Katoen Natie IOT Limited -...

37

Polymer Warehousing International Benchmarking & The Future 12 th Feb’2015 Katoen Natie IOT Limited Dibyendu Deepak

-

Upload

truongdang -

Category

Documents

-

view

221 -

download

3

Transcript of Katoen Natie IOT Limited -...

Polymer Warehousing

International Benchmarking & The Future 12th Feb’2015

Katoen Natie IOT Limited

Dibyendu Deepak

2

Disclaimer

Views expressed for the next 20 minutes are all mine, well its not even

mine, as most of them have been Cut-Copy-Pasted from somewhere. Even

the examples given are on real people and real situation…. are fictional. I

take the full responsibility of my views but any disagreements and

arguments can wait till 7 : 30 PM.

4

We know only about

Warehousing

5

“Warehouse” is “NOT” the most

Interesting of the subject

6

Since Morning , We are Hearing about

Crude Oil Positive Impact, Economy bouncing

back, Reforms waiting to happen, polymer -

Double Digit Growth

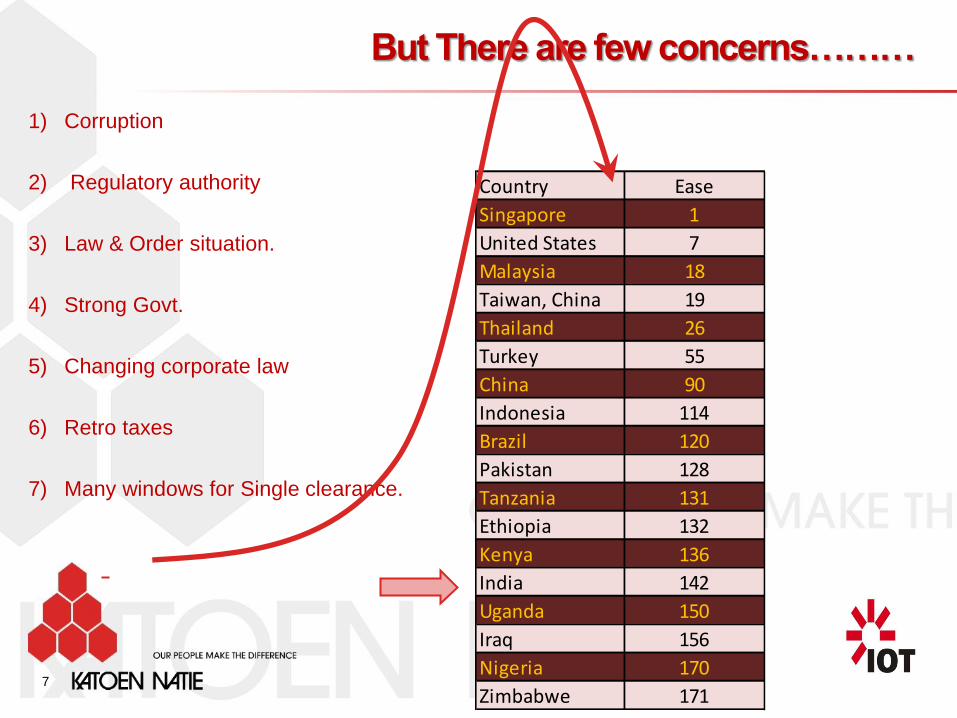

Country Ease

Singapore 1

United States 7

Malaysia 18

Taiwan, China 19

Thailand 26

Turkey 55

China 90

Indonesia 114

Brazil 120

Pakistan 128

Tanzania 131

Ethiopia 132

Kenya 136

India 142

Uganda 150

Iraq 156

Nigeria 170

Zimbabwe 171

But There are few concerns………

7

1) Corruption

2) Regulatory authority

3) Law & Order situation.

4) Strong Govt.

5) Changing corporate law

6) Retro taxes

7) Many windows for Single clearance.

8

1) Make in India : Autobiography of “ Investment in India” - Mr. K

Natie

2) Benchmarking of Indian Vs Developed countries Warehousing.

3) What WE must do with our future warehouses.

Autobiographical Journey of a

Warehousing Company in

India

Theme : Make in India

I heard ,back in Europe …..

10

Name: Mr K Natie

Country European Nation

Occupation Warehousing &

Engineering Entrepreneur

Still , I was apprehensive about …..

11

1) Long lead time.

2) Low margins

3) High Corruption

& I could not have expected better start….

12

1) Long lead NO ; Got “TWO” very prestigious project in “SIX” months.

2) Low margins YES ; but “Volumes” compensated for the LOW margins

3) Corruption NO ; Didn’t “PAY” a single cent “BRIBE” & continue to be ethical.

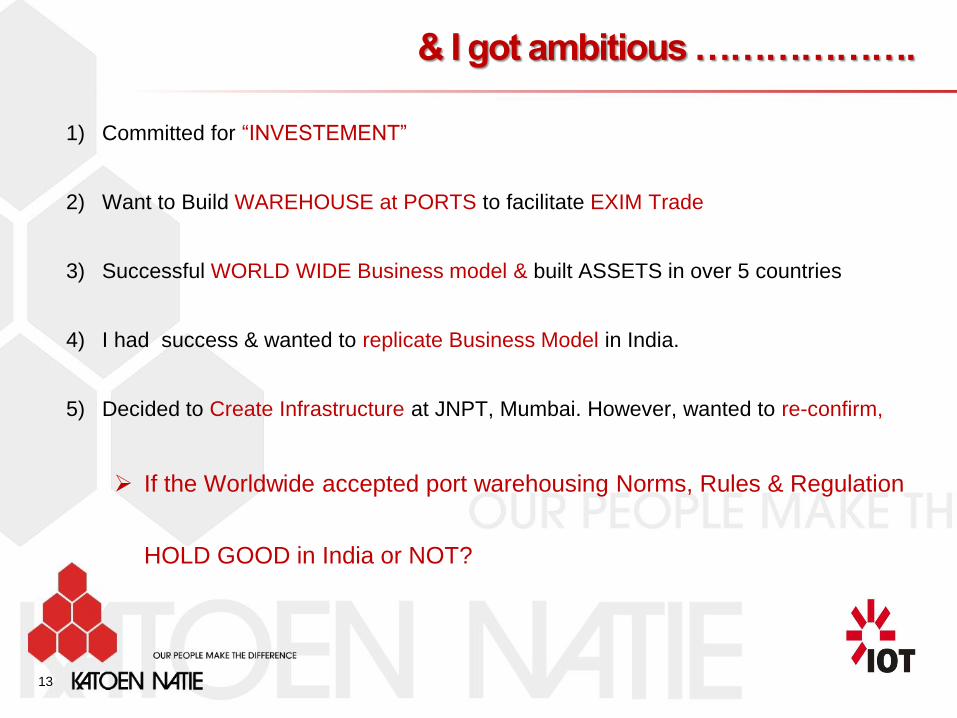

& I got ambitious ……………….

13

1) Committed for “INVESTEMENT”

2) Want to Build WAREHOUSE at PORTS to facilitate EXIM Trade

3) Successful WORLD WIDE Business model & built ASSETS in over 5 countries

4) I had success & wanted to replicate Business Model in India.

5) Decided to Create Infrastructure at JNPT, Mumbai. However, wanted to re-confirm,

If the Worldwide accepted port warehousing Norms, Rules & Regulation

HOLD GOOD in India or NOT?

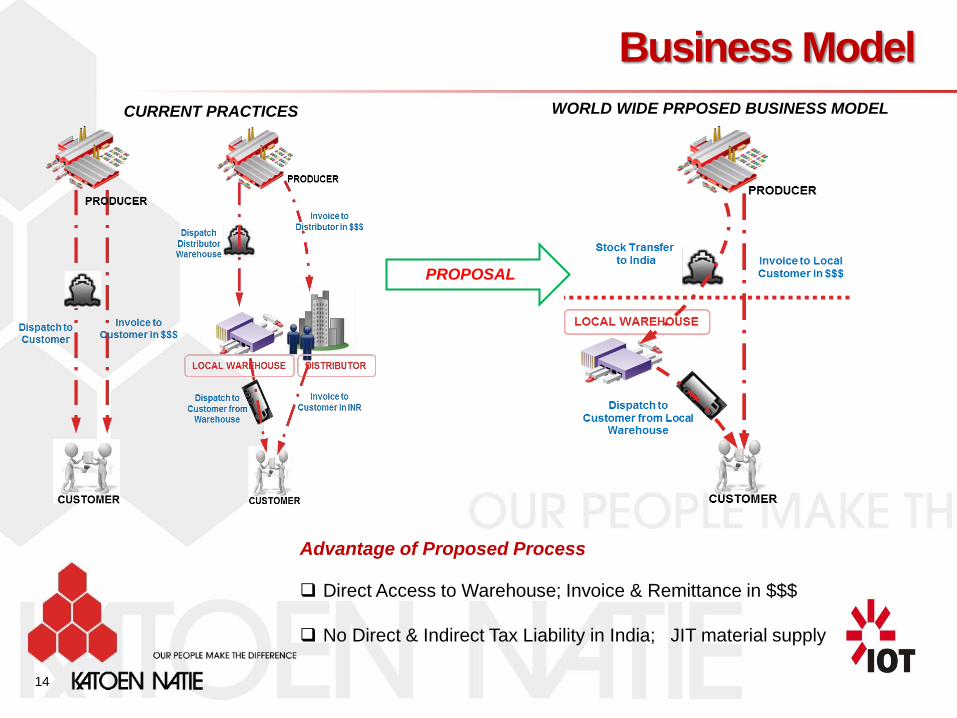

Business Model

14

CURRENT PRACTICES WORLD WIDE PRPOSED BUSINESS MODEL

Advantage of Proposed Process

Direct Access to Warehouse; Invoice & Remittance in $$$

No Direct & Indirect Tax Liability in India; JIT material supply

PROPOSAL

So, The quest started…

15

I Engaged “First “ than “ Second” and than “Third” well known “TAX”

and “CUSTOM” consultants

SOLUTION not possible

from BONDED Warehouse.

1. Possible but only from

Favorable DTAA Countries

2. No Local Marketing Activities

3. No IMPORT/VAT/CST Liability

4. $$ Invoicing to Local Customer

not possible

1. Possible but only from Favorable

DTAA Countries

2. Not Sure about VAT/CST Liability

3. Implication after 2-3 Years

4. Suggested about FTWZ, still NO

Guarantee of VAT/CST Liability

5. $$ Invoicing to Local Customer

possible

NO CLARITY BUT MORE AMBIGUITY

Message was clear …..

16

There is no ONE “Correct Process”.

Consultants were not ready to take Guarantee of their own findings.

We went directly to Users & Importers;

They were served notices by Sales Tax on Imports done from FTWZ. (

Who cares about bonded warehouse)

We found another way to get view from the authorities thru “ADVANCE

RULING” route.

AND , ADVANCE RULING takes 1 to 3 years.

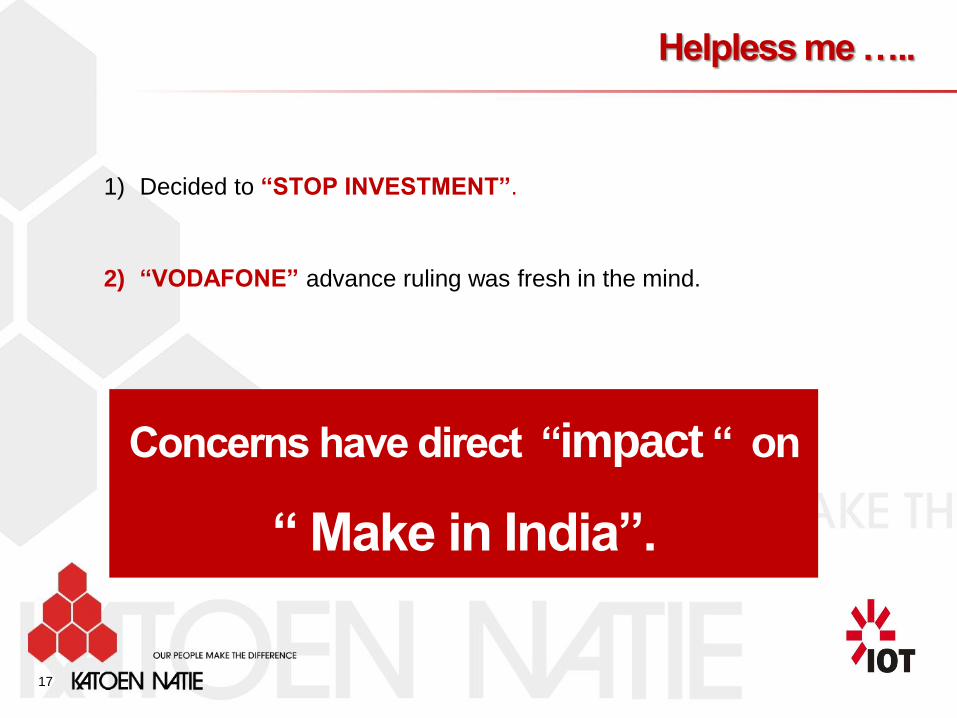

Helpless me …..

17

1) Decided to “STOP INVESTMENT”.

2) “VODAFONE” advance ruling was fresh in the mind.

Concerns have direct “impact “ on

“ Make in India”.

Benchmarking Indian vs Developed Country

Warehouse

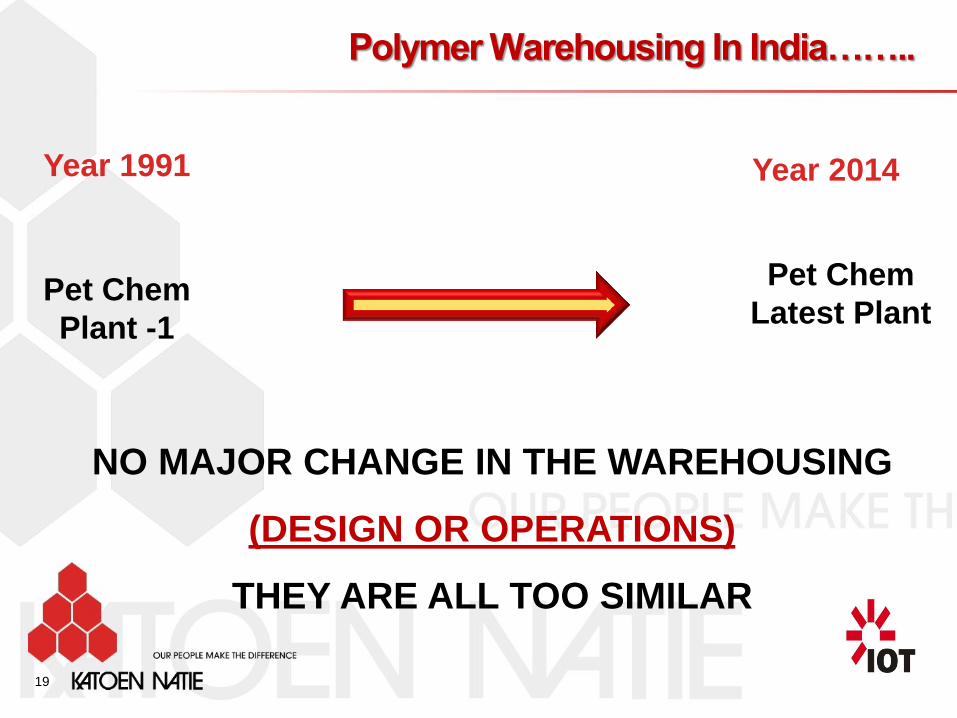

Polymer Warehousing In India……..

19

Year 1991 Year 2014

NO MAJOR CHANGE IN THE WAREHOUSING

(DESIGN OR OPERATIONS)

THEY ARE ALL TOO SIMILAR

Pet Chem

Plant -1

Pet Chem

Latest Plant

What Changed in Last 2 Decade

20

CUSTOMER PROFILE

MARKET PLACE

PRODUCT MIX

PACKAGING NEEDS

HIGHER CAPACITY PLANT

N O W T H E WAY W E

D O

WAR E H O U S I N G

M U S T

Benchmarking

21

OPEN MOUTH RAFFIA BAG FFS BAG

BAG AS STORAGE SILO AS STORAGE

25 KG BAG PACKAGING BULK/JUMBO/OCTABIN

LABOUR INTENSIVE (120) MECHANIZED OPS (50)

ROAD MODE (TRUCK) MULTI MODAL

LOOSE BAG DISTRIBUTION PALLETE DISTRIBUTION

MULTI PARTY -

Outsourcing

SINGLE POINT -

Outsourcing

WAREHOUSE PART OF

PRODUCTION UNIT

DESIGNED BY LOGISTIC /

MARKETING SPECIALIST.

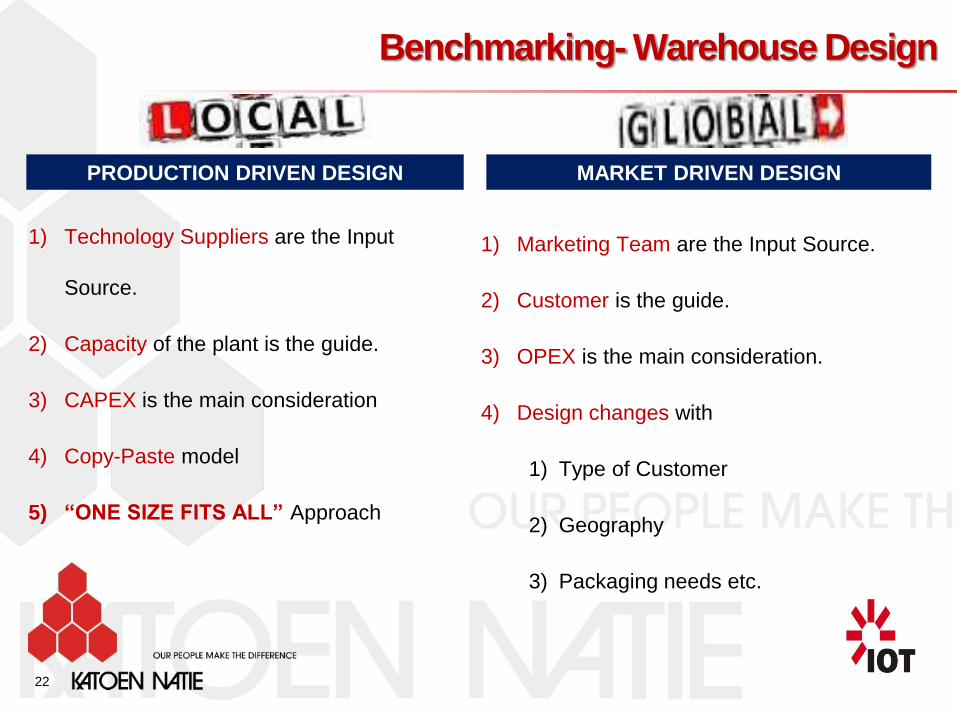

Benchmarking- Warehouse Design

22

PRODUCTION DRIVEN DESIGN MARKET DRIVEN DESIGN

1) Technology Suppliers are the Input

Source.

2) Capacity of the plant is the guide.

3) CAPEX is the main consideration

4) Copy-Paste model

5) “ONE SIZE FITS ALL” Approach

1) Marketing Team are the Input Source.

2) Customer is the guide.

3) OPEX is the main consideration.

4) Design changes with

1) Type of Customer

2) Geography

3) Packaging needs etc.

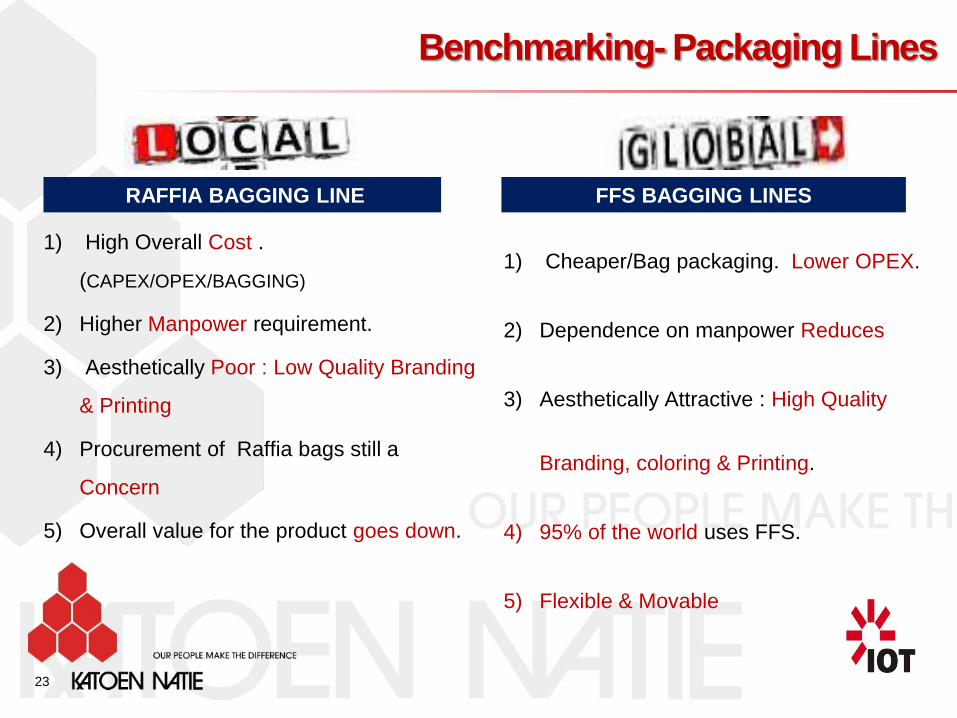

Benchmarking- Packaging Lines

23

RAFFIA BAGGING LINE FFS BAGGING LINES

1) High Overall Cost .

(CAPEX/OPEX/BAGGING)

2) Higher Manpower requirement.

3) Aesthetically Poor : Low Quality Branding

& Printing

4) Procurement of Raffia bags still a

Concern

5) Overall value for the product goes down.

1) Cheaper/Bag packaging. Lower OPEX.

2) Dependence on manpower Reduces

3) Aesthetically Attractive : High Quality

Branding, coloring & Printing.

4) 95% of the world uses FFS.

5) Flexible & Movable

Benchmarking- Packing

24

Packing & Storage Packing & Storage

SEA BULK CONTAINER BULK LOADING

PALLETIZED HANDLING JUMBO BAG

PALLETIZED HANDLING JUMBO BAG

SILO STORAGE

Benchmarking- Storage

25

Storage Storage

CONVENTIONAL STORAGE MIX STORAGE

Benchmarking- Warehouse Operations

26

Multi Contractor

5 or 6 Contractor

Single Point

Responsibility

Benchmarking- Automation

27

“NO” Huge Difference in the Degree of automation of the plant.

Focus is process improvement, reduction of

manpower and reducing redundancy in the

system.

Focus is on improvement of existing

processes.

Biggest Myth is that India has cheap labor.

Myth …….. Labour Cost Advantage

28

“5” People to a Change a Electrical Bulb from a Lamp post

Myth …….. Labour Cost Advantage

29

Availability of

Labour

High

Cost

What We MUST do here in India

Path Forward

Path Forward

31

Driven by marketing needs.

Take care of next 20 years.

Diverge the product warehouse

Design from the EPC of plant.

Design engagement to the Specialist.

It's SAFE & SAVE.

Warehouse Design FFS BAGGING LINES

Shift to FFS Packaging Line.

Reduce Cost ; Less dependency on

Manpower.

BULK LOADING

Reduce Cost : Bulk loading

Initially export & gradually to the

domestic customer.

Producers or Importers can SAVE by shifting

to Multi-Brand warehouse.

Independent warehouses at all major

consumption centers.

Path Forward

32

Avoid Multi Contract O&M.

Single point responsibility

Save management cost (Total Cost).

Easier to manage

Give jobs to the 3rd party specialist.

Warehouse Operations Multi User Warehouse

About us

34

KATOEN NATIE - IOT

(50%) (50%)

JV

(49%) (51%)

Katoen Natie IOT Limited

We are Part of Katoen Natie

We are Part of IOT & IOCL

Logistics Platform

Operations

Process Engineering

Supply Chain

Engineering

35

Areas of Operations

Design

Flexibility

Modularity

Cost effective

CAPEX / OPEX

Engineering

Purchasing

Construction

Project

Management

Commissioning &

Startup

Administration

Bagging/Compounding

Storage

Maintenance

O&M EPC Conceptual

Design

HUNTSMAWilton UK 36

Katoen Natie Customer….

Serve almost all the top Polymer producers in the world.

Summary

37

To “MAKE IN INDIA” , we must bring in Clarity in taxes.

Say “NO” to RETRO TAXES.

Benchmarking of warehousing Operations to the Global Best

Practices.

“NO” to business model driven on Cheap labor.

Time is ripe for Multi- User Warehouse at Major consumption

centers.

Outsource work to the Specialists

Thank You

38