IB Business and Management 5.3 Breakeven analysis.

35

IB Business and Management 5.3 Breakeven analysis

-

Upload

griffin-kristopher-norris -

Category

Documents

-

view

265 -

download

3

Transcript of IB Business and Management 5.3 Breakeven analysis.

IB Business and Management

5.3 Breakeven analysis

Quick test:1. Give 2 other names for Revenue (2)2. Give 2 examples of fixed costs (2)3. Give 2 examples of variable costs (2)4. What is the formula for Revenue? (1)A firm has fixed costs of £2000 per month.

Variable costs of £3 per unit and selling price of £5. In July they sell 1,200 units

5. How much revenue does the firm make? (1)6. What are the firms total costs? (1)7. How much profit does the firm make in July?

(1)

Total marks = 10

What Is Breakeven?

If a firm is breaking even it means that the business is neither making a profit or a loss.

Breakeven is the output at which a firm’s total revenue is equal to its total costs.

Profit = Total Revenue – Total Costs

Why might a firm use breakeven analysis?

• New firms need to estimate how much they must produce before they make a profit

• This may help them to decide if their business idea is viable

• May be required as part of a business plan• Existing firms may wish to know:• Profit/Loss at any level of output• The output needed to produce a certain

level of profit

Assumptions of simple break-even analysis

• The selling price remains the same, regardless of the number of units sold

• Fixed costs remain the same regardless of the number of units of output

• Variable costs vary in direct proportion to output

Finding The Breakeven Point

The Breakeven point can be found in 2 ways

1. Graphical Method2. Contribution method

Break Even ChartsCosts/Revenue

Output/Sales

Initially a firm will incur fixed costs, these do not depend on output or sales.

FC

As output is generated, the firm will incur variable costs – these vary directly with the amount produced.

VC The total costs therefore (assuming accurate forecasts!) is the sum of FC+VC

TC Total revenue is determined by the price charged and the quantity sold – again this will be determined by expected forecast sales initially.

The lower the price, the less steep the total revenue curve.

TR

Breakeven Output

The break even point occurs where total revenue equals total costs. The firm will have to produce and sell this number of units to breakeven

Breakeven Revenue

ExampleA small Photo frame manufacturer has the following

costs:Rent £5,000 per yearBusiness Rates £2,000 per yearRaw Materials £1.25 per unitUtilities £3,000 per yearPackaging £1 per unitSalaries £10,000 per year

The firm sells the photo frames for £4.50 to retailers

How many photo frames does the firm need to produce in a year in order to break-even?

Step 1: Creating a TableOutputOutput Fixed CostFixed Cost Variable Variable

CostCostTotal CostTotal Cost Total Total

RevenueRevenue

00

10001000

20002000

30003000

40004000

50005000

60006000

70007000

80008000

90009000

1000010000

ExampleA small Photo frame manufacturer has the following

costs:Rent £5,000 per yearBusiness Rates £2,000 per yearRaw Materials £1.25 per unitUtilities £3,000 per yearPackaging £1 per unitSalaries £10,000

The firm sells the photo frames for £4.50 to retailers

How many photo frames does the firm need to produce in a year in order to break-even?

Step 2:Adding Fixed CostsOutputOutput Fixed CostFixed Cost Variable Variable

CostCostTotal CostTotal Cost Total Total

RevenueRevenue

00 20,00020,000

10001000 20,00020,000

20002000 20,00020,000

30003000 20,00020,000

40004000 20,00020,000

50005000 20,00020,000

60006000 20,00020,000

70007000 20,00020,000

80008000 20,00020,000

90009000 20,00020,000

1000010000 20,00020,000

ExampleA small Photo frame manufacturer has the following

costs:Rent £5,000 per yearBusiness Rates £2,000 per yearRaw Materials £1.25 per unitUtilities £3,000 per yearPackaging £1 per unitSalaries £10,000

The firm sells the photo frames for £4.50 to retailers

How many photo frames does the firm need to produce in a year in order to break-even?

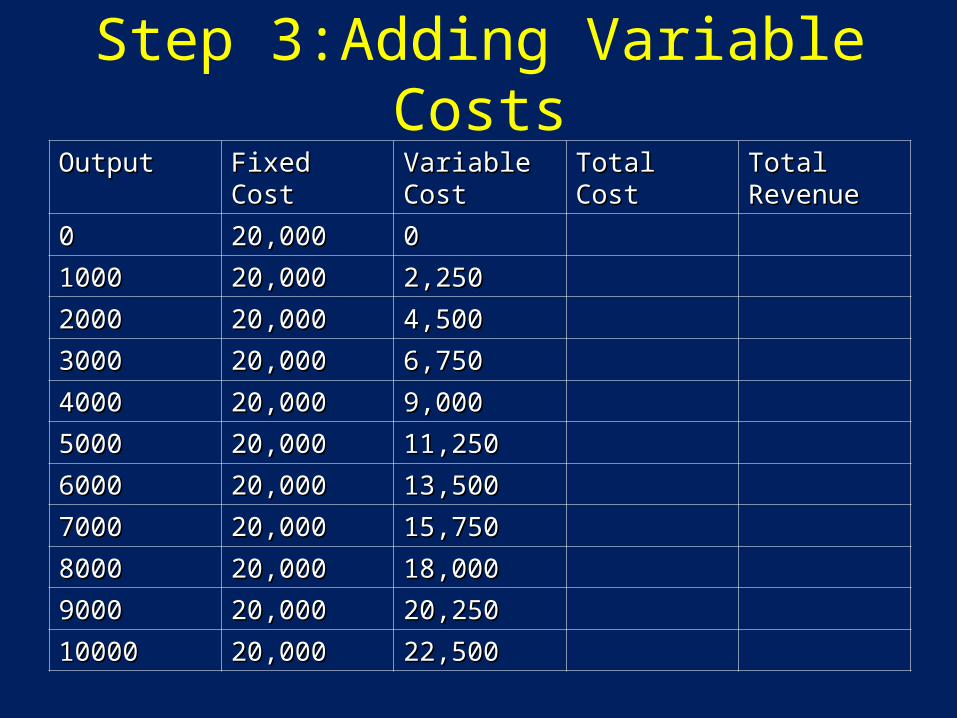

Step 3:Adding Variable Costs

OutputOutput Fixed CostFixed Cost Variable Variable CostCost

Total CostTotal Cost Total Total RevenueRevenue

00 20,00020,000 00

10001000 20,00020,000 2,2502,250

20002000 20,00020,000 4,5004,500

30003000 20,00020,000 6,7506,750

40004000 20,00020,000 9,0009,000

50005000 20,00020,000 11,25011,250

60006000 20,00020,000 13,50013,500

70007000 20,00020,000 15,75015,750

80008000 20,00020,000 18,00018,000

90009000 20,00020,000 20,25020,250

1000010000 20,00020,000 22,50022,500

ExampleA small Photo frame manufacturer has the following

costs:Rent £5,000 per yearBusiness Rates £2,000 per yearRaw Materials £1.25 per unitUtilities £3,000 per yearPackaging £1 per unitSalaries £10,000

The firm sells the photo frames for £4.50 to retailers

How many photo frames does the firm need to produce in a year in order to break-even?

Step 4:Adding Total CostsOutputOutput Fixed CostFixed Cost Variable Variable

CostCostTotal CostTotal Cost Total Total

RevenueRevenue

00 20,00020,000 00 20,00020,000

10001000 20,00020,000 2,2502,250 22,25022,250

20002000 20,00020,000 4,5004,500 24,50024,500

30003000 20,00020,000 6,7506,750 26,75026,750

40004000 20,00020,000 9,0009,000 29,00029,000

50005000 20,00020,000 11,25011,250 31,25031,250

60006000 20,00020,000 13,50013,500 33,50033,500

70007000 20,00020,000 15,75015,750 35,75035,750

80008000 20,00020,000 18,00018,000 38,00038,000

90009000 20,00020,000 20,25020,250 40,25040,250

1000010000 20,00020,000 22,50022,500 42,50042,500

ExampleA small Photo frame manufacturer has the following

costs:Rent £5,000 per yearBusiness Rates £2,000 per yearRaw Materials £1.25 per unitUtilities £3,000 per yearPackaging £1 per unitSalaries £10,000

The firm sells the photo frames for £4.50 to retailers

How many photo frames does the firm need to produce in a year in order to break-even?

Step 5:Adding Total Revenues

OutputOutput Fixed CostFixed Cost Variable Variable CostCost

Total CostTotal Cost Total Total RevenueRevenue

00 20,00020,000 00 20,00020,000 00

10001000 20,00020,000 2,2502,250 22,25022,250 4,5004,500

20002000 20,00020,000 4,5004,500 24,50024,500 9,0009,000

30003000 20,00020,000 6,7506,750 26,75026,750 13,50013,500

40004000 20,00020,000 9,0009,000 29,00029,000 18,00018,000

50005000 20,00020,000 11,25011,250 31,25031,250 22,50022,500

60006000 20,00020,000 13,50013,500 33,50033,500 27,00027,000

70007000 20,00020,000 15,75015,750 35,75035,750 31,50031,500

80008000 20,00020,000 18,00018,000 38,00038,000 36,00036,000

90009000 20,00020,000 20,25020,250 40,25040,250 40,50040,500

1000010000 20,00020,000 22,50022,500 42,50042,500 45,00045,000

Plotting the Graph

Draw a set of Axis• X axis= output (0-10,000)• Y axis= £ Cost/Revenue (0-50,000)Plot the line for Total CostsPlot the line for Total Revenues

Breakeven Chart

TC

TR

Output

Costs/Revenue

£

BEP

Answer

• Breakeven output is approx 8,900

• Breakeven Revenue = £40,000

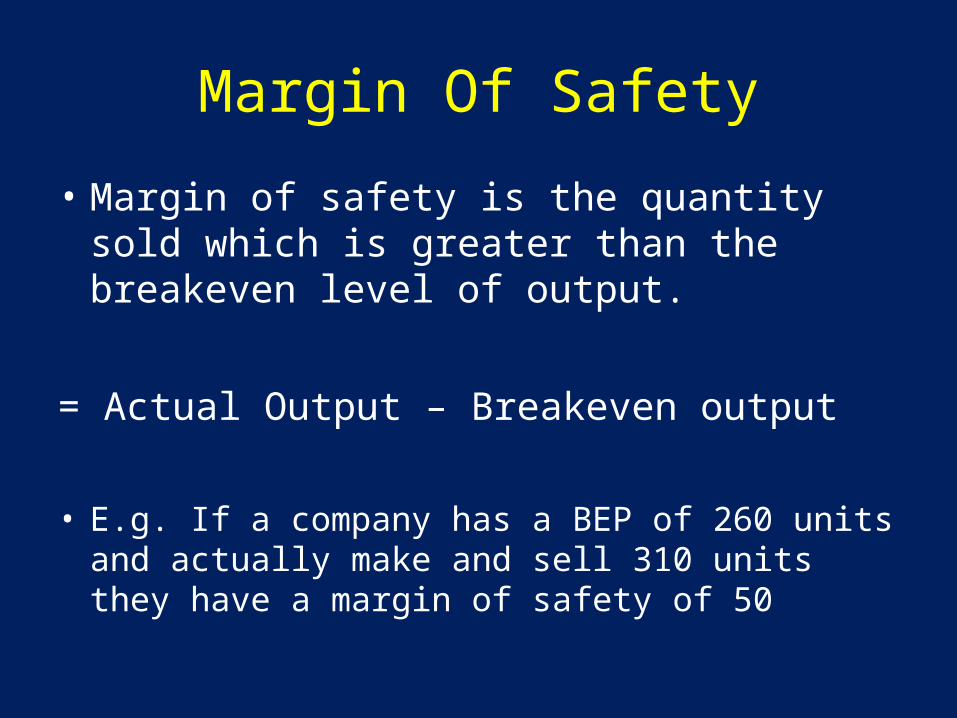

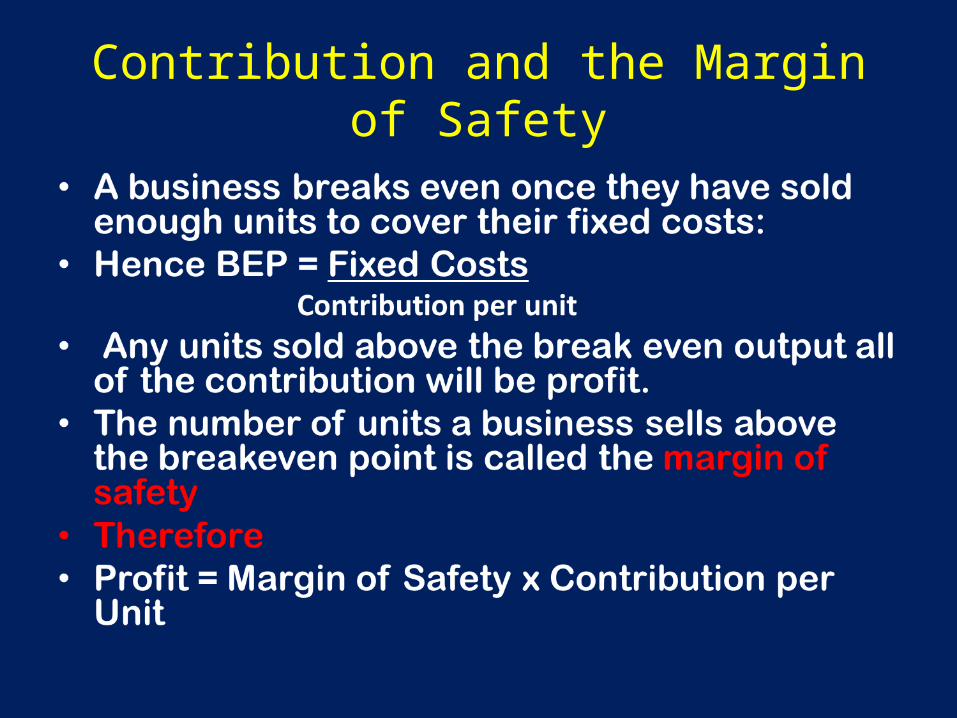

Margin Of Safety

• Margin of safety is the quantity sold which is greater than the breakeven level of output.

= Actual Output – Breakeven output

• E.g. If a company has a BEP of 260 units and actually make and sell 310 units they have a margin of safety of 50

Break Even Charts – What they show

Costs/Revenue

Output/Sales

TCTR

Breakeven OutputD1

Loss

D2

Profit

Margin of safety

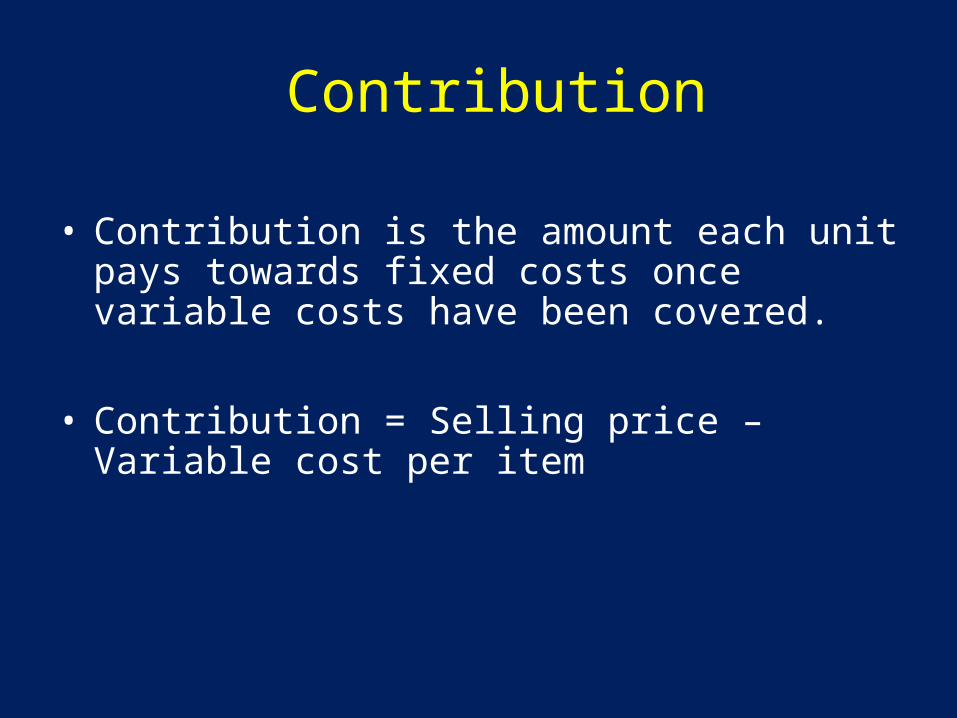

Contribution

• Contribution is the amount each unit pays towards fixed costs once variable costs have been covered.

• Contribution = Selling price – Variable cost per item

Using Contribution to calculate the Breakeven Point

To calculate the breakeven point in terms of output the following formula can be used

• Breakeven Output = Fixed Costs Contribution per Unit

• How can we work out the Breakeven Revenue?

• Multiply the Breakeven output by the Selling Price

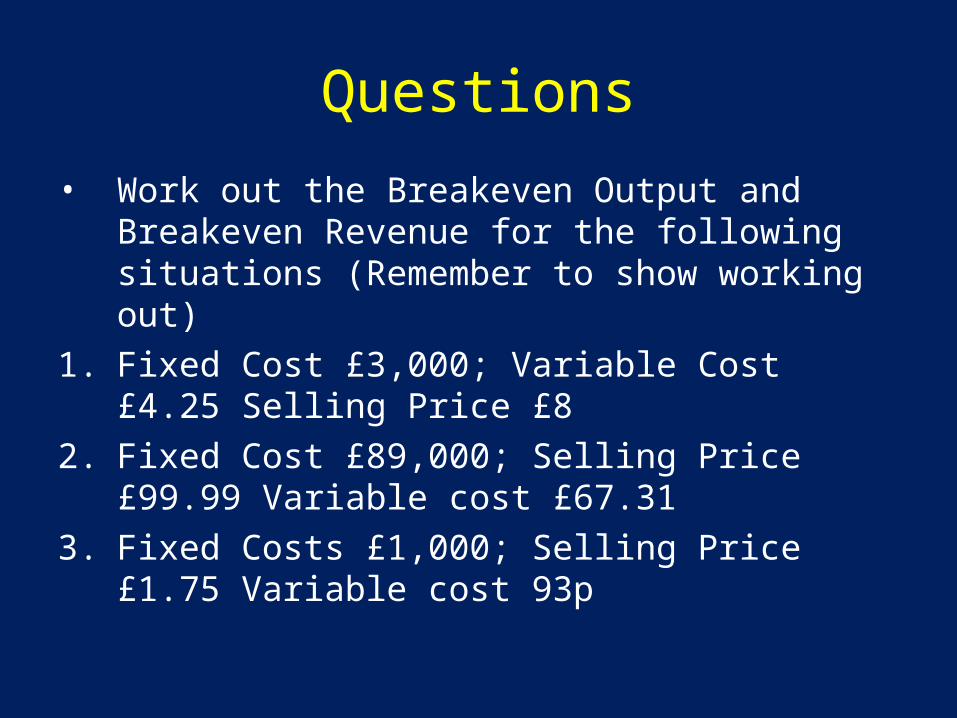

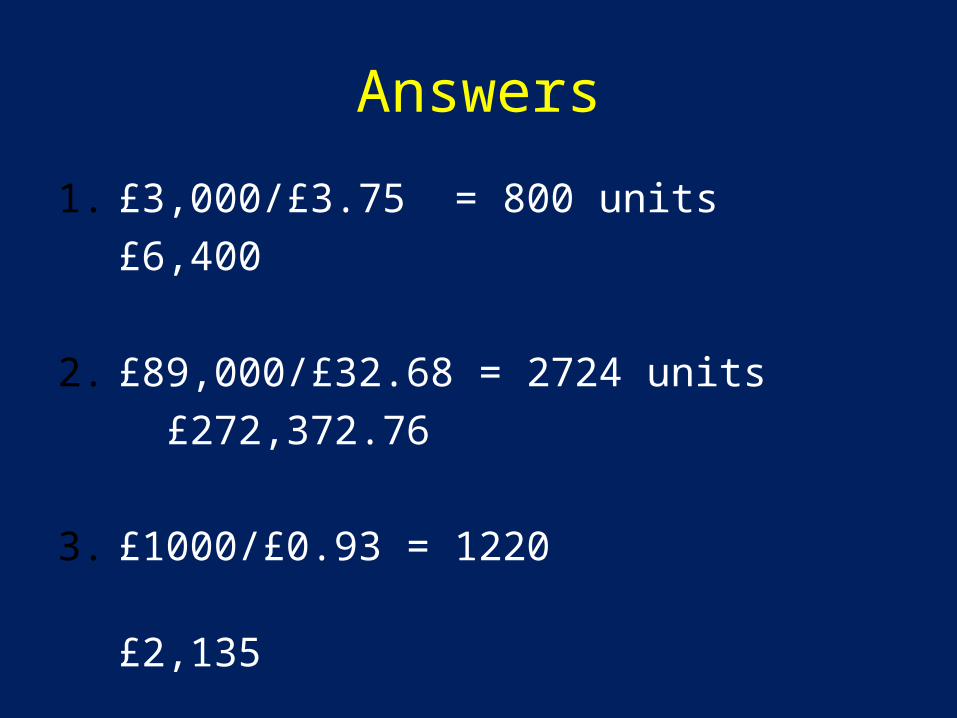

Questions

• Work out the Breakeven Output and Breakeven Revenue for the following situations (Remember to show working out)

1. Fixed Cost £3,000; Variable Cost £4.25 Selling Price £8

2. Fixed Cost £89,000; Selling Price £99.99 Variable cost £67.31

3. Fixed Costs £1,000; Selling Price £1.75 Variable cost 93p

Answers

1. £3,000/£3.75 = 800 units£6,400

2. £89,000/£32.68 = 2724 units £272,372.76

3. £1000/£0.93 = 1220 £2,135

Contribution and the Margin of Safety

Changes in Variable CostsCosts/Revenue

Output/Sales

TC

TR

BEP

The level of variable costs affects the gradient of the Total Costs line.

If Variable Costs go up the line will become steeper. What will happen to the Break Even Point?

If Variable Costs go down the line will become less steep. What will happen to the Break Even Point?

TC1

BEP1

TC2

BEP2

Changes in Fixed CostsCosts/Revenue

Output/Sales

TC

TR

BEP

The fixed cost line affects where the Total Cost line starts

If fixed costs go up, the Total Costs line will shift upwards

TC1

BEP1

If fixed costs go down, the Total Costs line will shift downwards

TC2

BEP2

Changes in Selling PriceCosts/Revenue

Output/Sales

TC

TR

BEP

A change in Selling price will affect the gradient of the Total Revenue line

An increase in the selling price will make the TR line steeper

TR1

BEP1

A decrease in the selling price will make the TR line less steep

TR2

BEP2

Example – Advertising costs increase

Costs/Revenue

Output/Sales

TCTR

BE1

TC2

BE2

An increase in Advertising causes an upwards shift of the Total Cost line. This results in an increase of the breakeven output from BE1 to BE2

Questions

Explain what will happen to the Breakeven output in the following situations. Illustrate with a diagram.

1. The cost of raw materials increases2. The company moves to premises with

cheaper rent3. The company decreases the selling price

to compete with a new competitor4. The electricity supplier increases their

prices

Limitations of Breakeven Analysis

• Information used may be unreliable as it is based on forecasts and predictions

• Assumes SP stays the same regardless of output

• Fixed Costs may not stay the same• Ignores factors such as economies of scale• Assumes that all output is sold• Only suitable for analysis of single products• Only considers quantitive factors

Breakeven TableOutputOutput Fixed Fixed

CostCostVariable Variable CostCost

Total CostTotal Cost Total Total RevenueRevenue

ProfitProfit

00

10001000

20002000

30003000

40004000

50005000

60006000

70007000

80008000

90009000

1000010000