here - Yole Developpement

32

Transcript of here - Yole Developpement

SEPTEMBER 11-12, 2013Seattle, WA, USA

PLATINIUM SPONSORS

“MEMS in Motion is a different way of doing business…you’re going to see a lot more of these in the future. I’ll attend again, and I’d recommend it to other companies in the MEMS fi eld.” John Brashear, VectorNav Technologies MEMS in Motion 2012 Participant “I love MEMS in Motion. I will absolutely dedicate the time to make sure I attend next time.” Kevin Shaw, Sensor Platforms MEMS in Motion 2012 Participant “I am extremely pleased with MEMS in Motion. It was great and I am looking forward to next year’s summit!” Vincent Fortin, Teledyne DALSA MEMS in Motion 2012 Participant “Some conferences you have just speakers and listeners, presentation afterpresentation. Forums like MEMS in Motion force interaction between peoplewhich tend to be more productive meetings. I would recommend this event to other industry people—100 percent.” Tom Flynn, Coventor MEMS in Motion 2012 Participant

Industry leaders will gather for the third edition of the two-day MEMS in Motion event. Qualified attendees will enjoy exclusive plenary sessions; hours of one-on-one meeting opportunities, plus a variety of social activities.

Mark your calendar, and help shape the future of inertial devices.

SAVE THE DATE

For more information,please contact S.Leroy at [email protected]

E D I T O R I A L

M E M S ’ T r e n d s 3

A P R I L 2 0 1 3 I S S U E N ° 1 4

PLATInum PARTnERs:

The $1B MEMS business model

Despite widespread semiconductor market contraction, the 2012 mEms segment

exhibited strong unit and business growth. This growth directly correlates with

the tremendous development of new portable device features, as well as sensor

adoption in consumer electronics and continuous expansion of automotive

applications. STMicroelectronics managed to reap the full benefits of this diversity,

reaching $1B in sales last year. As confirmed by Benedetto Vigna: “Unless you

have a wide portfolio, you can’t play a big role”.

The proliferation of applications linked to sensor penetration in mobile devices

has driven enormous sensor diversity and pushed standardization out of

manufacturing’s focus. In fact, the gap between consumer and industrial

applications is widening. On the one hand, mEms is becoming a commodity;

on the other hand, it remains highly strategic. This is clearly demonstrated by

sagem’s acquisition of Colibrys, the high-end gyros manufacturer.

On the subject of device criticality, there’s no need for an image stabilizer to

last more than a few years, while an engine oil pressure sensor must maintain

performance for 5+ years. Also, the price that the customer is willing to

pay is not driven by a device’s complexity, but by the features it offers. For

instance, embedding a $200 sensor in a plane is acceptable, but not in a phone.

Hardware specifications drive MEMS sensor design and increase complexity and

diversification, notwithstanding manufacturing cost.

more than ever, Yole Développement’s mEms law rings true: each company has

the process knowledge to create its own devices, with no need for industry

standardization. The numbers speak for themselves: five gyro makers using five

different processes are in the Top 10; no one is pushing standardization. so what

happens next? Yole Développement anticipates a significant push from consumer

electronics for cost reduction. Experience tells us this can only happen through

platform standardization, led by m&As and consolidation, resulting in large,

powerful mEms manufacturers.

Who will win: diversity or standardization? I’m convinced this issue of mEms

Trends will provide some answers.

Christophe FitamantSales & Marketing DirectorYole Dé[email protected]

For more information, please contact S. Leroy ([email protected])

...The gap between consumer and

industrial applications is widening...

• 19th World Micromachine Summit (MMS 2013) April 21 - shanghai, China

• MEPTEC - 11th Annual MEMS Technology Symposium may 22 - san Jose, usA

• Sensors Expo & Conference June 5 to 6 – Rosemont, usA

• Transducers June 16 to 20 – Barcelona, spain

E V E n T S

A P R I L 2 0 1 3 I S S U E N ° 1 4

gOLD PARTnERs:

FINANCIAL BUZZ • Sagem's acquisition of Colibrys: a game-changer 6

MEMS IN THE WORLD • MEMS in China – Semicon China 2013 8

INDUSTRY REVIEW • Top MEMS companies 2013: Smart phone market re-orders the MEMS

industry 10

ANALYST CORNER • Steady 10-12% growth will double the MEMS market over next six years 16

COMPANY INSIGHT • Tronics talks about industrializing CEA-LETI’s M&nEMS technology 20

• MicroVision gets consumer electronics partner 22

• X-FAB targets MEMS for growth in More-than-Moore foundry strategy 24

• SiTime: MEMS timing comes to mobile market 26

• BodyMedia goes beyond motion tracking to condition monitoring 28

EUROPEAN PROjECT • European Commission proposes to invest billions to provide finance

for new European technologies and small companies 30

C O n T E n T s

FROM I-MICRONEWS.COM

Stay connected with your peers on i-Micronews.com

W i t h 2 0 , 0 0 0 m o n t h l y v i s i t o r s , i-micronews.com provides for mEms area: cur rent news, market & technological analysis, key leader interviews, webcasts section, reverse engineering / costing, events calendar, latest reports…

Please visit our website to discover the last top stories in MedTech - Microfluidics and BiomEms:• ATEC and Sencio Sign Strategic Deal

to strengthen Assembly services for mEms and sensors

• Mouser expands IC and sensor lineup with Elmos and smI

• Growing MEMS markets by rethinking manufacturing

• Tronics reports record 2012 income of 16.7 million Euros

• SGX launch innovative MEMS pellistor

4 M E M S ’ T r e n d s

Courtesy of Benedetto Vigna, Corporate Vice President, General Manager of the Analog, MEMS and Sensors Product Group, STMicroelectronics

Sagem's acquisition of Colibrys: a game-changer

A P R I L 2 0 1 3 I S S U E N ° 1 4

6 M E M S ’ T r e n d s

F I n A n C I A L B u z z

Laurent Robin, Activity Leader,Inertial MEMS Devices& Technologies, Yole Développement

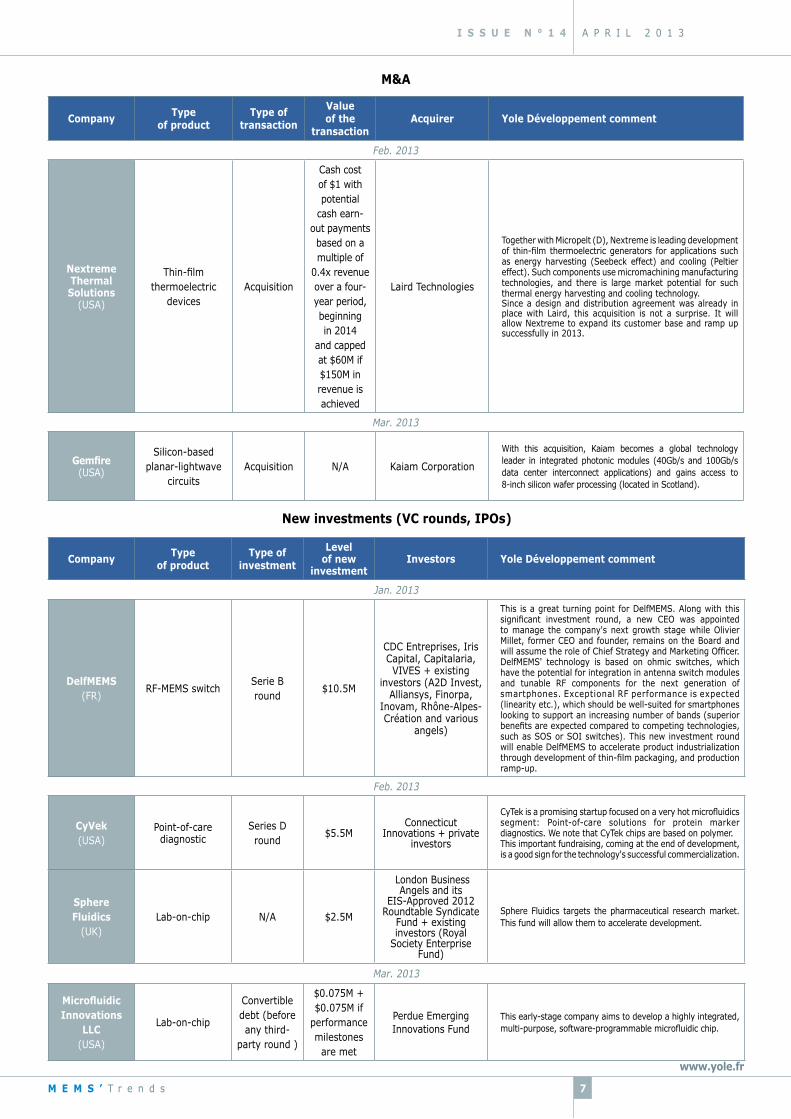

Over the last three months, Yole Développement has listed many microfluidics-related deals, including several fundraisings and one large acquisition (by Illumina). However, during that timespan two other significant transactions occurred in the silicon MEMS sector.

Company Typeof product

Type of transaction

Value of the

transactionAcquirer Yole Développement comment

Jan. 2013

Verinata Health, Inc

(usA)

In-vitro diagnostics

Acquisition

$350m, plus up to $100m in milestone payments through 2015

Illumina

Verinata began as a microfluidics company developing a technology based on patents from mIT and Harvard. With its acquisition, Illumina gains access to a large patent portfolio and a new, rapidly-growing market segment: prenatal test. not surprsingly, expectations are high.This is yet another strategic acquisition for Illumina, coming only a few months after its acquisition of Bluegnome.

Colibrys(CH)

High-performance mEms

accelerometer and foundry service

Acquisition n/A sagem sagem acquired Colibrys (see article below)

M&A

The first is Sagem's acquisition of Colibrys, which was the only provider of ITAR-free, high-end accelerometers to the military industry.

many developments are expected in the aftermath of this deal, as detailed in the analysis below.

The second is DelfMEMS' B round, which paralleled their CEO change. RF architecture changes linked to LTE introduction (and soon carrier aggregation)

are driving the need for new technologies; this was a hot topic at the recent mobile World Congress in Barcelona. For instance, there is an increasing demand for tuner components -- an area where we believe a large range of new devices will be introduced (mEms and non-mEms technologies) and where big RF companies such as RFmD, Qualcomm and On semiconductor will get involved, in addition to well-known start-ups.

Sagem is the world's 3rd-largest inertial sensor company, after Honeywell and northrop grumman. Yole estimates its 2011 revenue for Inertial Measurement Units was $165M (see the report “Gyroscope and Imus for Defense, Aerospace & Industrial”).For Sagem, this is a big change: for the first time, it gains access to a mEms technology, meaning the company is now involved in all major inertial technologies. It's likely that significant funds will need to be injected into Colibrys to pursue accelerometer developments -- and if sagem wants to develop a mEms gyro technology (which has always been on Colibrys' roadmap, but has never developed due to lack of funding), they'll have to spend even more. This transaction is not a big surprise, since the two companies had been close collaborators for several years, specifically on development of a new close-loop accelerometer to compete with Honeywell's QA-2000. The idea was to use it primarily for commercial aerospace.We expect this deal to have a huge impact on the competitive landscape, since Colibrys was the only firm able to sell such a high-performance accelerometer on the open market, and ITAR-free. Colibrys' direct competitors, including silicon Design (in the usA, but mostly for

industrial applications), Tronics (seismic applications, mainly) and Physical Logic (Israel, but not in mass-production yet) should benefit from the deal. Additionally, some gyroscope players may choose to enter the accelerometer market, and certain players currently limited to the industrial and medical markets could try to enter the aerospace and defense segments.We note that several large system manufacturers who used to buy Colibrys' accelerometers, such as AIS/ Goodrich and Al Cielo, could be impacted by this acquisition. since Colibrys was the only company selling such products, their old customers now need to either make an agreement with sagem, or manufacture similar components internally. For instance, Goodrich is using Colibrys' accelerometer in its MEMS IMUs, but was preparing for a transition to its own silicon mEms accelerometer technology, manufactured by sss, which introduced such products at the end of 2012. With such a critical component, it's difficult to quicky switch from one manufacturer to another, but we surmise that long-term agreements on existing contracts were already in place between goodrich and sss for some time, in order to cover contingencies such as the sagem/Colibrys acquistion.

M&A : Sagem acquired Colibrys

Company Typeof product

Type of investment

Level of new

investmentInvestors Yole Développement comment

Jan. 2013

DelfMEMS(FR)

RF-mEms switchserie B round

$10.5m

CDC Entreprises, Iris Capital, Capitalaria, VIVES + existing

investors (A2D Invest, Alliansys, Finorpa,

Inovam, Rhône-Alpes-Création and various

angels)

This is a great turning point for DelfmEms. Along with this significant investment round, a new CEO was appointed to manage the company's next growth stage while Olivier millet, former CEO and founder, remains on the Board and will assume the role of Chief Strategy and Marketing Officer.DelfMEMS' technology is based on ohmic switches, which have the potential for integration in antenna switch modules and tunable RF components for the next generation of smartphones. Exceptional RF performance is expected (linearity etc.), which should be well-suited for smartphones looking to support an increasing number of bands (superior benefits are expected compared to competing technologies, such as sOs or sOI switches). This new investment round will enable DelfmEms to accelerate product industrialization through development of thin-film packaging, and production ramp-up.

Feb. 2013

CyVek(usA)

Point-of-care diagnostic

series D round

$5.5mConnecticut

Innovations + private investors

CyTek is a promising startup focused on a very hot microfluidics segment: Point-of-care solutions for protein marker diagnostics. We note that CyTek chips are based on polymer.This important fundraising, coming at the end of development, is a good sign for the technology's successful commercialization.

Sphere Fluidics

(uK)Lab-on-chip n/A $2.5m

London Business Angels and its

EIs-Approved 2012 Roundtable syndicate

Fund + existing investors (Royal

society Enterprise Fund)

sphere Fluidics targets the pharmaceutical research market. This fund will allow them to accelerate development.

Mar. 2013

Microfluidic Innovations

LLC(usA)

Lab-on-chip

Convertible debt (before any third-

party round )

$0.075m + $0.075m if

performance milestones

are met

Perdue Emerging Innovations Fund

This early-stage company aims to develop a highly integrated, multi-purpose, software-programmable microfluidic chip.

New investments (VC rounds, IPOs)

www.yole.fr

I S S U E N ° 1 4 A P R I L 2 0 1 3

7M E M S ’ T r e n d s

Company Typeof product

Type of transaction

Value of the

transactionAcquirer Yole Développement comment

Feb. 2013

Nextreme Thermal Solutions

(usA)

Thin-film thermoelectric

devicesAcquisition

Cash cost of $1 with potential

cash earn-out payments based on a multiple of

0.4x revenue over a four-year period, beginning in 2014

and capped at $60m if $150m in revenue is achieved

Laird Technologies

Together with micropelt (D), nextreme is leading development of thin-film thermoelectric generators for applications such as energy harvesting (seebeck effect) and cooling (Peltier effect). such components use micromachining manufacturing technologies, and there is large market potential for such thermal energy harvesting and cooling technology.since a design and distribution agreement was already in place with Laird, this acquisition is not a surprise. It will allow nextreme to expand its customer base and ramp up successfully in 2013.

Mar. 2013

Gemfire (usA)

silicon-based planar-lightwave

circuitsAcquisition n/A Kaiam Corporation

With this acquisition, Kaiam becomes a global technology leader in integrated photonic modules (40gb/s and 100gb/s data center interconnect applications) and gains access to 8-inch silicon wafer processing (located in scotland).

M&A

Electronica China is a great event for meeting mEms players, while semicon China is geared towards general semiconductor and

equipment players. The mEms conferences and forums within both shows were very valuable, covering topics such as CsTIC 2013, automotive electronics applications and development, and mEms technology.

CsTIC (China semiconductor Technology International Conference) was as interesting as ever. Chinese companies and R&D centers presented their latest semiconductor manufacturing progress, including new mEms device developments. Also discussed were CmOs technology, new materials such as gan and siC for power devices, and different key manufacturing processes such as lithography, patterning and etching. During the conference, experts from well-known companies like IBM, Fujifilm and Dow Chemical gave informative speeches.

Advanced packaging technologies were hot topics at the mEms technology forum: 3DIC, wafer-level packaging, TSV, etc. attracted many attendees. CEOs and experts shared their point-of-view at both the technical and application level, while Yole Développement’s “MEMS Everywhere – Making the World more sensitive” presentation revealed our mEms market perspective and offered a glimpse at the future of global and emerging mEms devices.

As China is the world’s #1 market in vehicle production and sales, the forum dealing with automotive electronics applications, development and mEms technology was time well-spent. Constant innovation, coupled with growing customer expectations, has resulted in an ever-increasing range of emerging technologies, with new products continually being designed to improve control functions, engine performance, infotainment and other electronically-driven systems. The forum gave experts a chance to exchange opinions on the

Chinese automotive market and present their latest technologies; also, Yole Developpement was invited to give a presentation on “MEMS for Automotive Applications.”

Through all of these events and discussions with local players, it became obvious that the Chinese mEms market is consistently growing – perhaps faster than we first expected! Local MEMS fabless players and design houses are making real efforts to adopt new technologies and commence mass-production as soon as possible, in collaboration with foreign foundries, fabs and R&D centers.

The hottest components remain mEms microphones, pressure sensors, inertial sensors (accelerometers, gyroscopes and compasses) and infrared microbolometers. Combo sensors, either accelerometer + gyroscope or accelerometer + magnetometer, 6DOF or 9DOF, are very interesting for Chinese players like senodia and miramEms. The target market for these companies is still the low-end Chinese consumer electronics market (a.k.a. the “Shanzhai” market). Big manufacturers still prefer to use well-known companies’ products – and so at this early stage of development/production, companies like senodia and miramEms would rather go for low-end segments in order to be first to market.

Another promising device in China is the infrared microbolometer, for which there’s a huge and growing need in automotive applications. night vision is this market’s most popular sub-application. since fabless companies have grown to the point that mature foundries can no longer fulfill their needs, local foundry services have become a hot topic in China, with the government investing in existing foundries and new projects in order to increase the number of qualified players. SMIC, AsmC, CsmC and gsmC have all announced they’re ready for production, while other pilot lines in suzhou, zibo, Beijing, and shanghai are in development or construction. Consequently, we expect to see mature foundry players appearing in China very soon.

www.yole.fr

MEMS in China – Semicon China 2013

A P R I L 2 0 1 3 I S S U E N ° 1 4

8 M E M S ’ T r e n d s

m E m s I n I n T H E W O R L D

Wenbin Ding, Technology & Market Analyst, MEMS Devices& Technologies, Yole Développement

As usual, Yole Developpement attended march’s semicon China and Electronica China 2013 events in order to remain immersed in the Chinese mEms market.

MEMSensing's new packaged MEMS microphone (Courtesy of MEMSensing)

MiraMEMS’s 3-axis accelerometer and 3-axis magnetometer (Courtesy of MiraMEMS)

All over the World,stay connected

In-depth market & technology analysiswith a strategic eyeCombined reach to over 14,000 subscribersElectronic magazines - Quartely frequency

For more information, please visit www.i-micronews.comEditorial, Advertising & Subscriptions: S. Leroy ([email protected])

ISSUE N°5SEpTEmbER 2012

I n n o v a t i o n i n S o l i d S t a t e L i g h t i n g

LED

Prin

ted o

n r

ecyc

led p

aper

AnALyST CORnER2010’s blow-out cycle marked LED industryinvestment peak

COmpAny InSIGHT Veeco comes at lower LED costs from two sides

InDUSTRy REvIEW Front-end toolmakers support LED profi t push

F r e e r e g i s t r a t i o n o n www.i-micronews.com

TECHNOLOGY MAGAZINES

Powered by:

Part of Micronews Media

Prin

ted o

n r

ecyc

led p

aper

Prin

ted o

n r

ecyc

led p

aper

AnALyST CORnER2010’s blow-out cycle marked LED industryinvestment peak

COmpAny InSIGHT Veeco comes at lower LED costs from two sides

ISSUE N°7

OCTOBER 2012

Connect ing the Power E lectron ic Supply

IndusTRy REvIEw

Power module

producers blaze

new trails

COMPAny InsIGHT

Specialty Coating

Systems: Parylene

films show their

dielectric strengt

AnALysT CORnER

Electric vehicles

drive packaging

innovation

F r e e s u b s c r i p t i o n o n www.i-micronews.com

dev’POWER

Prin

ted

on r

ecyc

led

pape

r

ISSUE N°7

OCTOBER 2012

Connect ing the Power E lectron ic SupplyPOWERPOWER

Prin

ted

on r

ecyc

led

pape

r

Free subscription on www.i-micronews.com

ISSUE N°12

OCTOBER 2012

M a g a z i n e o n M E M S T e c h n o l o g i e s & M a r k e t s

INDUSTRY REVIEW

Emerging MEMS

ANALYST CORNER

Energy harvesting

market will approach

$250M in fi ve years.

COMPANY INSIGHT

poLight readies

production of optical

MEMS autofocus

MEMS’Trends

Firstrelease

in Sept.

2013

F r e e r e g i s t r a t i o n o n www.i-micronews.com

InDUSTRy REvIEW Front-end toolmakers support LED profi t push

IndusTRy TRy TR REvIEw

Power module

producers blaze

new trails

COMPAny InsIGHT

Specialty Coating

Systems: Parylene

films show their

dielectric strengt

AnALysALysAL T CORnER

Electric vehicles

drive packaging

innovation

F r e e s u b s c r i p t i o n o n www.i-micronews.com

3DPackaging Magazine on 3DIC, TSV, WLP & Embedded die Technologies

ISSUE N°24AUGUST 2012

Prin

ted o

n r

ecyc

led p

aper

F r e e s u b s c r i p t i o n o n www.i-micronews.com

INDUSTRY REVIEWEquipment makers say tools are ready for initial volumes of 2.5D/3DIC production

COMPANY INSIGHTSekisui Chemical: Reliability innovation in large size & fi nepitch WLCSP

ANALYST CORNERThe place of “middle-end” in the future landscape of 2.5D / 3DIC chip-to-package manufacturing

I n D U S T R Y R E V I E W

A P R I L 2 0 1 3 I S S U E N ° 1 4

Top MEMS companies: Smart phone market re-orders the MEMS industry

M E M S ’ T r e n d s10

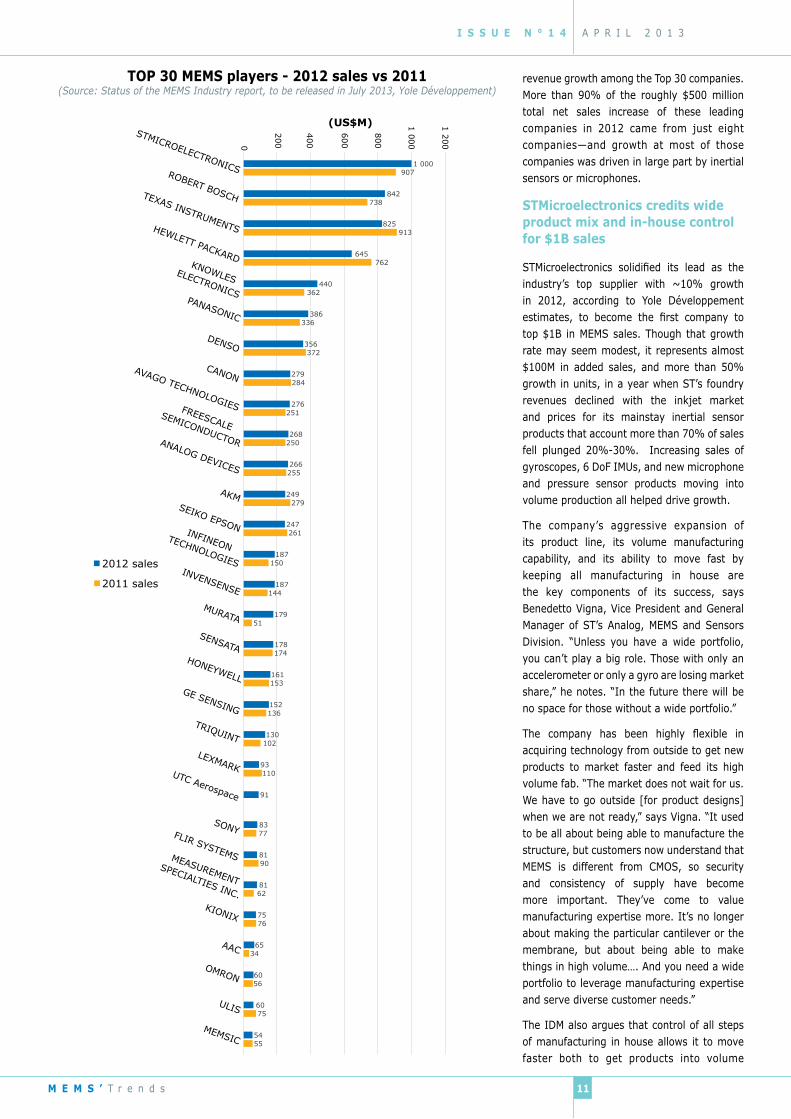

This year for the first time the top two MEMS suppliers on our annual Top 30 mEms company ranking are suppliers of inertial

sensors, not of the inkjet heads or micro-mirror actuators that long dominated the sector. And the expanding demand for mEms in both smart phones and automotive applications is creating a rising group of players with solid sales not so far behind.

STMicroelectronics (ST), the first company to grow a $1 billion mEms business, has clearly moved past Texas Instruments (TI) to become the sector’s largest company. Robert Bosch, with ~$842 million in mEms sales, has also pushed ahead of both TI and Hewlett Packard (HP) for the first time to become the second ranking player, according to Yole Développement figures.

Other companies with healthy growth from the right products in the right markets are closing the once large gap between the industry leaders and the rest of the industry. Knowles Electronics climbed

into fourth place with some $440 million in mEms microphone sales, closing in on HP. Panasonic and Denso each achieved better than $350 million in mEms sales in their largely automotive markets. nearly half of the Top 30 now have mEms revenues of more than ~$200 million.

On mEms foundry side, the Invensense inertial sensor business helped drive 80% growth at TSMC to ~$42 million, pushing the CmOs giant’s mEms sales up past the top pure-play specialty mEms foundries Teledyne DALsA at ~$39 million and silex microsystems at ~$34 million. IDms sT and sony continue to dominate the foundry business, though, with their contract production for big customers HP and Knowles respectively. note that we count only the value of the mEms production, not that of the AsIC.

Just how much the mEms market is currently being driven by inertial sensors and microphones is also clear from looking at who captured most of the total

strong demand for inertial sensors and mEms microphones for smartphones has re-ordered the mEms industry, with new industry leaders, and a crowd of fast followers closing the gap between the big four and a rising middle class.

“Unless you have a wide portfolio,

you can’t play a big role. Those with only an accelerometer or

only a gyro are losing market share,” says

Benedetto Vigna,sTmicroelectronics.

Xtrinsic eCompass Software(Courtesy of Freescale)

I n D U S T R Y R E V I E W

revenue growth among the Top 30 companies. More than 90% of the roughly $500 million total net sales increase of these leading companies in 2012 came from just eight companies—and growth at most of those companies was driven in large part by inertial sensors or microphones.

STMicroelectronics credits wide product mix and in-house control for $1B sales

STMicroelectronics solidified its lead as the industry’s top supplier with ~10% growth in 2012, according to Yole Développement estimates, to become the first company to top $1B in mEms sales. Though that growth rate may seem modest, it represents almost $100M in added sales, and more than 50% growth in units, in a year when sT’s foundry revenues declined with the inkjet market and prices for its mainstay inertial sensor products that account more than 70% of sales fell plunged 20%-30%. Increasing sales of gyroscopes, 6 DoF Imus, and new microphone and pressure sensor products moving into volume production all helped drive growth.

The company’s aggressive expansion of its product line, its volume manufacturing capability, and its ability to move fast by keeping all manufacturing in house are the key components of its success, says Benedetto Vigna, Vice President and General manager of sT’s Analog, mEms and sensors Division. “Unless you have a wide portfolio, you can’t play a big role. Those with only an accelerometer or only a gyro are losing market share,” he notes. “In the future there will be no space for those without a wide portfolio.”

The company has been highly flexible in acquiring technology from outside to get new products to market faster and feed its high volume fab. “The market does not wait for us. We have to go outside [for product designs] when we are not ready,” says Vigna. “It used to be all about being able to manufacture the structure, but customers now understand that mEms is different from CmOs, so security and consistency of supply have become more important. They’ve come to value manufacturing expertise more. It’s no longer about making the particular cantilever or the membrane, but about being able to make things in high volume…. And you need a wide portfolio to leverage manufacturing expertise and serve diverse customer needs.”

The IDm also argues that control of all steps of manufacturing in house allows it to move faster both to get products into volume

I S S U E N ° 1 4 A P R I L 2 0 1 3

11M E M S ’ T r e n d s

2012 sales

2011 sales

1 000

842

825

645

440

386

356

279

276

268

266

249

247

187

187

179

178

161

152

130

93

91

83

81

81

75

65

60

60

54

907

738

913

762

362

336

372

284

251

250

255

279

261

150

144

51

174

153

136

102

110

77

90

62

76

34

56

75

55

0

200

400

600

800

1 0

00

1 2

00

STMICROELECTRONICS ROBERT BOSCH TEXAS INSTRUMENTS HEWLETT PACKARD KNOWLES ELECTRONICS PANASONIC

DENSO

CANON AVAGO TECHNOLOGIES FREESCALE

SEMICONDUCTOR ANALOG DEVICES

AKM SEIKO EPSON INFINEON

TECHNOLOGIES INVENSENSE

MURATA

SENSATA HONEYWELL

GE SENSING TRIQUINT

LEXMARK UTC Aerospace

SONY FLIR SYSTEMS MEASUREMENT

SPECIALTIES INC. KIONIX

AAC

OMRON

ULIS

MEMSIC

(US$M)

TOP 30 MEMS players - 2012 sales vs 2011(Source: Status of the MEMS Industry report, to be released in July 2013, Yole Développement)

A P R I L 2 0 1 3 I S S U E N ° 1 4

M E M S ’ T r e n d s12

production and to respond quickly to issues that arise later. After expanding its front-end fab last year, this year’s challenge was to expand and ramp additional backend assembly and test capacity for multiple new products, all done in house. “The number one advantage of an IDM is speed, both for the faster development of new products and fast reaction time with problems,” says Vigna. “It’s all the same boss pushing to get things done, while at an OSAT the relatively small volume MEMS business might not always be that company’s highest priority. We have seen several examples where we couldn’t have solved a problem as quickly at a subcontractor. If you have everything under your own control you can push everything ahead faster.”

Vigna figures all these trends will continue to play to the advantage of the IDMs, making it harder for smaller and more specialized MEMS makers to compete. Selling prices continue to decline, but it’s getting harder to continue to bring down manufacturing costs than it was several years ago, raising the bar for ramping production and optimizing yields at ever higher speeds.

Going forward, ST plans to continue to decrease die size this year through designs and TSVs, and to move more new products into production. The company’s first automotive MEMS products will start to show up in commercial vehicles this year, first in an infotainment/navigation system and then a qualified accelerometer. Vigna expects almost all phones will have accelerometers this year, and almost all will have gyros by 2015. He predicts growth will next come from environmental sensors such as pressure, temperature and humidity, and from portable projectors.

Robert Bosch moves up into second spot on 14% growth

Robert Bosch moved up the top company ranks into second place, edging past Texas Instruments, as Yole Développement estimates the German IDM saw 14% growth to some $842 million in

MEMS revenues. Growth was driven both by a healthy automotive market and particularly by a broad portfolio of consumer devices at this other diversified supplier.

“We had huge growth, only limited by our capacity,” explains Stefan Finkbeiner, who took over as CEO of the consumer MEMS subsidiary Bosch Sensortec late last year, after a stint running the company’s microphone acquisition Akustica. “We have significantly increased capacity to grow to the next level,” he adds. “Watch how we will grow next.”

Growth in 2012 was driven particularly by demand for accelerometers and pressure sensors, with some early uptake of the company’s aggressively priced consumer 3-axis gyro introduced during the year. “A full portfolio is important. More and more customers want to buy several sensors at the same time,” argues Finkbeiner, noting that he is particularly proud of the number of new products the company introduced last year. Besides the 3-axis gyro, the company added a small accelerometer-gyro 6-axis combo IMU, an accelerometer-magnetometer 6-axis e-compass, a 9-axis sensor module, and 9-axis absolute orientation device integrating a microcontroller and software, as the first in a planned line of application-specific sensor nodes. Finkbeiner suggests that having the magnetometer technology in house as well the inertial sensors and ASIC capacity helps for developing these combo sensors that are increasingly in demand.

Going forward, the key issues for MEMS will move increasingly from device manufacturing to systems issues, making a wide portfolio of company technologies even more important, he says, and likely also driving MEMS makers to more partnerships with others for controllers and software. There’s still room to decrease die size, but it may no longer be the key driver. “We can do it technically, but we have to ask where is the benefit,” he notes, as integration of multiple components in the same package can also bring down manufacturing costs, as well as save the user more by making the device easier to integrate. He notes as a case in point integration of the microcontroller with the 9-axis IMU to run sensor fusion algorithms to ease customers’ time to market.

“More and more the issue is what is the systems benefit,” he notes. “Five years ago you just needed a sensor. Now the market requires more integration and intelligence.”

GLOBALFOUNDRIES starts to ramp production in 2012, aims at full volume by 2014

Though still ramping up production for initial customers, Yole Développement estimates GLOBALFOUNDRIES saw >50% growth to $6.2 million, entering the ranks of the Top 20 Foundries for the first time in its second BMC150 (Courtesy of Bosch Sensortec)

I S S U E N ° 1 4 A P R I L 2 0 1 3

13M E M S ’ T r e n d s

TELE

DYN

E D

ALS

A

23

TSM

C

47

SIL

EX

MIC

RO

SYSTEM

S

203

65

25

20

19

19

18

16

14

12

11

8 8

8

6

5

4

3

2

0

245

49

26

16 24

15

17

15

20

12

7 12

7

4

3

4

4

2 8

0

50

100

150

200

250

300

ST

SO

NY

ASIA

PACIF

IC

MIC

RO

SYSTEM

S

Xfa

b

IMT

TRO

NIC

S

MIC

RO

SYSTEM

S

UTC

SSS

MIC

RALY

NE

TI

SEM

EFA

B

TOW

ER J

AZZ

AD

VAN

CED

MIC

RO

SEN

SO

RS

TOUCH

M

ICRO

SYSTEM

S

UM

C

Glo

bal

Fou

ndries

Hon

eyw

ell

MIC

REL

SM

IC

DN

P

Sen

sonor

2012 sales 2011 sales

(US

$M

)

42

39

37

34

TOP 30 MEMS foundries - 2012 sales vs 2011 (Source: Status of the MEMS Industry report, to be released in July 2013, Yole Développement)

full year of operation. It aims to bring some of the IDm advantage to its fabless customers, and mEms capability to its IC IDm customers.

The IC foundry set up its mEms fab and started qualification for first customers in 2011, started its gradual ramp in 2012, and is now starting full manufacturing this year. The company reports it is in volume production for a few customers, with some needing more volume than expected, has transferred other processes from R&D for another few for production in 2013, and expects to be producing full volume by 2014.

“But it hasn’t been smooth all the way,” admits MEMS director Rakesh Kumar. “As a CmOs foundry we were used to stable, high volume tools, but some unique mEms tools still lack that level of maturity… We found it also required significant adjustment to transfer some processes from the lab.”

Kumar says that the foundry aims to concentrate on devices that can be made on common, high volume tools, using common modules, leaving early development and high value, low volume products to the boutique foundries. It particularly targets inertial and RF mEms devices with high volume potential, and where big consumer applications can demand the capability for rapid ramp up from 100 to 1000 wafers per month for a single customer.

Initial customers include not only fabless mEms companies, but also IDms from the IC side who want to enter a specialized market but not get into volume mEms production themselves. Kumar notes that IC companies entering the mEms market have all the capabilities already in place to offer controllers and software, and customer support, market knowledge of their customers’ needs, and distribution.

manufacturing the mEms component is just another small part of how they serve their market. Fabless mEms companies with great designs for low cost manufacturing of high performance products will also have to find ways to offer the rest of this full service package too. “The foundries will have to offer more of the solution that helps their customers compete with the mEms IDms,” says Kumar. “We want to add value by contract manufacturing first, but eventually we want to become a technology provider, and then become a solution provider.”

mEms foundries will eventually also have to become more like IC foundries, providing ready-to-use design kits and standardized process flows, Kumar argues, although the industry remains still a long way from that. But open platforms may be useful to speed initial development sooner, like that offered by Invensense if it turns out to be widely applicable for different devices. gLOBALFOunDRIEs is also working with others to develop a common platform for rapid design of proof-of-concept for RF and inertial products, which can then be optimized as needed.

The company continues to work on bringing more IC-like process controls to mEms manufacturing. For the more CmOs-like RF products, the fab has added structures to the die for inline monitoring. But for the more unique mEms processes it has to devise more indirect measures, such as test die with structures for monitoring hermiticity, since IR inspection can’t detect all the voids in bonding to mEms to CmOs wafers. Kumar reports considerable interest in WLP to reduce footprints. It’s now offering a hermetic version, and working on developing its own getters to prevent outgassing of a vacuum version.

For the future of mEms, Kumar sees big potential to come in industrial monitoring. “Every tool and every machine will have motion sensors to monitor its condition. It will be a big market that will develop as prices come down,” he suggests. “And I hope someone figures out a way to harvest energy to keep my cell phone charged”.

Freescale looks to adding intelligence to MEMS for advantage

Freescale Semiconductor saw ~7% growth in mEms sales in 2012 to 10th ranking—despite the added challenge of transferring its mEms manufacturing from its earthquake-damaged fab in sendai to its Oak Hill Fab in Austin.

GLOBALFOUNDRIES employee loading wafers on an automated wafer grinder polisher

(Courtesy of GLOBALFOUNDRIES)

A P R I L 2 0 1 3 I S S U E N ° 1 4

M E M S ’ T r e n d s14

The automotive IDm is growing its consumer-side business, and also counting on advantage from its in-house access to processors to more easily integrate intelligence into its mEms packages.

The planned transfer of mEms production from sendai to Austin was accelerated when the 2011 earthquake left the Japanese fab severely damaged, and the move was completed a year ahead of schedule, without disrupting any customers’ automotive lines, reports James grothe, strategic and Channel marketing for sensors at Freescale. Through it all the company saw growth in inertial sensor unit volumes, and >20% growth in tire pressure monitoring systems--driven by government mandates for safety in the us and for emissions control in the rest of the world-- although the traditional automotive pressure sensor business was flat.

The big automotive player has been steadily building up its consumer business, reporting >40% unit growth in consumer inertial sensors in 2012, adding some volume in smart phones. It’s completing the ramp and starting into volume production of its newer discrete magnetometer and combo accelerometer/magnetometer e-compass devices. These use the company’s rather unusual tunneling magneto-resistance technology, which measures the difference in resistance across a barrier layer as the magnetic field changes the alignment of a free magnetic layer on one side in relation to a pinned magnetic layer on the other. The approach allows sensors for all three axes to be made on one tiny die with CmOs technology. Freescale integrates one of its digital signal processors in the same package as the magnetometers to do signal conditioning and conversion, and provides a graphical interface to ease customer programming of the device.

Freescale sees interesting IDm advantage going forward in integrating more intelligence with its MEMS. “Like other IDMs, Freescale has access to IP that our competitors have to negotiate for, with immediate access to different types of cores, and the peripherals to go with those cores, so we can get integrate intelligence to get new capabilities to market faster,” says grothe, pointing to the company’s early integration of an 8-bit microcontroller, RF, and accelerometer in a TPms device. “But our challenge as an IDM is that we also have to drive the volumes and efficiencies in our fabs to maintain a cost-competitive position. Fabless companies using volume foundries may be able to ride that scale factor faster,” says Grothe. “The old one product, one process, one package system will have to end eventually, and it will become all about volume manufacturing, and the rest of us will have to get to those high volumes too.”

Freescale projects more and more mEms parts will include intelligence to manage the sensors, and especially to manage the efficient use of power in the device, to reduce power usage in the end system. This trend towards more value coming from beyond the basic sensor may bring more microcontroller and apps processor companies into this market, but they may find integrating MEMS is not so easy. “Adding MEMS to a package without expertise is a significant barrier to entry,” Grothe notes.

Paula Doe for Yole Développement

Stefan Finkbeiner, CEO, Bosch Sensortec.Dr. Finkbeiner joined Robert Bosch gmbH in 1995 and has been working for more than 17 years in different positions related to the research, development, manufacturing, and marketing of sensors. senior positions at Bosch have included Director of marketing for sensors, Director of Corporate Research in microsystems technology, and the Vice President of Engineering

for sensors, CEO of Akustica, a Bosch group company which develops mEms microphones for consumer electronics applications and is located in Pittsburgh, PA. since end of 2012 Dr. Finkbeiner has been the CEO of Bosch sensortec gmbH.

Rakesh Kumar, Senior Director of MEMS program, GLOBALFOUNDRIES.He received his B.s. (Hons.) and Ph.D. degrees in electrical engineering from Punjab Engineering College, India and nanyang Technological university, singapore, respectively. Prior to this, he was deputy director of semiconductor Process Technology Lab at Institute of microelectronics, singapore where he was

responsible for mEms process development and technology transfer. His areas of interest include advanced copper interconnects, 3D wafer level packaging and mEms technologies. He has authored and co-authored more than 90 research publications in journals and conferences.

jim Grothe, Marketing Manager, Freescale Semiconductor.He leads the strategy team for the sensors Division. Jim has been a member of the sensors Division for more than seven years and part of Freescale (and motorola semiconductor before it) for over 25 years, working in areas ranging from AsIC design to CAD Applications to Image sensor design and marketing.

Benedetto Vigna, Corporate Vice President, General Manager of the Analog, MEMS and Sensors Product Group ST Microelectronics.He held this position since September 2011. Vigna joined sTmicroelectronics’ R&D Lab in Castelletto, Italy, in 1995. six years later, he was appointed Director of the mEms Business unit, responsible for design, manufacturing and marketing of sT’s mEms

accelerometers and gyroscopes. In 2007, Vigna’s organization was transformed into a Product Division and his scope was subsequently enlarged to include management of sensors, RF, High-Performance Analog and mixed signal, as well as Interface, Audio for Portable, and General-Purpose Analog products.Vigna has filed more than 150 patents on micromachining to date, authored numerous publications in this field, and delivered many invited speeches at international conferences.

What counts as MEMS?Yole Développement defines MEMS as three dimensional

structures made by semiconductor-like processes, with primarily

mechanical, not electronic, function. This includes devices without cavities such as BAW

resonators and piezo and thermal devices where the physical function

is resonating or expansion; microfluidics without moving parts;

and three dimensional structures like gratings and micro tips with

neither cavities nor moving parts. We also include magnetometers, as they are now so closely integrated

with MEMS inertial sensors, and all microfluidics, including those

on polymer. We figure MEMS units and value at the first level of

packaged device. We figure foundry revenues from MEMS processing.

For companies that do not release MEMS revenues, we estimate

the figures based on our data for product market size, market share, product teardowns, reverse costing, and discussions with the companies.

Leti Innovation Days is a wonderful occasion for business executives and researchers to share their insights about the future of technology.

SPEAKERSInternational & European CEOs from large companies, innovative technology SMEs, researchers ATTENDEESInternational and European decision-makers : CEOs, CTOs, marketing & strategy Directors, R&D managers, IT & semicon companies, innovative SMEs, End-Users companies, Research Institutes, Start ups, International Press

CEA-Leti, a world-class center for applied research in the fields of microelectronics, information technology, and technology for healthcare, will hold the first-ever Leti Innovation Days on June 24–28, 2013.

The Leti’s traditional two-day Annual Review held every year for the past fifteen years will be a highlight of the four-day conference. The event, which gathers high-tech business executives, technology decision makers, and researchers, is a demonstration of Leti’s mission of transferring new technology to a broad range of industries.Over the presentation of the latest developments of Leti’s labs, the event will give professionals from the world of industry an opportunity to talk to Leti researchers about new advances in micro and nanotechnology. “Leti Innovation Days is a wonderful opportunity for businesses to explore the ways in which these emerging technologies can help drive growth,” said CEA-Leti CEO Laurent Malier.

Information and registration: www.leti-innovationdays.com

innovation • daysJune 24-28, 2013 | Grenoble, France

ww

w.le

ti.fr

15th Leti Annual Review Workshops Social Events

PL

EN

AR

Y

SE

SS

ION

S

PA

RA

LL

EL

S

ES

SIO

NS

Tuesday, June 25th

Wednesday,June 26th

Thursday, June 27th

Friday, June 28th

Safety & Security

15th Leti Annual Review

Memory WorkshopEnvironment & Health

Photonics WorkshopGreen IT Imaging Workshop

Microelectronics

Gala Dinner

Art & Science Exhibition

Design for 3D Workshop

Nanopackaging Workshop

A

B

C

D

A n A L Y s T C O R n E R

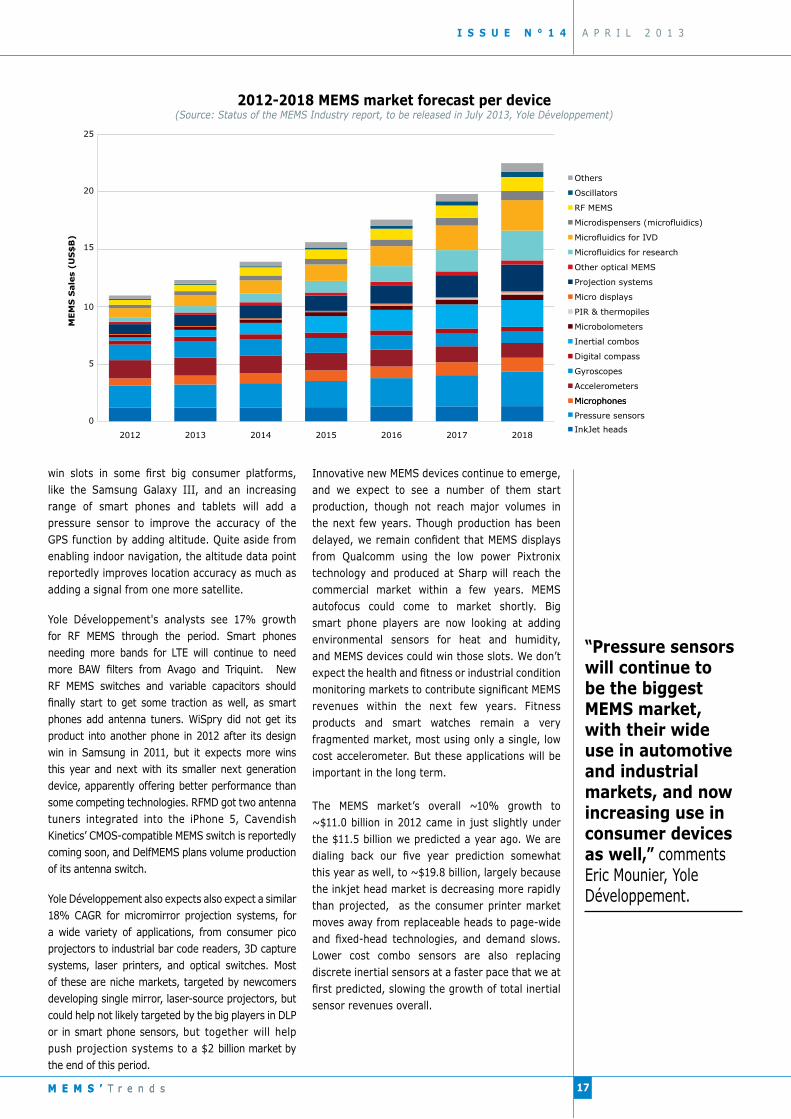

Steady 10-12% growth will double the MEMS market over next six yearssmart phones drove big growth in inertial sensors and microphones in 2012. Look for inertial combos to start to replace discretes, while oscillators and RF mEms to start to see more volumes going forward.

A P R I L 2 0 1 3 I S S U E N ° 1 4

In a year when the greater semiconductor industry saw a ~2% decline, the MEMS sector managed another year of ~10% growth in

2012, to become an $11 billion business. Yole Développement expects ongoing growth averaging ~12.7% through 2018 to create a $22.5 billion mEms market. given continually declining average selling prices, this projection is based on a steady 20.3% CAGR increase in units shipped, to 23.5 billion units in 2018.

Though that steady growth may look like a stable market, it actually masks plenty of change across the many different diverse mEms applications, as old products mature and new ones emerge.

We see big growth soon to come for combinations of inertial sensors and for mEms timing devices. Combination inertial sensors are starting to see high volume adoption in both consumer and automotive markets, and will quickly account for a significant part of inertial sensor sales. Combos have scored slots in big platforms like the samsung Galaxy III for their significant cost savings, as a gyro and an accelerometer in the same package with a shared AsIC may cost only slightly more than the gyro alone. This will increasingly cut into the sales of discrete accelerometers. going forward the same trend towards sensor integration will increasingly impact magnetometers as well, as more users go to accelerometer/magnetometer e-compass combos. As more smart phones come to use all three sensors, and more combo product options in smaller packages allow more flexible placement away from sources of magnetic interference, the 9-axis gyro/

accelerometer/magnetometer will displace even more discrete components. Yole Développement projects 43% compound average growth for inertial combos, to more than a $2 billion market by 2018.

Though the global semiconductor slowdown limited growth last year for the mEms timing devices used along with the chips, we expect very strong growth over the next few years. siTimes’ latest technology brings mEms oscillator performance to the levels required for the cell phones, at lower cost than quartz. That should start to drive uptake into that big potential market, with two units potentially used in every smart phone. suppliers siTime and Discera have both partnered with established conventional timing players for distribution, which should help gain acceptance in this conservative replacement market. new players IDT, sand9 and perhaps silicon Labs are entering the market, increasing options and awareness for the mEms alternative, and also likely bringing more price competition to the sector to help drive demand at better than 50% CAGR.

Healthy growth for pressure sensors, RF MEMS, projection systems as well

Pressure sensors will continue to be the biggest mEms market, with their wide use in automotive and industrial markets, and now increasing use in consumer devices as well. Yole Développement's analysts expect the mEms pressure sensors to be the first MEMS market to reach $2 billion in the next year or so, and to approach $3 billion by around 2018. Pressure sensors are starting to

16 M E M S ’ T r e n d s

Laurent Robin, Activity LeaderInertial MEMS Devices& Technologies, Yole Développement

Dr. Eric Mounier,Senior AnalystMEMS Devices& Technologies,Yole Développement

Difference between 2012 and 2011 top MEMS sales (Source: Status of the MEMS Industry report, to be released in July 2013, Yole Développement)

104 94

78

50 43 36 31 28 25 19 16

0

20

40

60

80

100

120

Bosc

h ST

Know

les

Pana

sonic

Inve

nSen

se

Infin

eon

AAC

Triquint

Avag

o MSI

GE Se

nsing

(US

$M

)

win slots in some first big consumer platforms, like the samsung galaxy III, and an increasing range of smart phones and tablets will add a pressure sensor to improve the accuracy of the gPs function by adding altitude. Quite aside from enabling indoor navigation, the altitude data point reportedly improves location accuracy as much as adding a signal from one more satellite.

Yole Développement's analysts see 17% growth for RF mEms through the period. smart phones needing more bands for LTE will continue to need more BAW filters from Avago and Triquint. new RF mEms switches and variable capacitors should finally start to get some traction as well, as smart phones add antenna tuners. Wispry did not get its product into another phone in 2012 after its design win in samsung in 2011, but it expects more wins this year and next with its smaller next generation device, apparently offering better performance than some competing technologies. RFmD got two antenna tuners integrated into the iPhone 5, Cavendish Kinetics’ CmOs-compatible mEms switch is reportedly coming soon, and DelfmEms plans volume production of its antenna switch.

Yole Développement also expects also expect a similar 18% CAGR for micromirror projection systems, for a wide variety of applications, from consumer pico projectors to industrial bar code readers, 3D capture systems, laser printers, and optical switches. most of these are niche markets, targeted by newcomers developing single mirror, laser-source projectors, but could help not likely targeted by the big players in DLP or in smart phone sensors, but together will help push projection systems to a $2 billion market by the end of this period.

Innovative new mEms devices continue to emerge, and we expect to see a number of them start production, though not reach major volumes in the next few years. Though production has been delayed, we remain confident that MEMS displays from Qualcomm using the low power Pixtronix technology and produced at sharp will reach the commercial market within a few years. mEms autofocus could come to market shortly. Big smart phone players are now looking at adding environmental sensors for heat and humidity, and mEms devices could win those slots. We don’t expect the health and fitness or industrial condition monitoring markets to contribute significant MEMS revenues within the next few years. Fitness products and smart watches remain a very fragmented market, most using only a single, low cost accelerometer. But these applications will be important in the long term.

The MEMS market’s overall ~10% growth to ~$11.0 billion in 2012 came in just slightly under the $11.5 billion we predicted a year ago. We are dialing back our five year prediction somewhat this year as well, to ~$19.8 billion, largely because the inkjet head market is decreasing more rapidly than projected, as the consumer printer market moves away from replaceable heads to page-wide and fixed-head technologies, and demand slows. Lower cost combo sensors are also replacing discrete inertial sensors at a faster pace that we at first predicted, slowing the growth of total inertial sensor revenues overall.

I S S U E N ° 1 4 A P R I L 2 0 1 3

M E M S ’ T r e n d s

2012-2018 MEMS market forecast per device(Source: Status of the MEMS Industry report, to be released in July 2013, Yole Développement)

0

5

10

15

20

25

2012 2013 2014 2015 2016 2017 2018

MEM

S S

ale

s (U

S$

B)

Others

Oscillators

RF MEMS

Microdispensers (microfluidics)

Microfluidics for IVD

Microfluidics for research

Other optical MEMS

Projection systems

Micro displays

PIR & thermopiles

Microbolometers

Inertial combos

Digital compass

Gyroscopes

Accelerometers

Microphones Microphones

Pressure sensors

InkJet heads

17M E M S ’ T r e n d s

“Pressure sensors will continue to be the biggest MEMS market, with their wide use in automotive and industrial markets, and now increasing use in consumer devices as well,” comments Eric mounier, Yole Développement.

A P R I L 2 0 1 3 I S S U E N ° 1 4

Big growth from smart phones, limited growth for many foundries

Results of our Top 30 and best growth make clear just how much the smart phone market is driving mEms demand. strong sales of MEMS microphones propelled AAC’s 90% growth to $65 million in MEMS revenues, to make the Top 30 for the first time. The Chinese electret microphone supplier has gotten into the mEms microphone business by buying bare MEMS die from Infineon, and packaging them and marketing them to its established microphone customer base, and also serves as the second source for the iPhone. more microphones in more phones also helped propel >20% sales growth at Infineon and Knowles.

Cell phone demand also drove strong growth for other mEms devices as well in 2012. Inertial sensor maker Invensense continued to prove the worth of its fabless model with a ~30% increase in sales. Triquint saw 27% growth as its BAW filters won more slots in smart phones, though Avago’s sales remain roughly twice as large. Acquisitions and automotive/industrial markets propelled murata’s big increase, as adding VTI helped grow the combined company to a ~$179 million mEms supplier.

But not all mEms sectors saw growth. markets for inkjet heads and DLPs have of course matured. Demand for uncooled microbolometers cooled as slower markets for construction and energy-saving audits and remodels limited thermography growth. In the magnetometer market, dominant supplier AKm saw more competition from companies like Yamaha and Alps, pushing ASPs down some 35% during the year.

Yole Développement's analysts think the MEMS foundry business is ripe for consolidation, as these 20 leading players scramble after a roughly $600 million business that’s seeing modest overall growth, as the decline in inkjet head demand counters the increase across other applications, and. We estimate that TsmC added ~$19 million in sales and Sony added ~$16 million, while X-FAB, Tronics microsystems and TowerJazz each captured roughly $4 million in new business, to together account for most of the foundry sector’s net growth. That didn’t leave much business for the rest of the crowd of small foundries. Touch microsystems recently decided to exit the mEms foundry market.

www.yole.fr

18 M E M S ’ T r e n d s

Laurent Robin is in charge of the mEms & sensors market research. He previously worked at image sensor company e2v Technologies (grenoble, France). He holds a Physics Engineering degree from the national Institute of Applied sciences in Toulouse, plus a master Degree in Technology & Innovation management from Em Lyon Business school, France.

Dr. Eric Mounier is a cofounder of Yole Développement since 1998, a market research company based in France. Dr. Eric mounier is in charge of market analysis for mEms, equipment and material. He is Chief Editor of micronews and mEms’Trends magazines (mEms Technologies & markets). He has a PhD in microelectronics from the InPg in grenoble.

Which of today’s

IP portfolios will

enable tomorrow’s

successful

gyro growth?

Discover the NEW report on

www.i-Micronews.com/reports

MEMS Gyroscope

Patent Investigation

“Results of our Top 30 and best growth make clear just how much the smart phone market is driving MEMS demand,” says Laurent Robin, Yole Développement.

Which of today’s

IP portfolios will

enable tomorrow’s

successful

gyro growth?

Discover the NEW report on

www.i-Micronews.com/reports

MEMS Gyroscope

Patent Investigation

Y O L E A s K s

Tronics talks about industrializing CEA-LETI’s M&NEMS technologyTronics is in the process of taking a breakthrough submicron mEms technology, developed by CEA-LETI, to production. This piezoresistive nanowire mEms technology is poised to usher in a whole new generation of combo sensors for motion sensing applications.

A P R I L 2 0 1 3 I S S U E N ° 1 4

Tronics microsystems is an international full-service mEms manufacturer with wafer fabs in Europe and the us, offering an extensive portfolio of mEms processes.

Yole Développement: Can you describe how this M&NEMS technology works?

julien BON: The basic concept behind this m&nEms technology is to combine in a single device a mEms part that is sensitive to inertial, magnetic, or other mechanical forces, with a suspended silicon nanowire strain gauge nEms part for motion sensing. The mEms and nEms parts can be optimized separately.

This technology uses piezoresistance for motion sensing. When a force is applied to a moving element, due to acceleration, the movement results in compressive or tensile stresses—depending on the position—in the suspended silicon nanowires. In silicon, a stress variation results in a change of electrical resistance that can be easily and precisely measured using a Wheatstone bridge.

YD: What makes this technology unique?

jB: It’s a big departure from traditional motion sensing and is a potential breakthrough in inertial mEms technology. Instead of measuring a change in capacitance because a mass is moving, we’re measuring a change in resistance (stress) on the piezoresistive nanowire.

The main advantage of m&nEms technology is that it enables the design of very small—6, 9, or more degrees of freedom (DOF)—m&nEms integrated on the same chip, which results in a drastic size and power consumption reduction.

This opens the door right now to smaller multi-DOF sensors for consumer applications and, in the future, a new generation of high-performance mEms that are smaller in size and cost less to produce.

YD: Is there anything unusual about the materials or processes?

jB: The inertial masses are made using traditional methods—etching silicon. The only tricky thing about the technology is mastering the dimensions of the nanowires and integrating this process step into the whole manufacturing flow. This had been done at LETI at the prototype level, with promising results, but hadn’t been done in production.

The m&nEms technology is based on a thin sOI substrate, with a silicon top layer thickness equal to the nEms gauge’s thickness. The process startsout with lithography and etching of the nEms gauges, followed by local protection of the gauge,thanks to an oxide layer, and by a few microns thick silicon epitaxial growth to build the mEms proof mass. The next step involves lithography and a deep reactive ion etching (DRIE) of a thick silicon layer to make the mEms structure and to open the siO2 protective layer that covers the nEms gauge. The final step is HF-vapor etching.

YD: What products will use this technology?

jB: The first targeted products are 6 DOF and 9 DOF components for consumer electronics. We envision it eventually being used in pressure sensors and microphones as either standalone products or integrated into inertial 9 DOF.

20 M E M S ’ T r e n d s

Julien Bon, Business Unit Manager, Multi-Sensor Technologies, Tronics Microsystems

“M&NEMS technology opens the door

right now to smaller multi-DOF sensors

for consumer applications,”says Julien Bon.

CEA-LETI’s M&NEMS technology (Courtesy of CEA-LETI)

Tronics transforms R&D concepts into reliable MEMS products (Courtesy of Tronics)

Julien Bon, Business Unit Manager, Multi-Sensor Technologies, Tronics MicrosystemsJulien holds a M.Sc. in Microelectronics from Polytechnic National Institute of Grenoble, and he joined Tronics in 2001 as a Test engineer. He became Head of Engineering & Product Industrialization and lead various MEMS developments. Now, Julien as Multi-Sensor Technologies Business Unit manager, is in charge of M&NEMS technology.

M&NEMS technology enables manufacturing of all sensors axes— accelerometers, gyroscopes, magnetometers, and even pressure sensors or microphones.

YD: What is Tronics’ role in industrializing the technology?

JB: Our main role is taking the technology to production. To do this, we’re adapting the processes to make the technology manufacturable in high volumes. We’re already manufacturing and expect to see the first batches out of our line before the end of 2013.

In terms of manufacturing very large volumes, Tronics is working with partners who can manufacture on 8-inch wafers.

YD: Can you disclose who your partners are for this project?

JB: Aside from CEA-LETI, which is a major research institute in Europe, a key partner is MOVEA, a data fusion software specialist.

We really can’t disclose any other partners at this point, but pilot customers and well-established industrial partners are involved in the initiative to ensure it aligns with market needs and to help speed its adoption in products.

Leading ASIC suppliers are also contributing their expertise to design a motion sensor chipset that fully leverages the M&NEMS strengths.

YD: Funding for the project?

JB: Tronics, together with our partners, are the financial backers of this project, and we’ve also received a substantial 6.5 million Euros grant from the French Ministry of Industry.

YD: Production timeline?

JB: Our plan is to be in production with 6 DOF devices by the second half of 2014, and to enter into production with 9 DOF devices by 2015.

www.tronicsgroup.comwww.leti.cea.fr

I S S U E N ° 1 4 A P R I L 2 0 1 3

Tronics Head Office in Grenoble, France(Courtesy of Tronics Microsystems)

C O M P A N Y I N S I G H T

MicroVision gets consumer electronics partnerMicroVision recently announced a $4.6 million development agreement with an unidentified major electronics OEM that will give welcome revenue this year, as the increased availability of green lasers begins to make laser-based projection systems more competitive.

A P R I L 2 0 1 3 I S S U E N ° 1 4

Under the agreement MicroVision is supporting the OEM’s development of a display engine based on its patented PicoP

display technology, and will receive $4.6 million in development fees over the next 13 months. MicroVision expects licensing and component supply agreements to follow for the OEM’s introduction of commercial products sometime next year.

Though there’s huge appeal to getting a big picture display from a pocket-sized mobile device, the market for pico projectors has yet to really take off, as current products still don’t meet consumers’ expectations for brightness or resolution or battery life or cost. While Texas Instruments’ established micro-mirror array dominates the market so far, single-mirror and laser-based alternatives are making progress as well towards hitting the needed performance and cost for wider adoption.

“The DLP has momentum and manufacturing volume, but we have a fundamental advantage for small size and real world image quality, and we have a clear roadmap to 50-100 lumens and under 2 Watts power for 2-3 hours of battery life,” maintains Dale Zimmerman, MicroVision VP of R&D. Current company products are about 25lm and 2.5W, but the company showed a second generation 35lm demonstration product inserted in an off-the-shelf tablet at CES this year. Although earlier product versions needed more complicated optics to convert other colored laser light to green, he notes that Nichia and Osram are now both producing direct green lasers, which may help begin to drive down costs, which have tended to be higher than for DLPs. It’s also getting easier to get the desired content into the projector from the mobile device, as half the phones and all tablets will have an easy-connection interface next year.

MicroVision’s deal to supply its components and technology to Pioneer for its pioneering heads-up automotive display significantly contributed to the company 49% jump in revenues in 2012 to $8.4 million. Now the company is concentrating on negotiating new development partnerships with a selection of the more than 50 companies that evaluated its second generation product last

year, particularly targeting those with content or software to add value to the projector hardware, and that offer upfront licensing fees. As of its annual report at year end, before this recent round of deals, Microvision reported cash on hand to last through June. The company has reported in financial calls that it counts on this NRE income for its revenue this year, with product revenue in 2014.

After making its own light engine, and even its own picoprojector for a while to demonstrate the product, MicroVision is now focusing on a components-plus-licensing model. It aims to supply the MEMS, ASIC and firmware components, which are made by its foundry and packaging partners, and then license the technology for the systems partner to build the light engine and the end product. “We work with users at the reference design level,” says Michael Franzi, VP Marketing & Business Development. “The customer then designs the system and finds their own manufacturing partners to make it… Some want us to supply more of the system, other want to do more of it themselves.” He says the company is in discussions with several additional key consumer OEM and ODMs on the pico projector side, and a number of automotive makers and suppliers on the heads-up display side, for navigation and collision avoidance systems.

Zimmerman says the company’s scanning laser approach offers considerable potential to get more brightness for less power. Modulating the laser sources pixel by pixel means each of the three colored lasers is only on when needed to create a particular color at a pixel, so power usage averages only ~10% of peak levels, allowing the thermally-limited devices to be run at high power and brightness. A new controller architecture is focused on further reducing power, using more advanced modulation schemes, while simultaneously increasing brightness.

The company has also figured out a simple solution to add touch control to the projected display. Because the device is scanning all the time, it can be made to respond to a touch on the projected image by sensing the reflected light from the tip of a stylus or a finger thimble. A small piece of stamped plastic reflector such as used in road

22 M E M S ’ T r e n d s

Dale Zimmerman, Vice President of Research & Development, MicroVision

Michael J. Franzi, Vice President, Marketing and Business Development, MicroVision

23

I S S U E N ° 1 4 A P R I L 2 0 1 3

M E M S ’ T r e n d s

signs reflects the light from the projector directly back to source, where the signal can be handled just like a touch to the touch screen by the applications software.

While the vastly improved high resolution displays on smart phones and larger tablets might seem to cut into demand for portable projection displays on these devices, it may just raise the bar for projected display quality instead. “More visual information on bigger and better displays on cell phones and tablets has only whetted consumer appetites for consuming and sharing more visual information,” claims Franzi. “It paves the way and opens up more applications.”

www.microvision.com

The sensor

application

is now driving

the MEMS

market !

Discover the NEW report on

www.i-Micronews.com/reports

Status of the MEMS

Industry

To be

relea

sed

soon

!

Dale Zimmerman, Vice President of Research & Development, MicroVisionDale Zimmerman joined MicroVision in June 2011 and serves as Vice President of R&D. mr. zimmerman has broad experience developing innovative technologies and building profitable businesses around them. He began his career in the Central Research Lab at Texas Instruments pioneering the development of gaAs microwave ICs. This technology developed into a healthy business and was spun out into TriQuint, a profitable $1B company. He was also an early pioneer in DLP technology and played an important role in launching the first conference room projectors, home theater projectors, and HDTVs. He received B.S. and m.s. degrees in electrical engineering from mIT and stanford. Michael j. Franzi, Vice President, Marketing and Business Development, MicroVisionMichael J. Franzi joined the company as Vice President, Marketing and Business Development in December, 2012. mr. Franzi has deep expertise in licensing and served as Vice President and General Manager of the Sonic Focus product line at synopsys Inc. In this position he was responsible for business development, product marketing and applications support for the licensing of intellectual property and technology across international markets. Prior to Synopsys Inc., Mr. Franzi was Vice President of Global Licensing and Business Development for sRs Labs, Inc. He has also held senior management positions at THX, Conexant and Tektronix. Mr. Franzi holds a Bachelor of science degree in Electrical Engineering from university of Pittsburgh - swanson school of Engineering.

Automotive head up display (Courtesy of MicroVision)

C O m P A n Y I n s I g H T

X-FAB targets MEMS for growth in More-than-Moore foundry strategyThe analog and mixed signal foundry looks for the acquired specialty Itzehoe mEms fab, a $50m investment budget, and a set of open platforms to keep its mEms business on a fast growth path.

A P R I L 2 0 1 3 I S S U E N ° 1 4

X-FAB is investing in growing its MEMS business as part of its more than moore foundry strategy. “We’ve seen 25% to 60% growth in MEMS sales since the downturn and we expect that growth to continue for the next few years,” says Iain Rutherford, X-FAB Business Line Manager for MEMS. MEMS now accounts for roughly 5%-10% of the analog and mixed signal foundry’s close to $300 million annual revenues. Yole Développement figures the company’s MEMS sales at about $20 million in 2012.

Though many may have traditionally seen the company as one of the boutique mEms foundries for niche applications, “We’re pretty much going to leave that behind,” notes Rutherford, citing the foundry’s total capacity of more than 60,000 wafer starts a month at five fabs.

The company has separated out the mEms business as a separate unit now named X-FAB MEMS Foundry to give it a higher profile, and given it $50 million budget to invest in development or equipment or clean room space over the next three years as needed to grow the business.

X-FAB has also upped its investment from 25% to a majority 51% in the Fraunhofer MEMS spinoff mEms Foundry Itzehoe, which is moving into a big new clean room area with more space available for X-FAB to rent if needed. The company already has some 6-10 projects running in the Itzehoe/Fraunhofer mEms fab that need more specialty approaches than can be easily handled in its more mainstream fabs. “It’s exciting that they bring us mEms/Fraunhofer access to quite a wide range of processes and more exotic materials that we wouldn’t want anywhere near our CmOs fab,” says Rutherford.

Also part of the growth strategy is a set of open platforms for common devices to ease integration of mEms sensors to a wider range of customers. “Though the sensor performance might not be leading edge, it opens up the mEms market for a lot of people who might not want to get into MEMS themselves,” Rutherford explains. “IMUs and sensor fusion will open up a lot of interesting applications that have largely been limited to the IDms so far.” Customers tend to be IDms or component makers in the CmOs area working with

24 M E M S ’ T r e n d s

Iain Rutherford, Product Marketing Manager/Business Line Manager, MEMS Product Line, X-FAB Group

“We’ll make more interesting things

than we have dreamed of so far,” says Iain Rutherford.

Gyroscope manufactured with surface micromachining technology. Specially developed buried contacts allow efficient layout of metal interconnects (Courtesy of X-FAB)

Product Marketing Manager/Business Line Manager, MEMS Product Line X-FAB Group Iain Rutherford is the Business Line Manager with X-FAB MEMS Foundry, based in Erfurt, germany. Working closely with X-FAB’s MEMS group, Iain covers business, strategy and service product development of mEms contract manufacturing in the pure-play foundry sector. With 20 years of experience in the semiconductor and mEms industry, Iain’s background includes product management, process engineering in high-volume wafer manufacturing and wafer inspection & metrology applications management. Before starting with X-FAB in 2010, Iain has previously worked with KLA-Tencor, motorola, Digital Equipment (DEC) and the university of Edinburgh.

sensors but not making them, who are getting sensors from somewhere and doing the interface chips themselves, who can differentiate their product by their AsIC or siP knowledge.

The company is starting production for a first lead customer of a product based on its open platform for 3-axis accelerometer and 3-axis gyroscope, both made using the same process. Besides inertial sensors, the platforms are also available for pressure sensors and for a thermopile infrared sensor. Designing a product with the open platform design rules and process specs, verifying the design from samples, and making some minor modifications could reportedly get a new product out in a few months, longer if changes need characterization. While the platforms can be customized, the degree worth doing typically depends on the volume of the product.

X-FAB’s main analog CMOS focus and history in the automotive IC market means its mEms business has tended to focus on automotive, medical and industrial mEms markets, though more recently it has been moving increasingly into the consumer space. The CmOs foundry background has also brought a focus on monolithic integration of mEms with analog/mixed-signal CmOs, which currently accounts for some 20%-30% of the MEMS business.

The company’s baseline process is mEms after CMOS, doing the MEMS-specific steps such as KOH etch after the CmOs layers, although sometimes on the bottom side of the wafer, and sometimes with sOI or cavity substrates. Rutherford says the monolithic integration may not necessarily be cheaper at the silicon level, but may simplify later manufacturing, and is often smaller and has better performance from reduced parasitics.

As always, producing mEms devices remains a balance between designing with established processes for faster time to market, and innovation that needs new materials and properties. “We’ll make more interesting things than we have dreamed of so far,” says Rutherford, noting the potential for mEms to play an increasing role in energy generation and control, from energy harvesting and fuel cells to monitoring usage, and in biomedical monitoring and control, and even robotics in daily life.

www.xfab.com

I S S U E N ° 1 4 A P R I L 2 0 1 3

C O M P A N Y I N S I G H T