Interest Rate Risk and Financing Choices Prof. Ian Giddy New York University Treasury 2000 NYU/GTA.

39

Interest Rate Risk and Financing Choices Prof. Ian Giddy New York University Treasury 2000 NYU/GTA

-

date post

19-Dec-2015 -

Category

Documents

-

view

217 -

download

1

Transcript of Interest Rate Risk and Financing Choices Prof. Ian Giddy New York University Treasury 2000 NYU/GTA.

Interest Rate Riskand Financing Choices

Prof. Ian GiddyNew York University

Treasury 2000

NYU/GTA

Copyright ©1999 Ian H. Giddy Interest Risk Management -2

Financial Risk Management

Why does it matter? Why and when should we hedge? What should we hedge? How should we

gauge exposure?

Financial risk management must be tied to the company’s business

Copyright ©1999 Ian H. Giddy Interest Risk Management -3

IBM’s Interest Rate Exposure

Copyright ©1999 Ian H. Giddy Interest Risk Management -4

Corporate Finance

CORPORATE FINANCE

DECISONS

CORPORATE FINANCE

DECISONS

INVESTMENTINVESTMENT RISK MGTRISK MGTFINANCINGFINANCING

CAPITAL

PORTFOLIO

M&ADEBT EQUITY

TOOLS

MEASUREMENT

Copyright ©1999 Ian H. Giddy Interest Risk Management -5

Corporate Finance

CORPORATE FINANCE

DECISONS

CORPORATE FINANCE

DECISONS

INVESTMENTINVESTMENT RISK MGTRISK MGTFINANCINGFINANCING

CAPITAL

PORTFOLIO

M&ADEBT EQUITY

TOOLS

MEASUREMENT

Copyright ©1999 Ian H. Giddy Interest Risk Management -6

Corporate Finance

CORPORATE FINANCE

DECISONS

CORPORATE FINANCE

DECISONS

INVESTMENTINVESTMENT RISK MGTRISK MGTFINANCINGFINANCING

CAPITAL

PORTFOLIO

M&ADEBT EQUITY

TOOLS

MEASUREMENT

Copyright ©1999 Ian H. Giddy Interest Risk Management -7

Corporate Finance

CORPORATE FINANCE

DECISONS

CORPORATE FINANCE

DECISONS

INVESTMENTINVESTMENT RISK MGTRISK MGTFINANCINGFINANCING

CAPITAL

PORTFOLIO

M&ADEBT EQUITY

TOOLS

MEASUREMENT

INVESTMENT

FINANCINGRISK

MANAGEMENT

Copyright ©1999 Ian H. Giddy Interest Risk Management -8

Financing Choices

Assets’ value is the present value of the cash flows from the real business of the firm

Value of the firm

=PV(Cash Flows)

From

How much debt?

to

What kind of debt?

You cannot change the value of the

real business just by shuffling paper

- Modigliani-Miller

Copyright ©1999 Ian H. Giddy Interest Risk Management -9

Corporate Financing Choices:What Kind of Debt?

Fixed/floating Currency of denomination Maturity or availability Domestic/Euro Public/private Asset-based Credit enhanced Swapped Equity-linked

Ciba-Geigy: What Kind of Debt?

Copyright ©1999 Ian H. Giddy Interest Risk Management -11

Short Term or Long Term?

In 1992, Ciba had fixed assets of SF13.9 billion and capital expenditures of SF1.9 billion.

Yet the majority of Ciba's debt is in the short-term commercial paper, bank debt, and suppliers-credit markets.

This suggests that if the proportion of debt financing as a whole is increased, much of it should be in the form of long-term debt.

Copyright ©1999 Ian H. Giddy Interest Risk Management -12

Geographic location of sales and capital assets.

Currency distribution of sales. Nature of the company's businesses

Currency of Denomination of Ciba's Debt? What Should It Be?

Copyright ©1999 Ian H. Giddy Interest Risk Management -13

Currency of Ciba’s Assets and Debt

Geographic distributionof

Currencydistribution

of sales Remarks on economic exposure

Estimatedcurrency

distribution ofdebt

Fixedassets Sales

Switzerland 41%

43%

2.4% Net short position because much ofproduction, but little of sales, here

9%

U.K.

27%

5.4% Part of sales effectively U.S. dollardenominated

7%

OtherEurope

34.6% 21%

U.S. andCanada

23% 32% 41.3% 54%

LatinAmerica

4% 7% 5.3% Most of sales effectively dollardenominated

2%

Asia 4% 13% 10.9% Part of sales effectively U.S. dollardenominated

6%

Rest of theworld

1% 5% Most of sales effectively dollardenominated

1%

Geographic distributionof

Currencydistribution

of sales Remarks on economic exposure

Estimatedcurrency

distribution ofdebt

Fixedassets Sales

Switzerland 41%

2.4% Net short position because much ofproduction, but little of sales, here

9%

U.K.

27%

5.4% Part of sales effectively U.S. dollardenominated

7%

OtherEurope

34.6% 21%

U.S. andCanada

23% 32% 41.3% 54%

LatinAmerica

4% 7% 5.3% Most of sales effectively dollardenominated

2%

Asia 4% 13% 10.9% Part of sales effectively U.S. dollardenominated

6%

Rest of theworld

1% 5% Most of sales effectively dollardenominated

1%

Copyright ©1999 Ian H. Giddy Interest Risk Management -14

What Kind of Debt? Some Considerations Fixed/floating:

How certain are the cash flows? Are operating profits linked to interest rates or inflation?

Currency:Consider currency of the assets: currency of

denomination vs. currency of location vs. currency of determination.

Maturity or availability:Are the assets short term or long term? Should the

firm assume ease of refinancing, or buy an option on access to financing?

Copyright ©1999 Ian H. Giddy Interest Risk Management -15

Guidelines for Financing

Liabilities to match assets: economic exposure of the firm determines base financing choices.

Decision on whether or not to fully match depends on company's view relative to the view implied by market prices.

When strategy is chosen, use the financing/hedging techniques that offer the lowest effective cost.

Copyright ©1999 Ian H. Giddy Interest Risk Management -16

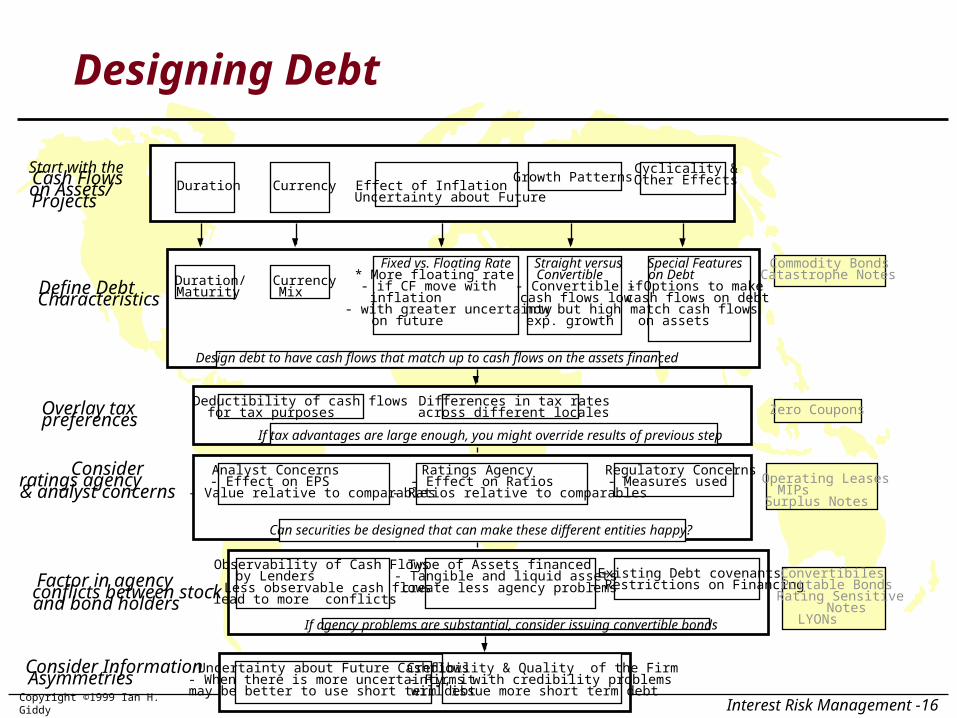

Designing Debt

Duration Currency Effect of InflationUncertainty about Future

Growth PatternsCyclicality &Other Effects

Define DebtCharacteristics

Duration/Maturity

CurrencyMix

Fixed vs. Floating Rate* More floating rate - if CF move with inflation- with greater uncertainty on future

Straight versusConvertible- Convertible ifcash flows low now but highexp. growth

Special Featureson Debt- Options to make cash flows on debt match cash flows on assets

Start with the Cash Flowson Assets/Projects

Overlay taxpreferences

Deductibility of cash flowsfor tax purposes

Differences in tax ratesacross different locales

Consider ratings agency& analyst concerns

Analyst Concerns- Effect on EPS- Value relative to comparables

Ratings Agency- Effect on Ratios- Ratios relative to comparables

Regulatory Concerns- Measures used

Factor in agencyconflicts between stockand bond holders

Observability of Cash Flowsby Lenders- Less observable cash flows lead to more conflicts

Type of Assets financed- Tangible and liquid assets create less agency problems

Existing Debt covenants- Restrictions on Financing

Consider Information Asymmetries

Uncertainty about Future Cashflows- When there is more uncertainty, itmay be better to use short term debt

Credibility & Quality of the Firm- Firms with credibility problemswill issue more short term debt

If agency problems are substantial, consider issuing convertible bonds

Can securities be designed that can make these different entities happy?

If tax advantages are large enough, you might override results of previous step

Zero Coupons

Operating LeasesMIPsSurplus Notes

ConvertibilesPuttable BondsRating Sensitive

NotesLYONs

Commodity BondsCatastrophe Notes

Design debt to have cash flows that match up to cash flows on the assets financed

Copyright ©1999 Ian H. Giddy Interest Risk Management -17

What is a Corporation’s Sensitivity to Interest Rate Changes?

The answer to this question is important because it it provides a measure of the duration of the

firm’s projectsit provides insight into whether the firm

should be using fixed or floating rate debt.

Copyright ©1999 Ian H. Giddy Interest Risk Management -18

Interest Rate Risk:Portfolio

Portfolio risk: interest rate fluctuations can affect the value of a bond investment portfolio

Bond price fluctuations will affect the balance sheet

Can be hedged, using duration as a risk/sensitivity measurement tool

Can be hedged with futures, bond options, and swaps.

Copyright ©1999 Ian H. Giddy Interest Risk Management -19

Pepsico Pension

Assets (each $10m):2-year GNMA6-year, 8% T-note12-year asset-

backed corporate

Pension liabilities:$100m 2 years$120m 5 years$85m 10 years

What is Pepsico pension fund’s risk? Duration of the assets (+ve)Duration of the liabilities (-ve)Net duration is the risk to be hedged!

Copyright ©1999 Ian H. Giddy Interest Risk Management -20

The Price-Yield Relationship

But plotting price vs yield shows that the relationship is non-linear:

100

9%

Price of a 9% bond

Copyright ©1999 Ian H. Giddy Interest Risk Management -21

Duration as a Measure of Price Sensitivity

Duration measures the % price change for a given change in yield:

PRICE

YIELD9%

100

The steeper the line, the more the price falls for a given rise in yield

Copyright ©1999 Ian H. Giddy Interest Risk Management -22

Greater Duration, Greater Risk

Duration is measured as the PV-weighted average life, so low-coupon bonds have greater duration

PRICE

YIELD9%

100

6% BOND

9% BOND

0% BOND

Copyright ©1999 Ian H. Giddy Interest Risk Management -23

Calculating Duration:MacCauley and Modified

D

tCFr

P

D PdP

P

D

r

MAC

tt

t

n

MOD

( )

%( )

1

1

1

Copyright ©1999 Ian H. Giddy Interest Risk Management -24

Calculating Modified Duration:Shortcut Method

ApproxD PP P

P yieldMOD %

( )( )

2 0

The average percentage price change, relative to the initial price, per 1-basis-point change in yield:

Copyright ©1999 Ian H. Giddy Interest Risk Management -25

Duration: An Excel Spreadsheet

Yield 8.0%

Bond A Time (year) 0.5 1 1.5 2Cash-Flows 4 4 4 104PV of CFs 3.84615 3.6982 3.556 88.9Price 100Weighted CFs 4 8 12 416PV of weighted CFs 3.84615 7.3964 10.668 355.6Sum of weight. CFs 377.509Semiannual duration 3.77509Macaulay duration is1.88755Modified 1.74773

Copyright ©1999 Ian H. Giddy Interest Risk Management -26

Assets (each $10m):1-year E$ deposit5-year, 6% T-note

Duration=4.69-year Strip

Fixed liabilities:$10m 3 years$10m 5 years$10m 7 years

Pension Fund’s risk? Asset Duration = 10(1%)+10(4.6%)+10(9%)Liab Duration = 10(3%)+10(5%)+10(7%)Net duration is 1.46-1.50 = -4m

Pension Fund, simplified

Copyright ©1999 Ian H. Giddy Interest Risk Management -27

Do Corporations Have Durations?

:Firm Value

Rates

Copyright ©1999 Ian H. Giddy Interest Risk Management -28

Firm Value versus Interest Rate Changes: Walt Disney Regressing changes in firm value against

changes in interest rates yields the following regression –

Change in Firm Value = 0.22 - 7.43 ( Change in Interest Rates)

Conclusion: The duration (interest rate sensitivity) of Disney’s asset values is about 7.43 years. Consequently, its debt should have at least as long a duration.

Copyright ©1999 Ian H. Giddy Interest Risk Management -29

Why the coefficient on the regression is duration..

The duration of a straight bond or loan issued by a company can be written in terms of the coupons (interest payments) on the bond (loan) and the face value of the bond to be –

Duration of Bond = dP/dr =

t * Coupon t

(1+ r) tt =1

t= N

N* Face Value

(1+ r)N

Coupon t

(1+ r) tt=1

t =N

Face Value

(1+ r)N

Copyright ©1999 Ian H. Giddy Interest Risk Management -30

Duration of a Firm’s Assets

This measure of duration can be extended to any asset with expected cash flows on it. Thus, the duration of a project or asset can be estimated in terms of the pre-debt operating cash flows on that project.

Duration of Project/Asset = dPV/dr =

t *CFt

(1+ r)tt=1

t = N

N * Terminal Value

(1 + r)N

CFt

(1 + r)tt =1

t= N

Terminal Value

(1 + r)N

Copyright ©1999 Ian H. Giddy Interest Risk Management -31

Duration of Disney Theme Park(Based on Cash Flow Projections)

Year FCFF Terminal Value Total FCFF PV of FCFF PV * t

1 ($39,078 Bt) ($39,078 Bt) (31,180 Bt) -31180.4

2 ($36,199 Bt) ($36,199 Bt) (23,046 Bt) -46092.4

3 ($11,759 Bt) ($11,759 Bt) (5,973 Bt) -17920

4 16,155 Bt 16,155 Bt 6,548 Bt 26193.29

5 21,548 Bt 21,548 Bt 6,969 Bt 34844.55

6 33,109 Bt 33,109 Bt 8,544 Bt 51264.53

7 46,692 Bt 46,692 Bt 9,614 Bt 67299.02

8 58,169 Bt 58,169 Bt 9,557 Bt 76454.39

9 70,423 Bt 838,720 Bt 909,143 Bt 119,182 Bt 1072635

Sum 100,214 Bt 1,233,498

Duration of the Project = 1,233,498/100,214 = 12.30 years

Copyright ©1999 Ian H. Giddy Interest Risk Management -32

Duration: Comparing Approaches

P/r=Percentage Change in Value for apercentage change in Interest Rates

Traditional DurationMeasures

Regression:

P = a + b (r)

Uses:1. Projected Cash FlowsAssumes:1. Cash Flows are unaffected by changes in interest rates2. Changes in interest rates are small.

Uses:1. Historical data on changes in firm value (market) and interest ratesAssumes:1. Past project cash flows are similar to future project cash flows.2. Relationship between cash flows and interest rates is stable.3. Changes in market value reflect changes in the value of the firm.

Copyright ©1999 Ian H. Giddy Interest Risk Management -33

Interest Rate Risk: Economic

Economic risk arises from the real business risk of the company, insofar as it is tied to market interest rates

It affects the shareholder value, but may be difficult to quantify

It can often be hedged using forwards, futures or interest-rate swaps.

Example: Cincinnati Constr. Co. uses collar to hedge its interest cost; this is consistent with its business risk.

Copyright ©1999 Ian H. Giddy Interest Risk Management -34

Liberty Travel

Liberty is afraid of a higher cost of funds in the future. Should it:Borrow at 8.85% for 3 years?Fix the cost for the next quarter with

an FRA (at 6.125%+1.85%)?Fix the cost for 3 years with an

interest rate swap at an effective cost of 8.82% (6.97%+1.85%=8.82%)?

Use futures (at 6.07%+1.85%)?Do nothing?

Copyright ©1999 Ian H. Giddy Interest Risk Management -35

Three Views of Interest Rate Risk

Transactions

Exposure

Transactions

Exposure

Portfolio

Exposure

Portfolio

ExposureEconomic

Exposure

Economic

Exposure

Copyright ©1999 Ian H. Giddy Interest Risk Management -36

Designing Debt

Duration Currency Effect of InflationUncertainty about Future

Growth PatternsCyclicality &Other Effects

Define DebtCharacteristics

Duration/Maturity

CurrencyMix

Fixed vs. Floating Rate* More floating rate - if CF move with inflation- with greater uncertainty on future

Straight versusConvertible- Convertible ifcash flows low now but highexp. growth

Special Featureson Debt- Options to make cash flows on debt match cash flows on assets

Start with the Cash Flowson Assets/Projects

Overlay taxpreferences

Deductibility of cash flowsfor tax purposes

Differences in tax ratesacross different locales

Consider ratings agency& analyst concerns

Analyst Concerns- Effect on EPS- Value relative to comparables

Ratings Agency- Effect on Ratios- Ratios relative to comparables

Regulatory Concerns- Measures used

Factor in agencyconflicts between stockand bond holders

Observability of Cash Flowsby Lenders- Less observable cash flows lead to more conflicts

Type of Assets financed- Tangible and liquid assets create less agency problems

Existing Debt covenants- Restrictions on Financing

Consider Information Asymmetries

Uncertainty about Future Cashflows- When there is more uncertainty, itmay be better to use short term debt

Credibility & Quality of the Firm- Firms with credibility problemswill issue more short term debt

If agency problems are substantial, consider issuing convertible bonds

Can securities be designed that can make these different entities happy?

If tax advantages are large enough, you might override results of previous step

Zero Coupons

Operating LeasesMIPsSurplus Notes

ConvertibilesPuttable BondsRating Sensitive

NotesLYONs

Commodity BondsCatastrophe Notes

Design debt to have cash flows that match up to cash flows on the assets financed

www.stern.nyu.edu

www.giddy.org