Merge Investor Presentation August 4 Final · • Age-related macular degeneration ... Q2 2013 Q3...

48

Investor Presentation August 2014

Transcript of Merge Investor Presentation August 4 Final · • Age-related macular degeneration ... Q2 2013 Q3...

Investor PresentationAugust 2014

Forward Looking Statement

2

The matters discussed in this presentation may include forward-looking statements, which

could involve a number of risks and uncertainties. When used in this presentation, the

words “will,” “believes,” “intends,” “anticipates,” “expects” and similar expressions are

intended to identify forward-looking statements. Actual results could differ materially from

those expressed in, or implied by, such forward looking statements. Except as expressly

required by the federal securities laws, the Company undertakes no obligation to update

such factors or to publicly announce the results of any of the forward-looking statements.

See the Company’s most recent earnings press release for explanation of non-GAAP

financial measures used in this presentation as well as reconciliation from GAAP to

non-GAAP metrics. Some of the products and/or product features discussed in this

presentation may be works in progress and not yet generally available for sale.

Why Merge Matters

3

images are

growingyou need to do

more with less

regulationsare pervasive

consolidationis happening

{ ARCHIVE • ACCESS • DIAGNOSE }

{ EDUCATE • EXECUTE • ADAPT }

{ AUTOMATE • ADOPT • INTEGRATE }

{ CONNECT • CENTRALIZE • EVOLVE }

Our Solutions Portfolio

4

Imaging & Interoperability

Cardiology Clinical Trials

Radiology

Interoperability

Cloud Archive

Eye Care

Orthopedics

Cardiology

Hemodynamics

EDC

CTMS

Merge Cardiology Solutions are #1 in KLAS!

5

Industry Leader!

Merge Named Top 10 Overall in KLAS

6

KLAS Overall Software Vendor Rankings 2013

Merge KLAS Special Report

7

Built directly on valuable

customer feedback

A report card of how well

we are delivering on

customer requirements

Merge KLAS Report – Overall Performance

1. Customers Buying In• Enterprise imaging strategy

• Image enabling the EMR

• Focus and transparency

2. Footprint Expanding• Clients plan to expand imaging suite

• Clients plan to stay at rate above

market average

• Clients looking into adding

interoperability and cardiology

8

We Are the Leader in MU for Radiology

9

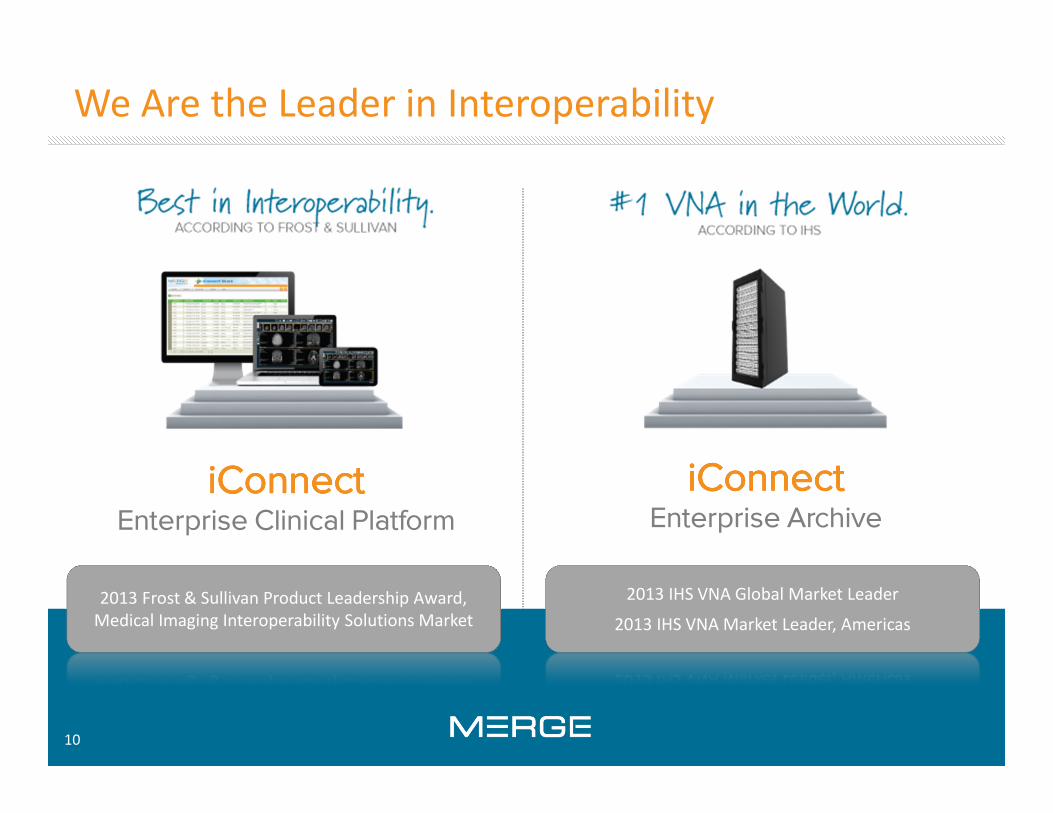

We Are the Leader in Interoperability

1010

iConnectiConnectiConnectiConnectEnterprise Clinical Platform

iConnectiConnectiConnectiConnectEnterprise Archive

2013 Frost & Sullivan Product Leadership Award,

Medical Imaging Interoperability Solutions Market

2013 IHS VNA Global Market Leader

2013 IHS VNA Market Leader, Americas

10

We’ve Made Enterprise Imaging Real

11

Chicago, IL

{ iConnect Access & Enterprise Archive, Merge PACS,Merge Cardio & Hemo }

Findlay, OH

{ iConnect Access & Enterprise Archive, Merge PACS,Merge Cardio & Hemo }

San Diego, CA

{ iConnect Access, Enterprise Archive & Outpatient Radiology }

{ iConnect Access and Enterprise Archive }

Lawton, OK

Every Image, Every EHR,

Every Time

12

Why iConnect Network?White Space Opportunity

13

What Are the Key Drivers?

14

Referral GrowthIncrease referring

physician loyalty and

expand business

Cost Savings Save time and money by

eliminating excess HL7

interfaces

Meaningful UseHelp community

physicians meet the imaging

requirement & attest

The Imaging Marketplace

15

Each year in

the USA,

800M+ studies

are done;

372M are

outpatient

Meaningful Use

now makes

interoperability

mandatory

EHR adoption

among referring

physicians is

nearing 60%

12%of every visit

800Million studies

60%EHR Adoption

MU2Mandates

12% of every

PCP visit in the

USA results in an

imaging order

(44 Million)

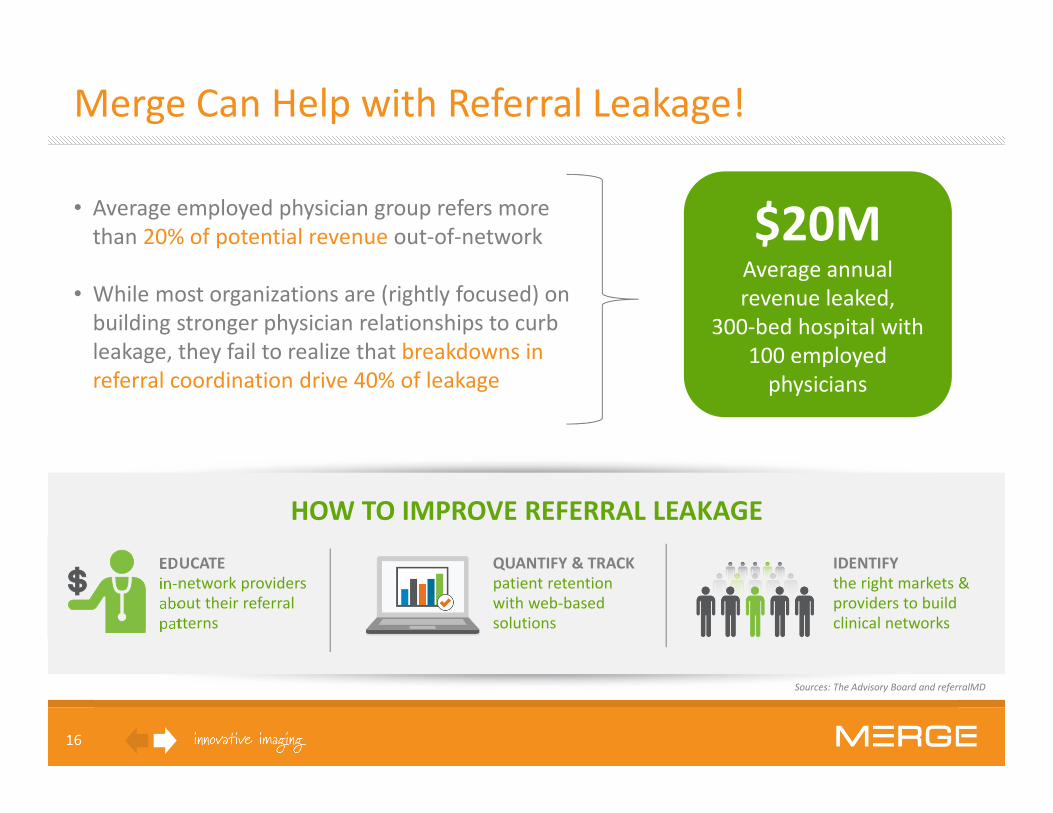

Merge Can Help with Referral Leakage!

• Average employed physician group refers more

than 20% of potential revenue out-of-network

• While most organizations are (rightly focused) on

building stronger physician relationships to curb

leakage, they fail to realize that breakdowns in

referral coordination drive 40% of leakage

16

$20M Average annual

revenue leaked,

300-bed hospital with

100 employed

physicians

Sources: The Advisory Board and referralMD

EDUCATE

in-network providers

about their referral

patterns

QUANTIFY & TRACK

patient retention

with web-based

solutions

IDENTIFY

the right markets &

providers to build

clinical networks

HOW TO IMPROVE REFERRAL LEAKAGE

Turn Referral Leakage into Referral “Keepage”

17

Source: Data from Mission Point Health Systems

The Referral Challenge for Imaging

18

Ph

ysic

ian

Imaging center

Hospital

imaging center

Reports

Orders

Images

More Referrals = More

How Do Providers Prevent Referral Leakage?!

Clients Work With Many Referring Physicians

19

Imaging Center /

Hospital System

Allscripts

Cerner

Epic

eClinical

Works

athena

NexGen

And They Work with Many Different EHRsHow will providers connect all disparate EHRs to imaging data & studies?

Referring Physicians

Who Sends Referrals?

20

clinicians & facilities

Sources: The Advisory Board and referralMD

$$$$

HL7 Interfaces Are Costly to Build & Maintain

21

EMR

PACS Archive

Imaging Center

Report includes

link to see image

in PACS archive

Costs to Deploy and Maintain HL7 Interfaces

• $20K‒$30K implementation fees

• PER bi-directional interface PER

referring physician practice

• 3‒6 month wait time PER interface

Sample Client

• 20 community EHR interfaces

• 20 corresponding RIS interfaces

• 80,000 annual studies

TCO over five years = $2.7M

For a facility with…

20 community EHR interfaces

20 related RIS interfaces

80,000 annual studies

Local Geographic Market Reality

22

Agfa

Siemens

McKesson

Philips

GE

Merge

Epic

Epic

Cerner

Greenway

Greenway

Allscripts

Allscripts

� Multiple Imaging Centers

Multiple Referring Practices �

� Multiple PACS Systems

Multiple EMR Vendors �

iConnect® Network Momentum

• Signed 7 net new

customers in Q2 ─

total of 29 contracted

(to date)

• Collected first dollar of

revenue

• Started work on the next

big release for electronic

referral order delivery –

coming in Q3

23

~10% of Total Ambulatory Radiology Base!

How iConnect Network Works

24

With Universal Viewer via Web Browser

25

Imaging Report

Hospital Feedback

26

“We’ve worked with Merge for several years, so it was an easy

choice to implement Merge’s VNA and iConnect Network for a

comprehensive, enterprise-wide imaging strategy…

Despite having an HIE in place, we needed a single solution that

handles imaging as it becomes more important to healthcare as

a whole. With iConnect Network, we’ll meet MU2 requirements

for the exchange of images and, most importantly,

enable better access to imaging for physicians in order to

provide the best care for our patients.”

Dave Holland, CIO, Southern Illinois Healthcare

Referring Physician Feedback

27

“iConnect Network gives us a competitive advantage for both our providers and patients. Since we are a part

of an ACO and are patient centered medical home certified,

iConnect Network is a true example of

a solution that integrates with our EHR, achieves

information exchange and helps our health center be more

efficient by automating time-consuming processes.

This ultimately enables us to improve treatment times,

reimbursements and patient care, as well as meet core

regulatory requirements.”

Luis Velasco, CIO, Marana Health Center

28

iConnect Retinal ScreeningAdvanced Interoperability Solution

for Population Health

What Problems Are We Solving?

29

diabetes, AMD, glaucoma, ALZ are

Increasing globally

institutions need

More Revenue with Volume

countries & socialized medicine need

Less Cost with More ServiceNo Complete Solutions

just band-aids

{ 382M DIABETICS WORLD WIDE – GROWS ~6% ANNUALLY }

{ DETECT DISEASE – TREAT EARLY – REDUCES COSTS }

{ DETECT DISEASE & INCREASE BILLABLE PROCEDURES }

{ NEED HARDWARE, SOFTWARE, CLOUD, ANALYTICS, ENGAGEMENT }

What is iConnect® Retinal Screening?

• An interoperable, end-to-end, subscription-

based offering for population health

• Leverages existing Merge solutions to simply

process of screening patients and deliver

information back to physicians

• Providers are able to capture images through

an automated camera, reducing the need for

specialty staff training

• We are targeting our large Eye Care

customer base

30

References:

• Economic Costs of Diabetes in the U.S. in 2012, American Diabetes Association,

http://www.diabetes.org/advocacy/news-events/cost-of-diabetes.html.

• 2013 International Diabetes Federation Diabetes Atlas, 6th Edition.

http://www.idf.org/sites/default/files/EN_6E_Atlas_Full_0.pdf.

How Does iConnect® Retinal Screening Work?

• Primary providers capture images and

upload to iConnect Cloud Archive (formerly know as Merge Honeycomb®)

• Client owned reading center interpret

images in Merge Eye Care PACS™

• Image reports route directly to

iConnect Network

• iConnect Network delivers image

reports to disparate providers’ EHRs

31

Disparate Sites

The Complete

iConnect

Retinal Screening

Solution

The Value of iConnect Retinal Screening

32

Institutions & Governments

Linked sites

Disparate sites

• Every ACO and payer is focused

on diabetic care management

and this complements their

strategy

• Eye care has a real play in hospital

and government markets

• Another international / OEM

solution for partners

• Increase potential market & sales

• Increase revenue from iConnect

Cloud Archive

Patients

Patients

What Is the Total Market Opportunity?

33

The U.S. is 10% of the global market opportunity$166M U.S. market opportunity**

* Estimate of fee over a five-year time horizon. / ** Includes additional revenue from iConnect Cloud Archive and iConnect Network. / *** 2013 International Diabetes Federation.

The market will continue to growdiabetes population increases each year and many regions will double by 2035***

Today, diabetes alone, is a $764M* global opportunity

What’s Next for iConnect Retinal Screening?

• Currently undergoing a pilot

program launch with Ontario

Telemedicine Network

• First phase offers diabetic

retinopathy screening

• Future stages of solution will include

screenings for:• Glaucoma

• Age-related macular degeneration

• Other serious neurological diseases

34

Merge eClinical OSA Truly Unified Platform

to Manage and Run Studies

35

What is Merge eClinical OS?

• Perfect mix of features & services

• Pay-as-you-go…what you use, when

• Manage user accounts, privileges,

options and training requirements

• Study build, support, training and

certification services on-demand

• Cost transparency with step-by-step, self-

service quoting & decision-support tools

36

eCOS is the Right-Size the Solution for Any Study!

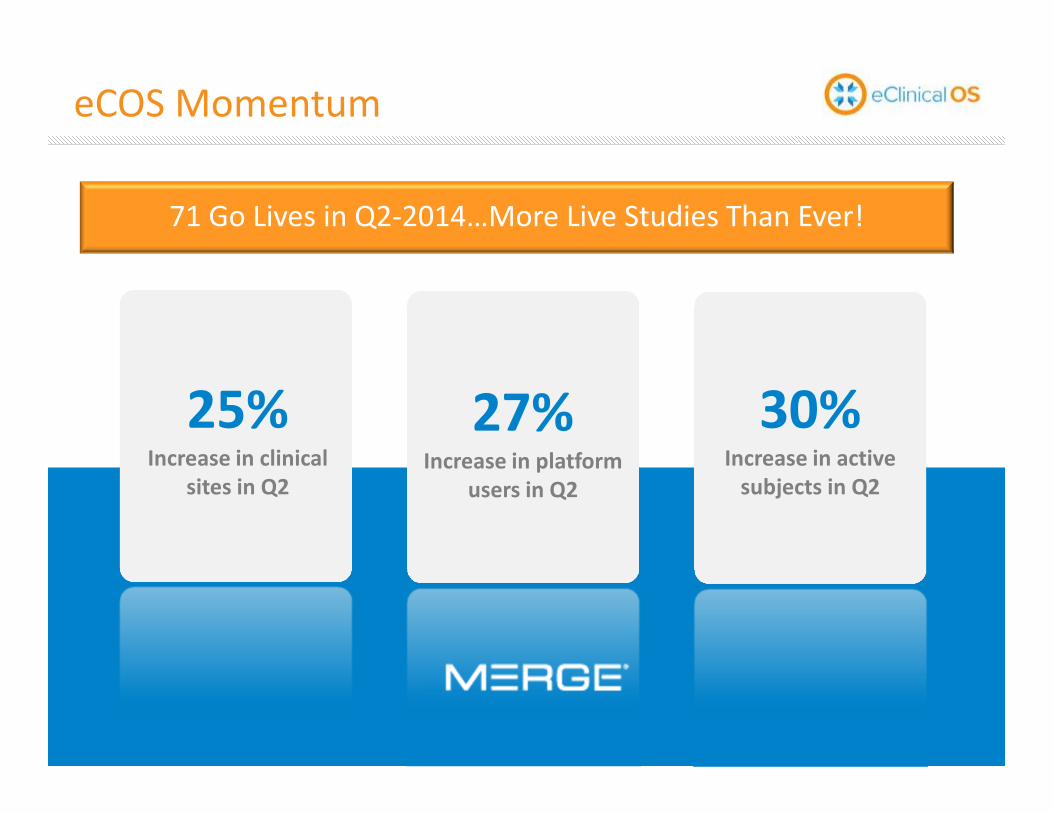

eCOS Momentum37

30%Increase in active

subjects in Q2

27%Increase in platform

users in Q2

25%Increase in clinical

sites in Q2

71 Go Lives in Q2-2014…More Live Studies Than Ever!

A Global Platform

38

# of countries where

Merge eClinical OS

is now in use!

65+

Why Merge?

39

Where We’ve Been

40

PACS for image intensive specialties

Clinical data and workflow tools

Firsts in enterprise imaging & interoperability

Our Client Base

41

1/3 of all U.S.

imaging centers

30% + of all

ortho groups

1,000 +

ophthalmology

sites

75% of all

worldwide

modality vendors

Top

pharmaceutical

companies &

CRO’s have used

Merge to run

clinical trials

1,500hospitals

6,000clinics

250partners

9 of 10top pharma

Including

many

hospitals on

“America’s

Best Hospital

Honor Roll”

Financial Information

42

Financial Improvements in Past Year

43

• iConnect Network, iConnect Cloud

Archive, iConnect Retinal Screening

and Merge eClinical OS

• Over 150 clinical trials went live on

eCOS in 1st half 2014

• Launched iConnect Retinal Screening

• Subscription backlog growth

of 12% YoY as of Q2 2014

• Strong cash generation leading to

cash balance of ~$24M and a 27%

decrease YoY in DSO to 88 days in Q2

• Refinancing of credit facility replaced

previous debt covenants with more

appropriate measures – which don’t

start until Q1 of 2015

• Maintained higher than industry

average spend of over 14% of our

revenue on R&D in 1st half 2014

Revenue & AEBITDA GrowthQuarterly

• Delivered a sequential quarterly

increase in revenue of 6%

• Excluding non-cash debt refinancing

cost in Q2, delivered another quarter of

increasing net income

• Grew adjusted EBITDA to 21% (40%

increase over Q2 2013)

• Adjusted net income increased to

$0.05 per share, compared to $0.01

in Q2 2013

Continued Innovations for Subscription

Offerings

Stabilized While

Investing

27.9 27.5 26.0 25.5 25.8

9.7 9.5 8.4 8.2 9.0

20.0 20.7 19.4

17.4 19.3

$57.6 $57.7

$53.8$51.1

$54.1

59.3%

56.9%

60.2%

61.9%

59.3%

40.0%

45.0%

50.0%

55.0%

60.0%

65.0%

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014

Maintenance Subscription Non Recurring Gross Margin %

Revenue and Adjusted EBITDA Trend

44

Gross Margin %

(net of D&A)

$8.5

$7.2

$8.9

$10.2$11.2

$10.6

$15.3$14.5

$13.5

$8.3

14.8%

12.5%

16.5%

20.0%20.8%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

$0

$5

$10

$15

$20

$25

$30

Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014

Adjusted EBITDA

Cash generated by business operations

Adjusted EBITDA %

Adjusted

EBITDA %

In Conclusion…

45

Why Stability Matters

Financial stability allows us to continue to invest

in research, development and innovation

46

• In 2014, we are spending over 14% of our revenue on R&D

• We continue to spend more than most organizations in our sector

• Our investments continue to pay off by industry recognitions

Why Focus Matters

Our priorities are in tact

47

• Industry is changing and our investments allow our clients to adapt

• Merge is changing but continues to focus on our core solutions

• Our teams that build, support, service our solutions are stable

Questions?

48