Investor Presentation - Marathon Petroleum presentation contains forward-looking statements within...

93

Investor Presentation September 2013 1

Transcript of Investor Presentation - Marathon Petroleum presentation contains forward-looking statements within...

Investor Presentation

September 2013

1

Forward-Looking Statements

2

This presentation contains forward-looking statements within the meaning of federal securities laws regarding both MPC and MPLX. These forward-looking statements relate to, among other things, MPC’s current expectations, estimates and projections concerning MPC’s and MPLX’s business and operations. You can identify forward-looking statements by words such as “anticipate,” “believe,” “estimate,” “expect,” “forecast,” “project,” “could,” “may,” “should,” “would,” “will” or other similar expressions that convey the uncertainty of future events or outcomes. Such forward-looking statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are beyond the company’s control and are difficult to predict. Factors that could cause MPC’s actual results to differ materially from those in the forward-looking statements include: the availability and pricing of crude oil and other feedstocks; slower growth in domestic and Canadian crude supply; completion of pipeline capacity to areas outside the U.S. Midwest; the reliability of processing units and other equipment; MPC’s ability to successfully implement growth opportunities; MPC’s ability to successfully achieve the strategic and financial objectives related to the acquisition of the Galveston Bay refinery and related assets, including achieving the projected synergies and the acquisition being accretive to its earnings; impacts from MPC’s repurchases of its shares of common stock under its stock repurchase authorization, including the timing and amounts of any common stock repurchases; other risk factors inherent to MPC’s industry; and the factors set forth under the heading “Risk Factors” in MPC’s Annual Report on Form 10-K for the year ended December 31, 2012 filed with the SEC. Factors that could cause MPLX’s actual results to differ materially from those in the forward-looking statements include: the adequacy of MPLX’s capital resources and liquidity, including, but not limited to, availability of sufficient cash flow to pay distributions and execute its business plan; completion of pipeline capacity by MPLX’s competitors; disruptions due to equipment interruption or failure; the suspension, reduction or termination of MPC’s obligations under its commercial agreements; MPLX’s ability to successfully implement its growth strategy, whether through organic growth or acquisitions; other risk factors inherent to MPLX’s industry; and the factors set forth under the heading “Risk Factors” in MPLX’s Annual Report on Form 10-K for the year ended December 31, 2012 filed with the SEC. Factors that could cause MPC’s and MPLX’s actual results to differ materially from those in the forward-looking statements include: the timing and extent of changes in commodity prices and demand for crude oil, refined products, feedstocks or other hydrocarbon-based products; volatility in and/or degradation of market and industry conditions; consumer demand for refined products; transportation logistics; and state and federal environmental, economic, health and safety, energy and other policies and regulations, including the cost of compliance with the Renewable Fuel Standard. In addition, the forward-looking statements included herein could be affected by general domestic and international economic and political conditions. Unpredictable or unknown factors not discussed here, in MPC’s Form 10-K or in MPLX’s Form 10-K could also have material adverse effects on results.

Strategic Vision

Achieve top tier safety/environmental performance

Grow enterprise value

Expand platform for MPLX growth

Deliver top quartile refining performance

Increase Speedway and Marathon brand assured sales volumes

Deliver profitable Speedway growth

3

Goal: Top Quartile Total Shareholder Return

Deliver Top Tier Safety Performance

4

Record safety performance across our operations in 2012

World-class safety performance for DHOUP

Continue industry leadership on preventive maintenance

Achieve Top Tier Safety/Environmental Performance

Grow Enterprise Value

Earnings growth

Strong dividend, growing over the long term

Sustained share repurchase program

Valuation re-rate/uplift

5

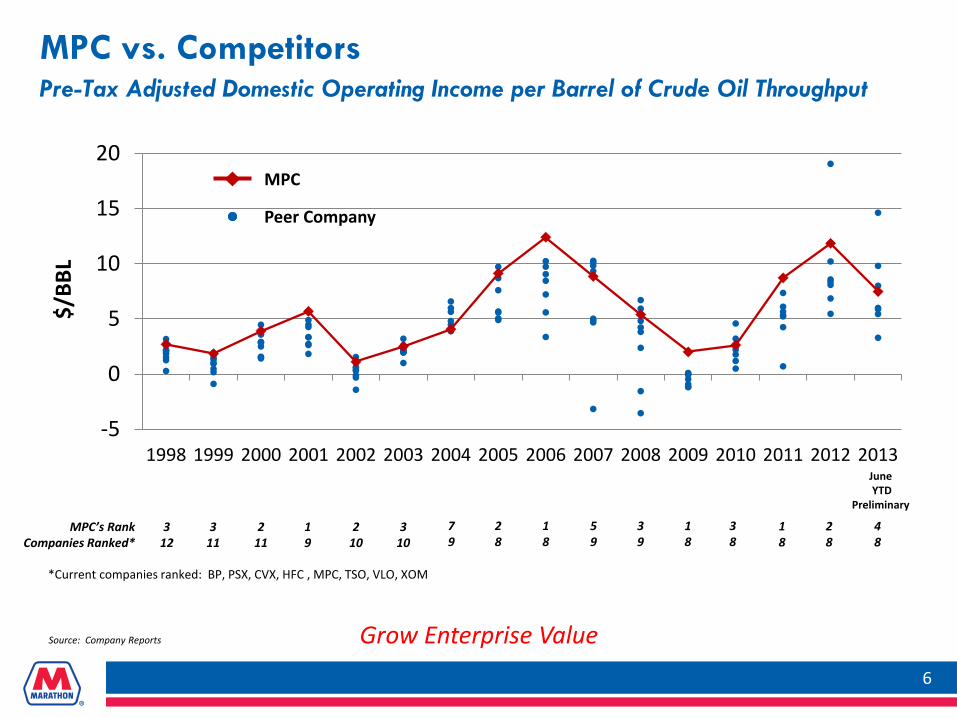

Grow Enterprise Value

MPC vs. Competitors Pre-Tax Adjusted Domestic Operating Income per Barrel of Crude Oil Throughput

6

$/BB

L

*Current companies ranked: BP, PSX, CVX, HFC , MPC, TSO, VLO, XOM

Source: Company Reports

2 11

MPC’s Rank Companies Ranked*

3 12

3 11

1 9

2 10

7 9

2 8

5 9

3 9

1 8

3 10

1 8

3 8

1 8

2 8

-5

0

5

10

15

20

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

MPC

Peer Company

4 8

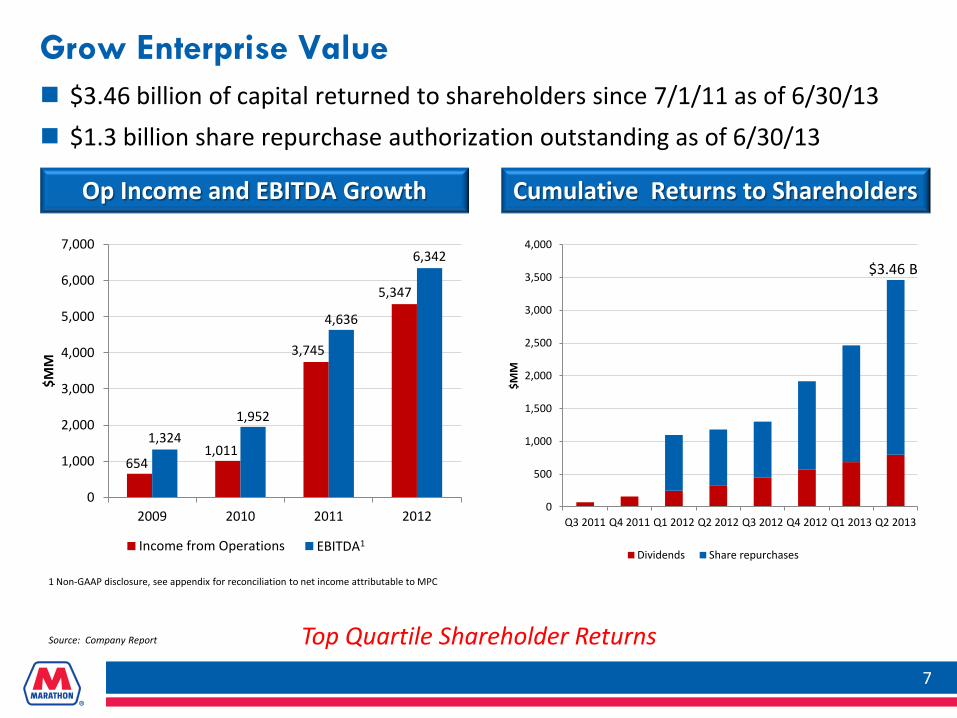

Grow Enterprise Value

June YTD

Preliminary

Grow Enterprise Value

Op Income and EBITDA Growth

$3.46 billion of capital returned to shareholders since 7/1/11 as of 6/30/13 $1.3 billion share repurchase authorization outstanding as of 6/30/13

Cumulative Returns to Shareholders

7

Top Quartile Shareholder Returns

1 Non-GAAP disclosure, see appendix for reconciliation to net income attributable to MPC

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013$M

M

Dividends Share repurchases

$3.46 B

654 1,011

3,745

5,347

1,324 1,952

4,636

6,342

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2009 2010 2011 2012

$MM

Income from Operations EBITDA(1)EBITDA1

Source: Company Report

Grow Enterprise Value Total Shareholder Return of 93% for 2012, 14% for 2013

8

31% 36%

67%

93%

43%

14%

0%

20%

40%

60%

80%

100%

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013

Cumulative Total Shareholder Return by Year

Top Quartile Shareholder Returns

9

Growth Drivers

MPC has Created an Industry-Leading MLP

10

Grow MPLX

20

25

30

35

40

45

10/2

5/12

11/1

2/12

11/2

7/12

12/1

1/12

12/2

6/12

01/1

0/13

01/2

4/13

02/0

7/13

02/2

2/13

03/0

8/13

03/2

2/13

04/0

8/13

04/2

2/13

05/0

6/13

05/2

0/13

06/0

4/13

06/1

8/13

07/0

2/13

07/1

7/13

07/3

1/13

08/1

5/13

08/2

9/13

Unit Price Focus on Fee-Based Businesses

Pursue Organic Growth Opportunities

Grow Through Acquisitions and Drop-downs

Maintain Safe and Reliable Operations

Acquisition of Galveston Bay Assets

451 MBPCD (475 MBPSD) high complexity refinery, Nelson Complexity Index of 15.3

Attractive base cash purchase price of ~$598 million

Potential $700 million earnout over six year period

Closed February 1, 2013; financed with cash on hand

Estimated incremental annual EBITDA based on:

2006-2010 Prices: ~$1,200 million

2011 Prices: ~$700 million

11

Deliver Top Quartile Refining Performance

Detroit Heavy Oil Upgrade Project Increased heavy oil capacity from

20,000 BPCD to 100,000 BPCD 28,000 BPCD delayed Coker

36,000 BPCD Distillate Hydrotreater (DHT)

Crude capacity increased ~14,000 BPCD

Discounted Canadian crude

Investment: $2.2 billion* project

Estimated incremental annual EBITDA based on: 2006 -2010 Prices: ~$200 million

2011 Prices: ~$350 million

Operated at design capacity YTD 2013

*Excludes capitalized interest

Deliver Top Quartile Refining Performance 12

Garyville Major Expansion (GME) Project

Garyville, LA refinery is last grassroots refinery built in the U.S. (1976)

Base Garyville refinery, 2008 Solomon survey Best U.S. cash cost operating expense Second-best U.S. Energy Intensity Index

GME Project completed in late 2009 - significantly expanded crude oil refining capacity and improved Garyville’s overall fixed cash cost by ~20% per barrel

Garyville is the 3rd largest refinery in U.S. at 522,000 BPCD

13

Deliver Top Quartile Refining Performance

$3.9 Billion* Garyville Major Expansion

1/1/2009 256 MBPCD

Crude Capacity 190 MBPCD

Gasoline 95 MBPCD

Diesel 18th Largest

U.S. refinery

1/1/2012 490 MBPCD

Crude Capacity 305 MBPCD

Gasoline 215 MBPCD

Diesel Third Largest

U.S. refinery

*Excludes capitalized interest

14

1/1/2010 436 MBPCD

Crude Capacity 290 MBPCD

Gasoline 175 MBPCD

Diesel Fourth Largest

U.S. refinery

1/1/2011 464 MBPCD

Crude Capacity 300 MBPCD

Gasoline 185 MBPCD

Diesel Third Largest

U.S. refinery

1/1/2013 522 MBPCD

Crude Capacity 320 MBPCD

Gasoline 230 MBPCD

Diesel Third Largest

U.S. refinery

Deliver Top Quartile Refining Performance

Cumulative crude capacity increases (180 MBPCD) (208 MBPCD) (234 MBPCD) (266 MBPCD)

15

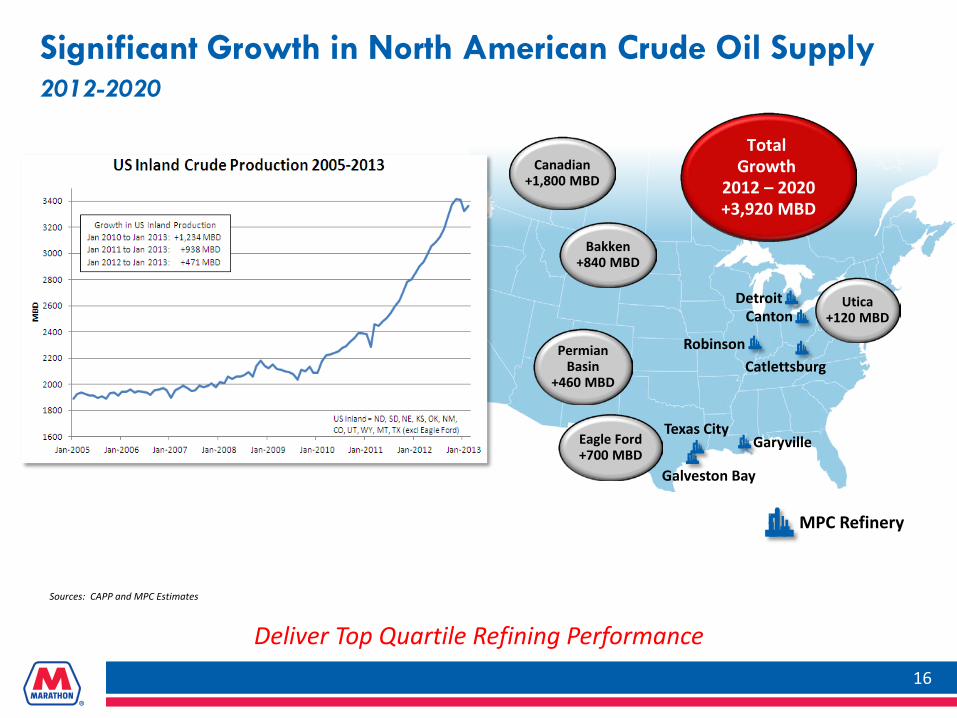

Supply Dynamics

Canadian +1,800 MBD

Permian Basin

+460 MBD

Eagle Ford +700 MBD

Utica +120 MBD

Total Growth

2012 – 2020 +3,920 MBD

Bakken +840 MBD

Significant Growth in North American Crude Oil Supply 2012-2020

16

Detroit Canton

Catlettsburg Robinson

Garyville Texas City

Sources: CAPP and MPC Estimates

Deliver Top Quartile Refining Performance

Galveston Bay

MPC Refinery

Balance in Refining Network

17 17

Midwest Capacity 646,000 BPCD

Louisiana Capacity 522,000 BPCD

Texas Capacity 531,000 BPCD

Canton (Ohio) 80,000

Catlettsburg (Ky.) 240,000

Detroit (Mich.) 120,000

Robinson (Ill.) 206,000

Galveston Bay (Texas) 451,000

Texas City (Texas) 80,000

Garyville (La.) 522,000

Total 1,699,000

Source: Oil & Gas Journal

As of Feb. 1, 2013

Deliver Top Quartile Refining Performance

Port Arthur Houston

Hardisty

Chicago

Wood River

Patoka

~$7.35/BBL Hardisty to USGC

~$1.95/BBL Houston to Chicago

~$5.50/BBL Hardisty to

Detroit

Detroit Value vs. USGC Refineries for Canadian Heavy Processing

Laid-In Crude Cost

$BBL

1.85

Higher Product Value 2.20*

Total Advantage 4.05

* Includes $0.25 time value of money to ship a light product barrel from Houston to Chicago

MPC Well Positioned to Capture Oil Sands Economics

Cushing

18

St. James

Deliver Top Quartile Refining Performance

Transportation Costs Set Crude Differentials

19

Sources: MPC Estimates based on publically available information, OPIS, and Argus Media.

Bakken

St. James

Patoka

Eagle Ford

Excludes gathering and truck transportation costs (up to ~$5.25/BBL)

$4.60

$16.75

$10.35 $16.00

Deliver Top Quartile Refining Performance

MPC Well Positioned for Utica Shale Options

Multiple Transportation Options Truck, barge, pipeline

Local capacity for Utica condensate ~25 MBPCD between Canton and

Catlettsburg presently

Condensate splitters at Canton and Catlettsburg Increase local capacity from ~25 to 60

MBPCD Canton start up end of 2014 Catlettsburg start up mid 2015

Additional capacity for Utica liquids at Robinson refinery Natural gasoline capacity: ~20 MBPCD Condensate capacity: ~20-25 MBPCD

20

To Robinson

MPC Refinery MPC Terminal MPC Pipeline Barge Route

Canton

Catlettsburg

Wellsville

Proposed Pipeline Harrison

Hubs

21

Distribution & Marketing

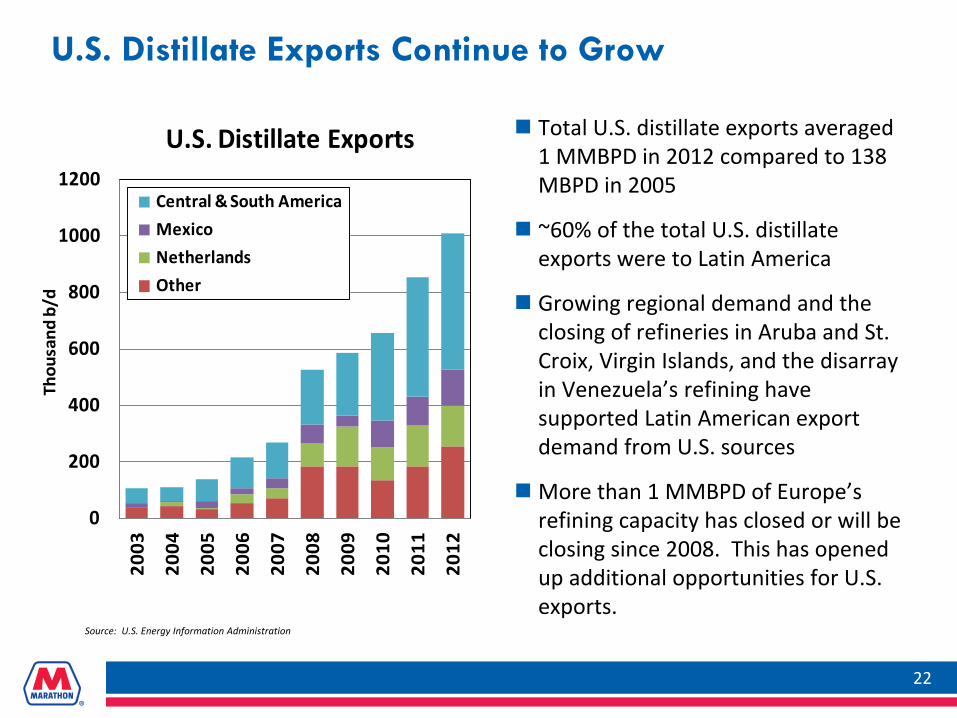

U.S. Distillate Exports Continue to Grow

Total U.S. distillate exports averaged 1 MMBPD in 2012 compared to 138 MBPD in 2005

~60% of the total U.S. distillate exports were to Latin America

Growing regional demand and the closing of refineries in Aruba and St. Croix, Virgin Islands, and the disarray in Venezuela’s refining have supported Latin American export demand from U.S. sources

More than 1 MMBPD of Europe’s refining capacity has closed or will be closing since 2008. This has opened up additional opportunities for U.S. exports.

22

Source: U.S. Energy Information Administration

0

200

400

600

800

1000

1200

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Thou

sand

b/d

U.S. Distillate Exports

Central & South AmericaMexico Netherlands Other

Diesel and Gasoline Export Success Currently selling gas and diesel

export cargos via term and spot transactions

Value added relative to domestic pipeline sales Product quality premium No RIN obligation

Optimize export logistics

23

Deliver Top Quartile Refining Performance

35 76

114 145

16

0

50

100

150

200

2010 2011 2012 2013*

MBP

D

Exports

Diesel Gas *Through 6/30/13 Note: Excludes Asphalt

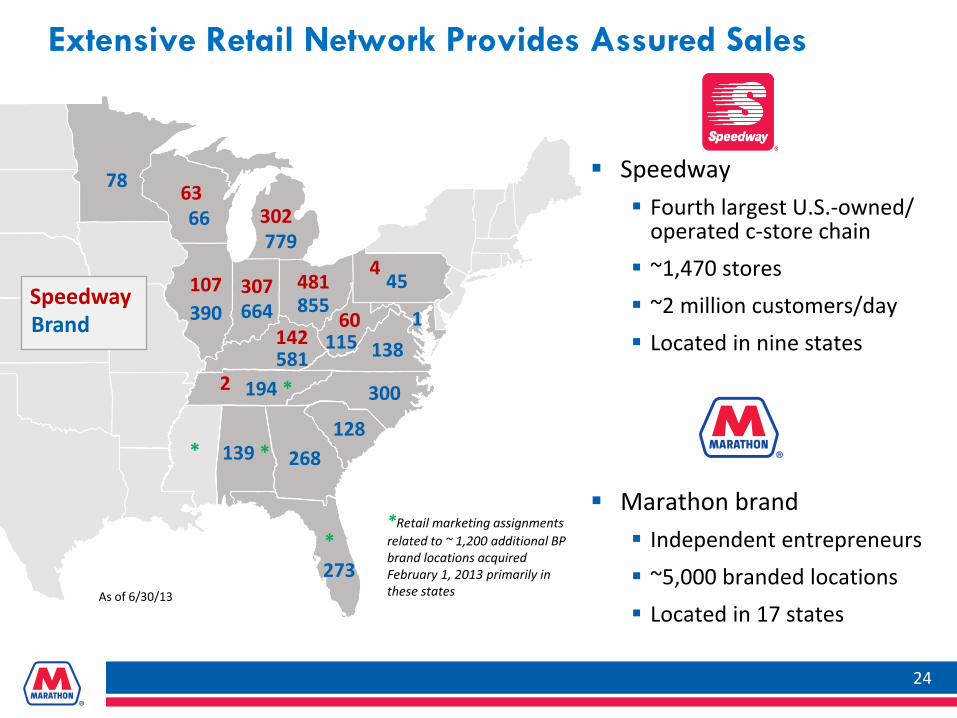

Extensive Retail Network Provides Assured Sales

24

Speedway Fourth largest U.S.-owned/

operated c-store chain ~1,470 stores ~2 million customers/day Located in nine states

Marathon brand Independent entrepreneurs ~5,000 branded locations Located in 17 states

481

302

307

142

107

63

60 855

779

664

581

390

78

66

138 115

45

268

273

300 194 *

139 * 128

1

As of 6/30/13

Speedway Brand

*Retail marketing assignments related to ~ 1,200 additional BP brand locations acquired February 1, 2013 primarily in these states

*

2

*

4

3.06

01234

2009 2010 2011 2012

$B

Merchandise Sales

Speedway Sales – Stable Merchandise Margin

25

Attributable to Minnesota assets sold on December 1, 2010

795

0200400600800

1,0001,2001,400

2009 2010 2011 2012 M

M$

Light Product and Merchandise Gross Margin

Merchandise Light Product

775 789 719

Profitable Speedway Growth

3.03

01234

2009 2010 2011 2012

B G

allo

ns

Light Product Volume

3.7 (1.2)

(Same Store % inside bars)

1.0 (0.9)

4.4 1.1 11.4 0.9

3.11 2.92 3.19

(Same Store % inside bars)

3.23 2.94 3.30

333 398 384 399

Increase Marathon Brand Assured Sales Volume

0

1,000

2,000

3,000

4,000

5,000

'98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

Mill

ions

of G

allo

ns Light Product Sales

26

Increase Speedway and Marathon Brand Assured Sales Volume

2013 Value Drivers

Growth of MPLX

Galveston Bay refinery

Detroit Heavy Oil Upgrade Project

Profitable Speedway growth

2013 $1.6 billion capital investments*

Capital return to shareholders Strong dividend, growing over the long term Continuing share repurchases – as of June 30, 2013, $1.3 billion authorization

remaining

27

Goal: Top Quartile Total Shareholder Return *Excludes purchase price of Galveston Bay refinery and related assets

Appendix

28

MPC is a Strong Strategic Sponsor for MPLX MPC is a leading independent R&M company

Enterprise value of $23.0 billion1 and LTM EBITDA generation of $6.3 billion²

2012 revenue of $82.2 billion, Fortune 50 company

Large integrated refining, marketing and logistics system Seven refineries with crude capacity of

~1.7 MMBPCD Speedway – fourth largest U.S. C-store chain

with ~1,470 locations in nine states Marathon brand – ~5,000 outlets in 17 states Significant retained midstream assets

MPC has a strong credit profile and significant liquidity Investment grade (BBB / Baa2) – stable/

positive outlook Debt / EBITDA of 0.5x1,2 and Debt / Total Capital of 22%1,3

~$6.6 billion of liquidity4

Notes: 1 313.1 MM shares outstanding at $73.33/share at 7/31/2013, $3.07 billion cash, $3.41 billion

debt at 6/30/2013 2 See Appendix for last twelve month (LTM) EBITDA reconciliation to net income as of 6/30/2013 3 Equity of $12.197 billion at 6/30/2013 4 Includes $3.07 billion cash, undrawn $2.5 billion revolver and undrawn $1 billion trade

receivables securitization facility at 6/30/2013

29

Water Terminals

Light Product Terminals

Connecting Pipelines

Refineries

Asphalt Terminals

Marketing Area

Tank Farms

Butane Caverns

Barge Dock

Source: Company Reports

MPC has Strong Earnings and Cash Flow, Investment Grade Credit Profile

$MM 6/30/13

Actual

Cash and Cash Equivalents 3,069

Total Debt 3,410

Equity 12,197

Total Capitalization 15,607

Total Debt/LTM EBITDA(2) 0.5x

Debt to Total Capital Ratio 22%

Financial Policies Committed to Investment Grade profile

Rating Current Agency MPC Rating S&P BBB/A-2 (Stable) Moody’s Baa2/P2 (Positive)

Maintain strong access to liquidity, with cash balance, 5-year revolver and access to CP markets

Maintain prudent capitalization and leverage statistics throughout the refining cycle

Capitalization

30

(1) Non-GAAP disclosure, see appendix for reconciliation to net income attributable to MPC. (2) Based on LTM EBITDA of 6,318 MM.

Non-GAAP disclosure, see appendix for reconciliation to net income attributable to MPC.

Committed to Investment Grade Credit Profile

654 1,011

3,745

5,347

1,324

1,952

4,636

6,342

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2009 2010 2011 2012

MM

$

Historical Financial Summary

Income from Operations EBITDA(1)EBITDA(1)

Executing on Commitment to Total Shareholder Return

Base dividend increased 110% since July 1, 2011

$2.66 billion share repurchases through June 30, 2013

Total shareholder return of 93% for 2012

31

Balanced Return

$3.46 B

0500

1,0001,5002,0002,5003,0003,5004,000

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

$MM

Cumulative Return of Capital

Dividends Share repurchases

31% 36%

67%

93%

0%

20%

40%

60%

80%

100%

Q1 2012 Q2 2012 Q3 2012 Q4 2012

2012 Cumulative Total Shareholder Return

Focused Return of Capital to Shareholders

$2,700

$542

$2,277

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

LTM Ended 6/30/13

Mill

ions

Dividends and sharerepurchases*

Change in cash and allother

Cash capital expendituresand acquisitions

32

*$464 MM dividends plus $1,813 MM share repurchases **Cash flow provided by operations less cash capital expenditures and acquisitions

~81% of Free Cash

Flow** Free Cash Flow** $2,819

Net cash provided by operations $5,519

38%

62%

Crude Oil Refining Capacity

PADD IIPADD III

As of 2/1/13

MPC Key Strengths

33

Balanced Operations

53% 47%

Crude Slate

Sour Crude

Sweet Crude

As of 6/30/13

~54%

~46% Assured Sales

Wholesale andOther Sales

Assured Sales of Gasoline Production (Speedway + Brand + Wholesale Contract Sales)

As of 6/30/13

Balanced and Diversified Portfolio

279 252

243

192 191 175 164 163

95 89

-50

50

150

250

350

Exxo

n

Citg

o

MPC BP

Che

vron

Val

ero

Phill

ips

Shel

l

Teso

ro

HFC

2,097 1,950

1,808 1,699

981 958 955 755 665 443

0

1,000

2,000

3,000

Val

ero

Exxo

n

Phill

ips

MPC

Shel

l

BP

Che

vron

Citg

o

Teso

ro

HFC

13.4 13.0 12.1 11.7 11.6 11.4 11.1 10.9

9.9 9.5

5.0

10.0

15.0

Che

vron

Exxo

n

HFC

Citg

o

MPC

Phill

ips

Val

ero

Shel

l

BP

Teso

ro

12 11

7 7 7 6

5 5 5

3

0

5

10

15

Val

ero

Phill

ips

Exxo

n

Teso

ro

MPC

Shel

l

BP

Che

vron

HFC

Citg

o

MPC Relative Refining Position

34

U.S. Crude Refining Capacity (1) # of U.S. Refineries (1)

Average Crude Capacity of U.S. Refineries (1)

Nelson Complexity Index (1)

(MBCD) (#)

(NCI)

(1) MPC data as of 1/1/2013 plus Galveston Bay acquisition. Other company data as reported in the O&GJ 2012 Worldwide Refining Survey, published on 12/3/2012. Owned interest of joint ventures are included in company statistics: Phillips includes 50% WRB, Exxon includes 50% Chalmette, BP includes 50% BP-Husky Toledo, Shell includes 50% Deer Park and Motiva. HollyFrontier data based on company presentations.

(MBCD)

Majors and Integrateds

MPC

Independent Refiners

Refinery Capacity

The Nelson Complexity Index is a construction cost-based measurement used to describe the investment cost of a refinery in terms of the process operations being conducted. It is basically the ratio of the process investment downstream of the crude unit to the investment of the crude unit itself. This index has many limitations as an indicator of value and is not necessarily a useful tool in predicting profitability. There is no consideration for operating, maintenance or energy efficiencies and no consideration of non-process assets such as tanks, docks, etc. Likewise it does not consider the ability to take advantage of market related feedstock opportunities.

BPCD NCI*

Garyville 522,000 10.8

Galveston Bay 451,000 15.3

Catlettsburg 240,000 10.3

Robinson 206,000 10.6

Detroit 120,000 9.9

Texas City 80,000 8.4

Canton 80,000 9.0

Total 1,699,000 11.6**

35

**Weighted Average NCI Source: MPC Data. Capacities as of January 1, 2013

*Nelson Complexity Index calculated per Oil and Gas Journal NCI Formula

U.S. Gulf Coast Offshore Imports

Domestic crude oil cannot be exported without a permit, therefore domestic crude oil must be priced to back out imports

Virtually all of the light sweet imports will be displaced in 2013

Other imports will be displaced as U.S. crude oil production increases

36

Rising North America Crude Oil Production Backs Out Waterborne Imports

Sources: DOE/EIA, MPC estimates

Positive Fundamentals

CAPP Western Canada Crude Oil Supply Forecast

37

Annual Growth from 2012 - 2030 MBD

Light Supply 17 Heavy Supply 241

8,000

7,000

6,000

5,000

4,000

3,000

MBD

0

2,000

1,000

Actual Forecast

June 2012 Forecast

Oil Sands Heavy*

Upgraded Light Conventional Heavy Conventional Light

*Oil Sands Heavy includes some volumes of upgraded heavy sour crude oil and bitumen blended with diluent or upgraded crude oil.

2010 2012 2014 2016 2020 2022 2024 2028 2026 2030 2018 2008 2006

Source: Canadian Association of Petroleum Producers (CAPP), June 2013

Growing Supply from America’s Largest Trading Partner

Positive Fundamentals Midwest Refineries’ Opportunity

38

Canada

South Dakota

Montana

North Dakota

Current North Dakota Production: ~820 MBPD 2012 Year-end: 770 MBPD

2011 Year-end: 535 MBPD 2010 Year-end: 344 MBPD 2008 Year-end: 202 MBPD

2020 North Dakota Production Forecast: Up to 1,500 MBPD

Pipeline takeaway capacity has not kept pace with growth

Rail transportation has filled the gap Current Railed Volume: ~650 MBPD

Current Loading Capacity: ~850 MBPD 2014 Projected Loading Capacity: ~970 MBPD

Bakken Production Increasing Rapidly Sources: ND Oil & Gas Div., NDPA, MPC Estimate

U.S. and Canadian Liquids Production Increases 45% from 2012 to 2025

Positive Industry Trends – Growing North American Production

“Resource plays” dominate U.S. output growth. Conventional production (Alaska, offshore, California, other legacy production) struggles to sustain output

NGL output growth is mostly associated with wet gas shale areas

U.S. liquid volume gains are concentrated in PADDs II - IV (mid-continent)

Canada oil sands account for all of its gains, concentrated in Alberta

New transportation investments will be required to move production to market

39

0.0

0.5

1.0

1.5

2.0

2.5

3.0

US Crude &Condensate

US NGL Canada Oil Sands,Crude &

Condensate

MM

BD

2000 - 2012 2012 - 2025

Sources: DOE/EIA, Canadian Association of Petroleum Producers, MPC Estimates

Texas City and Galveston Bay Refinery Opportunity

40

Eagle Ford is a very light (40+ API), sweet crude (0.2% sulfur)

Currently being piped to markets Dock facilities are in operation

and continue to increase utilization to market it as a “waterborne” crude to capture Brent/LLS pricing as opposed to WTI basis

Crude oil production rapidly expanding Currently: 700 MBPD

2012 Annual Average: 498 MBPD

2011 Annual Average: 206 MBPD

2010 Annual Average: 34 MBPD

2009 Annual Average: 3 MBPD

2015 (forecasted): 950 MBPD

Graph Source: EIA

Source: MPC Estimate

Eagle Ford Shale

Eagle Ford Production Increasing Rapidly

Portland

Cushing

Superior Clearbrook

Regina

Cromer

Montreal

Burnaby

Anacortes

Edmonton Trans

Mountain

Chicago Casper

Wood River

Patoka

Sarnia

Mustang SAX

Hardisty

Steele City

Seaway Houston Freeport

St James Houma Ho-Ho

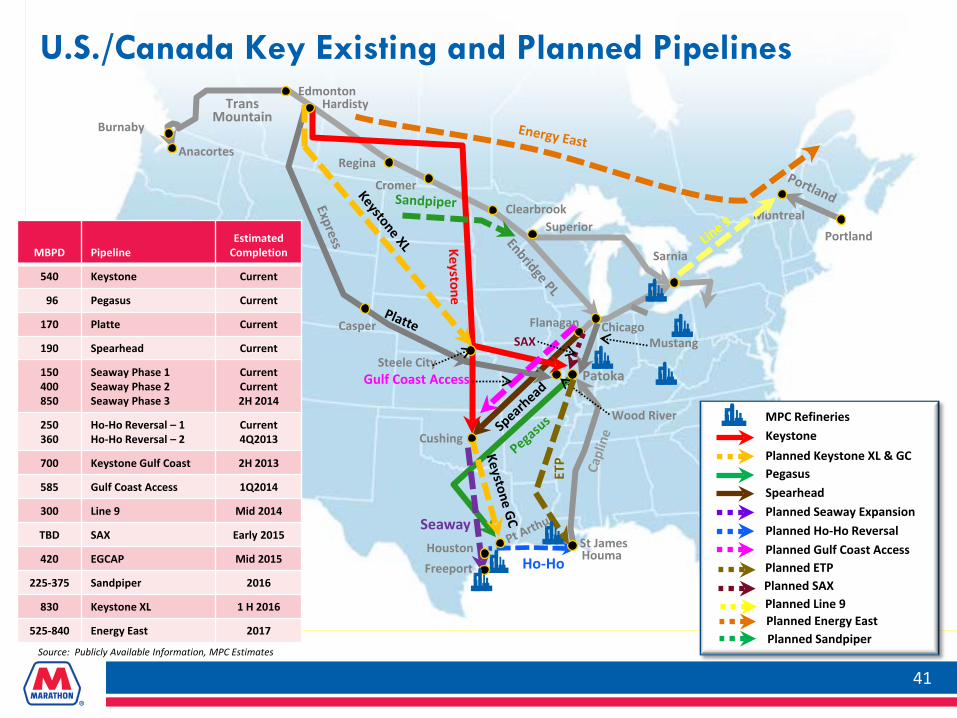

MBPD Pipeline Estimated

Completion

540 Keystone Current

96 Pegasus Current

170 Platte Current

190 Spearhead Current

150 400 850

Seaway Phase 1 Seaway Phase 2 Seaway Phase 3

Current Current 2H 2014

250 360

Ho-Ho Reversal – 1 Ho-Ho Reversal – 2

Current 4Q2013

700 Keystone Gulf Coast 2H 2013

585 Gulf Coast Access 1Q2014

300 Line 9 Mid 2014

TBD SAX Early 2015

420 EGCAP Mid 2015

225-375 Sandpiper 2016

830 Keystone XL 1 H 2016

525-840 Energy East 2017

Gulf Coast Access

Flanagan

U.S./Canada Key Existing and Planned Pipelines

41

ETP

MPC Refineries

Pegasus Planned Keystone XL & GC Keystone

Spearhead Planned Seaway Expansion Planned Ho-Ho Reversal Planned Gulf Coast Access Planned ETP Planned SAX Planned Line 9 Planned Energy East Planned Sandpiper

Source: Publicly Available Information, MPC Estimates

Indicative Transportation Costs

42

Sources: MPC Estimates based on publically available information, OPIS, and Argus Media.

Indicative Rail Costs Bakken to St. James(1) $/BBL

Railcar Loading 1.50

Rail Transportation 10.00

Railcar Lease 3.00

Railcar Unloading 1.50

Total 16.00

Indicative Rail Costs Bakken to U.S. East Coast(1) $/BBL

Railcar Loading 1.50

Rail Transportation 9.00

Railcar Lease 3.00

Railcar Unloading 1.50

Barge Loading .75

Barge Transportation 1.00

Total 16.75

Indicative Shipping Costs S. Texas to U.S. East Coast $/BBL

Pipeline to Houston 1.50

Shipping Transportation 8.85

Total 10.35

Indicative Pipeline Costs Bakken to Patoka(1) $/BBL

Pipeline to Patoka 3.60

*Pipeline to MPC Refineries 1.00

Total 4.60

*Up to $1.00 additional tariff to deliver to a MPC Midwest refinery

Bakken

St. James

Patoka

Eagle Ford

(1) Excludes gathering and truck transportation costs (up to ~$5.25/BBL)

Options… Detroit Logistics

Canadian crude via multiple routes

Virtually all world crudes available via pipelines from USGC

All gasoline production sold in regional market

43

Detroit

Enbridge 2 Enbridge

Capline

Patoka

Mid Valley

Lima

Wood River

Chicago

Stockbridge

Samaria

#1 #2

#3 Platte/Keystone

#4 #5

Strategically Located for Multiple Crude Supply Routes

Attractive Midwest/PADD II

Demand exceeds refining capacity in PADD II Net imported ~13% of petroleum

demand into PADD II, primarily from PADD III in 2012 Enhances margin opportunities Transportation premium embedded

in PADD II gasoline prices Higher refinery utilization rates Relatively leaner product stocks

Access to Canadian crude

Well positioned for Utica crude

44

7% 21%

50%

4% 18%

38%

62%

0%

20%

40%

60%

80%

PADD I PADD II PADD III PADD IV PADD VIndustry Distribution MPC

Percentage of Crude Oil Capacity by PADD

Source: MPC Estimate

Largest Midwest Exposure of All Major Refining Competitors

Sources: MPC, DOE, as of 2/1/2013

PADD I PADD II

PADD III

PADD V

PADD IV

Fully Integrated Downstream Business

Ratable sales

Optimized operations Refining Pipeline Terminal

Biofuels blending base load

Supply dislocation flexibility

Reduced credit risk (Speedway)

45

Coastal Water Terminals

Inland Water Terminals

Light Product Terminals

Connecting Pipelines Refineries Speedway Marketing Area

Capturing Value MPC Well Positioned – Benefits of Retail Integration

Speedway vs. Public Peers – 2012

46

177.1

0

50

100

150

200

250

300

Casey's Couche-Tard Pantry Susser Speedway Valero Murphy Tesoro Delek WesternRefining

M G

al/S

tore

/Mon

th

Light Product Sales

Average 103.5

Average 146.9

31.2

05

10152025303540

Casey's Couche-Tard Pantry Susser Speedway Valero Murphy Tesoro Delek WesternRefining

$M/S

tore

/Mon

th

Light Product Margin

Public C-Store

Independent Refiners

Public C-Store

Independent Refiners

Average 14.7

Average 23.7

#2 in Light Product Unit Sales Volume Source: Company Reports

Speedway vs. Public Peers – 2012

47

174.7

0

50

100

150

200

Casey's Couche-Tard Pantry Susser Speedway Valero Murphy Tesoro Delek WesternRefining

$M/S

tore

/Mon

th

Merchandise Sales

Average 115.7 Average 93.5

45.5

0

10

20

30

40

50

60

Casey's Couche-Tard Pantry Susser Speedway Valero Murphy Tesoro Delek WesternRefining

$M/S

tore

/Mon

th

Merchandise Margin

Public C-Store Independent Refiners

Public C-Store

Independent Refiners Average 40.6

Average 22.2

#1 in Merchandise Unit Sales Source: Company Reports

48

0

10

20

30

40

50

60

2000 2005 2010 2015 2020 2025

Mile

s Per

Gal

lon

Adjusted On-road New Autos (Model Year) New Automobiles (Model Year)

Adjusted On-road New Light Trucks (Model Year) New Light Trucks (Model Year)

Adjusted Total On-road Vehicle Fleet

Gasoline Vehicle Fuel Efficiencies

Sources: DOT, MPC Economics

2013 Significant Capital Projects

Upgrade Galveston Bay refinery

Speedway expansion

Garyville diesel projects

Utica Shale projects Condensate splitters Wellsville terminal

Patoka to Catlettsburg pipeline upgrade

Robinson unicracker revamp

Garyville gasoline and diesel export

Catlettsburg vacuum cut-point project

49

Market Indicators Used in Project EBITDA Calculations

2011 2006 - 2010 West Texas Intermediate 3-2-1 crack spread 23.31 10.68 Light Louisiana Sweet 3-2-1 crack spread 6.05 8.05 Arab Light 3-2-1 crack spread 11.16 14.03 Arab Medium 4-2-1-1 crack spread 7.71 9.54 Light Louisiana Sweet 6-3-2-1 crack spread 2.79 3.91 LLS to Lloyd Differential 33.98 20.16

50

Annual Price and Margin Sensitivities $ Millions (After Tax)

51

LLS 6-3-2-1 Crack Spread* Sensitivity ~$425 (per $1.00/barrel change) Sweet/Sour Differential** Sensitivity ~$225 (per $1.00/barrel change) LLS-WTI Spread*** Sensitivity ~$75 (per $1.00/barrel change) Refined Product Wholesale Margin Sensitivity ~$200

(per $0.01/gallon change) Speedway Refined Product Margin Sensitivity ~$20

(per $0.01/gallon change) Natural Gas Price Sensitivity ~140 (per $1.00/MMbtu change in Henry Hub)

*Weighted 38% Chicago and 62% USGC LLS 6-3-2-1 crack spreads and assumes all other differentials and pricing relationships remain unchanged

**Light Louisiana Sweet (prompt) - [Delivered cost of sour crudes: Arab Light + Kuwait + Maya + Western Canadian Select + Mars]

***Assumes 20% of crude throughput volumes are WTI-based domestic crudes

Galveston Bay Complements MPC’s Integrated System

52

Refinery 451,000 BPCD (475,000 BPSD) refinery Nelson Complexity Index: 15.3 Significant recent investments Excellent crude optionality Substantial products logistics opportunities Advantageous petrochemical configuration

Cogen Facility 1040 megawatts of electrical capacity and 4.6 million

lbs/hr steam Supplies power and steam to the refinery

Light Product Terminals Nashville, TN Charlotte, NC Selma, NC Jacksonville, FL

Pipelines More than 100 miles of NGL pipelines consisting of

three intrastate systems originating at the refinery 50 MBPD gasoline shipper history on Colonial Pipeline

Retail Assignments ~61 MBPD of BP brand gasoline contracts ~1,200 locations

Connecting Pipelines

MPC Operations

Refinery Terminal Coastal Water Terminal

Inland Water Terminal

Refinery and Cogen

Light Product Terminals

Primary Retail Assignment Region

As of Feb. 1, 2013

Galveston Bay Asset Acquisition Projected Synergies and Capital Investments (Millions)

EBITDA Synergies of ~$440 MM thru 2017, ~$130 MM annually thereafter

Feedstock optimization

Florida and export optimization

Refinery processing opportunities

Total Synergy Investments of ~$170 MM

Dock upgrades

Storage tank additions and connectivity

53

Projected Synergy Capital Investments

$0

$40

$80

$120

$160

2013E 2014E 2015E 2016E

Projected Incremental Synergies EBITDA

$0

$40

$80

$120

$160

2013E 2014E 2015E 2016E 2017E+

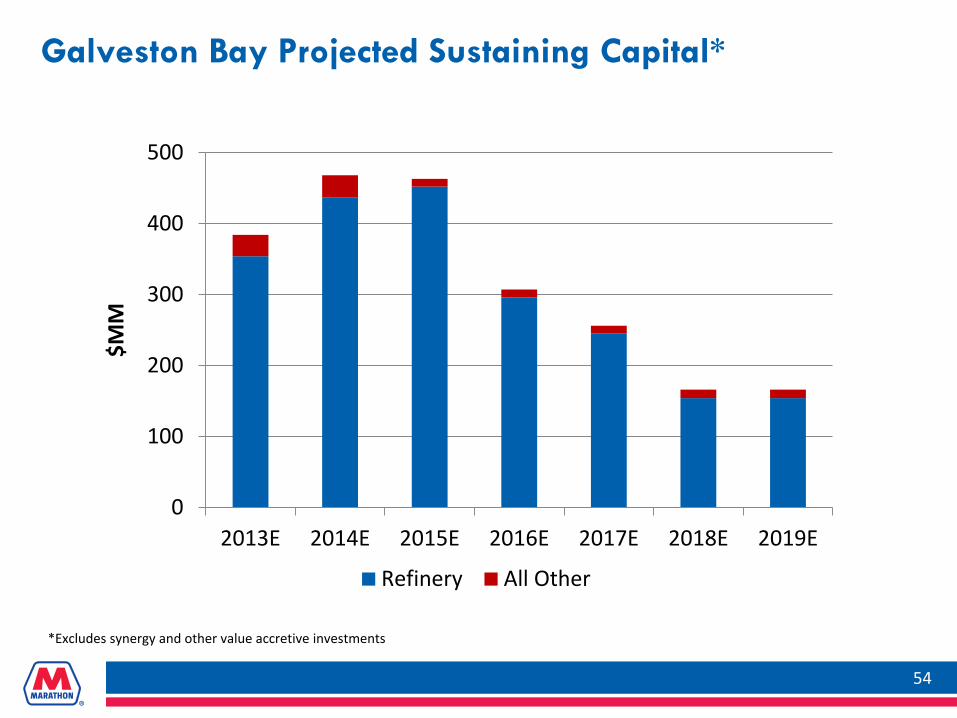

Enhancing Earnings

Galveston Bay Projected Sustaining Capital*

54

0

100

200

300

400

500

2013E 2014E 2015E 2016E 2017E 2018E 2019E

$MM

Refinery All Other

*Excludes synergy and other value accretive investments

Galveston Bay Transaction Product Logistics Opportunities

55 55 55

Exports to Mexico/SA/Europe

Pasadena Zachary

Southeast Midwest

Florida

Flexible product placement

Domestic and export opportunities

Synergies with MPC’s Texas City and Garyville refineries and MPC logistics

Garyville

Texas City

Galveston Bay Marketing Assets and Integration

Integrated acquisition includes Assignment of branded-jobber contracts

representing ~1,200 BP retail sites ~61 MBPD of gasoline sales Locations primarily in FL, MS, TN and AL BP trademark to be used during

transition process

Strategic step in retail growth Nearly doubles branded site count in

Southeast Complementary to recent regional

growth Partnership opportunity with premier

Southeast jobbers Opportunity to expand relationship with

existing Marathon jobbers

56

Galveston Bay Assets Expected Accretive Transaction (MM unless otherwise indicated)

57

MPC Base EBITDA - analyst 2013 consensus estimates(1) $ 4,759 $ 4,759 Assets acquired EBITDA using 2006-2010 pricing(2)(4) 1,200 Assets acquired EBITDA using 2011 pricing(2)(5) 700 Total EBITDA $ 5,959 $ 5,459

Improvement 25% 15%

MPC Base Net Income - analyst 2013 consensus estimates $ 2,425 $ 2,425 Assets acquired Net Income using 2006-2010 pricing(2)(4) 650 Assets acquired Net Income using 2011 pricing(2)(5) 325

Total Net Income $ 3,075 $ 2,750

MPC Base EPS(3) $7.11 $7.11 MPC + Assets acquired EPS(3) $9.02 $8.06

Accretion 27% 13%

(1) Consensus estimates as of October 4, 2012 (2) Based on MPC 2013 operating estimates and applicable historical price information (3) Assumes 341 million shares outstanding (4) Argus Sour Crude Price Index (ASCI) 3-2-1 crack spread of $15.10 used as pricing metric for 2006-2010 (5) ASCI crack spread of $11.57 used as pricing metric for 2011

MPC 2Q 2013 Earnings*

Adjusted Earnings Adjusted Earnings per Diluted Share

1.70 2.17

2.53 1.95

3.31

2.26

$0$2$4$6$8

$10$12

2012 2013

$/Sh

are

58

2Q 2013 2Q 2012

Earnings $593 MM $814 MM

Adjusted Earnings $632 MM $867 MM

Earnings per Diluted Share $1.83 $2.38

Adjusted Earnings per Diluted Share $1.95 $2.53

596 725

867 632

1,129

760

$0

$1,000

$2,000

$3,000

$4,000

2012 2013

Mill

ions

1Q 2Q 3Q 4Q *References to Earnings refer to Net Income attributable to MPC

3,352 9.79

Adjusted Earnings* 2Q 2013 vs. 2Q 2012 Variance Analysis

59

867 (422)

16 8

169 (6) 632

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

2Q 2012 Refining &Marketing

Speedway PipelineTransportation

IncomeTaxes

NoncontrollingInterests

2Q 2013

Mill

ions

*References to Earnings refer to Net Income attributable to MPC

Refining & Marketing Segment Income 2Q 2013 vs. 2Q 2012 Variance Analysis

60

1,325 (313)

640 (117) (101) (117)

(6) (381)

(27) 903

$0

$500

$1,000

$1,500

$2,000

$2,500

2Q 2012 *LLS6-3-2-1Crack

*Sweet/Sour Diff.

*LLS /WTISpread

*LLSPrompt vs.Delivered

*MarketStructure

DirectOperating

Costs

OtherGross

Margin

Other 2Q 2013

Mill

ions

*Based on market indicators using actual volumes

Speedway Segment Income 2Q 2013 vs. 2Q 2012 Variance Analysis

61

107

12 9 (5)

123

$0

$20

$40

$60

$80

$100

$120

$140

2Q 2012 Light Product GrossMargin

Merchandise GrossMargin

Other 2Q 2013

Mill

ions

Pipeline Transportation Segment Income 2Q 2013 vs. 2Q 2012 Variance Analysis

62

50

28 (6) (14)

58

$0

$20

$40

$60

$80

2Q 2012 Trans.Revenue

Depreciation OperatingExpenses

2Q 2013

Mill

ions

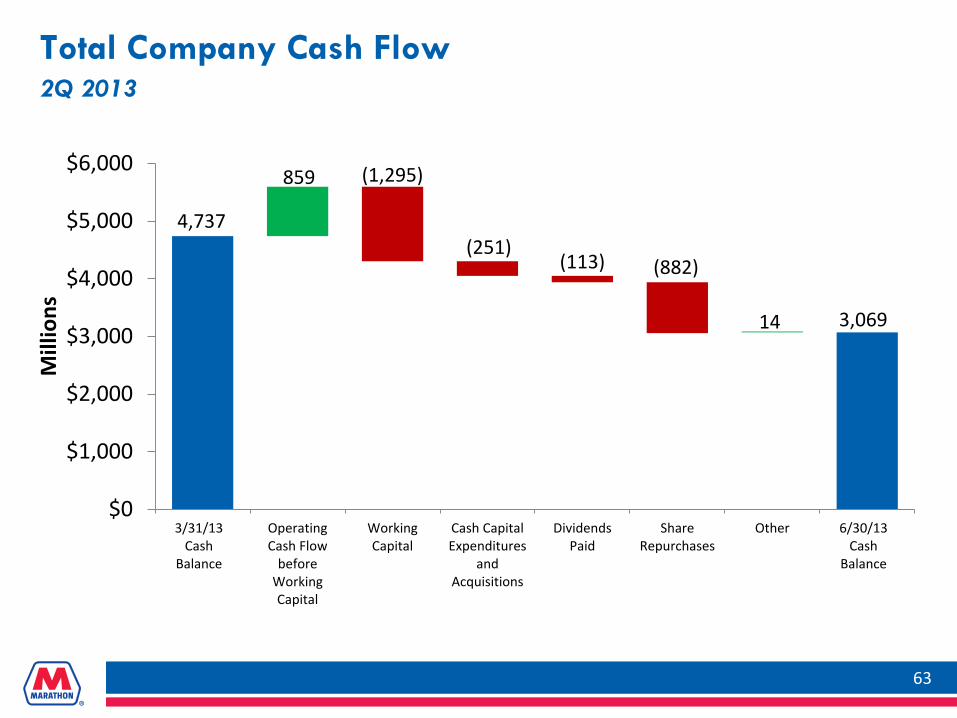

Total Company Cash Flow 2Q 2013

63

4,737

859 (1,295)

(251) (113) (882)

14 3,069

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

3/31/13Cash

Balance

OperatingCash Flow

beforeWorkingCapital

WorkingCapital

Cash CapitalExpenditures

andAcquisitions

DividendsPaid

ShareRepurchases

Other 6/30/13Cash

Balance

Mill

ions

Select Balance Sheet/Cash Flow Data

($MM) 2013 2013 2012 2012 2Q 1Q 4Q 3Q

As of quarter ended:

Cash and cash equivalents 3,069 4,737 4,860 3,387

Total debt 3,410 3,416 3,361 3,349

Equity 12,197 12,412 12,105 11,467

Debt-to-total-capital ratio 22% 22% 22% 23%

Last Twelve Months (LTM) EBITDA 6,318 6,599 6,342 4,942

Debt to LTM EBITDA 0.5x 0.5x 0.5x 0.7x

Quarter to date:

Cash provided by (used in) operations (436) 2,079 2,043 1,833

Cash provided by operations before changes in working capital 859 1,046 1,124 1,320

64

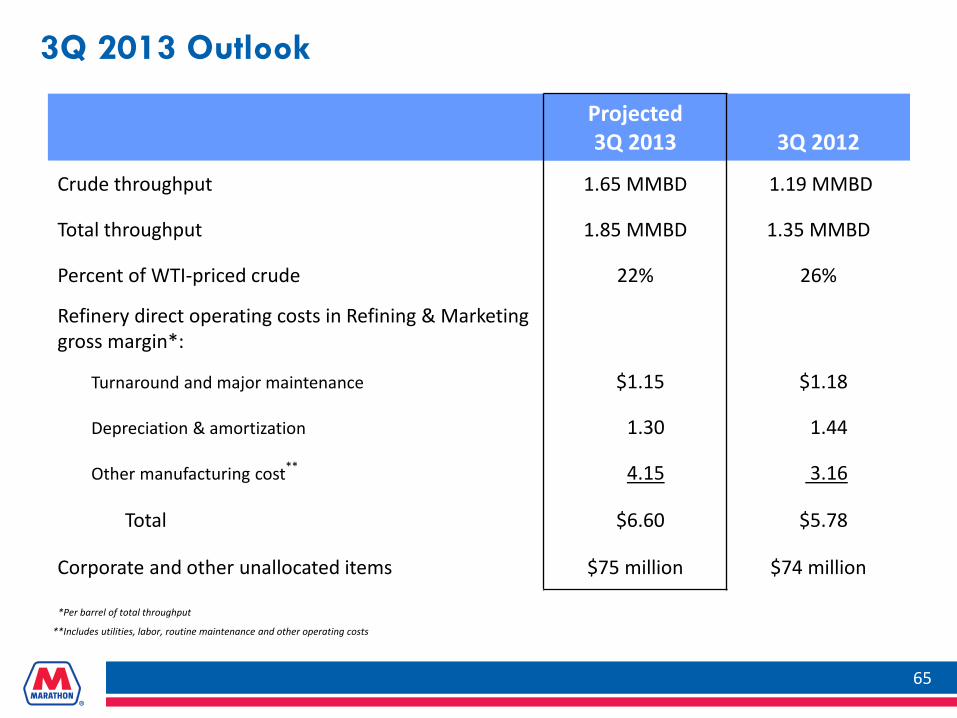

3Q 2013 Outlook

Projected 3Q 2013

3Q 2012

Crude throughput 1.65 MMBD 1.19 MMBD

Total throughput 1.85 MMBD 1.35 MMBD

Percent of WTI-priced crude 22% 26%

Refinery direct operating costs in Refining & Marketing gross margin*:

Turnaround and major maintenance $1.15 $1.18

Depreciation & amortization 1.30 1.44

Other manufacturing cost** 4.15 3.16

Total $6.60 $5.78

Corporate and other unallocated items $75 million $74 million

65

*Per barrel of total throughput

**Includes utilities, labor, routine maintenance and other operating costs

Reconciliation Earnings to Adjusted Earnings*

66

($MM) 2012 2013

1Q 2Q 3Q 4Q 1Q 2Q

Earnings 596 814 1,224 755 725 593

Pension settlement expenses** 53 22 5 39

MN asset sale settlement gain** (117)

Adjusted Earnings 596 867 1,129 760 725 632

*References to Earnings refer to Net Income attributable to MPC **Net of tax

Reconciliation

67

($MM) 2012 2013 (Quarter to date) 3Q 4Q 1Q 2Q

Net cash provided by (used in) operating activities 1,833 2,043 2,079 (436)

Additions to property, plant and equipment (331) (403) (195) (229)

Acquisitions* (27) - (1,493) (22)

Free cash flow 1,475 1,640 391 (687)

Last twelve months free cash flow 2,819

Free Cash Flow to Net Cash Provided from Operations

*Represents cash paid

Income

68

($MM unless otherwise noted) 2012 2013 1Q 2Q 3Q 4Q 1Q 2Q

Refining & Marketing segment income

Speedway segment income

Pipeline Transportation segment income

943

50

42

1,325

107

50

1,691

76

52

1,139

77

72

1,105

67

51

903

123

58

Corporate and other unallocated items (79) (92) (74) (91) (67) (64)

Pension settlement expenses - (83) (33) (8) - (60)

MN asset sale settlement gain - - 183 - - -

Income from operations 956

(22)

1,307

(17)

1,895

(25)

1,189

(45)

1,156

(48)

960

(45) Net interest and other financing income (costs)

Income before income taxes 934 1,290 1,870 1,144 1,108 915

Income tax provision 338 476 646 385 378 316

Net income 596 814 1,224 759 730 599

Less net income attributable to noncontrolling interests - - - 4 5 6

Net income attributable to MPC 596 814 1,224 755 725 593

Effective tax rate 36% 37% 35% 34% 34% 35%

EBITDA Reconciliation to Net Income (Loss) Attributable to MPC

69

($MM) 2009 2010 2011 2012 2013

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q Net Income (Loss) attributable to MPC 449 623 529 802 1,133 (75) 596 814 1,224 755 725 593

Less: Related party net interest and other financial income 45 24 17 18 - - - - 1 - - -

Less: Net interest and other financial income (costs) (14) (12) (14) (10) (15) (22) (22) (17) (26) (45) (48) (45)

Add: Net income attributable to noncontrolling interest - - - - - - - - - 4 5 6

Add: Provision (benefit) for income taxes 236 400 293 531 611 (105) 338 476 646 385 378 316

Add: Depreciation and amortization 670 941 216 218 227 230 230 236 246 283 287 302

EBITDA 1,324 1,952 1,035 1,543 1,986 72 1,186 1,543 2,141 1,472 1,443 1,262

Last Twelve Months EBITDA 4,636 4,787 4,787 4,942 6,342 6,599 6,318

Cash Provided from Operations Before Changes in Working Capital Reconciliation to Cash Provided by (Used in) Operations

70

($MM) 2012 2013

(Quarter to date) 3Q 4Q 1Q 2Q

Net cash provided by (used in) operations 1,833 2,043 2,079 (436)

Less changes in working capital:

Changes in current receivables (393) 491 (884) (655)

Changes in inventories 142 440 (517) 62

Changes in current accounts payable and accrued liabilities 862 (63) 2,491 (702)

Changes in the fair value of derivative instruments (98) 51 (57) --

Total changes in working capital 513 919 1,033 (1,295)

Cash provided from operations before changes in working capital 1,320 1,124 1,046 859

Capital Expenditures & Investments*

71

($MM) 2013 Budget 2Q 2013 2013 YTD

Refining & Marketing 1,016 134 257

Speedway 255 76 112

Pipeline Transportation 184 41 61

Corporate and Other 160 28 52

Subtotal 1,615 279 482

Capitalized Interest 43 4 8

Total Capital Expenditures & Investments 1,658 283 490

*Excludes $1.37 billion in capital expenditures and investments attributable to the acquisition of the Galveston Bay refinery and related assets

MPC Crude Slate

72

21 23 25 26 27 29 30 28 26 25 22 22

48 56 52 52 49 48 45 50 52 55

52 48

31 21 23 22 24 23 25 22 22 20 26 30

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

Other Sweet

Other Sour

WTI Based

Refining & Marketing Indicative Gross Margin – 2Q 2013

73 *Based on market indicators using actual volumes

1,671

506

364 (179) 43 (1,030)

(180) 1,195 (292)

903

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

*LLS6-3-2-1Crack

*Sweet/Sour Diff.

*LLS/WTISpread

*LLSPrompt vs.Delivered

*MarketStructure

DirectOperating

Costs

OtherGross

Margin

R&MGross

Margin

Other R&MSegmentIncome

Mill

ions

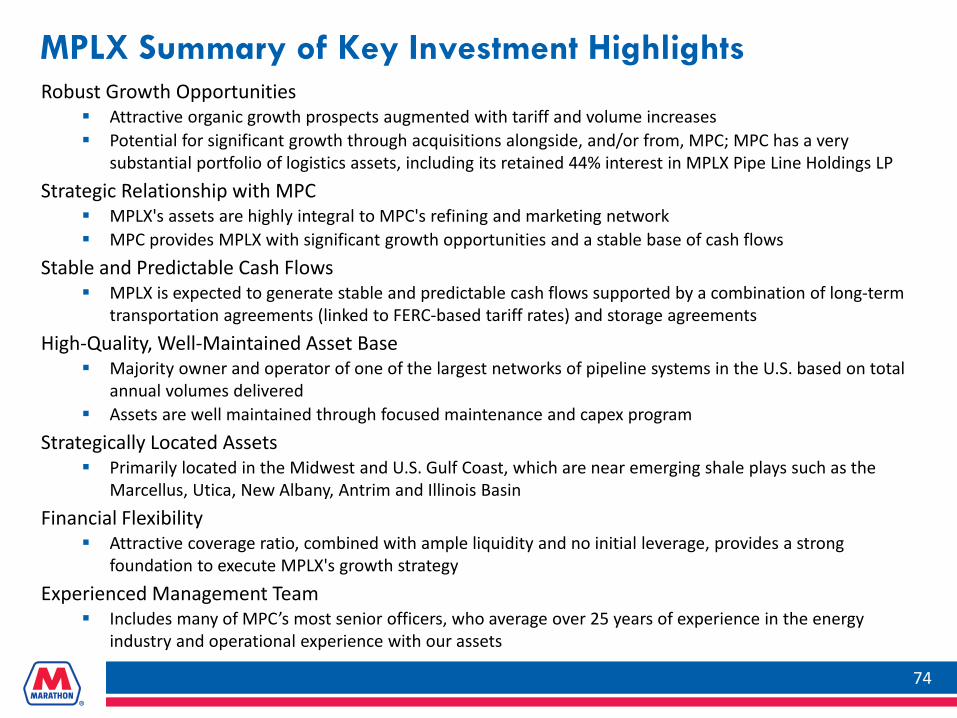

Robust Growth Opportunities Attractive organic growth prospects augmented with tariff and volume increases Potential for significant growth through acquisitions alongside, and/or from, MPC; MPC has a very

substantial portfolio of logistics assets, including its retained 44% interest in MPLX Pipe Line Holdings LP Strategic Relationship with MPC

MPLX's assets are highly integral to MPC's refining and marketing network MPC provides MPLX with significant growth opportunities and a stable base of cash flows

Stable and Predictable Cash Flows MPLX is expected to generate stable and predictable cash flows supported by a combination of long-term

transportation agreements (linked to FERC-based tariff rates) and storage agreements High-Quality, Well-Maintained Asset Base

Majority owner and operator of one of the largest networks of pipeline systems in the U.S. based on total annual volumes delivered

Assets are well maintained through focused maintenance and capex program Strategically Located Assets

Primarily located in the Midwest and U.S. Gulf Coast, which are near emerging shale plays such as the Marcellus, Utica, New Albany, Antrim and Illinois Basin

Financial Flexibility Attractive coverage ratio, combined with ample liquidity and no initial leverage, provides a strong

foundation to execute MPLX's growth strategy Experienced Management Team

Includes many of MPC’s most senior officers, who average over 25 years of experience in the energy industry and operational experience with our assets

MPLX Summary of Key Investment Highlights

74

MPLX Offering Summary

75

Issuer MPLX LP

Sponsor Marathon Petroleum Corporation

Exchange / Ticker NYSE / MPLX

Estimated Distribution Coverage 1.10x

Expected Tax Shield 80% for the period from the IPO until December 31, 2015

Use of Net Proceeds

$203 million to MPC $192 million to pre-fund certain expansion capital expenditures $10 million to MPLX for general partnership needs $33 million for underwriting discounts, financing costs and other

formation costs

Initial Offering Upsized Final Offering

Common Units Offered (with shoe) 15.0 million (17.3 million) 17.3 million (19.9 million)

Proposed Valuation Range Yield based on $1.05 annualized MQD

$19.00 - $21.00 per unit 5.00% - 5.53%

$22.00 per unit 4.77%

Offering Size (Base Offering Before Overallotment) $285 – $315 million $381 million

Offering Size (After Overallotment Exercised) $328 – $362 million $438 million

Creating Value

MPC has Created an Industry-Leading MLP

76

Focus on Fee-Based Businesses

Generate stable cash flows by providing primarily fee-based midstream services to MPC and third parties

Mitigate volatility in cash flows by entering into long-term transportation and storage agreements and by minimizing direct exposure to commodity prices

Pursue Organic Growth Opportunities

Increase pipeline systems revenue by developing organic investment opportunities through growth in: MPC’s operations Third-party activity

Grow Through Acquisitions and

Drop-downs

Acquire complementary assets from third parties, within current geographic footprint, as well as new areas

May also pursue acquisitions cooperatively with MPC

Significant drop-down potential from MPC

Maintain Safe and Reliable Operations

Provide safe, reliable and efficient services – another key to stable cash flows

Committed to maintaining and improving the reliability and efficiency of operations

MPLX’s Primary Business Strategies

Creating Value

MPC views MPLX as integral to its operations and is aligned with its success and incentivized to grow MPLX

MPLX assets consist of a 56% interest in Pipe Line Holdings as well as 100% ownership in the Neal, W.Va., Butane Cavern

MPC retains the remaining 44% interest in Pipe Line Holdings

MPC also owns 71.6% LP interest and 100.0% of MPLX’s GP interest and IDRs

44.0% limited partner interest

100.0% ownership interest

100.0% ownership interest

MPLX Operations LLC

r

MPLX Terminal and Storage LLC

100.0% ownership interest Public

100.0% ownership interest

2.0% GP interest 26.4% LP interest

Marathon Pipe Line LLC (“MPL”)

56.0% GP interest

Ohio River Pipe Line LLC (“ORPL”)

MPLX GP LLC (our General Partner)

71.6% LP interest

100.0% ownership interest

MPLX LP (NYSE: MPLX)

(the “Partnership”)

MPLX Pipe Line Holdings LP (“Pipe Line Holdings”)

Marathon Petroleum Corporation and Affiliates

(NYSE: MPC)

MPLX Organizational Structure*

MPC and MPLX are Aligned

77

*As of May 1, 2013

Marathon Pipe Line LLC and Ohio River Pipe Line LLC comprise one of the largest networks of pipeline systems in the U.S. based on total volume delivered 1,004 miles of common carrier

crude oil pipelines 1,902 miles of common carrier

products pipelines Inclusive of 230 miles of long-

term leased and operated pipelines

The ~1 million barrel Neal, W.Va., butane storage cavern adjacent to MPC’s Catlettsburg refinery is wholly owned and operated by MPLX

MPLX’s Assets are Integral to MPC

78

As of Feb. 1, 2013

Owned and operated terminals: 65 light product and 20 asphalt 271 transport loading racks

Logistics infrastructure is extremely important to MPC's success.

MPC intends to use MPLX as the primary growth vehicle for its midstream logistics business.

MPLX can pursue acquisitions directly from MPC.

MPLX can pursue third-party acquisitions independently and/or in cooperation with MPC.

MPC Midstream Assets

Remaining 44% interest in MPLX's pipeline assets Over 5,000 miles of additional crude and products pipelines

Owns, leases or has an ownership interest in these pipelines

146 owned transport trucks ~ 1,970 owned or leased railcars

One of the largest private inland bulk liquid barge fleets in the U.S. consisting of 15 owned inland waterway towboats, and 177 owned and 14 leased barges

MPC Relationship Provides Robust Growth Opportunities for MPLX

79

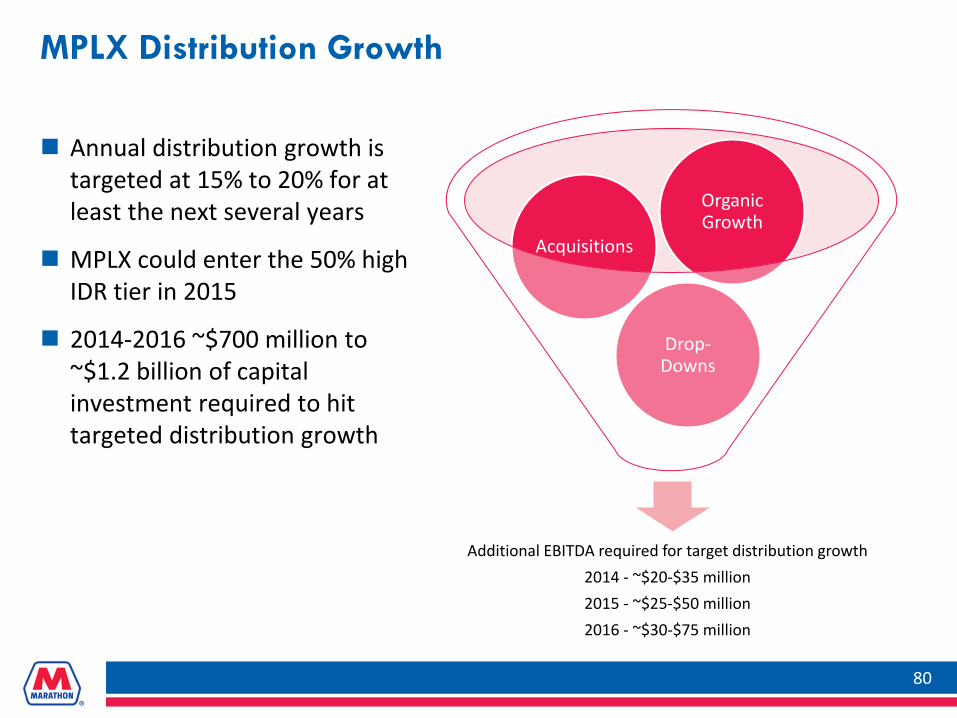

Annual distribution growth is targeted at 15% to 20% for at least the next several years

MPLX could enter the 50% high IDR tier in 2015

2014-2016 ~$700 million to ~$1.2 billion of capital investment required to hit targeted distribution growth

80

MPLX Distribution Growth

Additional EBITDA required for target distribution growth 2014 - ~$20-$35 million 2015 - ~$25-$50 million 2016 - ~$30-$75 million

Drop-Downs

Acquisitions

Organic Growth

MPLX’s assets consist of fee-based pipeline systems and storage assets

MPC has historically accounted for over 85% of the volumes shipped on MPLX’s pipelines

MPC has entered into multiple long-term transportation and storage agreements with MPLX Terms of up to 10 years Pipeline tariffs linked to FERC-based rates Indexed storage fees

2013 EBITDA estimate represents a ~60% increase over 2011 pro forma EBITDA Increase underpinned by FERC-based tariffs

and volume growth Capital projects pre-funded and supported

by MPC

Revenue – Product / Asset Mix1

Notes: 1 Estimate for the twelve months ending December 31, 2013 from Prospectus dated October 25, 2012 2 Includes revenues generated under Transportation and Storage agreements with MPC 3 Volumes shipped under joint tariff agreements are accounted for as third party for GAAP purposes, but represent MPC barrels shipped

Revenue – Customer Mix1

MPC = 89%

MPLX Stable and Predictable Cash Flows

81

73%

16%

11%

MPC Committed² ³ MPC Additional³ Third Party

$364 MM

$81 MM

$55 MM

46%

43%

4% 3%

4%

Crude Transportation Products Transportation Tank Storage Cavern Storage Operating and Mgmt. Fees

$232 MM

$216 MM

Historical crude and product volumes have been extremely stable with low variability despite material changes in the broader commodity price environment.

Butane cavern and storage facilities generate stable and ratable (capacity based) fees.

Throughput and storage agreements with MPC provide cash flow visibility and predictability.

Throughput (MBPD)

Crude Products % MPC 82% 85% 83% 82% 79% % MPC 91% 90% 93% 94%

MPC Throughput Third-party Throughput

MPLX - Ideal Assets for an MLP

82

873 856 904 971 909 899

960 953 968 1,031 980

0

200

400

600

800

1,000

1,200

2008 2009 2010 2011 2012 6 Mo YTD2013

939

697 676 732 811 827 853

850 798

883 993 1,029

0

200

400

600

800

1,000

1,200

2008 2009 2010 2011 2012 6 Mo YTD2013

1,075

80% 93% 96%

Source: MPC

Assets are primarily located throughout the Midwest and U.S. Gulf Coast

In 2011, these regions collectively comprised ~70% of total U.S. crude distillation capacity and ~50% of finished products demand

Existing and new capability to transport Canadian crude

Marathon Petroleum Corporation 646

BP2 468

Phillips 663 346

Flint Hills Resources (Koch) 304

Valero 287

HollyFrontier 258

ExxonMobil 238

Husky Energy2 238

Notes: 1 Refiners with PADD II capacities of less than 200 MBPCD excluded from list; aggregate additional

capacity of ~955 MBPCD 2 Includes 50% share of BP / Husky Toledo’s total capacity 3 Includes 50% share of Wood River’s total capacity

*Source: Oil & Gas Journal as of 1/1/2013

PADD II Refining Capacity* (MBPCD)1

MPC has the Largest Refining Capacity in PADD II

MPLX Strategically Located Assets

83

MPC Refineries

Pegasus Planned Keystone XL & GC Keystone

Spearhead Planned Seaway Expansion Planned Ho-Ho Reversal Planned Gulf Coast Access Planned ETP Planned SAX Planned Line 9 Reversal

Source: MPC

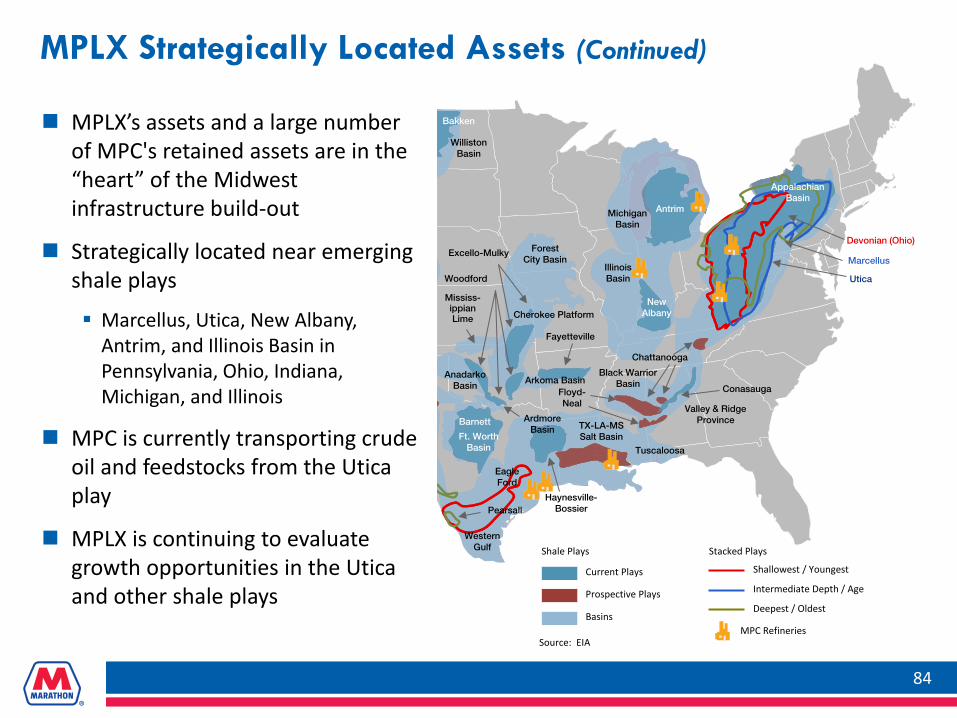

MPLX’s assets and a large number of MPC's retained assets are in the “heart” of the Midwest infrastructure build-out

Strategically located near emerging shale plays

Marcellus, Utica, New Albany, Antrim, and Illinois Basin in Pennsylvania, Ohio, Indiana, Michigan, and Illinois

MPC is currently transporting crude oil and feedstocks from the Utica play

MPLX is continuing to evaluate growth opportunities in the Utica and other shale plays

Source: EIA

Current Plays

Prospective Plays

Basins

Shale Plays

Shallowest / Youngest

Intermediate Depth / Age

Deepest / Oldest

Stacked Plays

MPC Refineries

MPLX Strategically Located Assets (Continued)

84

Bakken

Ardmore Basin

Anadarko Basin

Barnett

Pearsall

Eagle Ford

Haynesville- Bossier

Ft. Worth Basin

TX-LA-MS Salt Basin

Tuscaloosa

Floyd-Neal

Woodford

Arkoma Basin

Fayetteville

Cherokee Platform

Excello-Mulky

Williston Basin

Forest City Basin

Illinois Basin

Michigan Basin

Antrim

Appalachian Basin

New Albany

Chattanooga

Black Warrior Basin Conasauga

Valley & Ridge Province

Devonian (Ohio)

Marcellus

Utica

Western Gulf

Mississ- ippian Lime

MPLX continually invests in the maintenance and integrity of its assets

Uses a patented integrity management program to enhance pipeline safety and reliability

Top-tier reputation and active industry involvement

2013 Capex Budget1, 2 Certifications, Initiatives and Industry Partnerships

Note: 1 Capex budget represents both MPC and MPLX portions of capital budget 2 Excludes $100 million acquisition of additional 5% interest in MPLX Pipe Line Holdings LP

Quality Assets and Top-tier Reputation

(16% of 2013E EBITDA) (16% of 2013E EBITDA)

MPLX High-Quality, Well-Maintained Asset Base

85

Expansion $109 MM

Maintenance $33 MM

(~17% of 2013E EBITDA)

MPLX Operations Deliver Top Tier Safety Performance Patented integrity

management program fully compliant with DOT regulations

State of the art in-line assessment practices

Leading control room management practices

Industry leader in helping to improve Damage Prevention practices

86

MPLX Financial Performance

87

$ in millions $ / unit

Distribution Coverage 1.37x 1.25x

$18.2

$25.1 $26.7

4Q'12 1Q'13 2Q'13

Adjusted EBITDA*

$0.2625**

$0.2725

$0.2850

4Q'12 1Q'13 2Q'13

Distribution / Unit*

3.8% Growth

$16.7

$28.0 $27.2

4Q'12 1Q'13 2Q'13

Distributable Cash Flow* $ in millions

$13.1

$17.6 $18.6

4Q'12 1Q'13 2Q'13

Net Income* $ in millions

4.5% Growth

1.27x

**Represents Minimum Quarter Distribution (MQD) for 4Q ’12, actual $0.1769 equal to MQD prorated Note: 4Q ’12 is for 10/31/2012 to 12/31/2012, not a full quarter

*Attributable to MPLX

Note: 1 Tank Farms include the Patoka, Wood River, and Martinsville, IL, and Lebanon, IN tank farms 2 From Prospectus dated October 25, 2012 3 In light equivalent barrels for crude systems 4 In physical barrels

MPLX Pipeline Throughput Agreements

88

Initial MPC Min. 2011 MPC Est. 12 Mo. Ended 12/31/132 Term Diameter Commitment3 Throughput4 Weighted Average MPC Min.

Asset (Years) (Inches) (MBPD) (MBPD) Tariff ($ / BBL) Revenue ($MM) Crude Systems

Patoka to Lima 10 20" / 22" 40 117 $0.52 $7.6 Catlettsburg and Robinson 10 20" / 24" / 20" 380 428 $0.74 $101.4 Detroit 10 16" / 16" 155 107 $0.23 $12.8 Wood River to Patoka 5 22" / 12" 130 121 $0.20 $10.5 Wood River Barge Dock 5 -- 40 38 $1.32 $19.2

Total -- -- 745 811 -- $151.5 Products Systems

Garyville to Zachary 10 20" 300 258 $0.55 $59.8 Zachary Connect 10 36" 80 132 $0.04 $1.3 Texas City to Pasadena 10 16" 81 85 $0.27 $7.9 Pasadena Connect 10 30" / 36" 61 50 $0.07 $1.5 Ohio River Pipe Line (ORPL) 10 6" / 8" / 10" / 14" 128 126 $1.25 $58.2 Robinson 10 10" / 12" / 16" 209 320 $0.65 $49.9 Louisville Airport -NA- 8" / 6" -NA- -NA- -NA- -NA-

Total -- 859 971 -- $178.6

Initial MPC Min. 2011 MPC Est. 12 Mo. Ended 12/31/132

Term Commitment Capacity Leased Weighted Average MPC Min. Asset (Years) (MBBLS) (MBBLS) Fees ($ / BBL/month) Revenue ($MM) Agreements

Neal, W.Va. Butane Storage Cavern 10 1,000 -NA- $1.25 $15.0 Tank Farms¹ 3 3,293 3,293 $0.48 $19.0

Total -- 4,293 3,293 -- $34.0

Management team includes MPC executive officers with an average 25 years of experience with MPLX's assets

Position at MPC Position at MPLX Industry

Garry L. Peiffer Executive VP, Corporate Planning and Investor & Government Relations

Director and President 38 38

Donald C. Templin Senior VP and Chief Financial Officer

Director, VP and Chief Financial Officer

11 1

J. Michael Wilder VP, General Counsel and Secretary VP, General Counsel and Secretary 34 34

With MPC

Gary R. Heminger President and Chief Executive Officer

Chairman of the Board and Chief Executive Officer

37 37

Years Experience

31 31 Senior VP, Transportation and Logistics

VP and Chief Operating Officer George P. Shaffner

Craig O. Pierson President, Marathon Pipe Line LLC VP, Operations 34 34

Timothy T. Griffith VP, Finance and Treasurer VP and Treasurer 1 1

Michael G. Braddock VP and Controller 32 32 VP and Controller

Pamela K. M. Beall

16

16 VP, Investor Relations and Government & Public Affairs

VP, Investor Relations

Experienced MPLX Management Team

89

John R. Haley VP, Tax VP, Tax 31 31

As of 1/1/2013

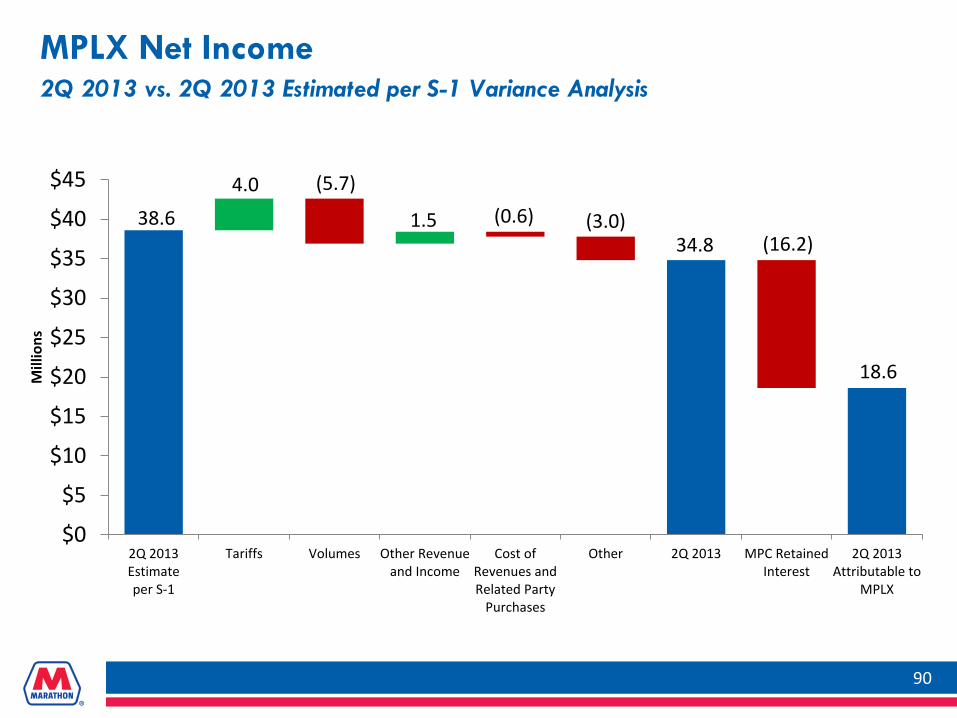

MPLX Net Income 2Q 2013 vs. 2Q 2013 Estimated per S-1 Variance Analysis

38.6 4.0 (5.7)

1.5 (0.6) (3.0) 34.8 (16.2)

18.6

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

2Q 2013Estimateper S-1

Tariffs Volumes Other Revenueand Income

Cost ofRevenues andRelated Party

Purchases

Other 2Q 2013 MPC RetainedInterest

2Q 2013Attributable to

MPLX

Mill

ions

90

MPLX Adjusted EBITDA and Distributable Cash Flow

91

($MM) 2Q 2013 Estimated 2Q 2013*

Adjusted EBITDA 47.4 49.7

Less: Adjusted EBITDA attributable to MPC-retained interest 20.7 23.2

Adjusted EBITDA attributable to MPLX LP 26.7 26.5

Less: Cash interest paid, net - 0.3

Income taxes paid - -

Maintenance capital expenditures paid 2.3 3.4

Plus: Increase in deferred revenue for committed volume deficiencies 2.8 -

Distributable cash flow 27.2 22.8

Distribution declared

Limited partners – public 5.7

Limited partners – MPC 15.4

General partner – MPC 0.4

Total distribution declared/estimated 21.5 19.8

Coverage ratio 1.27x 1.15x

*Based on information in Prospectus

MPLX LP Adjusted EBITDA and Distributable Cash Flow Reconciliation to Net Income

92

($MM) 2Q 2013 1Q 2013 4Q 2012* Net income 34.8 35.3 26.3

Less: Net income attributable to MPC-retained interest 16.2 17.7 13.2

Net income attributable to MPLX LP 18.6 17.6 13.1

Plus: Net income attributable to MPC-retained interest 16.2 17.7 13.2

Depreciation 11.9 11.7 7.9

Provision for income taxes 0.1 - 0.1

Non-cash equity-based compensation 0.3 0.2 0.1

Net interest and other financial costs (income) 0.3 0.2 0.2

Adjusted EBITDA 47.4 47.4 34.6

Less: Adjusted EBITDA attributable to MPC-retained interest 20.7 22.3 16.4

Adjusted EBITDA attributable to MPLX LP 26.7 25.1 18.2

Less: Cash interest paid - 0.2 0.2

Income taxes paid - - -

Maintenance capital expenditures paid 2.3 1.5 3.4

Plus: Increase in deferred revenue for committed volume deficiencies 2.8 4.6 2.1

Distributable cash flow attributable to MPLX LP 27.2 28.0 16.7 *For the period 10/31/12 to 12/31/12

MPLX Strong Financial Flexibility to Manage and Grow Asset Base

93

($MM except ratio data) As of 6/30/13

Cash and cash equivalents 115.3

Total assets 1,217.7

Long-term debt* 10.9

Total equity 1,128.6

Consolidated total debt to consolidated EBITDA ratio (covenant basis)** 0.1x

MPLX’s undrawn $500 million revolver provides significant liquidity to grow its business

*Represents a capital lease. Includes amounts due within one year **Maximum covenant ratio <= 5.0 or 5.5 during the six month period following certain acquisitions

![JEEP WRANGLER + AUTHENTIC ACCESSORIES · “ Jeep”ロゴ入り。 Wrangler [商品番号:LJ214636AA] 30,800円(28,000円) Wrangler Unlimited [商品番号:LJ214637AA] 39,600円(36,000円)](https://static.fdocuments.in/doc/165x107/5e6cd347498b75752a03b32e/jeep-wrangler-authentic-accessories-aoe-jeepaf-wrangler-cilj214636aa.jpg)

![LinkedIn Profile Tips That Really Work [28,000+ Connections]](https://static.fdocuments.in/doc/165x107/5442f6c0afaf9f0e118b47c7/linkedin-profile-tips-that-really-work-28000-connections.jpg)