![Page 6: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/6.jpg)

Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic...

138

SPRINGER BRIEFS IN MATHEMATICS Jesús Martínez-Frutos Francisco Periago Esparza Optimal Control of PDEs under Uncertainty An Introduction with Application to Optimal Shape Design of Structures

Transcript of Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic...

![Page 1: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/1.jpg)

S P R I N G E R B R I E F S I N M AT H E M AT I C S

Jesús Martínez-Frutos Francisco Periago Esparza

Optimal Control of PDEs under UncertaintyAn Introduction with Application to Optimal Shape Design of Structures

![Page 2: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/2.jpg)

SpringerBriefs in Mathematics

Series editors

Nicola Bellomo, Torino, ItalyMichele Benzi, Atlanta, USAPalle Jorgensen, Iowa City, USATatsien Li, Shanghai, ChinaRoderick Melnik, Waterloo, CanadaLothar Reichel, Kent, USAOtmar Scherzer, Vienna, AustriaBenjamin Steinberg, New York, USAYuri Tschinkel, New York, USAGeorge Yin, Detroit, USAPing Zhang, Kalamazoo, USA

SpringerBriefs in Mathematics showcases expositions in all areas of mathematicsand applied mathematics. Manuscripts presenting new results or a single new resultin a classical field, new field, or an emerging topic, applications, or bridges betweennew results and already published works, are encouraged. The series is intended formathematicians and applied mathematicians.

![Page 3: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/3.jpg)

BCAM SpringerBriefsEditorial Board

Enrique ZuazuaDeusto TechUniversidad de DeustoBilbao, Spain

and

Departamento de MatemáticasUniversidad Autónoma de MadridCantoblanco, Madrid, Spain

Irene FonsecaCenter for Nonlinear AnalysisDepartment of Mathematical SciencesCarnegie Mellon UniversityPittsburgh, USA

Juan J. ManfrediDepartment of MathematicsUniversity of PittsburghPittsburgh, USA

Emmanuel TrélatLaboratoire Jacques-Louis LionsInstitut Universitaire de FranceUniversité Pierre et Marie CurieCNRS, UMR, Paris

Xu ZhangSchool of MathematicsSichuan UniversityChengdu, China

BCAM SpringerBriefs aims to publish contributions in the following disciplines: AppliedMathematics, Finance, Statistics and Computer Science. BCAM has appointed an EditorialBoard, who evaluate and review proposals.

Typical topics include: a timely report of state-of-the-art analytical techniques, bridgebetween new research results published in journal articles and a contextual literature review,a snapshot of a hot or emerging topic, a presentation of core concepts that students mustunderstand in order to make independent contributions.

Please submit your proposal to the Editorial Board or to Francesca Bonadei, Executive EditorMathematics, Statistics, and Engineering: [email protected].

More information about this series at http://www.springer.com/series/10030

![Page 4: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/4.jpg)

Jesús Martínez-Frutos • Francisco Periago Esparza

Optimal Control of PDEsunder UncertaintyAn Introduction with Application to OptimalShape Design of Structures

123

![Page 5: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/5.jpg)

Jesús Martínez-FrutosComputational Mechanics and ScientificComputing Group, Departmentof Structures and Construction

Technical University of CartagenaCartagena, Murcia, Spain

Francisco Periago EsparzaDepartment of Applied Mathematicsand Statistics

Technical University of CartagenaCartagena, Murcia, Spain

ISSN 2191-8198 ISSN 2191-8201 (electronic)SpringerBriefs in MathematicsISBN 978-3-319-98209-0 ISBN 978-3-319-98210-6 (eBook)https://doi.org/10.1007/978-3-319-98210-6

Library of Congress Control Number: 2018951210

© The Author(s), under exclusive license to Springer Nature Switzerland AG 2018This work is subject to copyright. All rights are reserved by the Publisher, whether the whole or partof the material is concerned, specifically the rights of translation, reprinting, reuse of illustrations,recitation, broadcasting, reproduction on microfilms or in any other physical way, and transmissionor information storage and retrieval, electronic adaptation, computer software, or by similar or dissimilarmethodology now known or hereafter developed.The use of general descriptive names, registered names, trademarks, service marks, etc. in thispublication does not imply, even in the absence of a specific statement, that such names are exempt fromthe relevant protective laws and regulations and therefore free for general use.The publisher, the authors and the editors are safe to assume that the advice and information in thisbook are believed to be true and accurate at the date of publication. Neither the publisher nor theauthors or the editors give a warranty, express or implied, with respect to the material contained herein orfor any errors or omissions that may have been made. The publisher remains neutral with regard tojurisdictional claims in published maps and institutional affiliations.

This Springer imprint is published by the registered company Springer Nature Switzerland AGThe registered company address is: Gewerbestrasse 11, 6330 Cham, Switzerland

![Page 7: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/7.jpg)

Preface

Both the theory and the numerical resolution of optimal control problems of sys-tems governed by—deterministic—partial differential equations (PDEs) are verywell established, and several textbooks providing an introduction to the funda-mental concepts of the mathematical theory are available in the literature [11, 16].

All of these books as well as most of the researches done in this field assume thatthe model’s input data, e.g. coefficient in the principal part of the differentialoperator, right-hand side term of the equation, boundary conditions or location ofcontrols, among others, are perfectly known. However, this assumption is unreal-istic from the point of view of applications. In practice, input data of physicalmodels may only be estimated [5]. In addition, as will be illustrated in this book,solutions of optimal control problems may exhibit a dramatic dependence on thoseuncertain data. Consequently, more realistic optimal control problems shouldaccount for uncertainties in their mathematical formulations.

Uncertainty appears in many other optimization problems. For instance, instructural optimization, where one aims to design the shape of a structure thatminimizes (or maximizes) a given criterion (rigidity, stress, etc.). All physicalparameters of the model, e.g. the loads, which are applied to the structure, aresupposed to be known in advance. However, it is clear that these loads either varyin time or vary from one sample to another or are simply unpredictable.

Among others, the following two approaches are used to account for uncer-tainties in control problems:

• On the one hand, if there is no a priori information on the uncertain inputs shortof lower and upper bounds on their magnitudes, then one may use a worst-casescenario analysis, which is formulated as a min-max optimization problem.More precisely, the idea is to minimize the maximal value of the cost functionover a given set of admissible perturbations. The advantage of this formulationis that, in general, it does not require an exhaustive previous analysis of theuncertain parameters of the model, just the lower and upper bounds of those.However, this a priori advantage may become a disadvantage because if theupper and lower bounds on the uncertain data are relatively large, then optimal

vii

![Page 8: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/8.jpg)

solutions obtained from this approach may be too conservative, leading to apoor performance of the physical system under consideration [1].

• On the other hand, when statistical information on the random inputs is avail-able, it is natural to model uncertainties using probabilistic tools. In someapplications, the mean and the spatial correlation of these inputs are estimatedfrom experimental data. From this, assuming a Gaussian-type distribution ofsuch inputs, those may be modelled by using, for example, Karhunen–Loève-type expansions. More elaborated statistical methods may also be used torepresent input parameters [5, 15]. Due to the great interest in applications, veryefficient computational methods for solving PDEs with random inputs have beendeveloped during the last two decades (see, e.g. [2, 3, 6, 9]). These continuoustheoretical and numerical improvements in the analysis and resolution of ran-dom PDEs have enabled the development of control formulations within aprobabilistic setting (see, e.g. [7, 13, 14]). Probably, the fact that this proba-bilistic framework is fed with experimental data is the main drawback of thisapproach. On the other hand, optimal solutions obtained from these probabilisticmethods are, in general, better than those obtained from a worst-case scenario.

This book aims at introducing graduate students and researchers to the basictheoretical and numerical tools which are being used in the analysis and numericalresolution of optimal control problems constrained by PDEs with random inputs.Thus, a probabilistic description of those inputs is assumed to be known in advance.The text is confined to facilitating the transition from control of deterministic PDEsto control of PDEs with random inputs. Hence, a previous elementary knowledge ofoptimal control of deterministic PDEs and probability theory is assumed. Werecommend the monograph [16] for a basic and very complete introduction todeterministic optimal control. Concerning probability theory, any introductorytextbook on probabilities, e.g. [8], provides the bases which are required in thisbook. See also [12, Chap. 4] for a complete review of this material.

The book is composed of seven chapters:Chapter 1 is devoted to a very brief introduction to uncertainty modelling, by use

of random variables and random fields, in optimal control problems. To this end,three very simple but illustrative examples are introduced. These examples coverthe cases of elliptic and evolution (first and second order in time) PDEs. We willconsistently use these models, but especially the elliptic one, to illustrate (some of)the main methods in optimal control of random PDEs.

Chapter 2 introduces the mathematical and numerical tools which are required inthe remaining chapters. Special attention is paid to the numerical approximation ofrandom fields by means of Karhunen–Loève (KL) expansions.

Chapter 3 focusses on the mathematical analysis of optimal control problems forrandom PDEs. Firstly, well-posedness of such random PDEs is proved byextending the classical methods for deterministic PDEs (Lax–Milgram theorem forthe elliptic case and the Galerkin method for evolution equations) to a suitableprobabilistic functional framework. Secondly, the existence of solutions for robustand risk-averse optimal control problems is proved. The former formulation

viii Preface

![Page 9: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/9.jpg)

naturally arises when one is primarily interested in minimizing statistical quantitiesof the cost functions such as its expectation. In order to reduce the dispersion of theobjective function around its mean, it is reasonable to consider measures of sta-tistical dispersion such as standard deviation. This choice, usually referred to in theliterature as robust control [10], aims at obtaining optimal solutions less sensitive tovariations in the input data. However, if one aims to obtain optimal controls forunlike realizations of the random input data (which therefore have a very littleimpact on the mean and variance of the objective function but which could havecatastrophic consequences), then risk-averse models ought to be considered. In thissense, risk-averse control [4] minimizes a risk function that quantifies the expectedloss related to the damages caused by catastrophic failures. A typical examplewhich illustrates the main difference between robust and risk-averse control is thefollowing: imagine that our optimization problems amount to finding the optimalshape of a bridge. If one is interested in maximizing the rigidity of the bridge in theface of daily random loads (e.g. cars and people passing across the bridge), then arobust formulation of the problem is a suitable choice. However, if the interest is todesign the bridge to be able to withstand the effects of an earthquake, then one mustuse a risk-averse approach. In probabilistic terms, robust control focusses on thefirst two statistical moments of the distribution to be controlled. Risk-averse controlalso takes into account the tail of such distribution.

Chapter 4 is concerned with numerical methods for robust optimal controlproblems. Both gradient-based methods and methods based on the resolution of thefirst-order optimality conditions are described. Smoothness with respect to therandom parameters is a key ingredient in the problems considered in this chapter.Thus, we focus on stochastic collocation (SC) and stochastic Galerkin(SG) methods [2], which, in this context, are computationally more efficient thanthe classical brute force Monte Carlo (MC) method. An algorithmic expositionof these methods, focussing on the practical numerical implementation, is pre-sented. To this end, MATLAB computer codes for the examples studied in thischapter are provided in http://www.upct.es/mc3/en/book.

Chapter 5 deals with the numerical resolution of risk-averse optimal controlproblems. An adaptive gradient-based minimization algorithm is proposed for thenumerical approximation of this type of problem. An additional difficulty whichemerges when dealing with risk-averse-type cost functionals is the lack ofsmoothness with respect to the random parameters. A combination of a stochasticGalerkin method with a Monte Carlo sampling method is used for the numericalapproximation of the cost functional and of its sensitivity. As in the precedingchapter, an algorithmic approach supported with MATLAB computer codes forseveral illustrative examples is presented.

Chapter 6 aims to illustrate how the methods presented in the book may be usedto solve optimization problems of interest in real applications. To this end, robustand risk-averse formulations of the structural optimization problem are analysedfrom theoretical and numerical viewpoints.

Preface ix

![Page 10: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/10.jpg)

Finally, Chap. 7 includes some concluding remarks and open problems.A list of references is included in each chapter. Also, links are provided to

websites hosting open-source codes related to the contents of the book.We have done our best in writing this book and very much hope that it will be

useful for readers. This would be our best reward. However, since the book isconcerned with uncertainties, very likely there are uncertainties in the text associ-ated with inaccuracies or simply errors. We would be very grateful to readers whocommunicate any such uncertainties to us. A list of possible errata and improve-ments will be updated on the website: http://www.upct.es/mc3/en/book/.

We would like to thank Enrique Zuazua for encouraging us to write this book.We also acknowledge the support of Francesca Bonadei, from Springer, and of theanonymous reviewers whose comments on the preliminary draft of the book led to abetter presentation of the material. Special thanks go to our closest collaborators(David Herrero, Mathieu Kessler, Francisco Javier Marín and Arnaud Münch)during these past years. Working with them on the topics covered by this texthas been a very fruitful and enriching experience for us. Finally, we acknowledgethe financial support of Fundación Séneca (Agencia de Ciencia y Tecnologíade la Región de Murcia, Spain) under project 19274/PI/14 and the SpanishMinisterio de Economía y Competitividad, under projects DPI2016-77538-R andMTM2017-83740-P.

Cartagena, Spain Jesús Martínez-FrutosJune 2018 Francisco Periago Esparza

References1. Allaire, A., Dapogny, Ch.: A deterministic approximation method in shape optimization under

random uncertainties. SMAI J. Comp. Math. 1, 83–143 (2015)2. Babuška, I., Novile, F., Tempone, R.: A Stochastic collocation method for elliptic partial

differential equations with random input data. SIAM Rev. 52 (2), 317–355 (2010)3. Cohen, A., DeVore, R.: Approximation of high-dimensional parametric PDEs. Acta Numer.

Graduate Studies in Mathematics, 1–159 (2015)4. Conti, S., Held, H., Pach, M., Rumpf, M., Schultz, R.: Risk averse shape optimization.

SIAM J. Control Optim. 49(3), 927–947 (2011)5. de Rocquigny, E., Devictor, N., Tarantola, S.: Uncertainty in industrial practice: a guide to

quantitative uncertainty management. Wiley, New Jersey (2008)6. Gunzburger, M. D., Webster, C., Zhang, G.: Stochastic finite element methods for partial

differential equations with random input data. Acta Numer. 23, 521–650 (2014)7. Gunzburger, M. D., Lee, H-C., Lee, J.: Error estimates of stochastic optimal Neumann

boundary control problems. SIAM J. Numer. Anal. 49 (4), 1532–1552 (2011)8. Jacod, J., Protter, P.: Probability essentials (Second Edition). Springer, Heidelberg (2003)9. Le Maître, O. P., Knio, O. M.: Spectral methods for uncertainty quantification. with appli-

cations to computational fluid dynamics. Springer, New York (2010)10. Lelievre, N., Beaurepaire, P., Mattrand, C., Gayton, N., Otsmane, A.: On the consideration of

uncertainty in design: optimization—reliability—robustness. Struct. Multidisc. Optim.(2016) https://doi.org/10.1007/s00158-016-1556-5

x Preface

![Page 11: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/11.jpg)

11. Lions, J. L.: Optimal control of systems governed by partial differential equations. Springer,Berlin (1971)

12. Lord, G. L., Powell, C. E., Shardlow, T.: An introduction to computational stochastic PDEs.Cambridge University Press, Cambridge (2014)

13. Lü, Q, Zuazua, E.: Averaged controllability for random evolution partial differential equa-tions. J. Math. Pures Appl. 105(3), 367–414 (2016)

14. Martínez-Frutos, J., Herrero-Pérez, D., Kessler, M., Periago, F.: Robust shape optimization ofcontinuous structures via the level set method. Comput. Methods Appl. Mech. Engrg. 305,271–291 (2016)

15. Smith, R. C. Uncertainty quantification. Theory, implementation, and applications.Computational Science & Engineering, Vol. 12. Society for Industrial and AppliedMathematics (SIAM), Philadelphia, PA (2014)

16. Tröltzsch, F.: Optimal control of partial differential equations: Theory, methods and appli-cations. Graduate Studies in Mathematics Vol. 112. AMS. Providence, Rhode Island (2010)

Preface xi

![Page 12: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/12.jpg)

Contents

1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.1 Motivation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.2 Modelling Uncertainty in the Input Data. Illustrative

Examples . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21.2.1 The Laplace-Poisson Equation . . . . . . . . . . . . . . . . . . . . . 31.2.2 The Heat Equation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41.2.3 The Bernoulli-Euler Beam Equation . . . . . . . . . . . . . . . . . 5

References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

2 Mathematical Preliminaires . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92.1 Basic Definitions and Notations . . . . . . . . . . . . . . . . . . . . . . . . . . 92.2 Tensor Product of Hilbert Spaces . . . . . . . . . . . . . . . . . . . . . . . . 112.3 Numerical Approximation of Random Fields . . . . . . . . . . . . . . . . 15

2.3.1 Karhunen-Loève Expansion of a Random Field . . . . . . . . . 162.4 Notes and Related Software . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

3 Mathematical Analysis of Optimal Control Problems UnderUncertainty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 313.1 Variational Formulation of Random PDEs . . . . . . . . . . . . . . . . . . 31

3.1.1 The Laplace-Poisson Equation Revisited I . . . . . . . . . . . . . 323.1.2 The Heat Equation Revisited I . . . . . . . . . . . . . . . . . . . . . 343.1.3 The Bernoulli-Euler Beam Equation Revisited I . . . . . . . . 36

3.2 Existence of Optimal Controls Under Uncertainty . . . . . . . . . . . . . 383.2.1 Robust Optimal Control Problems . . . . . . . . . . . . . . . . . . 383.2.2 Risk Averse Optimal Control Problems . . . . . . . . . . . . . . . 40

3.3 Differences Between Robust and Risk-Averse Optimal Control . . . 413.4 Notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

xiii

![Page 13: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/13.jpg)

4 Numerical Resolution of Robust Optimal Control Problems . . . . . . . 454.1 Finite-Dimensional Noise Assumption: From Random PDEs

to Deterministic PDEs with a Finite-Dimensional Parameter . . . . . 464.2 Gradient-Based Methods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

4.2.1 Computing Gradients of Functionals MeasuringRobustness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

4.2.2 Numerical Approximation of Quantities of Interestin Robust Optimal Control Problems . . . . . . . . . . . . . . . . 52

4.2.3 Numerical Experiments . . . . . . . . . . . . . . . . . . . . . . . . . . 614.3 Benefits and Drawbacks of the Cost Functionals . . . . . . . . . . . . . 704.4 One-Shot Methods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 704.5 Notes and Related Software . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

5 Numerical Resolution of Risk Averse Optimal Control Problems . . . . . 795.1 An Adaptive, Gradient-Based, Minimization Algorithm . . . . . . . . 795.2 Computing Gradients of Functionals Measuring Risk Aversion . . . . . 825.3 Numerical Approximation of Quantities of Interest in Risk

Averse Optimal Control Problems . . . . . . . . . . . . . . . . . . . . . . . . 825.3.1 An Anisotropic, Non-intrusive, Stochastic Galerkin

Method . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 835.3.2 Adaptive Algorithm to Select the Level

of Approximation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 855.3.3 Choosing Monte Carlo Samples for Numerical

Integration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 855.4 Numerical Experiments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 875.5 Notes and Related Software . . . . . . . . . . . . . . . . . . . . . . . . . . . . 89References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90

6 Structural Optimization Under Uncertainty . . . . . . . . . . . . . . . . . . . 916.1 Problem Formulation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 916.2 Existence of Optimal Shapes . . . . . . . . . . . . . . . . . . . . . . . . . . . . 946.3 Numerical Approximation via the Level-Set Method . . . . . . . . . . . 98

6.3.1 Computing Gradients of Shape Functionals . . . . . . . . . . . . 986.3.2 Mise en Scène of the Level Set Method . . . . . . . . . . . . . . 101

6.4 Numerical Simulation Results . . . . . . . . . . . . . . . . . . . . . . . . . . . 1026.5 Notes and Related Software . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

7 Miscellaneous Topics and Open Problems . . . . . . . . . . . . . . . . . . . . 1097.1 The Heat Equation Revisited II . . . . . . . . . . . . . . . . . . . . . . . . . . 1097.2 The Bernoulli-Euler Beam Equation Revisited II . . . . . . . . . . . . . 1147.3 Concluding Remarks and Some Open Problems . . . . . . . . . . . . . . 118References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 120

Index . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 121

xiv Contents

![Page 14: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/14.jpg)

About the Authors

Jesús Martínez-Frutos obtained his Ph.D. from theTechnical University of Cartagena, Spain, in 2014 andis currently Assistant Professor in the Department ofStructures and Construction and a member of theComputational Mechanics and Scientific Computinggroup at the Technical University of Cartagena, Spain.

His research interests are in the fields of robustoptimal control, structural optimization under uncer-tainty, efficient methods for high-dimensional uncer-tainty propagation and high-performance computingusing GPUs, with special focus on industrial applica-tions. Further information is available at: http://www.upct.es/mc3/en/dr-jesus-martinez-frutos/.

Francisco Periago Esparza completed his Ph.D. atthe University of Valencia, Spain, in 1999. He iscurrently Associate Professor in the Department ofApplied Mathematics and Statistics and a memberof the Computational Mechanics and ScientificComputing group at the Technical University ofCartagena, Spain.

His main research interests include optimal control,optimal design and controllability. During his researchtrajectory, he has published a number of articlesaddressing not only theoretical advances of theseproblems but also their application to real-worldengineering problems. During recent years, his researchhas focussed on optimal control for random PDEs.Further information is available at: http://www.upct.es/mc3/en/dr-francisco-periago-esparza/.

xv

![Page 15: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/15.jpg)

Acronyms and Initialisms

a.e. Almost everywherea.s. Almost sureANOVA Analysis of VarianceATD Anisotropic Total Degreee.g. for example (exempli gratia)etc. etceteraFEM Finite Element MethodHDMR High-Dimensional Model Representationi.e. that is (id est)i.i.d. independent and identically distributedKL Karhunen-LoèveMC Monte CarloPC Polynomial ChaosPDEs Partial Differential EquationsPDF Probability Density FunctionPOD Proper Orthogonal Decompositionr.h.s. right-hand sideRB Reduced BasisRPDEs Random Partial Differential EquationsSC Stochastic CollocationSG Stochastic GalerkinUQ Uncertainty Quantificationw.r.t. With respect to

xvii

![Page 16: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/16.jpg)

Abstract

This book offers a direct and comprehensive introduction to the basic theoreticaland numerical concepts in the emergent field of optimal control of partial differ-ential equations (PDEs) under uncertainty. The main objective of the book is toprovide graduate students and researchers with a smooth transition from optimalcontrol of deterministic PDEs to optimal control of random PDEs. Coverageincludes uncertainty modelling in control problems, variational formulation ofPDEs with random inputs, robust and risk-averse formulations of optimal controlproblems, existence theory and numerical resolution methods. The exposition isfocussed on running the whole path starting from uncertainty modelling and endingin the practical implementation of numerical schemes for the numerical approxi-mation of the considered problems. To this end, a selected number of illustrativeexamples are analysed in detail along the book. Computer codes, written inMATLAB, for all these examples are provided. Finally, the methods presented inthe text are applied to the mathematical analysis and numerical resolution of the,very relevant in real-world applications, structural optimization problem.

Keywords Uncertainty quantification � Partial differential equations with randominputs � Stochastic expansion methods � Robust optimal controlRisk-averse optimization � Structural shape optimization under uncertainty

xix

![Page 17: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/17.jpg)

Chapter 1Introduction

... in the small number of things which we are able to know withcertainty, even in the mathematical sciences themselves, theprincipal means for ascertaining—induction and analogy—arebased on probabilities; so that the entire system of humanknowledge is connected with the theory set forth in this essay..

Pierre Simon de Laplace.A Philosophical Essay on Probability, 1816.

1.1 Motivation

Mathematical models (and therefore numerical simulation results obtained fromthem) of physical, biological and economical systems always involve errors whichlead to discrepancies between simulation results and the results of real systems. Inparticular, simplifications of the mathematical model are often performed to facili-tate its resolution but these generate model errors, the numerical resolution methodintroduces numerical errors, and a limited knowledge of the system’s parameters,such as its geometry, initial and/or boundary conditions, external forces and mate-rial properties (diffusion coefficients, elasticity modulus, etc.), induces additionalerrors, called data errors. Some of the above errors may be reduced, e.g., by buildingmore accurate models, by improving numerical resolution methods, by additionalmeasurements, etc. This type of errors or uncertainties that can be reduced is usu-ally called epistemic or systematic uncertainty. However, there are other sources ofrandomness that are intrinsic to the system itself and hence cannot be reduced. It isthe so-called aleatoric or statistical uncertainty. A classical example of this type isUncertainty Principle of Quantum Mechanics.

© The Author(s), under exclusive license to Springer Nature Switzerland AG 2018J. Martínez-Frutos and F. Periago Esparza, Optimal Control of PDEs under Uncertainty,SpringerBriefs in Mathematics, https://doi.org/10.1007/978-3-319-98210-6_1

1

![Page 18: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/18.jpg)

2 1 Introduction

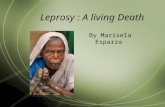

Quantification ofsources of uncertainty

Random variables

Model of the system Uncertainty Propagation

PDE Statistical moments

Probability of failure

Output PDF

Fig. 1.1 Uncertainty Quantification in PDEs-based mathematical models

For the above reasons, it is clear that if one aims at obtainingmore reliable numeri-cal predictions frommathematical models, then these should account for uncertainty.Aleatoric uncertainty is naturally defined in a probabilistic framework. In principle,the use of probabilistic tools to model epistemic uncertainty is not a natural choice.However, there is a tendency in Uncertainty Quantification (UQ) to reformulate epis-temic uncertainty as aleatoric uncertainty where probabilistic analysis is applicable[2]. In addition, from the point of view of numerical methods that will be proposedin this text, there is no difference between the above two types of uncertainty. Hence,a probabilistic framework for modelling and analysis of uncertainties is adoptedthroughout the book.

The termUncertainty Quantification is broadly used to define a variety ofmethod-ologies. In [5, p. 1] it is defined as “the science of identifying, quantifying, andreducing uncertainties associated with models, numerical algorithms, experiments,and predicted outcomes or quantities of interest”. Following [4, p. 525], in this textthe termUncertaintyQuantification is used to describe “the task of determining infor-mation about the uncertainty in an output of interest that depends on the solution ofa PDE, given information about the uncertainties in the system inputs”. This idea isillustrated in Fig. 1.1.

Remark 1.1 When statistical information on uncertainties is not available, othertechniques, such as worst case scenario analysis or fuzzy logic, may be used to dealwith uncertainty. These tools are outside the scope of this text.

1.2 Modelling Uncertainty in the Input Data. IllustrativeExamples

Among the different sources of uncertainty described in the preceding section, thistext is focussed on optimal control problems whose state variable is a solution ofa Random Partial Differential Equation (RPDE). The term random means that thePDE’s input data (coefficients, forcing terms, boundary conditions, etc.) are uncertainand are described as random variables or random fields.

In the following, we present several illustrative examples that will be analysed indetail along the book.

![Page 19: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/19.jpg)

1.2 Modelling Uncertainty in the Input Data. Illustrative Examples 3

1.2.1 The Laplace-Poisson Equation

Let D ⊂ Rd , d = 1, 2 or 3 in applications, be a bounded domain and consider the

following control system for Laplace-Poisson’s equation

{−div (a∇ y) = 1O u, in Dy = 0, on ∂ D,

(1.1)

where y = y(x), with x = (x1, . . . , xd) ∈ D, is the state variable and u = u(x) isthe control function, which acts on the spatial region O ⊂ D. As usual, 1O standsfor the characteristic function of O , i.e.,

1O (x) ={1, x ∈ O0, otherwise.

Here and throughout the text, both the divergence (div) and the gradient (∇) operatorsinvolve only derivatives with respect to the spatial variable x ∈ D. Recall that

∇ y =(

∂y

∂x1, . . . ,

∂y

∂xd

)

and

div (a∇ y) =d∑

j=1

∂

∂x j

(a

∂y

∂x j

).

Equation (1.1) is amodel for a variety of physical phenomena (deformation of elas-ticmembranes, steady-state heat conduction, electrostatics, steady-state groundwaterflow, etc.). For instance, in the case of heat conduction, y denotes the temperature ofa solid which occupies the spatial domain D, a is the material thermal conductivity,and u represents an internal heat source, which heats/cools the body (e.g., by elec-tromagnetic induction). For some nonhomogeneous materials, such as functionallygraded materials, large random spatial variabilities in the material properties havebeen observed [1].

Another example is the modelling of a steady-state, single-phase fluid flow. In thiscase y represents the hydraulic head, u is a source/sink term, and a is the saturatedhydraulic conductivity. In most aquifers, a is highly variable and never perfectlyknown (see [6, Chap. 1] where some experimental data for a are reported).

It is then natural to consider the coefficient a as a random function a = a (x,ω),where x ∈ D and ω denotes an elementary random event. As a consequence, thetemperature y, solution of (1.1), becomes a random space function y = y (x,ω).Hereafter, the probability distribution of a is assumed to be known and thus anunderlying abstract probability space (Ω,F ,P) is given. The sample space Ω isthe set of all possible outcomes (e.g., all possible measures of thermal conductivity),

![Page 20: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/20.jpg)

4 1 Introduction

F is the σ—algebra of events (hence, subsets of Ω to which probabilities may beassigned), and P : F → [0, 1] is a probability measure.

A typical optimal control problem that arises in this context amounts to finding acontrol u = u (x) such that its associated temperature y = y (u) is the best approx-imation (in a least-square sense) to a desired stationary temperature yd (x) in D.Hence, the cost functional

1

2

∫D

|y (x,ω) − yd (x) |2 dx + γ

2

∫O

u2 (x) dx, (1.2)

with γ ≥ 0, is introduced. The second term in (1.2) is a measure of the energy costneeded to implement the control u. It is observed that (1.2) depends on the realizationω ∈ Ω and hence a control u that minimizes (1.2) also depends on ω. Of course,one is typically interested in a control u, independent of ω, which minimizes (insome sense) the distance between y (x,ω) and yd (x). At first glance, it is naturalto consider the averaged distance, with respect to ω, of the functional (1.2). Theproblem then is formulated as:

⎧⎪⎪⎪⎪⎨⎪⎪⎪⎪⎩

Minimize in u : J (u) = 12

∫Ω

∫D |y (x, ω) − yd (x) |2 dx dP (ω) + γ

2

∫O u2 (x) dx

subject to−div (a (x, ω)∇ y (x, ω)) = 1Ou (x) , (x, ω) ∈ D × Ω

y (x, ω) = 0, (x, ω) ∈ ∂ D × Ω

u ∈ L2 (O) .

(1.3)

Following the usual terminology in Control Theory, throughout this text yd =yd(x) is the so-called target function, y = y(x,ω) is the state variable and u = u(x)

the control. To avoid awful notations, we shall make explicit only the variablesof interest that different functions depend on. For instance, to make explicit thedependence of the state variable y on the control u we will write y = y (u).

1.2.2 The Heat Equation

Consider the following control system for the transient heat equation

⎧⎪⎪⎨⎪⎪⎩

yt − div (a∇ y) = 0, in (0, T ) × D × Ω

a∇ y · n = 0, on (0, T ) × ∂ D0 × Ω

a∇ y · n = α (u − y) , on (0, T ) × ∂ D1 × Ω,

y (0, x,ω) = y0(x,ω) in D × Ω,

(1.4)

where the boundary of the spatial domain D ⊂ Rd is decomposed into two disjoint

parts ∂ D = ∂ D0 ∪ ∂ D1, and n is the unit outward normal vector to ∂ D. In system(1.4), yt denotes the partial derivative of y w.r.t. t ∈ (0, T ), and the control functionu = u (t, x) is the outside temperature, which is applied on the boundary region ∂ D1.

![Page 21: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/21.jpg)

1.2 Modelling Uncertainty in the Input Data. Illustrative Examples 5

As reported in [1], in addition to randomness in the thermal conductivity coeffi-cient a = a (x,ω), the initial temperature y0 and the convective heat transfer coeffi-cientα are very difficult tomeasure in practice and hence both are affected of a certainamount of uncertainty, i.e., y0 = y0 (x,ω) and α = α (x,ω). In real applications α

may also depend on the time variable t ∈ [0, T ] but, for the sake of simplicity, hereit is assumed to be stationary.

As in the preceding example, the state variable y = y (t, x,ω) of system (1.4),which represents the temperature of the material point x ∈ D at time t ∈ [0, T ] forthe random event ω ∈ Ω , is a random function.

Assume that a desired temperature yd (x) is given and that it is aimed to choosethe control u whichmust be applied to ∂ D1 in order to be as closer as possible to yd attime T . Similarly to problem (1.3), one may consider the averaged distance betweeny (T, x,ω) and yd (x) as the cost functional to be minimized. Another possibility isto minimize the distance between the mean temperature of the body occupying theregion D and the target temperature yd , i.e.,

∫D

(∫Ω

y(T, x,ω) dP(ω) − yd(x)

)2

dx .

Since only the mean of y (T ) is considered, there is no control on the dispersionof y (T ). Consequently, if the dispersion of y (T ) is large, then minimizing theexpectation of y (T ) is useless because for a specific random event ω, the probabilityof y (T,ω) of being close to its average is small. It is then convenient to minimizenot only the expectation but also a measure of dispersion such as the variance. Thus,the optimal control problem reads as:

⎧⎪⎨⎪⎩Minimize in u : J (u) = ∫

D(∫

Ω y(T, x,ω) dP(ω) − yd (x))2 dx + γ

2

∫D Var (y(T, x)) dx

subject to

y = y (u) solves (1.4), u ∈ L2(0, T ; L2 (∂ D1)

),

(1.5)where γ ≥ 0 is a weighting parameter, and

Var (y(T, x)) =∫

Ω

y2(T, x,ω) dP(ω) −(∫

Ω

y(T, x,ω) dP(ω)

)2

is the variance of y (T, x, ·).

1.2.3 The Bernoulli-Euler Beam Equation

Under Bernoulli-Euler hypotheses, the small random vibrations of a thin, uniform,hinged beam of length L , driven by a piezoelectric actuator located along the randominterval (x0 (ω) , x1 (ω)) ⊂ D := (0, L) are described by the system:

![Page 22: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/22.jpg)

6 1 Introduction

⎧⎪⎪⎨⎪⎪⎩

ytt + (ayxx )xx = v[δx1(ω) − δx0(ω)

]x , in (0, T ) × D × Ω

y(t, 0,ω) = yxx (t, 0,ω) = 0, on (0, T ) × Ω

y(t, L ,ω) = yxx (t, L ,ω) = 0, on (0, T ) × Ω

y(0, x,ω) = y0(x,ω), yt (0, x,ω) = y1(x,ω), in D × Ω,

(1.6)

where the beam flexural stiffness a = E I is assumed to depend on both x ∈ D andω ∈ Ω . i.e. a = a(x,ω). As usual E denotes Young’s modulus and I is the areamoment of inertia of the beam’s cross-section. Randomness in a is associated to anumber of random phenomena, e.g. variabilities of conditions during the manufac-turing process of the material’s beam (see [3] and the references therein).

In system (1.6), x0(ω) and x1(ω) stand for the end points of the actuator. Thedependence of these two points on a random event ω indicates that there is someuncertainty in the location of the actuator. δx j = δx j (x) is the Diracmass at the pointsx j ∈ D, j = 0, 1.

The function v : (0, T ) × Ω → R represents the time variation of a voltagewhichis applied to the actuator, andwhich is assumed to be affected by some randompertur-bation. Since physical controller devices are affected of uncertainty, it is realistic todecompose the control variable into an unknown deterministic and a known stochas-tic components. Moreover, it is reasonable to assume that the stochastic part bemodulated by the deterministic one. Thus, the function v = v(t,ω), which appearsin (1.6), takes the form

v(t,ω) = u(t)(1 + u(ω)

), (1.7)

where u : (0, T ) → R is the (unknown) deterministic control and u is a (known)zero-mean random variable which accounts for uncertainty in the controller device.

The random output y(t, x,ω) represents vertical displacement at time t of theparticle on the centreline occupying position x in the equilibrium position y = 0. Inthe above equations, yt and ytt denotefirst and secondderivativesw.r.t. t ∈ (0, T ), andthe subscripts “x” and “xx” are first and second derivatives w.r.t. x ∈ D, respectively.See Fig. 1.2 for the problem configuration.

Let H = L2(D) be the space of (Lebesgue) measurable functions v : D → R

whose norm

Fig. 1.2 Problemconfiguration for theBernoulli-Euler beam

y(t, x, ω) v(t, ω)

L

u (t)

x0 (ω) x1 (ω)

![Page 23: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/23.jpg)

1.2 Modelling Uncertainty in the Input Data. Illustrative Examples 7

‖v‖L2(D) :=(∫

Dv2(x) dx

)1/2

is finite. Consider the Sobolev space

V = H 2(D) ∩ H 10 (D) := {

v : D → R : v, v′, v′′ ∈ L2 (D) , v(0) = v(L) = 0},

endowed with the norm

‖v‖V = ‖v‖L2(D) + ‖v′‖L2(D) + ‖v′′‖L2(D).

The topological dual space of V is denoted by V �. For each random event ω ∈ Ω

and each control u ∈ L2 (0, T ), a measure of the amplitude and velocity of the beamvibrations at a control time T > 0 is expressed by

J (u,ω) = 1

2

(‖y (T,ω) ‖2H + ‖yt (T,ω) ‖2V �

). (1.8)

In this problem, one may be interested in computing a control u for rare occur-rences of the random inputs (which therefore have a very little impact on themean andvariance of J ), but which could have catastrophic consequences. For that purpose,the following risk averse model may be considered:

Jε (u) = P {ω ∈ Ω : J (u,ω) > ε} , (1.9)

where ε > 0 is a prescribed threshold parameter. The corresponding control problemis then formulated as:

⎧⎨⎩Minimize in u : Jε (u) = P {ω ∈ Ω : J (u,ω) > ε}subject to

y = y (u) solves (1.6), u ∈ L2 (0, T ) .

(1.10)

In the remaining chapters, we will consistently use the three above examples toillustrate the main theoretical and numerical methods in optimal control of randomPDEs.

References

1. Chiba, R.: Stochastic analysis of heat conduction and thermal stresses in solids: a review. In:Kazi, S.N. (ed.) Chapter 9 in Heat Transfer Phenomena and Applications. InTech (2012)

2. de Rocquigny, E., Devictor, N., Tarantola, S.: Uncertainty in Industrial Practice: A Guide toQuantitative Uncertainty Management. John Wiley & Sons, Ltd. (2008)

![Page 24: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/24.jpg)

8 1 Introduction

3. Ghanem, R.G., Spanos, P.D.: Stochastic Finite Elements: A Spectral Approach. Springer-Verlag, New York (1991)

4. Gunzburger, M.D., Webster, C., Zhang, G.: Stochastic finite element methods for partial dif-ferential equations with random input data. Acta Numer. 23, 521–650 (2014)

5. Smith, R.C.: Uncertainty quantification. Theory, implementation, and applications. Comput.Sci. Eng., 12. Society for Industrial andAppliedMathematics (SIAM), Philadelphia, PA (2014)

6. Zhang,D.: StochasticMethods for Flow inPorousMedia:CopingwithUncertainties.AcademicPress (2002)

![Page 25: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/25.jpg)

Chapter 2Mathematical Preliminaires

Everything should be made as simple as possible, but notsimpler.

Albert Einstein.

This chapter briefly collects the main theoretical and numerical tools which areneeded to the analysis and numerical resolution of control problems under uncer-tainty.Westartwith a fewbasic definitions andgeneral notations.Then, somematerialon tensor product of Hilbert spaces is reviewed. Finally, the numerical approximationof random fields by using Karhunen-Loève expansions is studied.

2.1 Basic Definitions and Notations

From now on in this text, D ⊂ Rd , d = 1, 2, 3 in applications, is a bounded and

Lipschitz domain with boundary ∂D. We denote by Lp (D), 1 ≤ p ≤ ∞, the space ofall (equivalence classes of) Lebesgue measurable functions g : D → R whose norm

‖g‖Lp(D) ={(∫

D |g(x)|p dx)1/p , p < ∞ess supx∈D |g(x)|, p = ∞

is finite. To make explicit the Lebesgue measure and hence avoid confusion, for1 ≤ p < ∞, Lp (D) will be denoted by Lp (D; dx) in some places in the next section.

Similarly, for 1 ≤ p < ∞,

Lp (∂D) ={g : ∂D → R measurable :

∫∂D

|g(x)|p ds < ∞}

,

© The Author(s), under exclusive license to Springer Nature Switzerland AG 2018J. Martínez-Frutos and F. Periago Esparza, Optimal Control of PDEs under Uncertainty,SpringerBriefs in Mathematics, https://doi.org/10.1007/978-3-319-98210-6_2

9

![Page 26: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/26.jpg)

10 2 Mathematical Preliminaires

where ds represents the surface Lebesgue measure on ∂D.The following Sobolev spaces will be of special importance in the remaining

of this book. H 1 (D) denotes the space of all functions y ∈ L2 (D) having first-orderpartial derivatives (in the sense of distributions) ∂xj y in L

2 (D). This space is endowedwith the inner product

< y, z >H 1(D)=∫Dyz dx +

∫D

∇y · ∇z dx,

which induces the norm

‖y‖H 1(D)

(∫D

(y2 + |∇y|2) dx

)1/2

.

As is well-known, H 1(D) is a separable Hilbert space. The space

H 10 (D) = {

y ∈ H 1(D) : y |∂D= 0},

where y |∂D denotes the trace of y, is also considered. In H 10 (D),

‖y‖H 10 (D) =

(∫D

|∇y|2 dx)1/2

defines a norm, which is equivalent to the norm in H 1 (D).(Ω,F , P) denotes a complete probability space. By complete it is meant thatF

contains all P-null sets, i.e., if B1 ⊂ Ω is such that there exists B2 ∈ F satisfyingB1 ⊂ B2 and P (B2) = 0, then B1 ∈ F . Notice that this concept of completenessmeans that the measure P is complete [10, p. 31].

For 1 ≤ p ≤ ∞, LpP(Ω) denotes the space composed of all (equivalence classes

of) measurable functions g : Ω → R whose norm

‖g‖LpP(Ω) =

{(∫Ω

|g (ω) |p dP (ω))1/p

, p < ∞ess supω∈Ω |g (ω) |, p = ∞

is finite. For convenience, LpP(Ω) will also be denoted by Lp (Ω; dP(ω)) in the next

section.If (X , ‖ · ‖X ) is a Banach space and 1 ≤ p ≤ ∞, Lp

P(Ω;X ) denotes the Lebesgue-

Bochner space composed of all (equivalence classes of) strongly measurable func-tions g : Ω → X whose norm

![Page 27: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/27.jpg)

2.1 Basic Definitions and Notations 11

‖g‖LpP(Ω;X ) =

{(∫Ω

‖g (·, ω) ‖pX dP (ω))1/p

, p < ∞ess supω∈Ω‖g (·, ω) ‖X , p = ∞

is finite. Since (Ω,F , P) is complete, LpP(Ω;X ) is complete (in the sense that every

Cauchy sequence in LpP(Ω;X ) is a convergent sequence; see [10, pp. 107 and 175]).

Given the probability space (Ω,F , P), the probability measure P induces a dis-tance d inF as follows: given E,F ∈ F ,

d (E,F) = P (E�F) ,

where E�F = (E F) ∪ (F E) is the symmetric difference between E and F . Theprobability space (Ω,F , P) is said to be separable if its associated metric space(F , d) is separable.1 It is proved that if (Ω,F , P) is separable, then Lp

P(Ω;X ) is

also separable [10, p. 177].Of particular interest in this book is the case p = 2. Precisely, let (H ,< ·, · >H )

be a separable Hilbert space. Analogously to the scalar case, it may be proved thatthe vector-valued space L2

P(Ω;H ), with the inner product

< f , g >L2P(Ω;H )=

∫Ω

< f (ω), g(ω) >H dP (ω)

is also a separable Hilbert space. The induced norm is given by

‖f ‖L2P(Ω;H ) =

(∫Ω

‖f (ω)‖2H dP (ω)

)1/2

.

2.2 Tensor Product of Hilbert Spaces

In this section, we review on some definitions and results on tensor product of Hilbertspaces, which shall be very useful in the study of random PDEs. We follow theapproach in [17, Chapter 2] and refer the reader to that reference for further details.All the Hilbert spaces considered in this section are assumed to be real and separable.

Definition 2.1 Let(H1,< ·, · >H1

),(H2,< ·, · >H2

)be two Hilbert spaces. Given

h1 ∈ H1 and h2 ∈ H2, the pure tensor h1 ⊗ h2 is defined as the bilinear form

h1 ⊗ h2 : H1 × H2 → R

(ϕ1, ϕ2) �→ (h1 ⊗ h2) (ϕ1, ϕ2) =< h1, ϕ1 >H1< h2, ϕ2 >H2 .(2.1)

LetH := span {h1 ⊗ h2, h1 ∈ H1, h2 ∈ H2} be the set of all finite linear combina-tions of such pure tensors. An inner product < ·, · >H is defined onH by definingit on pure tensors as

1We recall that a metric space (F , d) is separable if it has a countable dense subset.

![Page 28: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/28.jpg)

12 2 Mathematical Preliminaires

∀ϕ1 ⊗ ϕ2, ψ1 ⊗ ψ2, < ϕ1 ⊗ ϕ2, ψ1 ⊗ ψ2 >H =< ϕ1, ψ1 >H1< ϕ2, ψ2 >H2 ,

and then by extending it by linearity toH .It is proved that < ·, · >H is well defined in the sense that < ϕ,ψ >H , with

ϕ,ψ ∈ H , does not depend on which finite combinations are used to express ϕ andψ .

Definition 2.2 Let(H1,< ·, · >H1

),(H2,< ·, · >H2

)be two Hilbert spaces. The

tensor product of H1 and H2, denoted by H1 ⊗ H2, is the Hilbert space which isdefined as the completion of H with respect to the inner product < ·, · >H .

Proposition 2.1 [17, p. 50] If {ϕi}i∈N and{ψj

}j∈N are orthonormal bases of H1 and

H2, respectively, then{ϕi ⊗ ψj

}i,j∈N is an orthonormal basis of H1 ⊗ H2.

Remark 2.1 To simplify notation, both the spacesH1 andH2 in the preceding propo-sition have been taken infinite dimensional. The other cases, i.e. both spaces are finitedimensional or one of them is finite dimensional, are obviously similar.

In this book we are mainly concerned with random fields, i.e., with functionsf (x, ω) : D × Ω → R which depend on a spatial variable x ∈ D and on a randomevent ω ∈ Ω . Let us assume that f (x, ω) ∈ L2 (D × Ω; dx × dP (ω)), where dx isthe Lebesgue measure on D and P is the probability measure on Ω . As is usual,dx × dP (ω) denotes the associated product measure. Since f (x, ω) intrinsically hasa different structure with respect to x andω, thinking on the numerical approximationof such an f , the use of tensor product spaces is very convenient. Indeed, let {ϕi(x)}i∈Nand

{ψj(ω)

}j∈N be orthonormal bases of L2 (D; dx) and L2 (Ω; dP(ω)), respectively.

By Fubini’s theorem, it is not hard to show that{ϕi(x)ψj(ω)

}i,j∈N is an orthonormal

basis of L2 (D × Ω; dx × dP (ω)). Now, consider the mapping

U : L2 (D; dx) ⊗ L2 (Ω; dP(ω)) → L2 (D × Ω; dx × dP (ω)) ,

which is defined on the basis{ϕi(x) ⊗ ψj(ω)

}i,j∈N by

U(ϕi(x) ⊗ ψj(ω)

) = ϕi(x)ψj(ω)

and can be uniquely extended to a unitarymapping fromL2 (D; dx) ⊗ L2 (Ω; dP(ω))

onto L2 (D × Ω; dx × dP (ω)). Hence, if ϕ(x) = ∑∞i=1 ciϕi(x) ∈ L2 (D; dx) and

ψ (ω) = ∑∞j=1 djψj(ω) ∈ L2 (Ω; dP(ω)), then one has

U (ϕ ⊗ ψ) = U

⎛⎝∑

i,j

cidjϕi(x) ⊗ ψj(ω)

⎞⎠ =

∑i,j

cidjϕi(x)ψj(ω) = ϕ(x)ψ(ω).

In this sense, it is said that U defines a natural isomorphism between the spacesL2 (D; dx) ⊗ L2 (Ω; dP(ω)) and L2 (D × Ω; dx × dP (ω)). We write

![Page 29: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/29.jpg)

2.2 Tensor Product of Hilbert Spaces 13

L2 (D; dx) ⊗ L2 (Ω; dP(ω)) ∼= L2 (D × Ω; dx × dP (ω)) . (2.2)

Another interesting use of tensor product spaces is that they enable a nicerepresentation of vector-valued functions. Indeed, let (H ,< ·, · >H ) be a Hilbertspace with basis {ϕi}i∈N and consider the Bochner space L2

P(Ω;H ). Every function

f ∈ L2P(Ω;H ) may be written as

f (ω) = limN→∞

N∑k=1

fk(ω)ϕk , fk(ω) =< f (ω), ϕk >H and ω ∈ Ω.

The mapping

U :N∑

k=1

fk(ω) ⊗ ϕk �→N∑

k=1

fk(ω)ϕk

is well-defined from a dense subset of L2 (Ω, dP(ω)) ⊗ H onto a dense subset ofL2P(Ω;H ) and it preserves the norms. Hence, U may be uniquely extended to a

unitary mapping from L2 (Ω, dP(ω)) ⊗ H onto L2P(Ω;H ). As a consequence, if

f = f (ω) ∈ L2 (Ω, dP(ω)) andϕ ∈ H , then U (f (ω) ⊗ ϕ) = f (ω)ϕ. Because of thisproperty, it is said that U is a natural isomorphism between L2 (Ω, dP(ω)) ⊗ H andL2P(Ω;H ) and we may write

L2 (Ω, dP(ω)) ⊗ H ∼= L2P(Ω;H ) (2.3)

Remark 2.2 In the particular case in which H = L2 (D; dx), by (2.2) and (2.3) wehave the isomorphisms

L2P

(Ω;L2 (D)

) ∼= L2 (D; dx) ⊗ L2 (Ω; dP(ω)) ∼= L2 (D × Ω; dx × dP (ω)) .

As it will be shown in the next chapter, another very interesting case in which theisomorphism (2.3) applies is when H is a Sobolev space.

All the above discussion is summarized in the following abstract result:

Theorem 2.1 [17, Theorem II.10] Let (M1, μ1) and (M2, μ2) be measure spacesso that L2 (M1, dμ1) and L2 (M2, dμ2) are separable. Then:

(a) There is a unique isomorphism from the tensor space L2 (M1, dμ1) ⊗ L2

(M2, dμ2) to L2 (M1 × M2, dμ1 × dμ2) so that ϕ ⊗ ψ �→ ϕψ .(b) If (H ,< ·, · >H ) is a separableHilbert space, then there is a unique isomorphism

from L2 (M1, dμ1) ⊗ H to L2 (M1, dμ1;H ) so that f (x) ⊗ ϕ �→ f (x)ϕ.

Three typical situations to which the abstract results of this section will be appliedhereafter are the following:

• Let V be a Sobolev space, e.g. V = H 10 (D), and consider the space L2

P(Ω). By

part (b) of Theorem 2.1 one has the isomorphism

![Page 30: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/30.jpg)

14 2 Mathematical Preliminaires

L2P(Ω; V ) ∼= L2

P(Ω) ⊗ V .

• In the context of random PDEs, let us assume that inputs of the PDE dependon a finite number of uncorrelated real-valued random variables ξn : Ω → R,1 ≤ n ≤ N . Let us denote by Γn = ξn (Ω), by Γ = ∏N

n=1 Γn, and by ρ : Γ → R+the joint probability density function (PDF) of the multivariate random variableξ = (ξ1, . . . , ξN ), which is assumed to factorize as

ρ (z) =N∏n=1

ρn (zn) , z = (z1, . . . , zn) ∈ Γ,

with ρn : Γn → R+. Instead of working in the abstract space L2P (Ω) onemayworkin the image space

L2ρ (Γ ) ={f : Γ → R :

∫Γ

f 2 (z) ρ (z) dz < ∞}

,

which is equipped with the inner product

< f , g >L2ρ(Γ )=∫

Γ

f (z)g(z)ρ(z) dz.

We refer the reader to Sect. 4.1 in Chap. 4 for more details on this passage.Let

{ψpn (zn)

}∞pn=0, 1 ≤ n ≤ N , be an orthonormal basis of L2ρn

(Γn) composed of

a suitable class of orthonormal polynomials. Since L2ρ (Γ ) = ⊗Nn=1 L

2ρn

(Γn), amultivariate orthonormal polynomial basis of L2ρ (Γ ) is constructed as

{ψp (z) =

N∏n=1

ψpn (zn) , z = (z1, . . . , zN )

}

p=(p1,...,pN )∈NN

.

• Let y = y (z) ∈ L2ρ(Γ ;H 1

0 (D)). As it will be illustrated in Chaps. 4 and 5,

typically y is the solution of a given elliptic random PDE and one is inter-ested in its numerical approximation. As is usual, the vector valued functionz �→ y(·, z) ∈ H 1

0 (D) is identifiedwith the real-valued functionD × Γ � (x, z) �→y(x, z). Having in mind that L2ρ

(Γ ;H 1

0 (D)) ∼= L2ρ (Γ ) ⊗ H 1

0 (D), to approxi-mate numerically y(x, z), a standard finite element space Vh (D) ⊂ H 1

0 (D) andthe space Pp (Γ ) ⊂ L2ρ (Γ ) composed of polynomials of degree less than orequal to p, are considered. Hence, we look for a numerical approximationof y ∈ L2ρ (Γ ) ⊗ H 1

0 (D) in the finite dimensional space Pp (Γ ) ⊗ Vh (D). Let{ψm(z), 0 ≤ m ≤ Mp

}be a basis ofPp (Γ ) composed of orthonormal polynomi-

als in L2ρ (Γ ), and let {φn(x), 1 ≤ n ≤ Nh} be a basis of shape functions in Vh (D).Then,

{ψm ⊗ φn, 0 ≤ m ≤ Mp, 1 ≤ n ≤ Nh

}is a basis of Pp (Γ ) ⊗ Vh (D),

![Page 31: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/31.jpg)

2.2 Tensor Product of Hilbert Spaces 15

which is identified with{ψm(z)φn(x), 0 ≤ m ≤ Mp, 1 ≤ n ≤ Nh

}. Thus, an

approximation yhp (x, z) ∈ Pp (Γ ) ⊗ Vh (D) of y(x, z) is expressed in the form

yhp (x, z) =Nh∑n=1

p∑m=0

yn,mφn(x)ψm(z).

2.3 Numerical Approximation of Random Fields

As the examples in the preceding chapter show, uncertainty in the random inputsof a PDE are typically represented by functions a : D × Ω → R, which depend ona spatial variable x ∈ D and on a random event ω ∈ Ω . Such functions are calledrandom fields. Associated to a random field a (x, ω) it is interesting to consider thefollowing quantities:

• Mean (or expected) function a : D → R, which is defined by

a (x) = E [a (x, ·)] =∫

Ω

a (x, ω) dP (ω) . (2.4)

• Covariance function: Cova : D × D → R, which is defined by

Cova(x, x′) = E

[(a (x, ·) − a (x))

(a(x′, ·) − a

(x′))] (2.5)

and expresses the spatial correlation of the random field, i.e., Cova(x, x′) is the

covariance of the random variables ω �→ a (x, ω) and ω �→ a(x′, ω

).

• Variance function: Vara (x) = Cova (x, x).

The random field a is said to be second order if Vara (x) < ∞ for all x ∈ D. Aparticular type of random fields, which are widely used to model uncertainty insystems, is the class of Gaussian fields. A random field a (x, ω) is said to be Gaussianif for any M ∈ N and x1, x2, . . . , xM ∈ D the R

M -valued random variable X (ω) =(a(x1, ω

), a

(x2, ω

), . . . , a

(xM , ω

))follows the multivariate Gaussian distribution

N (μ,C), where

μ = (a(x1), . . . , a

(xM

))and Cij = Cova

(xi, xj

), 1 ≤ i, j ≤ M .

For computational purposes, it is very convenient to express a randomfield a(x, ω)

by means of a finite number of random variables {ξn (ω)}1≤n≤N , with N ∈ N+ ={1, 2, 3, . . .}. Among the different possibilities, Karhunen-Loève expansion is a veryusual choice to represent a random field.

![Page 32: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/32.jpg)

16 2 Mathematical Preliminaires

2.3.1 Karhunen-Loève Expansion of a Random Field

As it will be illustrated along this text, it is very appealing to have a representationof a random field in the form

a (x, ω) = a (x) +∞∑n=1

bn (x) ξn (ω) , (2.6)

with pairwise uncorrelated2 random variables{ξn (ω)

}∞n=1

having, for convenience,

zero mean and σ 2n variances, and L2 (D)-orthonormal functions {bn (x)}∞n=1.

To derive how the spatial functions bn (x) and the random variables ξn (ω) looklike, we continue our discussion in this section proceeding in a formal way. If (2.6)holds, then the covariance function (2.5) admits (at least formally) the representation

Cova(x, x′) = ∫

Ω

∞∑i=1

bi (x) ξi (ω)

∞∑n=1

bn(x′) ξn (ω) dP (ω)

=∞∑i=1

∞∑n=1

bi (x) bn(x′) ∫

Ω

ξi (ω) ξn (ω) dP (ω)

=∞∑n=1

σ 2n bn (x) bn

(x′) .

By multiplying this expression by bj(x′) and integrating in D, a direct (still formal)

computation leads to

∫DCova

(x, x′) bj (x′) dx′ = σ 2

j bj (x) ,

which means that{σ 2n , bn (x)

}∞n=1 are the eigenpairs associated to the operator

ψ �→∫DCova

(x, x′)ψ

(x′) dx′, ψ ∈ L2 (D) .

Denoting by ξn = 1σn

ξn, 1 ≤ n ≤ ∞, the random variables ξn have zero mean andunit variance. Then, (2.6) rewrites as

a (x, ω) = a (x) +∞∑n=1

σnbn (x) ξn (ω) . (2.7)

2We recall that a family of random variables{ξn (ω)

}∞n=1

having zero mean is said to be pairwise

uncorrelated if∫Ω

ξi (ω) ξj (ω) dP (ω) = 0 for i �= j.

![Page 33: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/33.jpg)

2.3 Numerical Approximation of Random Fields 17

Hence,

∫D[a (x, ω) − a (x)] bn (x) dx =

∞∑i=1

σiξi (ω)

∫Dbi (x) bn (x) dx = σnξn (ω) ,

that is,

ξn (ω) = 1

σn

∫D[a (x, ω) − a (x)] bn (x) dx.

These formal computations can be made rigorous, as the following results state.Before that, let us recall that a function C : D × D → R is symmetric if C

(x, x′) =

C(x′, x

)for all x, x′ ∈ D and C is non-negative definite if for any xj ∈ D and αj ∈ R,

1 ≤ j ≤ N , the inequalityN∑

j,k=1

αjαkC(xj, xk

) ≥ 0

holds.

Theorem 2.2 (Mercer) [14, Theorem 1.8] Let D ⊂ Rd be a bounded domain and

let C : D × D → R be a continuous, symmetric and non-negative definite function.Consider the integral operator C : L2 (D) → L2 (D) defined by

(Cψ) (x) =∫DC(x, x′)ψ

(x′) dx′. (2.8)

Then, there exist a sequence of, continuous in D, eigenfunctions {bn}∞n=1 of C , whichcan be chosen orthonormal in L2 (D), such that the corresponding sequence of eigen-values {λn}∞n=1 is positive. Moreover,

C(x, x′) =

∞∑n=1

λnbn (x) bn(x′) , x, x′ ∈ D, (2.9)

where the series converges absolutely and uniformly on D × D.

Theorem 2.3 (Karhunen-Loève expansion) [14, Theorems 5.28, 5.29, 7.52, 7.53]Let D ⊂ R

d be a bounded domain and let a = a (x, ω) be a random field with contin-uous covariance3 function Cova : D × D → R. Then, a (x, ω) admits the Karhunen-Loève expansion

3We recall that not any function may be taken as the covariance function of a random field. To bea valid covariance function it must be, in particular, non-negative definite. See [14, Theorem 5.18]for more details on this issue. All covariance functions considered in this text are assumed to becontinuous, symmetric and non-negative definite.

![Page 34: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/34.jpg)

18 2 Mathematical Preliminaires

a (x, ω) = a (x) +∞∑n=1

√λnbn (x) ξn (ω) , (2.10)

where the sum converges in L2P

(Ω;L2 (D)

). {λn, bn (x)}∞n=1 are the eigenpairs of the

operator C defined in Mercer’s theorem, with C(x, x′) = Cova

(x, x′), and

ξn (ω) = 1√λn

∫D[a (x, ω) − a (x)] bn (x) dx (2.11)

are pairwise uncorrelated random variables with zero mean and unit variance. If therandomfielda(x, ω) isGaussian, then ξn ∼ N (0, 1)are independent and identicallydistributed (i.i.d.) standard Gaussian variables.

Remark 2.3 Note that, thanks to Theorem 2.3, a Gaussian field a(x, ω) is completelydetermined by its expected function a (x) and its covariance function. Indeed, fromCova

(x, x′) one computes the eigenpairs {λn, bn(x)}∞n=1 of the operator (2.8). Thus,

if a (x) is known, then the KL expansion (2.10) determines the Gaussian field a(x, ω)

since the random variables that appear in (2.10) are i.i.d. standardGaussian variables.As a consequence, if the mean and covariance functions of the Gaussian field a(x, ω)

are properly estimated from experimental data, then a is completely characterized(see also Remark 2.4 for more details on this issue).

For numerical simulation purposes, the expansion (2.10) is always truncated at somelarge enough term N , i.e., the random field a (x, ω) is approximated as

a (x, ω) ≈ aN (x, ω) = a (x) +N∑n=1

√λnbn (x) ξn (ω) . (2.12)

The convergence rate of aN (x, ω) depends on the decay of the eigenvalues λn, whichin turn depends on the smoothness of it associated covariance function. Precisely, forpiecewise Sobolev regular covariance functions, the eigenvalue decay is algebraic.For piecewise analytic covariance functions, the rate decay is quasi-exponential (see[19] and the references therein).

A measure of the relative error committed by truncation of a KL expansion isgiven by the so-called variance error [14, 18]

EN (x) = Vara−aN (x)

Vara (x)= C (x, x) − ∑N

n=1 λnb2n (x)

C (x, x)= 1 −

∑Nn=1 λnb2n (x)

C (x, x), (2.13)

where, to alleviate the notation, from now on C = Cova is the covariance functionof a. Second equality in (2.13) is easily obtained from Theorems 2.2 and 2.3. See[14, Corollary 7.54] for more details. A global measure of this relative error, whichis called mean error variance, is

![Page 35: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/35.jpg)

2.3 Numerical Approximation of Random Fields 19

EN =∫D Vara−aN (x) dx∫

D Vara (x) dx=

∫D C (x, x) dx − ∑N

n=1 λn∫D C (x, x) dx

= 1 −∑N

n=1 λn∫D C (x, x) dx

.

(2.14)For some specific covariance functions and simple geometries of the physical

domain D, it is possible to find analytical expressions of KL expansions, as thefollowing example shows.

Example 2.1 (Exponential Covariance) Consider a Gaussian field a = a (x, ω) withzero mean, unit variance and having the following exponential covariance function:

C(x, x′) = e−|x−x′|/Lc , x, x′ ∈ D = (0,L) , (2.15)

where Lc is the so-called correlation length. The eigenpairs {λn, bn(x)}∞n=1 associatedto C

(x, x′) are obtained by solving the spectral problem

∫ x

0e− x−x′

Lc b(x′) dx′ +

∫ L

xe− x′−x

Lc b(x′) dx′ = λb (x) . (2.16)

By differentiating twice and by evaluating b′ (x) at the end points x = 0,L, thespectral problem (2.16) takes the form

{b′′ (x) + 1

Lc

(2λ

− 1Lc

)b (x) = 0, 0 < x < L

b′ (0) = 1Lcb (0) , b′ (L) = − 1

Lcb (L) .

(2.17)

Denoting by � = L/Lc, the eigenvalues of (2.17) are given by

λn = 2�2Lc�2 + γ 2

n

, (2.18)

where γn, n ∈ N, are the positive solutions of the transcendental equation

cot (γn) = γ 2n − �2

2�γn. (2.19)

Its associated normalized eigenfunctions are

bn (x) =√

2

�2 + γ 2n + 2�

[γn cos

(γnx

L

)+ � sin

(γnx

L

)], 0 < x < L. (2.20)

The energy of a is given by

‖a‖2L2(D)⊗L2P(Ω)

=∫ L

0Vara (x) dx =

∫ L

0C (x, x) dx = L. (2.21)

![Page 36: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/36.jpg)

20 2 Mathematical Preliminaires

Consider theN -term truncationaN (x, ω) = ∑Nn=1

√λnbn (x) ξn (ω),where the eigen-

values are ordered in decreasing order, i.e., λ1 ≥ λ2 ≥ · · · ≥ λN . Taking into accountthat {bn (x)}∞n=1 are orthonormal in L2 (D) and that ξn ∼ N (0, 1) are independent,a direct computation shows that

‖aN‖2L2(D)⊗L2P(Ω)

=N∑n=1

λn. (2.22)

Hence, if one aims to capture a certain amount, e.g. 90%, of the energy of the fielda, then the truncation term N must be chosen as to satisfy the condition EN ≤ 0.1,with EN given by (2.14), which, in this example, corresponds to

N∑n=1

λn ≥ 0.9L.

Figure 2.1a shows the first 100 eigenvalues obtained using (2.18), with L = 1 anddifferent values of Lc. The transcendental equation (2.19) is solved by the classicalNewton method. Figure 2.1b displays the first 5 eigenfunctions for Lc = 0.5.

The rate decay of eigenvalues determines how fast the variance error and themean error variance are reduced. This fact is observed in Fig. 2.2, where these errorsare depicted as a function of N and for several values of the correlation length Lc.One can observe how the number of terms needed to reduce the relative error to adesired threshold increases as Lc → 0. This issue is of paramount importance froma computational point of view since the number of terms of the KL expansion andthus the number of simulations required for an accurate representation of the field

(a) (b)

Fig. 2.1 Example 2.1: (a) Eigenvalues λn, 1 ≤ n ≤ 100 for the correlation lengths Lc = 0.05(dash red line), Lc = 0.5 (dot-dash blue line) and Lc = 5 (solid green line). (b) Eigenfunctions for1 ≤ n ≤ 5 and Lc = 0.5

![Page 37: Jesús Martínez-Frutos Francisco Periago Esparza Optimal ... · Thus, we focus on stochastic collocation (SC) and stochastic Galerkin (SG) methods [2], which, in this context, are](https://reader034.fdocuments.in/reader034/viewer/2022050102/5f41864da2ba796cc076a5aa/html5/thumbnails/37.jpg)

2.3 Numerical Approximation of Random Fields 21

(a) (b)

Fig. 2.2 Example 2.1: (a) Mean error variance EN for 1 ≤ N ≤ 100 and Lc = 0.05 (dash line),Lc = 0.5 (dot-dash line) and Lc = 5 (solid line), and (b) variance error EN (x) for Lc = 0.5 andN = 9, 21, 42

Fig. 2.3 Example 2.1: (a) Covariance of a(x, ω), and (b) Covariance of a42(x, ω)

would be large in case the spectrum decays slowly. Notice also that the largest valuesof EN (x) in Fig. 2.2b are located at the end points of the interval. This is due to thefact that since the eigenvalues are ordered in decreasing order, the dominant termin EN (x) is the first one, whose associated eigenfunction b1(x) takes its minimumvalues at x = 0, 1 (see Fig. 2.1b).

In the same vein, Fig. 2.3 displays the covariance functions of the random fielda(x, ω) and of its truncation at the 42-th term.