Integration of offshore wind generation in future electricity market s

14

1 Integration of offshore wind generation in future electricity markets Marian Klobasa, Fabio Genoese Fraunhofer Institute for System und Innovation Research European Offshore Wind Conference Stockholm, 16th September 2009 Alpha ventus Pressebild, July 2009

-

Upload

rana-langley -

Category

Documents

-

view

35 -

download

1

description

Integration of offshore wind generation in future electricity market s Marian Klobasa, Fabio Genoese Fraunhofer Institute for System und Innovation Research European Offshore Wind Conference Stockholm, 16th September 2009. Alpha ventus Pressebild, July 2009. Agenda. - PowerPoint PPT Presentation

Transcript of Integration of offshore wind generation in future electricity market s

1

Integration of offshore wind generation in future electricity markets

Marian Klobasa, Fabio Genoese

Fraunhofer Institute for System und Innovation Research

European Offshore Wind Conference

Stockholm, 16th September 2009Alpha ventus Pressebild, July 2009

2

Agenda

Characteristic of wind power generation in the North Sea

Fullload hours, periods with high and low wind generation

Methodological approach to analyse impacts on electricity markets

Future spot market prices affected by offshore generation

Influence of grid infrastructure and restrictions

Conclusion

3

Main assumptions for wind time series generation

Wind speed data

Time series generated from weather data (provided by DWD, 180 locations)

Distribution of installed onshore capacity according to DENA study

Adoption of improved power curves and increased hub heights makes it necessary to use wind speed data (data used from 1998, 2000 and 2001)

Power curves for wind turbines

Offshore: Enercon E 126, REPower 5M, Vestas V90 Offshore

Onshore: Enercon E66, E70, E82, E112, REPower 5M

Diffusion of modern turbine types

Increase of typical hub height from 65 m to around 80 m (limited by building-authority approval)

4

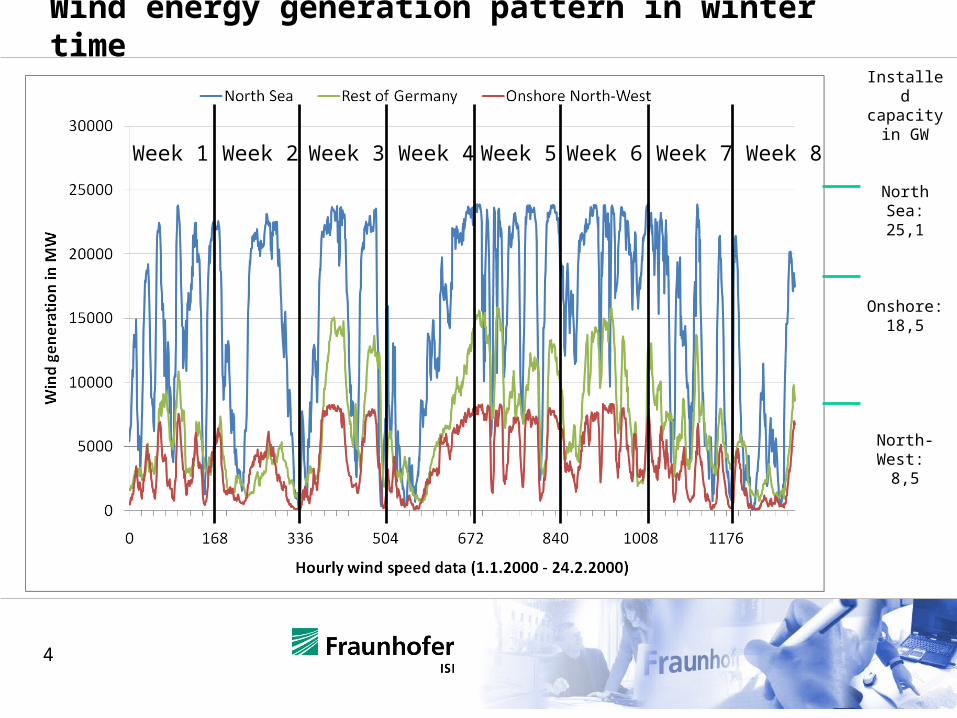

Wind energy generation pattern in winter time

Week 1 Week 2 Week 3 Week 4 Week 5 Week 6 Week 7 Week 8

Installed capacity

in GW

North Sea: 25,1

Onshore: 18,5

North-West: 8,5

5

Wind energy generation pattern in summer time

Week 1Week 2Week 3 Week 4 Week 5Week 6Week 7 Week 8

Installed capacity

in GW

North Sea: 25,1

Onshore: 18,5

North-West: 8,5

6

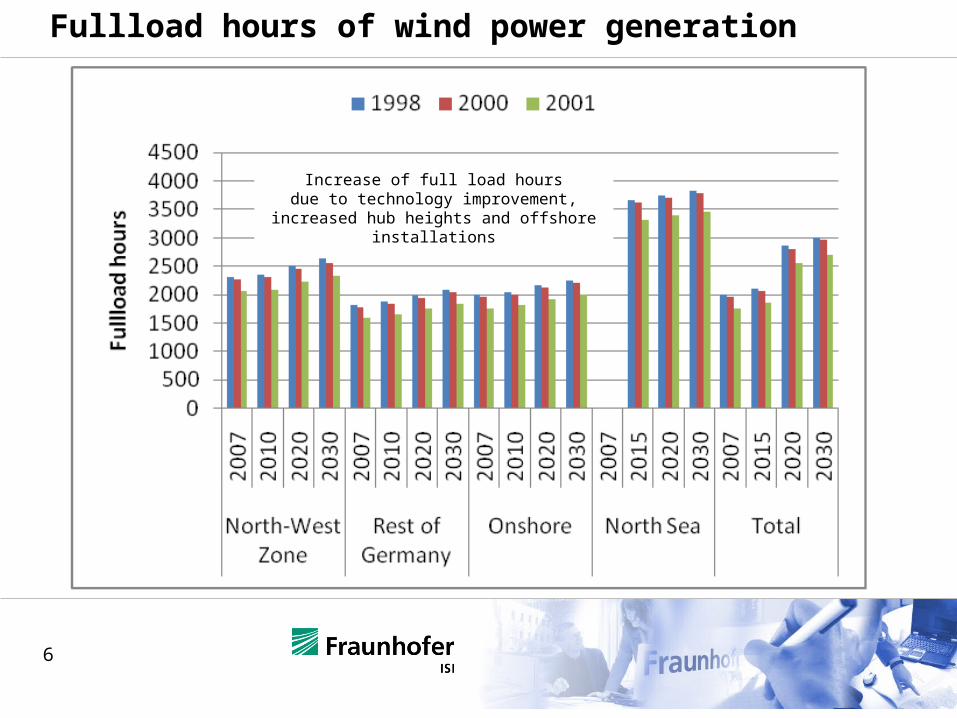

Fullload hours of wind power generation

Increase of full load hoursdue to technology improvement, increased hub

heights and offshore installations

7

Simulation of electricity markets with PowerACE

Agent-based power market model

Hourly time resolution Actors in the electricity sector

are simulated as agents

Main module: PowerACE Spot Market

Hourly auctions Uniform clearing price

auction Resembles EEX

Bidding process Variable costs Strategic costs

Focus on the German market

CO2 Market

0

10

20

30

40

50

hour

Spotmarket

0

10

20

30

40

50

hour

Services

Industry+ Others

Household

Supplier

Contracts

TransportRenewable Agents

load

bids

Gridoperator-Trader

support

load

support

Generator

Supply Trader

merit-order

offer

bid

Primary Reserve Balancing Trader

offer

Gridoperator

bids

Plant DB

plant data

REG-Load DB

REG-Capacity DB

Investment Planner

new plant

offer

CO2 Trader

merit-order

offer

bid

CO2TraderSaving Potential

Industry DB

Load DB

Demand DB

Load-Prognosis

Investment Planner

new plant

offer

bid

co2 balance

load profiles

demand+equipment(HH)

Agents

data

Flows

Database

Markets

Demand

Renewables

Utilities

LegendSecondary Reserve

Minute Reserve

PumpStorageDB

PumpStorageTrader

offer bid

CO2 Market

0

10

20

30

40

50

hour

CO2 Market

0

10

20

30

40

50

hour

Spotmarket

0

10

20

30

40

50

hour

Services

Industry+ Others

Household

Supplier

Contracts

TransportRenewable Agents

load

bids

Gridoperator-Trader

support

load

support

Generator

Supply Trader

merit-order

offer

bid

Primary Reserve Balancing Trader

offer

Gridoperator

bids

Plant DB

plant data

REG-Load DB

REG-Capacity DB

Investment Planner

new plant

offer

CO2 Trader

merit-order

offer

bid

CO2TraderSaving Potential

Industry DB

Load DB

Demand DB

Load-Prognosis

Investment Planner

new plant

offer

bid

co2 balance

load profiles

demand+equipment(HH)

Agents

data

Flows

Database

Markets

Demand

Renewables

Utilities

LegendSecondary Reserve

Minute Reserve

PumpStorageDB

PumpStorageTrader

offer bid

8

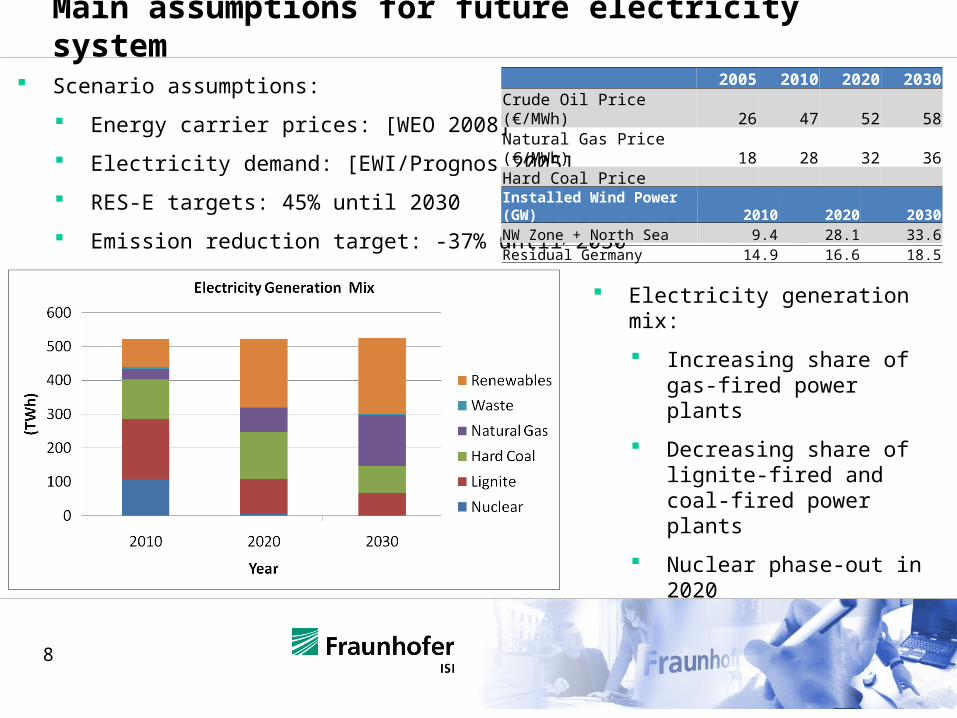

Main assumptions for future electricity system

Scenario assumptions:

Energy carrier prices: [WEO 2008]

Electricity demand: [EWI/Prognos 2005]

RES-E targets: 45% until 2030

Emission reduction target: -37% until 2030

2005 2010 2020 2030Crude Oil Price (€/MWh) 26 47 52 58Natural Gas Price (€/MWh) 18 28 32 36Hard Coal Price (€/MWh) 6 11 11 10Electricity Demand (TWh/a) 547 524 521 522

Electricity generation mix:

Increasing share of gas-fired power plants

Decreasing share of lignite-fired and coal-fired power plants

Nuclear phase-out in 2020

Installed Wind Power (GW) 2010 2020 2030NW Zone + North Sea 9.4 28.1 33.6Residual Germany 14.9 16.6 18.5

9

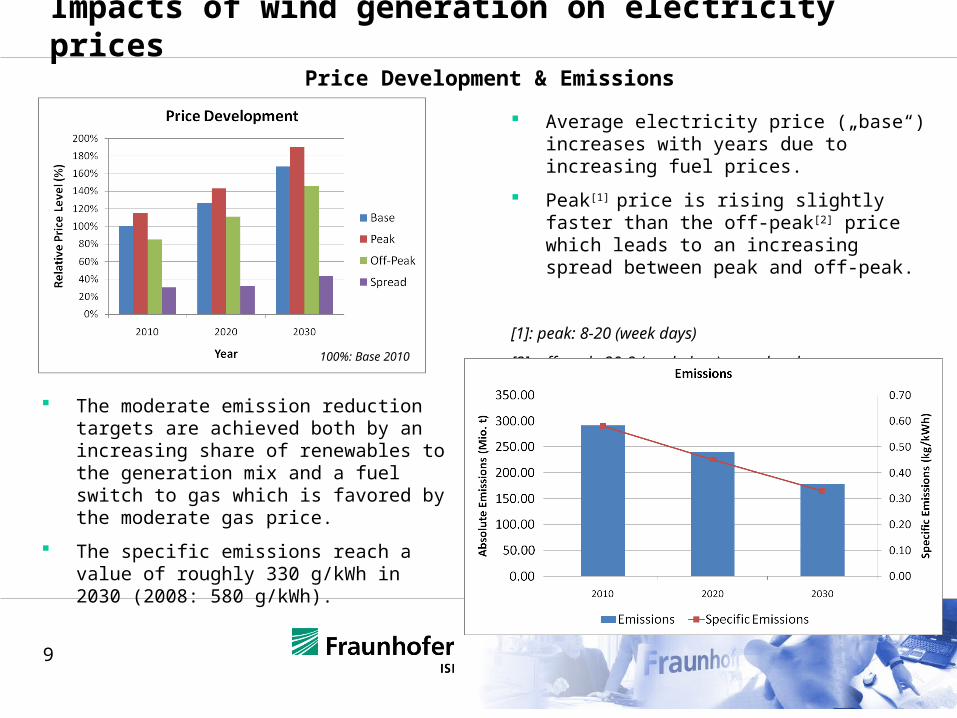

Impacts of wind generation on electricity prices

Price Development & Emissions

Average electricity price („base“) increases with years due to increasing fuel prices.

Peak[1] price is rising slightly faster than the off-peak[2] price which leads to an increasing spread between peak and off-peak.

[1]: peak: 8-20 (week days)

[2]: off-peak: 20-8 (week days) + weekends

The moderate emission reduction targets are achieved both by an increasing share of renewables to the generation mix and a fuel switch to gas which is favored by the moderate gas price.

The specific emissions reach a value of roughly 330 g/kWh in 2030 (2008: 580 g/kWh).

100%: Base 2010

10

Impacts of wind generation on electricity prices

Typical Price Variations

The graphs show the price variation around the average price of the corresponding year.

2010:

relatively low share of renewables: renewable load never exceeds system load

price variation: mostly around ±50%

2030:

higher contribution of renewables: renewable load exceeds system load in some hours

more frequent variations

20302010

11

Influences of grid infrastructure and restrictions Heavy influence expected in NW part of Germany (→

connection of North Sea wind parks)

Market simulation with two zones, limited transmission capacity between the zones

Definition of the zones similar to the Dena grid study

North-Western Zone (Dena: 2)

Residual Germany (Dena: 1,3,4,5,6)

Export capacity of NW zone: ~12 GW

S600 MVA

DK2260 MVA

NL2626 MVA

Münster987 MVA Bielefeld

3448 MVA

Hannover3160 MVA

Zone NWLoad,

Renewables, Thermal

Generation

12

Impacts of grid restrictions on electricity prices

No Grid Restrictions Grid Restrictions: NW Zone

Hours With Negative Residual Load 2010 2020 2030Grid Restrictions / NW Zone 0 1811 2717No Grid Restrictions 0 19 115

Price Level 2010 2020 2030MIN 0% 0% 0%MAX 259% 289% 364%AVG 100% 110% 136%

Price Level 2010 2020 2030MIN 0% 0% 0%MAX 259% 289% 364%AVG 100% 127% 168%

100%: AVG 2010

13

Conclusions Offshore wind generation

3800 fullload hours can be achieved in the North Sea, fullload hours of total wind generation increase from less than 2000 h to almost 3000 h

In winter time longer periods of several days with high wind feed-in. In summer time limited wind feed-in, but periods with high feed-in from offshore locations can occur.

Simulation of German spot market:

high share of renewables, moderate increase of energy carrier prices, increasing share of gas-fired power plants, moderate CO2-prices

Increasing spot market price and increasing price spread between peak and off-peak time

Negative residual demand in 2020 and 2030

~ 100 hours without considering grid restrictions in Germany

~ 2700 hours when considering grid restrictions in Germany

Grid restrictions in North-West Germany

Strong need for grid extensions up to 10 GW out of North-Western Zone

Value of wind feed-in is limited in the North-Western Zone without grid extensions

Further need for political support mechanism for offshore development

Average market prices could be to low to secure investment in offshore locations

Furthermore value of wind is below average market price due to the merit-order effect

14

Contact and further information

Dr. Marian KlobasaFraunhofer Institute for Systems and Innovation Research,

KarlsruheContact:

www.wind-last.de