KANSAI NEROLAC PAINTS LTD - Sify.comim.sify.com/sifycmsimg/may2011/Finance/14968999_kansai.pdf1...

16

1 SYNOPSIS • Kansai Nerolac Paints Ltd is the second largest coating company in India and market leader in Industrial Coatings. • Kansai Nerolac Paints Ltd is a subsidiary of Japan based Kansai Paint Company Limited, which is one of the top ten coating companies in the world. • The Company declares dividend at Rs.10 per share. • The Company divests its stake in Nipa Chemicals for Rs.25.72 crores. • EPS stood at Rs 10.91 against Rs 7.72 with a rise of 41% for the quarter ended Mar 31, 2011. • Net Sales and PAT of the company is expected to grow at a CAGR of 20% and 17% over 2010 to 2013E respectively. Years Net sales EBITDA Net Profit EPS P/E FY 11 21398.80 3139.60 2059.80 38.22 22.21 FY 12E 25678.56 3789.05 2295.28 42.59 19.93 FY 13E 29530.34 4315.61 2629.64 48.80 17.40 Stock Data: Sector: Paints Face Value Rs. Rs.10.00 52 wk. High/Low (Rs.) 1,055.00/657.73 Volume (2 wk. Avg.) 1,169 BSE Code 500165 Market Cap (Rs.In mn) 45752.61 Share Holding Pattern 1 Year Comparative Graph Kansai Nerolac Paints Ltd BSE SENSEX C.M.P: Rs.849.00 Target Price: Rs.976 .00 Date: 30 th April 2011 BUY KANSAI NEROLAC PAINTS LTD Result Update: Q4 FY 11

-

Upload

trinhkhanh -

Category

Documents

-

view

223 -

download

4

Transcript of KANSAI NEROLAC PAINTS LTD - Sify.comim.sify.com/sifycmsimg/may2011/Finance/14968999_kansai.pdf1...

1

SYNOPSIS

• Kansai Nerolac Paints Ltd is the second largest coating company in India and market leader in Industrial Coatings.

• Kansai Nerolac Paints Ltd is a subsidiary of Japan based Kansai Paint Company Limited, which is one of the top ten coating companies in the world.

• The Company declares dividend at Rs.10 per share.

• The Company divests its stake in Nipa Chemicals for Rs.25.72 crores.

• EPS stood at Rs 10.91 against Rs 7.72 with a rise of 41% for the quarter ended Mar 31, 2011.

• Net Sales and PAT of the company is expected to grow at a CAGR of 20% and 17% over 2010 to 2013E respectively.

Years Net sales EBITDA Net Profit EPS P/E

FY 11 21398.80 3139.60 2059.80 38.22 22.21

FY 12E 25678.56 3789.05 2295.28 42.59 19.93

FY 13E 29530.34 4315.61 2629.64 48.80 17.40

Stock Data:

Sector: Paints

Face Value Rs. Rs.10.00

52 wk. High/Low (Rs.) 1,055.00/657.73

Volume (2 wk. Avg.) 1,169

BSE Code 500165

Market Cap (Rs.In mn) 45752.61

Share Holding Pattern

1 Year Comparative Graph

Kansai Nerolac Paints Ltd

BSE SENSEX

C.M.P: Rs.849.00 Target Price: Rs.976 .00 Date: 30th April 2011 BUY

KANSAI NEROLAC PAINTS LTD

Result Update: Q4 FY 11

2

Peer Group Comparison

Name of the company CMP(Rs.) Market

Cap.(Rs.Mn.) EPS(Rs.) P/E(x) P/Bv(x) Dividend (%)

Kansai Nerolac Paints 849.00 45752.61 33.59 25.36 5.94 150.00

Asian Paints 2773.75 266057.5 81.40 34.08 17.09 270.00

Shalimar Paints 291.00 1101.6 28.34 10.27 2.58 75.00 *As on 30/04/2011

Investment Highlights

Results Updates (Q4 FY11)

For the fourth quarter, the top line of the company increased 23%YoY and stood at Rs.5195.90mn against Rs4241.30mn of the same period of the last year. The bottom line of the company for the quarter stood at Rs.588.00mn from Rs.339.20mn of the corresponding period of the previous year i.e. an increase of 73%YoY.

3

EPS of the company for the quarter stood at Rs.10.91 for equity share of Rs.10.00 each.

Expenditure for the quarter stood at Rs.4615.50mn, which is around 26% higher than the corresponding period of the previous year. Raw material cost of the company for the quarter accounts for 70% of the sales of the company and stood at Rs.3644.70mn. Employee cost stood at Rs.242.40mn from Rs.172.80mn.i.e, an increase of 40%YoY.

4

OPM and NPM for the quarter stood at 13% and 11% respectively from 15% and 8% respectively of the same period of the last year.

• FY11 Performance in line with expectation The Company’s Top line has increased 25.33% to Rs.21398.80mn from Rs.17074.10mn of FY10. Bottom line for the year increased 24% to Rs.2059.80mn. from Rs.1655.00mn of FY10. These numbers are in line with our expectation. Earnings per share of the company for the year stood at Rs.38.22 per share.

5

Expenditure of the company for the year stood at Rs.18482.30mn, which is around 28% higher than FY10. Raw materials Cost for the year stood at Rs.14004.6mn from Rs.10689.10mn of FY10 i.e. an increase of 31%YoY. Other Expenditure increased 20%YoY to Rs.3563.40mn. Interest decreased 30%YoY to Rs.8.40mn, and depreciation increased 12%YoY to Rs.493.60mn.

Kansai Nerolac Paints declares dividend at Rs.10 per share

The Company declared a dividend of Rs.10 per share at its annual general

meeting.

Kansai Nerolac Paints divests its stake in Nipa Chemicals

The Company divested its 49% stake in Nipa Chemicals Ltd., an unlisted Indian

Company, for an amount of Rs.25.72 crores. The Company decided that it is

not their core business so they decided to divest. With the amount of the money

the management is planning to invest in applications that provide competitive

advantage.

Company Profile

Kansai Nerolac Paints Ltd. is the second largest coating company in India and market

leader in Industrial Coatings. It’s Industrial Coatings it has a wide range of products

in the Automotive, Powder, General Industrial and High performance Coatings space.

Nerolac paint, as it is popularly known, is an established brand in decorative paints.

Kansai Nerolac Paints Ltd is a subsidiary of Japan based Kansai Paint Company

Limited, which is one of the top ten coating companies in the world. The technological

edge of Kansai helps us constantly innovate and come up with products that meet

consumer need gaps. Kansai Nerolac has always believed that the key to its business

is:

• Technology

• Research & Development

• Innovations

• Quality

6

Company Products

• Decorative Paints

• Automotive Coatings

• General Industries Coatings

• High Performance Coatings

• Powder Coatings

• Specialty Coatings

In India the company has presence in Assam, Goa, Gujarat, Haryana, Himachal

Pradesh, Madhya Pradesh, Orissa, West Bengal, Rajasthan, Maharashtra, Punjab,

Uttaranchal, Bihar, New Delhi, Tamil Nadu, Uttar Pradesh and many more.

Company’s manufacturing units have received ISO 9001-2000, ISO-14001 and

OHSAS-18001 for its quality management. Company has also implemented Japanese

5-S and TPM (total productive maintenance) concepts in organization.

Nerolac has a wide distribution network of over 11,000 dealers which one of the key

strength of company. Company also operates through 66 depots.

Company’s R&D facility focuses on improving its manufacturing processes and

innovate its products. This facility has officially recognized by the Department of

Science and Technology (DTI), Government of India.

Company has technically collaborated with two companies Kansai Paint Co. and

Oshima Kogyo Co. of Japan. The company markets its products under the brand

name such as 'Impressions', 'Beauty', 'Excel' and 'Suraksha'.

7

Financials Results 12 Months Ended Profit & Loss Account (Standalone)

Value(Rs.in.mn) FY10 FY11 FY12E FY13E

Description 12m 12m 12m 12m

Net Sales 17074.10 21398.80 25678.56 29530.34

Other Income 193.50 223.10 245.41 269.95

Total Income 17267.60 21621.90 25923.97 29800.30

Expenditure -14426.90 -18482.30 -22134.92 -25484.69

Operating Profit 2840.70 3139.60 3789.05 4315.61

Interest -12.00 -8.40 -13.31 -14.64

Gross profit 2828.70 3131.20 3775.74 4300.97

Depreciation -442.60 -493.60 -542.96 -597.26

Exceptional Items - 253.70 - -

Profit Before Tax 2386.10 2891.30 3232.78 3703.71

Tax -731.10 -831.50 -937.51 -1074.08

Net Profit 1655.00 2059.80 2295.28 2629.64

Equity capital 269.50 538.90 538.90 538.90

Reserves 7458.70 8828.70 11123.98 13753.61

Face Value 10.00 10.00 10.00 10.00

Total No. of Shares 26.95 53.89 53.89 53.89

EPS 61.41

38.22 42.59 48.80

8

Quarterly Ended Profit & Loss Account (Standalone)

Value(Rs.in.mn) 30-Sep-10 31-Dec-10 31-Mar-11 30-Jun-11E

Description 3m 3m 3m 3m

Net sales 5345.10 5603.80 5195.90 5975.29

Other income 46.40 43.30 81.30 89.43

Total Income 5391.50 5647.10 5277.20 6064.72

Expenditure -4504.30 -4916.30 -4615.50 -5102.89

Operating profit 887.20 730.80 661.70 961.82

Interest -2.00 -2.40 -0.90 -0.95

Gross profit 885.20 728.40 660.80 960.88

Depreciation -121.40 -127.90 -132.10 -136.06

Exceptional Items - - 253.10 -

Profit Before Tax 763.80 600.50 781.80 824.81

Tax -227.70 -184.60 -193.80 -230.95

Net Profit 536.10 415.90 588.00 593.87

Equity capital 538.90 538.90 538.90 538.90

Face Value 10.00 10.00 10.00 10.00

Total No. of Shares 53.89 53.89 53.89 53.89

EPS 9.95 7.72 10.91 11.02

9

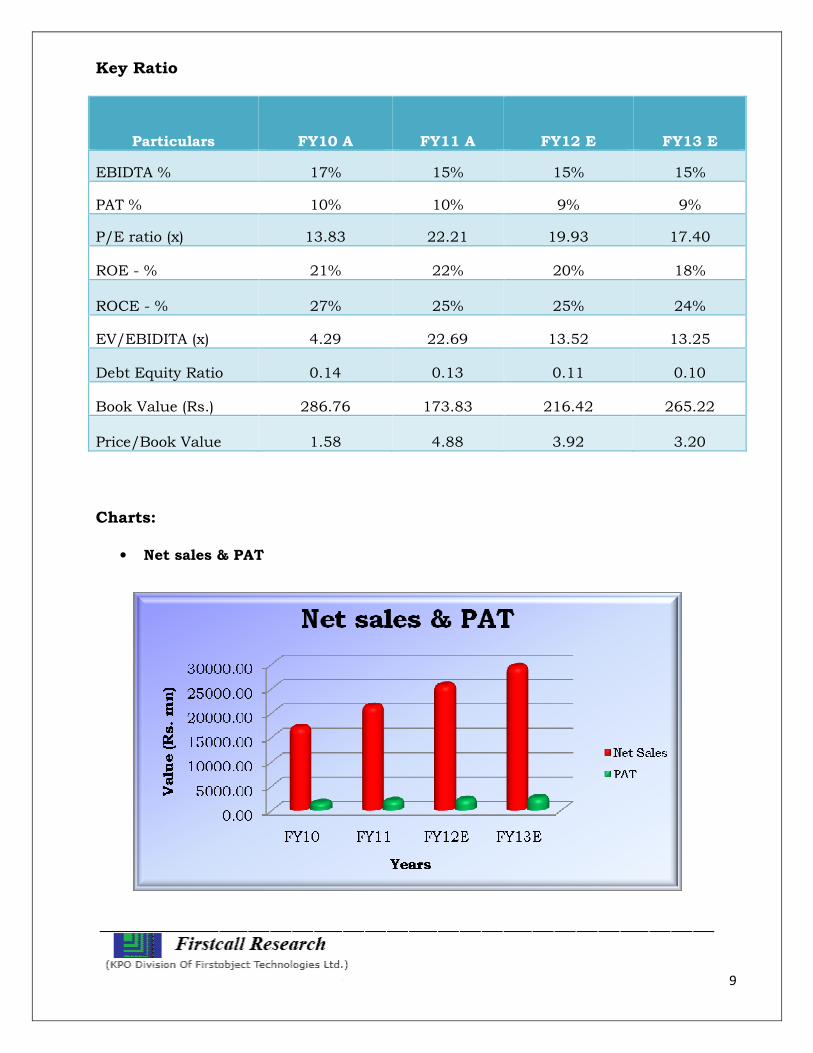

Key Ratio

Particulars FY10 A FY11 A FY12 E FY13 E

EBIDTA % 17% 15% 15% 15%

PAT % 10% 10% 9% 9%

P/E ratio (x) 13.83 22.21 19.93 17.40

ROE - % 21% 22% 20% 18%

ROCE - % 27% 25% 25% 24%

EV/EBIDITA (x) 4.29 22.69 13.52 13.25

Debt Equity Ratio 0.14 0.13 0.11 0.10

Book Value (Rs.) 286.76 173.83 216.42 265.22

Price/Book Value 1.58 4.88 3.92 3.20

Charts:

• Net sales & PAT

10

• P/E Ratio (x)

• P/BV (X)

11

• EV/EBITDA(X)

Outlook and Conclusion

At the market price of Rs.849.00, the stock is trading at 19.93 x and 17.40 x for FY12E and FY13E respectively.

On the basis of EV/EBDITA, the stock trades at 13.52 x for FY12E and 13.25 x for FY13E.

Price to book value of the company is expected to be at 3.92 x for FY12E and 3.20 x for FY13E respectively.

EPS of the company is expected to be at Rs.42.59 and Rs.48.80 for the earnings of FY12E and FY13E respectively.

The top line and bottom line of the company are expected to grow at a CAGR of 20% and 17% respectively over FY10 to FY13E.

We recommend ‘BUY’ this stock with a target price of Rs.976.00 for medium to long term investment.

12

Industry Overview Paint industry in India has been long considered as the barometer of Industrial

activity in the country. The industry has witnessed buoyant growth during the last

decade riding on increasing per-capita disposable incomes in the country and the

boom in real estate and automobile industry.

Despite the sharp growth in recent times, the per capita consumption of paints in

India remains very low at 0.8 kg per year compared with 4 kg in the South East Asian

nations and 22 kg in developed countries. The global average per capita consumption

is around 15 kg. This leaves much room for growth for the industry going forward as

the Indian economy braces for a high growth trajectory in the current decade.

Profile of the Industry

The paint market can be divided into decorative paints which cater to household and

industrial paints which cater to needs of automotive, white goods and other

industries. The demand for decorative paints is highly price-sensitive and also

cyclical in nature. Monsoon represents the slack season while the peak business

period is the Sept-Oct festival season when most people repaint their houses close to

Diwali. Decorative paints can further be classified into premium, medium and

distemper segments. Premium decorative paints are acrylic emulsions used mostly in

the metros and other large cities and high-end offices. The medium range consists of

enamels, popular in smaller cities and towns. Distempers are economy products and

are used in plenty in the suburban and rural markets. This segment is dominated by

the unorganized sector players.

The industrial paints segment, on the other hand, is a high volume-low margin

business. Industrial paints include powder coatings, high performance coating and

automotive and marine paints. Nearly two-thirds of the industrial paint demand in

the country comes from the automotive sector while the rest is constituted by

producers of white goods, electronics etc.

13

The share of industrial paints in the total paint consumption of the nation is very low

compared to global standards. It accounts for nearly 30% of the paint market with

70% of paints sold in India belonging to the decorative purposes. In most developed

countries, the ratio of decorative paints and industrial paints is around 50:50. But,

with the economy growing rapidly over the last decade and industries like automotive

and consumer durables picking up speed, the ratio is likely to improve going forward.

Market Structure

Paint industry is characterized by both organized and unorganized segments.

Organized segment controls nearly 80% of total industry output. Asian Paints is the

market leader in the organized sector with 37% of the market share. Other two big

companies Berger and Nerolac accounts for 18% and 15% share respectively.

Unorganized segment consists of around 2000 small companies which usually cater

to the local demand, particularly in household paints.

Current Scenario

Paint industry in India has seen tremendous growth in the last decade. However, like

the rest of the world, the industry faced surge in cost of production in early 2008 and

some slack in demand towards end of the year as economy slowed down. However,

with a rapid recovery in the Indian economy, the paint industry is back on track and

saw strong growth in 2009.

Strong Performance in FY10

The performance of the Industry in the last fiscal was much better than anticipated

at the beginning of the year. The first half of FY10 was better than expected and in

the second half the Indian growth story was seen in all sectors of the economy.

Construction activity revived and capital expenditure recovered across sectors. A

combination of good demand and lower than expected raw material prices helped the

paint industry record excellent growth in revenues and even better growth in profits.

The market for all categories of paints produced in India is estimated to have grown

by about 18% by value over the previous fiscal year.

14

Decorative Paints

As stated earlier, decorative paints account for around 70% of the overall paint

market in India and most of the companies saw good revenue in this segment. The

decline in raw material prices helped boost revenue of all the companies. All though

cost of production has started to increase in 2010-11, with strong overall economic

growth and revival in construction activity, the segment is set to perform well in the

current fiscal as well.

Industrial Paints

With sharp surge in the industrial activity, industrial paints segment too has

performed very well over the last one year. Both consumer durables and automotive

sales in the country have seen an unprecedented rally over last several months,

generating massive demand for the paint industry.

New Capex Cycle Begins

Riding on the strong sales seen over last few quarters and improvement in margins,

the paint industry is set to enter a new capex cycle. India's largest paint maker Asian

Paints is investing Rs 735 crore for a 400,000 tonne a year plant in Maharashtra and

the first phase of the project is expected to be commissioned by end-2012. Second

biggest paint company Kansai Nerolac Paints is also investing Rs 600 crore to raise

capacity by 50% over next three years. Berger Paints, the third-largest player, plans

to increase its capacity from 250,000 tonnes to 450,000 tonne over the next two

years. We expect that with rapid growth in economy, rising disposable incomes and

living standards and sharp surge in industrial production, the capacity expansion

will help the industry to cater to rising demand and boost top line of the industry.

Outlook

The Rs 13,000-crore paint industry has been growing at over 15% due to high

demand from decorative paints led by housing and real estate construction, and

industrial paints led by strong performance of automotive and white goods

industries. With strong outlook of the Indian economy, we expect per-capita paint

consumption will grow rapidly going forward, providing the key to sustained high

15

growth to the industry. Historically, the industry has grown at nearly 1.5x-2x the

growth of national income. We expect the Indian economy to post 8-10% average

growth over the next decade, which provides for a lot of scope for the paint industry

to sustain its high growth trajectory seen in recent years.

On the fillip side, the industry faces a volatile cost structure. After a surge in early

2008, cost of production for the paint industry came down as the commodity rally

waned. However, over the last couple of quarters, costs have started to increase

again. Prices of titanium dioxide, the key raw material, have risen 8% since January

and are expected to increase another 5% in the next few months. Prices of other raw

materials are also on an uptrend.

Overall, however, we believe that the oligopolistic nature of the organized sector and

strong demand growth scenario will provide enough market power to the paint

makers to pass on most of the increase in costs to consumers, particularly in the

decorative segment. In the industrial segment, while the prices often rise after

substantial lag to the rise in costs, increasing volumes in wake of high growth in

auto, consumer goods and infrastructure spaces projects can help mitigate the

impact of rise in costs.

16

_______________ ____ _________________________

Disclaimer:

This document prepared by our research analysts does not constitute an offer or solicitation

for the purchase or sale of any financial instrument or as an official confirmation of any

transaction. The information contained herein is from publicly available data or other

sources believed to be reliable but do not represent that it is accurate or complete and it

should not be relied on as such. Firstcall India Equity Advisors Pvt. Ltd. or any of it’s

affiliates shall not be in any way responsible for any loss or damage that may arise to any

person from any inadvertent error in the information contained in this report. This document

is provide for assistance only and is not intended to be and must not alone be taken as the

basis for an investment decision.

Firstcall India Equity Research: Email – [email protected]

C.V.S.L.Kameswari Pharma

U. Janaki Rao Capital Goods

D. Ashakirankumar Automobile

A. Rajesh Babu FMCG

H.Lavanya Oil & Gas

T.Joshna Devi Diversified

G.Bharani Bhukta Banking

Dheeraj Bhatia Diversified

Manoj kotian Diversified

Nimesh Gada Diversified

Firstcall India also provides

Firstcall India Equity Advisors Pvt.Ltd focuses on, IPO’s, QIP’s, F.P.O’s,Takeover

Offers, Offer for Sale and Buy Back Offerings.

Corporate Finance Offerings include Foreign Currency Loan Syndications,

Placement of Equity / Debt with multilateral organizations, Short Term Funds

Management Debt & Equity, Working Capital Limits, Equity & Debt

Syndications and Structured Deals.

Corporate Advisory Offerings include Mergers & Acquisitions(domestic and

cross-border), divestitures, spin-offs, valuation of business, corporate

restructuring-Capital and Debt, Turnkey Corporate Revival – Planning &

Execution, Project Financing, Venture capital, Private Equity and Financial

Joint Ventures

Firstcall India also provides Financial Advisory services with respect to raising

of capital through FCCBs, GDRs, ADRs and listing of the same on International

Stock Exchanges namely AIMs, Luxembourg, Singapore Stock Exchanges and

other international stock exchanges.

For Further Details Contact:

3rd Floor,Sankalp,The Bureau,Dr.R.C.Marg,Chembur,Mumbai 400 071

Tel. : 022-2527 2510/2527 6077/25276089 Telefax : 022-25276089

E-mail: [email protected]

www.firstcallindiaequity.com