Housing Financing and Leveraging MHSA Dollars CSH 9/07.

34

Housing Financing and Leveraging MHSA Dollars CSH 9/07

-

Upload

lilian-freeman -

Category

Documents

-

view

219 -

download

1

Transcript of Housing Financing and Leveraging MHSA Dollars CSH 9/07.

Housing Financing and Leveraging

MHSA Dollars

CSH 9/07

Objectives

How housing projects are financed Types of funding sources How communities can use MHSA funds to

create more housing How to leverage other funding sources

The Three “Flavors” of Money

Capital Operating

Services

How Funding for Supportive Housing Is Used

Type Uses

CAPITAL Land, buildings, new construction, soft costs of development, capitalized reserves

OPERATING Property operations such as management staff, landscaping, utilities, reserves

SERVICES Delivery of supportive services to tenants

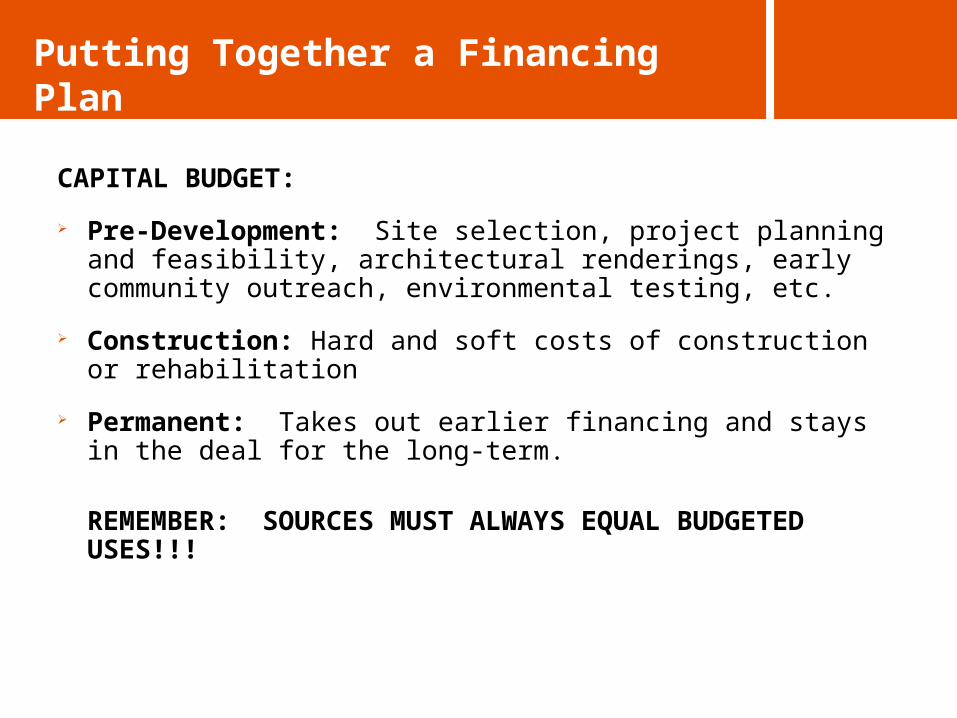

Putting Together a Financing Plan

CAPITAL BUDGET:

Pre-Development: Site selection, project planning and feasibility, architectural renderings, early community outreach, environmental testing, etc.

Construction: Hard and soft costs of construction or rehabilitation

Permanent: Takes out earlier financing and stays in the deal for the long-term.

REMEMBER: SOURCES MUST ALWAYS EQUAL BUDGETED USES!!!

Putting Together a Financing Plan

SERVICES BUDGET:

Wide array of relevant, efficient supports that enable individuals to maintain their housing.

REMEMBER: SOURCES MUST ALWAYS EQUAL BUDGETED USES!!!

Putting Together a Financing Plan

OPERATING BUDGET: The cost to operate the property Rents in supportive housing usually don’t cover these costs

EXAMPLE:Amount a tenant can afford in rent $210Monthly cost to operate a unit $435GAP THAT NEEDS TO BE FUNDED ($225)

AND REMEMBER: SOURCES MUST ALWAYS EQUAL BUDGETED USES!!!

Putting Together a Financing Plan: Addressing the Operating Gap

Operating Gaps can be addressed in two ways:

Obtain a rental or operating subsidy that will pay for that gap on a monthly or annual basis.– Such sources include: Project or Sponsor

Based Shelter Plus Care and Section 8 Vouchers

Capitalize upfront to cover the gap over time. - The MHSA Housing Program offers the

opportunity to apply for capitalized operating subsidy funds.

Capitalized Operating Reserves

Concept:

Establish a fund at the beginning of the project to meet the operating deficits you know you’ll experience over time (best to plan for as long a term as possible – the MHSA Housing Program application allows for up to 20 years)

CalHFA holds these funds and disburses them quarterly to the project.

Regular, scheduled draw downs subsidize rent over time

Calculating a Capitalized Operating Reserve

MHSA Example – Attachment B Operating Cost Per Unit (per year): $6,000Rental Income (per year): $2,536

Expected Operating Deficit Per Unit (Year 1): ($3,464)

Required Reserve (Per Unit),Based on 20-year operations period: $100,000

Capital Financing

What are Sources of Capital Funding?

FEDERAL Section 811, HOPWA, HOME, CDBG, Section 515 Rural Loans, Rural Homeless Assistance, Supportive Housing Program (SHP) (HOME, CDBG and HOPWA often administered by local gov’t or State)

STATE Low Income Housing Tax Credits (Tax Credit Allocation Committee), Multifamily Housing Program (MHP), CalHFA, Rural Predev. Loans, MHSA

LOCAL Redevelopment Agency Funds,

Housing Trust Funds, Inclusionary Funds

Intermediaries and Banks

Various loan and grant products

Prop 1C Supportive Housing Funds:

195 Million available at the state level

50 Million available specifically for supportive housing for youth

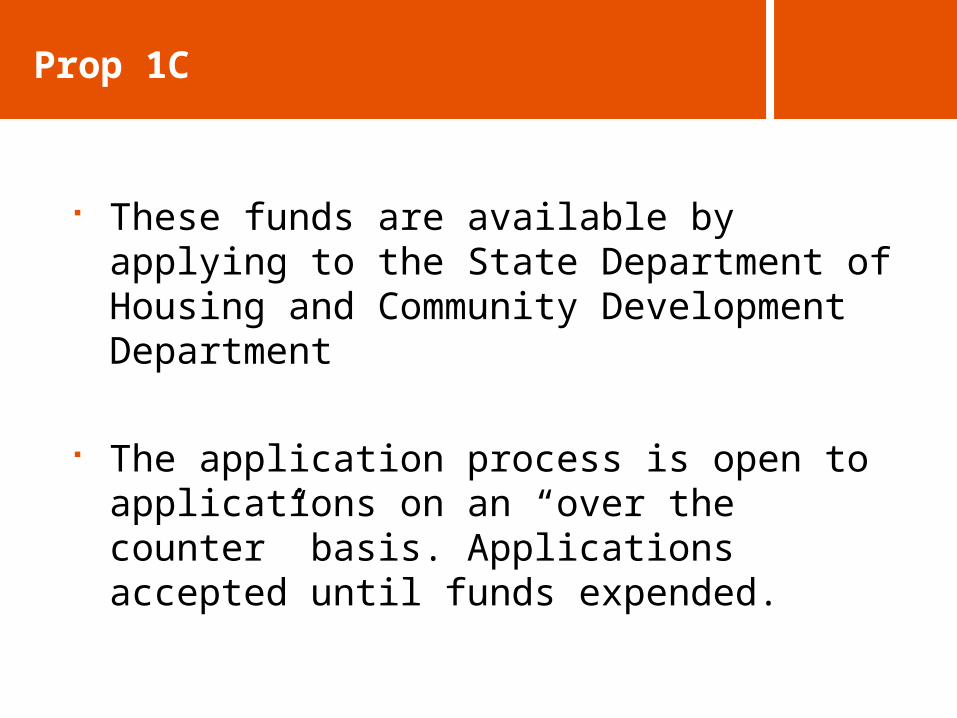

Prop 1C

These funds are available by applying to the State Department of Housing and Community Development Department

The application process is open to applications on an “over the counter” basis. Applications accepted until funds expended.

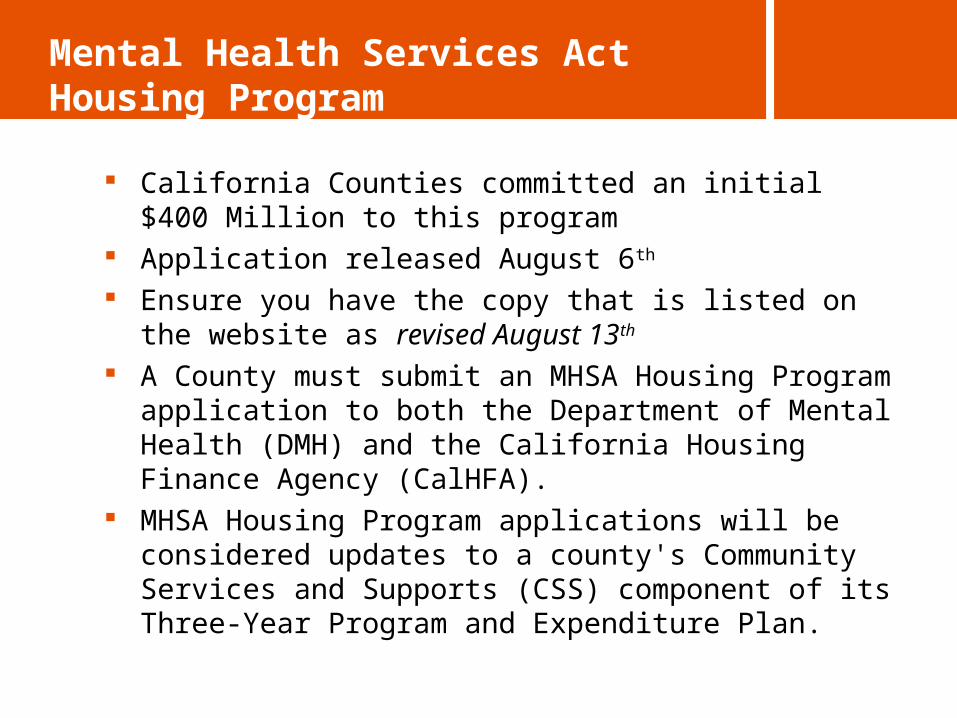

Mental Health Services Act Housing Program

California Counties committed an initial $400 Million to this program

Application released August 6th

Ensure you have the copy that is listed on the website as revised August 13th

A County must submit an MHSA Housing Program application to both the Department of Mental Health (DMH) and the California Housing Finance Agency (CalHFA).

MHSA Housing Program applications will be considered updates to a county's Community Services and Supports (CSS) component of its Three-Year Program and Expenditure Plan.

Operating Financing

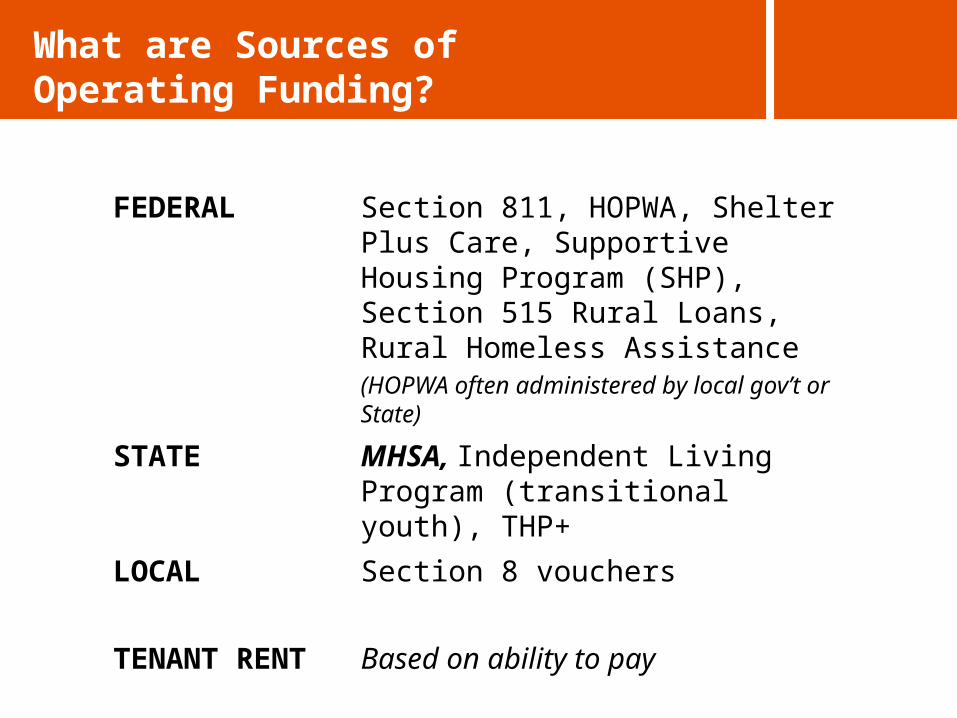

What are Sources of Operating Funding?

FEDERAL Section 811, HOPWA, Shelter Plus Care, Supportive Housing Program (SHP), Section 515 Rural Loans, Rural Homeless Assistance(HOPWA often administered by local gov’t or State)

STATE MHSA, Independent Living Program (transitional youth), THP+

LOCAL Section 8 vouchers

TENANT RENT Based on ability to pay

Services Financing

Where are Sources of Services Funding?

FEDERAL HOPWA, Supportive Housing Program (SHP) (HOPWA often administered by local gov’t or State)

STATE MHSA, THP+

LOCAL County Departments of Health and Human Services, Mental Health, Alcohol and Drug, HIV/AIDS and other social service programs, private foundations, MediCal

Leveraging Funds

Leverage is the Name of the Game

Supportive housing finance involves MANY different sources

Funders like to LEVERAGE their resources

Funders want others to share in the cost of developing a project; to share in the risk

Some funders will establish either a match requirement or a percentage of the total costs that they will contribute to a project

MHSA funding can be used with any of the other sources identified.

MHSA can “jump-start” a development serving your population and attract other funding sources.

Since MHSA funding is flexible, it can be used to fill gaps left once you’ve exhausted all other sources.

Please see the “CSH Supportive Housing Financing Map” for more information on leveraging MHSA dollars.

MHSA Funds Can Leverage Other Funds

Projecting and/or Evaluating

Operating Costs in Supportive

Housing

Tenancy Considerations

Identifying the Target Population(s) – community need, services experience and capacity

Planning the Unit / Tenant Mix – income levels, intensity of service needs, services experience and capacity, marketing plan

Tenant Income Considerations – rent levels, subsidized vs. non-subsidized units, employment histories, access to public benefits.

Planning for Changing Needs over Time – initial lease-up vs. projected vacancy rate, tenants’ increased stability

Vacancy factors should be tailored to the target population and local market conditions.

In supportive housing, vacancy factors may be as high as 10 – 12%, depending on target populations, referral and screening processes.

Vacancy Factors

Management Fee - % or per door fee

Office Supplies & Expenses

Legal – evictions, etc…

Accounting - tax filings, audit, reporting to investors

Operating Budget Categories

Staff / Payroll Costs

Administrative Payroll

Maintenance Payroll

Security Payroll

Operating Budget Categories

Utilities Heating Master Metering Common Area Utilities Water & Sewer Telephone

Operating Budget Categories

Maintenance and Repair Exterminating Supplies Repairs Trash Removal Snow Removal Grounds Upkeep & Landscaping Painting & Decorating Elevator Maintenance

Operating Budget Categories

Marketing and Leasing Advertising Credit Investigations/Leasing

Fees

Operating Budget Categories

Taxes and Insurance Real Estate Taxes Other Taxes Property Insurance

Operating Budget Categories

Contributions to Reserves

Replacement Reserves

Operating Reserves

Operating Budget Categories

Trending

Apply growth factors to both income (typically 1% to 3%) and expenses (typically 3% to 4%).

Growth factors may vary for subsidized vs. non-subsidized units, market-rate units vs. rent-restricted units

“Spread” = difference between income growth factor and expense growth factor.

Developing Supportive Housing

Additional CSH Resources: Publications: Not a Solo ActBetween the Lines: Legal Issues in Supportive HousingLaying A New the FoundationFamily Matters

WEB resources: On-line financing summaries (via Resource Library link) Toolkit for Ending Long-term Homelessness