JSW Ispat Special Products Ltd. JSW Steel Limited

16

JSW Steel Limited Investor presentation August, 2020 JSW Ispat Special Products Ltd. Formerly known as Monnet Ispat & Energy Ltd. Corporate Presentation October 2021

Transcript of JSW Ispat Special Products Ltd. JSW Steel Limited

JSW Steel Limited

Investor presentation August, 2020

JSW Ispat Special Products Ltd.

Formerly known as Monnet Ispat & Energy Ltd.

Corporate Presentation

October 2021

Confidential Better Everyday

Source: Company Reports, Bloomberg

Note: * Listed company

(a) Market Cap as per Bloomberg as of 30 September 2021

Latin text

Heading: Arial Body: Arial

East Asian text

Heading: SimHei Body: SimHei Cover title:

Arial/30pt/R255,G255,B255/Bold

Cover subtitle:

Arial/16pt/R255,G255,B255

79

129

189

Theme

Color

(RGB)

192

80

77 219

132

61 137

165

78 113

88

143 0

80

163

255

255

255 0

0

0 255

255

255 0

0

0

JSW Group overview

2

JSW Ispat Special Products Ltd. (JISPL) was acquired jointly by a consortium of JSW Steel Limited and AION Investments Private Limited (AION)

Presence across

the core sectors of

India

• One of India’s leading integrated steel producers

• Installed crude steel capacity of 18 mtpa (as on 30th

Sep’21), expected to grow to 30.5 mtpa in the next few

years

• Market capitalisation of c.US$21.8bn (a)

• Long standing track record in debt capital markets – raised

US$3.65bn through 7 issuances

• Power producer with installed capacity of 4.6 GW (Hydro,

Renewable and Thermal)

• Growing to 10 GW by FY25; and 20GW by FY30 with

84% renewable portfolio

• Market capitalisation of c.US$8.6bn(a)

• Debut USD bond offering in 2021 – raised US$707m

(Fitch Rating – BB+)

• Manufacturer of Portland Slag Cement (PSC),

Ordinary Portland Cement (OPC) and Ground

Granulated Blast Furnace Slag (GGBS)

• Operational capacity of 14 mtpa, growing to 25

mtpa

• Commenced operations in March 2019

• Annual operating capacity of 130,000 KL

• Fully automated coil coating capacity

• Fully automated water based plant

• Engaged in development and operations of ports

• Operational capacity 110 mtpa

• Operations across East, West & Southern coasts of

India

Confidential Better Everyday

(1) As of June 2021

Latin text

Heading: Arial Body: Arial

East Asian text

Heading: SimHei Body: SimHei Cover title:

Arial/30pt/R255,G255,B255/Bold

Cover subtitle:

Arial/16pt/R255,G255,B255

79

129

189

Theme

Color

(RGB)

192

80

77 219

132

61 137

165

78 113

88

143 0

80

163

255

255

255 0

0

0 255

255

255 0

0

0

Apollo overview

3

AION is an affiliate entity of Apollo

Key Attributes Global Footprint

Value-oriented, contrarian

approach

Opportunistic across market

cycles

Integrated platform across asset

classes and geographies

Deep industry knowledge

Equity and Hybrid

280+ Investment

Professionals

$133 bn in AUM1

Yield Assets

290+ Investment

Professionals

$339 bn in AUM1

New York

Bethesda

Houston

Los Angeles

London

Madrid

Frankfurt

Luxembourg Delhi

Mumbai

Shanghai

Hong Kong

Singapore

Firm Profile

Founded: 1990

AUM: ~$472 bn1

Employees: 2,000+

Offices Worldwide: 15

Tokyo

San Diego

Confidential Better Everyday 4

30

40

50

60

70S

ep-1

9

Dec-1

9

Ma

r-20

Jun

-20

Se

p-2

0

Dec-2

0

Ma

r-21

Jun

-21

Se

p-2

1

US EurozoneChina Japan

Global Economy

Energy shortages and elevated inflation could impact an otherwise robust global economic recovery

Source: IMF: World Economic Outlook Oct 2021, Bloomberg’s COVID-19 Tracker.

Note: * GDP forecast for India pertains to fiscal year, EMDEs: Emerging Market and Developing Economies, AEs: Advanced Economies

GDP growth Forecasts (%YoY)

• IMF reduced 2021 growth marginally (-10 bps) to 5.9%, due to

Delta variant outbreaks in turn leading to global supply chain

disruptions, longer-than-expected lead times, and high inflation in

many countries. Chip shortages affecting global auto industry.

• US: Slight moderation in an otherwise strong economy, due to

ongoing supply chain disruptions and rising commodity and

energy prices. Housing and labour markets continue to be robust.

• Europe: Despite headwinds pertaining to supply shortages and

elevated inflation, economic growth underpinned by high

vaccination rates and strong investment-driven recovery.

• Japan: Economic activities moderated in July to September as

infections soared. Strong catch-up in vaccinations which were

lagging vs. other Advanced Economies.

• China: Chinese economy slowing down due to reduced real

estate investment and energy shortages, while exports have

remained robust driven by demand from Advanced Economies.

Government and central bank expected to provide policy support

to aid growth. 0%

20%

40%

60%

80%

100%

Jan

Fe

b

Ma

r

Ap

r

Ma

y

Jun

Jul

Au

g

Se

p

05-O

ct

US EUChina Japan

% of Population vaccinated (CY21) PMI – Manufacturing

6.0

%

5.6

%

7.0

%

4.6

%

2.8

% 6

.3%

9.5

%

8.1

%

5.9

%

5.2

%

6.0

%

5.0

%

2.4

%

6.4

%

9.5

%

8.0

%

4.9

%

4.5

%

5.2

%

4.3

%

3.2

%

5.1

%

8.5

%

5.6

%

World AEs US Euro area Japan EMDEs India China

CY21F(July) CY21F(Oct) CY22F(Oct)

Confidential Better Everyday 5

2,000

2,500

3,000

3,500

4,000

Zinc (US$/mt)

Aluminium (US$/mt)

200

600

1,000

1,400

1,800

2,200

2,600

Oct-19 Apr-20 Oct-20 Apr-21 Oct-21

N.America ExW

N.Europe ExW

China FOB

Black Sea FOB

Global Steel 6

69

12

45

57

6

70

0

11

99

49

9

73

0

13

20

59

0

China World World ex-China

Jan-Aug CY19 Jan-Aug CY20 Jan-Aug CY21

Crude Steel Production – Jan-Aug (mt)

HRC prices US$/t

Source: Crude Steel production from World Steel Association (WSA), Bloomberg, Platts and NBS China.

Note: China published combined Export figures for Jan and Feb ’20 and ’21. The numbers have been equally distributed over Jan and Feb in the chart.

Steel prices supported by elevated input prices, moderating China production, and healthy demand outlook from World ex-China

China Steel Production and Export (mt)

Raw Material Price Trend (US$/t)

4.3%

10.1%

18.2%

0

2

4

6

8

10

0

50

100

150

Sep-19 Mar-20 Sep-20 Mar-21 Sep-21

China Crude Steel Production (LHS)

Exports (RHS)

50

550

1,050

50

100

150

200

250

Oct-19 Apr-20 Oct-20 Apr-21 Oct-21

Iron Ore 62% Fe

HCC Premium LV FOB Aus. (RHS)

HCC CFR China (RHS)

Steel Demand (mt)

Surge in Energy & Key Metal Prices

91

2

17

74

86

2

99

5

17

75

78

0

98

5

18

55

87

0

98

5

18

96

91

1

China World World ex-China

CY19 CY20 CY21F (Oct) CY22F (Oct)

-1%

4.5%

11.5%

5

15

25

35

120

160

200

240

Thermal Coal New Castle (US$/mt)

LNG JKM (US$/MMBtu) (RHS)

Confidential Better Everyday 6

0

100

200

300

400

0

50

100

150

Se

p-1

9

Dec-1

9

Ma

r-20

Jun

-20

Se

p-2

0

Dec-2

0

Ma

r-21

Jun

-21

Se

p-2

1

Tractor (LHS) CV (LHS)

PV (RHS)

Indian Economy

Source: MOSPI, SIAM, Ministry of commerce, EEPC, PIB

• Easing COVID restrictions and steady vaccination ramp-up have led

to strong bounce back in economic activity

• Auto production, mainly PV’s, affected by global chip shortages,

albeit expected to revive once chip supply eases

• Construction and Infra activities expected to gain momentum in H2

• Strong direct and indirect tax revenues reflect economic revival and

bode well for additional capital spending

• Govt. initiatives and benign longer-term trends supporting revival of

investment growth

o Announced National Monetization Pipeline of Rs.6tn of assets

over FY2022-25

o “Gati Shakti” launched with coordination across 16 ministries,

to deliver integrated multi-modal connectivity, reduce high

logistics costs in India and increase competitiveness

o Ongoing National Infrastructure Pipeline of Rs.110tn

o Improving housing cycle supported by low interest rates

o Stronger balance sheets of banks and corporates

• RBI stance is accommodative, while inflation and potential third

wave of COVID are risk

Supportive policy environment to aid strong recovery from H2 FY2022

Monthly Vehicle Production ('000s)

PMI – Manufacturing

202530354045505560

Se

p-1

9

Dec-1

9

Ma

r-20

Jun

-20

Se

p-2

0

Dec-2

0

Ma

r-21

Jun

-21

Se

p-2

1

India Merchandise Exports (US$ bn)

22%

24%

26%

28%

40

60

80

100

120

Jun

-19

Se

p-1

9

Dec-1

9

Ma

r-20

Jun

-20

Se

p-2

0

Dec-2

0

Ma

r-21

Jun

-21

Se

p-2

1

Total Exports (US$ Bn)

% of Engineering Goods (RHS)

0.000.200.400.600.801.001.201.401.60

Se

p-1

9

Dec-1

9

Ma

r-20

Jun

-20

Se

p-2

0

Dec-2

0

Ma

r-21

Jun

-21

Se

p-2

1

GST Collection (₹ Lakh Cr)

Confidential Better Everyday 7

Indian Steel

Steel Imports (mt) Steel Exports (mt) Production and Consumption (mt)

Production recovery in Q2 post second wave of COVID; strong demand expected in H2 FY22

Source: Joint Plant Committee

27.99

24.96

29.17

24.16

Crude Steel Production Apparent Steel Consumption

Q1 FY22 Q2 FY22

4.2% -3.2%

1.16 1.21

0.05 0.04

Q1 FY22 Q2 FY22

Finished Semis

1.21 1.25 3.7%

3.56 4.20

1.20 1.79

Q1 FY22 Q2 FY22

Finished Semis

4.76

5.99 25.8%

Qo

Q T

ren

d

Monthly Steel Imports (kt) and Exports (kt)

100

200

300

400

500

600

700

800

0

500

1,000

1,500

2,000

2,500

3,000

Ap

r-20

Ma

y-…

Jun

-20

Jul-2

0

Au

g-2

0

Se

p-2

0

Oct-

20

Nov-2

0

Dec-2

0

Jan

-21

Fe

b-2

1

Ma

r-21

Ap

r-21

Ma

y-…

Jun

-21

Jul-2

1

Au

g-2

1

Se

p-2

1

Exports (LHS) Imports (RHS)

6.36 7.69 8.15 8.46

9.40 9.21 10.26 10.17 9.61 9.71

8.96 7.85 8.15 8.01 7.92 8.23

Jun

-20

Jul-2

0

Au

g-2

0

Se

p-2

0

Oct-

20

Nov-2

0

Dec-2

0

Jan

-21

Fe

b-2

1

Ma

r-21

Ap

r-21

Ma

y-2

1

Jun

-21

Jul-2

1

Au

g-2

1

Se

p-2

1

-2.7 -2.9 -11.3 0.1 12.1 12 18.6 11 12.4 56.3 721.5 63.9

% YoY Change

Apparent Steel Consumption (mt) and YoY Growth

28.2 4.2 -10.3 -26

Confidential Better Everyday

Latin text

Heading: Arial Body: Arial

East Asian text

Heading: SimHei Body: SimHei Cover title:

Arial/30pt/R255,G255,B255/Bold

Cover subtitle:

Arial/16pt/R255,G255,B255

79

129

189

Theme

Color

(RGB)

192

80

77 219

132

61 137

165

78 113

88

143 0

80

163

255

255

255 0

0

0 255

255

255 0

0

0

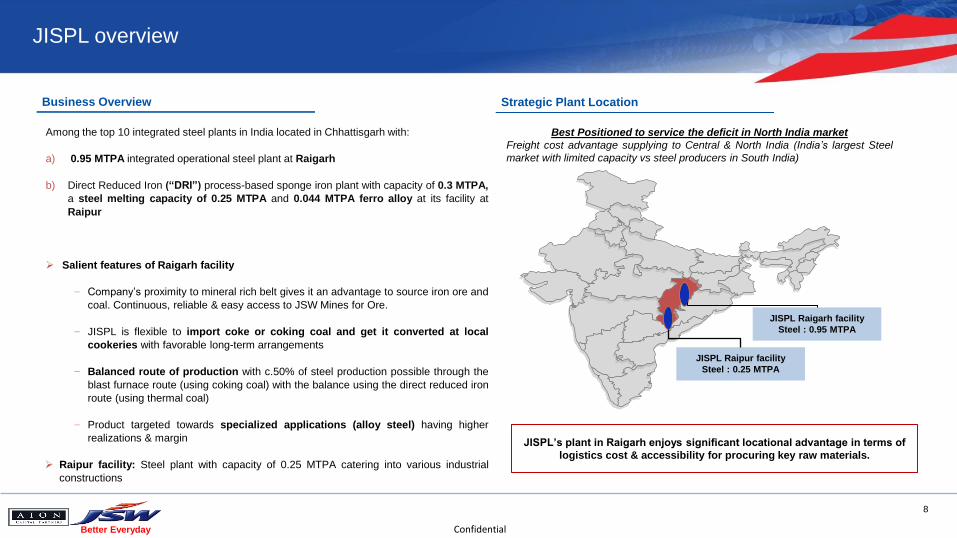

JISPL overview

8

Among the top 10 integrated steel plants in India located in Chhattisgarh with:

a) 0.95 MTPA integrated operational steel plant at Raigarh

b) Direct Reduced Iron (“DRI”) process-based sponge iron plant with capacity of 0.3 MTPA,

a steel melting capacity of 0.25 MTPA and 0.044 MTPA ferro alloy at its facility at

Raipur

Salient features of Raigarh facility

− Company’s proximity to mineral rich belt gives it an advantage to source iron ore and

coal. Continuous, reliable & easy access to JSW Mines for Ore.

− JISPL is flexible to import coke or coking coal and get it converted at local

cookeries with favorable long-term arrangements

− Balanced route of production with c.50% of steel production possible through the

blast furnace route (using coking coal) with the balance using the direct reduced iron

route (using thermal coal)

− Product targeted towards specialized applications (alloy steel) having higher

realizations & margin

Raipur facility: Steel plant with capacity of 0.25 MTPA catering into various industrial

constructions

JISPL’s plant in Raigarh enjoys significant locational advantage in terms of

logistics cost & accessibility for procuring key raw materials.

JISPL Raigarh facility

Steel : 0.95 MTPA

JISPL Raipur facility

Steel : 0.25 MTPA

Best Positioned to service the deficit in North India market

Freight cost advantage supplying to Central & North India (India’s largest Steel

market with limited capacity vs steel producers in South India)

Business Overview Strategic Plant Location

Confidential Better Everyday

Latin text

Heading: Arial Body: Arial

East Asian text

Heading: SimHei Body: SimHei Cover title:

Arial/30pt/R255,G255,B255/Bold

Cover subtitle:

Arial/16pt/R255,G255,B255

79

129

189

Theme

Color

(RGB)

192

80

77 219

132

61 137

165

78 113

88

143 0

80

163

255

255

255 0

0

0 255

255

255 0

0

0

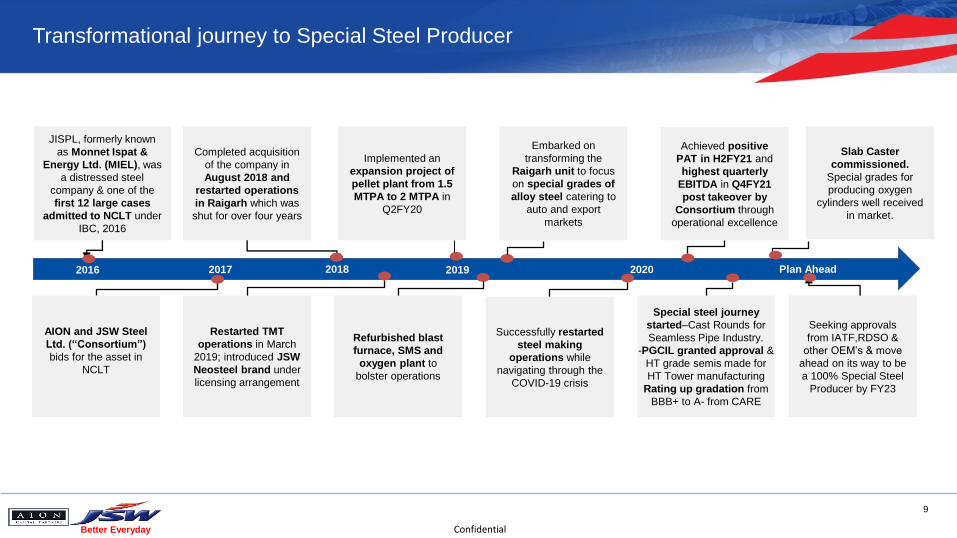

Transformational journey to Special Steel Producer

9

JISPL, formerly known

as Monnet Ispat &

Energy Ltd. (MIEL), was

a distressed steel

company & one of the

first 12 large cases

admitted to NCLT under

IBC, 2016

AION and JSW Steel

Ltd. (“Consortium”)

bids for the asset in

NCLT

Completed acquisition

of the company in

August 2018 and

restarted operations

in Raigarh which was

shut for over four years

Restarted TMT

operations in March

2019; introduced JSW

Neosteel brand under

licensing arrangement

Implemented an

expansion project of

pellet plant from 1.5

MTPA to 2 MTPA in

Q2FY20

Refurbished blast

furnace, SMS and

oxygen plant to

bolster operations

Embarked on

transforming the

Raigarh unit to focus

on special grades of

alloy steel catering to

auto and export

markets

Successfully restarted

steel making

operations while

navigating through the

COVID-19 crisis

Achieved positive

PAT in H2FY21 and

highest quarterly

EBITDA in Q4FY21

post takeover by

Consortium through

operational excellence

Seeking approvals

from IATF,RDSO &

other OEM’s & move

ahead on its way to be

a 100% Special Steel

Producer by FY23

2019 2016 2017 2018 2020 Plan Ahead

Special steel journey

started–Cast Rounds for

Seamless Pipe Industry.

-PGCIL granted approval &

HT grade semis made for

HT Tower manufacturing

Rating up gradation from

BBB+ to A- from CARE

Slab Caster

commissioned.

Special grades for

producing oxygen

cylinders well received

in market.

Confidential Better Everyday

Latin text

Heading: Arial Body: Arial

East Asian text

Heading: SimHei Body: SimHei Cover title:

Arial/30pt/R255,G255,B255/Bold

Cover subtitle:

Arial/16pt/R255,G255,B255

79

129

189

Theme

Color

(RGB)

192

80

77 219

132

61 137

165

78 113

88

143 0

80

163

255

255

255 0

0

0 255

255

255 0

0

0

Overview of manufacturing facilities

10

Other operational facilities:

1. Oxygen Plant: 400 TPD

2. Captive power plant + TRT: 174 MW

3. Railway siding

DRI plant

(0.31 MTPA)

Steel Melt-shop

(0.25 MTPA)

Billet caster

(0.3 MTPA) Structural mill

(0.15 MTPA)

Other facilities:

Captive power plant:

60 MW

Ferro Alloy

(0.044 MTPA)

Sinter plant

(0.96 MTPA)

Pellet plant

(2.2 MTPA)

Blast furnace

(0.62 MTPA)

DRI plant

(0.58 MTPA)

Steel Melt-shop I

(0.95 MTPA)

Steel Melt-shop II

(0.95 MTPA)

Billet caster

(1.2 MTPA)

Bar-rod mill

(0.5 MTPA)

Slab caster

(1.2 MTPA) Plate/Steckel Mill

(0.6 MTPA) Currently not operational Currently not operational

Raigarh Manufacturing Facility Overview

Raipur Manufacturing Facility Overview

Confidential Better Everyday

Latin text

Heading: Arial Body: Arial

East Asian text

Heading: SimHei Body: SimHei Cover title:

Arial/30pt/R255,G255,B255/Bold

Cover subtitle:

Arial/16pt/R255,G255,B255

79

129

189

Theme

Color

(RGB)

192

80

77 219

132

61 137

165

78 113

88

143 0

80

163

255

255

255 0

0

0 255

255

255 0

0

0

Key highlights

11

Attractive India steel macro environment

Attractive size and logistics cost advantage due to favorable location

Focusing on high value products with niche applications

Focus on ramping up volumes and expand product portfolio

Focus on cash flow generation and deleveraging

Leveraging JSW’s procurement, sale, distribution, brand & technical expertise

Confidential Better Everyday

*Sales are net of internal consumption

#Rolled products include TMT, Special Rolled, Structural Steel & Ferro Alloys

Latin text

Heading: Arial Body: Arial

East Asian text

Heading: SimHei Body: SimHei Cover title:

Arial/30pt/R255,G255,B255/Bold

Cover subtitle:

Arial/16pt/R255,G255,B255

79

129

189

Theme

Color

(RGB)

192

80

77 219

132

61 137

165

78 113

88

143 0

80

163

255

255

255 0

0

0 255

255

255 0

0

0

Q2FY22 performance at a glance – standalone

12

Intermediates Rolled Products#

480 KT 33 KT 293 KT 41 KT

INR 1,437 Cr INR 82 Cr

INR (37) Cr INR 19 Cr

Cast Products

103 KT 125 KT

Intermediates Rolled Products# Cast Products

Total production Total sales*

Revenue EBITDA

PAT Cash PAT

The production for Q2’22 was lower mainly due to shutdown of power plant for maintenance and consequent impact on production at Raipur and shutdown of blast

furnace for maintenance & stabilization of slab caster at Raigarh.

Confidential Better Everyday

*Sales are net of internal consumption

#Rolled products include TMT, Special rolled, Structural Steel & Ferro Alloys

Latin text

Heading: Arial Body: Arial

East Asian text

Heading: SimHei Body: SimHei Cover title:

Arial/30pt/R255,G255,B255/Bold

Cover subtitle:

Arial/16pt/R255,G255,B255

79

129

189

Theme

Color

(RGB)

192

80

77 219

132

61 137

165

78 113

88

143 0

80

163

255

255

255 0

0

0 255

255

255 0

0

0

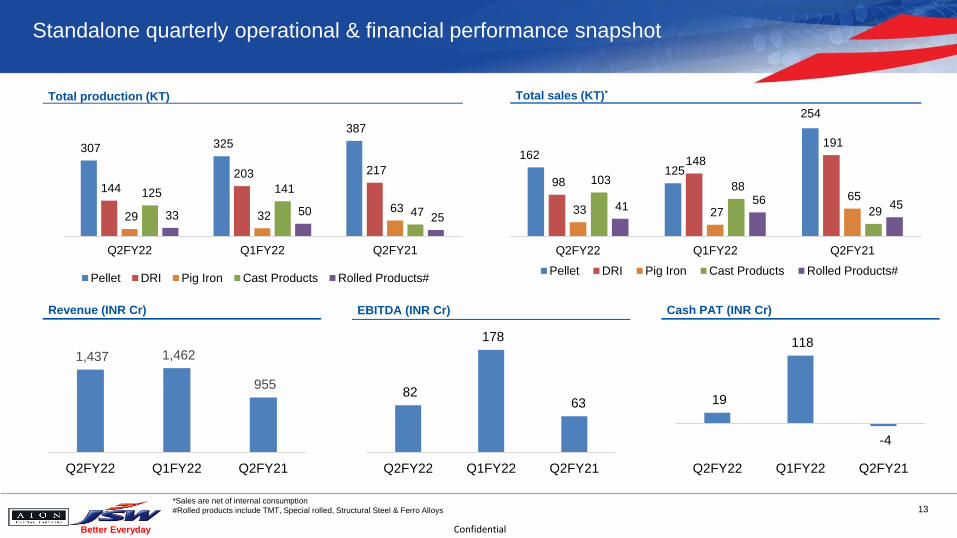

Standalone quarterly operational & financial performance snapshot

13

307 325

387

144

203 217

29 32 63

125 141

47 33 50 25

Q2FY22 Q1FY22 Q2FY21

Pellet DRI Pig Iron Cast Products Rolled Products#

162

125

254

98

148

191

33 27

65

103 88

29 41 56 45

Q2FY22 Q1FY22 Q2FY21

Pellet DRI Pig Iron Cast Products Rolled Products#

1,437 1,462

955

Q2FY22 Q1FY22 Q2FY21

82

178

63

Q2FY22 Q1FY22 Q2FY21

19

118

-4

Q2FY22 Q1FY22 Q2FY21

Total production (KT) Total sales (KT)*

Revenue (INR Cr) EBITDA (INR Cr) Cash PAT (INR Cr)

Confidential Better Everyday

Latin text

Heading: Arial Body: Arial

East Asian text

Heading: SimHei Body: SimHei Cover title:

Arial/30pt/R255,G255,B255/Bold

Cover subtitle:

Arial/16pt/R255,G255,B255

79

129

189

Theme

Color

(RGB)

192

80

77 219

132

61 137

165

78 113

88

143 0

80

163

255

255

255 0

0

0 255

255

255 0

0

0

Financial summary – standalone

14

Particulars (INR Cr) Q2FY22 Q2FY21 H1FY22 H1FY21

Revenue from operations 1,437 955 2,900 1,550

EBITDA 82 63 262 28

Other Income 5 2 12 5

Finance Cost 68 69 135 135

Depreciation 56 58 112 114

Profit Before Tax (37) (62) 27 (216)

Tax Expense/(Credit) - - - -

Profit After Tax (37) (62) 27 (216)

Cash PAT 19 (4) 139 (102)

Confidential Better Everyday

Latin text

Heading: Arial Body: Arial

East Asian text

Heading: SimHei Body: SimHei Cover title:

Arial/30pt/R255,G255,B255/Bold

Cover subtitle:

Arial/16pt/R255,G255,B255

79

129

189

Theme

Color

(RGB)

192

80

77 219

132

61 137

165

78 113

88

143 0

80

163

255

255

255 0

0

0 255

255

255 0

0

0

Forward looking and cautionary statement

15

Certain statements in this report concerning our future growth prospects are forward looking statements, which involve a number of risks, and uncertainties that could cause actual results to differ materially from

those in such forward looking statements. The risk and uncertainties relating to these statements include, but are not limited to risks and uncertainties regarding fluctuations in earnings, our ability to manage growth,

intense competition within Steel industry including those factors which may affect our cost advantage, wage increases in India, our ability to attract and retain highly skilled professionals, time and cost overruns on

fixed-price, fixed-time frame contracts, our ability to commission mines within contemplated time and costs, our ability to raise the finance within time and cost client concentration, restrictions on immigration, our

ability to manage our internal operations, reduced demand for steel, our ability to successfully complete and integrate potential acquisitions, liability for damages on our service contracts, the success of the

companies in which the Company has made strategic investments, withdrawal of fiscal/governmental incentives, impact of regulatory measures, political instability, legal restrictions on raising capital or acquiring

companies outside India, unauthorized use of our intellectual property and general economic conditions affecting our industry. The company does not undertake to update any forward looking statements that may be

made from time to time by or on behalf of the company.

JSW Steel Limited

Investor presentation August, 2020

Thank You