Höegh LNG The floating LNG services provider · Shell Australia Offshore FLNG Petronas Malaysia...

25

Höegh LNG – The floating LNG services provider 4Q 2014 Presentation of financial results 26 February 2015

Transcript of Höegh LNG The floating LNG services provider · Shell Australia Offshore FLNG Petronas Malaysia...

Höegh LNG – The floating LNG services provider

4Q 2014 Presentation of financial results

26 February 2015

Forward looking statements

2

This presentation contains forward-looking statements which reflects management’s current expectations, estimates and projections about

its operations. All statements, other than statements of historical facts, that address activities and events that will, should, could or may

occur in the future are forward-looking statements. Words such as “may,” “could,” “should,” “would,” “expect,” “plan,” “anticipate,” “intend,”

“forecast,” “believe,” “estimate,” “predict,” “propose,” “potential,” “continue” or the negative of these terms and similar expressions are

intended to identify such forward-looking statements. These statements are not guarantees of future performance and are subject to

certain risks, uncertainties and other factors, some of which are beyond our control and are difficult to predict. Therefore, actual outcomes

and results may differ materially from what is expressed or forecasted in such forward-looking statements. You should not place undue

reliance on these forward-looking statements, which speak only as of the date of this presentation. Unless legally required, Höegh LNG

undertakes no obligation to update publicly any forward-looking statements whether as a result of new information, future events or

otherwise.

Among the important factors that could cause actual results to differ materially from those in the forward-looking statements are: changes

in LNG transportation and regasification market trends; changes in the supply and demand for LNG; changes in trading patterns; changes

in applicable maintenance and regulatory standards; political events affecting production and consumption of LNG and Höegh LNG’s

ability to operate and control its vessels; change in the financial stability of clients of the Company; Höegh LNG’s ability to win upcoming

tenders and securing employment for the FSRUs on order; changes in Höegh LNG’s ability to convert LNG carriers to FSRUs including

the cost and time of completing such conversions; changes in Höegh LNG’s ability to complete and deliver projects awarded; increases in

the Company’s cost base; changes in the availability of vessels to purchase; failure by yards to comply with delivery schedules; changes

to vessels’ useful lives; changes in the ability of Höegh LNG to obtain additional financing, in particular, currently, in connection with the

turmoil in financial markets; the success in achieving commercial success for the projects being developed by the Company; changes in

applicable regulations and laws; and unpredictable or unknown factors herein also could have material adverse effects on forward-looking

statements.

Höegh LNG Holdings; Agenda for presentation of 4Q 2014 results

3

Sveinung J.S. Støhle

President & CEO

Highlights/Markets/Summary

Additional information

Steffen Føreid

CFO

Financials

Dedededw

Fourth Quarter 2014 highlights: Entering the operational phase of the

current FSRU expansion

4

EBITDA USD 6.8 million and net loss USD 57.7 million in fourth quarter 2014

PGN FSRU Lampung and Independence in operation and contributing to improved

operating performance

Net profit adversely impacted by impairment charges totalling USD 44.8 million mainly

relating to Port Dolphin expenditures capitalized in 2008 and 2009

Signature of two new long term FSRU contracts

Started the next FSRU expansion phase by ordering FSRU#7/HN2552

First quarterly dividend payment announced; USD 0.10 per share – HLNG share

trading ex dividend as of 5 March 2015 (subsequent event)

Signed pre-FEED agreement for a second North American FLNG project

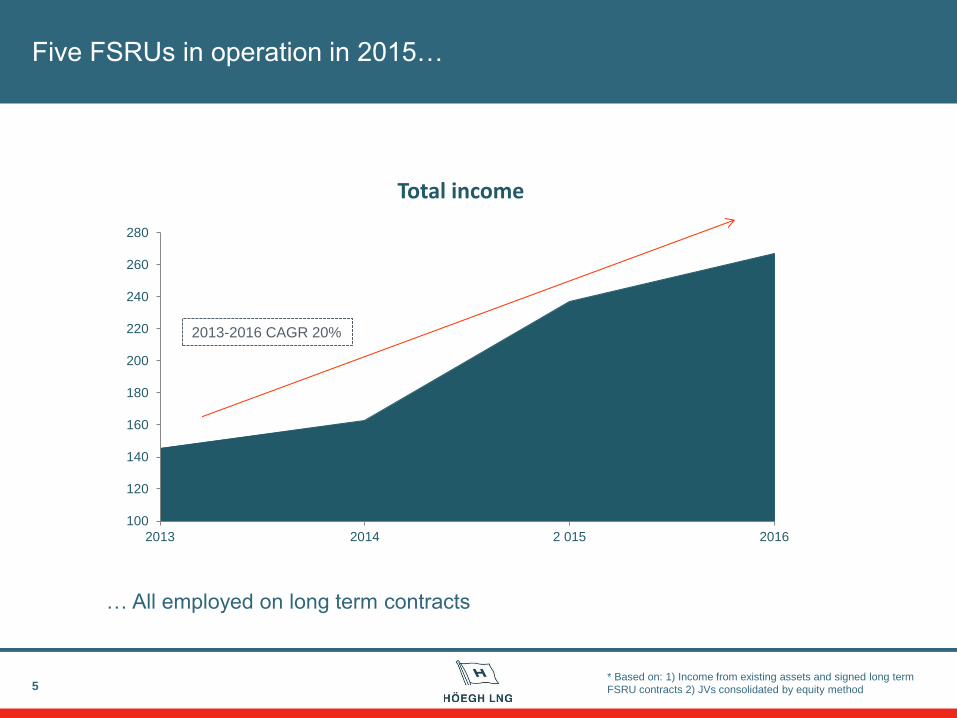

Five FSRUs in operation in 2015…

5

… All employed on long term contracts

* Based on: 1) Income from existing assets and signed long term

FSRU contracts 2) JVs consolidated by equity method

2013-2016 CAGR 20%

100

120

140

160

180

200

220

240

260

280

2013 2014 2 015 2016

Total income

Existing fleet operated according to contract and without incidents

6

Current fleet

100% availability/charter hire on LNGCs and GDF SUEZ FSRUs

PGN FSRU Lampung operating according to contract since end October; USD 7.2

million charged in Q3 (6.1) and Q4 (1.1) due to delayed start-up

FSRU Independence finalized commissioning according to schedule and operated

according to contract since end November

Höegh Gallant on schedule for start-up in Egypt by end of first quarter 2015

FSRUs under construction

FSRU#6/HN2551 (with employment) on schedule for the SPEC project

FSRU#7/HN2552 offered for various projects with the objective to sign a long term

FSRU contract by mid-2015

7

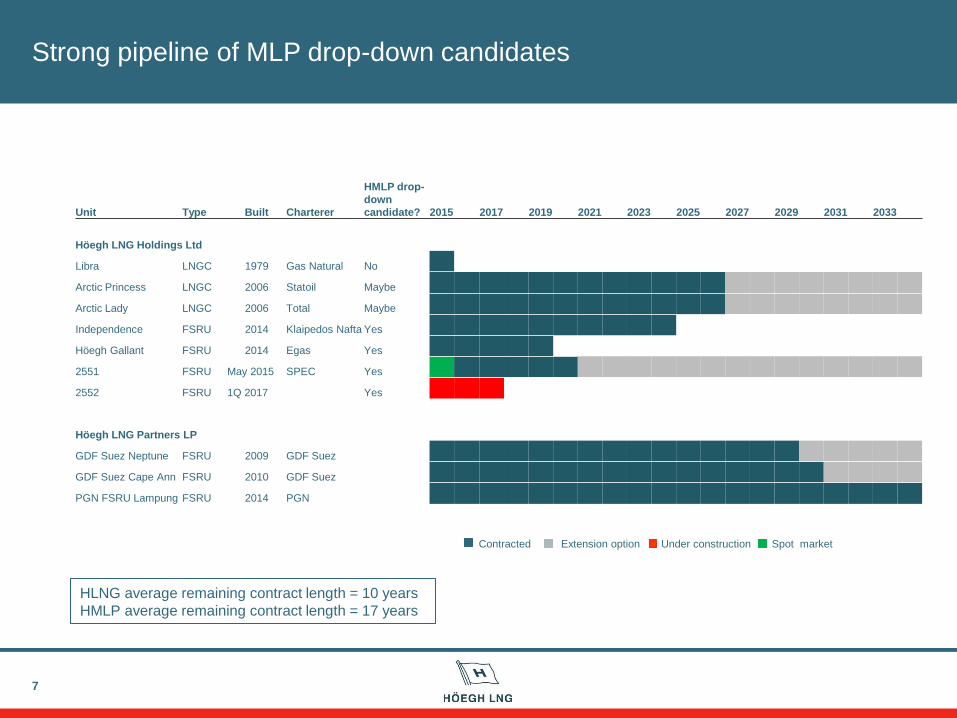

Strong pipeline of MLP drop-down candidates

HLNG average remaining contract length = 10 years

HMLP average remaining contract length = 17 years

Contracted Extension option Under construction Spot market

Unit Type Built Charterer

HMLP drop-

down

candidate? 2015 2017 2019 2021 2023 2025 2027 2029 2031 2033

Höegh LNG Holdings Ltd

Libra LNGC 1979 Gas Natural No

Arctic Princess LNGC 2006 Statoil Maybe

Arctic Lady LNGC 2006 Total Maybe

Independence FSRU 2014 Klaipedos Nafta Yes

Höegh Gallant FSRU 2014 Egas Yes

2551 FSRU May 2015 SPEC Yes

2552 FSRU 1Q 2017 Yes

Höegh LNG Partners LP

GDF Suez Neptune FSRU 2009 GDF Suez

GDF Suez Cape Ann FSRU 2010 GDF Suez

PGN FSRU Lampung FSRU 2014 PGN

Significant increase in demand for LNG in fast growing markets expected

over the next five years…

8 (Source: Shell)

Production Demand

Potential FSRU clients

… driven by fuel substitution and increased electricity generation from

natural gas …

9

LNG prices follow oil prices

For countries looking to replace expensive oil products with natural gas; LNG is the

most competitive substitute

For countries looking to replace pollutive coal with LNG; lower LNG prices makes

this decision easier

Sources: * Ship&Bunker (Singapore) , ** Platts LNG

0

5

10

15

20

25

Sep-14 Oct-14 Nov-14 Dec-14 Jan-15

USD

/MM

Btu

Diesel* LNG (JKM)** ARA Coal **

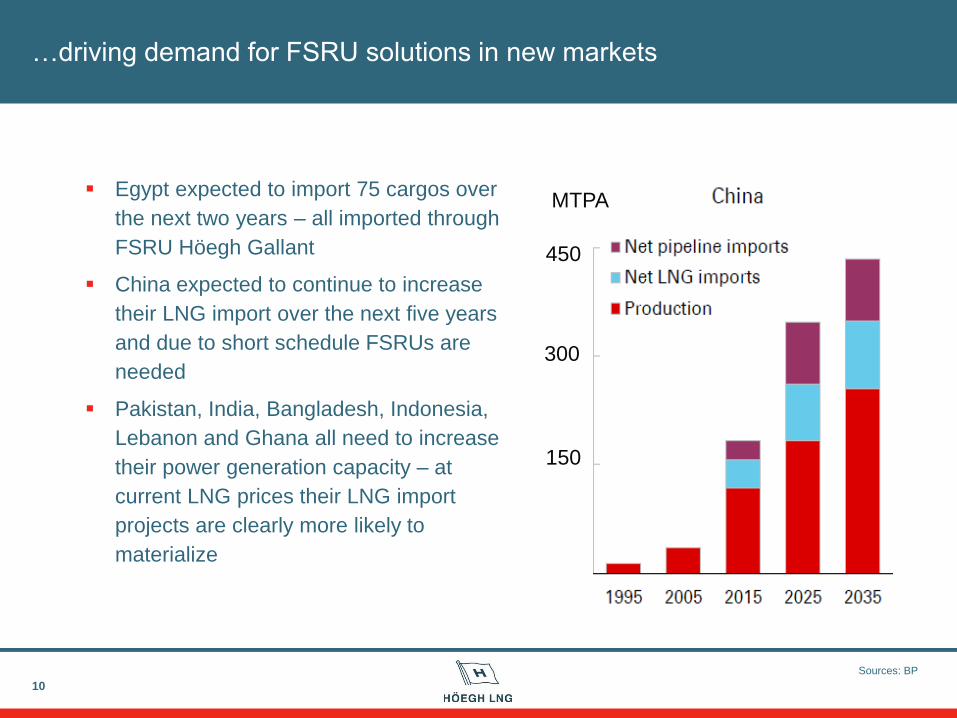

…driving demand for FSRU solutions in new markets

10

Egypt expected to import 75 cargos over

the next two years – all imported through

FSRU Höegh Gallant

China expected to continue to increase

their LNG import over the next five years

and due to short schedule FSRUs are

needed

Pakistan, India, Bangladesh, Indonesia,

Lebanon and Ghana all need to increase

their power generation capacity – at

current LNG prices their LNG import

projects are clearly more likely to

materialize

e

w

e

jl

w

e

jl

n

e

k

f

n

r

e

lf

n

rl

450

300

150

MTPA

Sources: BP

11

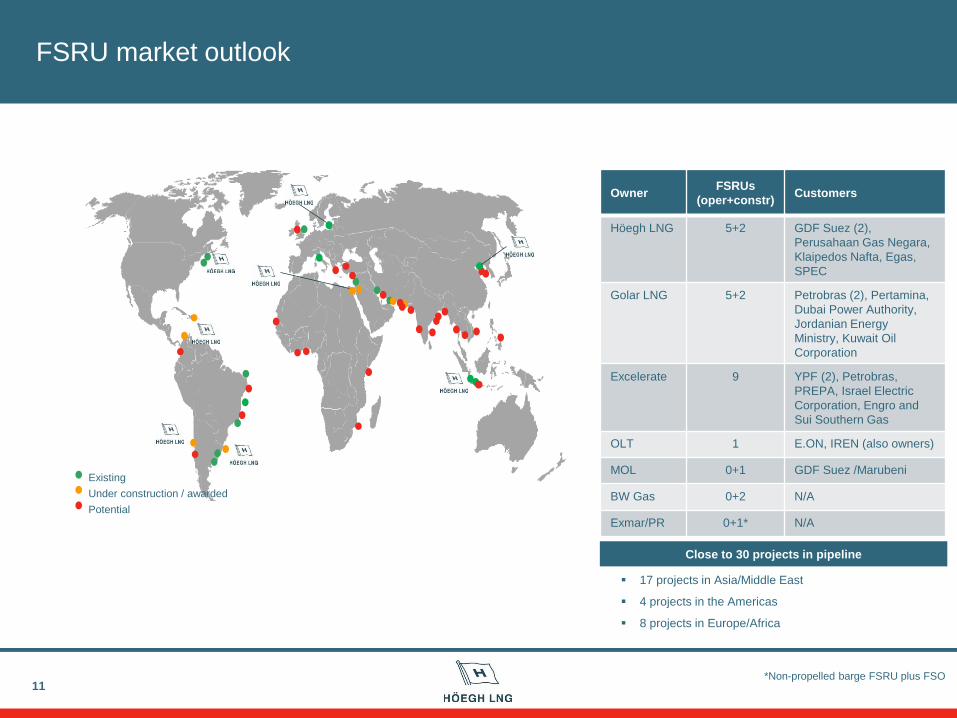

Close to 30 projects in pipeline

17 projects in Asia/Middle East

4 projects in the Americas

8 projects in Europe/Africa

FSRU market outlook

Owner FSRUs

(oper+constr) Customers

Höegh LNG 5+2 GDF Suez (2),

Perusahaan Gas Negara,

Klaipedos Nafta, Egas,

SPEC

Golar LNG 5+2 Petrobras (2), Pertamina,

Dubai Power Authority,

Jordanian Energy

Ministry, Kuwait Oil

Corporation

Excelerate 9 YPF (2), Petrobras,

PREPA, Israel Electric

Corporation, Engro and

Sui Southern Gas

OLT 1 E.ON, IREN (also owners)

MOL 0+1 GDF Suez /Marubeni

BW Gas 0+2 N/A

Exmar/PR 0+1* N/A

Existing

Under construction / awarded

Potential

*Non-propelled barge FSRU plus FSO

Low oil/gas price makes majority of land based LNG export projects still in

development phase not commercial

12

HLNG barge based FLNG

Source: IHS Cera

High cost LNG export projects (1500 USD/ton+) likely to be delayed and redesigned to

reduce project cost

Long term prospects for FLNG are still positive due to lower capex, smaller volumes to be

sold, lower unit cost and generally higher flexibility compared to land based export

projects

13

FLNG Projects under construction

Main sponsor Country Technical solution

Shell Australia Offshore FLNG

Petronas Malaysia Offshore FLNG

Petronas Malaysia Offshore FLNG

Pacific

Rubiales/Exmar

Colombia Barge FLNG

Exmar MOU - Kitimat Barge FLNG

Golar MOU - Cameroon LNGC conversion

Golar N/A LNGC conversion

The Company’s FLNG market focus

Main focus is North America; four potential projects

Under construction/Awarded other companies

Pre-FEED/FEED HLNG

Potential Barge FLNG HLNG

Summary

14

Improved operating results as 2 newbuild FSRUs entered operational stage

Net result adversely affected by one off impairment of assets mostly capitalized

pre-IPO phase

Dividend payment marks the Company’s entry into the operation and cash

generation phase from latest expansion program, with EBITDA expected to

increase significantly when all 4 new units in operation

Fast growing markets increasingly prefer FSRUs – positive outlook for FSRUs

going forward

Continued success with its FSRU strategy by winning two new long-term

contracts and ordering its seventh large size FSRU

Höegh LNG Holdings; Agenda for presentation of 4Q 2014 results

15

Additional information

Dedededw

Sveinung J.S. Støhle

President & CEO

Highlights/Markets/Summary

Steffen Føreid

CFO

Financials

16

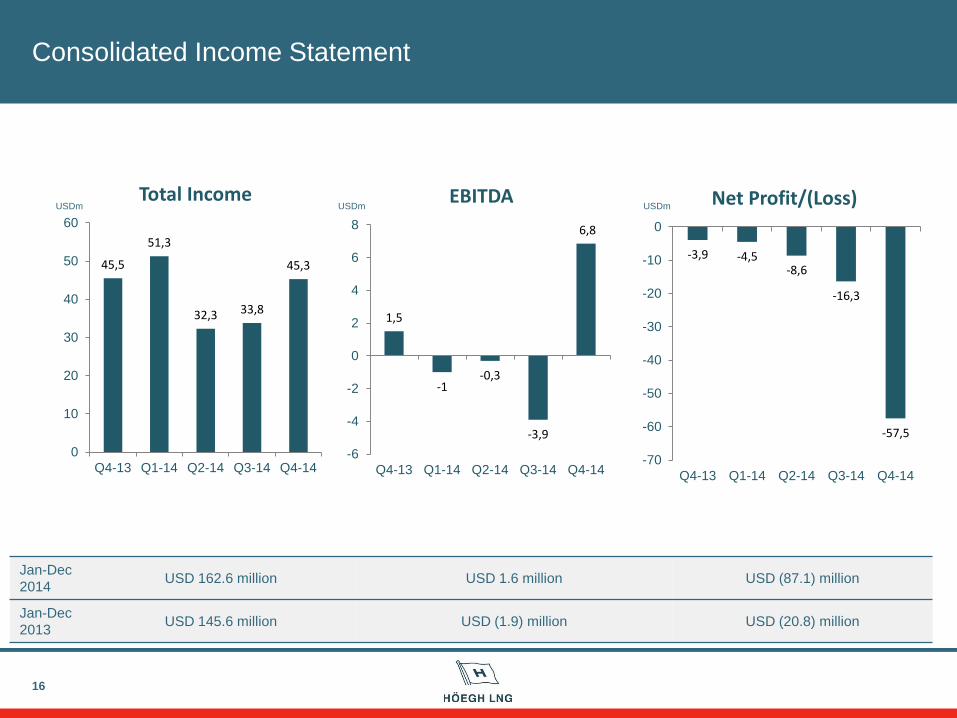

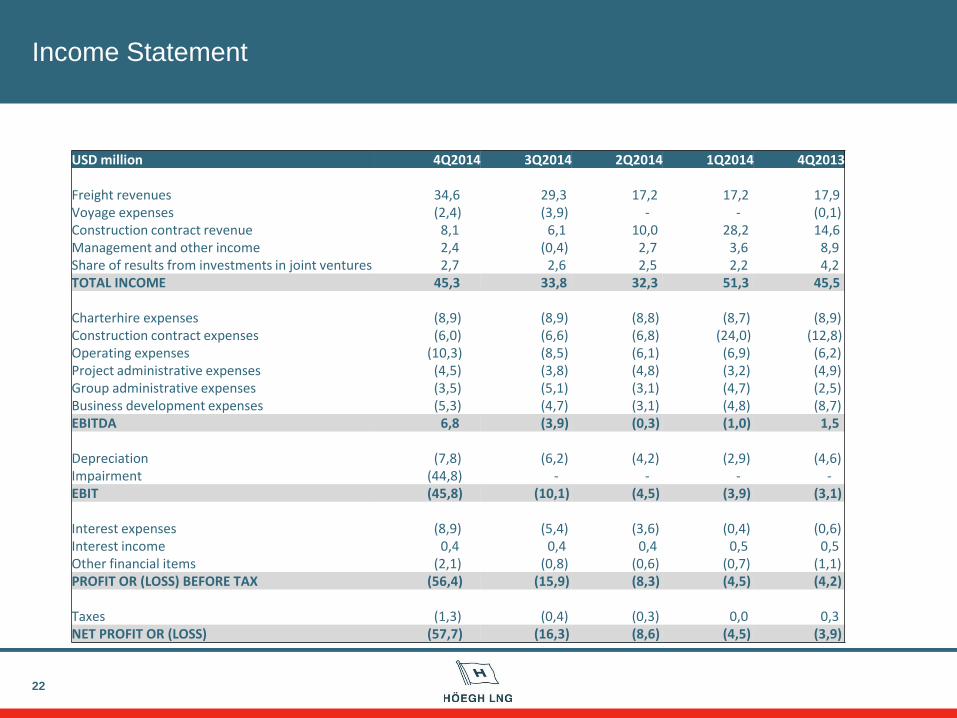

Consolidated Income Statement

Jan-Dec

2014 USD 162.6 million USD 1.6 million USD (87.1) million

Jan-Dec

2013 USD 145.6 million USD (1.9) million USD (20.8) million

USDm USDm USDm

45,5

51,3

32,3 33,8

45,3

0

10

20

30

40

50

60

Q4-13 Q1-14 Q2-14 Q3-14 Q4-14

Total Income

1,5

-1 -0,3

-3,9

6,8

-6

-4

-2

0

2

4

6

8

Q4-13 Q1-14 Q2-14 Q3-14 Q4-14

EBITDA

-3,9 -4,5 -8,6

-16,3

-57,5

-70

-60

-50

-40

-30

-20

-10

0

Q4-13 Q1-14 Q2-14 Q3-14 Q4-14

Net Profit/(Loss)

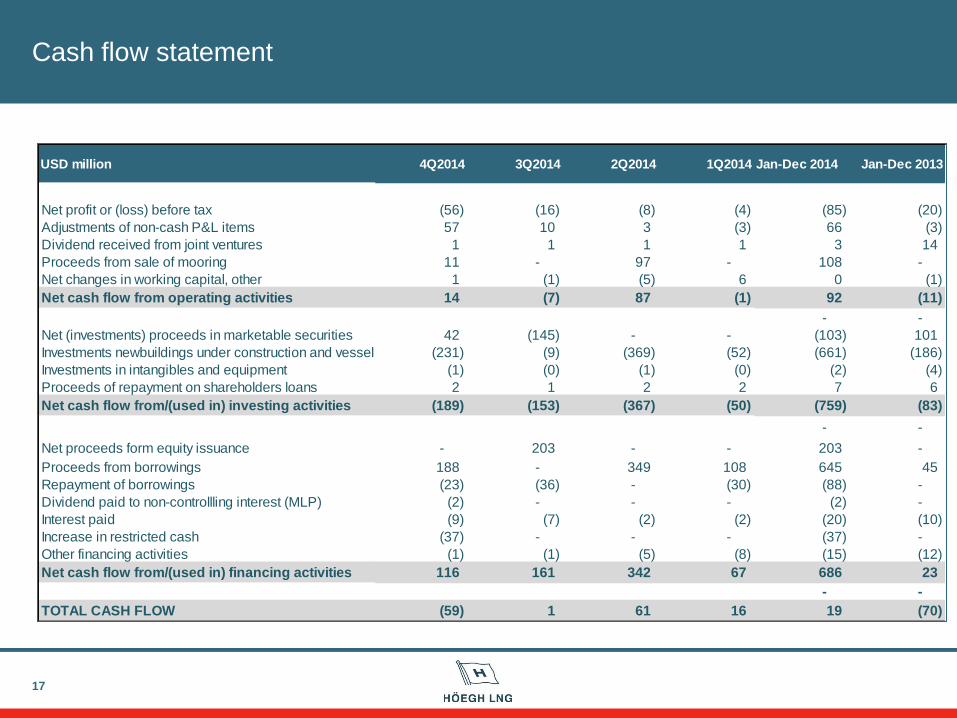

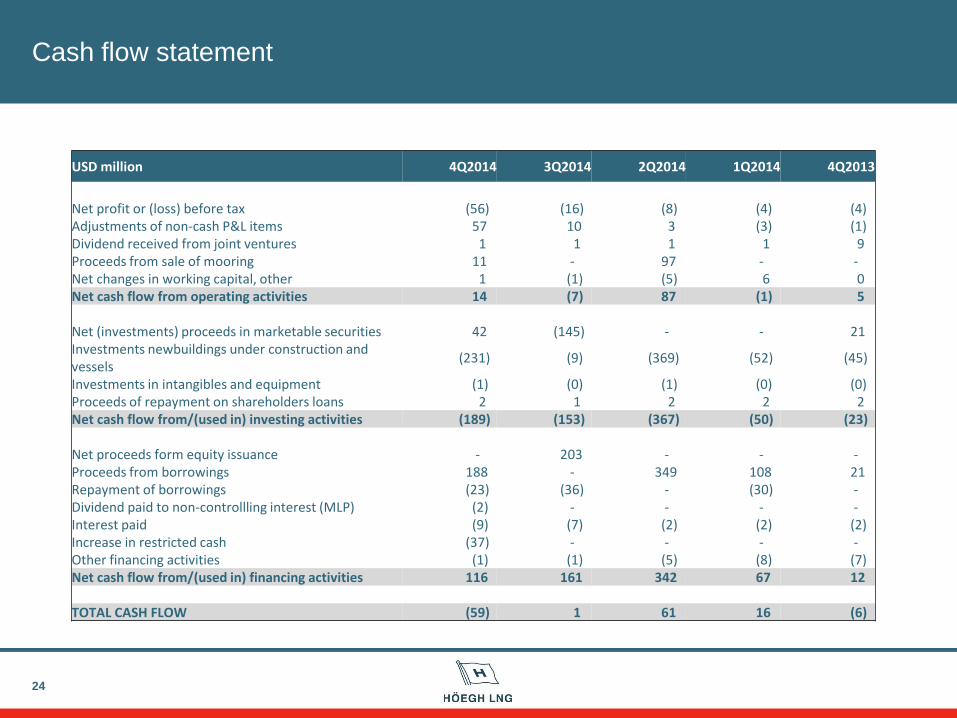

Cash flow statement

17

USD million 4Q2014 3Q2014 2Q2014 1Q2014 Jan-Dec 2014 Jan-Dec 2013

Net profit or (loss) before tax (56) (16) (8) (4) (85) (20)

Adjustments of non-cash P&L items 57 10 3 (3) 66 (3)

Dividend received from joint ventures 1 1 1 1 3 14

Proceeds from sale of mooring 11 - 97 - 108 -

Net changes in working capital, other 1 (1) (5) 6 0 (1)

Net cash flow from operating activities 14 (7) 87 (1) 92 (11)

- -

Net (investments) proceeds in marketable securities 42 (145) - - (103) 101

Investments newbuildings under construction and vessels (231) (9) (369) (52) (661) (186)

Investments in intangibles and equipment (1) (0) (1) (0) (2) (4)

Proceeds of repayment on shareholders loans 2 1 2 2 7 6

Net cash flow from/(used in) investing activities (189) (153) (367) (50) (759) (83)

- -

Net proceeds form equity issuance - 203 - - 203 -

Proceeds from borrowings 188 - 349 108 645 45

Repayment of borrowings (23) (36) - (30) (88) -

Dividend paid to non-controllling interest (MLP) (2) - - - (2) -

Interest paid (9) (7) (2) (2) (20) (10)

Increase in restricted cash (37) - - - (37) -

Other financing activities (1) (1) (5) (8) (15) (12)

Net cash flow from/(used in) financing activities 116 161 342 67 686 23

- -

TOTAL CASH FLOW (59) 1 61 16 19 (70)

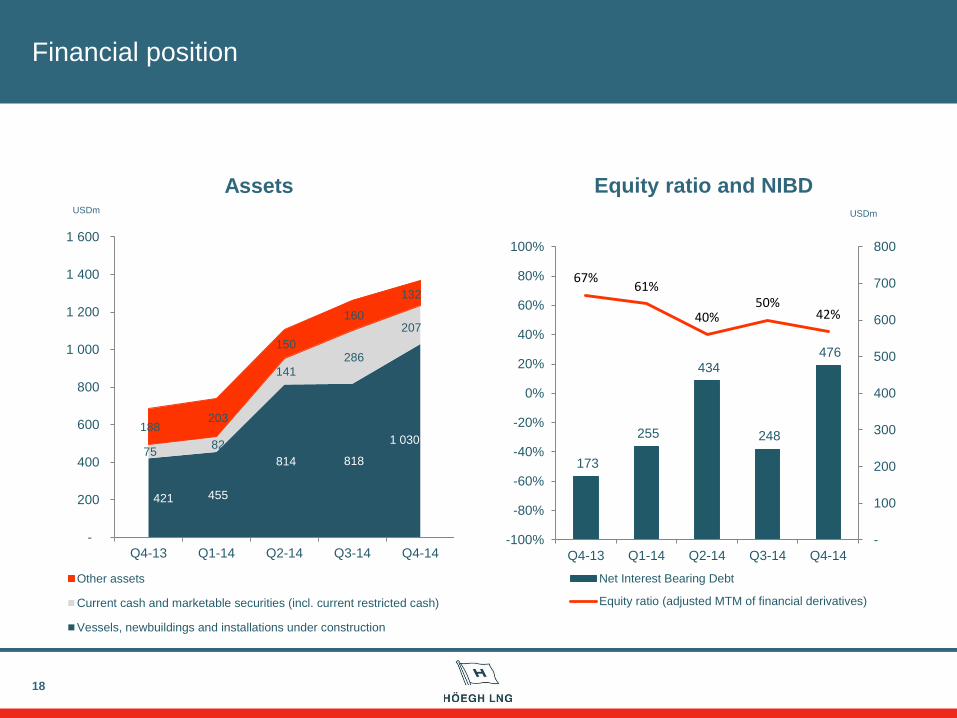

421 455

814 818

1 030 75

82

141

286

207

188 203

150

160

132

-

200

400

600

800

1 000

1 200

1 400

1 600

Q4-13 Q1-14 Q2-14 Q3-14 Q4-14

Other assets

Current cash and marketable securities (incl. current restricted cash)

Vessels, newbuildings and installations under construction

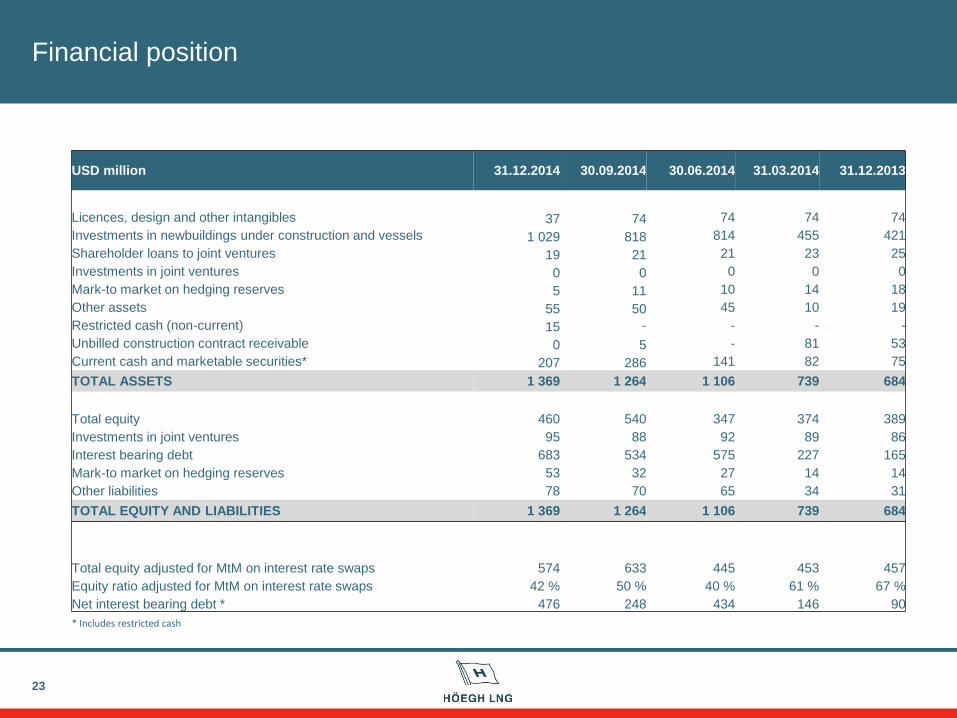

Financial position

18

USDm

Assets Equity ratio and NIBD USDm

173

255

434

248

476

67% 61%

40% 50%

42%

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

Q4-13 Q1-14 Q2-14 Q3-14 Q4-14

-

100

200

300

400

500

600

700

800

Net Interest Bearing Debt

Equity ratio (adjusted MTM of financial derivatives)

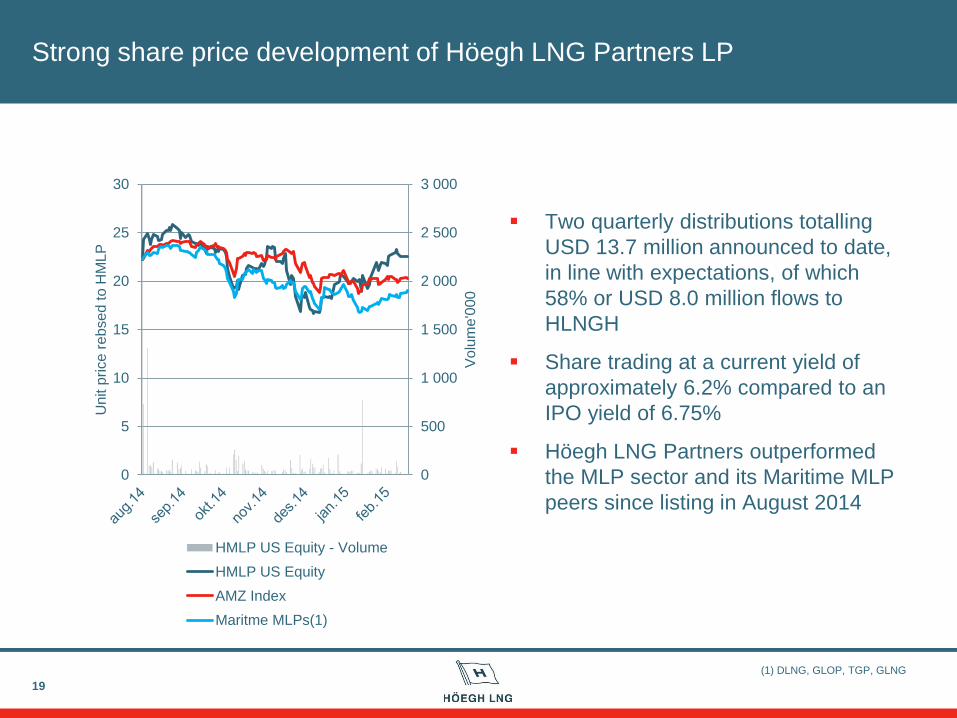

Strong share price development of Höegh LNG Partners LP

19

0

500

1 000

1 500

2 000

2 500

3 000

0

5

10

15

20

25

30

Volu

me'0

00

Un

it p

rice r

ebse

d to

HM

LP

HMLP US Equity - Volume

HMLP US Equity

AMZ Index

Maritme MLPs(1)

Two quarterly distributions totalling

USD 13.7 million announced to date,

in line with expectations, of which

58% or USD 8.0 million flows to

HLNGH

Share trading at a current yield of

approximately 6.2% compared to an

IPO yield of 6.75%

Höegh LNG Partners outperformed

the MLP sector and its Maritime MLP

peers since listing in August 2014

(1) DLNG, GLOP, TGP, GLNG

Financial summary fourth quarter 2014

20

Improved operating performance mainly due to Independence

Net profit adversely impacted by impairment charges

Strong balance sheet with capacity to fund further growth

Strong share price performance of Höegh LNG Partners LP

A dial-in Q&A session will be held at 3pm Oslo time / 9am EST time

See www.hoeghlng.com for dial-in details

Höegh LNG Holdings; Agenda for presentation of 4Q 2014 results

21

Additional information

Dedededw

Sveinung J.S. Støhle

President & CEO

Highlights/Markets/Summary

Steffen Føreid

CFO

Financials

Income Statement

22

USD million 4Q2014 3Q2014 2Q2014 1Q2014 4Q2013 Freight revenues 34,6 29,3 17,2 17,2 17,9 Voyage expenses (2,4) (3,9) - - (0,1) Construction contract revenue 8,1 6,1 10,0 28,2 14,6 Management and other income 2,4 (0,4) 2,7 3,6 8,9 Share of results from investments in joint ventures 2,7 2,6 2,5 2,2 4,2 TOTAL INCOME 45,3 33,8 32,3 51,3 45,5 Charterhire expenses (8,9) (8,9) (8,8) (8,7) (8,9) Construction contract expenses (6,0) (6,6) (6,8) (24,0) (12,8) Operating expenses (10,3) (8,5) (6,1) (6,9) (6,2) Project administrative expenses (4,5) (3,8) (4,8) (3,2) (4,9) Group administrative expenses (3,5) (5,1) (3,1) (4,7) (2,5) Business development expenses (5,3) (4,7) (3,1) (4,8) (8,7) EBITDA 6,8 (3,9) (0,3) (1,0) 1,5

Depreciation (7,8) (6,2) (4,2) (2,9) (4,6) Impairment (44,8) - - - - EBIT (45,8) (10,1) (4,5) (3,9) (3,1)

Interest expenses (8,9) (5,4) (3,6) (0,4) (0,6) Interest income 0,4 0,4 0,4 0,5 0,5 Other financial items (2,1) (0,8) (0,6) (0,7) (1,1) PROFIT OR (LOSS) BEFORE TAX (56,4) (15,9) (8,3) (4,5) (4,2)

Taxes (1,3) (0,4) (0,3) 0,0 0,3 NET PROFIT OR (LOSS) (57,7) (16,3) (8,6) (4,5) (3,9)

Financial position

23

USD million 31.12.2014 30.09.2014 30.06.2014 31.03.2014 31.12.2013

Licences, design and other intangibles 37 74 74 74 74

Investments in newbuildings under construction and vessels 1 029 818 814 455 421

Shareholder loans to joint ventures 19 21 21 23 25

Investments in joint ventures 0 0 0 0 0

Mark-to market on hedging reserves 5 11 10 14 18

Other assets 55 50 45 10 19

Restricted cash (non-current) 15 - - - -

Unbilled construction contract receivable 0 5 - 81 53

Current cash and marketable securities* 207 286 141 82 75

TOTAL ASSETS 1 369 1 264 1 106 739 684

Total equity 460 540 347 374 389

Investments in joint ventures 95 88 92 89 86

Interest bearing debt 683 534 575 227 165

Mark-to market on hedging reserves 53 32 27 14 14

Other liabilities 78 70 65 34 31

TOTAL EQUITY AND LIABILITIES 1 369 1 264 1 106 739 684

Total equity adjusted for MtM on interest rate swaps 574 633 445 453 457

Equity ratio adjusted for MtM on interest rate swaps 42 % 50 % 40 % 61 % 67 %

Net interest bearing debt * 476 248 434 146 90

* Includes restricted cash

Cash flow statement

24

USD million 4Q2014 3Q2014 2Q2014 1Q2014 4Q2013

Net profit or (loss) before tax (56) (16) (8) (4) (4) Adjustments of non-cash P&L items 57 10 3 (3) (1) Dividend received from joint ventures 1 1 1 1 9 Proceeds from sale of mooring 11 - 97 - - Net changes in working capital, other 1 (1) (5) 6 0 Net cash flow from operating activities 14 (7) 87 (1) 5 Net (investments) proceeds in marketable securities 42 (145) - - 21 Investments newbuildings under construction and vessels

(231) (9) (369) (52) (45)

Investments in intangibles and equipment (1) (0) (1) (0) (0) Proceeds of repayment on shareholders loans 2 1 2 2 2 Net cash flow from/(used in) investing activities (189) (153) (367) (50) (23) Net proceeds form equity issuance - 203 - - - Proceeds from borrowings 188 - 349 108 21 Repayment of borrowings (23) (36) - (30) - Dividend paid to non-controllling interest (MLP) (2) - - - - Interest paid (9) (7) (2) (2) (2) Increase in restricted cash (37) - - - - Other financing activities (1) (1) (5) (8) (7) Net cash flow from/(used in) financing activities 116 161 342 67 12 TOTAL CASH FLOW (59) 1 61 16 (6)

25