Coefficient = solvency capital* in proportion to solvency limit

© 2010 The Actuarial Profession www.actuaries.org.uk

Challenges for GI Actuaries

GIRO conference and exhibition 2010Solvency II IMAP Working Party

Our brief

The internal model approval process forSolvency II presents a number ofspecific challenges for GI actuaries. Forexample, what level of documentation issufficient for a third party actuary to gaincomfort over the model? How are therequirements for risk ranking andcalibration being interpreted in practice?And what level/extent of use are firmstargeting?

In this update, we will cover

the results of our research(esurvey, face-face interviews);

possible approaches to keyquestions on calibration, expertjudgement, risk ranking, profitand loss attribution,documentation and the use test

1Solvency II: IMAP

Agenda

Chair

Introduction

Key areas of research

Calibration

Expert Judgement

Risk Ranking

P&L Attribution

Documentation

Close & Next Steps

Solvency II: IMAP2

Our focusBridging CEIOPS requirements and business/modelling reality

Questions

How are the requirementsbeing interpreted byexperienced modellers?

How is the industryapproaching the tests?

Topics

Calibration

Expert Judgement

Use Test

Risk Ranking

Profit & Loss Attribution

Documentation

Solvency II: IMAP3

The ‘hurdle’ for each model test is likely to emerge over the next 2-3years. Views expressed here are those of the working party members.

Business Reality – your plans for the use test40+ firms responded to our esurvey

Top 5 – Uses Top 5 - Influence

4Solvency II: IMAP

94%

90%

90%

87%

81%

Capital management

Businessplanning/strategy

Measurement ofmaterial risks

Reinsurance

Development andmonitoring of risk

appetite73%

77%

80%

83%

93%

Eficient use ofcapital/performance

measurement

Developing andmonitoring of risk

appetite

Reinsurance

Businessplanning/strategy

Capital management

© 2010 The Actuarial Profession www.actuaries.org.uk

Calibration

Approach to estimating 12 months capital still unclear – ifmuch discussed !

How do you interpret therequirement?

Almost all plan to produceSCR on S2 basis(99.5% VaR over 1 year timehorizon, liabilities measured toultimate)

Most were plan to use analternative measure foreconomic capital

Few had developed prototypeSCR calculations

How do you plan toadjust your ICA model to

calculate the SCR over a 1year time horizon and VaR

measure?Are you consideringusing a different time

period or risk measure, ifso, why?

6Solvency II: IMAP

One year calibration methods identified

Perfectforesight

7Solvency II: IMAP

Simulatedre-reserving

Proportionalemergence

Merz-Wuthrich(simulated)

Hindsightre-estimation

QIS 5 USPMethod 1

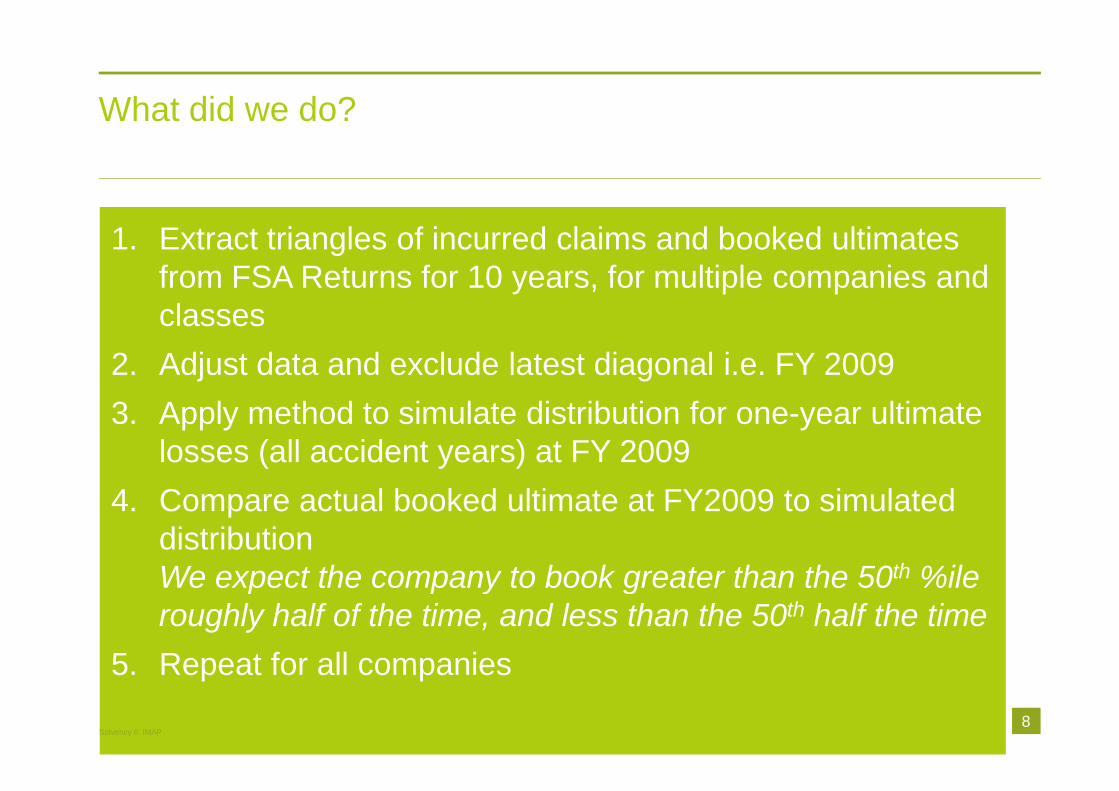

What did we do?

1. Extract triangles of incurred claims and booked ultimatesfrom FSA Returns for 10 years, for multiple companies andclasses

2. Adjust data and exclude latest diagonal i.e. FY 2009

3. Apply method to simulate distribution for one-year ultimatelosses (all accident years) at FY 2009

4. Compare actual booked ultimate at FY2009 to simulateddistributionWe expect the company to book greater than the 50th %ileroughly half of the time, and less than the 50th half the time

5. Repeat for all companies

8Solvency II: IMAP

Results – Incurred with a 10% reserve bias adjustment

One Year Calibration Predictiveness Test Results - Incurred with a 10%reserve bias adjustment

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

0% 20% 40% 60% 80% 100%

Recognised Percentile

CD

F

Perfect foresight

Simulated Re-reserving (CL)

Hindsight Re-estimation

Ultimate Emergence

Reserve Emergence

Simulated M-W

QIS 5 USP Method 1

Y=X

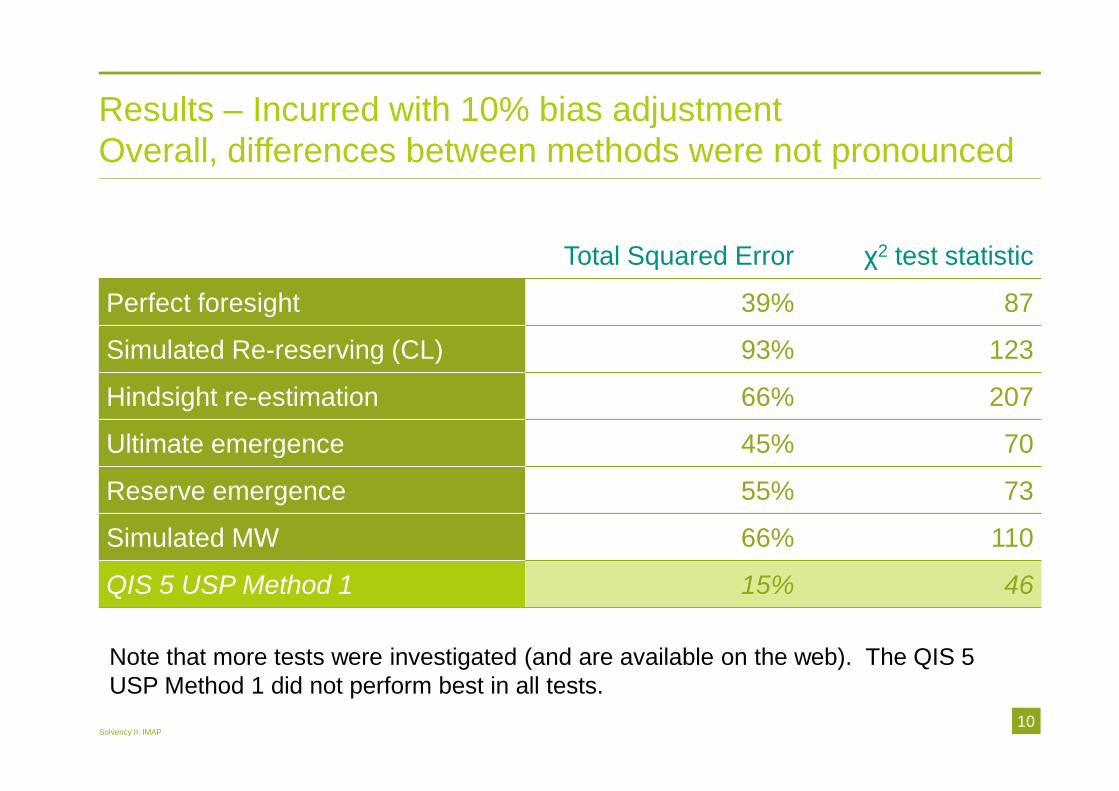

Results – Incurred with 10% bias adjustmentOverall, differences between methods were not pronounced

10Solvency II: IMAP

Total Squared Error χ2 test statistic

Perfect foresight 39% 87

Simulated Re-reserving (CL) 93% 123

Hindsight re-estimation 66% 207

Ultimate emergence 45% 70

Reserve emergence 55% 73

Simulated MW 66% 110

QIS 5 USP Method 1 15% 46

Note that more tests were investigated (and are available on the web). The QIS 5USP Method 1 did not perform best in all tests.

© 2010 The Actuarial Profession www.actuaries.org.uk

Expert Judgement

Scope of Expert Judgement

Our viewIt is sensible to include all expertjudgements, but if we do

Materiality and proportionalityare key

Where expert judgements arematerial, important to review anddocument thoroughly

Less detail needed if expertjudgement is less material

CEIOPS view

Do the requirements apply to

Data ...

or

… all expert judgements?

12Solvency II: IMAP

Independent review

– internal

– external

Other forms of validation

– Consideration of how well theassumption fits the data

– Comparison to other sources

– Back testing

What processes do or will you use to justify the expertjudgement, with respect to selection of data, methods,

parameters, or other areas?

13Solvency II: IMAP

Expert Judgement

How do you interpret the requirements?

Possible Process

1. Defineproblem orissue

14Solvency II: IMAP

2. Identifyappropriateexpert

3. Collectdata

5. Makejudgement

6.Document

7.Review

4. Analyseand considerdata

8. Sign offjudgement tobe used ininternal model

Key Issues

When is a judgement materialenough to document in detail?

Should the expert be:

– part of the risk managementfunction?

– business representative?

– part of the modelling team?

– external to the company?

How can you demonstrate thatsomeone is an expert?

What happens if experts disagree?

How do you allow for expertjudgement within change policy?

What are the implications if theexpert judgement is notcommissioned specifically for theinsurer?

How should you handle expertjudgements that are "inherited" fromexternal data or external models?

How easy is it to create a trackrecord of expert judgements?

What should the governancearrangements around the use ofexpert judgement look like?

15Solvency II: IMAP

© 2010 The Actuarial Profession www.actuaries.org.uk

Risk Ranking

What are our key risks? What are interrelationships? Do we model theseappropriately?

What are our most material risks? Do these drive the tail?

Does the model drive capital allocation?

Does the model reflect structure and nature of risks?

Needs to be a common sense and pragmatic solution

the ability of the internal model to rank risk shall besufficient to ensure that it is widely used in and plays an

important role ... their risk-management system and decision-making processes, and capital allocation” Article 121

17Solvency II: IMAP

Risk Ranking ....

How do you interpret the requirement?

Demonstrating that the model ranks risk appropriately –possible approaches

IndependentActuarialReview

18Solvency II: IMAP

Use ofResults

Analysis ofDrivers

Comparisonto RiskRegister

Stress andScenarioTesting

CoV, ReturnPeriod,CapitalAllocation

Review byManagement,Business orOperations

Risk ReturnMeasures

A worked example – Operational Risk

19Solvency II: IMAP

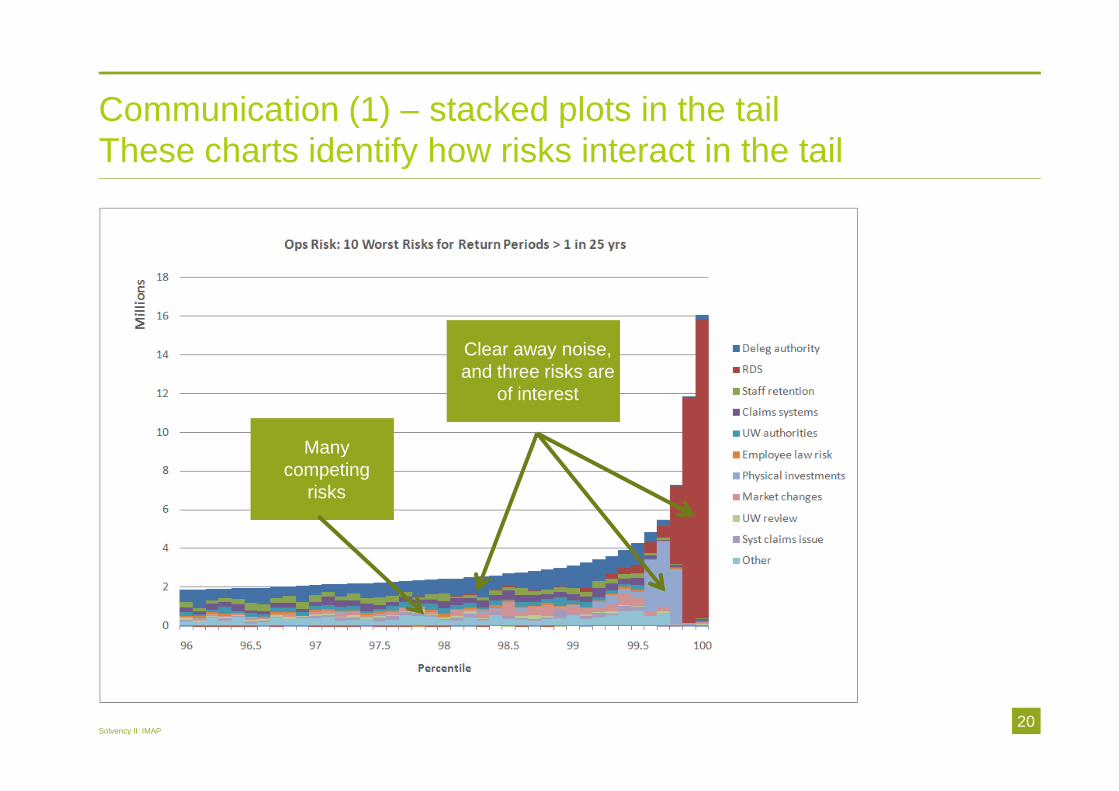

Manycompeting

risks

Clear away noise,and three risks are

of interest

Communication (1) – stacked plots in the tailThese charts identify how risks interact in the tail

Solvency II: IMAP20

Communication (2) – treemaps versus pie chartsTreemaps communicate relativities more effectively

21Solvency II: IMAP

vs

Note graphs show capital allocated by risk

Communication (3) – Frequency and Severity PlotsDrill down by function, or individual ...

Solvency II: IMAP22

© 2010 The Actuarial Profession www.actuaries.org.uk

Profit & Loss Attribution

“For each level of granularity, we will compare the actual profit or loss againstthe distribution of profit or losses projected by the model.”

“To support management in understanding the drivers of profitability”

“To validate the assumptions in the model against emerging experience”

Demonstrate how the categorisation of riskchosen in the internal model explains the causes and

sources of profits and losses. The categorisation of risk andattribution of profits and losses shall reflect the risk profile of

the insurance and reinsurance undertakings. Article 123

24Solvency II: IMAP

Profit and Loss Attribution ....

How do you interpret the requirement?

Graphical Display of Profitability

The variability in profit comes from avariety of sources:

Lines of business (ie. property,motor etc)

Risks (ie. non-life, market,operational etc.)

Terms of trade & commissionarrangements

Business Strategy

And can be controlled by levers thatcause profit variability:

Investment portfolio

Reinsurance protection

Pricing & underwriting

Terms of trade & commissionarrangements

Business Strategy

25Solvency II: IMAP

Graphical Display of Profitability

26Solvency II: IMAP

Pro

pe

rty

bu

sin

ess

Mo

tor

bu

sin

ess

Channel 1 Channel 2 Channel 3

Channel 1 Channel 2 Channel 3

Profit & Loss Attribution – a waterfall chart helps to track thekey movements in sources of profit from plan

This enables

– the business to understand the areas of the internal model where differences havearisen from what was expected

– the actuaries to backtest volatility assumptions in the model, by looking at year-onyear deviations, or more importantly trends

27Solvency II: IMAP

Profit & Loss Attribution – different approaches toimplementing the test

Challenges

Business Plan and CapitalAssessment may not bejoined up

SII analysis may not be seenas value add by management

Allocation of investment,expenses or reinsurance maybe arbitrary

Test increasingly spurious atlower levels of granularity

What trigger levels? Trendsor year on year deviations?

28Solvency II: IMAP

Definition of Profit

Solvency II

Accounting e.g. UK GAAP

Management e.g. UW Year

Granularity

By Entity, Division or LOB

Insurance, Investment oroperational results

Historical Data

• Current Year / Prior Years

© 2010 The Actuarial Profession www.actuaries.org.uk

Documentation

Documentation requirements ...

An independent,knowledgeablethird party can :

30Solvency II: IMAP

“form a sound judgment as to the reliability of the internalmodel ... and understand the reasoning and the underlyingdesign and operational details of the internal model.”Former CP56 9.53.

“understand the model framework, its methodology, theunderlying assumptions, and the limits of applicability of themodel” Former CP56 9.40

“use a different platform to build a consistent internal modelwithin a reasonable time period.” Former CP56 9.41

“in principle reproduce the model outputs if all theparameters and exposure data were available.” FormerCP56 9.40

Views from our surveyWhat do you need to form a sound judgement on the model?

Solvency II: IMAP31

KeyDocumentation

ModelPurposeand Uses

Clear AuditTrail

Plain Englishdescription

of themethodology

Flowchartsor Screenshots

Results

ValidationResults

(eg sensitivitytesting)

Access tomodel

Ability to runtesting andvalidation

Summary of CP requirements – Possible DocumentationFramework

Solvency II: IMAP32

Solvency II: IMAP

Our focusBridging CEIOPS requirements and business/modelling reality

Questions

How are the requirementsbeing interpreted byexperienced modellers?

How is the industryapproaching the tests?

Topics

Calibration

Expert Judgement

Use Test

Risk Ranking

Profit & Loss Attribution

Documentation

Solvency II: IMAP33

The working party continues next year –volunteers welcome !

Questions or comments?

Expressions of individual views by members ofThe Actuarial Profession and its staff areencouraged.

The views expressed in this presentation arethose of the presenters.

34© 2010 The Actuarial Profession www.actuaries.org.uk