JSW Steel Limited · modernization-cum-capacity enhancement, 0.2MTPA Tin plate mill ... Manage...

45

JSW Steel Limited Investor Presentation August 2017

Transcript of JSW Steel Limited · modernization-cum-capacity enhancement, 0.2MTPA Tin plate mill ... Manage...

JSW Steel LimitedInvestor PresentationAugust 2017

2

Agenda

Overview Value Proposition

Performance Overview

Guidance Business Environment

3* Listed company

^ USD/` = 64.0773 (RBI reference rate as on July 31, 2017)

JSW Group – overview

Presence across the core sectors

JSW Steel:8,346

JSW Energy:

1,803

As on July 31, 2017

JSW Steel*: India’s leading integrated steelproducer (Steel making capacity: 18 MTPA)

JSW Cement: Manufacturer of PSC, OPCand GGBS cement (Operational plants’capacity: 10.3 MTPA)

JSW Infrastructure: Engaged in development and operations of ports (Operational capacity: 70 MTPA)

JSW Energy*: Engaged across the value chainof power business (Operational plants’capacity: 4,531 MW)

Market cap of listed businesses ($10,149 mn^)

4

JSW Steel – India’s leading steel manufacturer

Leading steel manufacturer in

India

Integrated manufacturing

process

Diversified product portfolio

Strong distribution network and

export presence

Globalpresence

Technological competence

Combination of state-of-the-art steel making technologies: Corex, DRI, Blast Furnace

International presence in mining assets (Chile, US and Mozambique) and value-added facilities (Plate and Pipe mill in US)

Integrated steel manufacturing facilities – from raw material processing plants to value-added product capacities

Installed capacity 18 MTPA, at strategic locations in South and West India

Pan India marketing and distribution network, export presence in ~100 countries across the 5 continents

Extensive portfolio of products – HR, CR, galvanized/galvalume, pre-painted, tinplates, electrical steel (CRNO), TMT bars, wire rods, special steel bars, rounds and blooms

5(1) Calculated as consolidated EBITDA/steel sales, (2) From 31st March 2002 to 31st March 2017,

(3) USD/` = 64.8386 (RBI reference rate as on Mar 31, 2017)

Transformational journey to market leadership

FY2002 FY2010 FY2017

Capacity (MTPA) 1.6 7.8 18.0 CAGR FY2002–FY2017: 18%Capacity increased to 18MTPA in Mar 2016

Production (MTPA) 1.3 6.0 15.8 CAGR FY2002–FY2017: 18%

Revenue (USD mn) 268 3,006 9,336 CAGR FY2002–FY2017: 27%

EBITDA (USD mn) 43 641 1,878 CAGR FY2002–FY2017: 29%

EBITDA/ton(1) (USD/ton) 34 112 128 CAGR FY2002–FY2017: 9%

Market Cap (USD mn) 81 3,565 7,016 Significant value creation with 86x increase in market value(2)

Technology Corex Corex, BF Corex, BF, DRI Combination of industry leading technologies

Product Mix FlatsFlats, long,

special steel and value added

Flat, long, special steel & high value-added

auto, electrical grade

Continuously expanding product canvas with focus on high-end value-added products

Unrelenting progress through the economic cycles

6

Continuously evaluating opportunities to deliver value enhancing growth

Key new projects by 2020

Dolvi: Capacity expansion to 10 MTPA, 1.5MTPA Coke Oven at Dolvi Coke Projects Limited

Vijayanagar: BF-3 revamp & upgradation, CRM-1 complex capacity expansion, Pipe Conveyor System for Iron ore and new Water Reservoir

Salem: capacity expansion to 1.2MTPA

Vasind and Tarapur: modernization-cum-capacity enhancement, 0.2MTPA Tin plate mill

2017

74% stake in Praxair’s(3)

the industrial gases joint venture(4)

Won 5 iron ore mines in Karnataka (111 mntonnes estimated resources)

2015

CRM2—Phase 2

0.2MTPA Electrical Steel Mill

2016

18 MTPA

Won Moitra coal mine in Jharkhand

2009

7.8 MTPA

2014

New CRM2—Phase I

4 MTPA—Pellet Plant(2)

1 MTPA—Coke Oven Plant(2)

Welspun Maxsteel

50% stake in VallabhTinplate

2012

HSM-2 Capacity Expansion to 5 MTPA

2013

14.3 MTPA post Ispat merger

2010

3.5 MTPA—HSM-2

JSW-JFE Strategic Partnership

Coal mining concessions in US

2011

49.3% stake in Ispat Industries

2008

Iron Ore mines in Chile

2007

4.8 MTPA

1.0 MTPA—CRM

Plate and Pipe Mill in US

Coal mining concessions in Mozambique

2006

3.8 MTPA

2005

2.5 MTPA

Color Coating Line

EURO IKON2002

1.6 MTPA

2004

SISCOL(1)

(1) Southern Iron and Steel Company, (2) Amba River Coke Limited, (3) Praxair India Private Limited, (4) JSW Praxair Oxygen Private Limited

Combination of Organic and Inorganic growth

7(1) Translated at USD/` = 44.65 (RBI reference rate as on Mar 31, 2011)

JSW – JFE strategic partnership

Value creation for both the partners

JSW Steel:

Focused expansion plans in India

Optimized capital structure through deleveraging

Access to cutting edge technologies

JFE:

Presence in growing Indian market

Future growth through equity participation

Strategic production base in India for existing automobile customers

Technology agreements

Benefits to JSW Steel driven by:

Access to fast growing auto steel market

Technical know-how for electrical steel manufacturing

Short learning curve

Application engineering

New product development

Benchmarking and personnel training

General technical assistance agreements

Operational excellence and cost reduction for sustainable operations by:

Improvement in quality, productivity, yield , and energy efficiency

Sharing best maintenance, environment management, and safety practices

Benchmarking, training and talent sharing

Standardization of processes

One of the largest FDI in the Indian Metals and Mining space – Equity infusion by JFE of Rs. 5,410 Crores (~US$1.2 bn) (1) for 14.99% equity stake

Deleveraged Balance Sheet to support next phase of growth

Access to cutting edge technologies and fast growing automotive steel market

Operational excellence to result in cost reduction

8

Balanced corporate strategy

Selective Growth

Diversification of Product Profile and

Customer Base

Backward & Forward Integration, and Focus on Resource

Optimization

Prudent balance sheet management

Sustainability with focus on Quality, R&D and Innovation

Maintain market share through selective organic and inorganic growth

Undertake brownfield expansions at low specific investment cost per ton

Consider inorganic opportunities that are value accretive

Increase proportion of high margin value-added products

Diversify customer base, both within India and abroad

Continue to focus on rural markets in India

Continue to evaluate raw material assets in India and abroad to secure key raw material supplies and reduce cost of production by targeting strategic tie-ups and investments

Focus on cost reduction and energy efficiency

Continuously seek to improve financial profile

Manage capacity expansion and debt profile to capture market opportunities without excessive risk

Committed to sustainable and eco-friendly technologies to drive growth

Focus on Quality, R&D and Innovation to drive cost efficiency and new product development

9

Strong and balanced Board comprising experts of eminence & integrity

Savitri Devi JindalP. Hemalatha, IASNominee Director of KSIIDC

Executive Directors Independent Directors Nominee DirectorsChairperson—Emeritus

Sajjan JindalChairman & Managing Director

Seshagiri Rao M.V.SJoint Managing Director & Group CFO

Dr. Vinod Nowal Dy. Managing Director

Jayant AcharyaDirector (Commercial & Marketing)

Dr. Vijay Kelkar Ex-Finance Secretary, Ex-Secretary of MoP&G, Ex-Chairman Finance Commission

Promoter Director

Board fundamentally committed to sustainable business

Haigreve KhaitanSenior Partner at M/s. Khaitan& Co, India's one of the oldest and full service law firm

Malay Mukherjee 40yrs of rich experience in mining and steel industry

Seturaman MahalingamCA, Ex-CFO of TCS, Ex member of the Tax Administration Reform Commission

Kannan Vijayaraghavan, FCA and Certified Management Consultant

Dr. Punita Kumar Sinha Former CIO at The Asia Tigers Fund

Hiroyuki OgawaNominee Director of JFE Steel Corporation

10

FY17 performance on sustainability matrixes

8,73,635 GJ

Waste heat utilized4.12 MTMaterial Recycled

35%Recycled & reused water

28%Decrease in LTIFR over FY16

18%Increase in Expenditure for corporate social responsibility over FY16

20%Reduction in Specific Water consumption over FY16

18.4%Reduction in Specific Energy consumption over FY16

2016

‘Golden Peacock Innovative Product’ Award

‘Steelie Award 2016’ in the innovation category for “thedevelopment of advanced high strength automotive steels withspeed and innovation” by the World Steel Association

The National Award for Supply Chain and Logistics Excellenceunder steel industry Category by CII

Accreditation with level 5 for Total Cost Management (TCM)Maturity Model Assessment by TCM division of CII

2nd Prize in the National Energy Conservation Awards 2016 toVijayanagar Works in “Integrated Steel Sector” and KalmeshwarWorks in “Steel Re-Rolling Mills Sector” by ‘Bureau of EnergyEfficiency’ of India

2015 Porter’s Prize for ‘Leveraging Unique Activities’

JSW Group received Porter’s Prize for ‘Creating Shared Values’

11

Agenda

Overview Value Proposition

Performance Overview

Guidance Business Environment

12

Strong fundamentals to boost India steel demand

Multi-location manufacturing facilities

Diversified product profile

Domestic market leader with strong export presence

Strong sales and marketing platform

Focus on operational efficiency

Strategic expansion aided by strong project execution

Proven ability to acquire and turnaround assets

Robust financial profile

A platform of strength and agility

1

2

3

4

5

6

7

8

9

13(1) Reserve Bank of India and IMF, (2) World Steel Association, IMF [World Economic Outlook – 2016], (3) World Steel Association [Short range outlook – Oct 2016], (4) Bubble size represents total steel demand of respective country

Strong fundamentals to boost India steel demand

5.6% 6.5% 7.2% 7.9%

7.1% 7.2%

FY13 FY14 FY15 FY16 FY17E FY18E

Strong economic growth with improving fundamentals

India’s GDP growth continues to register stellar performance in a worldseeing sluggish growth

After temporary impact of demonetization, economy activity is improvingwith increasing public spending, declining fiscal deficit, benign inflation,lower oil prices and easing interest rate trajectory

India GDP growth(1)

• (%)

Government reforms to boost industry growth

Various measures in different sectors, easing FDI norms and initiatives such as‘Make in India’ aim at driving growth & development

The finance minister in his recent budget speech, stressed on continuingwith economic reforms along with increase in public investment ininfrastructure and development projects.

c.$60 Bn allocated for infrastructure development in 2017-18

India steel consumption to rise at a faster rate

o India’s steel consumption was 84 million tonnes in 2016 and is expected to rise to ~89 million tonnes in 2017(3)

Potential for substantial growth in steel consumption(2)(4)

o World Per Capita Consumption was ~206 Kgs in 2016o India Per Capita Consumption was ~64 Kgs in 2016

With the growth in economy, JSW Steel is well positioned to be part of the India growth story

(200)

0

200

400

600

800

1,000

1,200

1,400

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000

China

IndiaBrazilMexicoRussia

Italy

Japan

South Korea

France

Canada

Germany

USA

Per

cap

ita

Stee

l Co

nsu

mp

tio

n in

20

16

(K

g.)

GDP per capita in 2016 ($)

1

14*JSW Steel Coated Products Limited

^ JSW Steel (Salav) Limited

Multi-location manufacturing facilities

Leveraging locational advantage to increase market share strategically

2

Dolvi: 5 MTPA

3.5 MTPA Blast Furnace 1.6 MTPA gas based DRI 55 MW Power Plant

Salem: 1 MTPA

1 MTPA Blast Furnaces 0.5 MTPA Blooming Mill 60 MW Power Plant

Kalmeshwar (JSCPL*)

0.58 MTPA GP/GC 0.19 MTPA Colour

Coating Line

Vasind & Tarapur (JSCPL*)

1.18 MTPA GP/GC 0.5 MTPA Colour Coating Line 30 MW Power Plant

Vijayanagar: 12 MTPA

1.7 MTPA Corex 10.4 MTPA Blast Furnaces 854 MW Power Plant

Salav: 0.9 MTPA DRI (^)

Geographically diversified with manufacturing facilities in South and West India

US plate and pipe mill

JSW Steel ownership: 90%

Acquisition cost: $810mn

Capacity: 1.2 Net MTPA Plates and 0.55 Net MTPA Pipes

Acquired in 2007

Opportunity for diversification in terms of products, markets and geographies

US coal mines JSW Steel ownership: 100%

Acquisition cost: $70mn

Chile iron ore mines

JSW Steel ownership: 70%

Acquisition cost: $252mn

Started operations in FY11

Maritime concession to develop cape size port in North Caldera

Mozambique coal mines

JSW Steel ownership: 100%

Early stage development in progress

Strategic overseas presence

15

Wide offering of Flat and Long products

Continuously increasing value added products

Diversified portfolio to address growing demand for value-added steel

Commissioned new facilities to further enrich product mix

Leveraging JFE Steel’s well-established manufacturing technology for high value-added products for auto-grade steel

Developing new products, capturing niche markets

Automotive Grade Steel:

Enhanced focus on cold rolled, galvanised and galvanneal products for body panels of automobiles

Electrical Steel:

Commissioned Cold Rolled Non-grain Oriented (CRNO) steel plant to address domestic demand by substituting imports of high grade electrical steel

Color Coated Products:

Largest color coated facility to address construction, warehousing and roofing requirements

State-of-the-art color coating line for appliance grade products used in consumer durables

Diversified Product Profile

GC

TMT

Slabs

ColorCoated

HRC

Billets

HR Plates

Blooms

CRC

Wire Rods

Continuously enriching product mix

3

16Indicates new grade approval in 1QFY18

Above mentioned approved grades are the highest among the specific product/grade-group; the lower grades uptothe highest grades are also approved.

Product/Grade approvalsApplications Components

Hood 270F 340P 270F 340P JSC340HN CR240B2Roof 270F 590R CR210B2Doors 270F JSC270DU 270F JAC270DU SGARC40Body s ide outer 270F 270F JAC340PBIW (Inner) 980Y 590R 440WFloor 270F HX220YD SAGA270CStructura l 980Y 590Y 590R BSK46 SAPH 370 S550MCReinf. Pi l lar 980Y HX180YD SGARC440Fuel Tank DX57Wheels SPFH440 SPFH590 SAPH 590 HR 750Engine SCM435 S36CV 86B45 SAE1070 SAE4140 SAE1018 EN1APB 16MnCr5LSiTransmiss ion 16MnCr5 SAE4124 SAE8822 SAE5160 SAE4145 20MnCr5NiAxels 150M36Tractor 815M17Suspens ion 51CrMoVnBearings 100CrMnSi6-4 SAF5019Front Panel EDD IFSide Panel D DDOuter shel lLPG Cyl inder shel l IS 15194 HS345

Structura l SS540 MSL I Gr6 ASTM A 792 5700MCWeather Res is tant IRSM 41

Heat Exchanger SPCCTAlternator 50C1000 50C700 65C1000 65SP1000 50SP1050Auto Electrica ls 50C1000 50C800 50C600 50C470Fan 50C1000 50SP1000 35C360 35C360FHP Motors 50C1000 50C800 50C700 50C600 50SP1050 50SP890Generators 50C530 50C470 50C470 S 50C400 50C310 65C700Compresors 50C1000 50C800 (P) 50C600 50C530 50C470 50C470 PInd. Motors 50C800 50C600 65C600 50C530 65C530Pump Motors 50C1000 50C800 50C700 50SP1050 50SP890Trans Lam 50C1000 50C800 50C700 50C600 50C530 50C470 35C360 35C300

CR Coated HRPO HR

Alloy Steel Longs

Electrical Steel

Fully Processed Semi Processed

General Engineering

JIS G3131SPHD

Grades Approved

Automotive

Appliance

SCGA 270D + JAZ

BTC330R/BTC245R

3

17(1) Joint Plant Committee, (2) Revenue from operations as per Ind-AS from FY16 onwards

Domestic market leader with strong export presence

Penetrating further to capture growing domestic demand withunique marketing strategy – pan India retail network with morethan 8,100 outlets (includes JSW Connect, JSW Shoppe, JSWExplore as well as non-exclusive retailers)

Delivered industry leading sales volume growth at 20%YoY in FY17

One of the largest exporter of steel products from India withexport presence in over 100 countries

Ability to re-align sales effort and shift between domestic andexport markets as per market conditions – strategically reducedshare of exports to 12% of total sales in FY16, as global steelconsumption declined 3% YoY in CY15. Exports have againrecovered in FY17

Flexibility to shift between domestic and international markets based on market conditions

4

77%85% 84%

76%88%

75%

23%15% 16%

24%12%

25%

FY08 FY10 FY12 FY15 FY16 FY17

11.4% 13.4% 6.9% 3.3% India Finished Steel Consumption Growth(1)

JSW Export Turnover/ revenue(2) as % of Total

JSW Domestic Turnover/ revenue(2) as % of Total

4.5% 2.6%

18

Multi-sectoral volume growth

Optimizing market mix and product mix to derivemaximum benefit from sector growth

Leveraging export presence

New product approvals for Original EquipmentManufacturers (OEMs) and automotive customers

Increase in value added products leading toincremental growth in focus sectors and alsofacilitating import substitution

Focused on Retail Sales – increased reach andpenetration

Strong sales and marketing platform

Segmented approach to address different retail segments

Metro / Urban

Urban /Semi-urban

Semi-urban /

Rural

‘JSW explore’ Branded, multiple product service center

for steel solutions Just-in-time solution with in-house

profiling lines and Value Added Services Franchisee Model

‘JSW Shoppe’

Steel distribution

Enhanced customer experience

‘JSW Shoppe Connect’ Smaller retail format linked to JSW

explore/Shoppe Last mile link to talukas/rural areas Sales to end consumers and MSMEs

Increased customer focus and market penetration

5

19(1) Total production (15.80MT) divided by total no. of employees on Company payroll (11,848) in FY17

Focus on operational efficiency

Diverse blend of technology

Coke Making: Recovery and Non-recovery Coke Ovens

Agglomeration: Pelletisation and Beneficiation Plants

Iron Making: Blast Furnace, Corex, Sponge Iron (DRI)

Steel Making: Basic Oxygen Furnace (BOF), Electric Arc Furnace (EAF), Conarc

Casting: Continuous Casting, Thin Slab Casting, Billet Casting

High labourproductivity

Improving labour productivity: Current production of ~1,334 tons/ employee(1)

In-house training programs internal faculty

Continuously investing, building and enhancing competencies

Integrated operations

Integrated manufacturing facilities: From pelletisation / beneficiation to downstream value-add capabilities

Dedicated port and railway siding for logistics support

100% assured power supply through captive power plants and arrangements with JSW Energy and the power grid

Resulting in operational efficiency with:

Reduced raw material costs

Focus on process improvements

Waste gas utilization for power generation

Solid waste management and zero effluent discharge

Efficient operations resulting in low conversion cost

High level of integration and technological expertise leading to reduced production cost and time

6

20(1) IGAAP based Gross Block as on Mar 31, 2017 (` 65,485 Crores translated at USD/`. = 64.8386 RBI Reference as on Mar 31, 2017) divided by total capacity (18MTPA)

Strategic expansion aided by strong project execution

Focus on low cost and returns accretive brownfield projects to capitalise on expected demand growth

Strong project execution capabilities …

Experienced in-house project management team

Supported by cross-functional team (commercial, finance and legal department)

Established long-term relationship with key domestic and international suppliers

Savings in procurement cost by negotiating firm prices for follow-on orders

… at low specific investment cost(1)

Low specific investment cost of $561/ton of capacity expansion shows cost and project management efficiency

Major new & on-going Projects

Vijayanagar Works:

BF-3 revamp & upgradation, CRM-1 complex capacity expansion, Pipe Conveyor System for Iron ore and new Water Reservoir

Dolvi Works:

Capacity expansion to 10 MTPA, 1.5MTPA Coke Oven at Dolvi Coke Projects Limited

Salem Works:

Capacity expansion from 1 MTPA to 1.2 MTPA by setting up certain new facilities and debottlenecking/modification of existing facilities

Setting-up of Reheating Furnace in Bar Rod Mill, Coke Oven and Turbo Generator

Vasind and Tarapur Works:

Modernization-cum-capacity enhancement, 0.2MTPA Tin plate mill

7

21(1) Implemented in a wholly owned subsidiary Amba River Coke Limited.

Proven ability to acquire and turnaround assets

December 2010 Completed Initiatives—FY2011–2015 FY2016-2017

Inability to service existing debt

Inadequate cashflows

Corporate debt restructuring (CDR) case

Exit from CDR

Generating positive profit after tax

Plant under maintenance Loss making at EBITDA level High interest cost Financially distressed

Infusion of equity Alignment of marketing strategies resulting in freight

synergies and VAT benefits Reduction of high cost working capital funding Refinancing of existing debt Electricity sourcing from JSW Energy at competitive

prices Commissioning of 4MTPA pellet plant(1), 1MTPA coke

oven(1), waste gas based 55MW power plant, railway siding, and lime calcination plant

Capacity expanded to 5MTPA Diversified product offering from Flat

steel only to mix of Flat and Long steel

Stabilized/ ramped-up the expanded capacity

Case Study: Turnaround strategy at JSW Ispat’s Dolvi plant

JSW Steel has a proven track record of acquiring troubled assets and turning them around in record time by closely integrating them with its existing operations thus creating synergies and optimizing cost

Able to leverage an acquisition to maximum value accretion through application of knowledge and experience

8

22

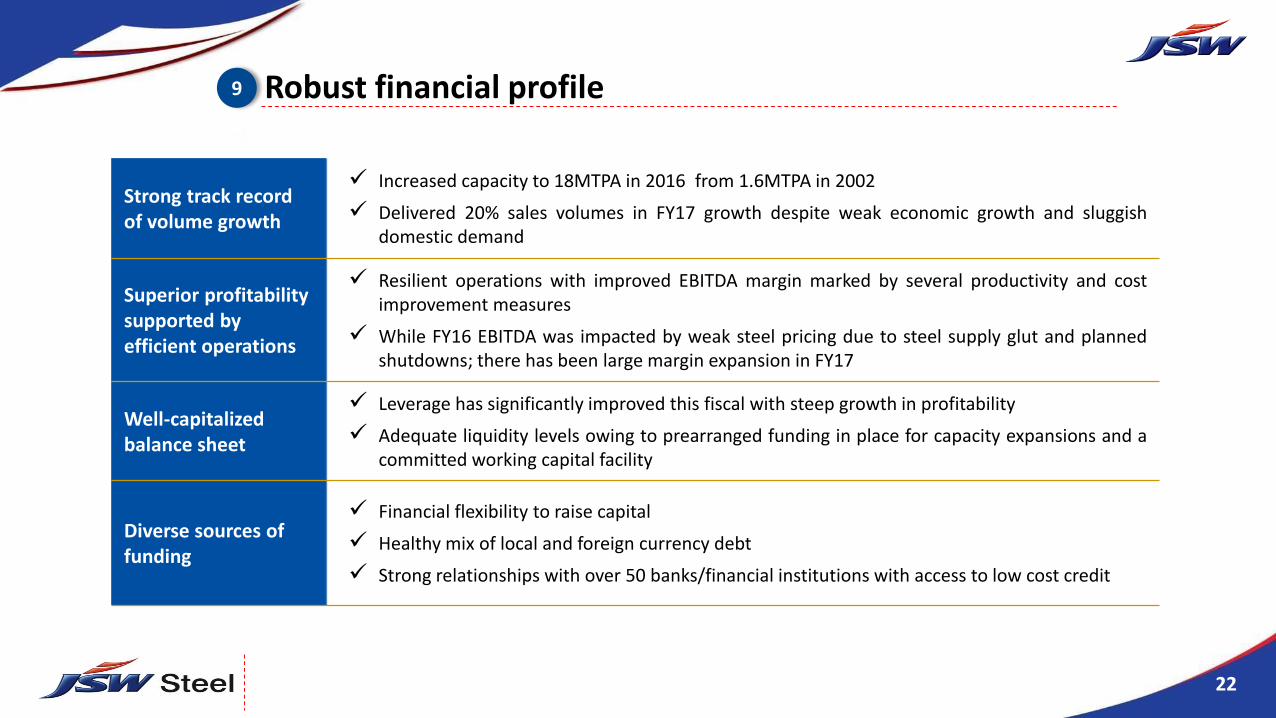

Robust financial profile

Strong track record of volume growth

Increased capacity to 18MTPA in 2016 from 1.6MTPA in 2002

Delivered 20% sales volumes in FY17 growth despite weak economic growth and sluggishdomestic demand

Superior profitability supported by efficient operations

Resilient operations with improved EBITDA margin marked by several productivity and costimprovement measures

While FY16 EBITDA was impacted by weak steel pricing due to steel supply glut and plannedshutdowns; there has been large margin expansion in FY17

Well-capitalized balance sheet

Leverage has significantly improved this fiscal with steep growth in profitability

Adequate liquidity levels owing to prearranged funding in place for capacity expansions and acommitted working capital facility

Diverse sources of funding

Financial flexibility to raise capital

Healthy mix of local and foreign currency debt

Strong relationships with over 50 banks/financial institutions with access to low cost credit

9

23

Historical EBITDA per ton – JSW Steel Standalone

6,2

62

7,5

88

7,5

89

7,0

77

9,2

31

5,8

92

4,0

59

5,4

00

5,3

98

5,4

69

6,9

88

8,5

34

8,5

45

8,0

52

7,4

78

7,1

37

6,8

59

6,9

85

6,0

54

7,0

28

8,4

02

7,1

51

6,5

69

6,8

87

8,3

40

9,5

46

6,2

79

6,2

68

8,6

86

1QF

18

4Q

FY

17

3Q

FY

17

2Q

FY

17

1QF

Y17

4Q

FY

16

3Q

FY

16

2Q

FY

16

1QF

Y16

4Q

FY

15

3Q

FY

15

2Q

FY

15

1QF

Y15

4Q

FY

14

3Q

FY

14

2Q

FY

14

1QF

Y14

4Q

FY

13

3Q

FY

13

2Q

FY

13

1QF

Y13

4Q

FY

12

3Q

FY

12

2Q

FY

12

1QF

Y12

4Q

FY

11

3Q

FY

11

2Q

FY

11

1QF

Y11

EB

IT

DA

(R

s p

er

to

n)

24

Agenda

Overview Value Proposition

Performance Overview

Guidance Business Environment

25

Key highlights – 1QFY18

Standalone performance

Crude Steel production: 3.91 million tonnes

Steel sales: 3.51 million tonnes

Quarterly EBITDA : ` 2,198 crores

Net Debt to Equity: 1.71x and Net Debt to EBITDA: 3.81x

JSW Steel Coated Products

Highest ever quarterly Steel sales: 0.48 million tonnes

Highest ever quarterly EBITDA: ` 205 crores

Consolidated performance

Quarterly Operating EBITDA : ` 2,617 crores

Net Debt to Equity: 1.97x and Net Debt to EBITDA: 3.76x

Key update

2nd prize to Tarapur works and 3rd prize to Kalmeshwar Works for excellence in energy conservation and management in ‘Metal & Steel’ category at 11th State level energy conservation award by Maharashtra Energy development Agency (MEDA)

26

3.87 3.914.10

1QFY17 1QFY18 4QFY17

Crude Steel Production

All figures are in million tonnes

Quarterly volumes – standalone

YoY

+1%

1QFY17 1QFY18 4QFY17

Flat 2.74 2.76 2.98

Long 0.85 0.83 0.82

3.343.51

3.96

1QFY17 1QFY18 4QFY17

Steel Sales

YoY

+5%

1QFY17 1QFY18 4QFY17

Flat 2.48 2.57 2.90

Long 0.74 0.75 0.78

Semis 0.12 0.18 0.27

QoQ

-5%

QoQ

-11%

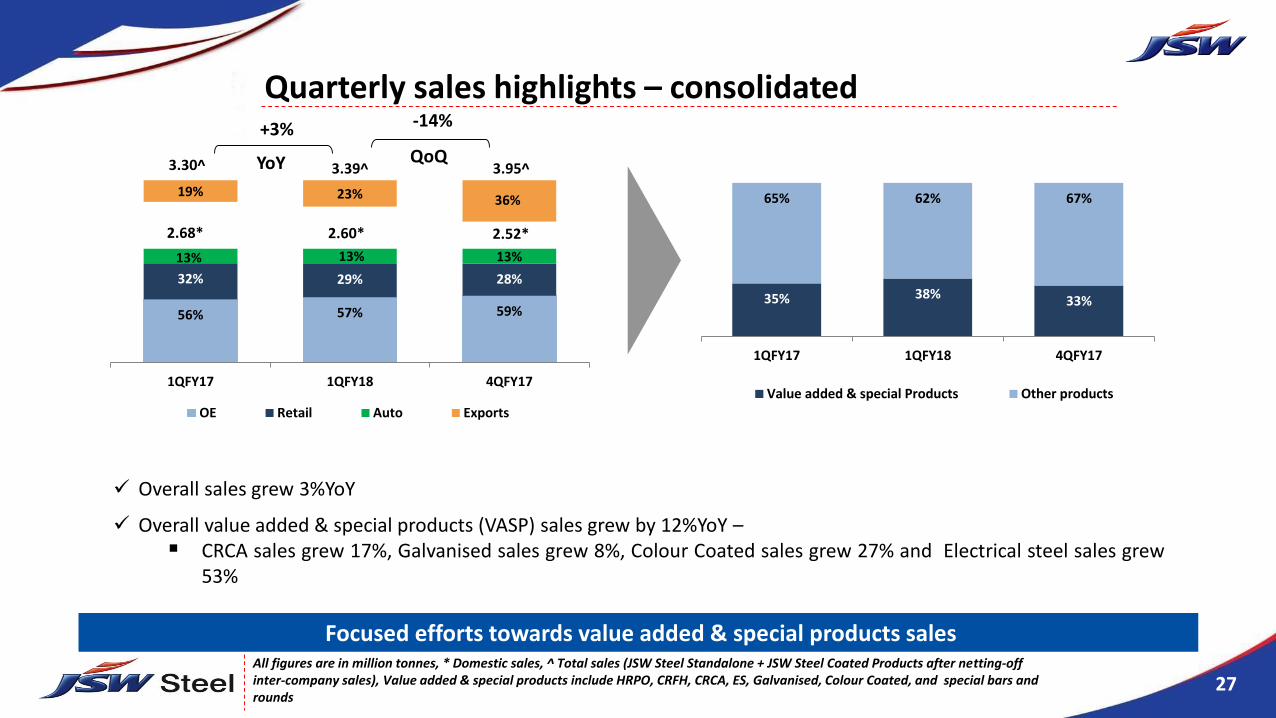

27All figures are in million tonnes, * Domestic sales, ^ Total sales (JSW Steel Standalone + JSW Steel Coated Products after netting-off inter-company sales), Value added & special products include HRPO, CRFH, CRCA, ES, Galvanised, Colour Coated, and special bars and rounds

Quarterly sales highlights – consolidated

56% 57% 59%

32% 29% 28%

13% 13% 13%

2.68* 2.60* 2.52*

19% 23% 36%

3.30^ 3.39^ 3.95^

1QFY17 1QFY18 4QFY17

OE Retail Auto Exports

35% 38% 33%

65% 62% 67%

1QFY17 1QFY18 4QFY17

Value added & special Products Other products

Overall sales grew 3%YoY

Overall value added & special products (VASP) sales grew by 12%YoY – CRCA sales grew 17%, Galvanised sales grew 8%, Colour Coated sales grew 27% and Electrical steel sales grew

53%

Focused efforts towards value added & special products sales

YoY

+3%

QoQ

-14%

28

Branded Sales ratio to overall retail sales grew to 54%

Added 263 new Retailers to the network; JSW now has footprints across 575 districts with over 8,100 exclusive and non-exclusive retail outlets

Engaged with 900+ influencer/ retailers through 90+ meets

Retail segment highlights for 1QFY18

846761

707

1QFY17 1QFY18 4QFY17

Retail sales (‘000 tonnes)

52% 54% 54%

48% 46% 46%

1QFY17 1QFY18 4QFY17

Branded Sales Others

29

Particulars 1QFY18 1QFY17

` Crores USD mn ` Crores USD mn

Revenue from operations 15,096 2,332 12,021 1,857

Operating EBITDA 2,198 340 3,083 476

Other Income 48 7 44 7

Finance Cost 907 140 863 133

Depreciation 732 113 729 113

Profit Before Tax 607 94 1,535 237

Tax 188 29 453 70

Profit after Tax 419 65 1,082 167

Diluted EPS (`)* 1.73 4.48

USD/` = 64.7379 (RBI reference rate as on June 30, 2017)

* Not Annualized

1Q financials – standalone

30

3,083

2,198

143

1,957

(3,009)

24

EBITDA1QFY17

Volume NSR Cost Others EBITDA1QFY18

$476 $22

$302

($465)

$4 $340

USD/` = 64.7379 (RBI reference rate as on June 30, 2017)

Operating EBITDA movement – standalone

` crore/ USD mn

31

Volumes 1QFY18 1QFY17

Production 0.44 0.41

Sales 0.48 0.40

` crore

Operational performance – JSW Steel Coated Products

Million tonnes

Key P&L data 1QFY18 1QFY17

Revenue from Operations 3,060 2,194

Operating EBITDA 205 159

Profit after Tax 117 74

32

Sales (net tonnes) 1QFY18 1QFY17

Plate Mill 52,410 27,542

Pipe Mill 11,993 5,618

Production (net tonnes) 1QFY18 1QFY17

Plate Mill 65,491 37,859

Utilization (%) 28% 16%

Pipe Mill 11,562 4,598

Utilization (%) 8% 3%

USD mn

Net tonnes = 0.907 metric tonnes

Operational performance – US Plate & Pipe Mill

Key P&L data 1QFY18 1QFY17

Revenue from Operations 58.67 25.26

EBITDA 5.10 (5.45)

33

Particulars 1QFY18 1QFY17

` Crores USD mn ` Crores USD mn

Revenue from operations 15,977 2,468 12,886 1,990

Operating EBITDA 2,617 404 3,256 503

Other Income 41 6 33 5

Finance Cost 945 146 936 145

Depreciation 819 127 817 126

Profit Before Tax 894 138 1,536 237

Tax 284 44 451 70

Share of Associates and Joint Ventures 14 2 11 2

Profit after Tax 624 96 1,096 169

Diluted EPS (`)* 2.59 4.63

USD/` = 64.7379 (RBI reference rate as on June 30, 2017)

* Not Annualized

1Q financials – consolidated

34

41,549 43,323

5,068

501

3,277

34 449

Net Debt*as on Mar'17

New Loan Taken Repayments Pre-payments Fx Impact Movement inCash & CashEquivalents

Net Debt*as on Jun'17

$6,418

$783

($77)

($506)

$5 $69 $6,692

USD/` = 64.7379 (RBI reference rate as on June 30, 2017)

*Net Debt excludes Acceptances

Net debt movement – consolidated

` crore/ USD mn

Particulars 30.06.2017 31.03.2017

Cash & cash equivalent (` crore) 1,336 1,785

Net Debt/Equity (x) 1.97 1.85

Net Debt/EBITDA (x) 3.76 3.41

35

Agenda

Overview Value Proposition

Performance Overview

Guidance Business Environment

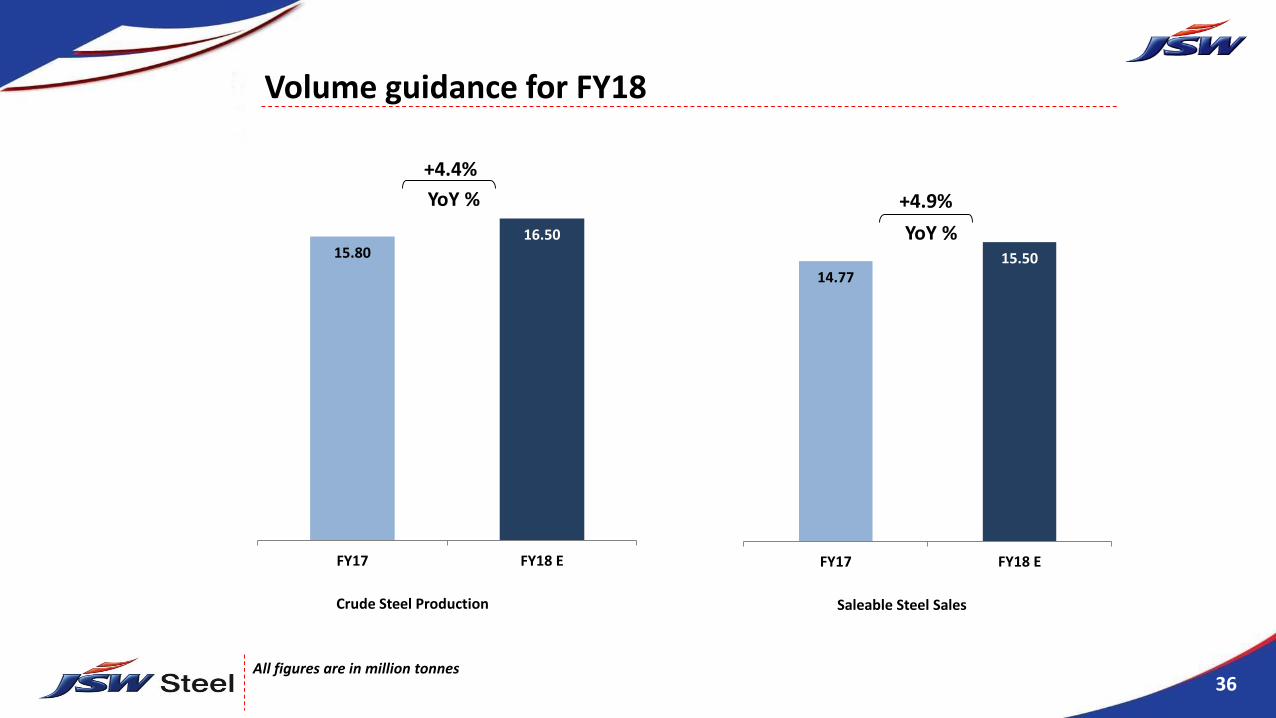

36

14.7715.50

FY17 FY18 E

Saleable Steel Sales

All figures are in million tonnes

Volume guidance for FY18

15.8016.50

FY17 FY18 E

Crude Steel Production

YoY %

+4.4%

YoY %

+4.9%

37All figures in ` crores

Rolling Capex Plan: FY18-21

FY17:4,300 2,800

8,000

FY18:2,700 4,200 1,050 530

19,200

3,235

18,815

Rolling Capex(FY17-FY18)

FY17 capexoutflow

CapexCarriedforward

Ind-ASimpact of

1.5mtpa CokeOven at DCPL

MiningCapex

Expansion/upgradtion

projects

Other costsaving

projects

Rolling Capex(FY18-FY21)

7,000

26,815

Debt:5,000

Debt:10,000

Equity:3,000

Equity:8,815

FY18 Capex FY19-FY21Capex

8,000

18,815

38

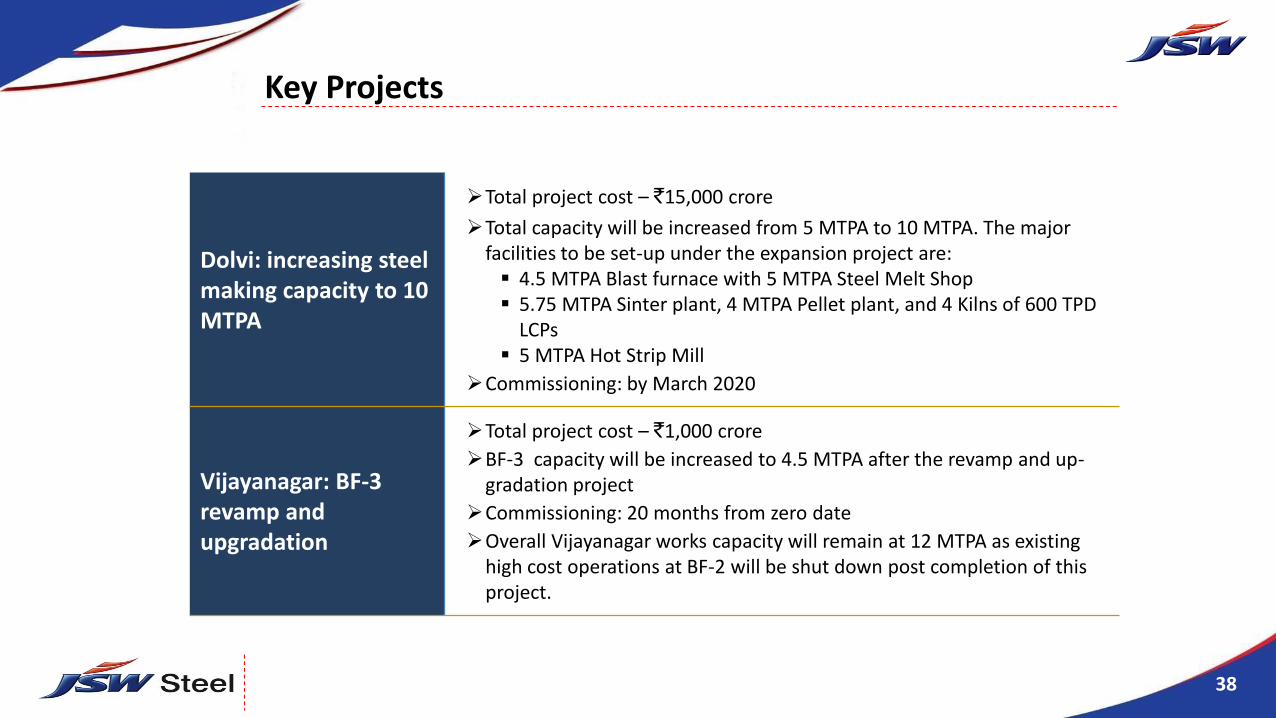

Key Projects

Dolvi: increasing steel making capacity to 10 MTPA

Total project cost – `15,000 crore

Total capacity will be increased from 5 MTPA to 10 MTPA. The major facilities to be set-up under the expansion project are: 4.5 MTPA Blast furnace with 5 MTPA Steel Melt Shop 5.75 MTPA Sinter plant, 4 MTPA Pellet plant, and 4 Kilns of 600 TPD

LCPs 5 MTPA Hot Strip Mill

Commissioning: by March 2020

Vijayanagar: BF-3 revamp and upgradation

Total project cost – `1,000 crore

BF-3 capacity will be increased to 4.5 MTPA after the revamp and up-gradation project

Commissioning: 20 months from zero date

Overall Vijayanagar works capacity will remain at 12 MTPA as existing high cost operations at BF-2 will be shut down post completion of this project.

39

Key Projects contd. …

Vijayanagar: CRM-1 complex capacity expansion

Total project cost – `2,000 crore

CRM1 complex capacity will be increased from 0.85 MTPA to 1.80 MTPA alongwith two Continuous Galvanizing Line of 0.45 MTPA each, a new 1.2 MTPA Continuous Pickling Line for HRPO products, and a new 0.80 MTPA HR Skin Pass Mill for HR Black & HRSPO products

Commissioning: by Sep 2019

Vasind and Tarapur : modernisation-cum-capacity enhancement

Total project cost – `1,200 crore

The modernisation cum capacity enhancement project includes:

increase in cold rolling capacity from 1.16 MTPA to 2.12 MTPA by replacing exisitng CR mills with Batch Tandem CR mills

increase in GI/GL capacity by 0.63 MTPA increase in colour coating capacity by 0.08 MTPA

Commissioning: by April 2019

40

Agenda

Overview Value Proposition

Performance Overview

Guidance Business Environment

41Source: Bloomberg, IMF and JSW Steel

Global economy

Global growth outlook remains firm

Global growth outlook on track, economic activity in bothadvanced and emerging / developing economies expected toaccelerate

US growth expectation marked down amidst less expansionarypolicy stance

Euro area activity continues to improve helped byexpansionary monetary policy and reduced politicaluncertainity as well as better domestic demand

Japan growth outlook turns marginally better than earliersupported by private consumption and export growth

Chinese economic growth positively surprise on the back offiscal policy supported front‐loaded infrastructure investment

3.2% 1.

7% 1.6%

1.8%

1.0% 4.

3%

7.1%

6.7%

3.5%

2.0%

2.1%

1.9%

1.3% 4.

6%

7.2

%

6.7%

World AMEs US EuroArea

Japan EMEs India China

2016 2017P

GDP growth - IMF projections for 2016 and 2017 (%YoY)

-4-202468

De

c-1

4

Mar

-15

Jun

-15

Sep

-15

De

c-1

5

Mar

-16

Jun

-16

Sep

-16

De

c-1

6

Mar

-17

Jun

-17

US Eurozone Japan China

Index of Industrial Production (% YoY)

42Source: World Steel, ISSB, MySteel and JSW Steel

Global steel scenario

Global steel demand growth appears to be better than earlier expectations

Global steel production grew by ~36mmt in 1HCY17 asagainst WSA’s CY17 estimate for demand growth of ~20mmt

However, China has positively surprised with a ~35mmtapparent steel demand growth in 1HCY17against a flattishdemand estimate by WSA’s for CY17. This growth wasprimarily driven by government stimulus

Overall Chinese steel exports have come down by ~28% in1HCY17

Exports from Japan and Korea continue to remain atelevated levels with pricing at a discount to their domesticmarket prices

Steel prices are improving with upward pressure on iron oreand coking coal amidst improved demand environment inChina

200

350

500

650

800

De

c-1

4

Mar

-15

Jun

-15

Sep

-15

De

c-1

5

Mar

-16

Jun

-16

Sep

-16

De

c-1

6

Mar

-17

Jun

-17

North America ExW North Europe ExWChina export FOB Black Sea export FOB

HR

C p

rice

s ($

/to

nn

e)

50

75

100

125

150

500

575

650

725

800

875

De

c-1

4

Mar

-15

Jun

-15

Sep

-15

De

c-1

5

Mar

-16

Jun

-16

Sep

-16

De

c-1

6

Mar

-17

Jun

-17

China apparent Steel Consumption (annualized, mmt)

China steel Exports (annualized, mmt) -RHS

43Source: JPC and JSW Steel, All figures are in million tonnes, ^Average monthly imports during FY16, * Apparent finished steel consumption net of double counting effect

Indian economy and steel industry

Steel imports, after correcting in April, have again risen to~8mmt on annualized basis

Crude steel production increased by 3.5%YoY in 1QFY18whereas apparent finished steel consumption grew by4.6%YoY

Steel demand is improving with increasing public sectorspending; reflected in increased activity in sectors likeroads, power T&D, solar energy, earthmoving equipments,pre-enginnered buildings, and water & gas pipelines,

Sluggish private capex remains a concern

Steel demand growth is on track to grow by ~5% in FY18

69

7

60

4

56

1 72

0

57

9

64

0 84

1

63

4

58

7

69

0

64

8

57

4

65

9

63

6

75

1 1,0

58

Jun

-17

May

-17

Ap

r-1

7

Mar

-17

Feb

-17

Jan

-17

De

c-1

6

No

v-1

6

Oct

-16

Sep

-16

Au

g-1

6

Jul-

16

Jun

-16

May

-16

Ap

r-1

6

FY1

6^

Monthly steel imports (in '000 tons)

23.7220.08

24.5621.01

Crude Steel

Production

Apparent Finished Steel

Consumption*

1QFY17

1QFY18

3.5%4.6%

44

Certain statements in this report concerning our future growth prospects are forward looking statements, which involve anumber of risks, and uncertainties that could cause actual results to differ materially from those in such forward lookingstatements. The risk and uncertainties relating to these statements include, but are not limited to risks and uncertaintiesregarding fluctuations in earnings, our ability to manage growth, intense competition within Steel industry including thosefactors which may affect our cost advantage, wage increases in India, our ability to attract and retain highly skilledprofessionals, time and cost overruns on fixed-price, fixed-time frame contracts, our ability to commission mines withincontemplated time and costs, our ability to raise the finance within time and cost client concentration, restrictions onimmigration, our ability to manage our internal operations, reduced demand for steel, our ability to successfully completeand integrate potential acquisitions, liability for damages on our service contracts, the success of the companies in which theCompany has made strategic investments, withdrawal of fiscal/governmental incentives, impact of regulatory measures,political instability, legal restrictions on raising capital or acquiring companies outside India, unauthorized use of ourintellectual property and general economic conditions affecting our industry. The company does not undertake to update anyforward looking statements that may be made from time to time by or on behalf of the company.

Forward looking and cautionary statement

45

Thank you