Genera Inc_Annual Report 2009

66

Annual Report 2009

description

report

Transcript of Genera Inc_Annual Report 2009

Annual Report 2009

Genera Inc. and subsidiaries

Consolidated and Standalone Financial Statements as at 31 December 2009 together with

Independent Auditor's Report

Genera d.d. 31 December 2009

CONTENT

Management Report 1-5

Report of the Supervisory Board 6-7

Responsibility of the Management for the Financial Statements

8

Independent Auditor's Report

9

Financial Statements:

Consolidated Balance sheet as at 31 December 2009 10 Balance sheet as at 31 December 2009 11 Consolidated Income Statement for the period from 1 January to 31 December 2009 12 Income Statement for the period from 1 January to 31 December 2009 13 Consolidated Cash Flow Statement for the period from 1 January to 31 December 2009 14

Cash Flow Statement for the period from 1 January to 31 December 2009 15

Consolidated Statement of Changes in Equity for the period from 1 January to 31

December 2009 16

Statement of Changes in Equity for the period from 1 January to 31 December 2009 17

Notes to the Financial Statements 18-62

Statement of the persons responsible for the preparation of the report

63

Genera d.d. 31 December 2009

1

Report of the Management Board

The total consolidated sales income for 2009 grew for 6% in relation to last year and amount to HRK 163.9

million. The consolidated gross profit recorded an increase of even 54.43% in relation to 2008. The gross

income in 2009 amounted to HRK 75.54 million, while in the same period last year it amounted to HRK

34.22 million. In relation to the preceding year when the company operated with a loss of HRK 37.76

million, the achieved operational profit in 2009 of HRK 2.1 million was a significant indicator of a trend of

more and more successful business operations. Therefore the consolidated loss prior to taxation in 2009

amounts to only HRK 0.35 million while in 2008 it amounted to HRK 37.3 million.

The significant decrease of losses in 2009 are the result of the abovementioned increase of income as well

as of a more efficient management of expenses (decrease of material and energy costs of 13.3% and

personnel costs of 8.6% in relation to 2008). During 2009 Genera Inc. acquired its own shares on several

occasions. On 31/12/2009 Genera Inc. held 50.412 shares, constituting 2.73% of the share capital of the

Company.

The complete audited individual and consolidated financial statement for 2009, including notes, contains, to

the best knowledge of the Management Board, a true overview of the development and results of the

business operations and the Company's position as well as that of the companies included in the

consolidation, which statement is an integral part of this report of the management.

Significant events in 2009

Change of the Company's name

The year 2009 was also marked by the proposal of the Management Board of the then Veterina Inc. to

change the company name from Veterina Inc. to Genera Inc., which was the result of the newly defined

strategic goals and the need to adapt to the new organisational structure of the Group.

It was establish that there was a realistic basis to expand the business operations of the Group in the future

also to human pharmaceutics, either through acquisitions or through the establishment of new companies,

therefore the Company's Management Board considered the company name Genera Inc. more appropriate.

Apart form this, as an umbrella company, Veterina Inc. was the owner of different companies of different

business activities some of which were not related to veterinarian activities. Apart from the strategic

orientation to human pharmaceutics, this was an additional argument to pass the decision on the change of

the company name. In accordance with the best practice of corporate management, the Management

Board of Veterina Inc. proposed to the Company's General Assembly the change of the company name,

which was confirmed at the session of the General Assembly held on 16 June 2009. Therewith the full

company name became Genera dioničko društvo za razvoj i proizvodnju farmaceutskih proizvoda (Genera

Incorporated for development and production of pharmaceuticals), and the abbreviated company name

Genera Inc.

Genera d.d. 31 December 2009

2

New limited liability companies commence operations

Genera Inc. is an umbrella company having the role of strategic and financial management of limited liability

companies constituting the Genera group. Already at the end of 2008 five limited liability companies were

established which commenced with their operational business operations in January 2009, having the

following activities:

VETERINA Ltd. – production, development and sale of vaccines and veterinarian drugs,

VETERINA NUTRICIUS Ltd. – production, development and sale of animal feed additives,

VITAMEDERA Ltd. - production, development and sale of disinfectants,

VETERINA KALINOVA Ltd. - production, development and sale of agrochemicals, and

VETERINA USLUGE Ltd. - support to the operative business activities by providing information, accounting,

energy, personnel and similar services.

Significant events in Veterini Ltd., the largest member of the Group

In January 2009, Veterina Ltd. was approved the Good Manufacturing Practice Certificate (hr. DPP, eng.

GMP) for the production of dry drugs on the territory of the European Union. The GMP Certificate is a

confirmation that Veterina Ltd. has adjusted the manufacturing process and the quality management system

to the EU Standards (requirements of good manufacturing practice of the European Union), which is a

prerequisite for the sale of veterinarian-medical products in the countries of the European Union. The

inspection included the dry drugs production machinery, quality control laboratories (chemical-

chromatographic laboratory, instrumental laboratory and part of the microbiological laboratory), logistics as

well as the entire quality assurance system.

The positive findings of the inspection and conformity of all dry drugs production processes with the strictest

European regulations and quality standards enables Veterina the registration, sale and distribution of

products in countries of the European Union which is a prerequisite for the survival and future growth in

these markets.

In December 2009, another GMP inspection was successfully conducted in Veterina Inc. which resulted in

the approval of a GMP Certificate in February 2010. This certificate refers to the production of lyophilised

vaccines and is a prerequisite for their sale on the European and other foreign markets.

Apart form this certificate being proof of the conformity with the strictest European regulations, it also

constitutes a significant step towards the most important goal in 2010 – the growth of production and

increase of export on foreign markets.

The intention of Genera Group is to confirm the entire pharmaceutical production process with a good

manufacturing practice as soon as possible and thus increase its competitiveness in all segments of its

business operations.

As the company already has a large share in the Croatian market, it is focused on the increase of export

which the company defined as the key factor of the growth and the main definition of business operations in

2009 and the following years. The year 2009 was marked by the beginning of the realisation of the

expansion strategy through the increase of export and the first shipments of vaccines were delivered to the

Genera d.d. 31 December 2009

3

new markets of Northern Africa (Algeria and Egypt). Also, the cooperation with the distributor in Iran was

intensified to whom an expanded range of products was offered and negotiations and preliminary activities

for the launching of products on the Russian market were initiated.

At the end of 2009 Veterina Ltd. also signed the agreement for the development of six strains of vaccines

with the laboratory Gezondheidsdienst voor Dieren BV, one of the leading verification-research laboratories

in Europe having their seat in the Netherlands. The development of six strains of vaccines will result in the

obtaining of European registration files for ten internationally competitive products.

The signing of this agreement constitutes a new phase in the development of Veterina Ltd. in which

significant financial assets are being invested for the development of vaccines.

Significant events in other members of the Group

In other affiliated companies: Veterina Kalinova Ltd., Veterina Nutricius Ltd., Vitamedera Ltd. , Veterina

usluge Ltd., Veterina Plus Ltd. and Genera Analitika Ltd. there were no important events which would

significantly affect the financial status of these companies. For the purpose of more successful business

operations in 2009, a number of smaller investments were initiated, such as investments into equipment,

reorganisation of the existing machinery and the renewal o ISO (9001:2000, 14001:2004, 13485:2003) and

HACCP (Codex Alimentarius) certificates. The continuance of stable and efficient business operations is

expected in the following period.

In July 2009 the Supervisory Board unanimously passed the decision by which it gave its consent to the

Management Board of the Company to proceed with the co-establishment of the company Genera Lijekovi

Ltd. and the establishment of the company Genera Analitika Ltd. These decisions were passed in

accordance with the announcements of the Management Board on the strategy of expanding the business

operations also to human pharmaceutics.

The basic business activity of the company Genera Lijekovi shall be the development, production and sale

of generic drugs. The business shares of Genera Inc. in the company Genera Lijekovi Ltd. amount to 10%.

Genera as the sole founder, also established the company Genera Analitika. The basic business activity of

this company shall be the rendering of services of laboratory analyses and quality control testing of raw

materials, intermediate goods and finished pharmaceutical products for human and veterinarian use.

Genera Analitika shall apply the quality system ISO 17025, as well as GMP and GLP standards. The

decision on the establishment of General Analitika results from the increased necessity for such analyses

within the Genera Group and the entire region. Genera Inc. recognised this trend on the market and its goal

is for Genera Analitika to position itself as an independent GLP centre for quality control and testing of

pharmaceutical products („Contract Analytical Laboratory“) which would render laboratory testing services

also outside the group. With Croatia's accession to the EU, analyses which the centre would perform would

be acknowledged in the member states of the EU. A significant element of the increase in the number of

such analyses within the Group refer to the expansion of business operations also to human pharmaceutics

Genera d.d. 31 December 2009

4

as well as the planned increase of the production of interactive and live vaccines for poultry within the

affiliated company Veterina Ltd.

Within the restructuring, the decision on the liquidation of the company Veterina Polska was passed due to

the multiannual losses in business operations. Despite the negative effect on the consolidated results of the

Group in 2009 these are positive and important strategic moves of which a positive result is expected in the

following period. During 2010 the procedure of closing the company should be completed.

Business events after the completion of the business year

All important events which occurred after the completion of the business year are described in the notes of

the reports and constitute an integral part of the management's reports.

Description of the most important risks and uncertainties

The company and the Group are primarily exposed to financial risks, such as risks of foreign exchange rate

changes, credit risks, liquidity risks and interest rate risks.

The risks of foreign exchange rate changes is a risk of the change of the value of financial instruments due

to exchange rate changes. The Company and the Group are mostly exposed to risks of EUR exchange rate

changes.

The interest risk presumes the risk that the interest costs for financial instruments will be changeable during

the period. The Company and the Group have long-term and short-term liabilities under loans to which

changeable interests are calculated which expose the Company and the Group to a price and cash flow

risk.

The credit risk is the risk that one party of a contractual relationship will not meet its obligations and

therewith cause financial losses to the other party. The Company and the Group accepted the business

policy of conducting business only with credit worthy companies and companies ensured with guarantees

wherewith the possibility of financial losses occurring due to non-fulfilment of obligations is decreased.

The Company and the Group are not exposed to large credit risks in relation to their partners or client

groups of similar characteristics.

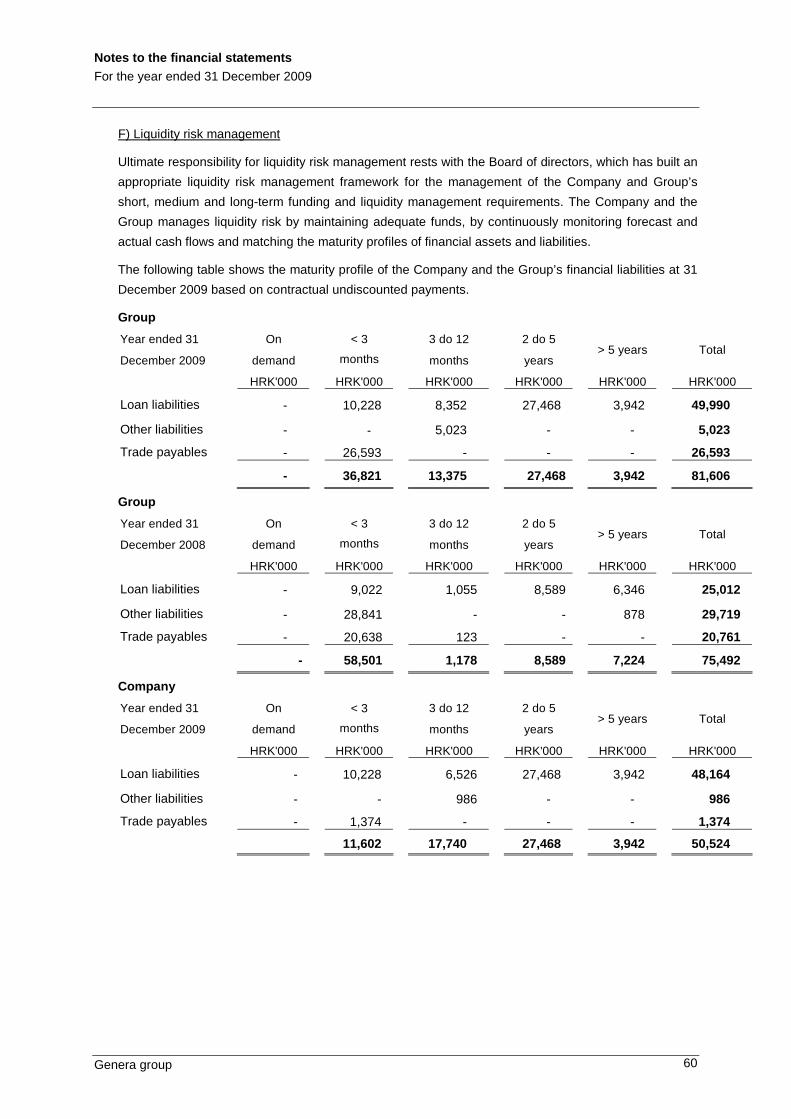

The Company and the Group manage the liquidity risk in the manner that they secure bank loans and

monitor the foreseen and actual cash flow comparing it with the maturity of the financial assets and

liabilities.

The entire business operations of Genera are adjusted to the securing and management of risks in the field

of health protection, security and environment. All activities in the implementation of safety at work are

directed at the removal, or decrease of risks in accordance with national laws and regulations.

The financial statement for 2009 will be available at Genera and at the Zagreb Stock-Exchange, as well as

published through HINA.

Genera d.d. 31 December 2009

5

As Genera is a joint-stock company the shares of which have been traded on an organised securities

market since 2008 also the Codex on corporate management is applied which is published on the pages of

the Zagreb Stock Exchange and the website of the Company, and in case of its non-application it has to

state the reason for the no-application. The main reason for the non-application of certain provisions of the

codex result from the specificity of the shareholder structure in which one shareholder holds almost 70% of

votes in the Company as well as in the effort for an efficient functioning of the Supervisory Board. Upon the

publishing of the questionnaire on the application of the Codex of corporate management it becomes an

integral part of this report.

Genera Inc. For and on behalf of Genera Inc.:

Svetonedjeljska 2, Kalinovica

10436 Rakov Potok

Croatia

Ivan Drpić Ana Hanžeković Čorak

Kalinovica, 31 March 2010 Chairman Member

of the Management Board of the Management Board

Genera d.d. 31 December 2009

6

Report of the Supervisory Board

During 2009 the members of the Supervisory Board of Genera Inc. ("the Company") were: Ivan Majdak,

Ph.D., as the Chairman and Mrs. Zrinka Vuković, BEc, Marcel Majsec, Ph.D., Franjo Gregurić, Ph.D. and

Mladen Vedriš, Ph.D. as members of the Supervisory Board.

Activities of the Supervisory Board

During 2009 the Supervisory Board in the abovementioned composition held four sessions at which the

following issues:

- the initiation of investments into facilities for the production of live and inactivated vaccines for

poultry farming. The Supervisory Board gave its consent to the implementation of a partial

reconstruction of the existing vaccine production facilty.

-Co-establishment of the company Genera Lijekovi Ltd. and the establishment of the company

Genera Analitika Ltd. and the said decisions were passed in accordance with the announcements

of the Management Board on the strategy on expanding the business operations to human

pharmaceutics.

-The initiation of the liquidation procedure of the company Veterina Polska due to multiannual

losses in the business operations.

-The potential activities of the Management Board on the acquisition of the company Genera

Istraživanje Ltd.

Apart from the abovementioned issues, the Supervisory Board discussed the current business operations of

the Company, the financial results as well as the preliminary income and expenditure plan for 2010.

Activities of the Audit Committee

In 2009 the composition of the Audit Committee remained unchanged in relation to 2008, and it was

composed of the following members: Ivan Majdak, Ph.D., Višnja Uzelac, BEc and Mrs. Zrinka Vuković, BEc,

During 2009 the Audit Committee met two times. The main issue of the first meeting was the potential credit

arrangement by Zagrebačka banka and in reference to that, the possibility of acquiring the ownership share

of Genera Inc. in Genera Istraživanje Ltd. as well as the issue of the conformity of the security instruments

for the said credit with the Companies Act, the Capital Market Act and the protection of rights of all

shareholders of the Genera Group. At the second meeting of the Audit Committee the potential increase of

the ownership share of Genera Inc. in the company Genera Lijekovi Ltd. was discussed as the most

transparent manner of financing the development of that company.

Financial statements

The Supervisory Board considered and approved the audited consolidated and non-consolidated financial

statements.

Genera d.d. 31 December 2009

7

The Management Board ensures the preparation of the financial statements in accordance with the

International Standards of Financial Reporting. Pursuant to the best knowledge of the Supervisory Board,

the annual financial statements were prepared in accordance with the state in the business books of the

Company and show the accurate assets and business status of the Company. The statements are prepared

in HRK – the reference currency of the Company.

The Supervisory Board also reviewed the report of the Management Board on the status of the Company to

which it had no objections.

The Supervisory Board accepted the proposal of the Management Board to use the realised profit of the

Company in 2009 in the amount of HRK 1,750,437.11 for the coverage of the transferred loss from the

preceding period.

The copies of all financial statements as well as of the report of the Management Board on the status of the

company are available for insight at the Company as well as at the website of the Zagreb Stock Exchange

and Genera Inc.

Audit report

The Supervisory Board reviewed and accepted the report of the authorised auditor of the Company, Nexia

Revizija d.o.o., on the consolidated and non-consolidated financial statements of the Company.

Conclusion

Pursuant to the performed supervision of the business operations of the company, the Supervisory Board

unanimously determined that the Company acts in accordance with the decisions of the general Assembly,

the Company deeds and the positive regulations of the Republic of Croatia.

Ivan Majdak

Chairman of the Supervisory Board

Genera d.d. 31 December 2009

8

Responsibility of the Management for the Financial S tatements

Pursuant to the Croatian Accounting Law (Official Gazette 109/07), the Board is responsible for ensuring

that financial statements are prepared for each financial year in accordance with statutory requirements on

financial reporting applicable in the Republic of Croatia for large companies and companies whose shares

or debt instruments are listed, or are in the process of being listed on the organized market for trading

securities which, until the date when Croatia becomes a member of the European Union, are based on

International Financial Reporting Standards, their amendments, and related interpretations that are defined

by the Croatian Committee for the Standards on Financial Reporting (further: the Committee) and which are

published in the Official Gazette.

The Board has a reasonable expectation that the Company and Group have adequate resources to

continue in operational existence for the foreseeable future. For this reason, the Board continues to adopt

the going concern basis in preparing the financial statements.

In preparing those financial statements, the responsibilities of the Board include ensuring that:

• appropriate accounting policies are selected and then applied consistently;

• judgements and estimates are reasonable and prudent;

• applicable accounting standards are followed, subject to any material departures disclosed and

explained in the financial statements; and

• financial statements are prepared on the going concern basis unless it is inappropriate to presume that

the Company will continue in business.

The Board is responsible for keeping proper accounting records, which disclose with reasonable accuracy

at any time the financial position of the Company and Group and must also, ensure that the financial

statements comply with the Croatian Accounting Law (Official Gazette 109/07). The Board is also

responsible for safeguarding the assets of the Company and Group and hence for taking reasonable steps

for the prevention and detection of fraud and other irregularities.

Genera Inc.

Svetonedjeljska 2, Kalinovica

10436 Rakov Potok, Croatia

Ivan Drpić Ana Hanžeković Čorak

Kalinovica, 31 March 2010 Chairman of the Member of the

Management Board Management Board

9

Independent Auditor’s Report

To the Management Board and Shareholders of Genera I nc.:

We have audited the accompanying consolidated and standalone financial statements of Genera Inc.

(herein below: the Group/Company), which comprise of the Balance Sheet as at 31 December 2009, the

Income Statement, Statement of Changes in Equity and Cash Flow statement for the year then ended, and

a summary of significant accounting policies and other explanatory notes as presented on pages 8 to 59.

Management’s Responsibility for the financial statem ents

Management is responsible for the preparation and fair presentation of these financial statements in

accordance with statutory requirements on financial reporting applicable in the Republic of Croatia for large

companies and companies whose shares or debt instruments are listed, or are in the process of being listed

on the organized market for trading securities (further referred as “statutory requirements on financial

reporting for large companies”). This responsibility includes: designing, implementing and maintaining

internal control relevant to the preparation and fair presentation of financial statements that are free from

material misstatement, whether due to fraud or error; selecting and applying appropriate accounting

policies; and making accounting estimates that are reasonable in the circumstances.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted

our audit in accordance with International Standards on Auditing. Those standards require that we comply

with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the

financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the

financial statements. The procedures selected depend on the auditor's judgment, including the assessment

of the risks of material misstatement of the financial statements, whether due to fraud or error. In making

those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair

presentation of the financial statements in order to design audit procedures that are appropriate in the

circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal

control. An audit also includes evaluating the appropriateness of accounting policies used and the

reasonableness of accounting estimates made by management, as well as evaluating the overall

presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our

audit opinion.

Opinion

In our opinion, the financial statements give true and fair view of the Company and the Group as of 31

December 2009 and the results of its operations, cash flows and changes in equity for the year then ended

in accordance with statutory requirements on financial reporting applicable in the Republic of Croatia for

large companies and companies whose shares or debt instruments are listed, or are in the process of being

listed on the organized market for trading securities.

Nexia revizija d.o.o. Siniša Dušić

Zagreb, 31 March 2010 certified auditor

Consolidated Balance Sheet As at 31 December 2009

Genera group 10

Notes 31/12/2009 31/12/2008

HRK '000 HRK '000

ASSETS

Long term assets 98,051 103,147Intangible assets 4 1,834 1,510Property, plant and equipment 5 95,825 101,048Financial assets 6 181 589Deferred tax asset 211 -

Current assets 151,505 141,346Inventory 7 53,047 53,258Trade receivables 8 72,124 68,747Other receivables 9 9,353 6,408Financial assets 10 1,702 21Cash and cash equivalents 11 15,279 12,912

TOTAL ASSETS 249,556 244,493

EQUITY AND LIABILITIES

Equity 12 166,598 169,001Share capital 184,486 184,486Legal reserves - 1,000Reserves for treasury shares 8,430 8,430Treasury shares (3,946) (1,430)Retained earnings (21,770) 14,366Exchange differences on translation of a foreign operation 4 (82)Profit or loss for the current period (606) (37,769)

Long term liabilities 32,092 15,814Long term loans 14 31,410 14,936Long term provisions 13 682 878

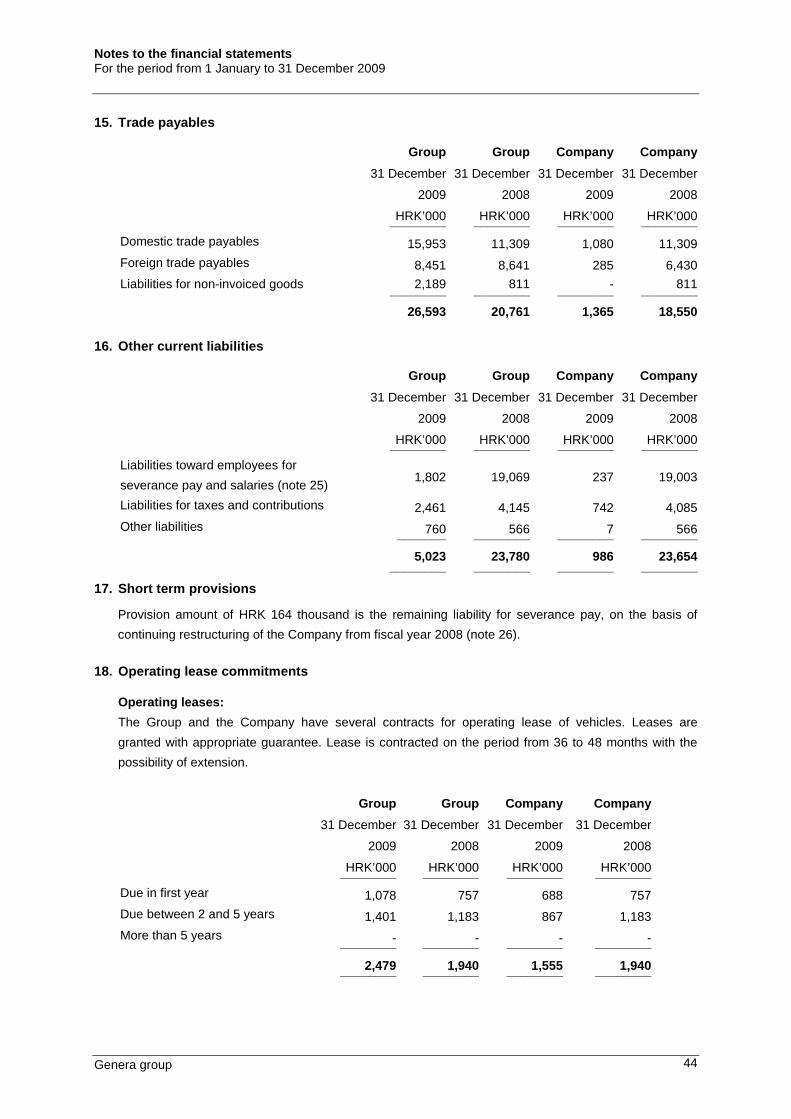

Current liabilities 50,360 59,462Trade payables 15 26,593 20,761Short term provisions 17 164 4,845Short term loans 14 18,580 10,076Other current liabilites 16 5,023 23,780

Accrued expenses 506 216

TOTAL EQUITY AND LIABILITIES 249,556 244,493

Notes are an integral part of Consolidated Balance Sheet

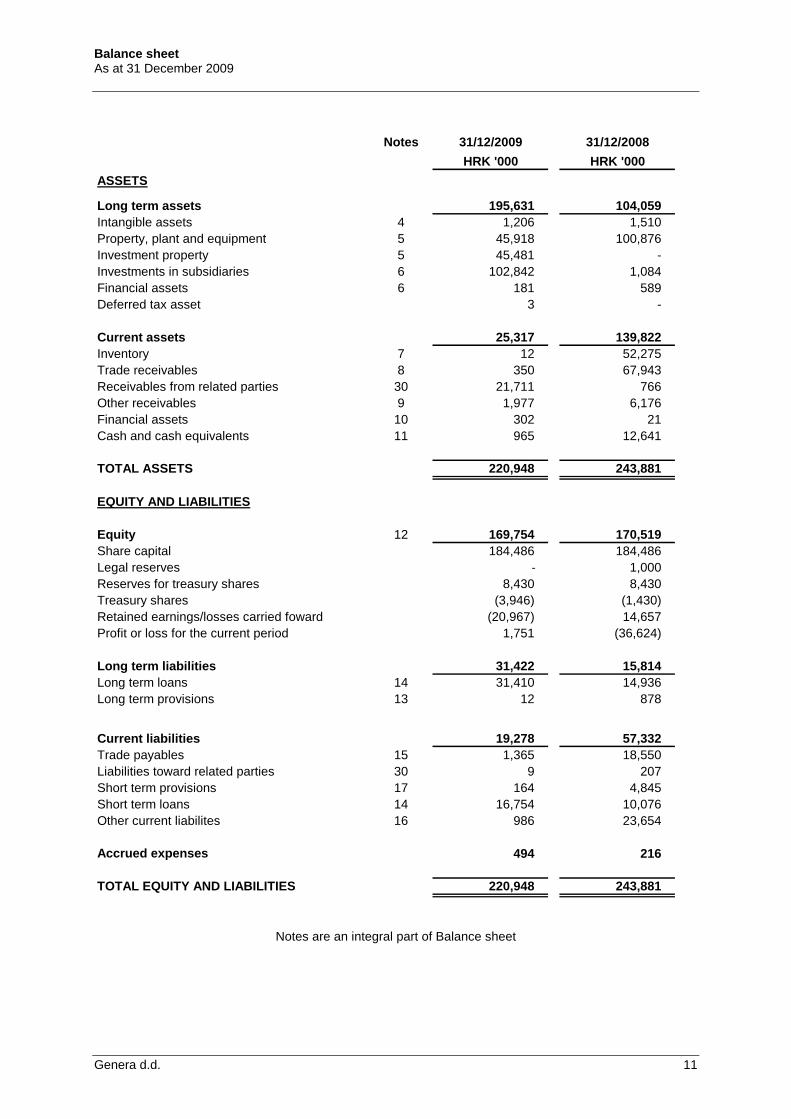

Balance sheet As at 31 December 2009

Genera d.d. 11

Notes 31/12/2009 31/12/2008

HRK '000 HRK '000

ASSETS

Long term assets 195,631 104,059Intangible assets 4 1,206 1,510Property, plant and equipment 5 45,918 100,876Investment property 5 45,481 -Investments in subsidiaries 6 102,842 1,084Financial assets 6 181 589Deferred tax asset 3 -

Current assets 25,317 139,822Inventory 7 12 52,275Trade receivables 8 350 67,943Receivables from related parties 30 21,711 766Other receivables 9 1,977 6,176Financial assets 10 302 21Cash and cash equivalents 11 965 12,641

TOTAL ASSETS 220,948 243,881

EQUITY AND LIABILITIES

Equity 12 169,754 170,519Share capital 184,486 184,486Legal reserves - 1,000Reserves for treasury shares 8,430 8,430Treasury shares (3,946) (1,430)Retained earnings/losses carried foward (20,967) 14,657Profit or loss for the current period 1,751 (36,624)

Long term liabilities 31,422 15,814Long term loans 14 31,410 14,936Long term provisions 13 12 878

Current liabilities 19,278 57,332Trade payables 15 1,365 18,550Liabilities toward related parties 30 9 207Short term provisions 17 164 4,845Short term loans 14 16,754 10,076Other current liabilites 16 986 23,654

Accrued expenses 494 216

TOTAL EQUITY AND LIABILITIES 220,948 243,881

Notes are an integral part of Balance sheet

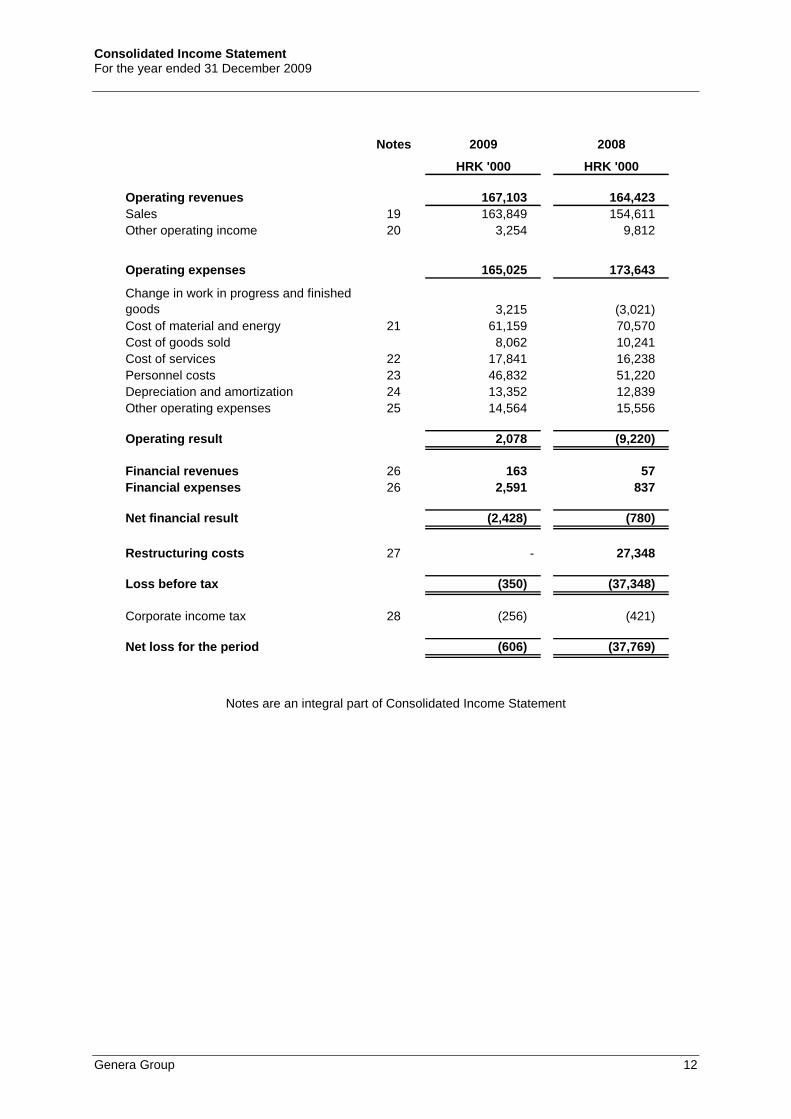

Consolidated Income Statement For the year ended 31 December 2009

Genera Group 12

Notes 2009 2008

HRK '000 HRK '000

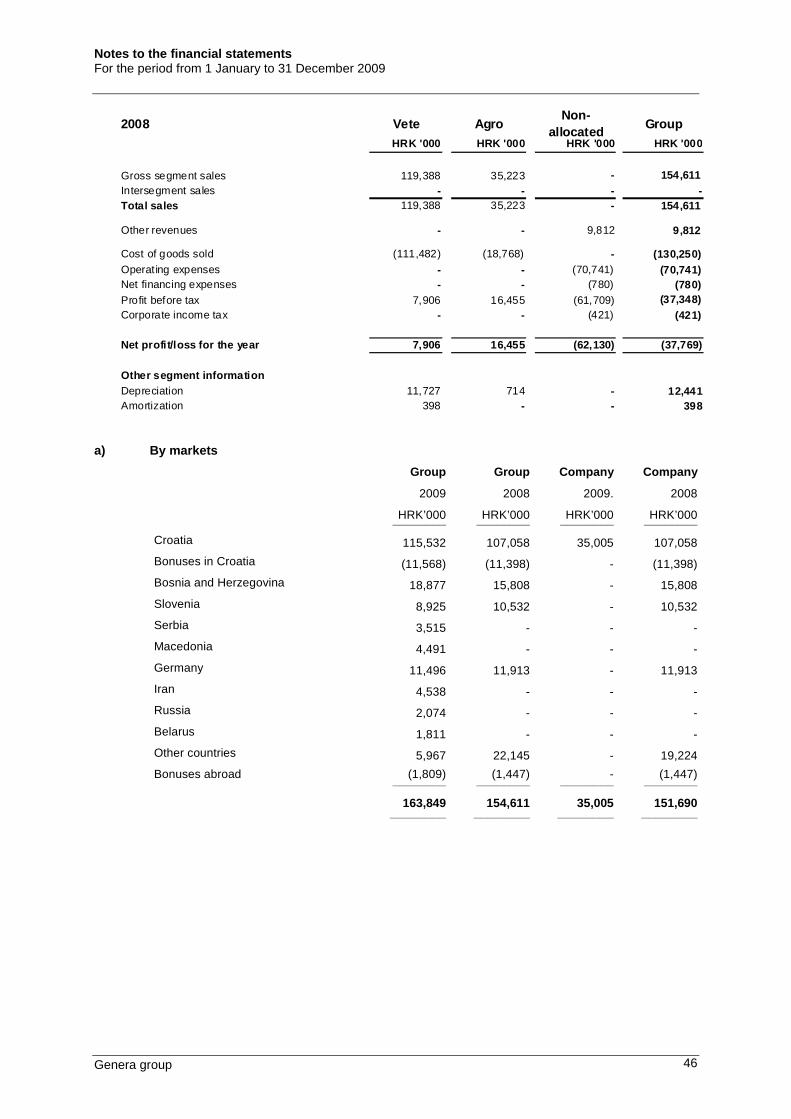

Operating revenues 167,103 164,423Sales 19 163,849 154,611Other operating income 20 3,254 9,812

Operating expenses 165,025 173,643

Change in work in progress and finished goods 3,215 (3,021)Cost of material and energy 21 61,159 70,570Cost of goods sold 8,062 10,241Cost of services 22 17,841 16,238Personnel costs 23 46,832 51,220Depreciation and amortization 24 13,352 12,839Other operating expenses 25 14,564 15,556

Operating result 2,078 (9,220)

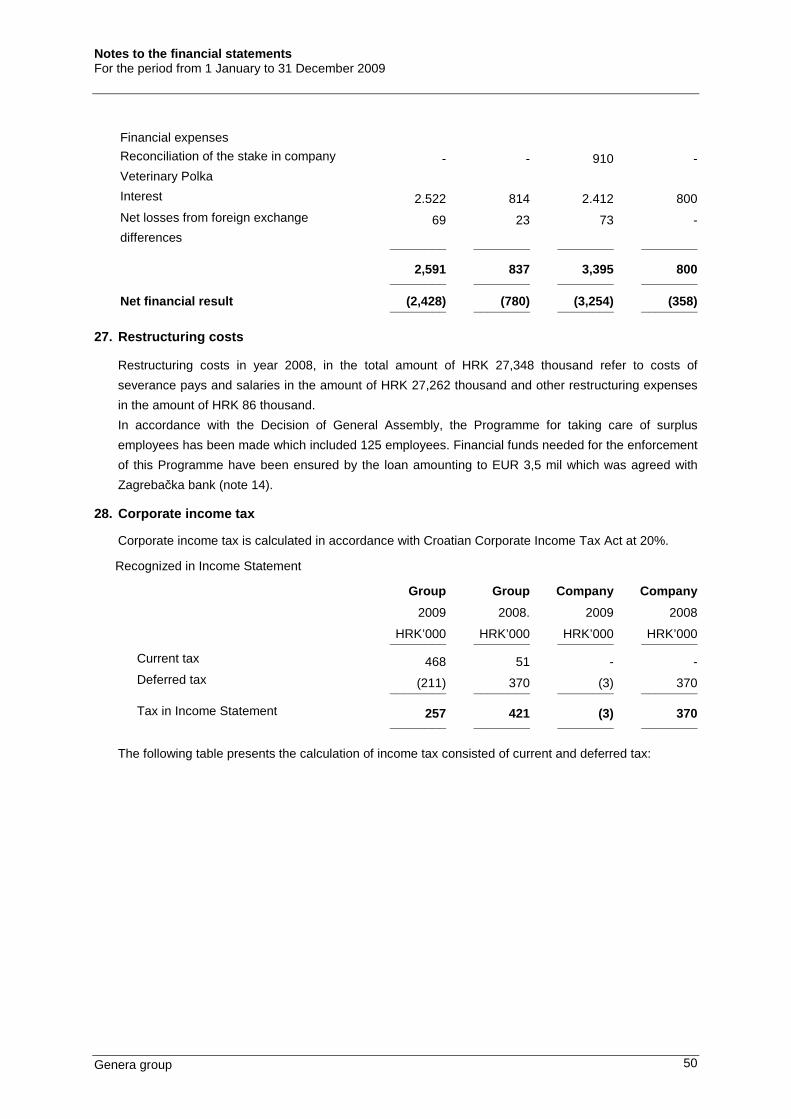

Financial revenues 26 163 57Financial expenses 26 2,591 837

Net financial result (2,428) (780)

Restructuring costs 27 - 27,348

Loss before tax (350) (37,348)

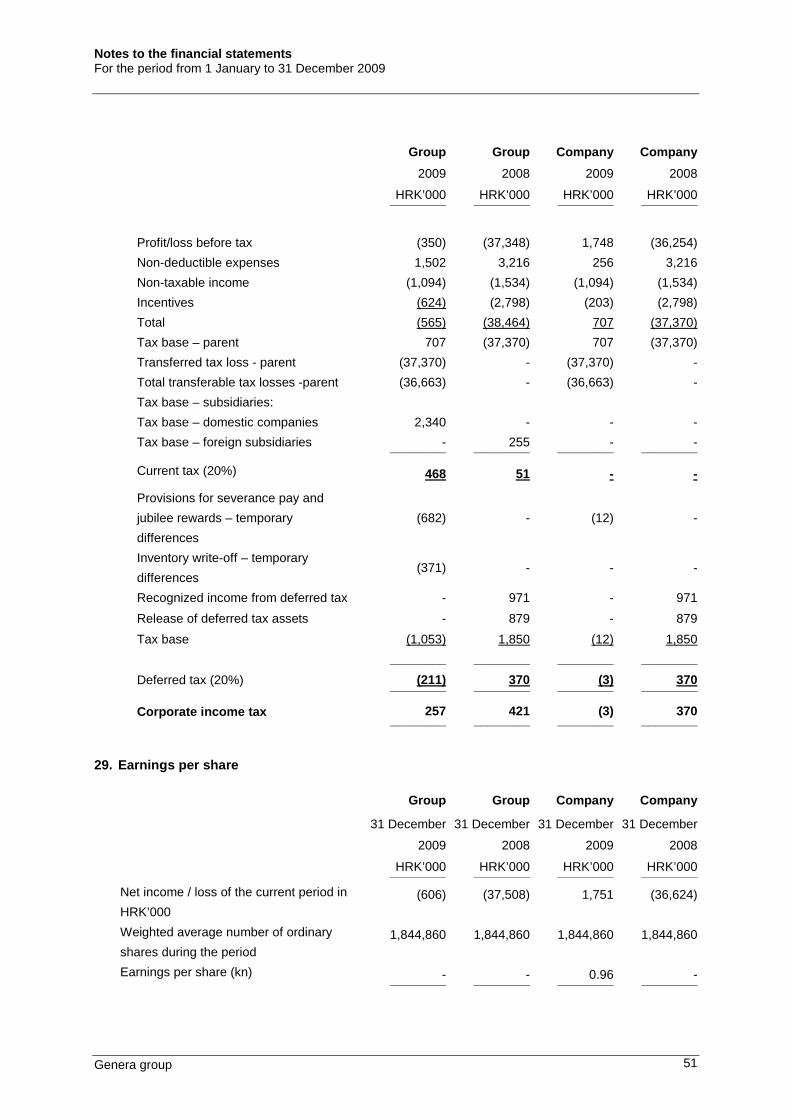

Corporate income tax 28 (256) (421)

Net loss for the period (606) (37,769)

Notes are an integral part of Consolidated Income Statement

Income Statement For the year ended 31 December 2009

Genera d.d. 13

Notes 2009 2008

HRK '000 HRK '000

Operating revenues 38,445 161,502Sales 19 35,005 151,690Other operating income 20 3,440 9,812

Operating expenses 33,443 170,050

Change in work in progress and finished goods

- (3,021)

Cost of material and energy 21 3,785 70,456Cost of goods sold 2,417 7,945Cost of services 22 2,441 17,842Personnel costs 23 8,395 49,371Depreciation and amortization 24 13,289 12,780Other operating expenses 25 3,116 14,677

Operating result 5,002 (8,548)

Financial revenues 26 141 442Financial expenses 26 3,395 800

Net financial result (3,254) (358)

Restructuring costs 27 - 27,348

Profit before tax 1,748 (36,254)

Corporate income tax 28 3 (370)

Net profit for the period 1,751 (36,624)

Notes are an integral part of Income Statement

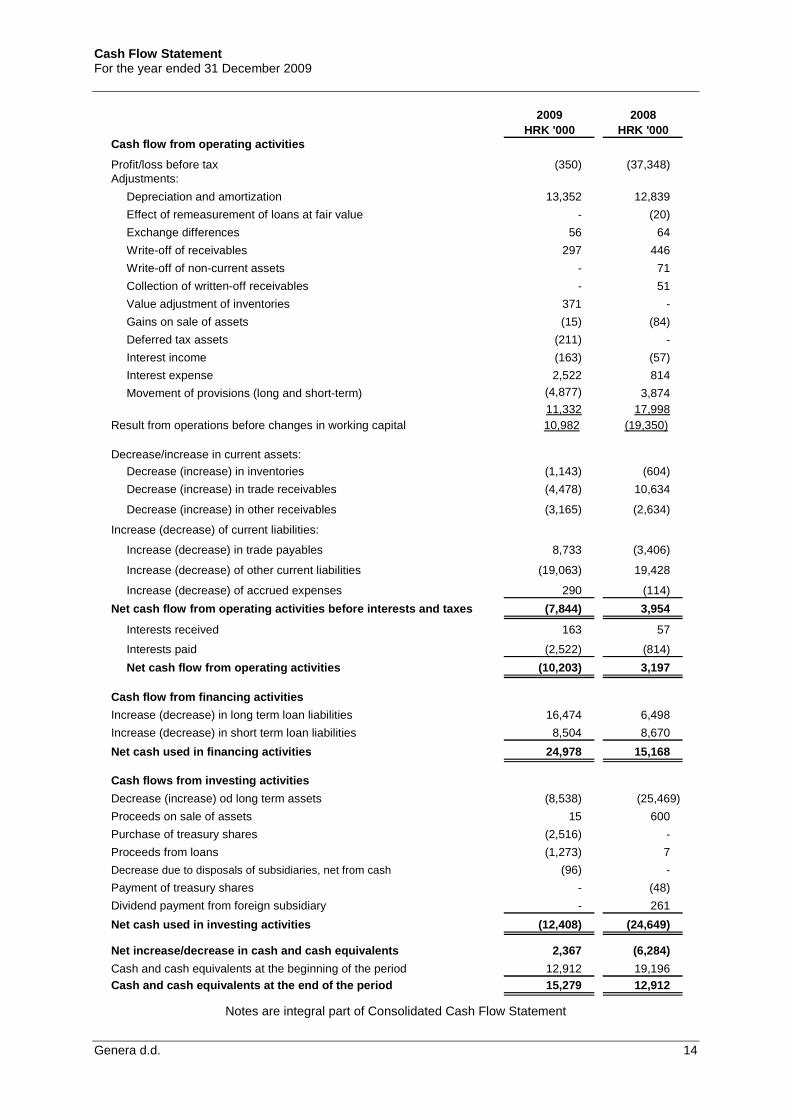

Cash Flow Statement For the year ended 31 December 2009

Genera d.d. 14

2009 2008HRK '000 HRK '000

Cash flow from operating activities

Profit/loss before tax (350) (37,348)Adjustments:

Depreciation and amortization 13,352 12,839

Effect of remeasurement of loans at fair value - (20)

Exchange differences 56 64

Write-off of receivables 297 446

Write-off of non-current assets - 71

Collection of written-off receivables - 51

Value adjustment of inventories 371 -

Gains on sale of assets (15) (84)

Deferred tax assets (211) -

Interest income (163) (57)

Interest expense 2,522 814

Movement of provisions (long and short-term) (4,877) 3,87411,332 17,998

Result from operations before changes in working capital 10,982 (19,350)

Decrease/increase in current assets:

Decrease (increase) in inventories (1,143) (604)

Decrease (increase) in trade receivables (4,478) 10,634

Decrease (increase) in other receivables (3,165) (2,634)

Increase (decrease) of current liabilities:

Increase (decrease) in trade payables 8,733 (3,406)

Increase (decrease) of other current liabilities (19,063) 19,428

Increase (decrease) of accrued expenses 290 (114)

Net cash flow from operating activities before inte rests and taxes (7,844) 3,954

Interests received 163 57

Interests paid (2,522) (814)

Net cash flow from operating activities (10,203) 3,197

Cash flow from financing activities

Increase (decrease) in long term loan liabilities 16,474 6,498

Increase (decrease) in short term loan liabilities 8,504 8,670

Net cash used in financing activities 24,978 15,168

Cash flows from investing activities

Decrease (increase) od long term assets (8,538) (25,469)

Proceeds on sale of assets 15 600

Purchase of treasury shares (2,516) -

Proceeds from loans (1,273) 7

Decrease due to disposals of subsidiaries, net from cash (96) -

Payment of treasury shares - (48)

Dividend payment from foreign subsidiary - 261

Net cash used in investing activities (12,408) (24,649)

Net increase/decrease in cash and cash equivalents 2 ,367 (6,284)

Cash and cash equivalents at the beginning of the period 12,912 19,196Cash and cash equivalents at the end of the period 1 5,279 12,912

Notes are integral part of Consolidated Cash Flow Statement

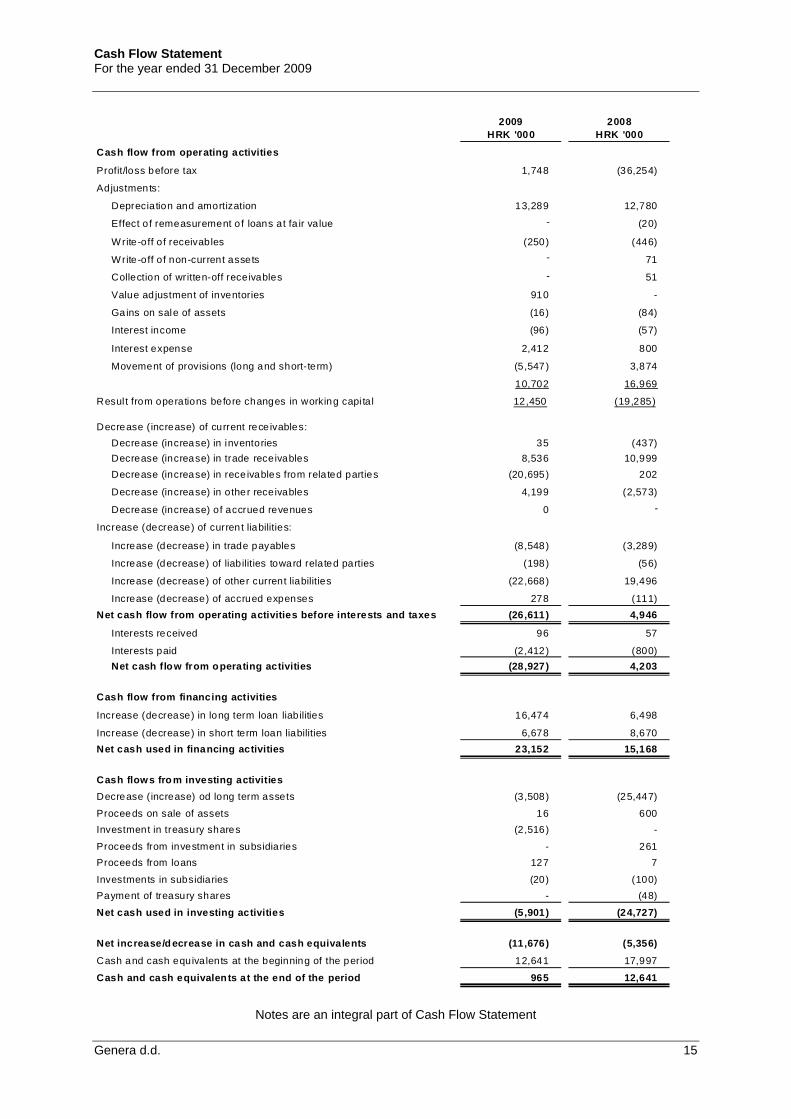

Cash Flow Statement For the year ended 31 December 2009

Genera d.d. 15

2009 2008HRK '000 HRK '000

Cash flow from operating activities

Profit/loss before tax 1,748 (36,254)

Adjustments:

Depreciation and amortization 13,289 12,780

Effect o f remeasurement o f loans at fa ir value - (20)

Write -off of receivables (250) (446)

Write -off of non-current assets - 71

Collection of written-off receivables - 51

Value ad justment of inventories 910 -

Gains on sale of assets (16) (84)

Interest income (96) (57)

Interest expense 2,412 800

Movement of provisions (long and short-term) (5,547) 3,874

10,702 16,969

Result from operations before changes in working capi ta l 12,450 (19,285)

Decrease (increase) of current rece ivables:

Decrease (increase) in inventories 35 (437)

Decrease (increase) in trade receivables 8,536 10,999

Decrease (increase) in rece ivables from rela ted parties (20,695) 202

Decrease (increase) in other receivables 4,199 (2,573)

Decrease (increase) of accrued revenues 0 -

Increase (decrease) of current liabilities:

Increase (decrease) in trade payables (8,548) (3,289)

Increase (decrease) of liabilities toward related parties (198) (56)

Increase (decrease) of other current liabilities (22,668) 19,496

Increase (decrease) of accrued expenses 278 (111)

Net cash flow from operating activities before inte rests and taxes (26,611) 4,946

Interests received 96 57

Interests paid (2,412) (800)

Net cash flow from operating activities (28,927) 4,203

Cash flow from financing activities

Increase (decrease) in long term loan liabilities 16,474 6,498

Increase (decrease) in short term loan liabilities 6,678 8,670

Net cash used in financing activities 23,152 15,168

Cash flows fro m investing activities

Decrease (increase) od long term assets (3,508) (25,447)

Proceeds on sale of assets 16 600

Investment in treasury shares (2,516) -

Proceeds from investment in subsidiaries - 261

Proceeds from loans 127 7

Investments in subsidiaries (20) (100)

Payment of treasury shares - (48)

Net cash used in investing activities (5,901) (24,727)

Net increase/d ecrease in cash and cash equivalents ( 11,676) (5,356)

Cash and cash equivalents at the beginning of the period 12,641 17,997

Cash and cash equivalen ts a t the end of the period 965 12,641

Notes are an integral part of Cash Flow Statement

Consolidated Statement of Changes in Equity For the year ended 31 December 2009

Genera d.d. 16

Share Reserves for Treasury Legal Retained Earnings/ Exc hange Profit/loss

capital treasury shares shares reserves Loss carried fo rward differences for the period

HRK'000 HRK'000 HRK'000 HRK'000 HRK'000 HRK'000 HRK'000 HR K'000

As at 1 January 2008 184,486 1,740 (1,740) - 18,064 64 3,793 206,407

Loss for the period - - - - - - (37,769) (37,769)

Exchange rate differences - - - - - (146) - (146)

Recognized revenues and expenses in 2008 - - - - - (146) (37,769) (37,915)

Creation of reserves for treasury shares - 7,000 - - (7,000) - - -

Creation of legal reserves - - - 1,000 (1,000) - - -

Purchase of treasury shares - (310) 310 - 248 - - 248

Allocation of 2007 result - - - - 3,793 - (3,793) -

Dividends declared - - - - 261 - - 261

As at 31 December 2008 184,486 8,430 (1,430) 1,000 14,366 (82) (37,769) 169,001

Loss for the period - - - - - - (606) (606)

Recognized revenues and expenses in 2009 - - - - - -

(606) (606)

Purchase of treasury shares - - (2,516) - - - - (2,516)

Allocation of 2008 result - - - (1,000) (36,769) - 37,769 -

Exclusion of Veterina Polska from the group - - - - 633 86 - 719

As at 31 December 2009 184,486 8,430 (3,946) - (21,770) 4 (606) 166,598

Total

Notes are an integral part of Consolidated Statement of Changes in Equity

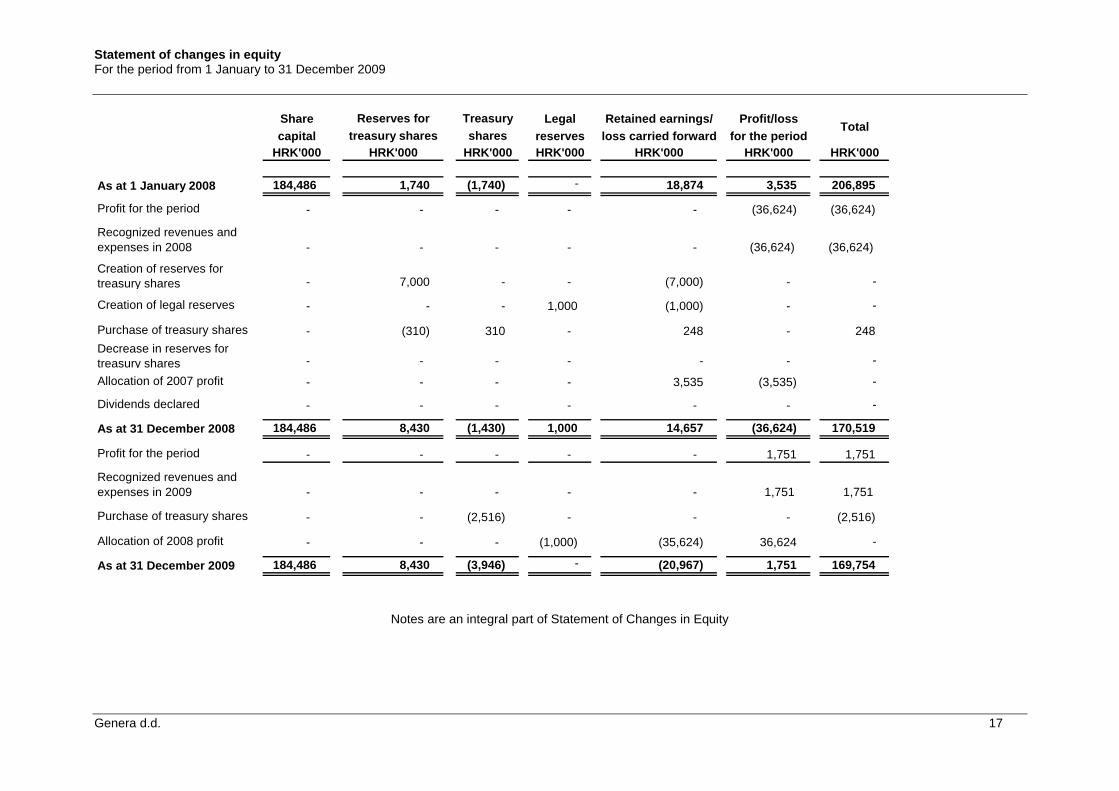

Statement of changes in equity For the period from 1 January to 31 December 2009

Genera d.d. 17

Share Reserves for Treasury Legal Retained earnings/ Profit/losscapital treasury shares shares reserves loss carried forward for the period

HRK'000 HRK'000 HRK'000 HRK'000 HRK'000 HRK'000 HRK'000

As at 1 January 2008 184,486 1,740 (1,740) - 18,874 3,535 206,895

Profit for the period - - - - - (36,624) (36,624)

Recognized revenues and expenses in 2008 - - - - - (36,624) (36,624)

Creation of reserves for treasury shares - 7,000 - - (7,000) - -

Creation of legal reserves - - - 1,000 (1,000) - -

Purchase of treasury shares - (310) 310 - 248 - 248

Decrease in reserves for treasury shares - - - - - - -

Allocation of 2007 profit - - - - 3,535 (3,535) -

Dividends declared - - - - - - -

As at 31 December 2008 184,486 8,430 (1,430) 1,000 14,657 (36,624) 170,519

Profit for the period - - - - - 1,751 1,751

Recognized revenues and expenses in 2009 - - - - - 1,751 1,751

Purchase of treasury shares - - (2,516) - - - (2,516)

Allocation of 2008 profit - - - (1,000) (35,624) 36,624 -

As at 31 December 2009 184,486 8,430 (3,946) - (20,967) 1,751 169,754

Total

Notes are an integral part of Statement of Changes in Equity

Notes to the financial statements For the period from 1 January to 31 December 2009

Genera d.d. 18

Notes to the financial statements

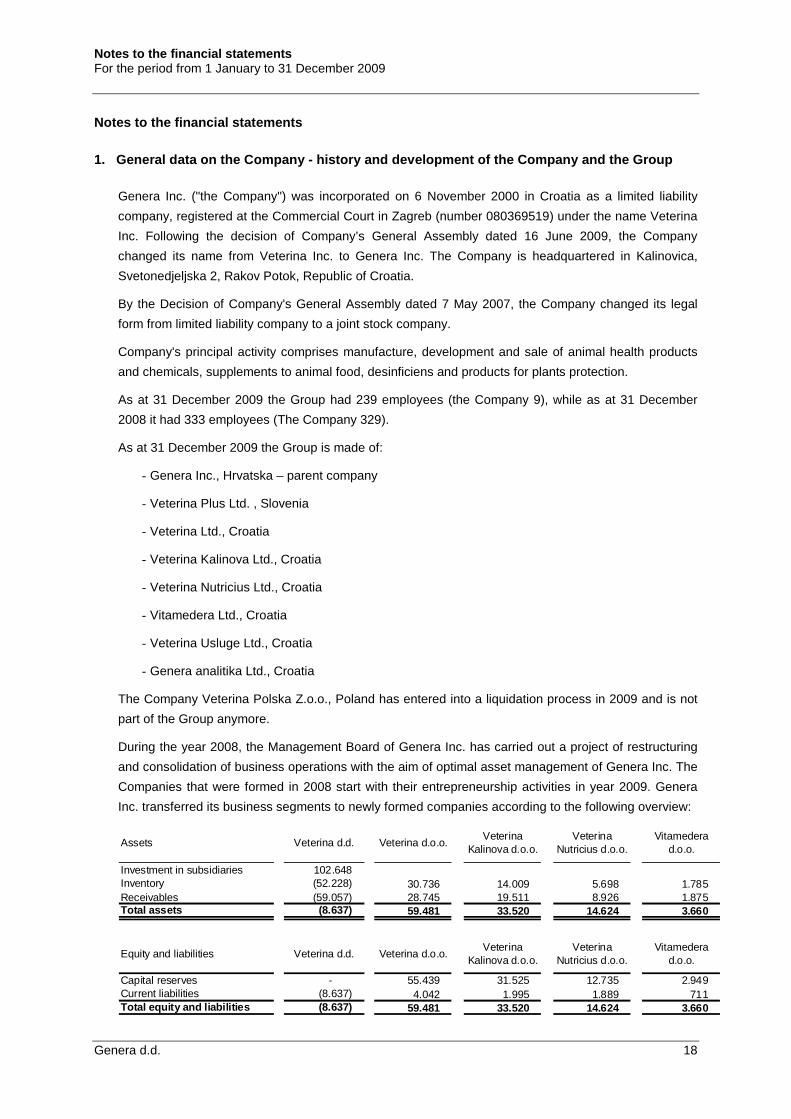

1. General data on the Company - history and deve lopment of the Company and the Group

Genera Inc. ("the Company") was incorporated on 6 November 2000 in Croatia as a limited liability

company, registered at the Commercial Court in Zagreb (number 080369519) under the name Veterina

Inc. Following the decision of Company’s General Assembly dated 16 June 2009, the Company

changed its name from Veterina Inc. to Genera Inc. The Company is headquartered in Kalinovica,

Svetonedjeljska 2, Rakov Potok, Republic of Croatia.

By the Decision of Company's General Assembly dated 7 May 2007, the Company changed its legal

form from limited liability company to a joint stock company.

Company's principal activity comprises manufacture, development and sale of animal health products

and chemicals, supplements to animal food, desinficiens and products for plants protection.

As at 31 December 2009 the Group had 239 employees (the Company 9), while as at 31 December

2008 it had 333 employees (The Company 329).

As at 31 December 2009 the Group is made of:

- Genera Inc., Hrvatska – parent company

- Veterina Plus Ltd. , Slovenia

- Veterina Ltd., Croatia

- Veterina Kalinova Ltd., Croatia

- Veterina Nutricius Ltd., Croatia

- Vitamedera Ltd., Croatia

- Veterina Usluge Ltd., Croatia

- Genera analitika Ltd., Croatia

The Company Veterina Polska Z.o.o., Poland has entered into a liquidation process in 2009 and is not

part of the Group anymore.

During the year 2008, the Management Board of Genera Inc. has carried out a project of restructuring

and consolidation of business operations with the aim of optimal asset management of Genera Inc. The

Companies that were formed in 2008 start with their entrepreneurship activities in year 2009. Genera

Inc. transferred its business segments to newly formed companies according to the following overview:

Assets Veterina d.d. Veterina d.o.o.Veterina

Kalinova d.o.o.Veterina

Nutricius d.o.o.Vitamedera

d.o.o.

Investment in subsidiaries 102.648Inventory (52.228) 30.736 14.009 5.698 1.785Receivables (59.057) 28.745 19.511 8.926 1.875Total assets (8.637) 59.481 33.520 14.624 3.660

Equity and liabilities Veterina d.d. Veterina d.o.o.Veterina

Kalinova d.o.o.Veterina

Nutricius d.o.o.Vitamedera

d.o.o.

Capital reserves - 55.439 31.525 12.735 2.949Current liabilities (8.637) 4.042 1.995 1.889 711Total equity and liabilities (8.637) 59.481 33.520 14.624 3.660

Notes to the financial statements For the period from 1 January to 31 December 2009

Genera d.d. 19

Veterina Ltd. has continued its business operations in the production of vaccines and chemo

pharmaceutical potions. Veterina Kalinova Ltd. in the production of pesticides and other agrochemicals,

Veterina Nutricius Ltd. in the production of supplements to provender, and Vitamedera Ltd. in the

production of desinficiens. Veterina Usluge Ltd. operates the business of providing support services (IT,

accounting, human resource, etc).

To accommodate the need for the treatment of redundant workers, the Company started using funds

from the agreed upon loan with Zagrebačka banka d.d. (note 14).

Supervisory and Management Board

Members of Supervisory Board are:

• Ivan Majdak, President

• Zrinka Vuković, Vice President

• Mladen Vedriš, Member

• Franjo Gregurić, Member

• Marcel Majsec, Member

Members of Management Board are:

• Ivan Drpić, President

• Ana Hanžeković Čorak, Member

During the year 2008 there were some changes in members of Supervisory and Management Board.

Members of Supervisory Board until 28 July 2008 were as follows:

• Anne Marie Goebel-Krstelj, President

• Dražana Kuliš,Vice President

• Domagoj Radin, Member

• Lovorka Penavić, Member

• Damir Kuštrak, Member

Members of Management Board until 28 July 2008 were as follows:

• Nenad Štiglić, President

• Biserka Furčić, Member

After that date members of Supervisory and Management Board became the above named current

members.

Financial statements are presented in thousands of Croatian kuna (HRK).

Notes to the financial statements For the period from 1 January to 31 December 2009

Genera group 20

2. Basis of preparation

a) Statement of Compliance

Financial statements of the Company have been made based on statutory requirements for financial

reporting applicable in the Republic of Croatia for large and listed companies, or companies which

are in process of listing into the organized stock market, and are based, until the Croatia's

acceptance as an European Union member, on International Financial Reporting Standards including

amendments and interpretations, as issued by Croatian Financial Reporting Standards Board

(hereinafter: the Board) and published in Official Gazette.

Accounting policies have not been changed during the reporting period compared to the previous

year. The Company has not applied any new or amended IFRSs and their interpretations that would

have effect on financial position or results, or would require additional disclosures in financial

statements.

b) Standards and Interpretations issued by IASB and adopted by the Croatian Board, but not

yet effective

At the date of authorisation of these financial statements the following standards and interpretations

adopted by Republic of Croatia on 12 November 2009 were in issue but not effective for reporting

periods ending on 31 December 2009:

o IFRS 1 First-time Adoption of IFRS (revised) – effective for annual periods beginning

on or after 1 January 2010,

o IFRS 2 Share based payment (revised) – effective for annual periods beginning on or after 1

January 2010,

o IFRS 7 Financial Instruments: Disclosures – effective for annual periods beginning on or after 1

January 2010,

o IAS 1 Presentation of Financial Statements (revised) – effective for annual periods beginning

on or after 1 January 2010,

o IAS 16 Property, Plant and Equipment (revised) – effective for annual periods beginning

on or after 1 January 2010,

o IAS 18 Revenue – effective for annual periods beginning on or after 1 January 2010,

o IAS 19 Employee Benefits (revised) – effective for annual periods beginning on or after 1

January 2010,

o IAS 20 Accounting for Government Grants and Disclosure of Government Assistance –

effective for annual periods beginning on or after 1 January 2010,

o IAS 23 Borrowing costs (revised) – effective for annual periods beginning on or after 1 January

2010,

o IAS 27 Consolidated and Separate Financial Statements – Cost of an investment at first

application – effective for annual periods beginning on or after 1 January 2010,

o IAS 28 Investments in Associates (revised) – effective for annual periods beginning on or after

1 January 2010,

Notes to the financial statements For the period from 1 January to 31 December 2009

Genera group 21

o IAS 29 Financial Reporting in Hyperinflationary Economies (revised) – effective for annual

periods beginning on or after 1 January 2010,

o IAS 31 Interests in Joint Ventures (revised) – effective for annual periods beginning on or after

1 January 2010,

o IAS 32 Financial Instruments: Presentation and IAS 1 Puttable Financial Instruments and

Obligations Arising on Liquidation (revised) – effective for annual periods beginning on or after

1 January 2010,

o IAS 36 Impairment of Assets (revised) – effective for annual periods beginning on or after 1

January 2010,

o IAS 38 Intangible Assets (revised) – effective for annual periods beginning on or after 1

January 2010,

o IAS 39 Financial Instruments: Recognition and Measurements (revised) – effective for annual

periods beginning on or after 1 January 2010,

o IAS 40 Investment Property (revised) – effective for annual periods beginning on or after 1

January 2010,

o IAS 41 Agriculture (revised) – effective for annual periods beginning on or after 1 January

2010,

o IFRIC 15 Agreements for the Construction of Real Estate – effective for annual periods

beginning on or after 1 January 2010,

o IFRIC 16 Hedges of a Net Investment in a Foreign Operation – effective for annual periods

beginning on or after 1 January 2010,

o IFRIC 17 Distributions of Non-cash Assets to Owners – effective for annual periods beginning

on or after 1 January 2010,

o IFRIC 18 Transfers of Assets from Customers – effective for annual periods beginning

on or after 1 January 2010,

o IFRS 3 Business Combinations (revised) – effective for annual periods beginning on or after 1

January 2010,

o IFRS 5 Non-current Assets Held for Sale and Discontinued Operations (revised) – effective for

annual periods beginning on or after 1 January 2010,

o IAS 27 Consolidated and Separate Financial Statements – effective for annual periods

beginning on or after 1 January 2010,

o IAS 28 Investments in Associates (revised based on IFRS improvements) – effective for

annual periods beginning on or after 1 January 2010,

o IAS 31 Interests in Joint Ventures (revised based on IFRS 3 amendment) – effective for annual

periods beginning on or after 1 January 2010,

o IAS 39 Financial Instruments: Recognition and Measurement: Eligible Hedged items – effective

for annual periods beginning on or after 1 January 2010,

o IFRS 9 Financial Instruments – effective for annual periods beginning on or after 1 January

2013,

o IFRIC 19 Extinguishing Financial Liabilities with Equity Instruments – effective for annual

periods beginning on or after 1 July 2010

Notes to the financial statements For the period from 1 January to 31 December 2009

Genera group 22

c) Basis of preparation of Financial Statements

Financial Statements of the Company and the Group have been prepared on the historical cost basis,

except for derivative financial instruments, financial assets at fair value through Profit and Loss,

financial instruments available for sale (except those which are not subject of active market trading and

which are recognised at cost less impairment losses), which are valuated at fair value.

Financial Statements of the Company and the Group are prepared on going concern basis.

d) Functional and reporting currency

Financial Statements of the Company and the Group are presented in Croatian kuna which is

Company's functional and reporting currency and rounded to the nearest thousand (HRK '000), unless

stated otherwise. As at 31 December 2009 currency for 1 USD and 1 EUR amounted to 5.09 HRK and

7.31 HRK respectively (31 December 2008: 5.16 HRK and 7.33 HRK respectively).

e) Estimates and assumptions

The preparation of financial statements in conformity with IFRS requires management to make

judgements, estimates and assumptions that affect the application of policies presented in Financial

Statements and Notes. Although these estimates are based on all available information about current

affairs, actual results may differ from these estimates.

Key assumptions concerning the future on which significant estimates are based, and other key

sources of estimation uncertainty, which involve a significant risk of causing a material adjustment to

the carrying value of assets and liabilities within the next financial year, are disclosed as follows:

Impairment of trade receivables

Receivables are assessed for impairment on the basis of collectability assessment of individual trade

receivables. Collectability assessments of trade receivables are made at least once a year.

f) Basis of preparation of Consolidated financial st atements

The consolidated financial statements include parent company and subsidiaries after elimination of all

material transactions between companies within the Group. Subsidiary is a legal entity under the control

of parent Company, in which parent company directly or indirectly owns more than 50 percent of the

voting rights or associate over which parent company has management control.

Subsidiaries are consolidated from the date of acquisition, being the date on which the Group obtains

control, and continue to be consolidated until the date that such control ceases (at the date of their sale

or liquidation).

Acquisitions of subsidiaries are recorded using the cost method.

The financial statements of subsidiaries are prepared for the same reporting period as the parent

company, using consistent accounting policies. Adjustments are made where they became the

difference in the change in accounting policy that possibly exists.

Notes to the financial statements For the period from 1 January to 31 December 2009

Genera group 23

Minority interests in equity and results of the companies that control the parent company are presented

separately in the consolidated financial statements.

Basis of consolidation:

a. Only companies in which the Company has control are consolidated on the basis of individual

position of balance sheet or income statement. Investments in associates are expressed using

the equity method.

b. Companies that are purchased during the year are included in the consolidated financial

statements from the date of acquisition or up to date of sales.

c. The difference between the acquisition cost and capital on the same date, the Company

distributed on the basis of assessment of the Board on the assets and liabilities included in the

investment and the remaining amount is considered as goodwill

d. All intra-group balances, income and expenses and unrealised gains and losses resulting from

intra-group transactions are eliminated in full.

General accounting policies used in the preparation of financial statements are explained below:

3. Summary of significant accounting policies

a) Intangible assets

Where patents, licences and similar rights are acquired by the Company or the Group from third parties

the costs of acquisition are capitalised to the extent that future economic benefits are probable and will

flow to the Group. Licences are amortised over their estimated useful lives, but not exceeding 10 years.

Estimated useful lives are reviewed annually and impairment reviews are undertaken if there are any

indications of impairment.

Changes in estimated useful lives or in estimated usage of future economic benefits is stated in the

period of change and treated as change in accounting estimate.

Subsequent expenditure is capitalised only if it is probable that it increases the future economic benefits

embodied in the specific asset to which it relates and if the benefits will flow into the Company or the

Group. All other expenditure is recognised in the income statement as an expense as incurred.

Research and development costs

Research costs are recognised in the income statement as incurred.

Internal development costs are capitalised as intangible assets only when development costs can be

reliably measured, the products or process are technically and commercially feasible, it is probable that

future economic benefits will flow to the Company or the Group, and the Company or the Group has

sufficient resources to complete the development and to use or sell the asset. The expenditure

capitalized includes the costs of materials, direct labour, and overhead costs that are directly

attributable to preparing the asset for its intended use. Other development expenditure is recognized in

the income statement when incurred.

In-process research and development assets acquired either through in-licensing arrangements,

business combinations or separate purchases are capitalised as intangible assets (in the amount of

Notes to the financial statements For the period from 1 January to 31 December 2009

Genera group 24

payments made by Group companies to third parties and associates). Such intangible assets are stated

at cost less accumulated amortisation and impairment losses. They are amortised on a straight-line

basis over the period of the expected benefit, and are reviewed for impairment at each balance sheet

date.

b) Property, plant and equipment

Items of property, plant and equipment are stated at cost less accumulated depreciation and

impairment losses. Cost includes all costs directly attributable to bringing the asset to a working

condition for its intended use.

Subsequent expenditure is capitalised only when it increases the future economic benefits embodied in

an item of property, plant and equipment and those benefits will flow to the Group and if the cost of the

item can be measured reliably. All other expenditure is recognised in the income statement as an

expense as incurred.

Depreciation is recognised in the income statement on a straight-line basis over the estimated useful

lives of each part of an item of property, plant and equipment. Assets in the course of construction are

not depreciated. The estimated useful lives are as follows:

2009 2008

Buildings 10-40 years 10-40 years

Plant and equipment 4-20 years 4-20 years

Depreciation is provided on a straight-line basis for each fixed asset item over their useful economic

life.

Net loss or gain from asset disposal is recognized under other operating income or expenses in the

Income Statement of the Company or the Group.

Impairment of tangible and intangible assets excluding goodwill

At each balance sheet date, the Company or the Group reviews the carrying amount of its tangible and

intangible assets to determine whether there is any indication that those assets have suffered an

impairment loss. If any such indication exists, the recoverable amount of the asset is estimated in order

to determine the extent of the impairment loss (if any). Where it is not possible to estimate the

recoverable amount of the individual asset, the Company or the Group estimated the recoverable

amount of the cash-generating unit to which the asset belongs. Where a reasonable and consistent

basis of allocation can be identified, corporate assets are also allocated to individual cash-generating

units, or otherwise they are allocated to the smallest Company’s cash-generating units for which a

reasonable and consistent allocation basis can be identified.

Intangible assets with indefinite useful lives and intangible assets not yet available for use are tested

for impairment annually, and when ever there is an indication that the asset may be impaired.

Recoverable amount is higher of fair value less costs to sell and value in use. In assessing value in

use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate

Notes to the financial statements For the period from 1 January to 31 December 2009

Genera group 25

that reflects current market assessments of the time value of money and the risks specific to the asset

for which the estimates of future cash flows have not been adjusted.

If the recoverable amount of an asset (or cash-generating unit) is estimated to be less than its carrying

amount, the carrying amount of the asset (or cash-generating unit) is reduced to its recoverable

amount. An impairment loss is recognized immediately in profit or loss, unless the relevant asset is

carried at a revaluated amount, in which case the impairment loss is treated as a revaluation decrease.

The Company and the Group determine the impairment of goodwill at least once a year. It requires a

value estimate in use of the unit that generates cash to which the goodwill is intended for. The

Company has estimated that the whole business is one unit that generates cash. The value estimate in

use requires the estimation of future cash flows of the unit that generates cash and the selection of an

appropriate discount rate for discounting future cash flows to their present value.

c) Investment property

Investment property is property held either to earn rental income or for capital appreciation or both.

Investment property is initially measured at cost. After initial recognition, investment property is

measured at cost less accumulated depreciation and accumulated impairment losses. Cost includes

purchase price and expenditure that is directly attributable to the acquisition of the asset. Investment

property in progress is classified as property, plant and equipment, except land which is immediately

recognised as investment property. Land is not amortised. After putting into use, investment property

will be depreciated over the useful economic life.

d) Investment in subsidiaries

Subsidiaries are entities in which the Company has the power, directly or indirectly, to exercise control

over their operations. Control is achieved where the Company has the power to govern the financial

and operating policies of an entity so as to obtain benefit from its activities. Financial statements of

subsidiaries are included in consolidated financial statements from the date that the control commences

until the date that control ceases. Investments in subsidiaries are stated at cost in standalone financial

statements of the Company.

Transactions eliminated during the consolidation

All intra-group transactions, balances and unrealised gains on transactions between Group entities are

eliminated in full on consolidation, unrealised losses are also eliminated but to the extent that there is

no evidence of impairment.

Unrealised gains arising from transactions with associates are eliminated to the extent of the Group's

interest in the associate. Unrealised losses are eliminated in the same way as unrealised gains, but

only to the extent that there is no evidence of impairment.

Notes to the financial statements For the period from 1 January to 31 December 2009

Genera group 26

e) Inventory

Inventories encompass raw materials and supplies, spare parts, finished goods and goods for sale.

Inventories are measured at the lower of cost or net realizable value. Costs of inventories comprise all

purchase costs, costs of conversion and other costs incurred in bringing the inventories to their present

location and condition.

Inventories are valued by the weighted average cost method while finished goods and semi-finished

products are valuated at standard cost. Small inventory is depreciated by 100% when put into use.

Value adjustment of inventories is made upon estimation of the value decrease of inventories on item-

by-item basis if those inventories are damaged, if they have become wholly or partially obsolete, or if

their selling prices have declined.

f) Receivables

Receivables represent the right to collect determined amounts from customers or other debtors with

regard to the company's operations. Receivables are reported in the total amount and decreased by the

provisions for doubtful and bad debts. Bad debt provisions are made when collection of a part or a total

of this receivable is uncertain based on the Management’s estimation.

g) Cash and cash equivalents

Cash and cash equivalents consist of deposits, cash at banks and similar institutions and cash on

hand. This item includes cash immediately available and utilizable and is characterized by its absence

of collection risk and collection accessory charges.

h) Revenue recognition

Sales, which are reported net of returns, discounts, bonuses and premiums, as well as net of taxes

directly connected with the sale of products and services rendered, represent amounts invoiced to third

parties. Revenue is recognized at the time when services are rendered, and the company dispatches

goods, as this is the point at which significant risks and rewards of ownership of the goods are

transferred to the customer.

Sale of goods

Revenue from the sale of goods is recognized when all the following conditions are satisfied:

� The company has transferred to the buyer the significant risks and rewards of ownership of the

goods;

� The company retains neither continuing managerial involvement to the degree usually

associated with ownership nor effective control over the goods sold;

� The amount of revenue can be measured reliably;

� It is probable that the economic benefits associated with the transaction will flow to the entity;

and

� The costs incurred in respect of the transaction can be measured reliably.

Interests

Interest income is recognized in the Income Statement in period in which incurred.

Notes to the financial statements For the period from 1 January to 31 December 2009

Genera group 27

Dividends

Dividend income is recognized in the Income Statement in the period in which Company’s right to

receive the dividends is established.

i) Borrowing costs

Borrowing costs are recognized as an expense in the period in which they are incurred regardless of

how the borrowings are applied.

j) Foreign currencies

Foreign currency transactions are translated into the functional currency using the exchange rates

prevailing at the dates of the transactions. Monetary assets and liabilities denominated in foreign

currency at the reporting date are translated into the functional currency at the foreign exchange rate

ruling at that date. Foreign exchange gains and losses resulting from the settlement of such

transactions and from the translation of monetary assets and liabilities denominated in foreign

currencies are recognised in the income statement.

Non-monetary assets and items that are not measured by historic cost in foreign currencies are not

converted under the new exchange rates. Non-monetary assets and liabilities denominated in foreign

currencies that are measured at fair value are converted into the functional currency at foreign

exchange rates ruling at the dates the values were determined.

Group entities

Items included in the financial statements of each of the Group’s entities are measured using the

currency of the primary economic environment in which the entity operates (“the functional currency”).

Income and expense items and cash flows of foreign operations that have a functional currency

different from the presentation currency are translated into the Group presentation currency at the

foreign exchange rates ruling at the dates of the transactions and their assets and liabilities are

translated at the exchange rates ruling at the reporting date. All resulting exchange differences are

recognised in a separate component of equity.

Net investment in Group entities

Exchange differences arising from the translation of the net investment in foreign operations are taken

to equity. When a foreign operation is sold, such exchange differences are released in the income

statement as part of the gain or loss on sale.

k) Financial liabilities

Financial liabilities are initially measured at fair value, net of transaction costs. They are subsequently

measured at amortised cost using the effective interest method. All differences between gains (net of

transaction costs) and residual value are recognised on the Income statement throughout the duration

of the liability using the effective interest rate method.

l) Provisions

Provisions are recognized when the Company or the Group has a present obligation (legal or

constructive) as a result of a past event, it is probable that the Company or the Group will be required

to settle the obligation, and a reliable estimate can be made of the amount of the obligation.

The amount recognized as a provision is the best estimated of the consideration required to settle the

present obligation at the balance sheet date, taking into account the risks and uncertainties

Notes to the financial statements For the period from 1 January to 31 December 2009

Genera group 28

surrounding the obligation. Where a provision is measured using the cash flows estimated to settle the

present obligation, its carrying amount is the present value of those cash flows.

When some or all of the economic benefits required to settle a provision are expected to be recovered

from a third party, the receivable is recognized as an asset if it is virtually certain that reimbursement

will be received and the amount of the receivable can be measured reliably

m) Employee benefits

a) Pension obligations and post-retirement benefits

Defined contribution plans

For defined contribution plans, the company pays contributions to publicly or privately administered

pension insurance funds on a mandatory, contractual or voluntary basis. Once the contributions

have been paid, the company has no further payment obligations. The regular contributions

constitute net periodic costs for the year in which they are due and as such are included in staff

costs.

b) Retirement benefits and jubilee rewards

For defined benefit retirement benefit plans, the cost of providing benefits is determined using the

Projected Unit Credit Method, with actuarial valuations being carried out at each balance sheet

date. Actuarial gains and losses are recognised in full in the period in which they occur and they

are recognised in income statement.

Past service cost is recognised immediately to the extent that the benefits are already vested, and

otherwise is amortised on a straight-line basis over the average period until the benefits become

vested.

The retirement benefit obligation recognised in the balance sheet represents the present value of

the defined benefit obligation as adjusted for unrecognised past service cost, and as reduced by

the fair value of scheme assets. Any asset resulting from this calculation is limited to past service

cost, plus the present value of available refunds and reductions in future contributions to the plan.

c) Bonus plans

A liability for employee benefits is recognised in provisions based on the Company’s formal plan

and when past practice has created a valid expectation by the Management Board/key employees

that they will receive a bonus and the amount can be determined before the time of issuing the

financial statements.

Liabilities for bonus plans are expected to be settled within 12 months of the balance sheet date

and are measured at the amounts expected to be paid when they are settled

n) Financial revenues and expenses

Financial revenues and expenses comprise of interests on loans granted calculated by using the

effective interest rate method, receivables for interests on investments, revenues from dividends, gains

and losses from exchange rate differences, gains and losses from Financial assets at fair value though

the Profit and Loss account.

Interest revenues are recognized in the income statement on an accrual basis using the effective

interest rate method. Dividends are recognized in the income statement at the date when the

shareholder’s right to receive payment is established.

Notes to the financial statements For the period from 1 January to 31 December 2009

Genera group 29

Financial cost is the sum of the cost of calculated interest on loans, change in fair value of the financial

assets recognised at fair value through profit and loss, loss from impairment of financial assets and loss

from the exchange rate differences. Borrowing costs are recognized in the income statement using the

effective interest rate method.

o) Dividends

Dividends are recognized in the Statement of changes in equity and disclosed as liability in the period in

which were approved by Group’s shareholders.

p) Taxes

The Company provides for taxation liabilities in accordance with Croatian law. Corporate tax for the

year comprises current and deferred tax.

Current tax is the expected tax payable on the taxable income for the year, using tax rates enacted at

the balance sheet date.

Deferred tax reflects the net tax effect of the temporary differentials between the book values of the

assets and the liabilities for the purpose of the financial reporting and the values used for the purpose

of establishing profit tax. A deferred tax asset for the carry-forward of unused tax losses and unused

tax credits is recognized to the extent that it is probable that future taxable profit will be available

against which the unused tax losses and unused tax credits can be utilised. Deferred tax assets and

liabilities are calculated using the tax rate applicable to the taxable profit in the years in which these

assets and liabilities are expected to be collected or paid.

Current and deferred tax are recognized as an expense or income in profit or loss, except when they

relate to items credited or debited directly to equity, in which case the tax is also recognized directly in

equity.

q) Earnings per share

The Company and the Group disclose data on basic earnings per share. The basic earnings per share

are calculated by dividing net profit or loss for the year attributable to ordinary equity holders by the

weighted average number of ordinary shares outstanding during the year.

r) Leases

Leases are classified as finance leases whenever the terms of the lease transfer substantially all the

risks and rewards of ownership to the lessee. All other leases are classified as operating leases.

Assets held under finance leases are initially recognised as assets of the Company at their fair value at

the inception of the lease or, if lower, at the present value of the minimum lease payments. The

corresponding liability to the lessor is included in the balance sheet as a finance lease obligation.

Lease payments are apportioned between finance charges and reduction of the lease obligations so

as to achieve a constant rate of interest on the remaining balance of the liability. Finance charges are

charged directly to profit or loss.

Operating lease payments are recognized as an expense on a straight-line basis over the lease term.

Notes to the financial statements For the period from 1 January to 31 December 2009

Genera group 30

s) Financial assets and financial liabilities

Financial assets

Investments are recognized and derecognized on trade date where the purchase or sale of an

investment is under a contract whose terms require delivery of the investment within the timeframe

established by the market concerned, and are initially measured at fair value, plus transaction costs,

except for those financial assets classified as at fair value through profit or loss, which are initially

measured at fair value.

Financial assets are classified into the following specified categories:

• “At fair value through profit or loss” (FVTPL)

Financial assets are classified as at FVTPL where the financial asset is either held for trading or it is

designated as at FVTPL. A financial asset is classified as held for trading if:

1. it has been acquired principally for the purpose of selling in the near future; or

2. it is a part of identified portfolio of financial instruments that the Company manages

together and has a recent actual pattern of short-term profit-taking; or

3. it is a derivative that is not designated and effective as a hedging instrument.

Financial assets at FVTPL are stated at fair value, with any resultant gain or loss recognized in profit or

loss. The net gain or loss recognized in profit or loss incorporates any dividend or interest method less

any impairment, with revenue recognized on an effective yield basis.

• “Held-to-maturity”

Bills of exchange and debentures with fixed or determinable payments and fixed maturity dates that the

Company has the positive intent and ability to hold to maturity are classified as held-to-maturity

investments. Held-to-maturity investments are recorded at amortized cost using the effective interest

method less any impairment, with revenue recognized on an effective yield basis.

• “Loans and receivables”

Trade receivables, loans, and other receivables that have fixed or determinable payments that are not

quoted in an active market are classified as loans and receivables. Loans and receivables are

measured at amortised cost using the effective interest method, less any impairment. Interest income is

recognized by applying the effective interest rate, except for short-term receivables when the

recognition of interest would be immaterial.

Impairment of financial assets

Financial assets, other than those at FVTPL, are assessed for indicators of impairment at each balance

sheet date. Financial assets are impaired where there is objective evidence that, as a result of one or

more events that occurred after the initial recognition of the financial asset, the estimated future cash

flows or the investment have been impacted.

For all other financial assets, including redeemable notes classifies as AFS and finance lease

receivables, objective evidence of impairment could include:

Notes to the financial statements For the period from 1 January to 31 December 2009

Genera group 31

• Significant financial difficulty of the issuer or counterparty; or

• Default or delinquency in interest or principal payments; or

• It becoming probable that the borrower will enter bankruptcy or financial re-organisation.

For certain categories of financial asset, such as trade receivables, assets that are assessed not to be

impaired individually are subsequently assessed for impairment on a collective basis. Objective

evidence of impairment for a portfolio of receivables could include the Company’s past experience of

collecting payments, an increase in number of delayed payments in the portfolio past the average credit

period of 60 days, as well as observable changes in national or local economic conditions that correlate

with default on receivables.

For financial assets carried at amortised cost, the amount of the impairment is the difference between

the asset’s carrying amount and the present value of estimated future cash flow, discounted at the

financial asset’s original effective interest rate.

The carrying amount of the financial assets is reduced by the impairment loss directly for all financial

assets with the exception of trade receivables, where the carrying amount is reduced through the use of

an allowance account. When a trade receivable is considered uncollectible, it is written off against the

allowance account. Subsequent recoveries of amounts previously written off are credited against the

allowance account. Changes in the carrying amount of the allowance account are recognised in profit or

loss.

With the exception of AFS equity instruments, if in a subsequent period, the amount of the impairment

loss decreases and the decrease can be related objectively to an event occurring after the impairment