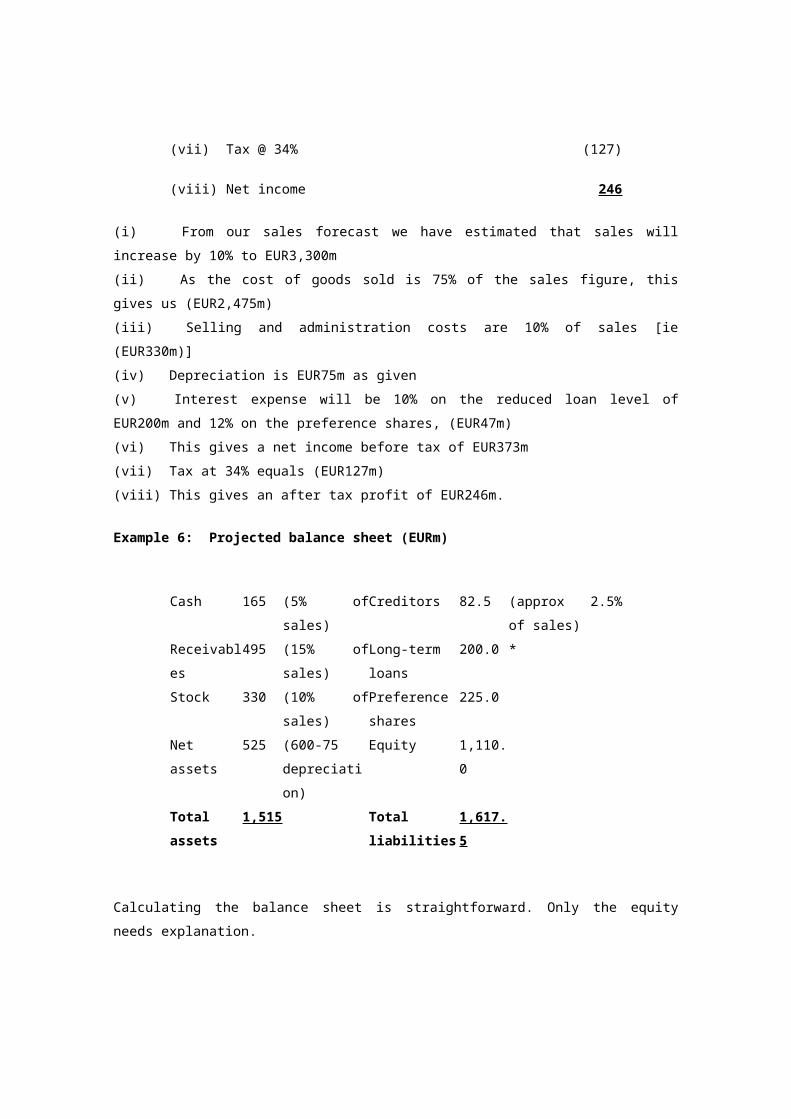

Icm Manual Total

641

Introduction Chapter 1 - Introduction to cash management Overview This chapter looks at the role of the corporate treasurer and introduces a number of definitions of cash management used by companies and banks. Learning Objectives A. To understand the role of treasury in large companies B. To understand what cash management is and how it fits into treasury and impacts on other treasury functions C. To appreciate the benefits of good cash management D. To be aware of the basic bank cash management model 1.1 The role of the treasurer The treasurer's role has been evolving over many years, but it can still be a very different job from company to company. Some treasurers spend most of their time managing cash, while others concentrate on risk; there is also a new breed who are becoming managers of 'working capital' rather than treasury managers in the accepted sense. To some extent, the differences between the treasury role in different companies can be explained with reference to the following: • size; • industry; • country of domicile; • level of international versus domestic business; • corporate culture; • personal style and experience of the treasurer; • corporate history; • life cycle/stage of development and

-

Upload

ho-jing-seok -

Category

Documents

-

view

379 -

download

0

Transcript of Icm Manual Total

Introduction

Chapter 1 - Introduction to cash management

Overview

This chapter looks at the role of the corporate treasurer and introduces a number of definitions

of cash management used by companies and banks.

Learning Objectives

A. To understand the role of treasury in large companies

B. To understand what cash management is and how it fits into treasury and impacts on

other treasury functions

C. To appreciate the benefits of good cash management

D. To be aware of the basic bank cash management model

1.1 The role of the treasurer

The treasurer's role has been evolving over many years, but it can still be a very different job

from company to company. Some treasurers spend most of their time managing cash, while

others concentrate on risk; there is also a new breed who are becoming managers of 'working

capital' rather than treasury managers in the accepted sense. To some extent, the differences

between the treasury role in different companies can be explained with reference to the

following:

• size;

• industry;

• country of domicile;

• level of international versus domestic business;

• corporate culture;

• personal style and experience of the treasurer;

• corporate history;

• life cycle/stage of development and

• the nature of business.

No doubt there are many other factors that influence the role of the treasurer and the staff that

work in his department. In some companies, additional non-treasury responsibilities can be

assigned to the treasurer as well. For example, one airline regards the treasury function as

essentially one of risk management, therefore it is not surprising that this company's treasurer is

also responsible for insurance. Nor is it surprising that the management of commodity risk

becomes important in industries which are closely tied to commodities, such as the oil industry,

or where commodities form a large part of the cost base (ie airlines or confectionery). It is also

fairly common, particularly in those companies where the treasury has developed out of the

chief accountant function, for an accountancy-trained treasurer to be given additional

responsibility for corporate tax. We also see a number of less fathomable company-specific

anomalies. For example, there is one multinational company where the group treasurer also

manages the real estate portfolio!

Although there will always be exceptions, the core responsibilities of treasury can generally be

divided into six broad areas as follows:

1.2 Foreign exchange

At its simplest level, this may be no more than the purchase or sale of currencies against a base

currency. Trades may be done on a standard spot basis (ie usually trade today for settlement

two working days ahead), but in certain cases one day ahead, 'Tomnext', for settlement the day

after the trade or today's settlement. Alternatively, they may be trades in the forward or futures

markets where trades that are fixed today will not settle for many days, weeks, months or even

years. Most of these types of trades will be carried out over the telephone with a bank dealer.

Increasingly, however, trades, particularly for small amounts, can be carried out electronically

with banks and other organisations using a PC and authorised software or via dedicated single

bank or multibank portals. (Dealing systems will be covered in detail in chapter 21 which

includes corporate treasury systems and foreign exchange portals).

1.3 Risk management

Risk management normally refers to two main types of risk in treasury, although the role has

been extended increasingly. The traditional areas of risk management of concern to the

treasurer relate to currency risk and interest rate risk. Currency risk is usually broken down

further into transaction risk, translation risk and economic risk.

Transaction risk is the simplest and most common. These risks relate to the differences

between the foreign exchange rates on the day that a business transaction is entered into and

the prevailing rates on the date of receipt or payment of funds that relate to it. Exchange rates

fluctuate and can either move favourably (resulting in an exchange gain) or adversely (resulting

in a loss). 'Hedging' on the date that the transaction first becomes known to the company will

lock in a fixed rate so that there is no risk to the company.

Translation risk is often referred to as 'balance sheet risk' and usually refers to the revaluation of

a balance sheet or profit and loss item to take account of movements in foreign exchange rates.

These are essentially accounting exposures, rather than relating to real transactions. For

example, the US subsidiary of a UK company earns profits of USD 10m each year. Last year,

the average USD/GBP exchange rate was GBP1 = USD1.50. This year, the US subsidiary

meets its USD10m target, but the average USD/GBP rate has moved to 1.60. This means that

the parent's profit and loss account includes profits from the US subsidiary that, on translation,

are GBP416,667 lower than the previous year. As these are not real gains or losses (ie there is

no cash effect) some companies do not bother to hedge them. On the other hand, other

companies do try to manage translation exposures, especially where movements in the balance

sheet figures give rise to breaches of loan covenants, such as debt/equity ratio levels.

Economic risks are usually associated with competitive strategies that can be used against a

rival company. Although economic exposures may relate to simple differences in cost bases, (ie

the cost of manufacturing clothes in South-East Asia compared with Germany) they can be

complicated by currency movements. If one takes the example of a US-based importer of

clothes from Venezuela and a US manufacturer of the same goods. In a period of steady

appreciation by the dollar, the former will have gained an economic advantage, whereas the

latter will have suffered an economic loss, reflected in either lower margins or, at the extreme,

lost sales.

The other standard area of risk management is interest rate risk. The risk that interest rates will

move against the company, making borrowings more expensive, or reducing returns on

investments. This can be extended to include market risk, ie the risk that the price of an asset

will move against you. This can be due to simple movements in the financial markets, such as

share prices, or a result of the impact of interest rate movements on the value of fixed-interest

instruments.

These types of risks can all be hedged using a variety of financial instruments, and will be

discussed in more detail in chapter 16 in terms of their impact on cash management.

Other types of risk that are increasingly being covered under this heading include: counterparty

risk (the risk that a counterparty will default on a trade or transaction); settlement risk (the risk

that settlement of a particular transaction may not occur); and, systemic risk (the risk that one of

the systems that the company or its bankers use will fail, resulting in a loss to the company).

1.4 Funding

This relates to the management of long-term debt (ie with a maturity in excess of one year). It

may be a simple term loan, or a more sophisticated instrument, such as a bond issue or

redeemable debentures. Debt under one year should be considered as a cash management

function.

1.5 Investments

Similarly, management of investments also refers only to items with a maturity of one year or

greater. Investments maturing in periods of less than one year should be considered a cash

management function.

1.6 Bank relations

This function is different to those listed above because it does not involve any treasury

operations directly. Indeed, it can almost be regarded as the treasury department' s public

relations function. However, the role is sufficiently important that some large companies employ

a dedicated senior treasury professional (often on a full-time basis) to keep its banks advised of

its needs and activities and to provide a focal point for bank negotiations and selection.

Regardless of size, all companies need to keep track of the business it transacts with each

bank, with a view to meeting current and future banking needs. There is also a need to track the

performance of banks and to ensure that the relationship is mutually beneficial. Whether it

adopts a transaction or relationship-based approach to purchasing bank services, the exact

form of a company' s relationship with its banks is a frequently discussed subject and never

more so than at times of reduced liquidity.

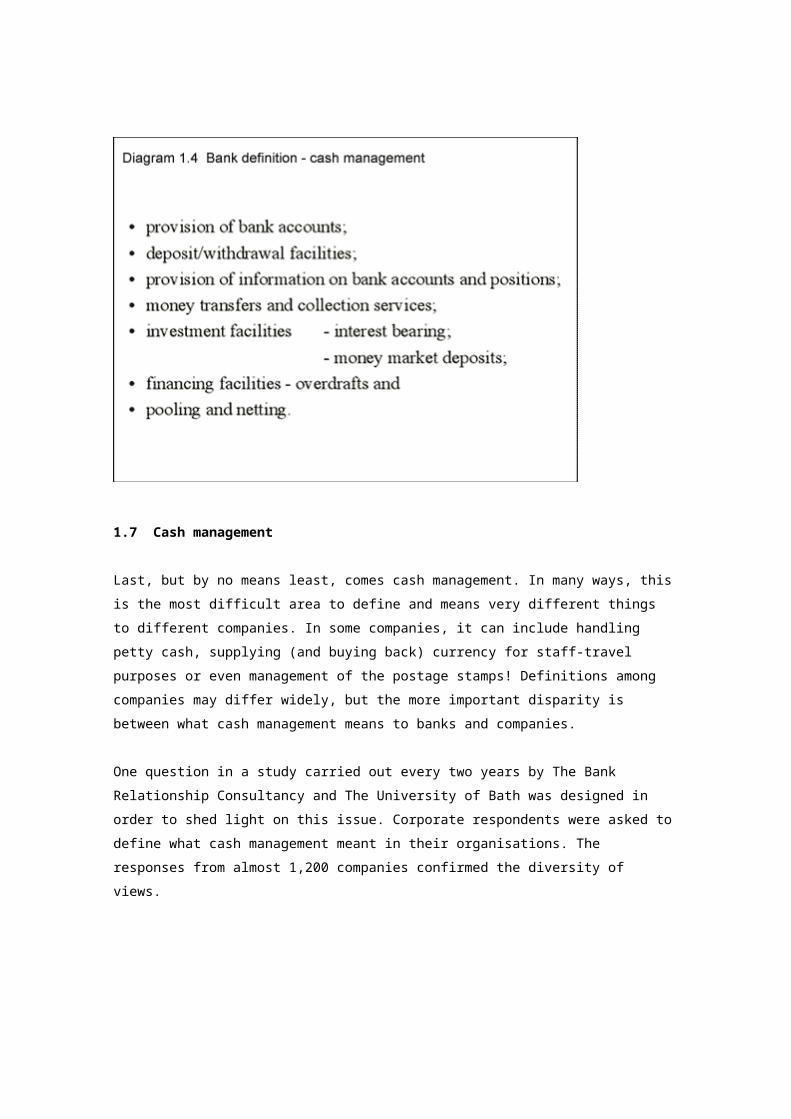

1.7 Cash management

Last, but by no means least, comes cash management. In many ways, this is the most difficult

area to define and means very different things to different companies. In some companies, it

can include handling petty cash, supplying (and buying back) currency for staff-travel purposes

or even management of the postage stamps! Definitions among companies may differ widely,

but the more important disparity is between what cash management means to banks and

companies.

One question in a study carried out every two years by The Bank Relationship Consultancy and

The University of Bath was designed in order to shed light on this issue. Corporate respondents

were asked to define what cash management meant in their organisations. The responses from

almost 1,200 companies confirmed the diversity of views.

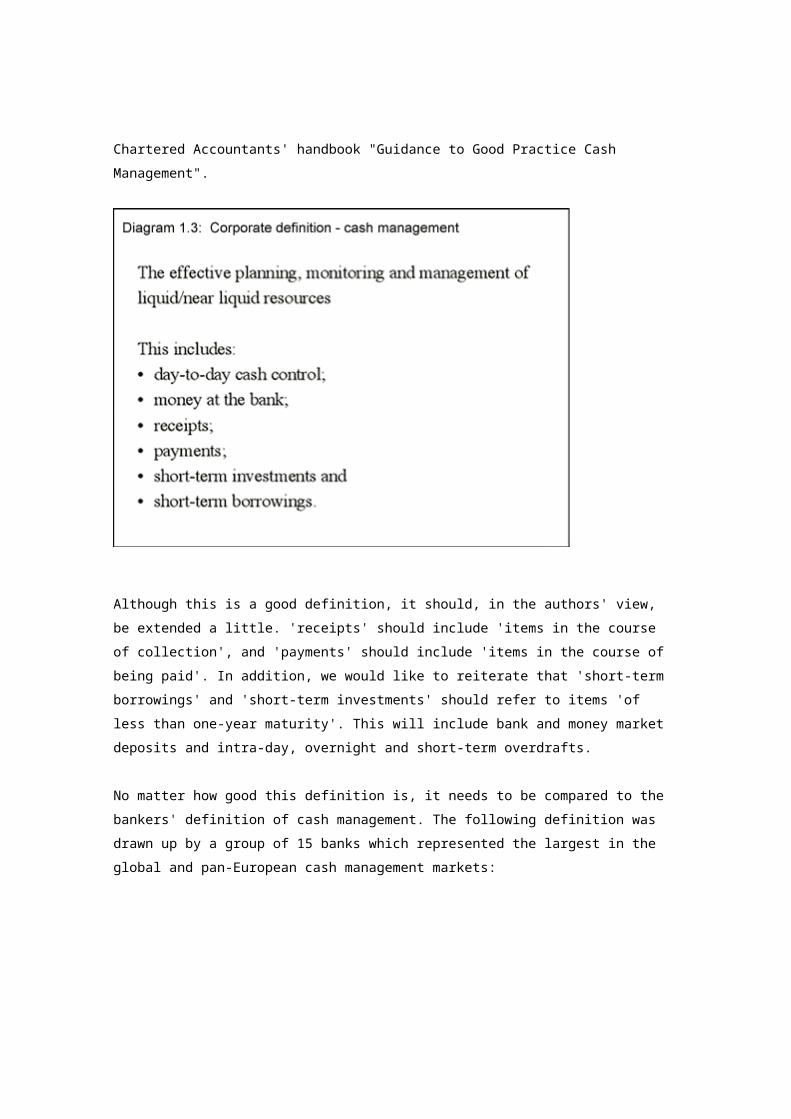

A definition of cash management for companies, which has found favour amongst many

treasury departments, can be found in the Institute of Chartered Accountants' handbook

"Guidance to Good Practice Cash Management".

Although this is a good definition, it should, in the authors' view, be extended a little. 'receipts'

should include 'items in the course of collection', and 'payments' should include 'items in the

course of being paid'. In addition, we would like to reiterate that 'short-term borrowings' and

'short-term investments' should refer to items 'of less than one-year maturity'. This will include

bank and money market deposits and intra-day, overnight and short-term overdrafts.

No matter how good this definition is, it needs to be compared to the bankers' definition of cash

management. The following definition was drawn up by a group of 15 banks which represented

the largest in the global and pan-European cash management markets:

1.7 Cash management

Last, but by no means least, comes cash management. In many ways, this is the most difficult

area to define and means very different things to different companies. In some companies, it

can include handling petty cash, supplying (and buying back) currency for staff-travel purposes

or even management of the postage stamps! Definitions among companies may differ widely,

but the more important disparity is between what cash management means to banks and

companies.

One question in a study carried out every two years by The Bank Relationship Consultancy and

The University of Bath was designed in order to shed light on this issue. Corporate respondents

were asked to define what cash management meant in their organisations. The responses from

almost 1,200 companies confirmed the diversity of views.

A definition of cash management for companies, which has found favour amongst many

treasury departments, can be found in the Institute of Chartered Accountants' handbook

"Guidance to Good Practice Cash Management".

Although this is a good definition, it should, in the authors' view, be extended a little. 'receipts'

should include 'items in the course of collection', and 'payments' should include 'items in the

course of being paid'. In addition, we would like to reiterate that 'short-term borrowings' and

'short-term investments' should refer to items 'of less than one-year maturity'. This will include

bank and money market deposits and intra-day, overnight and short-term overdrafts.

No matter how good this definition is, it needs to be compared to the bankers' definition of cash

management. The following definition was drawn up by a group of 15 banks which represented

the largest in the global and pan-European cash management markets:

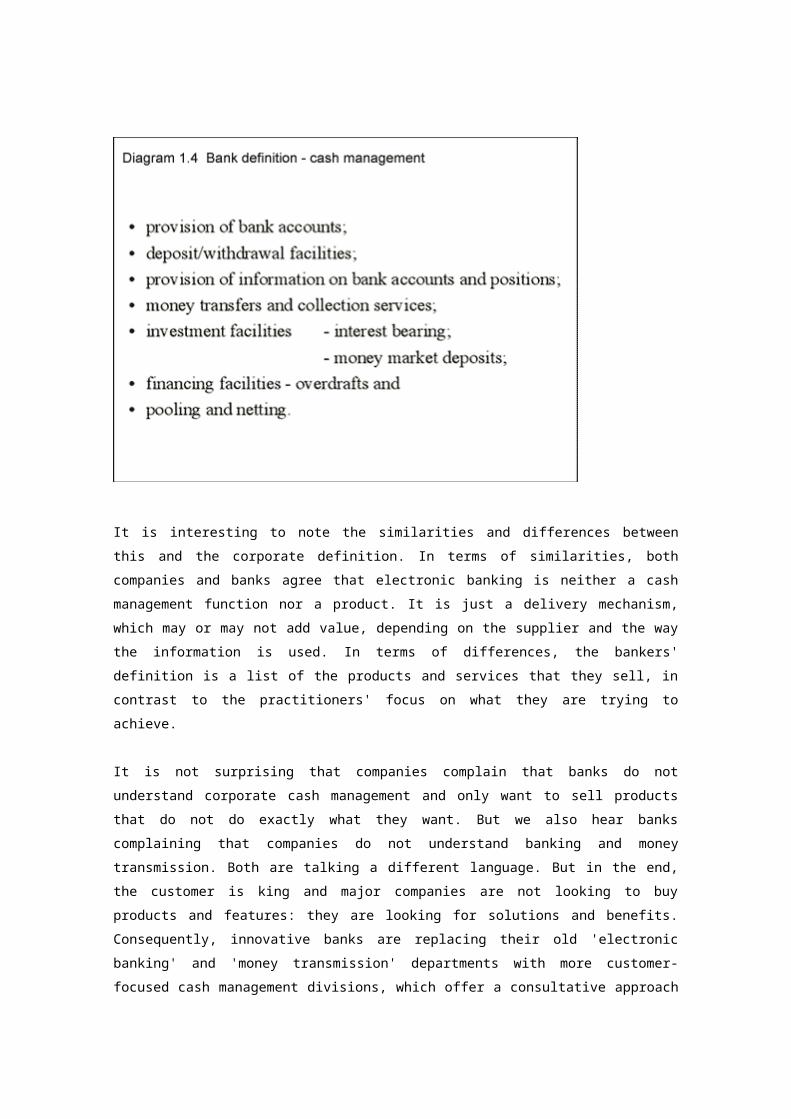

It is interesting to note the similarities and differences between this and the corporate definition.

In terms of similarities, both companies and banks agree that electronic banking is neither a

cash management function nor a product. It is just a delivery mechanism, which may or may not

add value, depending on the supplier and the way the information is used. In terms of

differences, the bankers' definition is a list of the products and services that they sell, in contrast

to the practitioners' focus on what they are trying to achieve.

It is not surprising that companies complain that banks do not understand corporate cash

management and only want to sell products that do not do exactly what they want. But we also

hear banks complaining that companies do not understand banking and money transmission.

Both are talking a different language. But in the end, the customer is king and major companies

are not looking to buy products and features: they are looking for solutions and benefits.

Consequently, innovative banks are replacing their old 'electronic banking' and 'money

transmission' departments with more customer-focused cash management divisions, which offer

a consultative approach to cash management and customised solutions-based services.

Much time is spent quantifying the benefits of cash management, both by companies and

banks. Again, the Institute of Chartered Accountants handbook lists the benefits of good cash

management to companies as follows:

1.8 Better control of financial risk

Control of financial risk is a clear benefit of good cash management to the company. Even a

profitable company can become bankrupt if it runs out of cash. Good cash management

techniques will be reflected in the balance sheet, as well as the profit and loss account.

1.9 Opportunity for profit

Many treasury managers will claim that their departments are set up as cost centres rather than

profit centres. However, in the current business environment, few corporate functions continue

to exist for long if they do not contribute positively to the company' s bottom line. It might be

better to turn this statement on its head and to suggest that good cash management offers an

opportunity to reduce costs and enhance financial returns. But this new statement hides two

additional problems; measurement and risk. First, how does one isolate - and measure - the

extra value added from treasury operations? Secondly, how much risk should the treasury

department take on in order to improve profitability? Both these questions go beyond the scope

of this manual but should nevertheless be borne in mind.

1.10 Strengthened balance sheet

It is perfectly possible to identify whether a company observes good cash management practice

by studying its annual report and accounts. It is easy to calculate liquidity ratios, compare

average debtor and creditor outstanding days, note funds in the bank against borrowings, or

check for interest cover etc. Be warned however that ratios are not always helpful in isolation,

and must be considered in relation to industry norms and trends. Remember also that as a

balance sheet is a snapshot in time, amounts shown under cash at the bank will be cashbook

items and will not take account of items in the course of being cleared.

1.11 Increased confidence with customers, suppliers and shareholders

Well-managed cash positions are important to customers, suppliers and shareholders.

Particularly in the case of long-term relationships, customers entering into business with a new

supplier will need to be convinced of the suppliers future profitability. They will also want to

know if a supplier is able to fund its existing manufacturing processes, invest in new technology

to maintain quality and competitiveness as well as be a reliable supplier.

Suppliers want to be assured that they will be paid. Most companies will make credit enquiries

on their customers before doing business with them. Information and reports such as those

produced by Dun & Bradstreet provide basic assessments of companies' cash

management/payments track records (ie how much credit they have taken in the past).

Additionally, bank references can be taken.

Shareholders will be interested in a company's cash management record for two reasons. First,

they will want to be assured that the company in which they are investing will have enough cash

to fund working capital and to continue in business. Secondly, they will want to be assured that

there is enough cash to pay them a dividend. Increasingly, at shareholder meetings, company

directors have to explain treasury and cash management policies particularly to institutional

investors. This information can be used to generate confidence that the management have their

business under control and an understanding of a companys hedging policy allows fund

managers to adjust their own risk positions.

1.12 Role of cash management in different types of companies

Cash management is an essential task for all companies but larger companies, particularly

multinational companies (MNCs) have additional challenges. In small- or medium-size

companies, where predominantly only one domestic cash flow needs to be managed, cash

management is often very much a part-time function. Particularly if the Accounts Payable (A/P)

and Accounts Receivable (A/R) functions are managed by another area - often under the control

of the 'Chief Accountant' or 'Financial Controller'. This function may be using rudimentary and

home-grown systems.

In MNC's where the cash flows may relate to many different legal entities for many geographic

locations, and may be denominated in different currencies, the cash management function

becomes an important full-time role and will require sophisticated systems for data collection,

analysis and decision support.

1.13 Cash management and banking

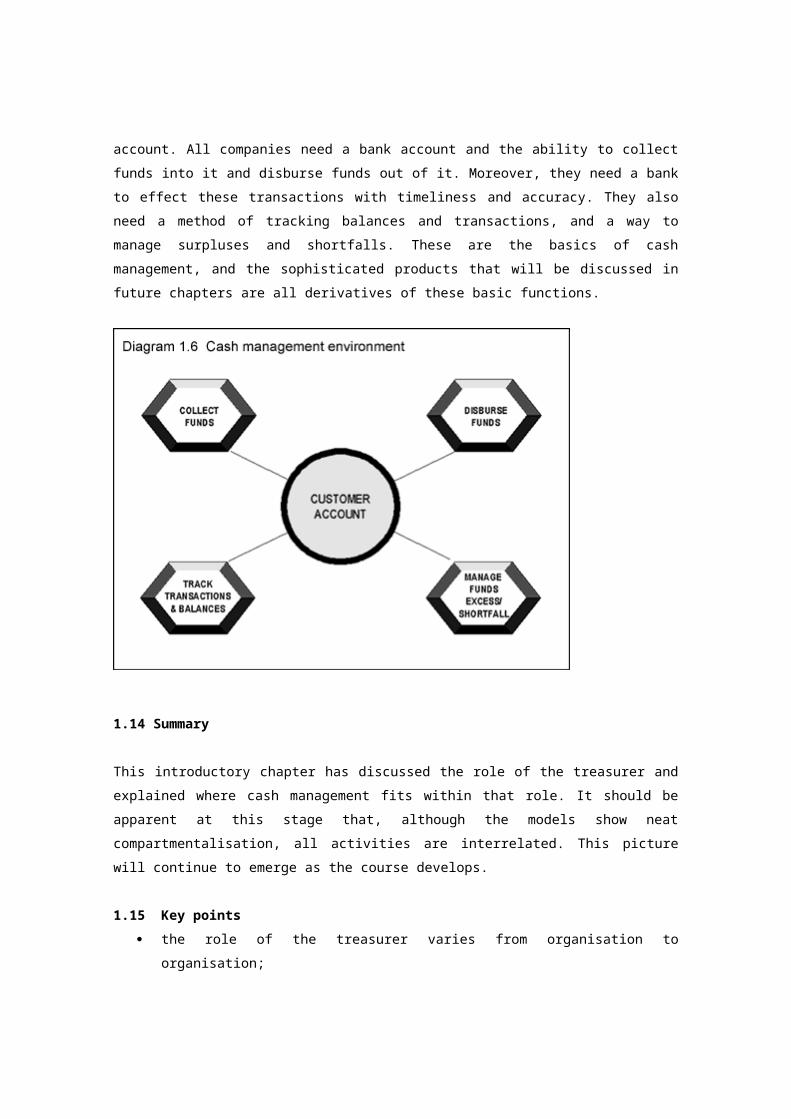

The most basic cash management product offered by banks is the current account. All

companies need a bank account and the ability to collect funds into it and disburse funds out of

it. Moreover, they need a bank to effect these transactions with timeliness and accuracy. They

also need a method of tracking balances and transactions, and a way to manage surpluses and

shortfalls. These are the basics of cash management, and the sophisticated products that will

be discussed in future chapters are all derivatives of these basic functions.

1.14 Summary

This introductory chapter has discussed the role of the treasurer and explained where cash

management fits within that role. It should be apparent at this stage that, although the models

show neat compartmentalisation, all activities are interrelated. This picture will continue to

emerge as the course develops.

1.15 Key points

the role of the treasurer varies from organisation to organisation;

within treasury, cash management can encapsulate different responsibilities;

bankers and treasurers tend to approach cash management from different perspectives.

Bankers as products and features, treasurers as tasks and benefits; and

basic cash management can be encapsulated by the cash management environment

diagram 1.6. More sophisticated practices build on these basics.

Instruments and Infrastructure

Chapter 2 - Back to Basics - banks and bank accounts

1. Overview

This introductory chapter looks at banking relationships, types of bank accounts and account

holders.

Learning objectives

A. To appreciate the different potential relationships between a company and a bank

B. To understand the differences between types of bank accounts

C. To appreciate the different types of account holders and the bank requirements for

opening such accounts

2.1 Banker / customers relationship [Italicised part of this section non-examinable]

It is important that the relationship between a bank and its customers takes on a proper set of

rules and regulations so that there can be no doubt that either party is aware of their

responsibilities to each other. While this is not a full legal summary, some of the key points are

covered in this chapter. In some countries, a bank must comply with legal statutes before it can

be authorised to accept deposits from companies or institutions. In other countries banking is

not governed by statute, but by central bank regulations. In the UK, for example, the Banking

Act of 1979 (later confirmed and updated by the 1987 Act) sets out the terms under which a

bank must operate. These include:

• having a high reputation and standing in the community;

• providing a wide range of banking products and services to include the acceptance of monies

for current and deposit accounts and the provision of borrowing facilities and

• having net assets of at least GBP5m.

What constitutes a banking customer varies country by country. Again in some countries that

will be defined by statute, by central bank regulations or legal precedent, based on case law. In

the UK, to be recognised as a customer under the legal definition of the term, a person or

corporate entity must have entered into a contract to open an account in their name. This was

established in the case of Ladbroke & Co vs Todd (1914). Additionally, legal precedent also

states that an account does not need to have been opened for any length of time.

In another case, Foley vs Hill, (1848), it was established that the basic relationship between

banker and customer is that of debtor/creditor. The bank holds money for a customer and this

money has to be repaid by the bank at some stage in the future (ie the banker is acting as the

‘debtor’, and the customer as the ‘creditor’). When the customer is borrowing from the bank, the

situation is reversed. This definition is common to many countries.

2.2 The main duties of a bank

Again these may be set out in law or in central bank requirements. In some cases individual

banks will put in place service level agreements or banking charters to describe these.

Generally, a bank has:

• a duty of care to handle customers’ business in a safe and professional manner;

• to honour customers’ cheques, provided that there are available funds and that there are no

legal reasons for refusing payment;

• to comply with any express (written) instruction from the customer, ie a standing order;

• to maintain secrecy about customers’ affairs unless compelled to do otherwise within a narrow

band of legal justifications;

• to give reasonable notice if it wishes to close an account;

• to provide a balance of account on request and to send statements to customers on a regular

basis;

• to receive customers’ money and cheques and credit them to the correct accounts;

• to repay money on demand during banking hours;

• to advise customers immediately of any improper event affecting the account and

• to exercise proper care and skill when performing all its duties so that it can earn the legal

protection given to it by the statutes, central bank regulations, or through the courts.

The customer's main duty is to exercise reasonable care in issuing instructions such as writing

cheques so that forgery is not easily possible; more recently, customers are required to take

care and protect passwords and tokens so that fraudulent funds transfer instructions cannot be

issued.

2.3 Types of bank account

In this section we will examine the different types of bank account and also the different sorts of

documentation that a banks seeks to obtain.

2.3.1 Current account

The current account is the standard, traditional bank account. There are little or no restrictions

on the type of transaction that can be passed over this type of account and a chequebook is

normally available. The US banks often refer to these accounts as 'demand deposit'

or 'checking accounts'. This latter description is quite often used in Europe in countries where

large numbers of cheques are used. Increasingly however, cheques are not used for corporate-

to-corporate business in more advanced European countries. For example, in the Netherlands

and Germany where cheques are not used for corporate payments, giro or electronic funds

transfers are the norm. The current account provides immediate access to funds and, subject to

agreement, can be overdrawn in some jurisdictions and used as a means of borrowing. Until the

last few years, no interest was ever paid on credit balances. Competitive pressure, however,

has meant that some form of interest bearing arrangements can be negotiated in many

countries. In some countries however payment of interest on current accounts is prohibited by

law or by local banking regulations (eg USA). In others interest may be payable only to 'non-

residents' (eg France).

2.3.2 Deposit or savings accounts

The traditional means by which a bank's customer can obtain interest on surplus credit balances

has been to open a deposit account. These come in various forms, but, generally speaking, the

greater the restrictions placed on the account (ie the less liquid) the higher the interest paid.

Chequebooks are not normally available and, indeed, few banks will agree to pay direct debits

or standing orders from this sort of account. For a 'time deposit' , notice is often required from

the customer in advance of any withdrawal. If the bank is not given prior notice, it is likely to levy

an interest penalty, either in the form of a specific charge or by means of a back-valued debit to

the account. In some countries, companies are not allowed to hold savings accounts, whilst in

others there may be minimum terms applied to deposits.

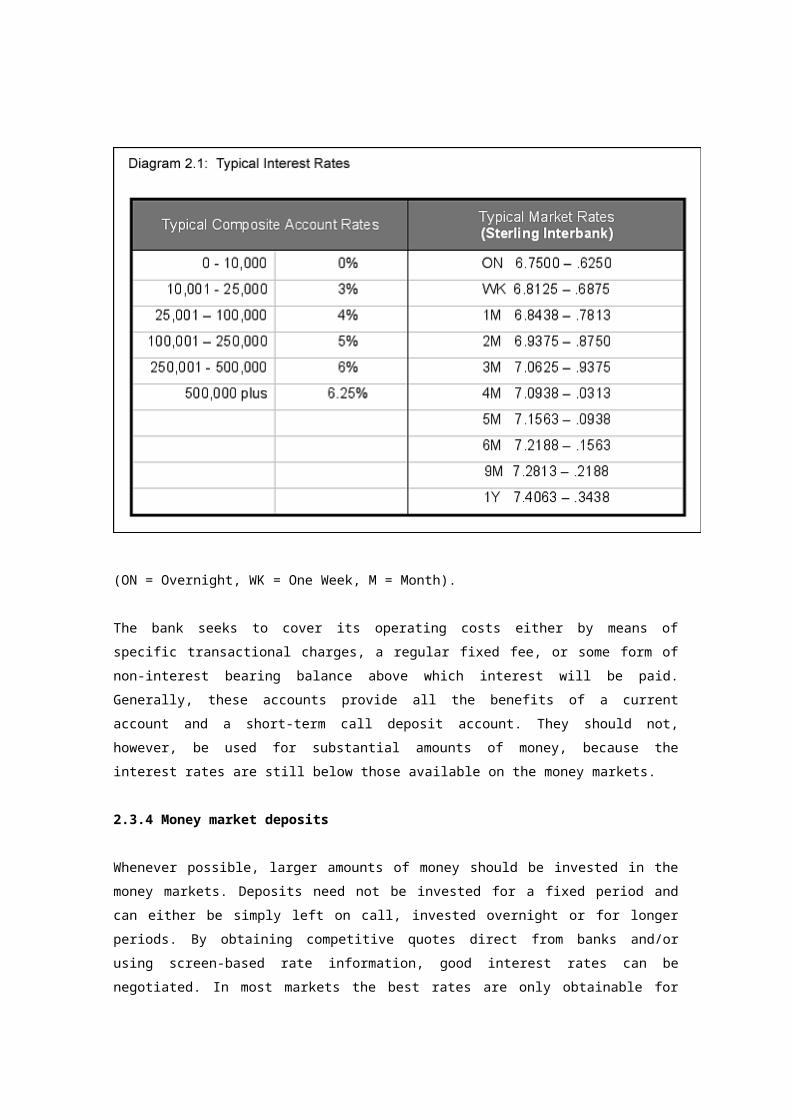

2.3.3 Composite accounts or interest bearing accounts

As mentioned above, where permitted by law, many banks will agree to pay interest on a

current account. This is sometimes called a composite account since it is an amalgam of both a

current and a deposit account. The level of interest paid is sometimes tiered according to the

extent to which the balance is in credit, and is normally set below the prevailing money market

rates:

(ON = Overnight, WK = One Week, M = Month).

The bank seeks to cover its operating costs either by means of specific transactional charges, a

regular fixed fee, or some form of non-interest bearing balance above which interest will be

paid. Generally, these accounts provide all the benefits of a current account and a short-term

call deposit account. They should not, however, be used for substantial amounts of money,

because the interest rates are still below those available on the money markets.

2.3.4 Money market deposits

Whenever possible, larger amounts of money should be invested in the money markets.

Deposits need not be invested for a fixed period and can either be simply left on call, invested

overnight or for longer periods. By obtaining competitive quotes direct from banks and/or using

screen-based rate information, good interest rates can be negotiated. In most markets the best

rates are only obtainable for amounts over a certain threshold. Each market threshold will differ.

Often the threshold is one million currency units. We will look at the money markets in more

detail in chapter 14 (Short-term investments).

2.3.5 Overdrafts

In many countries a current account can be overdrawn with prior approval from the providing

bank. The overdraft is a very flexible form of borrowing and, providing prior arrangement is

made with the bank, competitive terms can be negotiated. Non pre arranged overdrafts normally

carry heavy penalty interest rates. Although more flexible, overdrafts are, however, normally

more expensive than the terms that might be arranged for a fixed-term loan. Nevertheless, the

overdraft remains one of the most flexible forms of finance because borrowings can be repaid or

reduced whenever surplus cash balances allow. Overdrafts are usually granted for periods of

one year and are typically renewable, even though banks insist that they are repayable on

demand'. As overdrafts may be drawn down through the issuance of cheques, they are often

provided by a company's cheque issuing bank.

2.3.6 Loan accounts

When a more long-term/permanent borrowing is envisaged, a separate loan facility may be

appropriate. The amount of money borrowed is simply debited to a loan account and credited or

transferred to a current account, from where it can be used as required. Regular reductions to

the loan amount will be made on a pre-agreed basis, often by standing orders or regular

transfers from current account. More competitive terms can often be negotiated for loans.

This facility may be taken from a lead bank or any other bank, and would not be restricted to a

clearing bank.

.4 Different types of account holder

Bank accounts can be opened by private individuals, companies and organisations. In this

section we will briefly outline the different types.

2.4.1 Personal customers

A personal account can be opened by any individual who can sign his or her own name, but

because in most countries minors (persons not considered adults in law) cannot make legally

binding contracts, banks normally restrict the issue of any form of credit facility or credit card to

those customers who are recognised as adults.

Opening an account at a bank requires only a limited amount of information from the

prospective account holder: his or her name, permanent address, occupation and specimen

signature. However, in order to comply with money laundering regulations, banks are

increasingly required to make rigorous checks on an individuals identity (see section 9.13

"Money laundering").

2.4.2 Joint accounts

When a bank opens an account for two or more people (or entities), they require an explicit

instruction, or mandate, as to who is required to sign when funds are withdrawn from the

account. Typically, any one of the account holders can withdraw balances from the account.

The mandate, which is signed by all the parties to the account, usually incorporates a statement

acknowledging that, in the event of any borrowing, all parties are jointly and severally liable to

the bank. This means that if one person overdraws the account without the consent of the

others then all the parties to the account are still liable for the debt. In simple terms, this means

that any one individual can become solely responsible for the entire debt.

2.4.3 Sole traders

Many businesses are simply private individuals trading under a business name, and, as such,

the procedures required for opening the account are similar to those required for opening a

personal account, with the exception that proof of the trading name/business capacity must be

provided. In some cases, formal permission may be required to use certain words in the trading

name eg 'Royal' , 'Windsor' , 'Chemist' , 'Bank' .

In some countries the government, or the banks themselves run small business development

programmes. Often banks offer free banking to new businesses (including partnerships and

sometimes even companies) in their first year, after which time a business tariff is applied. This

tariff is typically higher than that applied to personal accounts.

2.4.4 Partnership accounts

These accounts are opened when two or more persons enter into business together as

partners. Such partnerships can range from small local businesses up to the very large firms of

solicitors and accountants. Much the same features apply to these accounts as those for the

sole trader, except that partners bear the same liability to the bank as joint account holders (ie

each partner is liable for all the liabilities of the partnership - unlike limited companies). If the

partnership is governed by a formal partnership agreement then the bank will request a copy of

this.

2.4.5 Limited liability (corporations)

Limited companies are often regarded by banks as the most important category of account

holder. This is because they are a most-profitable source of income to the bank, given the vast

variety of services they can require.

Before a company can open an account, the bank will require the company to produce a set of

documents and complete a number of forms. Forms and documents vary by country, however

some items are fairly commonly requested:

account mandate incorporating specimen signatures. This will be provided by the bank

for completion by the company;

certificate of incorporation - the birth certificate of the company;

board resolution authorising the opening of a bank account and the signatories;

documents of existence. In the UK memorandum and articles of association which

govern the rules and regulations of the company and say what it can and cannot do;

certificate of commencement to trade - this is required by all public companies before

they can commence business. In some countries in Europe this may take the form of a

Value Added Tax (VAT) registration certificate; or a corporation tax code number and

signature cards with specimens of each signatory's signature.

Similar requirements exist in most countries and, since money laundering legislation has been

implemented in many jurisdictions, signatories will often have to provide certified copies of

passports or similar documentation. In Germany and France, some banks will require all

documentation to be translated into the local language.

In law, a company is classed as a separate legal person and the law relating to companies is

very complex. The main point which should be appreciated is that a company is owned by

shareholders, but managed on their behalf by directors who may be shareholders. As far as any

borrowing is concerned, a shareholder is only liable for the amount of share capital he owns

unless he has provided any form of personal guarantee. This contrasts quite dramatically with

sole trader and partnership accounts (where the individuals are personally liable).

2.4.6 Trustee accounts

A trust has been defined as: "an equitable obligation imposing upon a person (who is called a

trustee) the duty of dealing with property over which he has control (which is called the trust

property), for the benefit of persons (who are called the beneficiaries or cestuis que trust) of

whom he may himself be one, and any one of whom may enforce the obligation" [Underhill].

Banks normally require to see a trust deed when opening bank accounts for trustees and are

expected to ensure all transactions across accounts are in accordance with the trust deed.

2.4.7 Resident and non-resident accounts

In most countries banks differentiate between those accounts owned by residents and those

owned by non-residents. Often different charging methods are applied and movements between

resident and non-resident accounts (over a certain value) have to be reported to the Central

Bank (for balance of payment purposes). In some countries where exchange control regulations

are in force, approval may have to be sought from the Central Bank prior to transfers between

residents and non-residents being allowed.

Transfers between residents and accounts held overseas will be treated in the same manner.

Chapter 3 - Back to Basics - collection and payment instruments

Overview

This chapter looks at the various payment and collection instruments used domestically (ie

within the borders of one country). It also introduces the important concepts, such as 'float',

'value dating', and 'finality', which will be built upon later in the course.

Learning objectives

A. To understand the concepts of:

float;

value dating and

finality.

and how they may be different for each instrument used

B. To understand the different instruments used to make payments and receive collections, both

paper-based and electronic items, in various countries

C. To be able to discuss the pros and cons for using each type of instrument

D. To understand the different importance placed on instruments by different countries.

3.1 Collection and payment instruments

Debits are payments made from an account and credits are payments into the account - usually

called 'receipts'. In the course of this chapter, we will look at different types of credit and debit

transactions. Wherever appropriate, we examine how both the debit and the credit are applied

to the respective accounts that are involved, and the concepts of float, value dating and finality.

Diagram 3.1

Float

The general definition of float is

'The time lost between a payor making a payment and a beneficiary receiving value'

In fact this is a definition of 'bank float'. There are other types of float.

(The concept of float is discussed further in chapter 22)

Diagram 3.2

Value dating

Definition of value:

Value is the moment when funds cease to be useable to the originating party and instead

become useable funds to the beneficiary in the sense that they can reduce overdraft balances,

earn interest or be withdrawn

Definition of forward value dating:

The time between a bank being notified of a transaction in favour of a customer and the

customer receiving future value for the item.

Definition of back value dating:

The time between a bank being notified of a transaction to the customer’s account and the item

being valued on a date prior to the date of the transaction.

An example of forward valuing would be when a bank collects value for cheques cleared in five

days, but does not give value to the customer until day six.

An example of back valuing might be processing items received late on a Friday, early on the

following Monday, but giving Friday's date.

In some countries banks will take a day's value for outgoing international funds transfers by

effectively value dating the debit entry to the customers account one day before they pay over

the funds to their correspondent. (Value dating is discussed again later in this chapter and in

chapter 10).

Diagram 3.3

Finality

Definition

The time after which a payment is considered to become irrevocable and cannot be returned

without the permission of the beneficiary account holder.

It is important to establish when finality of payment occurs so as to limit:

risk of non-payment, ie, the risk that an item is recalled by the originator or the

originating bank (eg, a stopped cheque) and

unnecessary loss of value in both the collection and the payment cycle.

It should also be noted that finality varies by instrument.

3.2 Domestic collection and payment instruments

Collection and payment instruments generally fall into the following categories:

Paper based

Cash

Cheques

Bank transfers or giros

Postal giros

Bills of exchange

Promissory notes

Banker' s drafts

Electronic

Urgent electronic funds transfer

Standard electronic funds transfer or giros or

Automated clearing house payments

Credit/charge cards

Debit cards

Standing order

Direct debit

Electronic bills of exchange

3.2.1 Cash

Cash is the most basic medium of exchange and was, of course, in use long before the

commercial banking system ever existed. Banks tend to regard cash as a necessary evil. Only

in exceptional circumstances does it earn interest when held and it is expensive to handle by

either companies or banks. Part of the obligation of a bank, however, is to honour and cash its

customers' cheques. In fact, the history of banking is littered with 'runs' on banks that have

failed to maintain sufficient liquidity (ie enough funds to meet all current, foreseen and

unforeseen obligations).

As far as the bank account is concerned, a cash withdrawal is simply debited to the account,

usually on a same-day basis (eg, when a cheque has been cleared [or ‘cashed’] at the account-

holding branch). Similarly, cash deposits should normally be credited to the account for value on

the same-day.

3.2.2 Cheques

The cheque is by far the most common instrument or means of exchange used in countries

such as Spain, Italy, the USA and the UK, but cheques are not so widely used in other areas,

such as Central and Eastern Europe and the Nordic countries. The following table identifies the

terminology used with cheques and those elements that make the cheque acceptable as a

method for the transfer of money.

Payee The name of the person or company to whom the money is to be

paid. When cashing funds, 'cash' , or 'self' can be written here.

Drawer The person or company issuing the cheque.

Drawee The name of the bank and branch where the account is held.

Amount In the event of any doubt, the amount written in words takes

precedence over the figures in the UK. Due to automation, the

amount written in figures prevails in many other countries (eg

USA).

Date The date on which the cheque was issued.

Bank/Branch Number Identifies the bank and the branch so that bank clearing Number

departments can sort and deliver the cheque to the correct bank,

branch and account. The bank and branch code are encoded onto

the cheque usually with magnetic ink using a standard known as

Magnetic Ink Character Recognition (MICR).

MICR ·Magnetic Ink Character Recognition (MICR) is the standard used

to encode bank /branch numbers on cheques with magnetic ink

and

Account Numbers The individual number of the customer' s account. This is MICR

Number encoded for the clearing/sorting process.

Cheque Numbers Consecutive number of the cheque. This is also included in

Number MICR.

The drawer of the cheque, ie, issuer, normally gives or sends the cheque to the beneficiary who

then pays it into his/her bank account. A credit to the bank account, which can comprise one or

more cheques or cash on a single credit slip, appears on the account as a single amount. In

fact, the value (see chapter 4) applied to the cash and the cheques will usually be different. If

cheques and cash are deposited on a single credit slip they are often processed as if all the

items are cheques ie, value takes longer.

The bank accepting the cheque for deposit is known as the 'collecting bank' .

The cheque is then processed through the clearing system (described in chapter 6) and

presented for payment at the drawee bank. At this point, the drawee bank debits the drawer' s

account. The proceeds are credited to the beneficiary' s bank usually to its clearing settlement

account held at the central bank.

Cheques are subject to various types of float (discussed further in chapter 22) relating to

production time;

postage time;

recipient handling;

clearing time and

value dating.

In countries that have a high volume of cheque usage, cheque clearing is, with some notable

exceptions, a highly automated process, and therefore attracts low costs.

There is, however, an element of uncertainty in terms of finality of payment by cheque. It is

possible that the cheque may be returned (bounced) either because of lack of funds, technical

reasons (words and figures 'disagree' , post-dated, not signed, etc), or the drawer could have

countermanded payment by placing a 'stop' on the cheque with the drawee branch.

Clearing times vary dramatically depending on the country concerned and the city or town in

which the cheque is drawn. Typically, local cheques, drawn in the same town will be cleared

within one to three days. In remote areas such as North India a cheque might take up to two

weeks to clear.

In some countries post-dated cheques are not allowed to be processed, whereas in others (eg

Spain) they are common and reasonably acceptable.

3.2.3 Paper-based bank transfers or bank giros

Bank transfers or bank giros are paper-based instruments that can be used to pay funds into a

beneficiary’s account. If the account is not held at the bank or branch of deposit, the item has to

go through a credit clearing. The various types of giros range from a simple blank form

completed in a bank, which is lodged with the bank cashier either with cash or cheques

attached, to the more sophisticated ‘accept’ giro used in countries such as The Netherlands and

the Nordic (Sweden, Norway, Denmark, Iceland and Finland) countries. Accept giros are

normally supplied and completed by the beneficiary and will be sent to the payor along with an

invoice. The payor will sign the giro (ie, accept it) and forward it to his/her bank. The bank will

debit the payer’s account and put the giro in the clearing system. Details included in a giro are

normally:

Amount

Recipient bank details

name;

address and

bank code.

Recipient account details

name and

account number.

Deposit date

Details of payor

name and

reference.

Remittance details

In some countries the physical forms are cleared and pass through the clearing system in the

same way as cheques (eg UK). In more sophisticated countries, giros are dematerialised (ie the

details are captured electronically at the depositing bank) and only the information passes

through the clearing system (eg The Netherlands and Nordic countries).

Giros normally take one to three days to pass through the banking system, thus creating float.

Unless printed with an invoice, giros necessitate much manual work in their preparation,

physical delivery to the bank (mail or personal visit) and much manual handling in the bank. This

is therefore an expensive instrument to use. Banks may therefore charge the depositor and the

beneficiary, and may also take some compensation through value dating.

To be of maximum use to the beneficiary, a full description of the transaction (ie name of

depositor, reference, and transaction reference) needs to pass through the system to enable full

reconciliation. This often does not happen and such detail is frequently truncated when the item

is dematerialised.

Companies that regularly receive a large volume of giro payments will probably take an

electronic report of the details, either on disk or by data transmission which they will use to

update their Accounts Receivable systems.

3.2.4 Postal giros

Postal giros are similar to bank giros, but are often operated through a separate clearing circuit

run by the local post office. Depositors will initiate the transactions at a post office. In some

countries, the post office and bank circuits are connected and operate to the same standards

(eg, UK, the Netherlands), but in others the two are separate or do not interconnect well (eg,

Switzerland). In the latter case, it may be necessary for companies to hold an account with the

post office as well as with a bank to ensure that the full remittance detail is received to enable

reconciliation.

Again, many postal giro systems enable beneficiaries to receive details of transactions received

via disk or data transmission.

3.2.5 Bills of exchange

Although often regarded as an international and foreign currency based instrument, bills of

exchange are often used domestically, particularly in continental Europe. A good definition of a

bill of exchange is provided by the UK' s Bills of Exchange Act 1882, Section 3:

(1) "A bill of exchange is an unconditional order in writing, addressed by one

person to another, signed by the person giving it, requiring the person to whom

it is addressed to pay on demand or at a fixed or determinable future time a

sum certain in money to or to the order of a specified person, or to bearer.

(2) An instrument which does not comply with these conditions, or which orders

any act to be done in addition to the payment of money, is not a bill of

exchange. Once accepted it is a legally binding document on all parties."

In fact a cheque is a bill of exchange drawn on a bank and payable on demand [1].

It should be remembered that a bill of exchange is often a dual instrument. It is both a method of

payment and a method of granting the payee credit. If the drawee (payor) is sufficiently

creditworthy, the drawer (payee) may be able to discount the value of the bill prior to maturity.

Bills can, and often are, drawn payable at the drawee' s bank, and would therefore be debited to

the drawee' s account on presentation/maturity. Clearing bills often creates float and finality of

payment will normally be a number of days after presentment/maturity in case the bill is returned

unpaid (rather like a cheque).

3.2.6 Promissory note

This instrument is similar to a bill, and used extensively in continental Europe for trade-related

transactions between counterparties that are usually well known to each other. Part IV of the

UK' s Bills of Exchange Act 1882 is devoted to promissory notes. Section 83 defines a

promissory note as follows: "A promissory note is an unconditional promise in writing made by

one person to another, signed by the maker, engaging to pay, on demand or at a fixed or

determinable future time, a sum certain in money, to, or to the order of, a specified person or to

bearer."

A promissory note does not have the legal standing of a bill of exchange and may not be able to

be discounted, unless the drawer is considered a strong credit risk.

3.2.7 Banker's drafts

A banker' s draft is similar to a cheque, but is in fact drawn by a branch of a particular bank on

its head office. It could, therefore, be regarded as a banker's cheque, the effect being that the

payment is 'guaranteed' by the bank. Until the development of same-day value electronic funds

transfers, the banker's draft was the most popular method for settling major transactions (house

or car purchase). It is still a popular method for paying for goods and services when the vendor

insists on payment in a form that ensures he gets his money at the same time as exchanging an

asset (delivery against payment). The company or person buying the banker's draft will pay for it

on issue, whereas the beneficiary will only obtain value once it clears (like a cheque). Therefore

the banker enjoys the float.

It should be noted, however, that, in the UK, building society or financial institution cheques,

although fundamentally different from banker' s drafts, frequently fulfil the same purpose. Unlike

a banker' s draft, where the cheque is effectively drawn by a bank on itself, the building society

draws a cheque on its own bankers.

Banker' s drafts, which may be denominated in any freely tradable currency, are normally

expensive to obtain, and if lost or stolen, they can be 'stopped' like a cheque.

3.2.8 Tested telex (or wire transfer)

Prior to the advent of electronic funds transfer systems and SWIFT, both bank-to-bank funds

transfers and large corporate-to-bank transfers were carried out using telex machines. Often

these messages would be unstructured and therefore processed manually at the recipient bank.

It was vital that the messages included a code or test key that could only be deciphered by the

receiving bank.

Banks would supply correspondents or corporate customers with sheets of code

numbers that would be ticked off in sequence and used as part of a number that

would be constructed as a test key. For example, a payment of USD2,101,787.94,

Value 6 June 2000 might have a test key constructed as follows:

First six whole currency amount

numbers

210178

Value date 060600

Random code from bank test

code sheet

172611

TOTAL = Test Key 443,389

Whilst this code could confirm the identity of the sending corporation and ensure that the

amount of the payment could not be altered after testing, it did not stop the beneficiary' s name

and bank details being changed, neither did it confirm that the person sending the instruction

had authority.

Tested telexes are still used occasionally, often as a back-up to an electronic funds transfer

service, between non-SWIFT member banks, or between low-tech companies and their banks.

3.2.9 Urgent electronic funds transfers

In most developed countries, high-value electronic payment systems clear funds on an urgent

(same-day) basis. In some cases, the word 'urgent' is not really appropriate, as settlement

occurs the day following initiation in less developed banking environments.

Normally urgent electronic payment systems do not create float, although they may create intra-

day credit exposure problems, and finality depends on the basis on which settlement occurs

(net settlement at the end of the day or real time gross settlement clearing transactions item by

item immediately). Both these issues are discussed further in chapters 5-9 on clearing and

settlement and payments.

These types of system are for credit transfers only, and items will be submitted to banks via

browser-based or electronic banking terminals, tape, disk, or computer-to-computer data

transmission.

3.2.10 Standard electronic funds transfers

These types of payments may be referred to as:

Automated bank transfers

Automated giros

Automated clearing house (ACH) transfers

(Automated clearing houses will be discussed in chapters 5 and 6)

They are essentially automated versions of the paper-based instruments discussed above.

They are usually future-dated payments, and may or may not create float, depending on the

country, the bank and the credit standing of the customer.

In some countries, standard electronic funds transfers may also create credit exposures where

the bank transmits the transactions to the clearing house and is liable to pay the clearing house

in one or two days' time, and to debit its customer. The risk to the bank is that the customer will

not have the funds on the debit day. Some banks will, therefore, debit less creditworthy

customers with immediate effect in order to clear that risk. More creditworthy customers may be

given a 'clearing facility' .

Finality of payment varies as settlement between participating banks normally takes place at the

end of the settlement day on a net basis. Therefore, finality often occurs the day following

settlement.

Items will typically be submitted by companies via electronic banking, tape, and disk or data

transmission. Such systems usually handle ‘one-off’, low value or non-urgent payments as well

as both repetitive debit and credit transfers such as standing orders and direct debits. In some

countries maximum amounts are imposed to prevent high value items being cleared on this

basis and thus limit systemic risk.

3.2.11 Standing orders

A standing order is an instruction given by an account holder to his/her bank to pay a

beneficiary a regular amount of money on a periodic basis (ie, monthly or quarterly). Examples

include mortgage and loan repayments, lease and rent payments, and insurance premiums.

The bank carries out the instruction by debiting the customer' s account and crediting the

beneficiary by forwarding a payment to his/her bank. While the customer is debited on day one,

the beneficiary normally has to wait two or three days for the credit to be processed by the

clearing system before obtaining value. In the interim, the benefit of the monies accrues to the

bank. This money left in the system in the course of the transaction is referred to by banks as

'float' , (chapter 22 deals with float in more detail). However, standing orders provide certainty in

terms of value date, and finality for the beneficiary is usually the day after he/she receives the

credit to his account.

A standing order can be cancelled either by the payor or his bank.

3.2.12 Direct debits

The direct debit is a similar payment method to the standing order, except that instead of the

remitter instigating the transfer, the beneficiary originates a debit which is transferred through

the clearing system to the account holder who is due to make the payment. In order to accept

direct debits on an account, banks in most countries will require the owner of the account to be

debited to give them authority prior to the commencement of the service. The account holder' s

consent to this authority is acknowledged in a direct debit mandate. Debits are originated via the

ACH system, which normally processes both the debit to the account holder and the credit to

the beneficiary at the same time. As a result, both credit and debit are usually applied to the

account on the same working day and there is no float benefit to the banks. In addition, this

system is an entirely electronic process and, therefore, the transactional charges levied by the

banks tend to be quite low. Like cheques, however, direct debits can be refused by banks and

finality of payment varies considerably from country to country. In some cases, finality can take

several weeks as direct debits can be governed by consumer protection laws.

3.2.13 Electronic bills of exchange

Certain European countries, such as France and Italy, make common use of electronic bills of

exchange. A beneficiary (drawer) electronically draws a bill on a drawee domiciled at the

drawee' s bank. The drawee will 'accept' the bill and it will be warehoused by the drawer' s bank

until maturity, at which point it is cleared via the local ACH (all of these processes are conducted

electronically). In France, where these bills are known as LCRs (Lettres de Change Relevé),

payment is passed to the holder four days after maturity and the drawee is debited three days

after maturity. Clearly, this creates float in the banking system and finality will take place on the

day following payment (ie start of business five days after maturity).

3.2.14 Financial EDI

Financial EDI (Electronic Data Interchange) payments are becoming more common and more

important with larger corporations. Financial EDI is the transmission of payment information in

standard formats, from customer to bank, bank to bank or bank to customer. This can be either

directly through a bank' s own telecommunications network or through a third party value-added

network (VAN) or a combination of both. EDI opens up new perspectives for payments, enabling

the concept of 'just in time' technology to be applied to financial transactions. This is partly

because financial EDI permits virtually endless amounts of transaction data to be included with

one concentrated electronic payment, using information or data direct from the payor' s logistics

(purchases or sales) systems.

Thus, it is possible for a single payment to represent many hundreds of individual invoice

amounts. Additionally, the data element of the message will supply the invoice details to assist

the supplier with reconciliation. The United Nations has led the way in developing this

technology by setting common standards. Its EDIFACT standard is the most widely used format

for financial EDI both domestically and internationally. Some countries and some industries

have developed their own domestic standards for EDI. In the US, for example, there are several

EDI standards. The most commonly used, ANSI ASC X12 is now compatible with EDIFACT.

[1] Unlike for cheques, however, it is the beneficiary who draws the cheque and the

person/institution to whom it is addressed who is the payor.

3.3 Plastic cards

It is important to remember to distinguish credit cards from charge cards, store cards, cash

dispenser and cheque guarantee cards.

Credit cards are used as a means of payment for goods and services by cardholders who effect

payment by authorising a debit to their credit card account. Each customer can buy goods and

services up to a given credit limit. A credit card account is completely separate from any bank

account and is, therefore, an independent source of credit. Traditionally, borrowing on credit

card accounts is more expensive than borrowing on overdraft or term loan. From the receiving

company’s point of view, credit cards are simply a payment mechanism that may be used by

some of its customers. Any ‘credit cards’ supplied to its staff are more accurately described as

charge cards, or purchasing cards (see next paragraph). In most countries, credit cards provide

extended credit as cardholders are allowed to pay off their credit card balances over a period of

time.

Charge cards are a similar means of payment to a credit card, but the full amount must be paid

when the account is rendered (normally monthly). Most charge card holders also pay an annual

fee. Cheque guarantee cards are a means of guaranteeing the payment of cheques up to a

stated amount. Cash dispenser cards are used to obtain cash from a cash dispenser machine

or automated teller machine (ATM). More recently, the development of the debit card has meant

that some of these plastic cards can be used to authorise an electronic debit to the cardholder’s

current account and a corresponding credit to the retailer’s account.

In many countries banks have combined the functions of the cash dispenser card, cheque

guarantee card, and debit card into a single card.

From the company’s point of view, there are several different charges that are relevant to these

cards. An annual fee will be levied for any charge cards supplied to employees. Far more

important to a retailer, however, are the charges levied by the merchant acquiring company

(normally a bank that ‘buys’ the transactions from the retailer at a discount). These include a

turnover fee charged by the credit card company which processes the credit card payments on

behalf of the retailer. The charges are negotiable and depend on the volumes of transactions,

the average transaction size, the method of processing and the credit quality of the transactions.

Float time and finality of payment on credit and charge cards vary not only from country to

country but also from company to company, depending on the deal negotiated with the

‘acquirer’ [1].

[1] An ‘acquirer’ is a financial institution - often a subsidiary of a bank - that ‘buys’ credit card

transactions, with recourse, from a retailer. The acquirer will present the transactions to the card

issuer for payment and will then pay the retailer the amount of the card transactions less a

discount - which covers their own and the card issuer’s fee for handling the transaction. This is

how retailers get paid.

3.4 Summary of payment and collection instruments in Europe

In summary, it is important to understand the payment norms in each country and the different

level of usage of instruments. Across European countries and the USA national characteristics

are apparent:

low use of cheques (Belgium, Germany, the Netherlands);

high use of cheques ( France, Greece, Ireland, Portugal, Spain, UK);

high use of ACH/giro system (Austria, Belgium, Finland, Germany, Italy, The

Netherlands, Norway, Sweden);

high use of Urgent EFT (Austria, Belgium, Finland, Germany, The Netherlands, UK);

high use of bank drafts (Greece, Portugal) and

high use of bills (France, Spain, Italy).

3.5 Payment instruments in other areas

Cheques are widely used in Asia-Pacific, the Middle East, USA, Canada and South America.

Several countries in the Asia-Pacific area have introduced giro-type services, but these tend to

be used mainly for consumer to business payments and direct debits.

3.6 Impact of payment and collection instruments on cash flow

The effective management of cash flow is an important part of a treasury function. Every

member of the treasury team can help to make sure that cash is received as quickly as possible

by encouraging the company’s customers to use the most efficient instruments. Treasury can

also ensure that the company uses the most appropriate methods of payment to suppliers. It is

important that the instruments in question are then factored into forecasting techniques.

Subsequently, forward projection of the anticipated inflows and outflows of cash allows a

business to assess whether it is likely to have short-term borrowing requirements or whether it

may be in a position to invest surplus funds. (Cash flow forecasting techniques are covered in

chapter 13).

While payment terms are often beyond the control of the cash management department,

efficient movement of cash into, out of, and within the company can have a significant impact on

cash flow and bank and interest charges.

Chapter 4 - Back to Basics - interest and bank charges

Overview

This final introductory chapter covers basic concepts such as interest calculation, bank charges

and ways to reduce them. (Bank tendering is dealt with in chapter 19: 'Selecting banks for cash

management purposes').

Learning objectives

A. To be able to calculate interest on a bank account

B. To understand the different types of bank charges levied for domestic services

C. To appreciate methods that can be used to reduce charges

D. To understand banks’ pricing/cost recovery strategies

4.1 Understanding domestic interest calculations

4.1.1 Value dates

When we discuss clearing systems in the following chapters we will see that cheques and

credits take several working days to clear. During this period, the 'value' of the items is not

available to the beneficiary. Clearly, the 'value date' applied to any transaction is different from

the date on which it appears on the bank statement (the ledger date). Taking the example of a

cheque drawn on a bank in one town and paid into an account at the account-holding branch in

another town, the credit will appear on the bank depositor's statement on the deposit day but

the 'value' will not be applied until some days later.

This difference between ledger date and value date has implications for the amount of interest

paid on the account. The important point is that the bank calculates interest on the 'cleared

balance' (ie only including transactions which have been cleared).

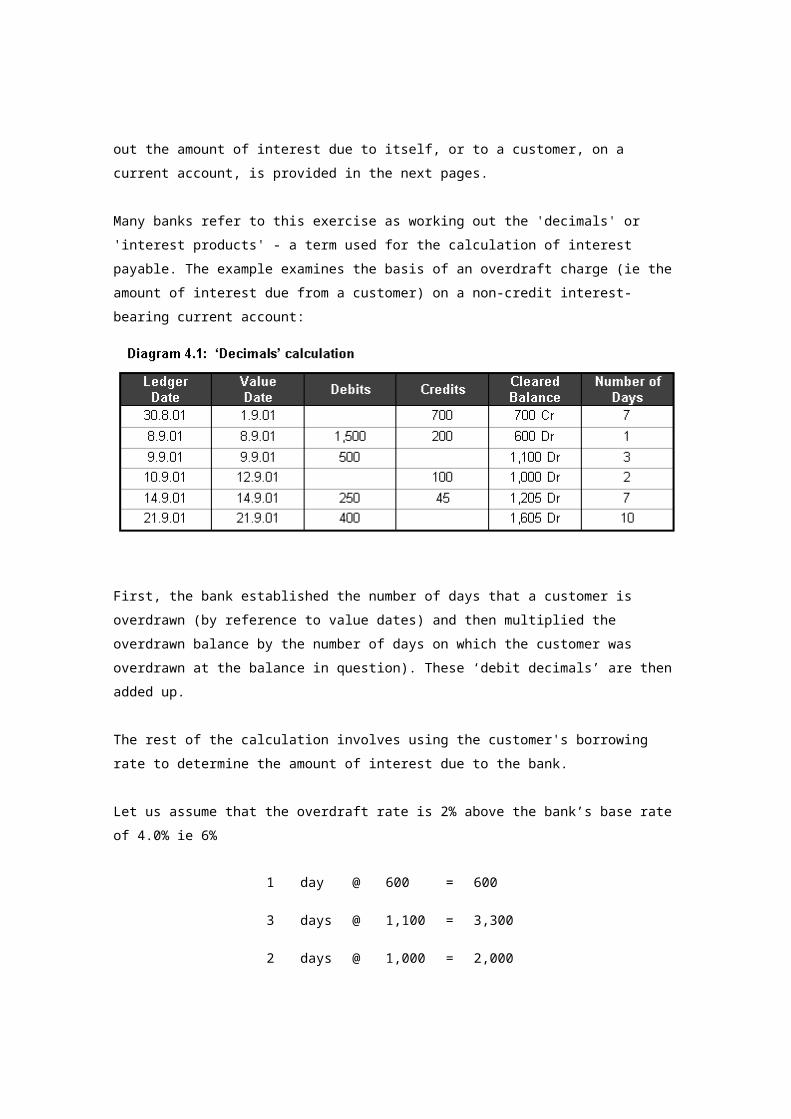

4.1.2 Interest calculations

A practical example of how a bank using the UK banking system works out the amount of

interest due to itself, or to a customer, on a current account, is provided in the next pages.

Many banks refer to this exercise as working out the 'decimals' or 'interest products' - a term

used for the calculation of interest payable. The example examines the basis of an overdraft

charge (ie the amount of interest due from a customer) on a non-credit interest-bearing current

account:

First, the bank established the number of days that a customer is overdrawn (by

reference to value dates) and then multiplied the overdrawn balance by the number

of days on which the customer was overdrawn at the balance in question). These

‘debit decimals’ are then added up.

The rest of the calculation involves using the customer's borrowing rate to

determine the amount of interest due to the bank.

Let us assume that the overdraft rate is 2% above the bank’s base rate of 4.0% ie

6%

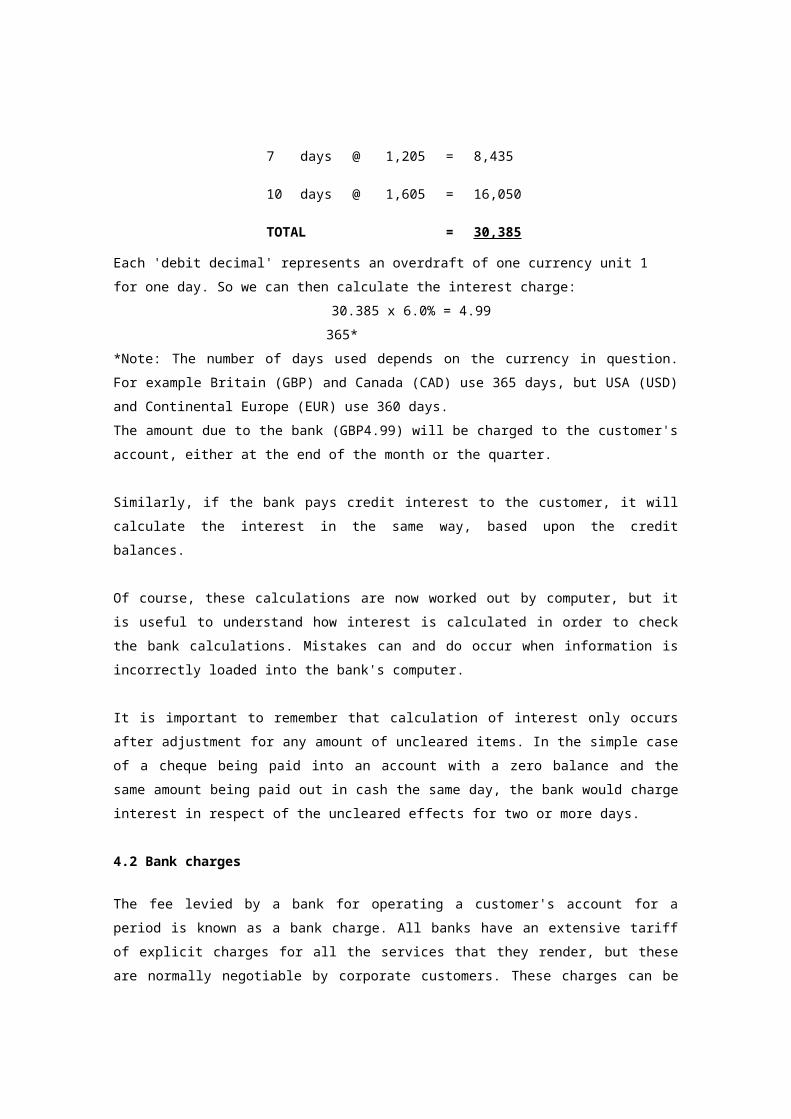

1 day @ 600 = 600

3 days @ 1,100 = 3,300

2 days @ 1,000 = 2,000

7 days @ 1,205 = 8,435

10 days @ 1,605 = 16,050

TOTAL = 30,385

Each 'debit decimal' represents an overdraft of one currency unit 1 for one day. So we can then

calculate the interest charge:

30.385 x 6.0% = 4.99

365*

*Note: The number of days used depends on the currency in question. For example Britain

(GBP) and Canada (CAD) use 365 days, but USA (USD) and Continental Europe (EUR) use

360 days.

The amount due to the bank (GBP4.99) will be charged to the customer's account, either at the

end of the month or the quarter.

Similarly, if the bank pays credit interest to the customer, it will calculate the interest in the same

way, based upon the credit balances.

Of course, these calculations are now worked out by computer, but it is useful to understand

how interest is calculated in order to check the bank calculations. Mistakes can and do occur

when information is incorrectly loaded into the bank's computer.

It is important to remember that calculation of interest only occurs after adjustment for any

amount of uncleared items. In the simple case of a cheque being paid into an account with a

zero balance and the same amount being paid out in cash the same day, the bank would

charge interest in respect of the uncleared effects for two or more days.

4.2 Bank charges

The fee levied by a bank for operating a customer's account for a period is known as

a bank charge. All banks have an extensive tariff of explicit charges for all the

services that they render, but these are normally negotiable by corporate

customers. These charges can be levied as a detailed tariff, a fixed charge or a

requirement to hold non-interest-bearing balances. The corporate customer should

always be aware of the basis on which charges are being paid.

The amount charged will vary according to several factors such as:

Balances maintained - A notional credit allowance on any non-interest-bearing

credit balances often offsets or reduces any charges

Turnover - Calculated based on debit or credit values through the

account

Number of entries - The more debits and credits the higher the charges. Each

type of transaction will have a different charge. But when

volume is sufficient, reductions can be negotiated.

Number of additional services

taken

- These additional charges can include stopped cheques,

returned cheques, ACH batch charges, statements

issued, pooling costs, management time, etc.

(Bank charges are discussed in more detail in chapter 10 - Foreign currency accounts)

4.3 Reducing bank charges

There are four broad areas that need to be considered when trying to reduce bank charges:

• understand the charging methods;

• review types of payments and methods of submission;

• reviewing existing arrangements and

• using better cash management techniques.

4.3.1 Understand charging methods

Customers should be aware that turnover charges rarely work to the customer's advantage and

that a fixed or per item tariff is normally more advantageous than either ad valorem or turnover-

based pricing. A 'sensitivity analysis' will enable the customer to identify the charges of most

importance to them. Interest rates and calculations should, of course, be checked as well as

commission charges.

Bank customers must understand how their charges are being calculated in order to be able to

reduce these costs.

Normally, there are no 'free' services given by banks, but there are services for which there is

no explicit charge. In fact, the cost for these services is often paid for by hidden charges

elsewhere.

However, hidden charges are less of an issue in those countries which have adopted Banking

Charters and/or the EC Directive on The Transparency of Banking Charges (see chapter 8

section 8.6).

4.3.2 Review types of payments and method of submission

Volumes of items need to be analysed to ensure that maximum use is being made of automated

low-cost payment methods such as future-dated electronic funds transfer, (giro or ACH) and

only minimal use is made of expensive same-day/urgent electronic funds transfers.

Banks tend to profit from economies of scale and will normally offer discounts for higher

volumes of items when they are automated. Moreover, spreading transactions between too

many banks often results in higher charges overall.

Payments that are delivered to the bank 'fully formatted' can be processed automatically using

straight-through-processing (STP) technology. These will also normally be charged at lower

rates than partially formatted payments that may require some manual intervention by the

bank's payment processing staff.

Unspecified supplementary charges should be avoided. These are particularly prevalent with

international payments and collections.

The increasing use of competitive tenders can be a powerful tool in reducing charges, but a

tender must be properly run if it is to be effective. The banks often seek commitment for several

years when submitting quotes and suggest the charges are linked to increases in the Retail

Pricing Index. This is usually not appropriate as an 'across the board' agreement. Often

corporate customers will offer their business for tender, enabling several banks to compete for

the company's custom. (Bank tenders (RFPs) are covered in detail in chapter 19.)

4.3.3 Reviewing existing arrangements

Companies often underestimate the delays inherent in their existing arrangements. Are cheques

that are received paid in promptly? Is there a quicker, more efficient, cheaper way of receiving

funds? Are the most cost-effective payment methods being used? Can the use of a courier help

accelerate the process?

An examination of payment procedures often leads to further economies.

4.3.4 Better cash management

Improved cash management techniques, from simple pooling or netting arrangements to more

sophisticated cash concentration facilities, can lead to significant reductions in costs or

improved investment returns (these techniques are discussed in detail in later sections of the

course).

Electronic banking has advantages and disadvantages, but can be an important tool that can be

used to improve cash management. However, companies should understand the increased

risks and responsibilities involved in its use.

Proper recognition of risk is also a fundamental function of better cash management.

In summary, companies should:

• seek competitive credit interest/debit interest on all balances;

• only pay a charge if they understand it and agree with it;

• compare terms and conditions available from other bank suppliers regularly;

• consider whether they can use the banking system more effectively and