Hungary: assessing the impact of the package István Hamecz Director Head of Economics and Monetary...

19

Hungary: assessing the impact of the package István Hamecz Director Head of Economics and Monetary Policy Directorate

-

Upload

laura-pierce -

Category

Documents

-

view

215 -

download

0

Transcript of Hungary: assessing the impact of the package István Hamecz Director Head of Economics and Monetary...

Hungary: assessing the impact of the package

István HameczDirector

Head of Economics and Monetary Policy Directorate

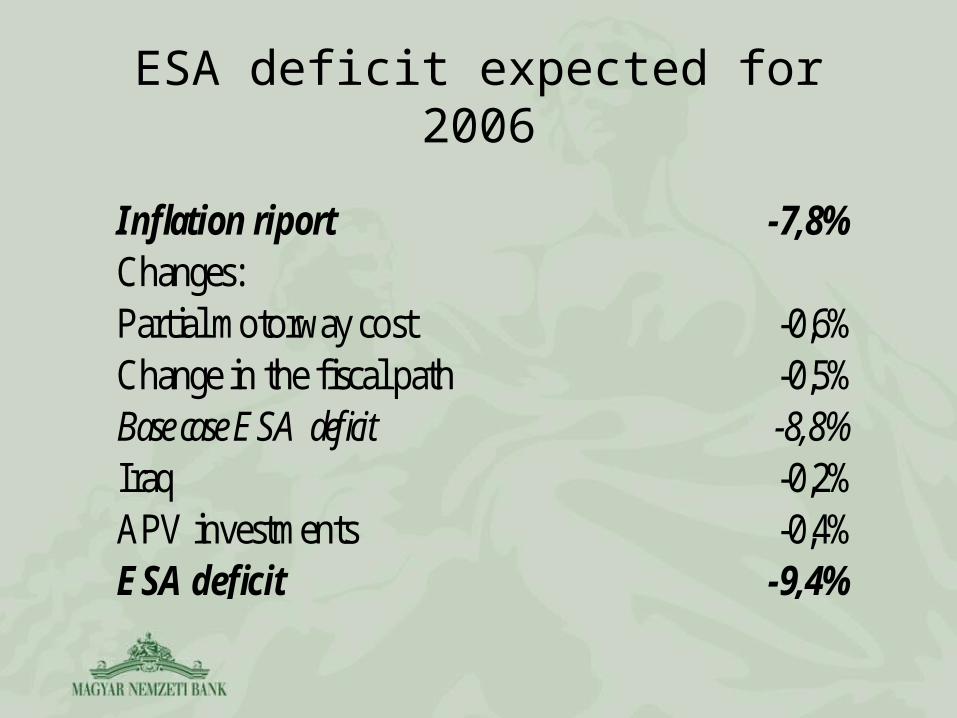

ESA deficit expected for 2006

Inflation riport -7,8%Changes:Partial motorway cost -0,6%Change in the fiscal path -0,5%Base case ESA deficit -8,8%Iraq -0,2%APV investments -0,4%ESA deficit -9,4%

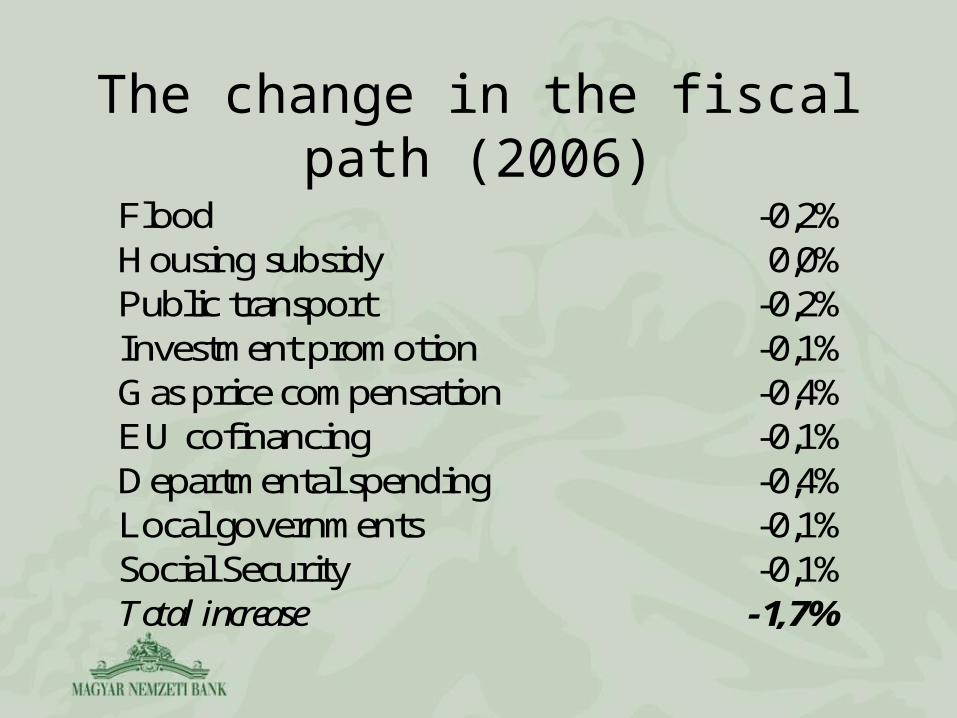

The change in the fiscal path (2006)

Flood -0,2%Housing subsidy 0,0%Public transport -0,2%Investment promotion -0,1%Gas price compensation -0,4%EU cofinancing -0,1%Departmental spending -0,4%Local governments -0,1%Social Security -0,1%Total increase -1,7%

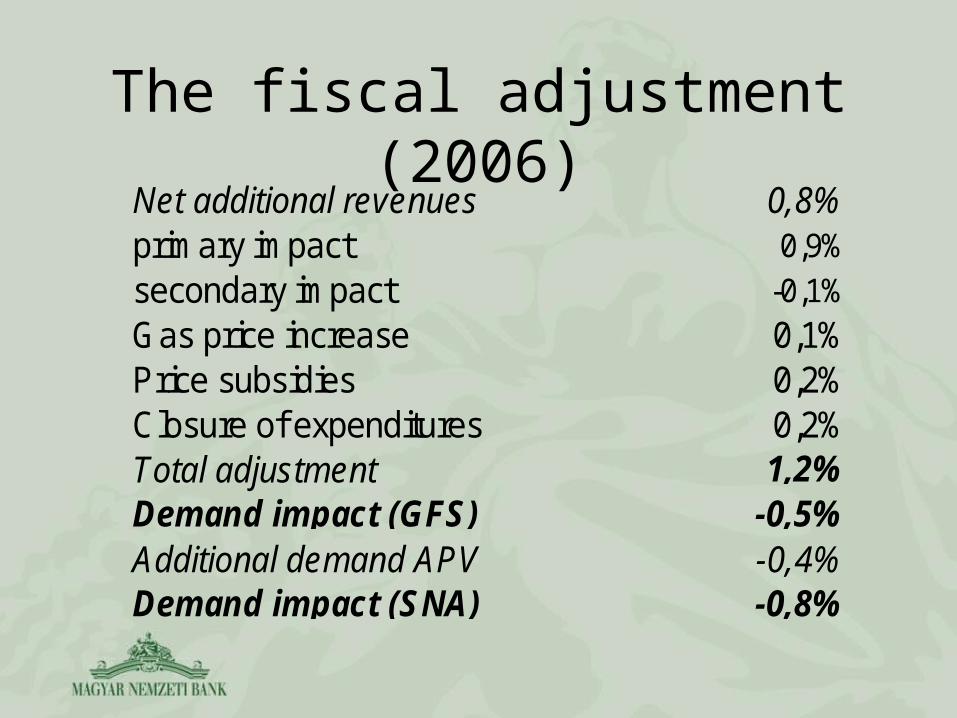

The fiscal adjustment (2006)

Net additional revenues 0,8%primary impact 0,9%secondary impact -0,1%Gas price increase 0,1%Price subsidies 0,2%Closure of expenditures 0,2%Total adjustment 1,2%Demand impact (GFS) -0,5%Additional demand APV -0,4%Demand impact (SNA) -0,8%

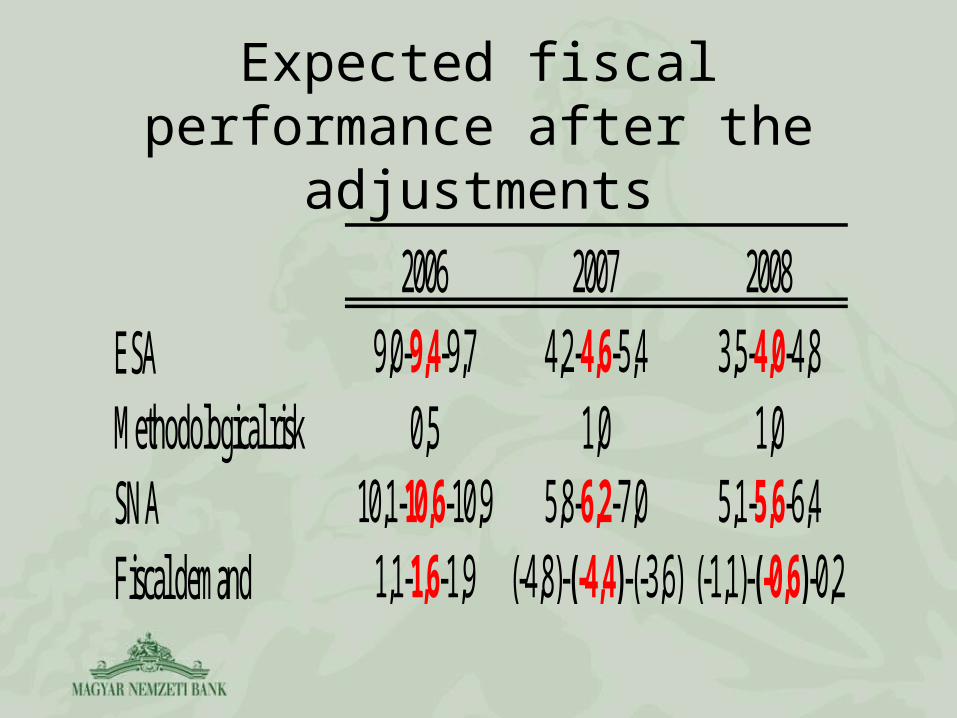

Expected fiscal performance after the adjustments

2006 2007 2008ESA 9,0-9,4-9,7 4,2-4,6-5,4 3,5-4,0-4,8Methodological risk 0,5 1,0 1,0SNA 10,1-10,6-10,9 5,8-6,2-7,0 5,1-5,6-6,4Fiscal demand 1,1-1,6-1,9 (-4,8)-(-4,4)-(-3,6) (-1,1)-(-0,6)-0,2

Fiscal demand impact developments

-6-5-4-3-2-1012345

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

%

On the expected impact• 4 „pure type” (Horváth et al, MNB

Ocasional Papers 52, 2006)• The standard shock makes 1% of

GDP fiscal adjustment• Current adjustment: Linear

combination of the 4 pure shock• The tool we have used: MNB NEM

model– Neo-keynesian model, backward

looking expectations– estimated for the Hungarian economy

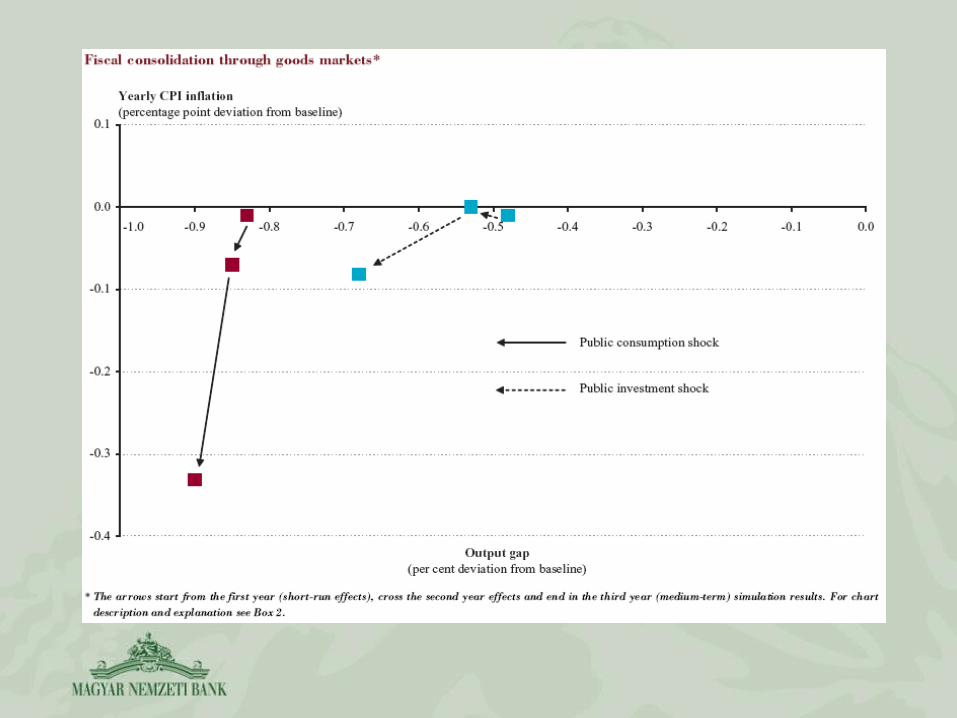

1. Fiscal consolidation through goods markets

• Cut in public consumption or investment

• relative large first year growth drop (0,5-0,9 multiplier)

• The negative impact of investment cut is smaller due to higher import content

• Positive but small inflationary impact: max -0,35% after 3 years

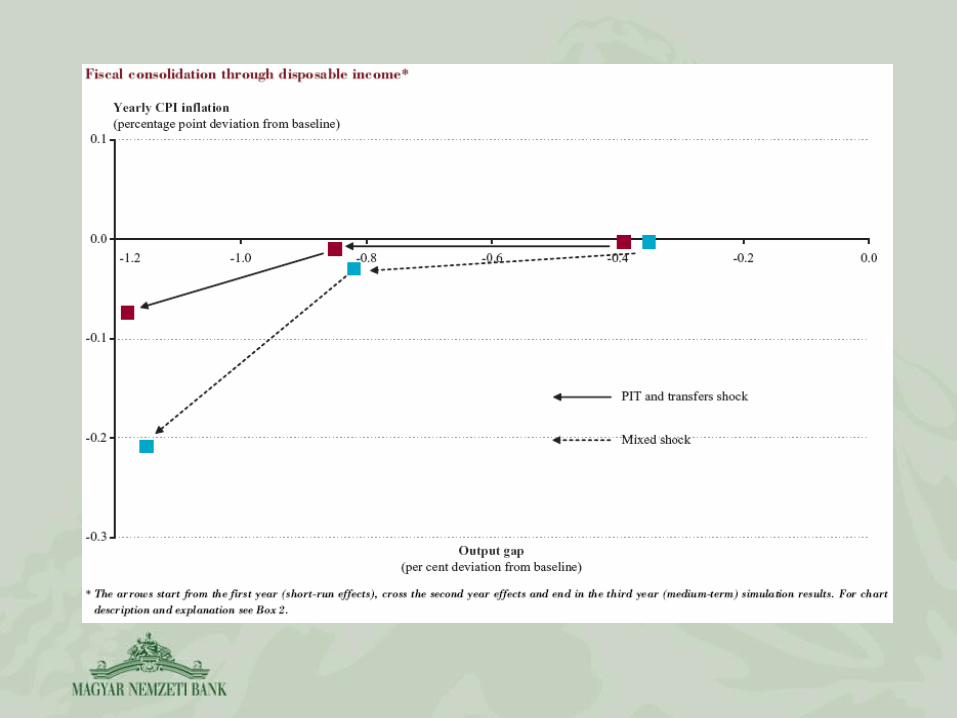

2. Consolidation through disposable income

• Indirect effects – tax hikes, transfer reductions– Through disposable income– Important: No supply side

reactions modeled• The effects „slowly” appears• Smaller output loss in the short

run, larger in the long run• Small positive inflationary impact

3. Consolidation through labour markets

• Reducing public employment or increasing social security contributions (SSC)

• Slow but strong impacts• Largest long term GDP sacrifice• Inflation: different in the two scenario

– SSC case increases inflation– Reduction in employment decreases

inflation• SSC case raises a monetary policy

dilemma

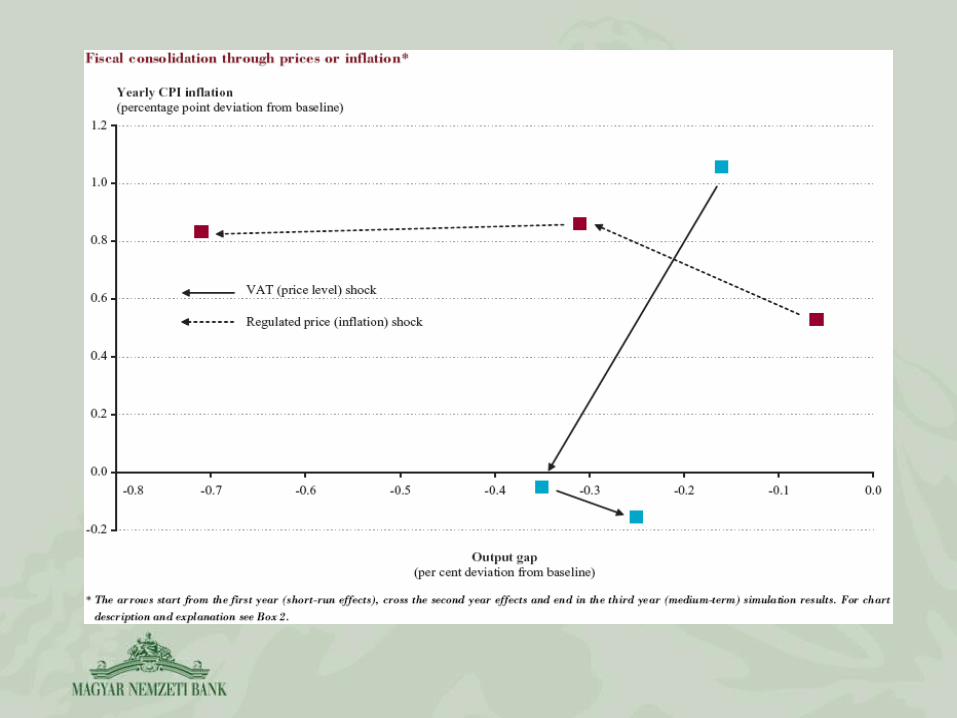

4. Consolidation through prices or inflation

• (non-energy) regulated price hikes or indirect taxation

• indirect taxation: temporary rise in inflation and small GDP decline

• (non-energy) regulated price: persistent inflationary impact, larger negative long term growth impact– It raises monetary policy dilemma

The monetary policy dilemma • Three type of adjustment from monetary

policy point of view– GDP hardly change, inflation rises temporary

(VAT case, 4A)– GDP and inflation both declines in the short

run (1, 2)– GDP declines, inflation rises in the short run

(regulated prices, SSC increase, 3, 4B)• The implied monetary policy reaction

– 1st type: no reaction needed– 2nd type: policy loosening– 3rd type: ambiguous policy reactions

• How important is the inflation in the reaction function?

• How well anchored the inflationary expectations are?

Our preliminary quantitative assessment

Inflation Report May 2006GDP Inflation CA

20064,5 2,1 8,320074,2 3,3 8,220083,8 3,2 8,0

After the adjustmentGDP Inflation CA

20064,5 3,3 8,320072,0-3,0 6,0-7,0 5,0-6,020082,0-3,0 3,5-4,5 5,0-6,0

Qualitative assessment• First step to the right direction to

reduce vulnerabilities• Poor quality from the long term

sustainability point of view– Revenue oriented– Inflationary

• Fiscal transparency has not improved (so far)

• Poor communication

Thank you for your attention!

The views expressed here are those of the authors and do not necessarily reflect the official view of the central bank

of Hungary (Magyar Nemzeti Bank).