mobile banking

15

Mobile Banking

-

Upload

merina-parvin -

Category

Documents

-

view

65 -

download

1

Transcript of mobile banking

Mobile Banking

Mobile Banking will create a revolution in banking and financial services in the emerging countries where most of the population are still out of the financial services.

Specifically in Bangladesh there will be phenomenal growth. Peoples leaving out-of-reach of traditional banking network, busy profession, traffic congestion and most important is the new generation who are interested for smart banking without step-into a bank branch will quickly sign-up for this service.

Enterprises and the government organizations, which needs to disburse or collect huge number of payments regularly, will be benefited greatly.

Thus, Mobile Banking will bring huge benefit for all the eco-system players like banks, agents, consumers, merchants, card networks and the government.

2

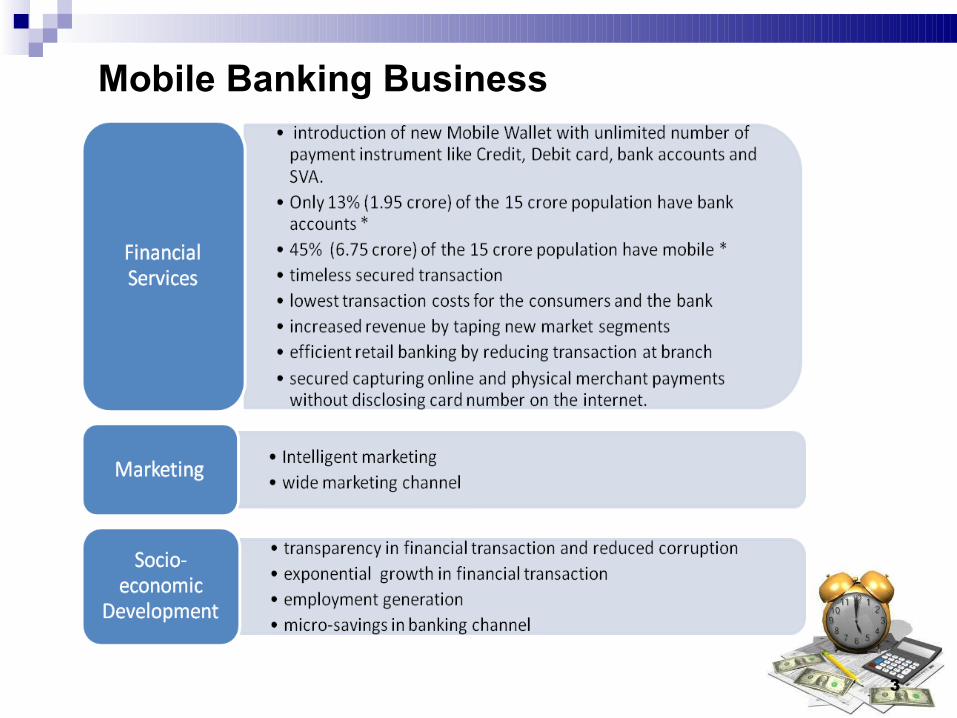

Mobile Banking Business

3

TARGET CUSTOMER SEGMENTS

•Ministries•Departments•Projects•AG offices units•National Board of Revenue•Government e

•Garment manufacturers and other industries•Large business conglomerates•Group of companies•Real-state companies•Utility companies•Security companies•Hospitals, diagnosis labs•Employees of the above industries/companies•Universities and other educational institutions•Brokerage Houses

•All type of merchants like shops, restaurants, superstores, travel agents, cinema etc.

•Union Information Service Centers•Mobile Network Operators•NGOs•Distribution companies•Couriers•Post office•Bank’s own commission based agents

•Students•Farmers/Doctors/Professionals•Beneficiaries of international remittance•Beneficiaries of pension, welfares and other similar schemes•Garments, industries, government and other employees•Contractors and suppliers

Consumers

Enterprises Government

Merchants

Agents

3.a

GOALS AND OBJECTIVES

Mobile Banking project have specific goals of benefits for every one of the eco-system players:

CONSUMERS, GOVERNMENT AND ENTERPRISES• Banking and payments Anywhere, Anytime, Any Channel.• Government introduces digital financial services for more efficiency and transparency.

AGENTSExecute transaction on-behalf of the bank and earn fees and commission.

MERCHANTSAcquire payments through a new channel which offer low financial cost for merchant as well as bank.

4

CARD NETWORKS• Introduce new channel of acquiring payments.

MOBILE NETWORK OPERATORS• Earn more revenue through network usage (voice, SMS, data, USSD etc.).• Share service charges/commission /fees with the banks by delivering end-

customer service through their outlets/channel partners.

BANK• Open new revenue stream through mobile financial services• Offer various market specific services and increase customer base• Reduce bank’s per customer acquisition cost• Reduce bank’s per customer operational cost• Reduce per transaction cost• Divert retail banking load to consumers pocket and increase branch operation

efficiency• Reduce cash management effort and cost• Increase low cost deposit, thus reduce cost of fund and earn from the floats• Create employment ‘out of the bank payroll’ and also within the payroll.• Take competitive advantage over the competing banks

5

MARKET OPPORTUNITIES

Source: http://en.wikipedia.org/wiki/Mobile_banking#Mobile_banking_in_the_world

As of the above pyramid, the new opportunities are in the middle segment of the pyramid and the size is around 4.80 crore mobile users who does not have a bank account. However, the upper segment with 1.95 crore people also a target for migration from other bank by offering convenient and efficient services.

6

OPERATIONAL MODEL

7

SERVICESProposed Services:• Mobile Wallet services• National Money Transfers• Merchant Payment Services• Government/Enterprise Payment Services• Local and International Remittance (inward)• Bill Payment• Mobile Airtime Top up (self, street and shop)

Future Services (subject to central bank approval and procuring the modules):

• Mobile Reservation and Ticketing• Internet Merchant Acquiring • Mobile Marketing• Mobile Brokerage• National Hub Payment Services

8

Mobile Banking Project Analysis

5 Years Customer Acquisition Plan

Assumptions Year-1 Year-2 Year-3 Year-4 Year-5

Existing Mobile Users in Bangladesh 7,52,00,000 8,39,00,000 9,14,00,000 9,78,00,000 10,31,00,000

Net Mobile Users (considering 50% duplicate) 3,76,00,000 4,19,50,000 4,57,00,000 4,89,00,000 5,15,50,000

No. of Banks offering Mobile Banking (appx) 5 8 12 18 25

Approximate Mobile Account 10% 15% 25% 30% 35%

Expected Mobile Banking Users in Bangladesh 37,60,000 62,92,500 1,14,25,000 1,46,70,000 1,80,42,500

Expected Market Share of IFIC Bank 15% 25% 20% 18% 15%

Projected Mobile Banking Customer of IFIC Bank 5,64,000 15,73,125 22,85,000 26,40,600 27,06,375

9

ACQUISITION COSTS

Per Customer Acquisition Cost

Cost Head Commission (in BDT)

Registration 10.00

KYC Form 5.00

Misc. 3.00

Per customer acquisition cost: 18.00

10

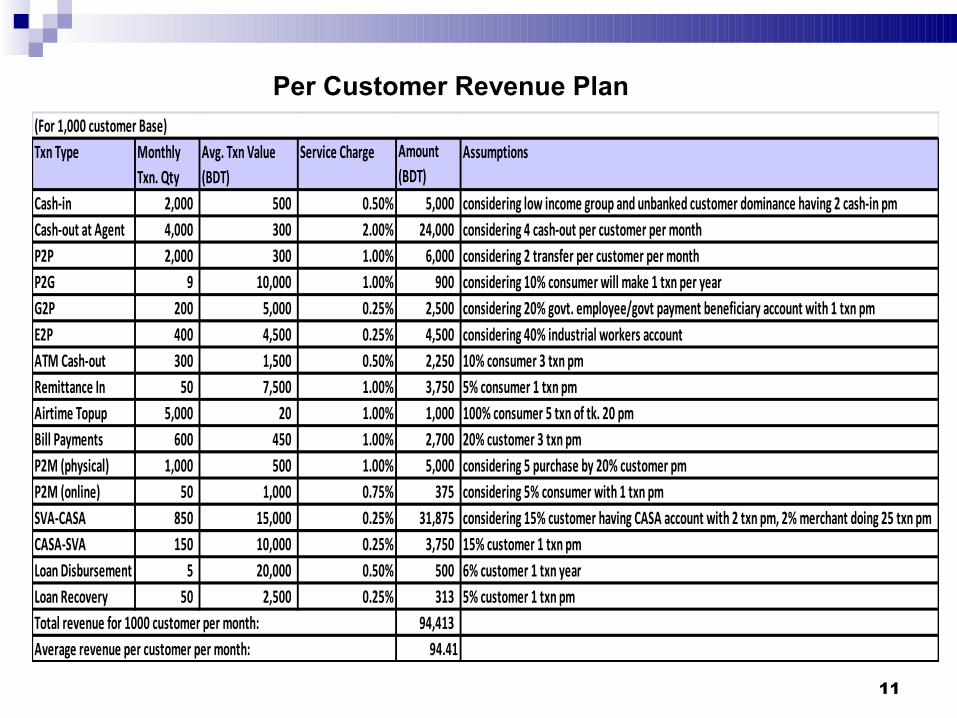

Per Customer Revenue Plan

Txn Type Monthly Txn. Qty

Avg. Txn Value (BDT)

Service Charge Amount (BDT)

Assumptions

Cash-in 2,000 500 0.50% 5,000 considering low income group and unbanked customer dominance having 2 cash-in pmCash-out at Agent 4,000 300 2.00% 24,000 considering 4 cash-out per customer per monthP2P 2,000 300 1.00% 6,000 considering 2 transfer per customer per monthP2G 9 10,000 1.00% 900 considering 10% consumer will make 1 txn per yearG2P 200 5,000 0.25% 2,500 considering 20% govt. employee/govt payment beneficiary account with 1 txn pmE2P 400 4,500 0.25% 4,500 considering 40% industrial workers accountATM Cash-out 300 1,500 0.50% 2,250 10% consumer 3 txn pmRemittance In 50 7,500 1.00% 3,750 5% consumer 1 txn pmAirtime Topup 5,000 20 1.00% 1,000 100% consumer 5 txn of tk. 20 pmBill Payments 600 450 1.00% 2,700 20% customer 3 txn pmP2M (physical) 1,000 500 1.00% 5,000 considering 5 purchase by 20% customer pmP2M (online) 50 1,000 0.75% 375 considering 5% consumer with 1 txn pmSVA-CASA 850 15,000 0.25% 31,875 considering 15% customer having CASA account with 2 txn pm, 2% merchant doing 25 txn pmCASA-SVA 150 10,000 0.25% 3,750 15% customer 1 txn pmLoan Disbursement 5 20,000 0.50% 500 6% customer 1 txn yearLoan Recovery 50 2,500 0.25% 313 5% customer 1 txn pm

94,413 94.41

(For 1,000 customer Base)

Total revenue for 1000 customer per month:Average revenue per customer per month:

11

CAPEX (in BDT) Year-1 Year-2 Year-3 Year-4 Year-5Mobile Banking Software 5,00,00,000 60,00,000 12,00,000 100,00,000 100,00,000Hardware & 3rd Party SW 1,00,00,000 - 10,00,000 - 50,00,000Data Center/Infra/Network 50,00,000 - - - - Establishment 1,57,31,250 71,18,750 6,22,000 35,91,750 - Total Capex 8,07,31,250 1,31,18,750 28,22,000 1,35,91,750 1,50,00,000Avg. Depreciation 2,50,52,750 2,50,52,750 2,50,52,750 2,50,52,750 2,50,52,750

Notes: Software SW price AMCAMC+ AMC+ AMC+

Upgrade Up grade UpgradeNotes: Hardware & DB Initial Setup Upgrade UpgradeNotes: Establishment BDT 10 per customer per year

setup for Year-

1 upgrade for Year-

3 growthUp grade for

Year-4 growthUp grade for

Year-5 growth

Capital Expenditure (5 Year)

Operational Expense (5 Year)

Head \ Year Year-1 Year-2 Year-3 Year-4 Year-5 Number of our Mobile Account (IFIC Bank) 5,64,000 15,73,125 22,85,000 26,40,600 27,06,375

Market Communication (BDT 10 per Customer/month) 6,76,80,000 18,87,75,000 27,42,00,000 31,68,72,000 32,47,65,000

Human Resource @ BDT 100 per customer 5,64,00,000 15,73,12,500 22,85,00,000 26,40,60,000 27,06,37,500

Data Centre/Network (BDT 4 per customer) 2,70,72,000 7,55,10,000 10,96,80,000 12,67,48,800 12,99,06,000

Total Operational Expense 15,11,52,000 42,15,97,500 61,23,80,000 70,76,80,800 72,53,08,500

12

13

Assumption of Deposit Collection

Head\ Year Year -1 Year -2 Year-3 Year- 4 Year -5No. of projected mobile account in IFIC Bank 5,64,000 15,73,125 22,85,000 26,40,600 27,06,375Consumer deposit Expected No. of Consumer(Considering 98% of the customer are consumer) 5,52,720 15,41,662 22,39,300 25,87,788 26,52,248Expected Consumer Deposit (@ BDT 600 per consumer)

33,16,32,000

92,49,97,500 1,34,35,80,000

1,55,26,72,800

1,59,13,48,500

Agent Deposit Expected No. of Agents (1.25% of Customers are agent) 7,050 19,664 28,563 33,008 33,830

(BDT 25000 per Agent;

17,62,50,000

49,16,01,563

71,40,62,500 82,51,87,500 84,57,42,188 Merchant DepositPercentage of Merchant A/C 0.10% 0.15% 0.20% 0.25% 0.30%Expected No. of Merchants 564 2,360 4,570 6,602 8,119

Expected Deposit @ BDT 50000 per merchant 2,82,00,000

11,79,84,375

22,85,00,000 33,00,75,000 40,59,56,250 Enterprise DepositPercentage of Enterprise A/C 0.05% 0.08% 0.10% 0.12% 0.15%Expected No. of Enterprise 282 1259 2285 3169 4060Expected Deposit @ BDT 0.20 Crore per Enterprise

56,40,00,000 2,51,70,00,000 4,57,00,00,000

6,33,74,40,000

8,11,91,25,000

Govt./Biller Deposit Expected No. of Govt./Biller Accounts A/C 5 8 12 15 20

Approx. Govt. /Biller Accounts Deposit 150,00,00,000 200,00,00,000 250,00,00,000 300,00,00,000 400,00,00,000 Total Expected Deposit 260,00,82,000 605,15,83,438 935,61,42,500 1204,53,75,300 1496,21,71,938

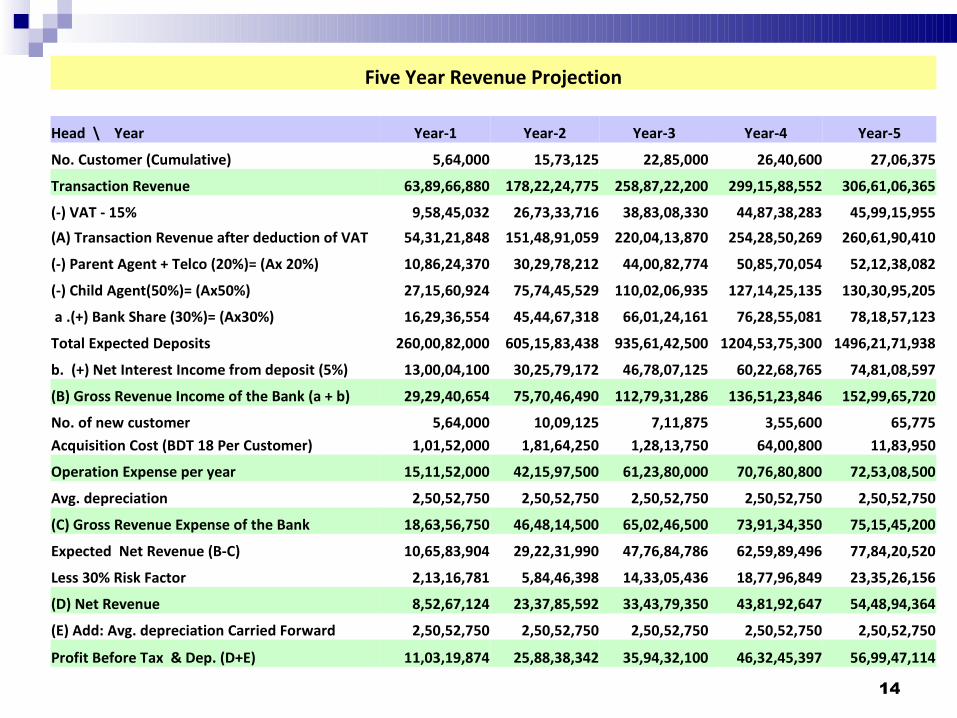

Five Year Revenue Projection

Head \ Year Year-1 Year-2 Year-3 Year-4 Year-5

No. Customer (Cumulative) 5,64,000 15,73,125 22,85,000 26,40,600 27,06,375

Transaction Revenue 63,89,66,880 178,22,24,775 258,87,22,200 299,15,88,552 306,61,06,365

(-) VAT - 15% 9,58,45,032 26,73,33,716 38,83,08,330 44,87,38,283 45,99,15,955

(A) Transaction Revenue after deduction of VAT 54,31,21,848 151,48,91,059 220,04,13,870 254,28,50,269 260,61,90,410

(-) Parent Agent + Telco (20%)= (Ax 20%) 10,86,24,370 30,29,78,212 44,00,82,774 50,85,70,054 52,12,38,082

(-) Child Agent(50%)= (Ax50%) 27,15,60,924 75,74,45,529 110,02,06,935 127,14,25,135 130,30,95,205

a .(+) Bank Share (30%)= (Ax30%) 16,29,36,554 45,44,67,318 66,01,24,161 76,28,55,081 78,18,57,123

Total Expected Deposits 260,00,82,000 605,15,83,438 935,61,42,500 1204,53,75,300 1496,21,71,938

b. (+) Net Interest Income from deposit (5%) 13,00,04,100 30,25,79,172 46,78,07,125 60,22,68,765 74,81,08,597

(B) Gross Revenue Income of the Bank (a + b) 29,29,40,654 75,70,46,490 112,79,31,286 136,51,23,846 152,99,65,720

No. of new customer 5,64,000 10,09,125 7,11,875 3,55,600 65,775

Acquisition Cost (BDT 18 Per Customer) 1,01,52,000 1,81,64,250 1,28,13,750 64,00,800 11,83,950

Operation Expense per year 15,11,52,000 42,15,97,500 61,23,80,000 70,76,80,800 72,53,08,500

Avg. depreciation 2,50,52,750 2,50,52,750 2,50,52,750 2,50,52,750 2,50,52,750

(C) Gross Revenue Expense of the Bank 18,63,56,750 46,48,14,500 65,02,46,500 73,91,34,350 75,15,45,200

Expected Net Revenue (B-C) 10,65,83,904 29,22,31,990 47,76,84,786 62,59,89,496 77,84,20,520

Less 30% Risk Factor 2,13,16,781 5,84,46,398 14,33,05,436 18,77,96,849 23,35,26,156

(D) Net Revenue 8,52,67,124 23,37,85,592 33,43,79,350 43,81,92,647 54,48,94,364

(E) Add: Avg. depreciation Carried Forward 2,50,52,750 2,50,52,750 2,50,52,750 2,50,52,750 2,50,52,750

Profit Before Tax & Dep. (D+E) 11,03,19,874 25,88,38,342 35,94,32,100 46,32,45,397 56,99,47,114

14