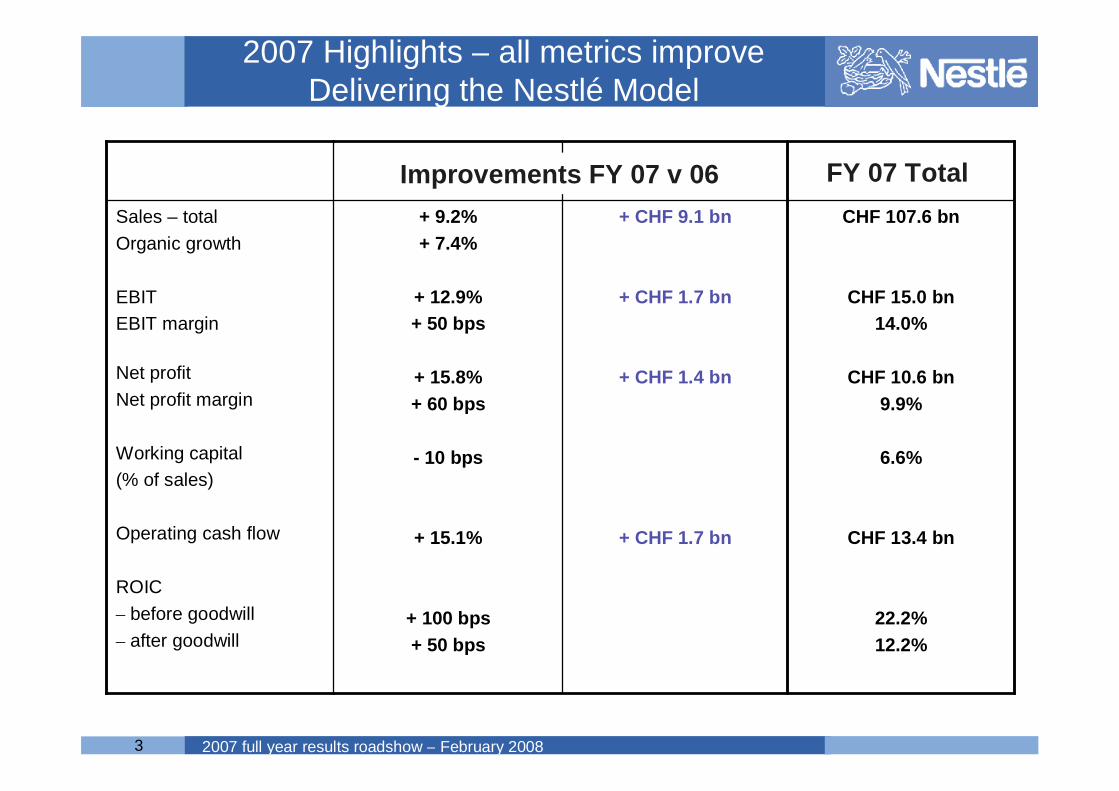

3 2007 full year results roadshow – February 2008

+ 9.2%+ 7.4%

+ 12.9%+ 50 bps

+ 15.8%+ 60 bps

- 10 bps

+ 15.1%

+ 100 bps+ 50 bps

CHF 107.6 bn

CHF 15.0 bn14.0%

CHF 10.6 bn9.9%

6.6%

CHF 13.4 bn

22.2%12.2%

+ CHF 9.1 bn

+ CHF 1.7 bn

+ CHF 1.4 bn

+ CHF 1.7 bn

Sales – totalOrganic growth

EBITEBIT margin

Net profitNet profit margin

Working capital (% of sales)

Operating cash flow

ROIC– before goodwill– after goodwill

Improvements FY 07 v 06 FY 07 Total

2007 Highlights – all metrics improveDelivering the Nestlé Model

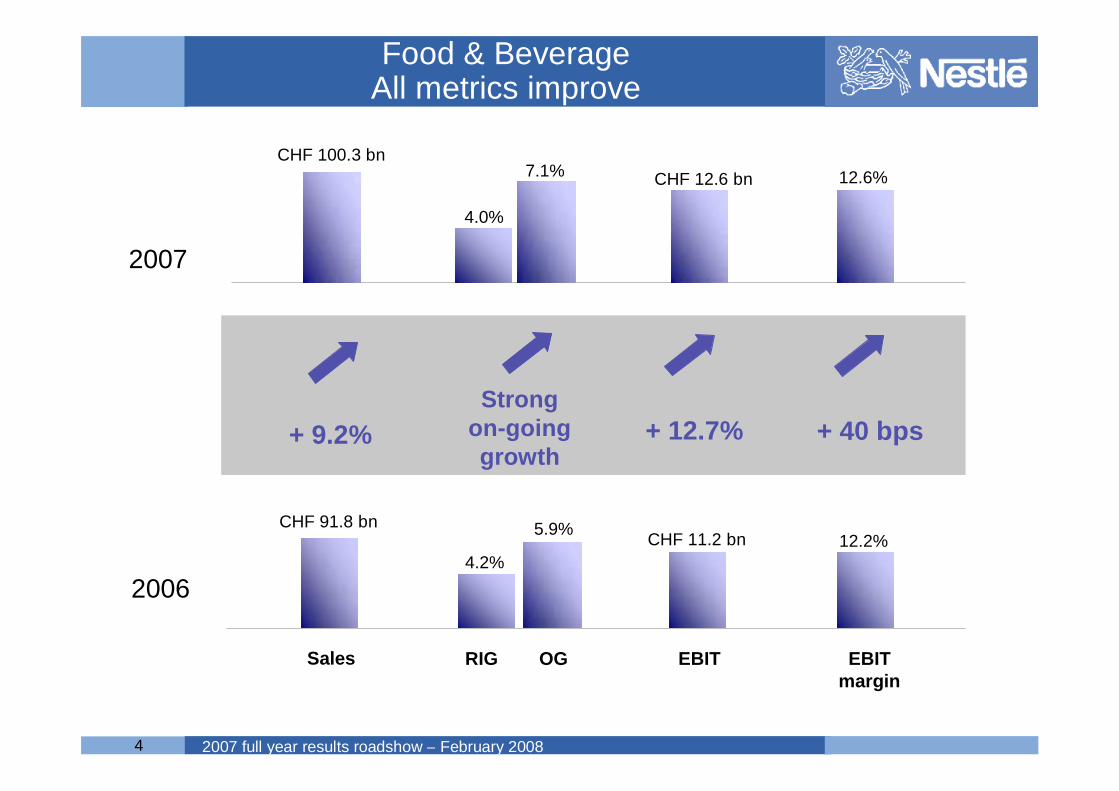

4 2007 full year results roadshow – February 2008

Food & BeverageAll metrics improve

2007

2006

RIG OG EBIT margin

Sales

CHF 100.3 bn

CHF 91.8 bn

+ 9.2% + 40 bps

12.6%

12.2%

Strongon-goinggrowth

4.0%

7.1%

5.9%

4.2%

EBIT

+ 12.7%

CHF 12.6 bn

CHF 11.2 bn

5 2007 full year results roadshow – February 2008

Total Performance Management

Growth & Value of GrowthGrowth & Value of Growth

Scale BenefitsScale Benefits

Operational EfficienciesOperational Efficiencies

Channel DevelopmentChannel Development

Region DevelopmentRegion Development

Skills & CompetencesSkills & Competences

Delivering long term sustainable performance improvement

6 2007 full year results roadshow – February 2008

The Nestlé Model

EBIT margins correspond to published figures – not restated for accounting changes

% Organic Growth1996 1997 1998 1999 2001 2002 20032000 2004 2005 2006 2007

5.2%

6.4%

5.1% 4.5%

6.2% 6.2%

7.4%

5.1%

6.9%

3.8%

5.4%4.9%

EBIT margin

10.2% 10.3% 10.3%11.1%

11.8% 11.8%12.3% 12.5% 12.6% 12.9%

13.5%14.0%

7 2007 full year results roadshow – February 2008

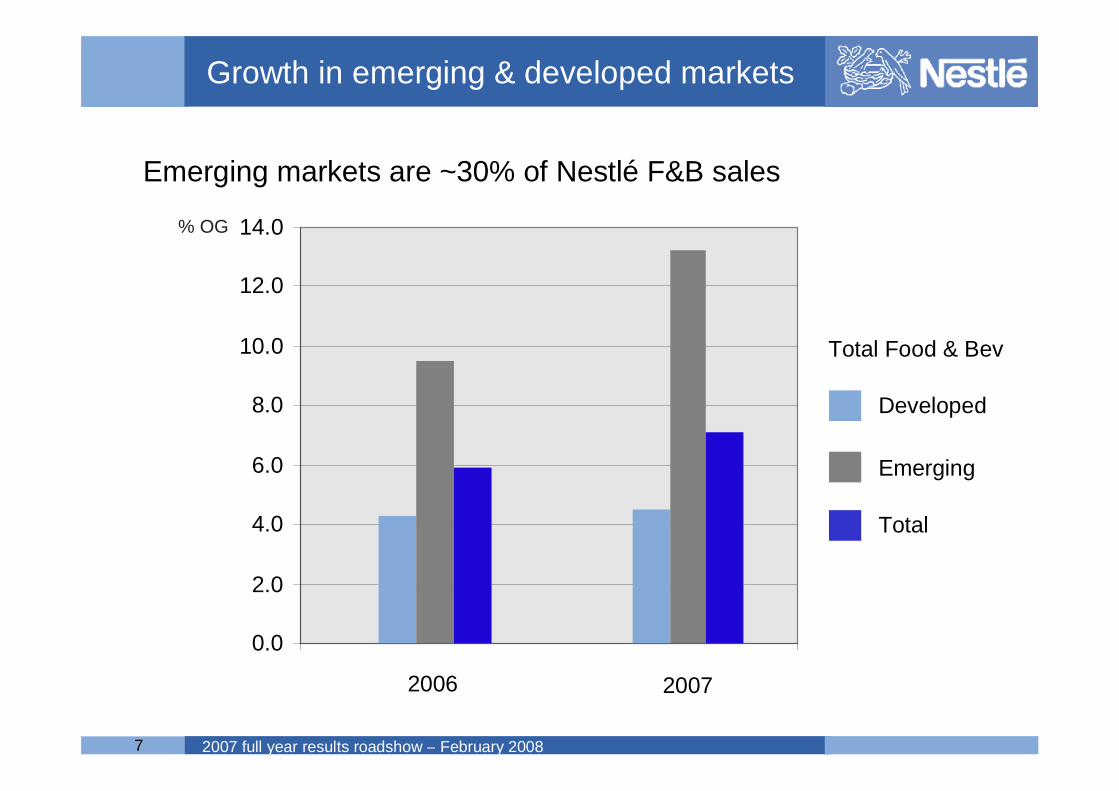

Growth in emerging & developed markets

2006 2007

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Developed

Emerging

Total

Emerging markets are ~30% of Nestlé F&B sales

Total Food & Bev

% OG

8 2007 full year results roadshow – February 2008

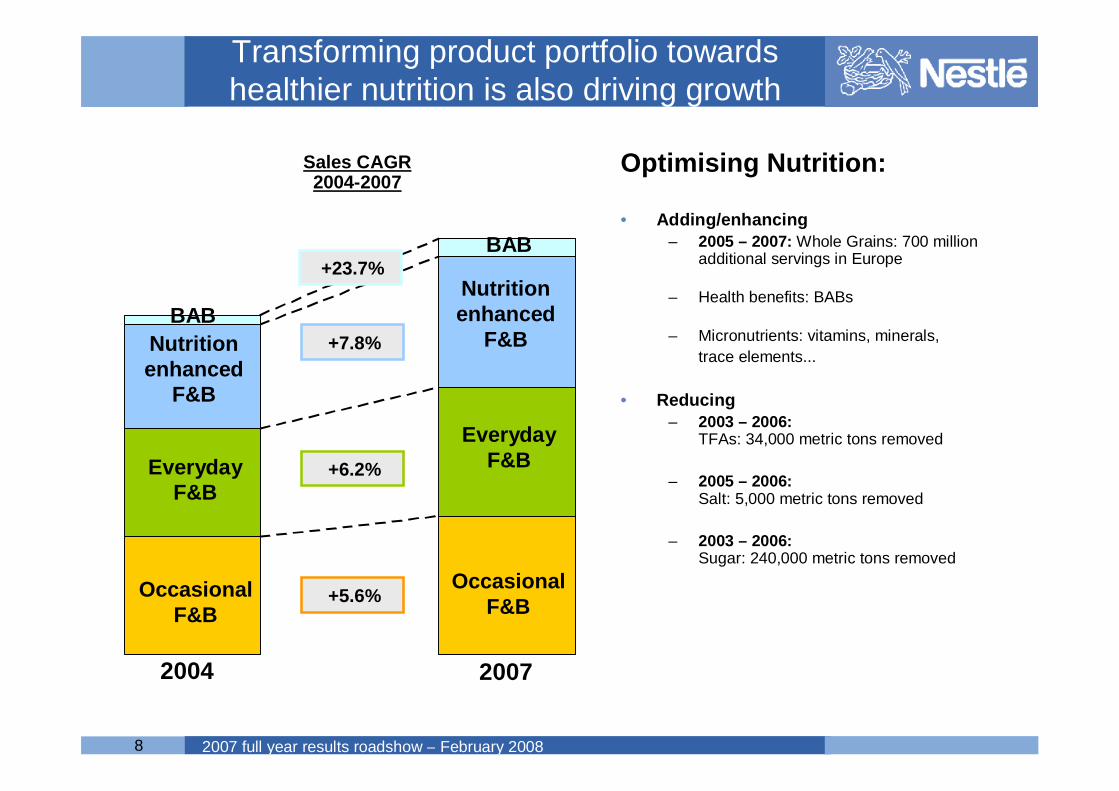

Transforming product portfolio towards healthier nutrition is also driving growth

Optimising Nutrition:

• Adding/enhancing– 2005 – 2007: Whole Grains: 700 million

additional servings in Europe

– Health benefits: BABs

– Micronutrients: vitamins, minerals,trace elements...

• Reducing– 2003 – 2006:

TFAs: 34,000 metric tons removed

– 2005 – 2006:Salt: 5,000 metric tons removed

– 2003 – 2006:Sugar: 240,000 metric tons removed

2004 2007

Sales CAGR 2004-2007

+23.7%

+7.8%

+6.2%

+5.6%Occasional F&B

Everyday F&B

Nutrition enhanced

F&B

BAB

Occasional F&B

Everyday F&B

Nutrition enhanced

F&B

BAB

9 2007 full year results roadshow – February 2008

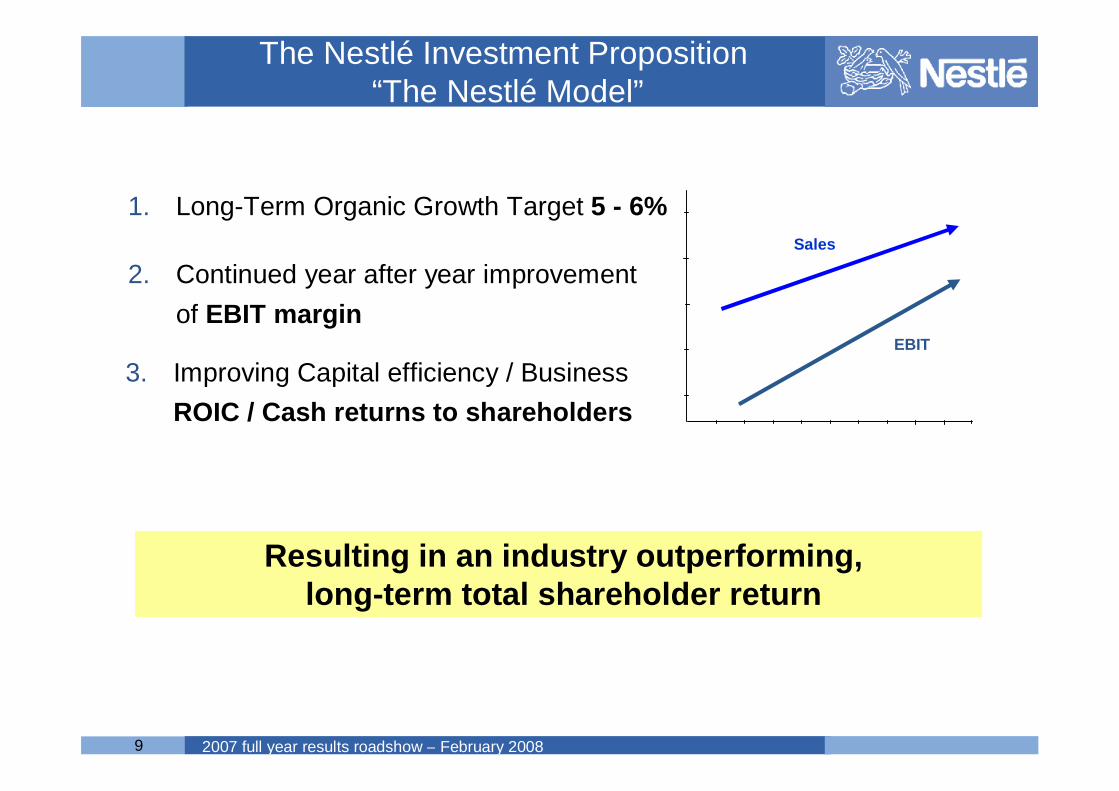

The Nestlé Investment Proposition“The Nestlé Model”

1. Long-Term Organic Growth Target 5 - 6%

Resulting in an industry outperforming, long-term total shareholder return

2. Continued year after year improvement of EBIT margin

3. Improving Capital efficiency / Business ROIC / Cash returns to shareholders

EBIT

Sales

10 2007 full year results roadshow – February 2008

• Discipline driving performance

• Operational control

• Leveraging scale and skills

• Strategy and performance

Focus areas

11 2007 full year results roadshow – February 2008

Discipline driving performance

• Discipline, increased transparency and excellence in execution are material influences on the 2007 results

• Underperformers improved overall, especially Ice cream, European PetCare: 10 bps contribution to Group EBIT margin

• Working capital improved by 10 bps despite strong growth and raw material cost pressure

• Cash conversion cycle improved by 7 daysAll areas contributed

12 2007 full year results roadshow – February 2008

Discipline driving performance

• 10% reduction in SKUs in 2007

• 10% improvement in bad goods

• Simplifying structures (200 fewer legal entities)

• CHF700mn excess real estate disposed over 3 years

Focus areas for 2008 include

• Leverage scale & skills – overheads

• Reduced working capital as % of sales

• Underperformers and SKU reduction

13 2007 full year results roadshow – February 2008

Leveraging scale

Industrial Performance TeamIndustrial Performance Team

European PurchasingEuropean Purchasing

Regional Treasury CentresRegional Treasury Centres

Supply Chain Optimisation TeamSupply Chain Optimisation Team

Strategic Generating Demand UnitStrategic Generating Demand Unit

Global Media BuyingGlobal Media BuyingStrategic Business UnitsStrategic Business Units

Innovation Acceleration TeamInnovation Acceleration Team

Global Nestlé Business ServicesGlobal Nestlé Business Services

Enabled by GLOBE Leveraging best practices, efficiencies, skills & know-how

Global Business Excellence TeamGlobal Business Excellence Team

14 2007 full year results roadshow – February 2008

GNBS contributing to profitable growth

Expand

Standardize & Streamline

Get-in

§ Transition "as-is" activities to NBS

§ Full accountability for service delivery with NBS

§ One global best-in-class end-to-end solution

§ Optimized retained organizations

§ New Markets

§ New Services

§ Scale...

§ ...resulting in consolidation savings

§ Process improvement...

§ ...resulting in lower cost

§ Business focus on demand generation...

§ ...resulting in profitable growth

Stage

Focus

Outcome

15 2007 full year results roadshow – February 2008

Update on GLOBE

• GLOBE Objectives changed from:

• Implementation of harmonized NestléBusiness Excellence Best Practice

• Implementation of Data Standards and Data Management –"Managing Data as a Corporate Asset"

• Implementation of standardized information systems & technology

To:

• Move from "Best in Nestlé" to "Best in Class" best practices confirmed with external benchmarking

• Move from historical/explanatory reporting to forward looking/real time/predictive information with a greater focus on customers and consumers

• Enable a fast, focused and flexible "front line" with a slim, cost efficient "back-line"

16 2007 full year results roadshow – February 2008

Operational control

• Balance sheet optimisation within "Gold Standard" parameters –minimise cost of capital

• Controls – oversight of Nestlé marketsDevolved responsibility balanced by controls

• Guardian of shareholders' interests –Use of funds, returns hurdles, risk policies, etc

• GLOBE brings improved transparency, greater speed, and enhanced benchmarking

• The opportunity is to leverage best in class practices, to share excellence in execution and to enhance discipline – continuous improvement

17 2007 full year results roadshow – February 2008

The role of Finance

• Finance is central to value creationby identifying opportunities for performance improvement

• Finance is central to value protectionthrough controls, systems, governance

• Focus on maximising long term total shareholder return

18 2007 full year results roadshow – February 2008

Differentiating strategies

Benchmark & Fix Benchmark & Fix ObjectivesObjectives

Focus & ImplementFocus & ImplementMeasure & TrackMeasure & Track

Responsibility, Responsibility, LeadershipLeadership

to get Resultsto get Results PerformancePerformanceManagementManagement

CycleCycle

Differentiating Differentiating StrategiesStrategies

2007 full year results roadshow – February 2008

Nestlé Full Year Results 2007

Name of chairman

Full Year Results Roadshow

Name of chairman2007 full year results roadshow – February 2008

Nestlé Full Year Results 2007

Name of chairman

2007 full year results roadshow

Delivering the NestléModel in 2008

Driving performance longer term

Name of chairman2007 full year results roadshow – February 200821

Agenda

Ø The last decade

Ø 2008 – another year of the Nestlé Model

Ø Beyond 2008 – opportunity rich

Name of chairman2007 full year results roadshow – February 2008

Creating...

Transforming...

Delivering...

Rewarding...

Nestlé – The Last Ten Years

Name of chairman2007 full year results roadshow – February 200823

The transformational opportunity

Organisational• Creating an agile fleet of

businesses/markets• Efficient support

structure • Increased focus on

demand generation

Strategic• Towards Nutrition,

Health& Wellness

The "What" The "How"

Name of chairman2007 full year results roadshow – February 2008

Creating…

Nestlé has evolved from Food & Beverage

to create

the global leader in Nutrition, Health and Wellness

60/40+

Name of chairman2007 full year results roadshow – February 200825

...independently strong and flexible, following their own rules for success,

with business specific knowledgeable management.

...an agile fleet of businessesFrom super-tanker to…

Transforming…

Name of chairman2007 full year results roadshow – February 200826

Delivering... (The Nestlé Model)

Ø Sustainable Organic Growth of 5 - 6% 12 year average = 5.9%CHF 60bn to CHF 107.6bn

Ø Annual improvement of EBIT margin 12 year average = 35 basis points to 14%CHF 6.2bn to CHF 15bn

Ø Total cash returned to shareholdersCHF 36bn in 12 years

Name of chairman2007 full year results roadshow – February 200827

Rewarding...

CHF

TSR of 408%

Over CHF 150bn of incremental value

since 1996

Name of chairman2007 full year results roadshow – February 2008

• The right strategy• Performance is trending higher

Creating...Transforming...Delivering...Rewarding...

Our mission is to build on that success– Deliver the strategy– Enhance financial performance

We intend to make Nestlé the referencefor both Nutrition, Health & Wellness

and for Financial Performance

Name of chairman2007 full year results roadshow – February 200829

Agenda

Ø The last decade

Ø 2008 – another year of the Nestlé Model

Ø Beyond 2008 – opportunity rich

Name of chairman2007 full year results roadshow – February 2008

Market concerns• Raw material costs• Impact of high energy costs• Recession – impact on consumer

demand & companies' ability to price• Fall-out from sub-prime

2008: Achieving the Nestlé Model despite tough market conditions

Nestlé's commitment in 2008 To deliver the Nestlé Model

Name of chairman2007 full year results roadshow – February 2008

• By delivering our strategyNutrition, Health & WellnessBillionaire Brands

• By being the best in executionSpeed & DisciplineOperational efficiency

• Management priorities

2008: Achieving the Nestlé Model despite tough market conditions

Name of chairman2007 full year results roadshow – February 200832

F&B “Billionaire Brands” representabout 70% of F&B sales

Name of chairman2007 full year results roadshow – February 2008

• By delivering our strategyNutrition, Health & WellnessBillionaire Brands

• By being the best in executionSpeed & DisciplineOperational efficiency

• Management priorities

2008: Achieving the Nestlé Model despite tough market conditions

Name of chairman2007 full year results roadshow – February 200834

• Businesses need to "earn the right" to belong – underperformers, lower performing or commoditised categories and SKUs

• Overheads, total delivered costs, trade spend, etc

• Focus on bigger brands – spend, R&D, resource

• Rewards structure

Speed & Disciplinedriving financial performance

Name of chairman2007 full year results roadshow – February 200835

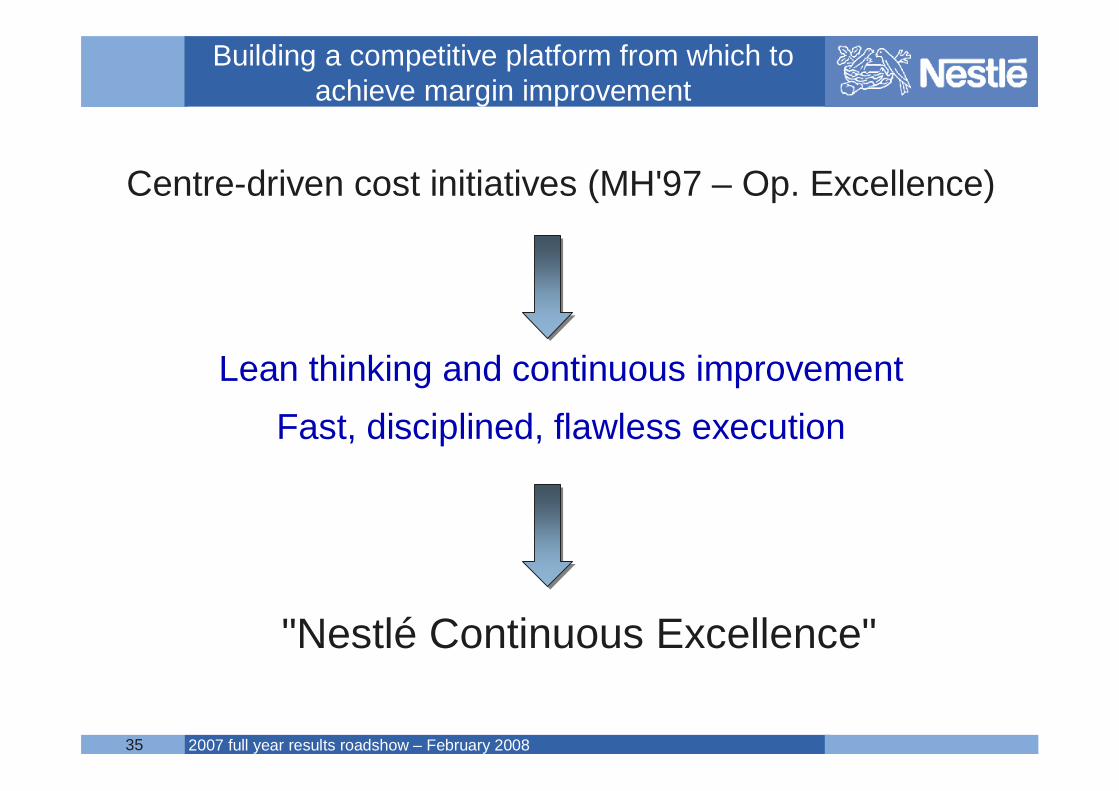

Centre-driven cost initiatives (MH'97 – Op. Excellence)

Lean thinking and continuous improvementFast, disciplined, flawless execution

"Nestlé Continuous Excellence"

Building a competitive platform from which to achieve margin improvement

Name of chairman2007 full year results roadshow – February 200836

CI

MH'97

• Continuous Improvements

Target 2004+

• Functional Targets out of Best Practice

• Restructuring the Industrial Network

Optimizing Total Delivered Cost by...

• Aligned targets across the Supply Chain

• Integrated Distribution and Industrial Networks

• Continuous Improvement culture

OperationEXCELLENCE 2007

An average CHF1 billion a year savings

From centre-driven initiatives

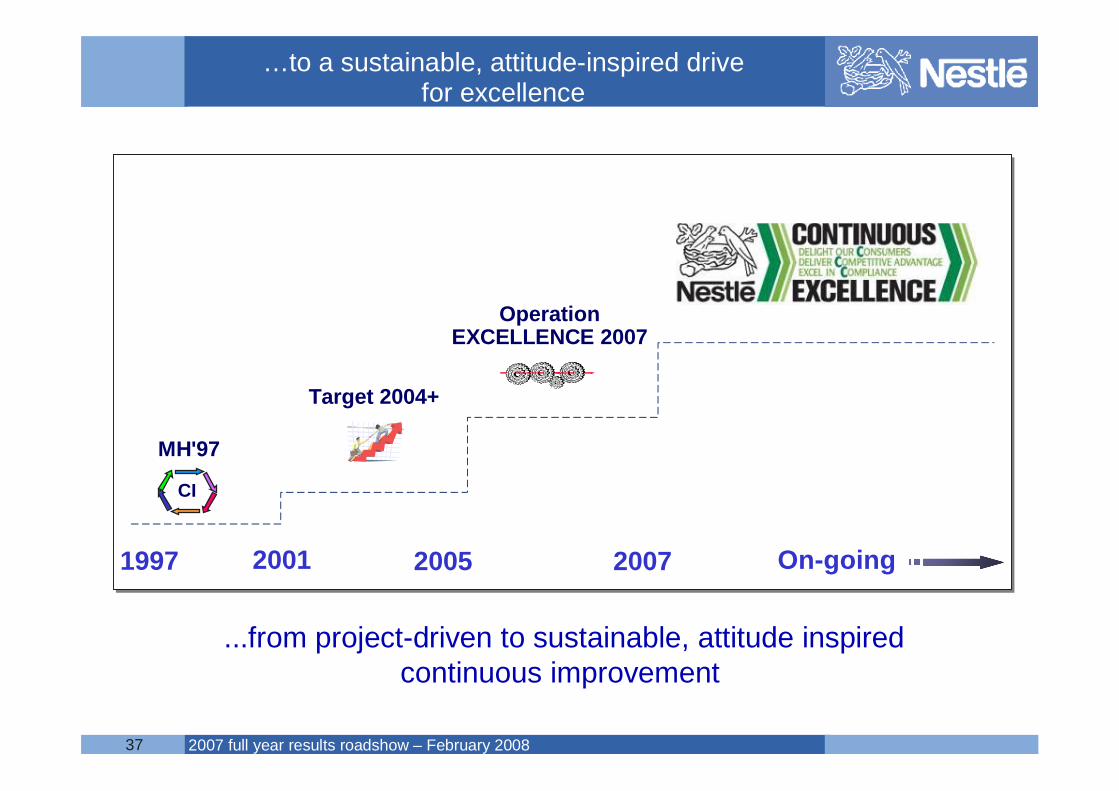

Name of chairman2007 full year results roadshow – February 200837

...from project-driven to sustainable, attitude inspired continuous improvement

CI

MH'97

Target 2004+

OperationEXCELLENCE 2007

1997 2001 2005 2007 On-going

…to a sustainable, attitude-inspired drivefor excellence

Name of chairman2007 full year results roadshow – February 200838

Deliver CCompetitive Advantage

Delight our CConsumers

Excel in CCompliance

...and create a sustainable attitude inspired approach

Eliminate Supply Chain

Losses

Eliminate Factory Losses

Engage 160’000 people

Outstanding Leadership Capability

FullOperationsCompliance

Value Stream Optimization (VSO)

Total Performance Management (TPM)

Organization Alignment

Leadership

Foundation Building Blocks

Performance Improvements

One Nestlé operating model:Nestlé Continuous Excellence

Name of chairman2007 full year results roadshow – February 200839

Raw MaterialConsumer Customer Distribution Centres Manufacturing Packaging Material

VSO : Consumer focused flow optimization across the full value chain (including R&D)

TPM

Zero Error

Zero Loss

Zero Waste

... ensures high performance equipment

Upstream Input...Downstream Input...

~85% of our people in Operations work in factories. ~82% of our delivered costs are linked to factories.

Continuous Excellence across the wholevalue chain

Name of chairman2007 full year results roadshow – February 200840

• 55% reduction in absenteeism

• 33% reduction in consumer complaints

• 50% reduction in waste

• 20% reduction in change-over time

• 70% reduction in unplanned stoppages

• 15% increase in line efficiency

• 15% reduction in rework

Pilot results show scale of opportunity

Name of chairman2007 full year results roadshow – February 200841

• Nestlé has a proven ability to drive efficiencies

• Nestlé Continuous Excellence takes us to a new level:

– combines best practices from different industries

– reaches from supplier to customer; service focused

– goes beyond cost to working capital & other KPIs

• GLOBE provides transparency, discipline,

measurement, faster decision making

Operational efficiencies provide a competitive base for margin improvement

Name of chairman2007 full year results roadshow – February 200842

• An enhanced demand-focused organisationNetwork structure, rapid decision making, leveraging scale, complexity with efficiency

• A flexible network structureImprove agility/service levels in marketsContinuous excellence to drive out costs

• A mentality of continuous improvementPride in "flawless" executionPerformance culture & rewards

Discipline enhanced by GLOBE

Name of chairman2007 full year results roadshow – February 2008

• By delivering our strategyNutrition, Health & WellnessBillionaire Brands

• By being the best in executionSpeed & DisciplineOperational efficiency

• Management priorities

2008: Achieving the Nestlé Modeldespite tough marketing conditions

Name of chairman2007 full year results roadshow – February 200844

Four objectives• RIG & organic growth (5-6%)• Increased EBIT margin

(constant currency)

• Reduce working capital• Improve ROICOperational priorities – with internal targets• Improve returns on trade spend• Operational efficiency & reduced overheads

The Nestlé Model

2008: Management prioritiesDriving financial performance

Name of chairman2007 full year results roadshow – February 200845

Agenda

Ø The last decade

Ø 2008 – another year of the Nestlé Model

Ø Beyond 2008 – opportunity rich

Name of chairman2007 full year results roadshow – February 200846

• Four competitive advantages

• Four growth areas

• Four Pillar strategy

Beyond 2008:Nestlé is opportunity rich

Name of chairman2007 full year results roadshow – February 200847

• Product and brand portfolio

• The industry's leading R&D capability

• Unmatched geographic presence

• People, culture, values, attitude

Beyond 2008:Four competitive advantages

Name of chairman2007 full year results roadshow – February 200848

Food, Nestlé Nutrition,Dairy, CPW, BPW, Chocolate, Confectionery & Biscuits, Ice cream, Nestlé Waters, NestléPurina PetCare

Protection

WeightManagement

Skin Health &Beauty

Healthy Recovery

Growth &Development

Digestive Comfort

Performance

Healthy Ageing

Relevant categoriesNestlé Nutrition, Coffee & Beverages, Dairy, CPW, Ice cream

innéov, Coffee & Beverages, Dairy, BPW, Nestlé Waters

Nestlé Nutrition

Nestlé Nutrition, NestléPurina PetCare, Coffee &

Beverages,Dairy, Ice cream

Dairy, Nestlé Nutrition,Nestlé Purina PetCare

Nestlé Nutrition, Ice cream, Chocolate, Confectionery &

Biscuits, Coffee & Beverages, Nestlé Waters

Nestlé Nutrition,Chocolate,

Confectionery & Biscuits, Dairy, Food,Coffee & Beverages,

Nestlé Purina PetCare

Consumer Benefit Areas

Name of chairman2007 full year results roadshow – February 200849

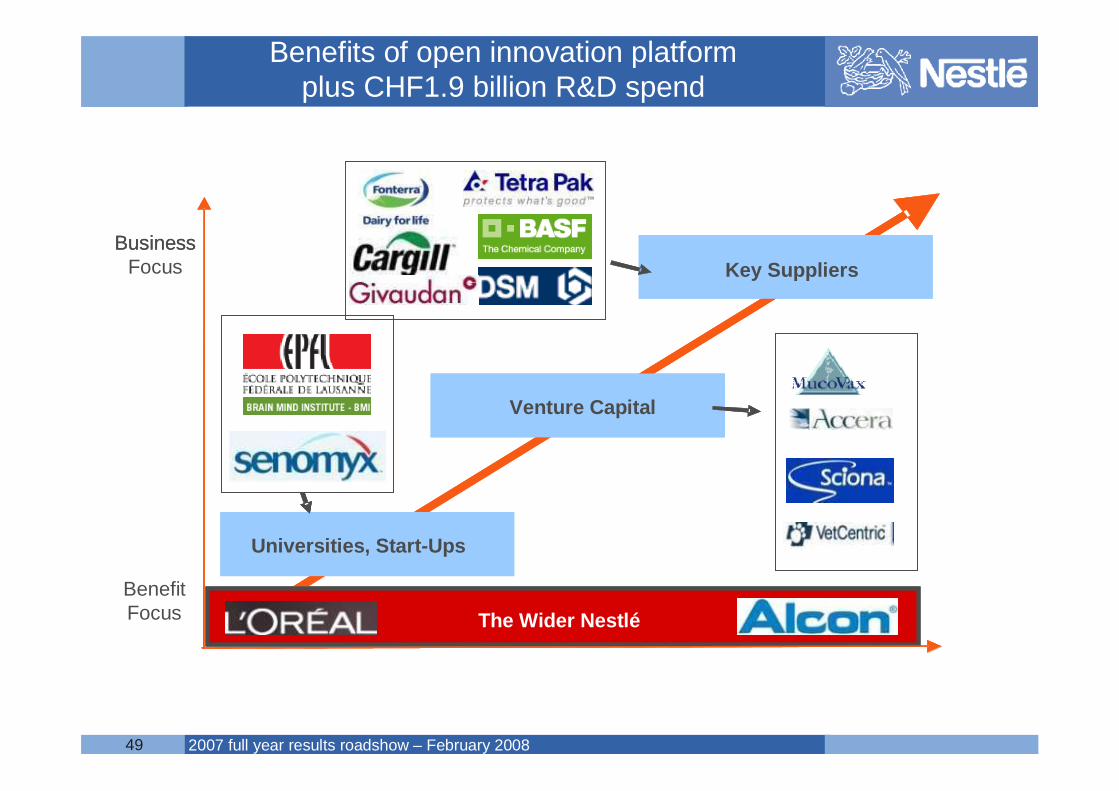

BenefitFocus

Business

Universities, Start

Venture Capital

Key Suppliers

The “ wider Nestl é”…

BusinessFocus

Universities, Start-Ups

Venture Capital

Key Suppliers

The Wider Nestlé

Benefits of open innovation platformplus CHF1.9 billion R&D spend

Name of chairman2007 full year results roadshow – February 200850

Population growth 2000-2050

Developing world* +3.3bn

North America +0.15bn

Europe -0.05bn

NestléF&B sales (CHF)

34 billion

29 billion

38 billion

Source for population growth: http://www.census.gov*Developing does not include Eastern Europe.

Unmatched geographic presence

Name of chairman2007 full year results roadshow – February 200851

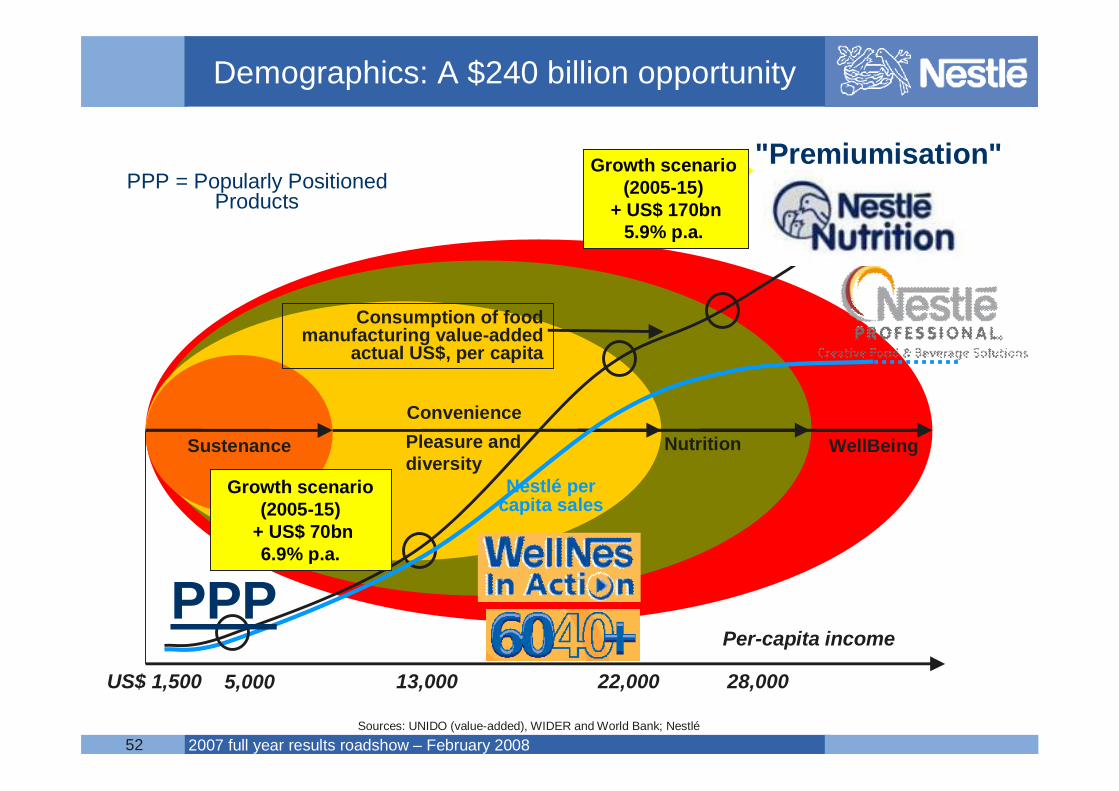

• Nutrition, Health & Wellness

• Emerging markets & PPP

• Leadership in "out of home"Nestlé Professional

• Premiumisation

Beyond 2008:The Four growth areas

Name of chairman2007 full year results roadshow – February 200852Sources: UNIDO (value-added), WIDER and World Bank; Nestlé

Demographics: A $240 billion opportunity

US$ 1,500

Sustenance Pleasure anddiversity

Convenience

5,000 13,000 22,000

Per-capita income

28,000

"Premiumisation"Growth scenario (2005-15)

+ US$ 170bn5.9% p.a.

Growth scenario (2005-15)

+ US$ 70bn6.9% p.a.

PPP

Consumption of food manufacturing value-added

actual US$, per capita

Nutrition WellBeing

Nestlé per capita sales

PPP = Popularly PositionedProducts

Name of chairman2007 full year results roadshow – February 200853

CHF1.3 trillion:Value of 'traditional trade' grocery

sales in our Top 10 emerging markets

Grow in emerging markets

Source: Planet Retail, Europanel, Market Data, SGDU Estimate

Name of chairman2007 full year results roadshow – February 200854

Emerging markets and PPP –A $70 billion opportunity

Name of chairman2007 full year results roadshow – February 200855

People, mn

Sources: UN WIDER and World Bank (also for outlook on economic growth 2005-2015);

+ 355

+ 885+ 133

+ 230

+ 448

+ 199

1970 1653 1429

2153 26012354

710940 1825

389522

443175

235286

295

494

849

0

1'000

2'000

3'000

4'000

5'000

6'000

7'000

1995 2005 2015

> 28'000

22'000-28'000PPP$

13'000-22'000PPP$

5'000-13'000PPP$

1500-5000 PPP$

< 1500 PPP$

Moving up on the escalator: World population by income bracket – 1995-2005-2015

Name of chairman2007 full year results roadshow – February 200856

Premiumisation

3. Own Retail Outlets

2. Strong Emotional Affiliation

Boutiques & BarsGift boxes

4. Own the Expert Client Community1. True Product

Differentiation

Name of chairman2007 full year results roadshow – February 200857

• Operational efficiency

• Innovation & Renovation

• Consumer communication

• Whenever, wherever, however

Beyond 2008:The Four Pillar Strategy

Name of chairman2007 full year results roadshow – February 200858

• Due to shifts in demographics and socio-economic factors foodservice represents an increasingly important consumer option

• Consumer demand for convenience, taste & nutrition is driving foodservice growth in all markets

• In mature economies, OOH spend today accounts for 30-50% of consumer food & beverage purchases

• The trend is for further long term growth in OOH consumption

Out of home (OOH)A growing trend & a $400 billion market

Name of chairman2007 full year results roadshow – February 200859

“The global leader in branded hot and cold

non-carbonated Beverage solutions”

“The local and regional leader in strategic food

product solutions”

Name of chairman2007 full year results roadshow – February 200860

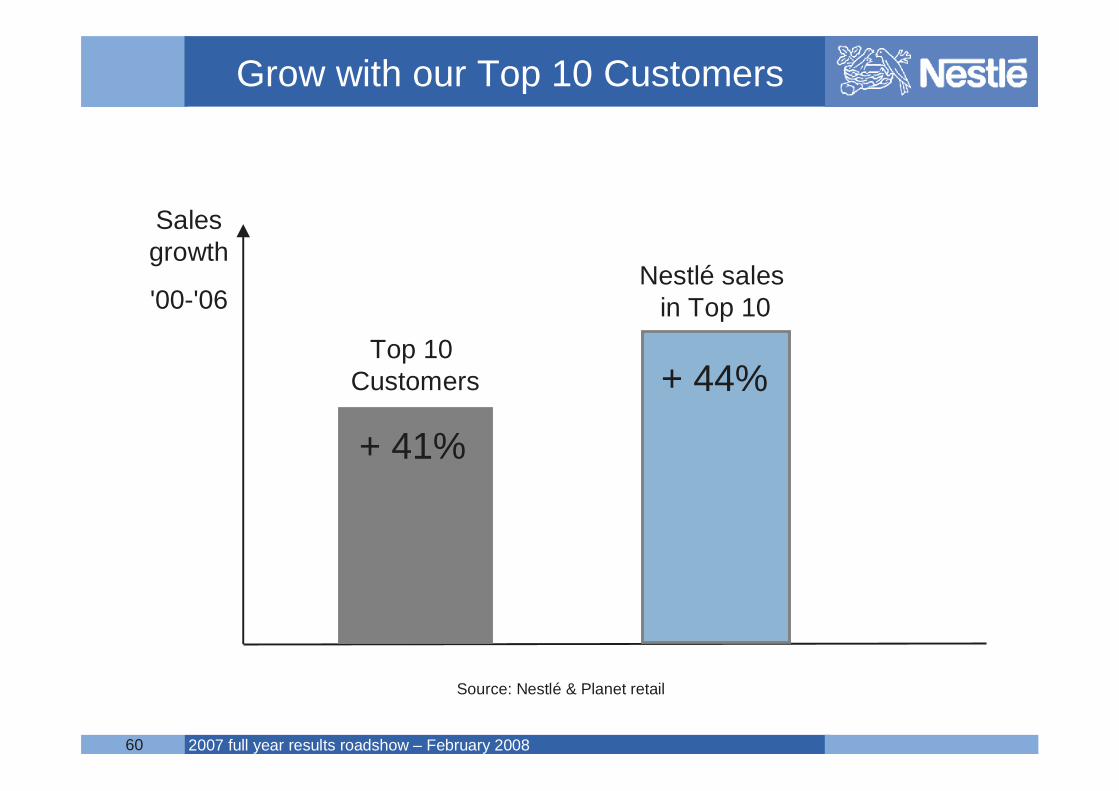

Sales growth

'00-'06

Top 10 Customers

Grow with our Top 10 Customers

Source: Nestlé & Planet retail

+ 41%

+ 44%

Nestlé sales in Top 10

Name of chairman2007 full year results roadshow – February 200861

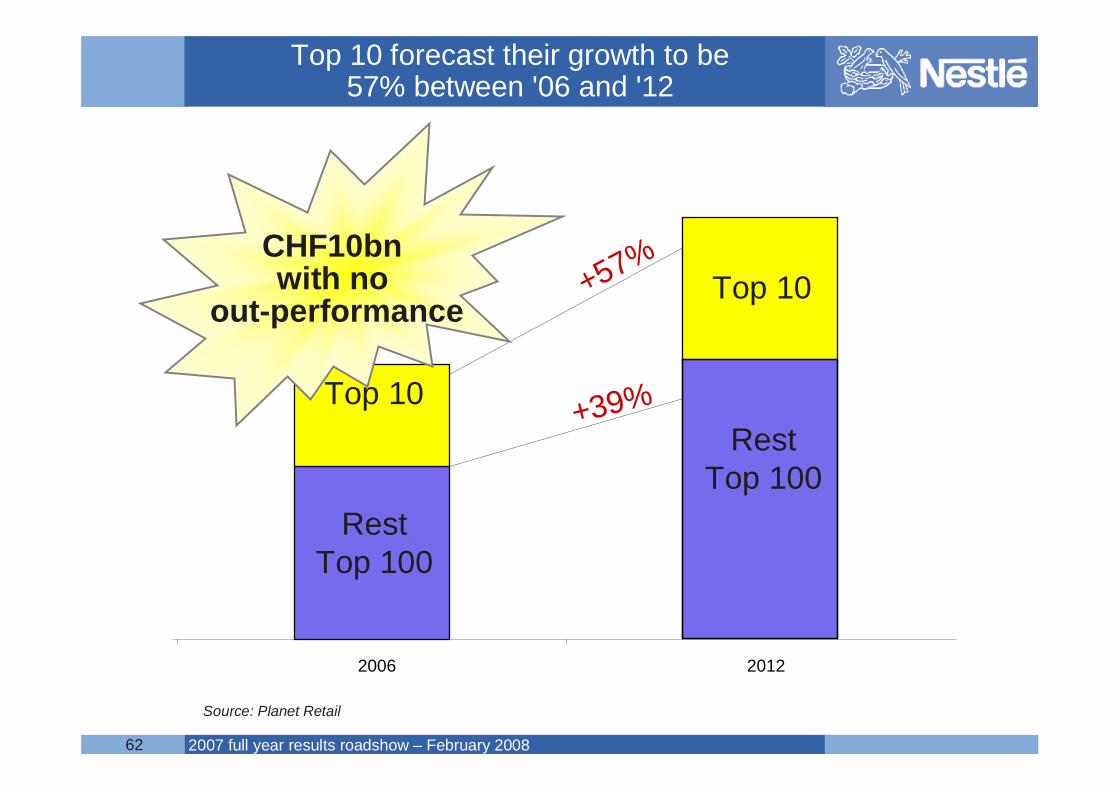

2006 2012

RestTop 100

Top 10

Top 10

+39%

+57%

RestTop 100

Source: Planet Retail

Top 10 forecast their growth to be57% between '06 and '12

Name of chairman2007 full year results roadshow – February 200862

2006 2012

RestTop 100

Top 10

Top 10

+39%

+57%

RestTop 100

Source: Planet Retail

Top 10 forecast their growth to be57% between '06 and '12

CHF10bn with no

out-performance

Name of chairman2007 full year results roadshow – February 2008

We intend to make Nestlé the referencefor both Nutrition, Health & Wellness

and for Financial Performance

Summary

Name of chairman2007 full year results roadshow – February 200864

Deliver the strategy – continuity• Nutrition, Health & Wellness higher margin/growth categories• Organisational Transformation structural efficiencies & growth• Key growth opportunities above market growth

Build on the Competitive advantages – to higher levels• Brand, presence, people, R&D Profitable growth• Leverage GLOBE, GNBS Nestlé Continuous Excellence• Discipline & accountability swift, flawless execution

"The Result" – enhanced financial performance• Achieve "the Nestlé Model" with greater capital efficiency

Beyond 2008:Building on momentum to drive performance

Name of chairman2007 full year results roadshow – February 200865

The Nestlé Investment Proposition“The Nestlé Model”

1. Long-Term Organic Growth Target 5 - 6%

Resulting in an industry outperforming, long-term total shareholder return

2. Continued year after year improvement of EBIT margin

3. Improving Capital efficiency / Business ROIC / Cash returns to shareholders

EBIT

Sales

Name of chairman2007 full year results roadshow – February 200866