a successful story in Mexico - platts.com · awarded with the supply of Ethane to build a Ethylene...

36

... a successful story in Mexico

Transcript of a successful story in Mexico - platts.com · awarded with the supply of Ethane to build a Ethylene...

... a successful story in Mexico

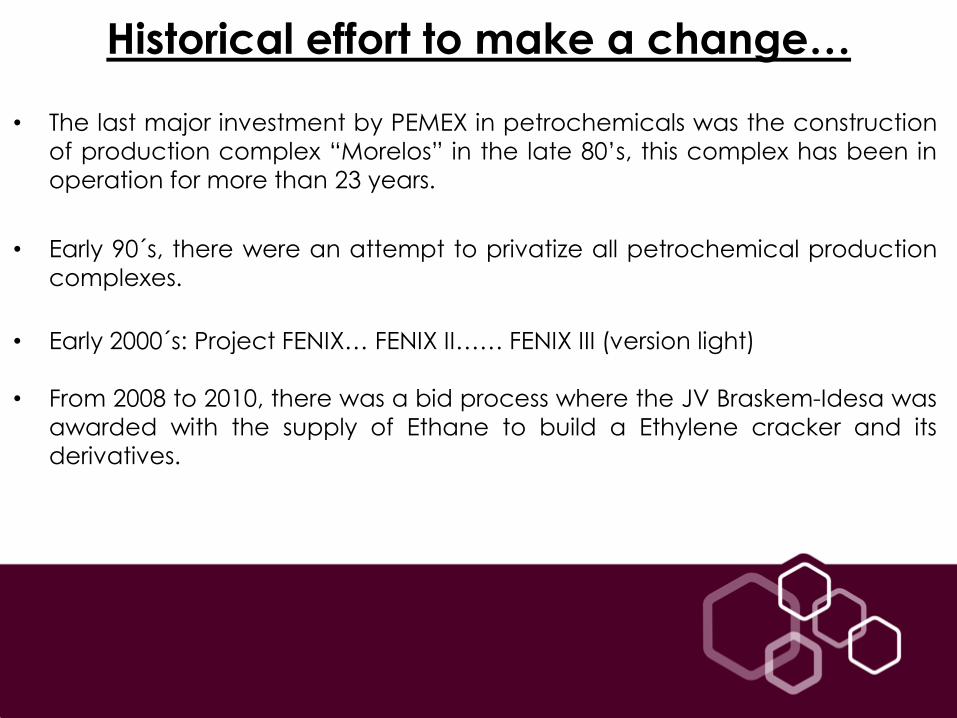

• The last major investment by PEMEX in petrochemicals was the construction

of production complex “Morelos” in the late 80’s, this complex has been in

operation for more than 23 years.

• Early 90´s, there were an attempt to privatize all petrochemical production

complexes.

• Early 2000´s: Project FENIX… FENIX II…… FENIX III (version light)

• From 2008 to 2010, there was a bid process where the JV Braskem-Idesa was

awarded with the supply of Ethane to build a Ethylene cracker and its

derivatives.

Historical effort to make a change…

3

PEMEX Gas Pet.Básica – PGPB

Ethane Cracker

3 PE Plants

Ethane Ethylene 66,000 bpd 1,050 kT/a

1050 kT/a

PEMEX Expl. Prod. - PEP

Gas

HDPE 350 kT/a

LDPE 300 kT/a

HDPE 400 kT/a

What was Etileno XXI project? • It was the project aim to promote the production of 1 Million Tons of Ethylene

and derivatives through the first Mexican private cracker in Mexico.

• BRASKEM IDESA, a JV among the Brazilian BRASKEM and the Mexican IDESA

was awarded with a long term Ethane supply contract.

Polypropylene Polyethylene

Caustic Soda PVC

Basic Inputs Green Ethylene

28 Units in Brazil

5 Units in U.S.

2 Units in Germany

1 Project under implementation

Operational Units Projects under evaluation

Implementation Projects

Leading Petrochemical in Latin America

Largest producer of thermoplastic resins

in the Americas

Larger producer of polypropylene in the

US

First company in the world to launch a

Polyethylene production based on

renewables raw materials

Annual production capacity of 11

million tons of chemicals and

petrochemicals

Financial Ratios: 2011 (USD Mil Millones)

Revenue $ 17.2

EBITDA $ 1.9

Listed on stock exchanges in Brasil, NY

and Spain

Shareholders: Grupo Odebrecht 53,8% Petrobras 46.2% (% del Capital Votante)

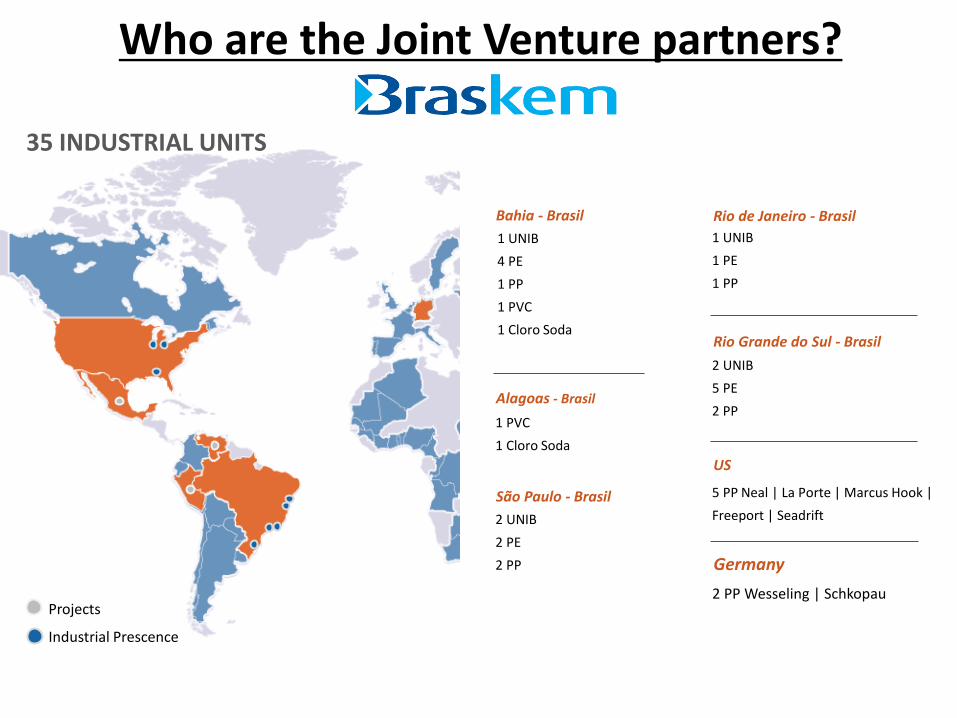

Who are the Joint Venture partners?

Bahia - Brasil

1 UNIB

4 PE

1 PP

1 PVC

1 Cloro Soda

Alagoas - Brasil

1 PVC

1 Cloro Soda

São Paulo - Brasil

2 UNIB

2 PE

2 PP

Rio de Janeiro - Brasil

1 UNIB

1 PE

1 PP

Rio Grande do Sul - Brasil

2 UNIB

5 PE

2 PP

US

5 PP Neal | La Porte | Marcus Hook |

Freeport | Seadrift

Germany

2 PP Wesseling | Schkopau

Industrial Prescence

Projects

35 INDUSTRIAL UNITS

Who are the Joint Venture partners?

Fifth most important Mexican Player in

petrochemicals in Mexico with 56 years experience.

Annual production capacity of 350 thousand tons of products

Indicadores Financieros 2011 Revenues $ 625 (million USD) EBITDA $ 86 (million USD) Assets 4 Industrial production units 12 Distribution branches

Mexican Private Shareholders

Who are the Joint Venture partners?

TIJUANA Baja California Norte

SALTILLO Coahuila

MONTERREY Nuevo León

QUERÉTARO Querétaro

LEÓN Guanajuato

IRAPUATO COATZACOALCOS Veracruz

PUEBLA Puebla

DISTRITO FEDERAL

APIZACO Tlaxcala

GUADALAJARA Jalisco

CULIACÁN Sinaloa

Idesa Petroquímica

Alveg Distribuidor

Idesa Corporativo

Braskem-Idesa Joint venture

Negocios de

Aplicación Joint venture

Excellence Sea & Land

Logistics Logística

VERACRUZ Veracruz

Who are the Joint Venture partners?

Successful factors in the Petrochemical industry:

o Access to market

o Raw Materials

o Technology

o Human Talent

Competitiveness in the Industry

Successful factors in the Petrochemical industry:

o Access to market

o Raw Materials

o Technology

o Human Talent

Competitiveness in the Industry

Manufacturing Production Index (2007=100)* Mexican exports (2007=100)*

80

90

100

110

2007 2008 2009 2010 2011

México

Estados Unidos

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

2007 2008 2009 2010 2011 2012

Química

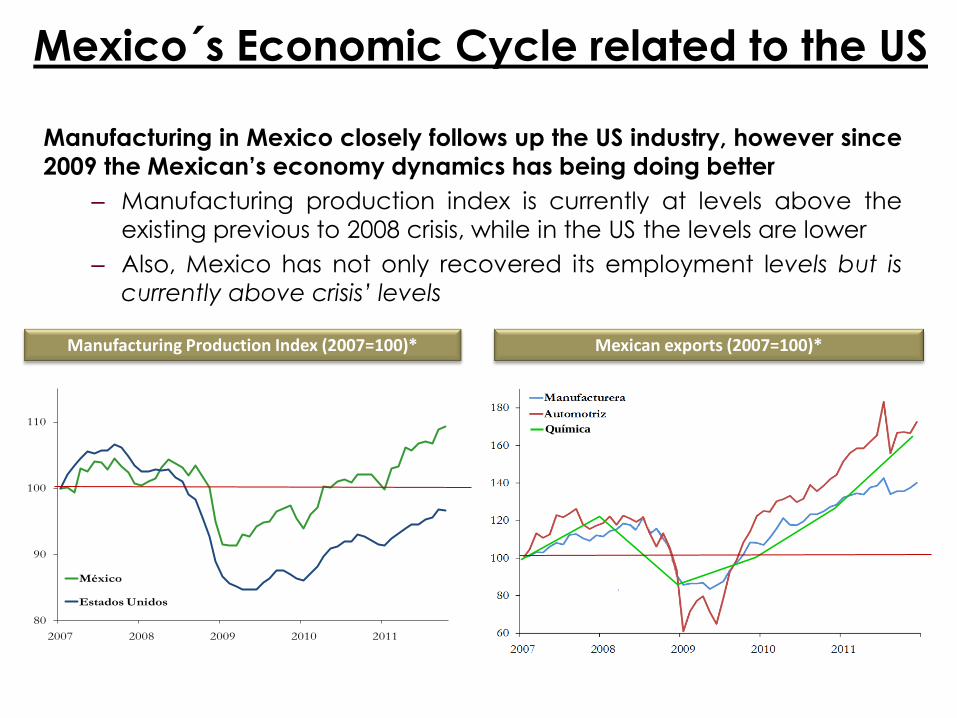

Mexico´s Economic Cycle related to the US

Manufacturing in Mexico closely follows up the US industry, however since

2009 the Mexican’s economy dynamics has being doing better

– Manufacturing production index is currently at levels above the

existing previous to 2008 crisis, while in the US the levels are lower

– Also, Mexico has not only recovered its employment levels but is

currently above crisis’ levels

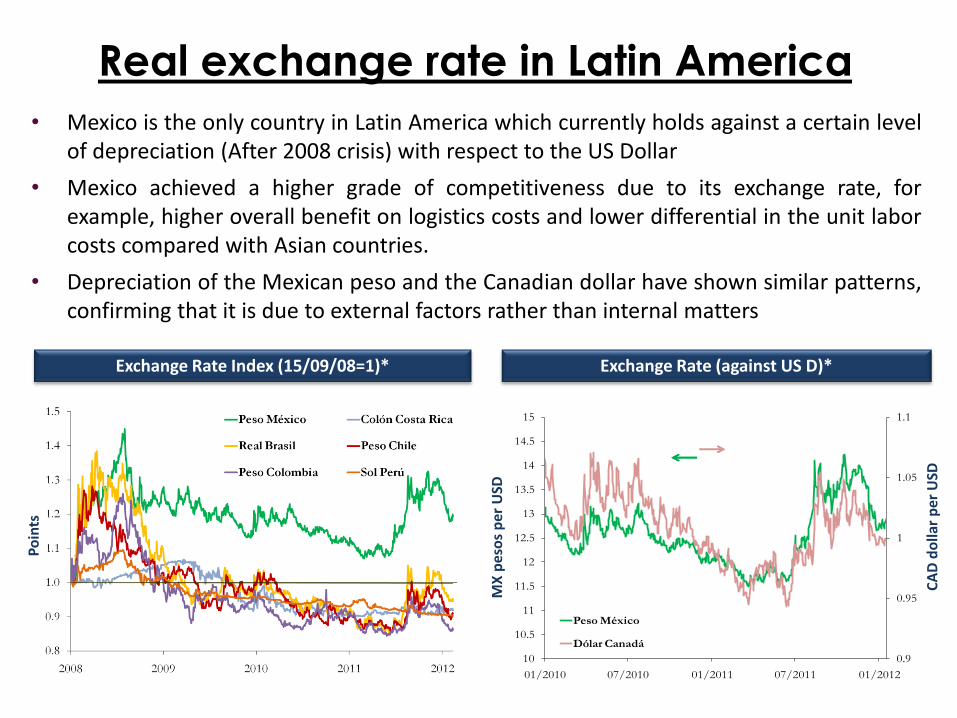

Real exchange rate in Latin America

Exchange Rate Index (15/09/08=1)* Exchange Rate (against US D)*

• Mexico is the only country in Latin America which currently holds against a certain level of depreciation (After 2008 crisis) with respect to the US Dollar

• Mexico achieved a higher grade of competitiveness due to its exchange rate, for example, higher overall benefit on logistics costs and lower differential in the unit labor costs compared with Asian countries.

• Depreciation of the Mexican peso and the Canadian dollar have shown similar patterns, confirming that it is due to external factors rather than internal matters

0.9

0.95

1

1.05

1.1

10

10.5

11

11.5

12

12.5

13

13.5

14

14.5

15

01/2010 07/2010 01/2011 07/2011 01/2012

Peso México

Dólar Canadá

MX

pes

os

per

USD

CA

D d

olla

r p

er U

SD

Po

ints

Global competitiveness trends

• The manufacture is changing from off-shore outsourcing to near sourcing

• China is losing competitiveness:

• Chinese wages have risen between 15% to 20% annually over the past

decade,

• Logistics costs have increased and

• The Chinese yuan continues to appreciate

Monterrey to Chicago 4-5 days by land

(53 foot land container)

Shanghai to Chicago 22 days by sea and land

(40 foot maritime container)

Do

llars

per

ho

ur

Unit Labor Costs (USD/ hrs)* Transportation Costs (USD)*

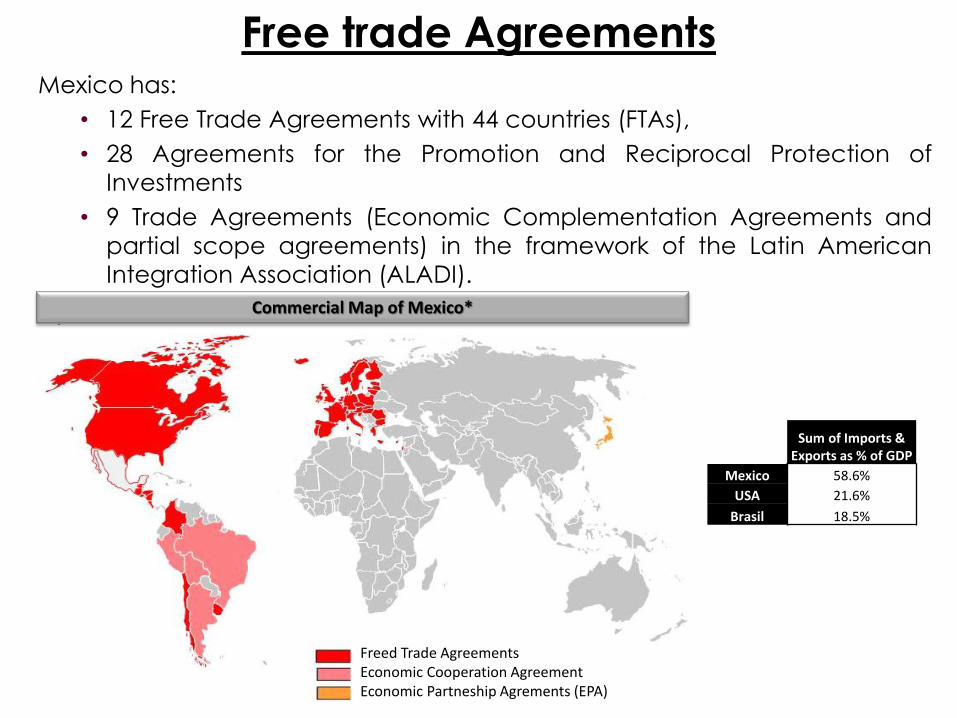

Free trade Agreements Mexico has:

• 12 Free Trade Agreements with 44 countries (FTAs),

• 28 Agreements for the Promotion and Reciprocal Protection of

Investments

• 9 Trade Agreements (Economic Complementation Agreements and

partial scope agreements) in the framework of the Latin American

Integration Association (ALADI).

Commercial Map of Mexico*

Freed Trade Agreements Economic Cooperation Agreement Economic Partneship Agrements (EPA)

Sum of Imports & Exports as % of GDP

Mexico 58.6%

USA 21.6%

Brasil 18.5%

Polyethylene Mexican Market

Current EXXI

Total demand

Successful factors in the Petrochemical industry:

o Access to market

o Raw Materials

o Technology

o Human Talent

Competitiveness in the Industry

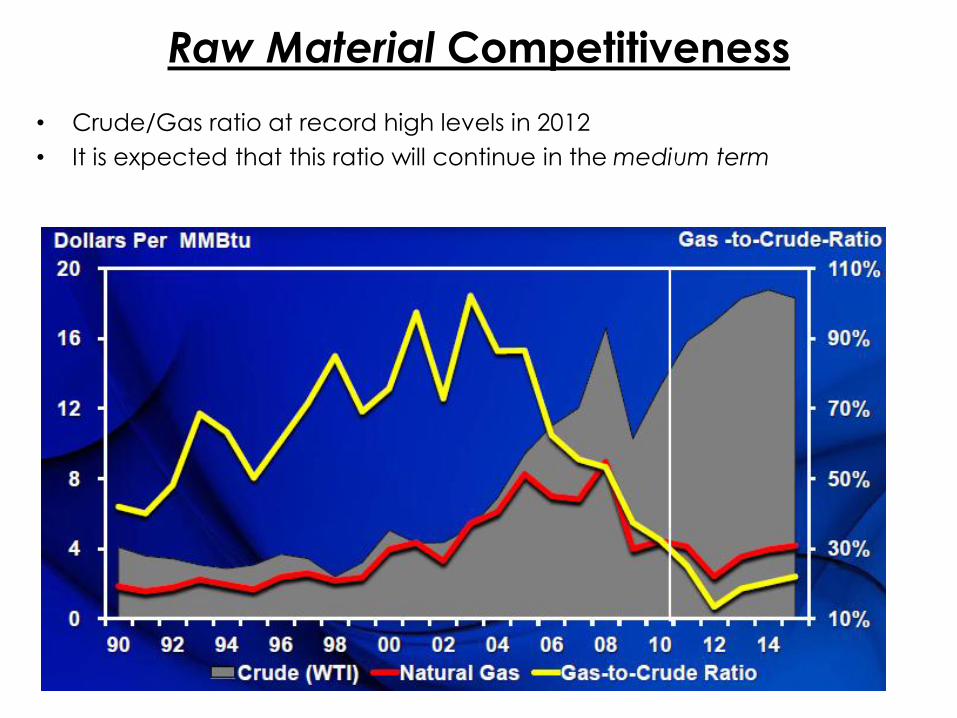

Raw Material Competitiveness

• Crude/Gas ratio at record high levels in 2012

• It is expected that this ratio will continue in the medium term

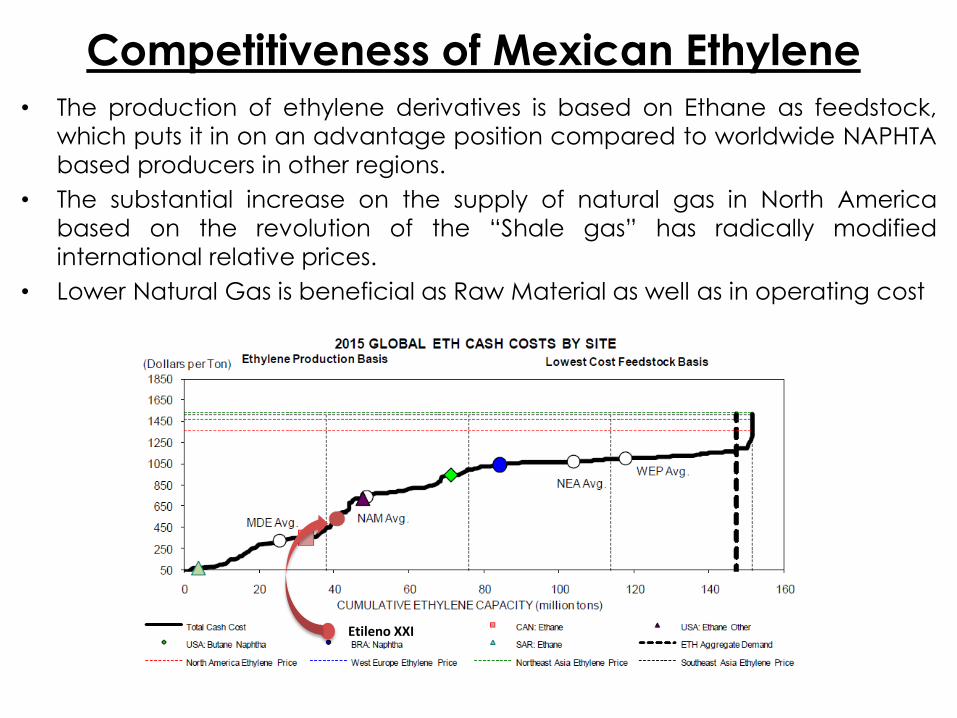

Competitiveness of Mexican Ethylene

México

• The production of ethylene derivatives is based on Ethane as feedstock,

which puts it in on an advantage position compared to worldwide NAPHTA

based producers in other regions.

• The substantial increase on the supply of natural gas in North America

based on the revolution of the “Shale gas” has radically modified

international relative prices.

• Lower Natural Gas is beneficial as Raw Material as well as in operating cost

Etileno XXI

Successful factors in the Petrochemical industry:

o Access to market

o Raw Materials

o Technology

o Human Talent

Competitiveness in the Industry

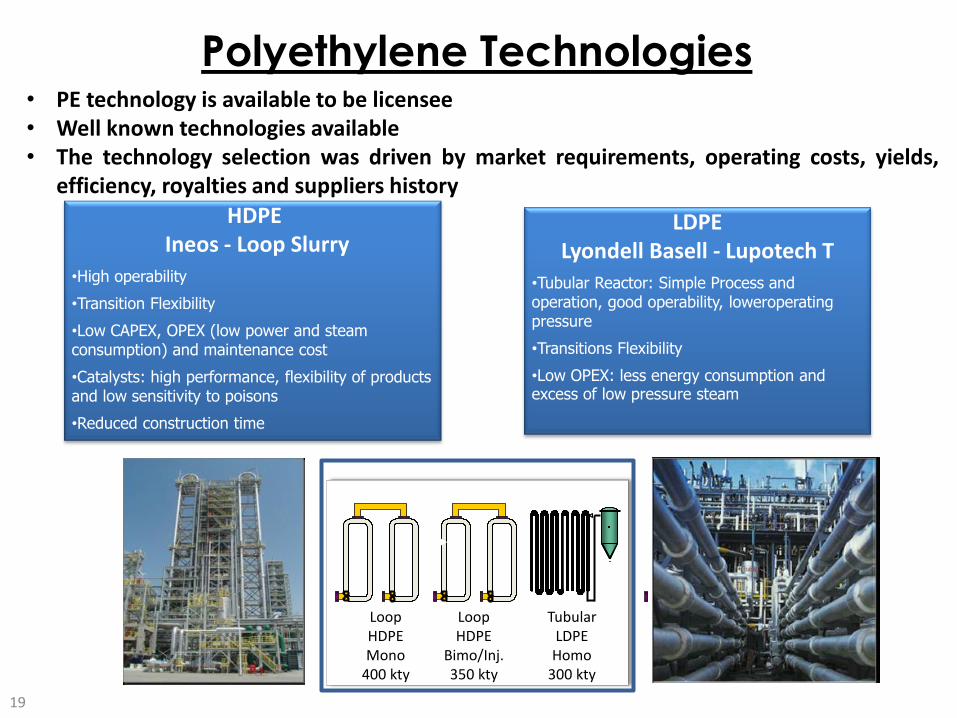

HDPE Ineos - Loop Slurry

•High operability

•Transition Flexibility

•Low CAPEX, OPEX (low power and steam consumption) and maintenance cost

•Catalysts: high performance, flexibility of products and low sensitivity to poisons

•Reduced construction time

• PE technology is available to be licensee • Well known technologies available • The technology selection was driven by market requirements, operating costs, yields,

efficiency, royalties and suppliers history

LDPE Lyondell Basell - Lupotech T

•Tubular Reactor: Simple Process and operation, good operability, loweroperating pressure

•Transitions Flexibility

•Low OPEX: less energy consumption and excess of low pressure steam

Loop HDPE Mono

400 kty

Loop HDPE

Bimo/Inj. 350 kty

Tubular LDPE Homo

300 kty

19

Polyethylene Technologies

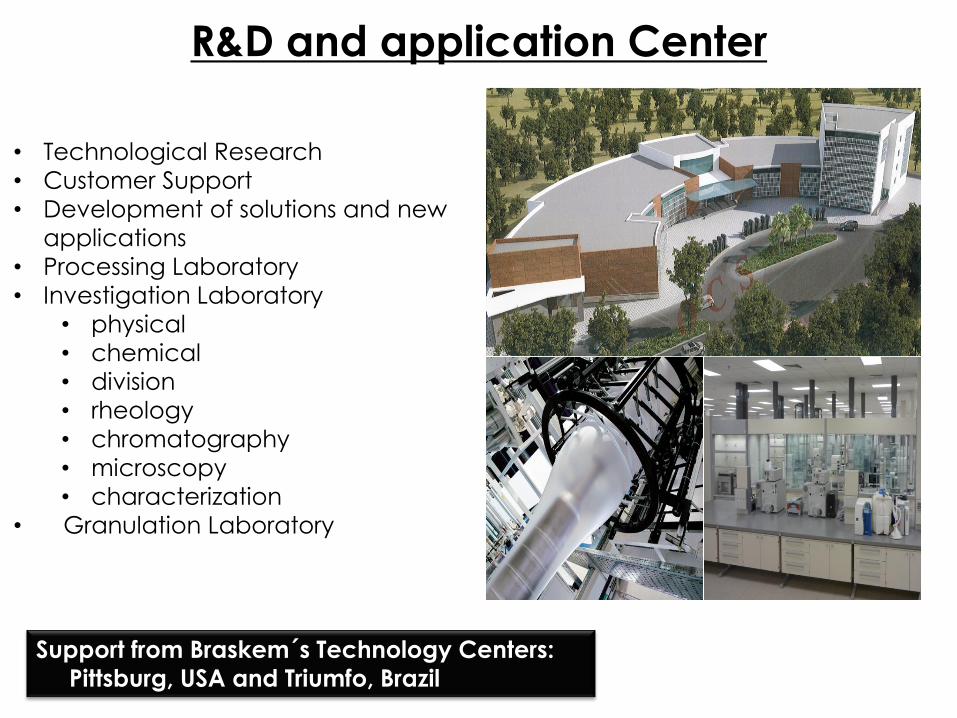

• Technological Research

• Customer Support

• Development of solutions and new

applications

• Processing Laboratory

• Investigation Laboratory

• physical

• chemical

• division

• rheology

• chromatography

• microscopy

• characterization

• Granulation Laboratory

Support from Braskem´s Technology Centers:

Pittsburg, USA and Triumfo, Brazil

R&D and application Center

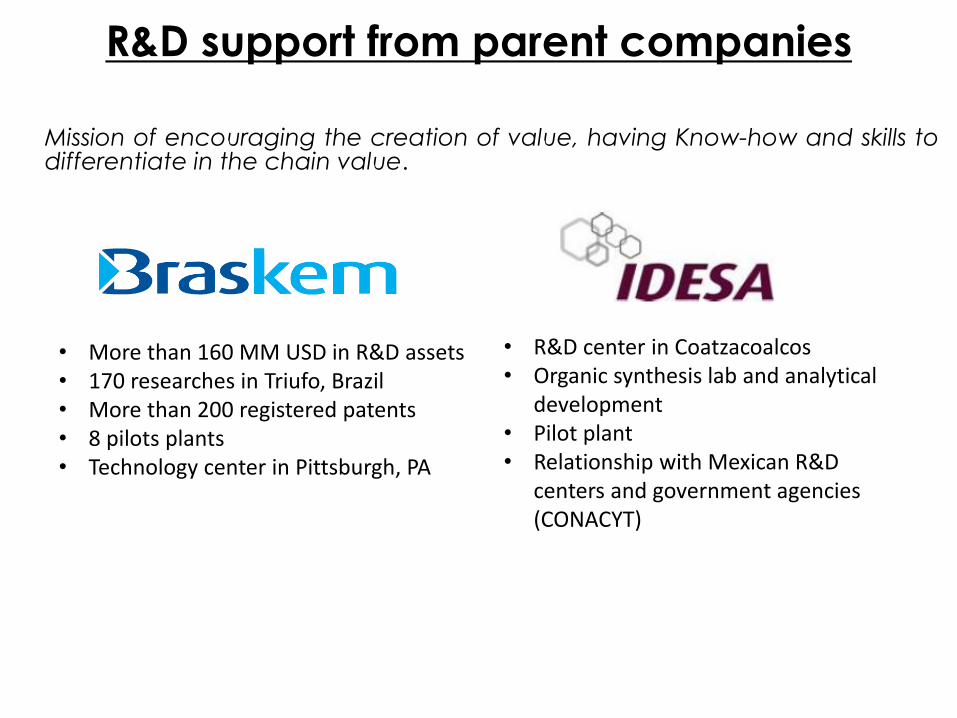

Mission of encouraging the creation of value, having Know-how and skills to differentiate in the chain value.

R&D support from parent companies

• More than 160 MM USD in R&D assets • 170 researches in Triufo, Brazil • More than 200 registered patents • 8 pilots plants • Technology center in Pittsburgh, PA

• R&D center in Coatzacoalcos • Organic synthesis lab and analytical

development • Pilot plant • Relationship with Mexican R&D

centers and government agencies (CONACYT)

Successful factors in the Petrochemical industry:

o Access to market

o Raw Materials

o Technology

o Human Talent

Competitiveness in the Industry

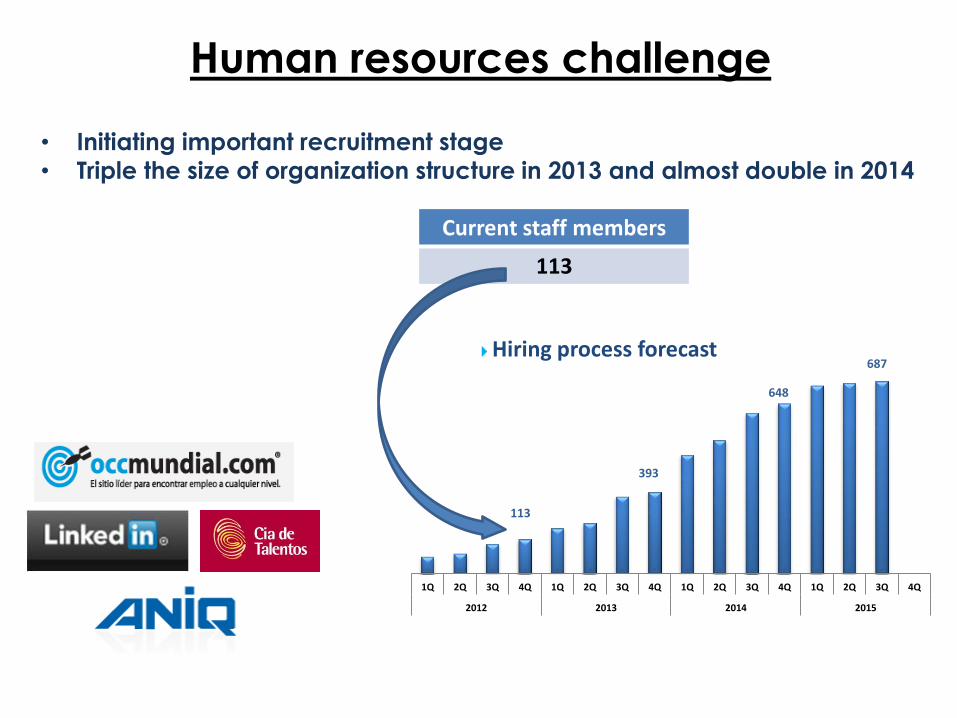

113

393

648

687

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2012 2013 2014 2015

Hiring process forecast

Current staff members

113

• Initiating important recruitment stage

• Triple the size of organization structure in 2013 and almost double in 2014

Human resources challenge

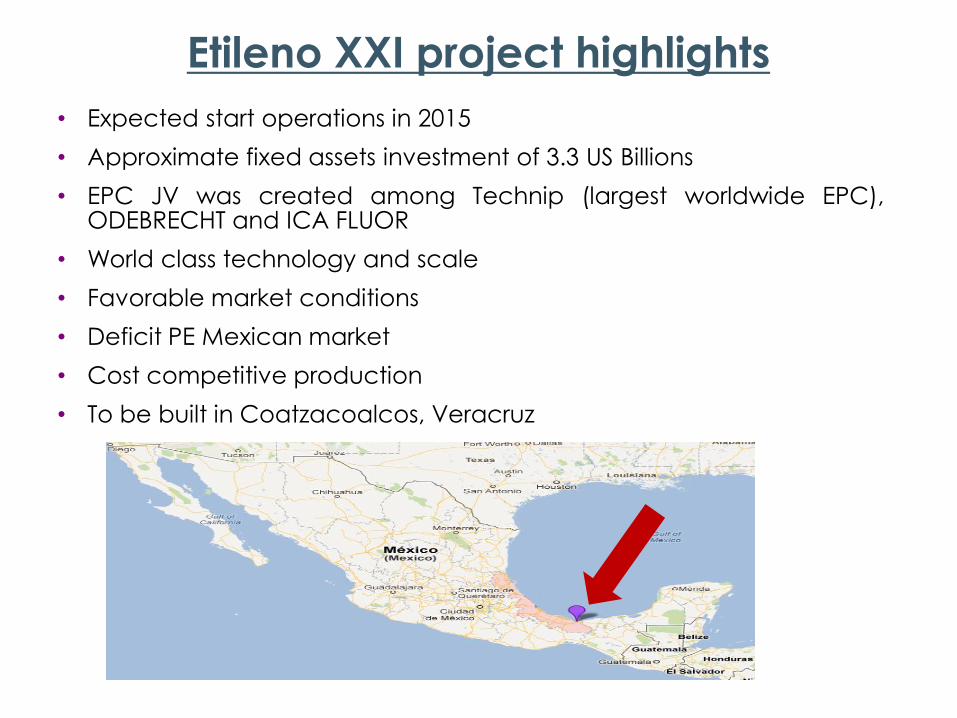

Etileno XXI project highlights

• Expected start operations in 2015

• Approximate fixed assets investment of 3.3 US Billions

• EPC JV was created among Technip (largest worldwide EPC), ODEBRECHT and ICA FLUOR

• World class technology and scale

• Favorable market conditions

• Deficit PE Mexican market

• Cost competitive production

• To be built in Coatzacoalcos, Veracruz

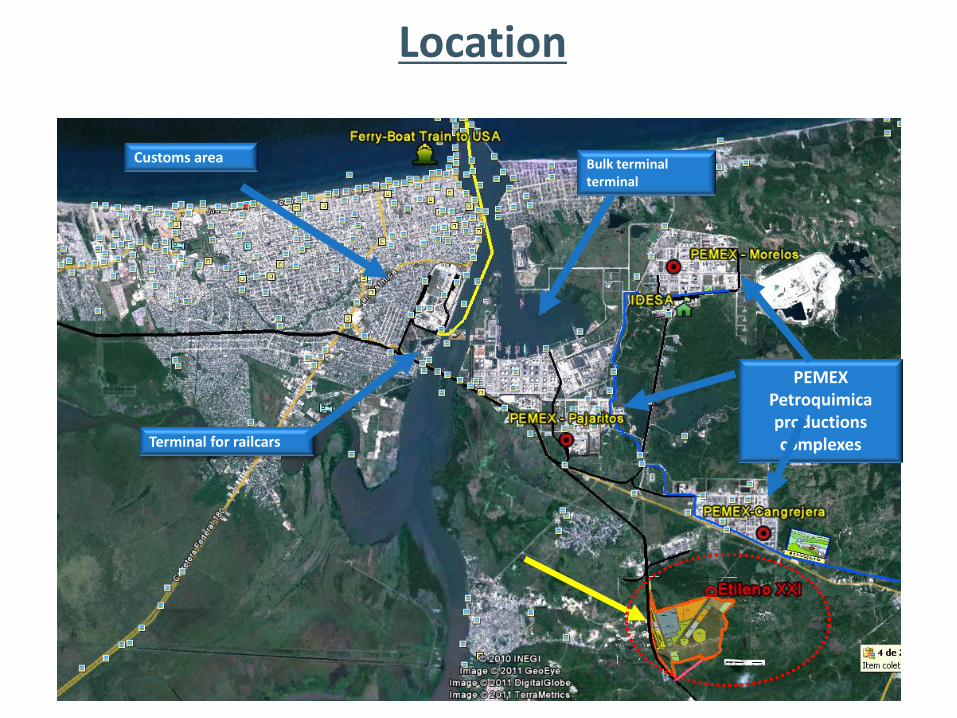

Location

Customs area

Terminal for railcars

Bulk terminal terminal

PEMEX Petroquimica productions complexes

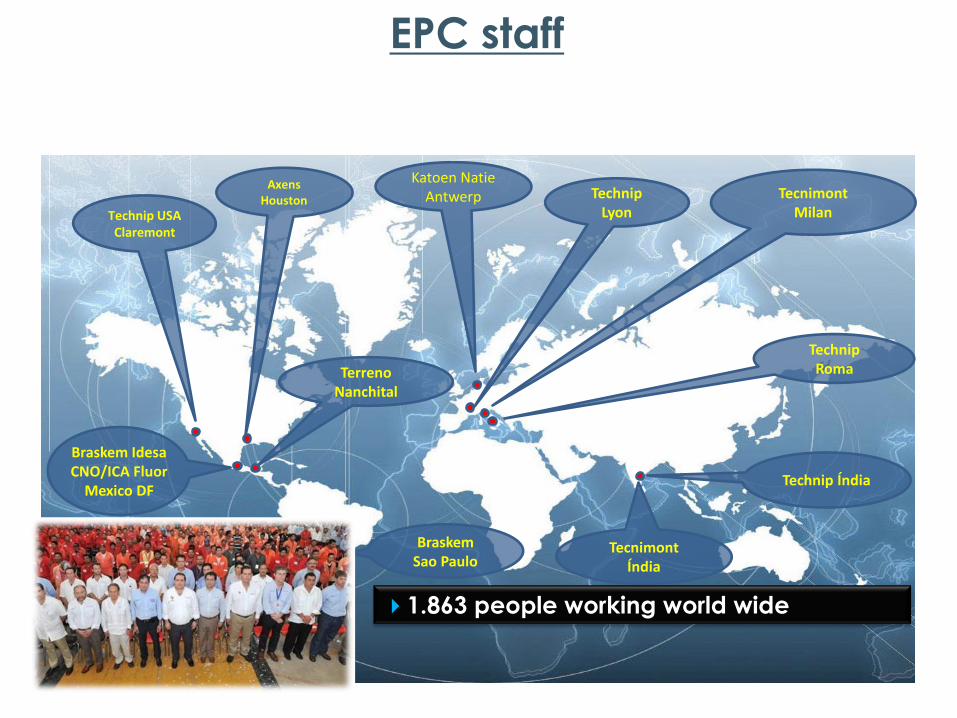

Tecnimont Índia

Braskem Sao Paulo

Technip Lyon

Tecnimont Milan

Technip Roma

Axens Houston

Technip USA Claremont

Terreno Nanchital

Braskem Idesa CNO/ICA Fluor

Mexico DF Technip Índia

Katoen Natie Antwerp

1.863 people working world wide

Equipo Internacional EPC staff

27

Construction headquarters

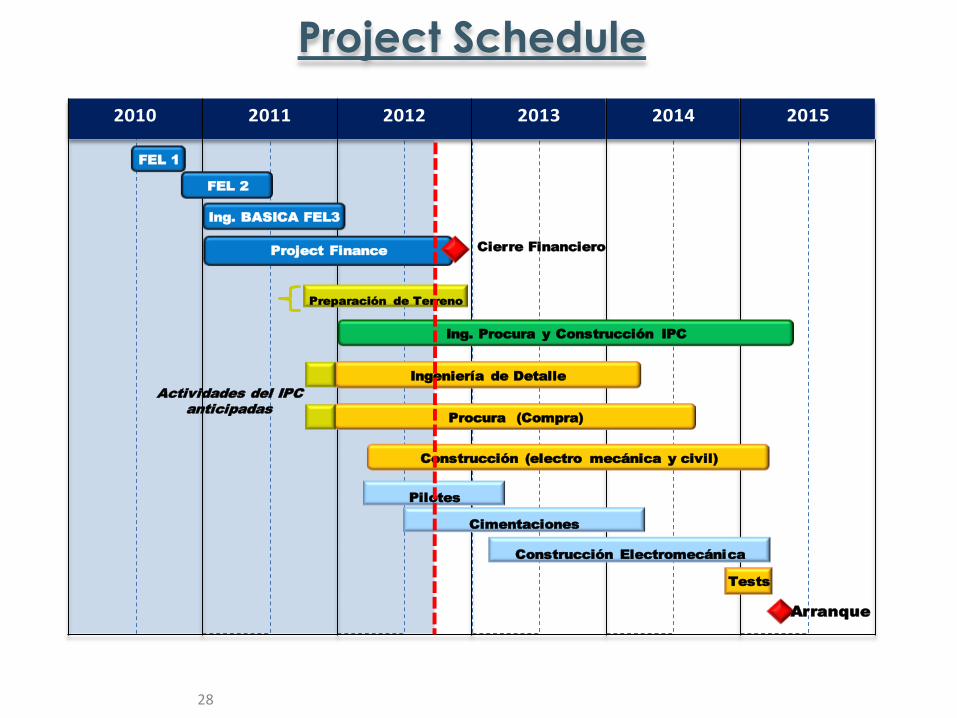

Project Schedule

28

2010 2011 2012 2013 2014 2015

Construcción (electro mecánica y civil)

Preparación de Terreno

Pilotes

Cimentaciones

Construcción Electromecánica

Tests

Ingeniería de Detalle

Procura (Compra)

Ing. Procura y Construcción IPC

FEL 1

FEL 2

Ing. BASICA FEL3

Actividades del IPC

anticipadas

Project FinanceCierre Financiero

Arranque

08 Mar 2012

27 Oct 2011

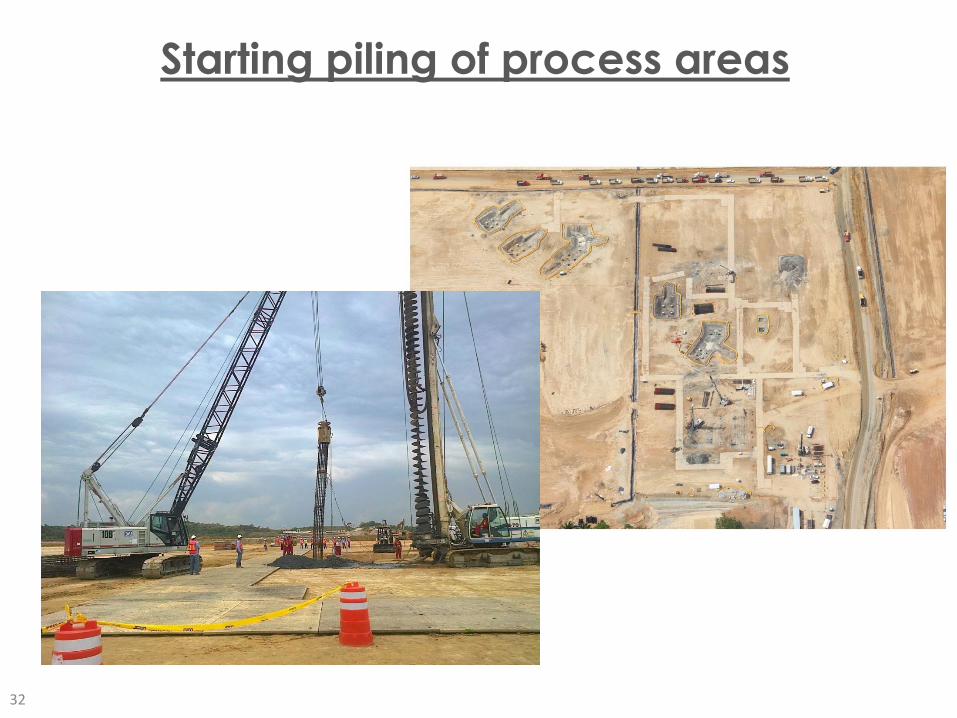

Progress in land preparation

Julio 2011

30

Agosto 2012

Land preparation…..land is ready

Logistic

Utilities

LDPE

Cracker

Progreso de la Preparación del Terreno Land preparation…..land is ready

Starting piling of process areas

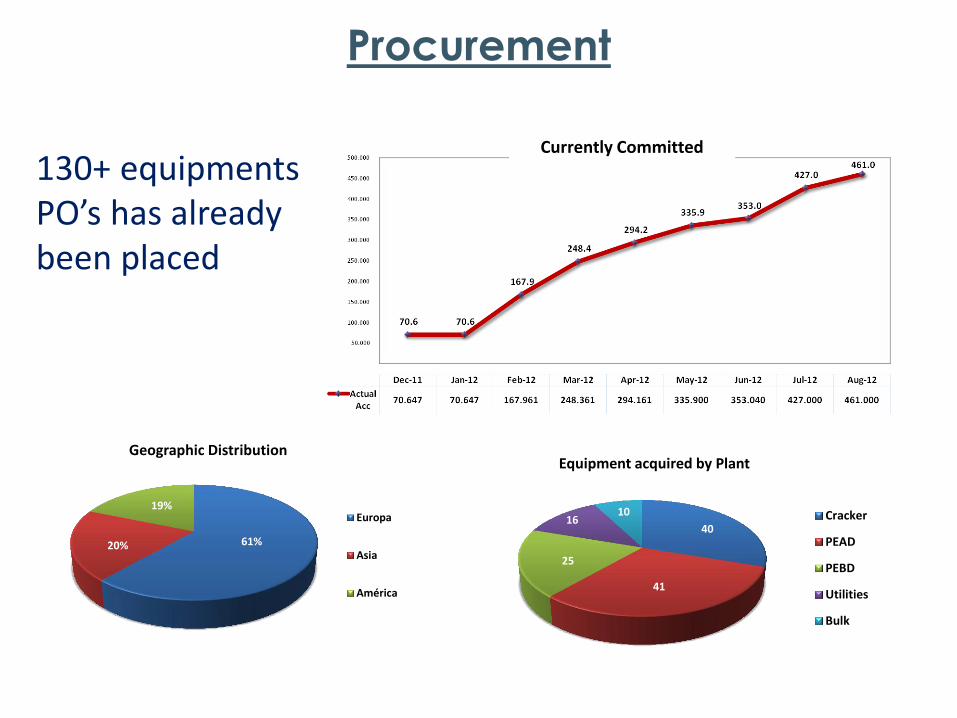

32

40

41

25

16 10

Equipment acquired by Plant

Cracker

PEAD

PEBD

Utilities

Bulk

130+ equipments PO’s has already been placed

61% 20%

19%

Geographic Distribution

Europa

Asia

América

Procurement

Currently Committed

• Identify, pictures, GPS Tags and removal of flora

• Transfer to environmental reserve to be replanted

• ID: Photos, GPS Tags

34

Environmental activities during

land preparation

•Capture

•Relocation to environmental reserve

•Release

•So far in the environmental program for Wildlife relocation, we counted a total of 422 individuals belonging to 64 species

35

Environmental activities during

land preparation

…..Thank you