INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY … · customer satisfaction choosing Bank...

13

INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 7, ISSUE 9, SEPTEMBER 2018 ISSN 2277-8616 148 IJSTR©2018 www.ijstr.org The Influence Of Marketing Mix, Culture And Quality Of Service To Customer Satisfaction Mediated Decision Of Selecting Sharia Bank In Gorontalo Province Soeharto Puluhulawa, Machfudnurnajamuddin, Syarhrir Mallongi, Mukhlis Sufri Abstract : The purpose of this research is to know and analyze the marketing mix, culture and service quality to customer's decision, to know and analyze the influence of marketing mix, culture and service quality to customer satisfaction, to know and analyze influence of customer decision to customer satisfaction, to know and analyze the role of customer decisions mediate the influence of marketing mix, culture and quality of service on customer satisfaction choosing Bank Syariah. The population in this study are the customers of Syariah Bank in Gorontalo Province consisting of Bank Syariah Mandiri, Bank Muamalat and Bank Mega Syariah with total population of 750. Sample of 16 0 customers by using sampling proportional random sampling technique. Data collection through questionnaires and analytical techniques using Structural Equation Modeling (SEM). The results of this study indicate that: marketing mix has a significant effect on customer's decision, culture has significant effect to customer's decision, service quality has significant effect to customer's organizational culture, marketing mix has significant effect to customer satisfaction, culture has no significant effect to customer satisfaction, customer satisfaction, customer decisions have a significant effect on customer satisfaction, marketing mix significant effect on customer satisfaction through customer satisfaction, culture significantly influence customer satisfaction through customer satisfaction, service quality significantly influence customer satisfaction through customer satisfaction. Keywords: Marketing Marketing Mix, Quality of service, Customer decisions and Customer satisfaction —————————— —————————— I. Introduction According to The Almanac Book of Facts (2011), in the last ten years, the world's population has grown by 137%. Where the adherents of Christianity increased by 46%. While the followers of Islam increased by 235%. With such huge growth, Indonesia has the potential to develop sharia banking system more quickly. Simple assumptions Indonesia has a population of 207,176,162 Muslims and if the Muslim population of Indonesia united to use the Sharia Bank then the acceleration of growth of Islamic banking can be done. Banking is one sector that has an important role in implementing development, especially in supporting the business world in all sectors. According to the Law of the Republic of Indonesia Number 10 of 1998 dated November 10, 1998 on Banking, the bank is a business entity that collects funds from the public in the form of savings and distributes it to the community in the form of credit and or other forms in order to improve the standard of living of many people. Excess funds customers keep their money in the bank in the form of savings accounts, savings and deposits. The law also provides guidance for conventional banks to open sharia branches or even completely convert themselves into sharia banks. Syafi'i Antonio (2001: 26) and the law No.23 of 1999 and Act No.3 of 2004 on Bank Indonesia. According to M. Arief Mufraini (2009) Islamic Bank is a bank that in carrying out all its activities based on and strive in accordance with the principles of sharia. Interest (usury) is prohibited in Islam, ie banks are not allowed to make payments or withdrawal of interest in all forms of transactions. A unique feature offered by sharia banks is profit-and-loss-sharing ( profit-and-loss-sharing) systems. Despite the many contracts in Islam, there are several important types of transactions: mudaraba (capital contract); musyarakah (contract partnership or partnership ) ( Lewis and Latifa, 2005: 11-14 ). The number of banks conducting business based on sharia principles in 2014 increases with the operation of several new banks. The number of BUSs recorded did not increase from the previous year which was 11 BUS, while the number of UUS was reduced to 23 UUS with the closing of HSBC UUS as part of the global consolidation of its parent bank. The number of BPRS increased from 158 BRPS to 163 BPRS. _____________________________ Soeharto Puluhulawa, Machfudnurnajamuddin, Syarhrir Mallongi, Mukhlis Sufri Muslim University of Indonesia

-

Upload

truongphuc -

Category

Documents

-

view

214 -

download

0

Transcript of INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY … · customer satisfaction choosing Bank...

INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 7, ISSUE 9, SEPTEMBER 2018 ISSN 2277-8616

148 IJSTR©2018 www.ijstr.org

The Influence Of Marketing Mix, Culture And Quality Of Service To Customer Satisfaction

Mediated Decision Of Selecting Sharia Bank In Gorontalo Province

Soeharto Puluhulawa, Machfudnurnajamuddin, Syarhrir Mallongi, Mukhlis Sufri

Abstract : The purpose of this research is to know and analyze the marketing mix, culture and service quality to customer's decision, to know and

analyze the influence of marketing mix, culture and service quality to customer satisfaction, to know and analyze influence of customer decision to customer satisfaction, to know and analyze the role of customer decisions mediate the influence of marketing mix, culture and quality of service on customer satisfaction choosing Bank Syariah. The population in this study are the customers of Syariah Bank in Gorontalo Province consisting of Bank Syariah Mandiri, Bank Muamalat and Bank Mega Syariah with total population of 750. Sample of 16 0 customers by using sampling proportional random sampling technique. Data collection through questionnaires and analytical techniques using Structural Equation Modeling (SEM). The results of this study indicate that: marketing mix has a significant effect on customer's decision, culture has significant effect to customer's decision, service quality has significant effect to customer's organizational culture, marketing mix has significant effect to customer satisfaction, culture has no significant effect to customer satisfaction, customer satisfaction, customer decisions have a significant effect on customer satisfaction, marketing mix significant effect on customer satisfaction through customer satisfaction, culture significantly influence customer satisfaction through customer satisfaction, service quality significantly influence customer satisfaction through customer satisfaction. Keywords: Marketing Marketing Mix, Quality of service, Customer decisions and Customer satisfaction

————————————————————

I. Introduction According to The Almanac Book of Facts (2011), in the last ten years, the world's population has grown by 137%. Where the adherents of Christianity increased by 46%. While the followers of Islam increased by 235%. With such huge growth, Indonesia has the potential to develop sharia banking system more quickly. Simple assumptions Indonesia has a population of 207,176,162 Muslims and if the Muslim population of Indonesia united to use the Sharia Bank then the acceleration of growth of Islamic banking can be done. Banking is one sector that has an important role in implementing development, especially in supporting the business world in all sectors. According to the Law of the Republic of Indonesia Number 10 of 1998 dated November 10, 1998 on Banking, the bank is a business entity that collects funds from the public in the form of savings and distributes it to the community in the form of credit and or other forms in order to improve the standard of living of many people. Excess funds customers keep their money in the bank in the form of savings accounts, savings and deposits. The law also provides guidance for conventional banks to open sharia branches or even completely convert themselves into sharia banks. Syafi'i Antonio (2001: 26) and the law No.23 of 1999 and Act No.3 of 2004 on Bank Indonesia. According to M. Arief Mufraini (2009) Islamic Bank is a bank that in carrying out all its activities based on and strive in accordance with the principles of sharia.

Interest (usury) is prohibited in Islam, ie banks are not allowed to make payments or withdrawal of interest in all forms of transactions. A unique feature offered by sharia banks is profit-and-loss-sharing ( profit-and-loss-sharing) systems. Despite the many contracts in Islam, there are several important types of transactions: mudaraba (capital contract); musyarakah (contract partnership or partnership ) ( Lewis and Latifa, 2005: 11-14 ). The number of banks conducting business based on sharia principles in 2014 increases with the operation of several new banks. The number of BUSs recorded did not increase from the previous year which was 11 BUS, while the number of UUS was reduced to 23 UUS with the closing of HSBC UUS as part of the global consolidation of its parent bank. The number of BPRS increased from 158 BRPS to 163 BPRS.

_____________________________

Soeharto Puluhulawa, Machfudnurnajamuddin, Syarhrir Mallongi, Mukhlis Sufri

Muslim University of Indonesia

INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 7, ISSUE 9, SEPTEMBER 2018 ISSN 2277-8616

149 IJSTR©2018 www.ijstr.org

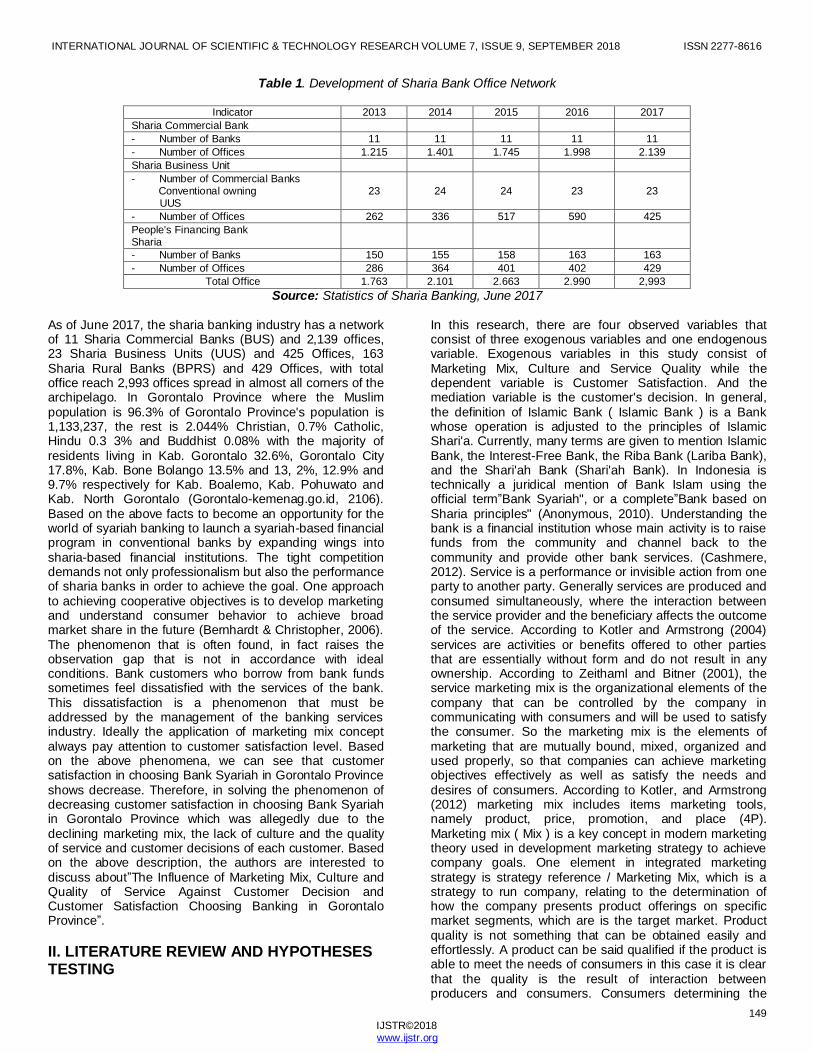

Table 1. Development of Sharia Bank Office Network

Indicator 2013 2014 2015 2016 2017

Sharia Commercial Bank

- Number of Banks 11 11 11 11 11

- Number of Offices 1.215 1.401 1.745 1.998 2.139

Sharia Business Unit

- Number of Commercial Banks Conventional owning

UUS

23

24

24

23

23

- Number of Offices 262 336 517 590 425

People's Financing Bank Sharia

- Number of Banks 150 155 158 163 163

- Number of Offices 286 364 401 402 429

Total Office 1.763 2.101 2.663 2.990 2,993

Source: Statistics of Sharia Banking, June 2017

As of June 2017, the sharia banking industry has a network of 11 Sharia Commercial Banks (BUS) and 2,139 offices, 23 Sharia Business Units (UUS) and 425 Offices, 163 Sharia Rural Banks (BPRS) and 429 Offices, with total office reach 2,993 offices spread in almost all corners of the archipelago. In Gorontalo Province where the Muslim population is 96.3% of Gorontalo Province's population is 1,133,237, the rest is 2.044% Christian, 0.7% Catholic, Hindu 0.3 3% and Buddhist 0.08% with the majority of residents living in Kab. Gorontalo 32.6%, Gorontalo City 17.8%, Kab. Bone Bolango 13.5% and 13, 2%, 12.9% and 9.7% respectively for Kab. Boalemo, Kab. Pohuwato and Kab. North Gorontalo (Gorontalo-kemenag.go.id, 2106). Based on the above facts to become an opportunity for the world of syariah banking to launch a syariah-based financial program in conventional banks by expanding wings into sharia-based financial institutions. The tight competition demands not only professionalism but also the performance of sharia banks in order to achieve the goal. One approach to achieving cooperative objectives is to develop marketing and understand consumer behavior to achieve broad market share in the future (Bernhardt & Christopher, 2006). The phenomenon that is often found, in fact raises the observation gap that is not in accordance with ideal conditions. Bank customers who borrow from bank funds sometimes feel dissatisfied with the services of the bank. This dissatisfaction is a phenomenon that must be addressed by the management of the banking services industry. Ideally the application of marketing mix concept always pay attention to customer satisfaction level. Based on the above phenomena, we can see that customer satisfaction in choosing Bank Syariah in Gorontalo Province shows decrease. Therefore, in solving the phenomenon of decreasing customer satisfaction in choosing Bank Syariah in Gorontalo Province which was allegedly due to the declining marketing mix, the lack of culture and the quality of service and customer decisions of each customer. Based on the above description, the authors are interested to discuss about”The Influence of Marketing Mix, Culture and Quality of Service Against Customer Decision and Customer Satisfaction Choosing Banking in Gorontalo Province”.

II. LITERATURE REVIEW AND HYPOTHESES TESTING

In this research, there are four observed variables that consist of three exogenous variables and one endogenous variable. Exogenous variables in this study consist of Marketing Mix, Culture and Service Quality while the dependent variable is Customer Satisfaction. And the mediation variable is the customer's decision. In general, the definition of Islamic Bank ( Islamic Bank ) is a Bank whose operation is adjusted to the principles of Islamic Shari'a. Currently, many terms are given to mention Islamic Bank, the Interest-Free Bank, the Riba Bank (Lariba Bank), and the Shari'ah Bank (Shari'ah Bank). In Indonesia is technically a juridical mention of Bank Islam using the official term”Bank Syariah", or a complete”Bank based on Sharia principles" (Anonymous, 2010). Understanding the bank is a financial institution whose main activity is to raise funds from the community and channel back to the community and provide other bank services. (Cashmere, 2012). Service is a performance or invisible action from one party to another party. Generally services are produced and consumed simultaneously, where the interaction between the service provider and the beneficiary affects the outcome of the service. According to Kotler and Armstrong (2004) services are activities or benefits offered to other parties that are essentially without form and do not result in any ownership. According to Zeithaml and Bitner (2001), the service marketing mix is the organizational elements of the company that can be controlled by the company in communicating with consumers and will be used to satisfy the consumer. So the marketing mix is the elements of marketing that are mutually bound, mixed, organized and used properly, so that companies can achieve marketing objectives effectively as well as satisfy the needs and desires of consumers. According to Kotler, and Armstrong (2012) marketing mix includes items marketing tools, namely product, price, promotion, and place (4P). Marketing mix ( Mix ) is a key concept in modern marketing theory used in development marketing strategy to achieve company goals. One element in integrated marketing strategy is strategy reference / Marketing Mix, which is a strategy to run company, relating to the determination of how the company presents product offerings on specific market segments, which are is the target market. Product quality is not something that can be obtained easily and effortlessly. A product can be said qualified if the product is able to meet the needs of consumers in this case it is clear that the quality is the result of interaction between producers and consumers. Consumers determining the

INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 7, ISSUE 9, SEPTEMBER 2018 ISSN 2277-8616

150 IJSTR©2018 www.ijstr.org

limits of producers are trying to reach those limits through the production stage. Cultures include awareness and unconsciousness of the values, ideas, attitudes, and symbols that shape human behavior and are passed on from one generation to the next. Culture is”the collective order of the mind that distinguishes that member from one category of person to another. Geert Hofstede (2001). Culture in a business setting is defined as learning, sharing, coercive as well as a collection of mutual symbols, related and meaningful and provides a set of orientations for community members. Culture contains branches of culture that have little common ground between one culture and another. Kotabe ( 2007). Cultural values that exist in a society give a greater impact on the behavior of consumer consumption, which in this case included into the general category that is in the form of orientation values that reflect the image of a society as well as about the correct relationship between individuals and groups in society. This relationship has a major influence in marketing practices. In the perspective of Islamic culture are all values, thoughts, and symbols that affect the behavior, attitudes, beliefs, and habits of people and society. An example is the timely culture taught in Islam. The quality of services should start from the customer's needs and end in customer's perception. The customer's perception of the quality of the service itself is the overall assessment of the top customer excellence of a service. The long development of the SERVQUAL model can be traced to eight main stages: birth, instrumentation, extended gaps model, service expectations determinant, SERVQUAL instrument revision, SERVQUAL impact on behavioral interest, service quality information system, and SERVQUAL. Tjiptono (2005) explains that quality can not be defined if it is not related to a particular context. Quality is a characteristic or product attribute, this means that to define quality must first be determined. For example reliability is the characteristic quality of a car, the quality of the letter is the clarity of its contents or the length of the letter. So the conclusion can be drawn from the opinion expressed by Tjiptono (2005) that:”Quality is the subjective judgment of the customer, this assessment is determined by the customer's perception of the product (goods and services). These perceptions may change due to various influences, such as effective advertising, the reputation of a particular product, experience, friends, and so on. So it's important to understand: (a) how the product is perceived by the customer, and (b) when that perception changes.” The decision of the community to be a customer of Bank Syariah according to Prasetijo and Ilhalauw's decision is an option of action of the two or more alternative choice. In other words, the person making the decision should has one or several alternative options available. When someone confronted by two choices of buying and not buying and then he buy, then there is a position to make a decision (Prasetijo & Ilhalauw, 2004). In contrast to Atmosudirjo (2010) which explains that decisions are a termination rather than a process of thinking about a problem or problem to answer the question of what must be done to overcome the problem, by choosing an alternative. Customer satisfaction is the customer's perception that the expectation has been fulfilled, the optimal result for every customer and banking service by taking into account the ability of the customer and his family, the attention to his /

her family, the attention to the customer's needs so that the best continuity between satisfaction and yield. Tjiptono in Noviyantie (2001) customer satisfaction is a buyer evaluation where the chosen alternatives at least provide the outcomes equal to the customer's expectations. Dissatisfaction arises if the results obtained do not meet customer expectations. According to Kottler (2000: 35) customer satisfaction is the level of a person's feelings after comparing the performance or results he received compared to his expectations. New customers will feel satisfied if the performance of banking services that they get the same or more than what they expect and feelings of disappointment customers will arise if the performance is not in accordance with what the expectations. Caruana & Msida (2002) argue that customer satisfaction as a whole has three antecedents of perceived quality, perceived value and customer's expectation. Perceived quality has a positive effect on customer satisfaction and overall negatively affects customer complaints and positively affects customer loyalty

III. RESEARCH METHODS In accordance with the research objectives that have been formulated, then this research uses the explanation pattern is research that is intended to explain the position of variables - the variables studied and the relationship between one variable with other variables and test the hypothesis that has been formulated. Thus this study explains the magnitude of the influence of the marketing mix variables, the culture, and the quality of service to customer decisions and customer satisfaction. This research will be conducted on Syariah Banking in Gorontalo Province with the consideration that the data and information required in this study can be identified and obtained accurately and very relevant to the subject matter encountered in this study. Methods of data collection in this study consisted of observations, questionnaires and documentation. According to the source, then the type of data used in this study there are two types: Primary Data is data obtained from direct interviews with customers of Sharia Banking in Gorontalo Province and Secondary Data That is data obtained from various sources either from writing, documentation or from information from related parties related to the issues studied such as Age; Gender; Religion ; Workers ; Income; Funds / Savings; Old Customer; Other Clients. Population in this research is all sharia banking customer in Gorontalo Province Paying attention to bank population in sharia banking industry in Gorontalo Province, hence taken target population of syariah bank based on consideration ( purposive sampling ) that is amount of net profit and representation of bank group by ownership. Of the total population of 750 customers of Bank Syariah with 7% precision description of sample size of 160 respondents The following is the population recapitulation and sample research. To test the truth of the Hypothesis that has been formulated before, then the method of analysis used in this study is by testing the research instrument that is by using two test methods of validity and reliability test. This test is conducted to ensure that the research instrument (questionnaire) is eligible to be used as a data collection tool. Having tested the validity and reliability testing later This research uses two approaches of method an alisas, namely descriptive analysis and

INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 7, ISSUE 9, SEPTEMBER 2018 ISSN 2277-8616

151 IJSTR©2018 www.ijstr.org

Structural Equation Modeling (SEM) using AMOS application 16.0 0. (Solimun, 2004).

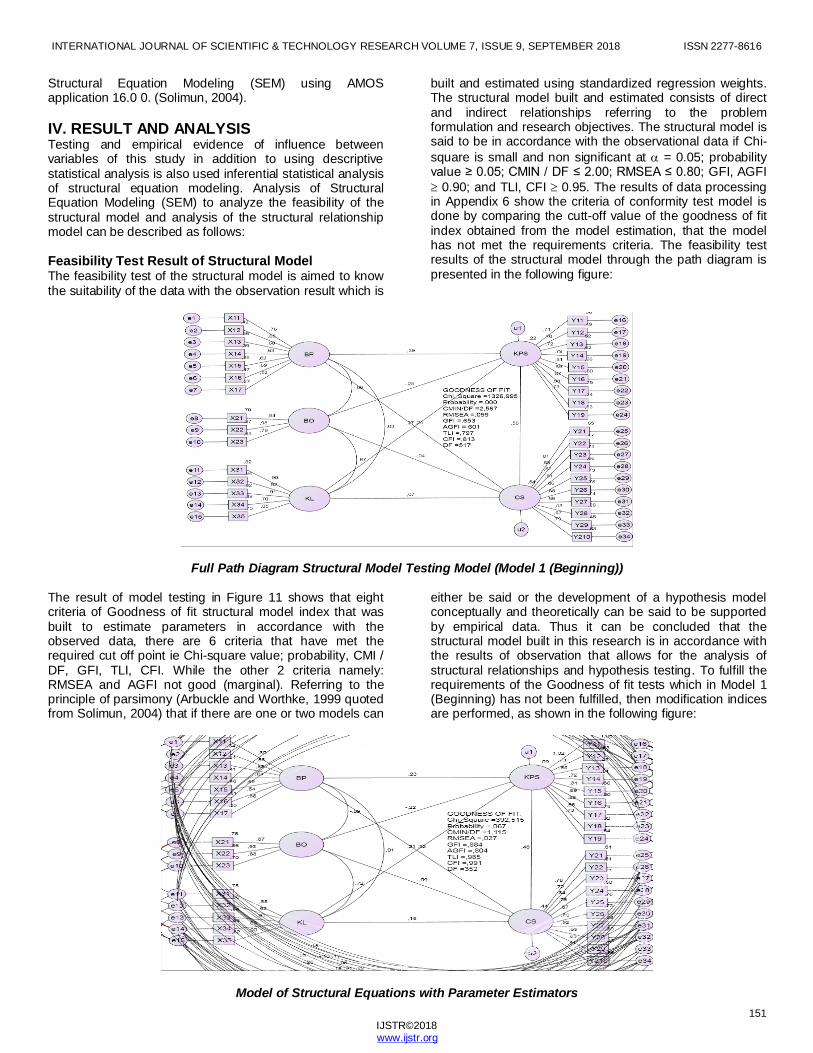

IV. RESULT AND ANALYSIS Testing and empirical evidence of influence between variables of this study in addition to using descriptive statistical analysis is also used inferential statistical analysis of structural equation modeling. Analysis of Structural Equation Modeling (SEM) to analyze the feasibility of the structural model and analysis of the structural relationship model can be described as follows: Feasibility Test Result of Structural Model The feasibility test of the structural model is aimed to know the suitability of the data with the observation result which is

built and estimated using standardized regression weights. The structural model built and estimated consists of direct and indirect relationships referring to the problem formulation and research objectives. The structural model is said to be in accordance with the observational data if Chi-

square is small and non significant at = 0.05; probability value ≥ 0.05; CMIN / DF ≤ 2.00; RMSEA ≤ 0.80; GFI, AGFI

0.90; and TLI, CFI 0.95. The results of data processing in Appendix 6 show the criteria of conformity test model is done by comparing the cutt-off value of the goodness of fit index obtained from the model estimation, that the model has not met the requirements criteria. The feasibility test results of the structural model through the path diagram is presented in the following figure:

Full Path Diagram Structural Model Testing Model (Model 1 (Beginning))

The result of model testing in Figure 11 shows that eight criteria of Goodness of fit structural model index that was built to estimate parameters in accordance with the observed data, there are 6 criteria that have met the required cut off point ie Chi-square value; probability, CMI / DF, GFI, TLI, CFI. While the other 2 criteria namely: RMSEA and AGFI not good (marginal). Referring to the principle of parsimony (Arbuckle and Worthke, 1999 quoted from Solimun, 2004) that if there are one or two models can

either be said or the development of a hypothesis model conceptually and theoretically can be said to be supported by empirical data. Thus it can be concluded that the structural model built in this research is in accordance with the results of observation that allows for the analysis of structural relationships and hypothesis testing. To fulfill the requirements of the Goodness of fit tests which in Model 1 (Beginning) has not been fulfilled, then modification indices are performed, as shown in the following figure:

Model of Structural Equations with Parameter Estimators

INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 7, ISSUE 9, SEPTEMBER 2018 ISSN 2277-8616

152 IJSTR©2018 www.ijstr.org

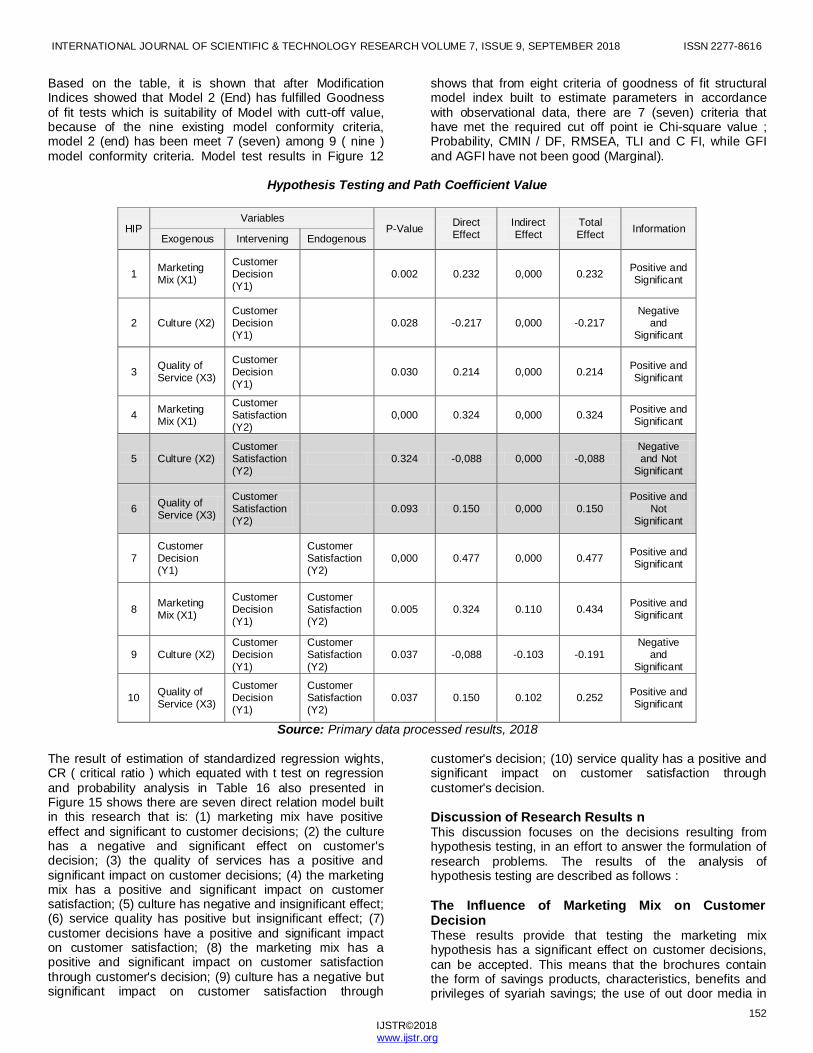

Based on the table, it is shown that after Modification Indices showed that Model 2 (End) has fulfilled Goodness of fit tests which is suitability of Model with cutt-off value, because of the nine existing model conformity criteria, model 2 (end) has been meet 7 (seven) among 9 ( nine ) model conformity criteria. Model test results in Figure 12

shows that from eight criteria of goodness of fit structural model index built to estimate parameters in accordance with observational data, there are 7 (seven) criteria that have met the required cut off point ie Chi-square value ; Probability, CMIN / DF, RMSEA, TLI and C FI, while GFI and AGFI have not been good (Marginal).

Hypothesis Testing and Path Coefficient Value

HIP Variables

P-Value Direct Effect

Indirect Effect

Total Effect

Information Exogenous Intervening Endogenous

1 Marketing Mix (X1)

Customer Decision (Y1)

0.002 0.232 0,000 0.232 Positive and Significant

2 Culture (X2) Customer Decision (Y1)

0.028 -0.217 0,000 -0.217 Negative

and Significant

3 Quality of Service (X3)

Customer Decision (Y1)

0.030 0.214 0,000 0.214 Positive and Significant

4 Marketing Mix (X1)

Customer Satisfaction (Y2)

0,000 0.324 0,000 0.324 Positive and Significant

5 Culture (X2) Customer Satisfaction (Y2)

0.324 -0,088 0,000 -0,088 Negative and Not

Significant

6 Quality of Service (X3)

Customer Satisfaction (Y2)

0.093 0.150 0,000 0.150 Positive and

Not Significant

7 Customer Decision (Y1)

Customer Satisfaction (Y2)

0,000 0.477 0,000 0.477 Positive and Significant

8 Marketing Mix (X1)

Customer Decision (Y1)

Customer Satisfaction (Y2)

0.005 0.324 0.110 0.434 Positive and Significant

9 Culture (X2) Customer Decision (Y1)

Customer Satisfaction (Y2)

0.037 -0,088 -0.103 -0.191 Negative

and Significant

10 Quality of Service (X3)

Customer Decision (Y1)

Customer Satisfaction (Y2)

0.037 0.150 0.102 0.252 Positive and Significant

Source: Primary data processed results, 2018

The result of estimation of standardized regression wights, CR ( critical ratio ) which equated with t test on regression and probability analysis in Table 16 also presented in Figure 15 shows there are seven direct relation model built in this research that is: (1) marketing mix have positive effect and significant to customer decisions; (2) the culture has a negative and significant effect on customer's decision; (3) the quality of services has a positive and significant impact on customer decisions; (4) the marketing mix has a positive and significant impact on customer satisfaction; (5) culture has negative and insignificant effect; (6) service quality has positive but insignificant effect; (7) customer decisions have a positive and significant impact on customer satisfaction; (8) the marketing mix has a positive and significant impact on customer satisfaction through customer's decision; (9) culture has a negative but significant impact on customer satisfaction through

customer's decision; (10) service quality has a positive and significant impact on customer satisfaction through customer's decision. Discussion of Research Results n This discussion focuses on the decisions resulting from hypothesis testing, in an effort to answer the formulation of research problems. The results of the analysis of hypothesis testing are described as follows :

The Influence of Marketing Mix on Customer Decision These results provide that testing the marketing mix hypothesis has a significant effect on customer decisions, can be accepted. This means that the brochures contain the form of savings products, characteristics, benefits and privileges of syariah savings; the use of out door media in

INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 7, ISSUE 9, SEPTEMBER 2018 ISSN 2277-8616

153 IJSTR©2018 www.ijstr.org

the form of billboards, banners and posters make it easy for people to recognize syariah savings; giving rewards as an effort to maintain loyalty can be perceived both by the customer. Facts in the field based on respondents' assessment of marketing mix variables is known that the majority of respondents perceive is good in assessing the procedure of opening an easy savings account. This means that when seen from the empirical fact that the real through customer perception of the ease of Islamic banks makes it easier to open an account with regard to the marketing mix that includes product (product), price (price), location (place), promotion (promotion), those (people), physical evidence ( phisical avidence ) and process ( process ) is good. Furthermore, regarding the assessment of respondents on promotion ( promotion ) has the highest average value compared with other indicators. The respondent's statement about promotion is good. This condition can be mirrored by distributing brochures containing products to every public place, both in offices, schools and shopping centers, the more distribution to the society, the more people understand the product of syariah savings, the characteristics, the use of billboards or signboards that are installed as videotron so that the public road users can see firsthand the advertisements given about sharia products even if only at a glance, banners and posters that make it easy for people to recognize syariah savings, giving rewards as an effort to maintain customer loyalty. Based on the path analysis model shows that the marketing mix is able to contribute to customer decisions. Research on the ground in accordance with research findings from Nasrun Fuad, et.al (2014); states that the marketing mix affects customer decisions. This study supports the opinions of Booms and Bitner (Lovelock et al., 2013) suggesting a marketing mix of both tangible and intangible services creates value for the customer so that it can influence the decision to be taken by the customer. Marketing mix is not always appropriate to be used, applied and accepted on all temoat because under certain conditions the marketing mix is more necessary. In this research hasl underlies that a promotion for savings products can be done in accordance with the opinion Sumiyanto (2008) that techniques that can be used in marketing savings products is advertising, approach and establish cooperation. Advertising is done by sending a letter containing information on the progress of the business that has been run, the capital application, congratulating the Muslim figures or entrepreneurs. Approach by holding meetings and assessments that collect the potential of Muslims, disseminating opinions about sharia economy, there to be a potential candidate member. Furthermore, the implementation aspect of wa'diah system and mudharabah saving product at Sharia Bank gives positive impact to customers. The availability of Syariah savings product with wa'diah and mudharabah system causes an influence on customer's decision to save on Sharia Bank. Cultural Influence On Customer Decision These results provide that testing the cultural hypothesis has a negative but significant impact on customer decisions, can be rejected. This means that if the community is principled if the profit-sharing system affects the customers to choose syariah syllah bank so that it is perceived both by customers who use the services of

sharia. Facts in the field based on respondents' research on cultural variables is known that the majority of respondents perceive is good. This means that if observed from the real empirical facts through customer perceptions of cultures related to the culture itself, sub-culture that exist in an area and social groups. Further assessment of respondents on social group indicators have the highest average score or are in very good category. In this case the social group indicators are well perceived by the respondents. This condition may reflect through the results of a cultural overview of the principles of revenue sharing that can influence customers to choose the Mudharabah Sharia Bank. Hypothesis test results found that culture has a negative but significant impact on customer decisions. This means that in improving customer decisions does not mean to rely on cultural variables in the improvement so that the findings in this field received support from Kotler and Kevin (2007) which states that there are several factors in influencing consumer behavior in determining decisions such as culture, sub culture and social class. This condition also supports the results of research from Suharto (2015) which states that cultural factors can affect the behavior of customers in choosing financing services. Cultural factors have an influence on customer decisions because of business agreements between different cultures and customs may be affected by additional challenges. If one party from a high-context culture takes part in the deal, the factors discussed may be more complicated because of the different beliefs about the significance of the agreement both formally and the obligations that all parties bind to, for example, the marketing manager really believes that only the written well needed to allow his company to accept all binding obligations. But it was also a marketing manager can not understand denganbaik, things can only happen when there is a personal connection because sometimes the personal relationships also need to implement something in the context of the environment is low.

Influence of Service Quality to Customer Decision These results provide that testing of service quality hypotheses has a significant effect on customer decisions, is acceptable. This means that if the employees of Syariah Banks instill trust and sense of security to customers and always perform their duties properly and appropriately it will be perceived both by the customer. Field findings support Wei-Ming Ou's research, et al., (2011 ) which states that service quality can improve customer decisions. This condition is also supported by the opinion of Parasumraman et al. (1988) which states that the quality of service is a comparison of the expectations of customers with services received it will affect the decision to be taken by customers. Furthermore, according to Zethaml et.al (1990) argues that the quality of service to the expectations of customers based on information obtained through word of mouth so that the fact the community can receive the information well. The existence of different dimensions of measurement of service quality encouraging the researcher's consideration to re-examine the service quality indicator especially on service based on customer's point of view. Guarantees of good service assurance according respondents and the guarantee of customer safety in terms of the interference can be guaranteed well, which is perceived good by the customer, then the sincere attention

INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 7, ISSUE 9, SEPTEMBER 2018 ISSN 2277-8616

154 IJSTR©2018 www.ijstr.org

given from the employees with sincerity and thoroughness in providing services that are good dipersesikan by the customer, then the customer will tend to take the right decision in choosing the offered sharia banking.

The Influence of Marketing Mix Against Customer Satisfaction This implies that the marketing mix affects customer satisfaction. Path coefficient marked positive means there is a unidirectional relationship between the marketing mix that has product, price, place, promotion, people, physical avidence and process, will increase customer satisfaction in Syariah Banking in Gorontalo Province. This is very reasonable because customers need a detailed understanding of the existing products in the Islamic Banking with the convenience given to customers. The results of the field research support what has been suggested by Tse and Wilton (2000), states that customer satisfaction is the customer's response to the evaluation of the perceived mismatch between previous expectations or other performance norms and the actual performance of the perceived product after use. Some of the factors that affect the marketing mix as revealed by Ita Rosdiana (2011) marketing mix (product, place, price and promotion) affect customer satisfaction. For the devout Muslims, the bank interest is forbidden by religion. Because bank interest is categorized as usury. In 1992 the bank was born Muamalat Indonesia as a operate by not using interest (usury). Since Bank Muamalat Indonesia uses profit sharing system, Bank Muamalat is free from interest rate risk, exchange rate risk and credit risk and this causes Bank Muamalat Indonesia to survive and exist when Indonesia is hit by monetary crisis. In general, marketing revolves around how to set or target ( targeting ), which is to strategically select a custom that just wants to be satisfied, positioning, and designing a product or service that has the usefulness and benefits that people want and not acquired elsewhere and builds good brand. Marketing also deals with advertising and pricing of promotions and distribution and other marketing programs. The Influence of Culture on Customer Satisfaction This suggests that culture has no effect on customer satisfaction. Path coefficient marked negative means there is unidirectional relationship which has culture indicator, sub culture and social group not able to increase customer satisfaction at Syariah Banking in Gorontalo Province. The results of this study support research findings from Acik Uhya (2013) who found that culture has no significant effect on customer satisfaction. Results in this field support the theory of Hall (1989) which explains that culture is communication so if the communication is not going well will cause dissatisfaction. In the perspective of Islamic culture are all values, thoughts, and symbols that affect the behavior, attitudes, beliefs, and habits of people and society. An example is the timely culture taught in Islam. In the hadith narrated by Imam Baihaqi, Prophet Muhammad SAW said which means”Prepare five before (coming) five. The period of your life before your time of death, your healthy life before your time of illness, your spare time before your busy time, your youth before your old age, and yours before your poor time comes.”(Baihaqi from Ibn Abbas) The lack of cultural influence on customer satisfaction is one of them because there are ancestral

values and moral upbringing of families that should be able to influence customers to make choices, but this is not the case. Basically, the majority of people in Gorontalo province are Muslim should be able to understand well the culture but in reality it can not help the community well in understanding the existence of Islamic banking so that it becomes very limited knowledge, their motion to know the basic difference with conventional banking thereby impacting on the not satisfaction of the customers. The Effect of Service Quality on Customer Satisfaction The result of perception of respondents that empathy ( emphaty ) has the lowest role in describing service quality variables. However, based on the estimated value of loading assurance indicators ( assurance ) to be the lowest indicator of influence. Thus from the test results of the measurement model of service quality variables that have the lowest contribution is the assurance indicator ( assurance ) that has not been implemented properly according to the respondent's assessment. However, the results of this study support the findings of research from Padma et al., (2010) which states that the quality of service that has no significant effect on the satisfaction of officers is clinical care. Research conducted by Parasuraman et al., (1988) with business to business object and this research with Hospital object. These two studies show that different objects mean the relationship of the influence of service quality to customer satisfaction applies not only to private institutions, hospitals but also to other objects, the findings of this study extend the results that have been done by previous researchers. Not influencing the quality of service to customer satisfaction disebebkan because attitudes shown by employees are less friendly in serving transactions so as to make customers do not feel comfortable with the services provided although not all employees who behave like that. When in fact that happens only a few people who behave less friendly in serving but as customers feel all forms of services provided by Islamic banks together, it gives a negative impact to customers. Not affect the quality of service to customer satisfaction due to the facilities provided are less attractive, for example, customers complain ATM facilities are rarely found at the center so that the customer difficulties when transacting and its ATM is also difficult to use to transact in mini markets for different MCB reasons and cost to transact. Furthermore, the waiting room facility at the time of transactions in the Bank also does not allow sometimes make the customer stand up and do not get a seat, customers also sometimes complain of parking spaces that are on the roadside inconvenience other riders that can cause congestion. Effect of Customer's Decision on Customer Satisfaction Facts in the field based on respondents' assessment of customer decision variables is known that the majority of respondents perceive is good. This means that if examined from the real empirical facts through customer perceptions of customer decisions related to the customer decides the variety of products, ratio and profit sharing, sharia principles, knowing the strategic location, knowing the account procedures, knowing the loan procedures, the ease

INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 7, ISSUE 9, SEPTEMBER 2018 ISSN 2277-8616

155 IJSTR©2018 www.ijstr.org

of using ATM,, mobile banking services, the average respondent's answer indicates that customer decisions are good. Further assessment of respondents on indicators know the account procedure has the highest average score or is in very good category. In this case the account procedure indicators are perceived both by the respondent. This condition can be seen from the fact that there are some customers decide to choose Bank Syariah because knowing the procedure of opening account / saving which facilitate in doing transaction. Furthermore, according to Ralph C. Davis (2010) decision is the result of solving the problem he faced firmly. A decision is a definite answer to a question. The decision should be able to answer the question of what is being discussed in relation to the planning. Decisions can also be actions against execution that are very deviant from the original plan. The decision of the community to be a customer of Bank Syariah according to Prasetijo and Ilhalauw decision is an option of action of two or more alternative options. The role of Customer's Decision in mediating the effect of marketing mix on Customer Satisfaction The results show that the more effective marketing mix followed by high customer decisions can improve customer satisfaction. These results mean that the marketing mix directly affects customer satisfaction, but the marketing mix will affect customer satisfaction if through customer decisions. The results of this study support the customer decision theory proposed by Kotler (2008) stating that the customer decision process has specific stages that greatly affect the decisions of the people who will become customers in Bank Syariah. As has been proven that the marketing mix directly affects customer satisfaction, whether mediated by customer decisions. Based on the result of this research, that customer decision influence to customer satisfaction. In accordance with the fact that the customer has made the decision to choose the appropriate savings. Customers are satisfied with the privilege of syariah savings with profit sharing system that is far from usury.

The role of Customer's Decision in mediating the influence of Culture on Customer Satisfaction Based on the results of this study as has been explained above that the culture has no direct effect on customer satisfaction. Strengthening the results of previous research conducted by Acik Uhya (2013) who found that culture has no significant effect on customer satisfaction. Results in this field support the theory of Hall (1989) which explains that culture is communication so if the communication is not going well will cause dissatisfaction. In the perspective of Islamic culture are all values, thoughts, and symbols that affect the behavior, attitudes, beliefs, and habits of people and society. Research in the field is inconsistent with research findings from Roni Andespa (2017) which states that the culture of West Sumatera people has significantly improved on customer satisfaction to save in sharia bank. The results of this study is supported by the opinion of Machmud and Rukmana (2016) which states that the concept of sharia and profit sharing system that is able to distinguish itself with existing conventional banks, according to Lamb, Hair and McDaniel (2011) culture is an important character of a social which distinguishes it from that culture

group others. Banking services have functions, values, forms and meanings. When customers use banking services they expect it to function as expected, and customers continue to use it only when their expectations are met well. Culture is usually studied since a customer is still small, so customers can start getting the values of beliefs and habits from the environment that then shapes the culture. In many ways, culture can be learned. As is commonly known when an adult or an older client friend taught customers how to behave. The role of Customer's Decision in mediating the influence of Quality of Service on Customer Satisfaction The results show that the more effective quality of service followed by high customer decisions can improve customer satisfaction. This result means that the quality of service does not directly affect customer satisfaction, but the quality of service will affect customer satisfaction if through customer decisions. Quality of service refers to the quality of service offerings expected and perceived. This is mainly by determining customer satisfaction or dissatisfaction. Many companies are prioritizing the quality of services that are expected and perceived to enhance the quality of these services. Based on the results of research descriptively that attitudes shown by employees are less friendly in serving transactions so as to make customers do not feel comfortable about the services provided although not all employees who behave like that. When in fact that happens only a few people who behave less friendly in serving but as customers feel all forms of services provided by Islamic banks together, it gives a negative impact to customers. To generate high customer satisfaction requires a friendly attitude. This is in line with the quality of service can be know by comparing the customer perceptions of the real service in order to meet the needs and expectations of customers. If in fact greater than expected, then the service can be said quality, whereas if the reality is less than expected, then the service can be said not qualified; if reality equals expectations, then the service is called satisfactory. Quality of service refers to the quality of service offerings expected and perceived. This is mainly by determining customer satisfaction or dissatisfaction. Many companies are prioritizing the quality of services that are expected and perceived to enhance the quality of these services.

V. CONCLUSIONS AND RECOMMENDATIONS Based on the results of the analysis and discussion, it can be concluded about the Role of Client's Decision in mediating the influence of Marketing Mix, Culture, Quality of Service to Customer's Satisfaction on Sharia Practices in Gorontalo as follows: Marketing Mix affects customer decisions. This is caused by the promotion that is done. Promotion carried out contains products, characteristics, advantages as well as privileges of syariah savings, the use of billboards, banners and posters that make it easy for people to recognize syariah savings, gift giving as an effort to maintain customer loyalty

INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 7, ISSUE 9, SEPTEMBER 2018 ISSN 2277-8616

156 IJSTR©2018 www.ijstr.org

Culture affects customer decisions. This is due to social groups. Social groups are reflected through the results of a cultural overview of the principles of profit sharing that can influence customers to choose the Mudharabah Sharia Bank. Service quality affects customer decisions. This is caused by the assurance (assurance). Assurance (assurance) is meant by way of instilling trust and sense of security to customers, and employees perform their duties properly and correctly. Marketing mix affects customer satisfaction. Caused by customers need a detailed understanding of the existing products in the Islamic Banking with the convenience provided to customers. Culture has no effect on customer satisfaction. This is caused by the culture of Islamic banking. This means that the ancestral values and moral education of the family will influence the customer to make choices; choose sharia bank because customer perception about bank interest is haram and prefer to use syariah banking service from conventional bank. Quality of service has no effect on customer satisfaction. This is due to empathy (emphaty). This means that some empathy form factors (emphaty) are employees who are friendly and polite in serving the transaction; employees with care and patience in serving the transaction. Customer decisions affect customer satisfaction. This is due to the fact that some customers decide to choose a Sharia Bank because they know the procedure of opening an account / savings that facilitates the transaction. The role of customer decisions in mediating the influence of the marketing mix with customer satisfaction. Customer decisions provide an overview of the marketing mix and customer satisfaction. This means that the customer has made the decision to choose the appropriate savings. Customers are satisfied with the privilege of syariah savings with profit sharing system that is far from usury. The role of customer decisions in mediating cultural influences with customer satisfaction. Customer decisions do not provide cultural descriptions and customer satisfaction. This means that although some customers are Muslim but in reality it can not help the community well in understanding the existence of Islamic banking so that it becomes very limited knowledge, their motion to know the fundamental difference with conventional banking so that the impact is not maximnya satisfaction owned by the customer. The role of customer decisions in mediating the impact of service quality with customer satisfaction. Customer decisions do not provide an overview of service quality and customer satisfaction. This means that when the sense of security at the time the customer is saving and space at the time of transaction that makes the customer is free in moving.

B. Suggestions Based on the above conclusions, the advice given is as follows : It is expected that the management of Islamic Banking is more focused in providing understanding - understanding of the noble values that exist in the culture especially in Goromtalo where some people are Muslims. It is expected that Shariah Banking management to further improve the quality of service to customers so that the information provided can be well understood, provide friendly service and explain in detail information about sharia products. The results of this study are expected to be useful for generating a mix of marketing, culture, service quality, customer satisfaction in an effort to improve customer's satisfaction that has not received maximum attention. For the next researcher is expected to develop this research, especially to add some constructs (variable) or research object that have similarity in the respondent's construct, both in terms of work and location so that it can be genaralisir.

BIBLIOGRAPHY [1] Abadi, YT (2010). Comparative Analysis of

Financial Performance between Sharia Banking and Conventional Banking (In the period March 2007 to March 2009). Not Published. Faculty of Economics and Business. Gadjah Mada University

[2] Abdullah, Thamrin. 2013. Marketing Management.

Jakarta: PT. RajaGrafindo Persada.

[3] Acep Jayaprawira. Gorontalo Times 2015. Natural Sharia Banking Slows Growth. Thursday, November 12, 2015.

[4] Achmad, Sobirin (2007). Organizational Culture

Understanding, Its Meaning and Its Application In Organizational Life. Yogyakarta: IBPP STIM YKPN.

[5] Adiwarman, A. Karim.2004. Islamic Bank Fiqh and

Financial Analysis, Jakarta: PT. Raja Grapindo Persada.

[6] Afrida Shela Mevita, 2015. The Influence of

Marketing Mix Against Consumer Satisfaction

[7] Agus Widyantoro second printing, Jakarta., PT. INDEX

[8] Ahmad Sumiyanto, 2008. BMT Toward a Modern

Cooperative, Yogyakarta: PT ISES With Partnership Principle), Yogyakarta: Genta Press.

[9] Algaoud, Latifa M. and Mervyn K. Lewis. 2005.

Sharia Banking: Principles, Practices and Prospects. Jakarta: Serambi Ilmu Semesta

INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 7, ISSUE 9, SEPTEMBER 2018 ISSN 2277-8616

157 IJSTR©2018 www.ijstr.org

[10] Alma, Buchari. 2005. Marketing Management and Service Marketing. Alfabeta, Bandung

[11] Al-Qur'an Surah Al-Baqarah (2) verses 278-279.

Al-Qur'an and Translation. Prints to 7: Al-Mizan Publishing House

[12] Andri Soemitra, 2009, Bank and Sharia Financial

Institution, Prenada Media,. Jakarta.

[13] Anonymous”Market and Marketing in an Islamic perspective" in http://d3manajemen.blogspot.com/2012/01/ market-and-marketing-in-perspective.html (4April 2013)

[14] Antonio, Muhammad Shafi'i. 2001. Sharia Bank

from Theory to Practice. Jakarta: Gema Insani and Tazkia Cendikia.

[15] Anwar King Mangkunegara. 2005. Human

Resources company. Teens Rosdakarya: Bandung

[16] Arikunto, Suharsimi and Yuliana, Lia. 2009. Education Management. Aditya Media and Faculty of Education UNY. Yogyakarta

[17] Arthur, MB, Hall, DT & Lawrence, BS (1989).

Generating new directions in career theory: The case for a transdisciplinary approach. In MB Arthur, DT Hall, & BS Lawrence (Eds.), Handbook of career theory (pp. 7-25). Cambridge, UK: Cambridge University Press.

[18] Assauri, Sofjan. 2010. Marketing Management:

Basics, Concepts & Strategies. Jakarta: Raja Grafindo Persada.

[19] Assauri, S. ( 2014 ). Marketing Management,

Jakarta: Rajawali Pers

[20] Atmosudirjo. 2010. Basic-Da Sar Science Administration. Ghalia Indonesia. Jakarta.

[21] Azwar, S. 1997. Reliability and Validity.

Yogyakarta: Student Literature

[22] Central Bureau of Statistics (BPS) in 2010 the number of Muslim population in Indonesia

[23] Barnes, James G., (2003). Secrets Of Customer

Relationship Management, ANDI, Yogyakarta.

[24] Bank Indonesia. 1998. Law Number 10 Year 1998 concerning Amendment of Law no. 7 of 1992 concerning Banking. Jakarta: Gramedia

[25] Bank Indonesia. 2002. Blueprint for Sharia Banking

Development. http: // www. bi.go.id. Retrieved April 20, 2012.

[26] Bank Indonesia and the Financial Services

Authority. Indonesian Banking Statistics (datas

throughout the period 2010-2014). www.bi.go.id and www.ojk.go.id.

[27] Bernhardt & Christopher, PC 2006. Profit sharing

(with workers) facilitates collusion (among firms). RAND Journal of Economics. RAND Corporation.

[28] Boulding, William, et al. (1993) A Dynamic Process

Model Of Service Quality: From Expectations to Behavioral Intantions. Journal of Marketing Research, Vol. XXX (February), 7-27.

[29] Boshoff, C. and B. Gray. (2004). The Relationships

Between Service Quality, Customer Satisfaction and Buying Intentions in The Private Hospital Industry. South African Journal of Business Management. Vol. 35. pg. 27-37

[30] Caruana, A., and Msida. (2002). Effects of Service

Quality And The Mediating Role of Customer Satisfaction. European Journal of Marketing.Vol. 36, 811-82

[31] C. Mowen, John. Michael Minor. 2002. Consumer

Behavior. Jakarta. Erland

[32] Charles W. Lamb, Joseph F. Hair, Carl Mcdaniel. 2011. Marketing. Salemba Four, Jakarta.

[33] Daryanto. 2011. Marketing Management: Sari

Kuliah. Bandung: One Nusa.

[34] Davis, Keith. 2010. Organizational Behavior - Human Behavior at Work 13th Edition. New Delhi: Mcgraw Hill Company

[35] Ministry of Religious Affairs, Al - Qur'an and

Terjemahnya, (Jakarta, CV Bumirestu, 1990. Al-Quran Surah al-Imran verse 159.

[36] Dendawijaya, Lukman, 2005. Banking

Management, Second Edition, Second Print, Ghalia Indonesia, Bogor Jakarta

[37] Duggirala et al., 2008. Patient-Perceived

Dimensions Of Total Quality Services In Healtheare. Benchmarking: An Inetrnational Journal, 15 (5): 560-583

[38] Engel, Blackwell, and Miniard. 1994. Consumer

behavior. Jakarta: Binarupa. Script.

[39] Engel. James.F.Roger. D.Black Well And Paul.W.Miniard, 1995., Consumer Behavior.Jakarta.Bina RupaAksara.Hal. 3.

[40] Fatwa of the National Sharia Board-MUI. 2003.

Syariah-Based Islamic Accounting PSAK Syariah.

[41] Fandy Tjiptono, 1997, Marketing Strategy, Issue 1, Andi Publisher, Yogyakarta.

INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 7, ISSUE 9, SEPTEMBER 2018 ISSN 2277-8616

158 IJSTR©2018 www.ijstr.org

[42] Fandy Tjiptono, 2005, Service Marketing, First edition, Yogyakarta; Publisher. Bayumedia Publishing

[43] Fandy Tjiptono. 2006. Service Management. First

Edition. Yogyakarta: Andi. Gerry Ramadhan.

[44] Febi Kurniawan. 2015. Basic Coaching Science. Bandung: CV Alfabeta

[45] Fitzsimmons, James A, and Mona J. Fitzsimmons,

1994, Service Management for Competitive Advantage, New York: Mc. Graw Hill International Edition, 1994.

[46] Freddy Rangkuti. ( 2003 ). SWOT Analysis

Techniques Dissecting Business Cases. Jakarta. Gramedia Pustaka Utama

[47] Hansen Flemming, ( 1972 ), Consumer Behavior: A

Cognitive Behavior Theory. New York: The Free Press.

[48] Hall, et al., 1989. Theories of Personality. New

York: John Welly & Sons.

[49] Husein, Umar, 1999, Human Resources Research In Organization, Jakarta: PT Gramedia Pustaka Utama,

[50] Husein Umar. (2003). Marketing Research and

Consumer Behavior, PT. Gramedia Pustaka Utama, Jakarta.

[51] Hurriyati, Ratih. 2010. Marketing Mix and

Consumer Loyalty. Alfabeta, Bandung

[52] Hofstede, Geert 1997. Cultures and Organizations Software Of The Mind. New York: McGrow Hill

[53] Garvin, David. 1994. Product Quality: Important

Strategy Tool, Jakarta: Free Press.

[54] Gounaris, Spiros P., Vlassis Stathakopoulos, and Antreas D. Athanassopoulos, 2003. Antecedents to perceive service Quality: an Exploratory Study in The Bank of Indusry, International Journal of Banking Industry, 21, 4/5, 168-190

[55] Indriyo Gitosudarmo & Agus Mulyono. 2001. Basic

Principles of Management Edition 3.Yogyakarta: BP

[56] Indonesia, Investment. 2017”Islam in Indonesia".

www. Indonesia-investments.com, accessed January 5, 2017.

[57] Joesron, Tati Suhartati and Fathorrozi. 2003.

Theory of Microeconomics Equipped. Some Form of Production Function. Jakarta: Salemba Four.

[58] Cashmere. 2008. Bank and Other Financial Institutions.Edisi Revisi 2008.Jakarta: PT.Rajagrafindo Persada.

[59] Cashmere. ( 2012 ), Financial Statement Analysis.

Jakarta: PT. Raja Grafindo Persada.

[60] Kartajaya Hermawan, 2009.New Wave Marketing, The World is Still Round The Market is Already Flat.Gramedia. Indonesia

[61] Khaliq, Ilham & Marnis. 2015.Pengaruh

Organizational Culture, Work Discipline and Leadership on Employee Performance At Regional Secretariat of Indragiri Hulu Regency. Journal of Business Management Tepak, Vol. VII, No.1

[62] Kotler, Philip. 2000. Principles - Marketing

Management Principles, Jakarta: Prenhalindo

[63] Kotler, Philip., And Gary Armstrong., 2004, Marketing Basics, 9th Edition, Volume 1, translated by Alexander Sindoro, Jakarta: Index

[64] Kotler, Philip. 2005, Marketing Management,

Volume I and II, PT. Index, Jakarta

[65] Kotler, Philip and Kevin Lane Keller., 2007, Marketing Management, Twelfth Edition, Volume 1, translated by Benjamin Molan, Jakarta: PT Index

[66] Kotler, Philip. 2008. Marketing Management Issue

12 Volume 2. Jakarta: Index

[67] Kotler and Keller. 2009. Marketing Management. Volume I. 13th Edition Jakarta: Erlangg a.

[68] Kotler, philip & Keller, KL (2009). Marketing

Management. Issue 13. Volume 1. Jakarta: Erland

[69] Kotle r, Philip and Gary Armstron g. 2012. Marketing Principles. Edition. 13. Volume 1. Jakarta: Erland.

[70] Kotabe, Masaaki and Helsen, Kristiaan. 2007.

Global Marketing Management.4thEd., John Wiley & Sons, Inc., Danvers

[71] Koentjaraningrat. 1984. Javanese culture. Jakarta:

PN. Balai Pustaka

[72] Krajewski, Lee J., Larry P. Ritzman, 2002, Operations Management (Strategy and Analysis), 6thed., New Jersey: Prentice Hall

[73] Lamb, Chales W., Joseph Hair, and McDaniel,

2011, Marketing, First Book, Translator: David Octarevia, Jakarta: Publisher Salemba Four

[74] Lalromawia, K., & Venkata R. 2013. Title An

Emperical Study Of The Impact Of Marketing Mix Factor On Tourist Satisfaction: A Case Of Selected

INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 7, ISSUE 9, SEPTEMBER 2018 ISSN 2277-8616

159 IJSTR©2018 www.ijstr.org

Three States In India. International Journal Of Business Strategy, l (1), 87-94.

[75] Lovelock, HC and Wright, KL, 2005., Marketing

Services Management., Interpreting

[76] Lovelock Christopher. et. Al, (2013), Marketing Services, Issue 7, Volume 1, Erland: Jakarta

[77] Lupiyoadi, Rambat, (2013): Marketing

Management Services. Jakarta: Salemba Four

[78] Lovelock, Christopher., Et. Al. (2011). Services Marketing: People, Technology, Strategy Volume 1 -7 / E. Jakarta: Erland

[79] Lovelock, Christoper. Et. 2013. Marketing

Management Services - Indonesia's seventh edition of volumes 2. Translation, Dian Wulandari and Devri Barnadi Putera. Publisher Erlangga. Jakarta

[80] Moh. Nazir, Ph.D. 1983. Research methods. PT.

Ghalia Indonesia.

[81] Mudie, Peter and Pirrie, Angela. 2006. Services Marketing Management (Third Edition). Burlington. Elsevier Butterworth-Heinemann

[82] Nurlaeli, Ida & Surya, Mintaraga Eman.”Religious

Behavior and Development of Sharia Banking." Islamadina (2015): 67-83. http://jurnalnasional.ump.ac.id/index.php/ISLAMADINA/article/view/1664 accessed on November 11, 2017

[83] Otler, Philip, 2007, Marketing Management,

Volume 2, Issue 12, PT Index., New Jersey

[84] Otani, KA and Kurz, RS 2004. The Impact of Nursing Care and Other Healthcare Attributes on Hospitalized Patient Satisfaction and Behavioral Intentions. Journal of Healthcare Management. Vol. 49, Pp. 181-97

[85] Oliver, Richard, 1993, A Conceptual Model of

Service Quality and Service Satisfaction; Compatible Goal, Different Concept, in Advance in Service Marketing and Management, Vol 2; p. 65 - 85

[86] Oliver, Riscrd L, ( 1997 ), Satisfaction A Behavioral

Perspective On The. Consumer. McGraw-Hill Education, Singapore.

[87] Parasuraman, Et, al., (1988), Zeithmal and Bitner

(1996), Concepts and Techniques for Measuring Product Quality, Business and Management, Vol 4, No I, Page 55-56.

[88] Padma et al., 2010. Services Quality and Its Impact

on Customer Safisfaction in Indian Hospitals. 807-

841. Bechamarking: An International Journal, Volume 17 No. 6

[89] Prasetijo, R. and JJO IhalauW. 2004. Consumer

Behavior. Andi Offset. Yogyakarta

[90] Rangkuti, F., 2009, Creative Promotion Strategy, First Edition, First Print, Jakarta: Gramedia Pustaka Utama

[91] Riadh. 2009.”Service Quality, Emotional

Satisfaction and Behavioral Intentions A Study In The Hotel Industry". Emerald Group Publishing Limited Vol. 19 No. 3, Canada: Faculty of Business Administration Laval University Que bec

[92] Rao, KM, et al,. (2006). Diet and nutritional status

of adolescent tribal population in nine States of India. Asia Pac J Clin Nutr, 15 (1): 64-71. Retrieved June 26, 2014, from http: //apcjn.nhri.org.tw/server/APJCN/15/1/64.pdf

[93] Rohini, R., B. Mahadevappa. 2006. Service Quality

in Bangalore Hospitals: An Empirical Study. Journal of Services Research. 6 (1): 59-84.

[94] Roni Andespa. 2017. Journal of Financial

Institutions and Banking-Volume 2, Number 1, January-June 2017

[95] Rosdiana Ita. 2011. Effect of Marketing Mix

Strategy Muamalat Savings Against Customer Satisfaction Level Bank Muamalat Indonesia Branch Bumi Serpong Damai Tangerang, Journal Management, UIN Syarif Hidayatullah. Jakarta

[96] R. Vandamme, J. Leunis, (1993)”Development of a

Multiple - item Scale for Measuring Hospital Service Quality", International Journal of Sustainability Industry Management, Vol. 4 Issue: 3, pp.30-49, https://doi.org/10.1108/09564239310041661

[97] Sagiyanto, Asriyani. (2014). Integrated Marketing

Communication Strategy Jacloth Summer Festival 2014. Journal of Communicators, Vol. 6, No. 2. 167-178.

[98] Saladin, Djaslim, 2003,”Marketing Essence and

Elements of Marketing", Third Print, Bandung: Linda Karya Schiffman and Kanuk. 2008. Consumer behavior. Issue 7. Jakarta: Index

[99] Shyh-Jane Li, Yu-Ying Huang, Miles M. Yang.

(2010). How satisfaction modifies the strength of the influence of perceived service quality on behavioral intentions. Journal of Leadership in Health Services. 24 (2). 91-105

[100] Singarimbun, Masri.1995. Survey Research

Method. LP3S, Jakarta

INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 7, ISSUE 9, SEPTEMBER 2018 ISSN 2277-8616

160 IJSTR©2018 www.ijstr.org

[101] Singarimbun, Masri and Sofian Effendi. 1989. Survey Research Methods. LP3ES. Jakarta.

[102] Solimun. 2010. Multivariate Analysis of Structural

Modeling of Partial Least Square-PLS Methods. CV Publisher. Image: Malang

[103] Suseno, Indro Kimpling. (2009). Good thing Big

Business event organizer. Yogyakarta: Galang Press.

[104] Suharto, Edi. 2014. Building People Empowering

Communities. Bandung: Publisher PT Refika Aditama.

[105] Sugiyono, Prof., Dr., 1999, Business Research

Methods, 6th Print, Bandung, CV. Alpha Beta

[106] Sumarwan, Ujang, et al. 2010. Strategic Marketing (Prespective Value-Based Marketing & Performance Pebgukurab). IPB Pres. Bogor

[107] Suminto. 2004. APBN Management in the State

Financial Management System. Jakarta: DG of Budget, MOF.

[108] Marketing Strategy, 3rd Edition, ANDI: Yogyakarta.

Alma, Buchari, 2007, Marketing Management and Service Marketing, Revised Edition, Alfabeta: Bandung. Kotler, Philip and Keller, Kevin L., 2007, Marketing Management, Issue 12, Index: Jakarta.

[109] Trenholm, Sarah & Arthur Jensen, 1995.

Interpersonal Communication (California: Wadswort,) Uhlenbeck, EM 1982. The study of word classes in javanese. Jakarta

[110] Law of the Republic of Indonesia Number 10 of

1998 dated November 10, 1998 on Banking

[111] Law No.23 of 1999 and Act No.3 of 200 4 concerning Bank Indonesia

[112] Ujang Sumarwan. 2004. Consumer Behavior

Theory and Its Application in the Mind. Bogor: Ghalia Indonesia Publisher.

[113] Uhya, Acik Almaknunin. 2013. Factors Affecting

Customer's Behavior in Choosing Funding Services Ba'i Bitsaman Ajil in BMT Heroes (POKUSMA) Notorejo Gondang Tulungagung. STAIN Tulungagung. World Islamic Banking Competitiveness Report 2013-2014

[114] Wirdyaningsih. ( 2005 ). Bank and Islamic

Insurance in Indonesia.Jakarta: Prenada. Media

[115] Zeithaml, V.et al.1990.Delivering Quality.5thEdition, Free Press A Division of Macmillan Inc.

[116] Zeithaml. Valarie, Bitner & Gremler. 2000. Service

Marketing. Singapore: McGraw-Hill Companies Inc.

[117] Zeithaml and Bitner (2001). Services Marketing: Integrating Customer Focus Across the Firm. International Edition. McGraw-Hill, United Stated of America.

[118] Zeithaml, Valarie A. and Bitner, Mary Jo. Service

Marketing. McGraw Hill Inc., Int'l Edition, 2003 New York.